Downloads

Download the report as a PDF

PDF | 1.65 MB

Download the summary as a PDF

PDF | 616.43 KB

This final report of the Pensions Review, a major project launched in April 2023 by the Institute for Fiscal Studies, in partnership with abrdn Financial Fairness Trust, examines the main risks to today’s working-age individuals in the UK pension system and sets out policy proposals primarily focused on improving outcomes for future generations of retirees. This report does further analysis and draws on the large number of reports we have published as part of this review.

Challenges within the current system

The current UK pension system, with automatic enrolment of most employees into private pensions alongside a flat-rate state pension payable from a single state pension age, offers significant advantages. This simple design encourages private pension saving while also providing flexibility for those who wish to either opt out of saving or alternatively contribute more. It does not need a complete overhaul. But despite its strengths, the system faces significant challenges.

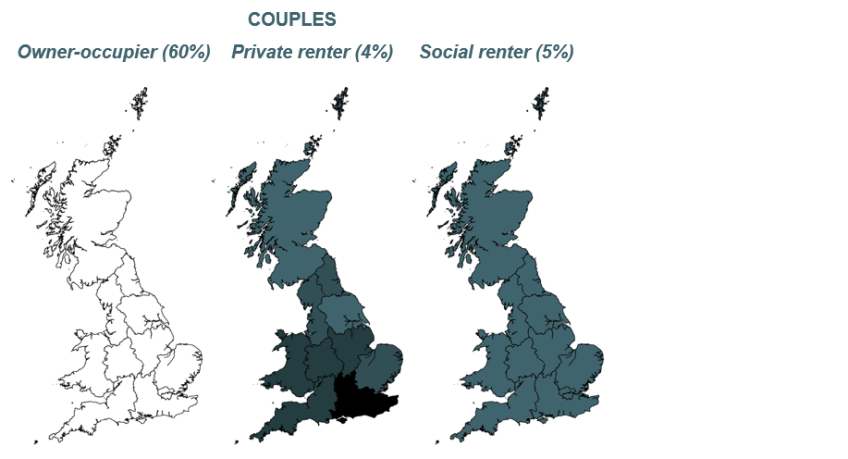

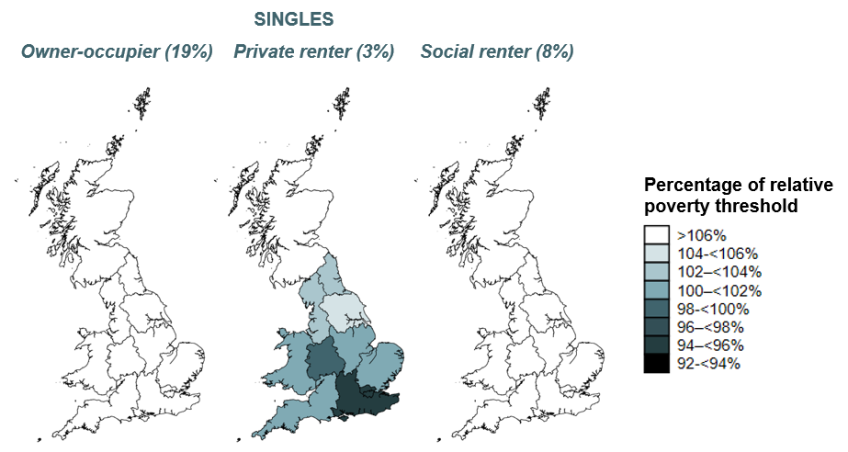

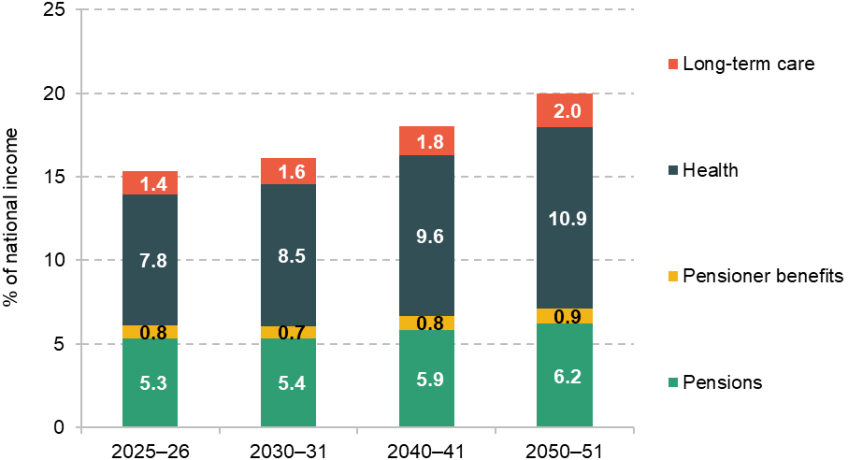

An ageing population places pressures on the public finances through increased spending on state pensions and in particular on health and social care. A generously indexed state pension adds to these growing pressures. The ‘triple lock’ increases the value of the state pension in an unpredictable way and it could reasonably be expected to push up state pension spending by anywhere between £5 billion and £40 billion a year in 2050 in today’s terms. Rising state pension ages have substantially pushed up the risk of income poverty among those in their mid 60s. Those reaching retirement in the private rented sector, increasing in number, are also at a heightened risk of poverty throughout their retirement.

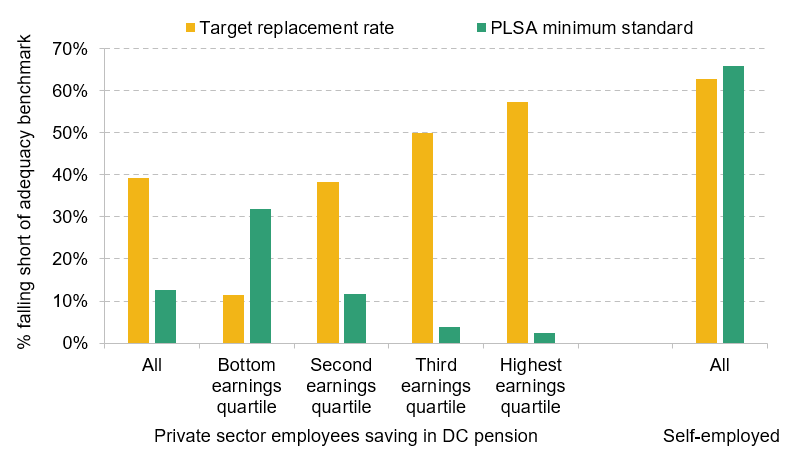

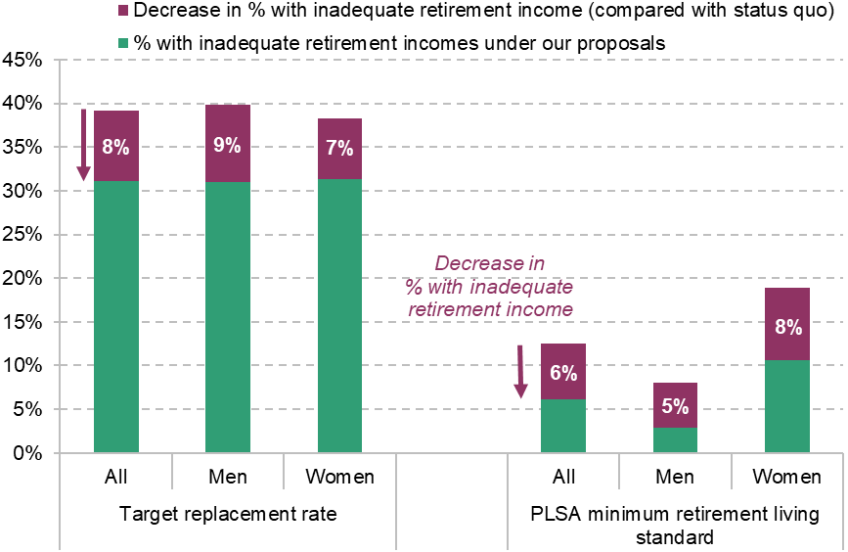

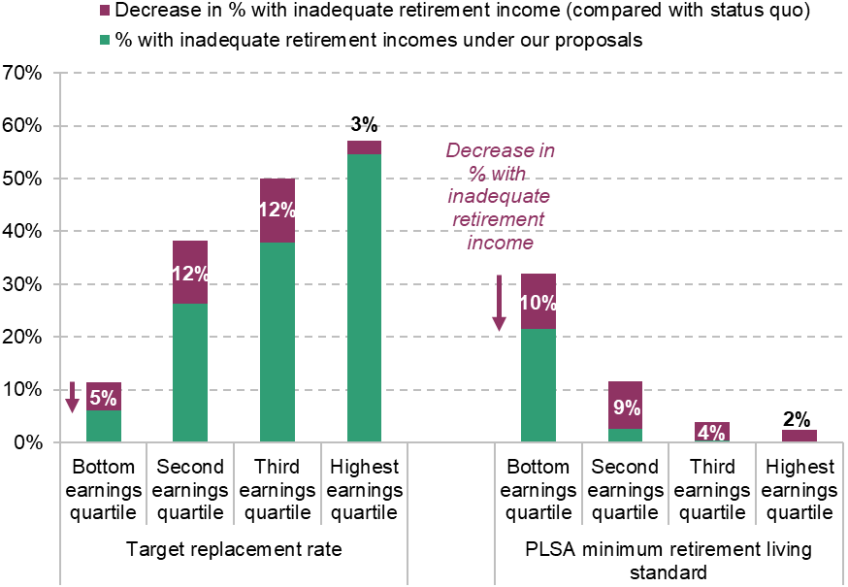

Additionally, many employees – and an even higher fraction of the self-employed – are not saving enough privately for their retirement. As shown in Figure ES.1, 39% of private sector employees are not on track to reach their ‘target replacement rate’ – a benchmark for avoiding large falls in standards of living at retirement as defined by the 2002–06 Pensions Commission. The graph also shows that 13% are not on track for the Pensions and Lifetime Savings Association (PLSA) minimum standard (a post-tax income of £13,400 per year for a single pensioner or £21,600 for a pensioner couple, after housing costs and living outside London). Low earners are considerably more likely not to meet the PLSA minimum standards (32% are projected not to meet this level on the basis of their individual incomes). Middle and higher earners are particularly likely to face a significant drop in living standards at retirement (e.g. 50% of those in the third quartile of the earnings distribution would miss their target replacement rate). With low rates of pension participation among the self-employed, 63% of self-employed workers are projected to fall short of their target replacement rate and 66% are projected to miss the PLSA minimum standard. More saving is needed.

Figure ES.1. Retirement income adequacy: percentage of private sector employees saving into a defined contribution pension, and self-employed, projected to fall short of selected benchmarks

Source: The sample contains 25- to 59-year-olds in Round 7 of the Wealth and Assets Survey. We simulate their projected future retirement income under their current saving rate, modelling everyone at the individual level and without accounting for future housing costs or receipt of inheritances.

At the same time, while there is a clear case for many working-age people to save more for retirement, it is important to recognise that increasing saving – and therefore reducing spending – of working-age households who are currently on a low income and struggling would create greater hardship today. Evidence suggests that this trade-off remains the case if the saving is undertaken by employers on behalf of their employees, as wages would likely fall (or grow less quickly) – at least somewhat – in response to higher mandated employer contributions.

There are also clear challenges in the current pension system for when and how pension wealth is accessed. The introduction of ‘pension freedoms’, which means that since 2015 no one is obliged to purchase an annuity with their pension pots, has had advantages for many. But it also exposes some people to risks they would not have faced had they either had a defined benefit pension or purchased an annuity, and then spent their income each year. Many are insufficiently supported on how best to manage longevity, investment and inflation risk when drawing down on their pension wealth through retirement, especially at older ages. This is an even bigger challenge when each change of employer creates a new pension pot for employees, which fragments retirement savings, making them easier to lose track of and unduly hard to manage well.

Combined, these factors are a recipe for too many to have poor financial security through retirement. In this report, we therefore make a set of proposals designed to address these key issues facing the pension system.

Reforms for an improved pension policy framework

Our proposals aim to ensure that the state pension system provides a reliable foundation for private saving. We focus on reforms to improve outcomes for those most at risk of poor retirement outcomes under the current system. We recognise that not everyone can afford to save more every year, so our recommendations help protect take-home pay for lower-income groups. More needs to be done to simplify decision-making for individuals, to help strike a fairer balance of responsibility among the state, individuals and employers when it comes to pension saving.

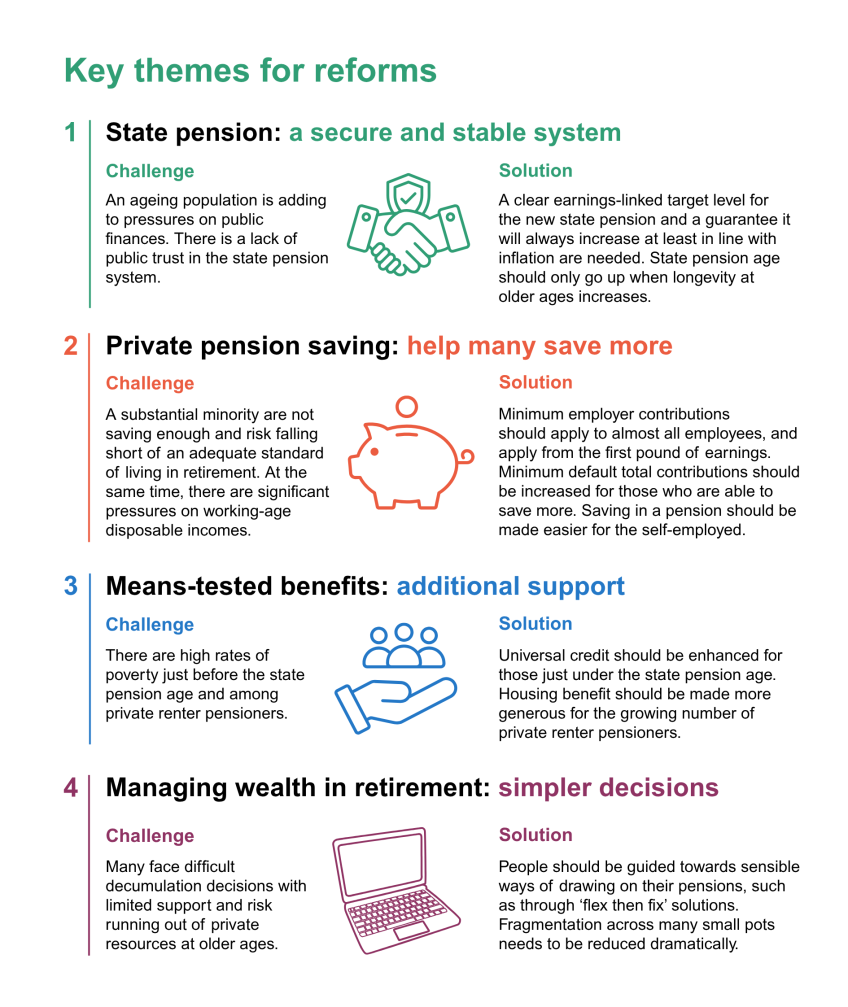

To achieve these outcomes, we propose a series of reforms, set out in more detail in Chapter 2. The key themes of these reforms are:

- State pension. We propose a ‘four-point guarantee’ for the state pension to increase confidence in the state pension as a stable and secure basis of the pension system. This guarantee means that: (1) a clear earnings-linked target for the new state pension should be set to improve predictability and to make sure that pensioner incomes keep up with increases in living standards; (2) the state pension will always increase in line with at least inflation; (3) the state pension will never be means-tested; and (4) the state pension age should continue to increase as longevity at older ages rises, but not by as much as that increase in longevity.

- Private pension saving. Many need more income in retirement. Too many employees miss out on employer pension contributions, so minimum employer contributions should be extended to almost all employees and apply from the first pound of their earnings. The automatic enrolment system should help people save at points of life when it is easier for them to do so. By increasing defaults for total pension contributions when individuals are on (and above) average earnings, the government can protect take-home pay when individuals are on low earnings, but still deliver a boost to many people’s retirement incomes. The government should make it easier for self-employed people to participate in a private pension, utilising HMRC’s Self Assessment system and drawing on the lessons of what has made automatic enrolment such a success in boosting workplace pension participation among private sector employees.

- Means-tested support. As the state pension age continues to rise, universal credit should be enhanced for those in the run-up to that age. This can be done for a small fraction of the fiscal savings from increasing the state pension age, and would help to alleviate the increase in poverty that would otherwise occur. Means-tested support for pensioners should be streamlined to boost take-up, and housing benefit should be made more generous for the growing number of pensioners residing in the private rental sector.

- Managing retirement incomes. Pensions need to be easier to manage, particularly through retirement. Fragmentation across many small pots needs to be reduced dramatically, with the level for automatic consolidation of pensions rising once it has been successfully implemented for the very smallest pots. People should be guided towards sensible ways of drawing on their pensions that reduce the risk of them running out of private resources, such as hybrid ‘flex then fix’ solutions (combining the flexibility of drawdown earlier in retirement and the purchase of an annuity later in retirement). However, even very well-designed default solutions will not be right for all, and people should be able to get high-quality information to make sensible decisions without having to take expensive financial advice.

Benefits of our policy reforms

Our proposals for the state pension would improve the predictability of the future level of the state pension and guarantee that state pension income is never means-tested, building confidence in the state pension system and allowing it to provide a stable foundation upon which to build private retirement savings.

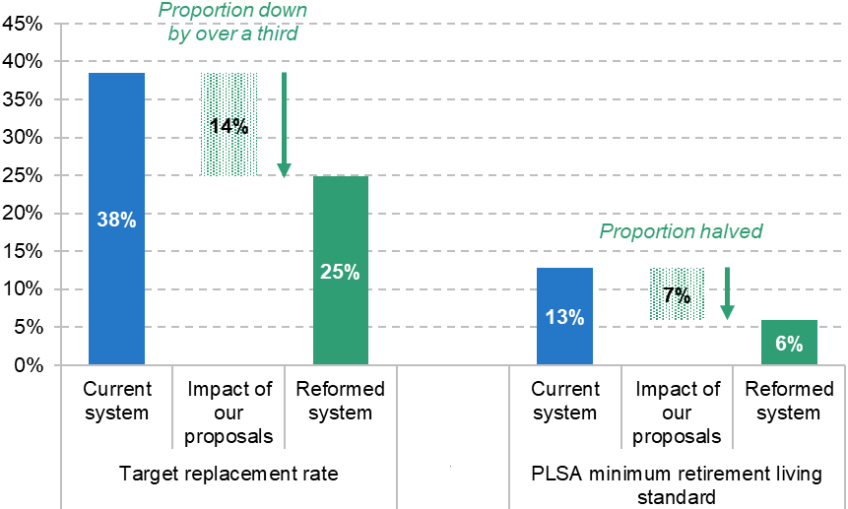

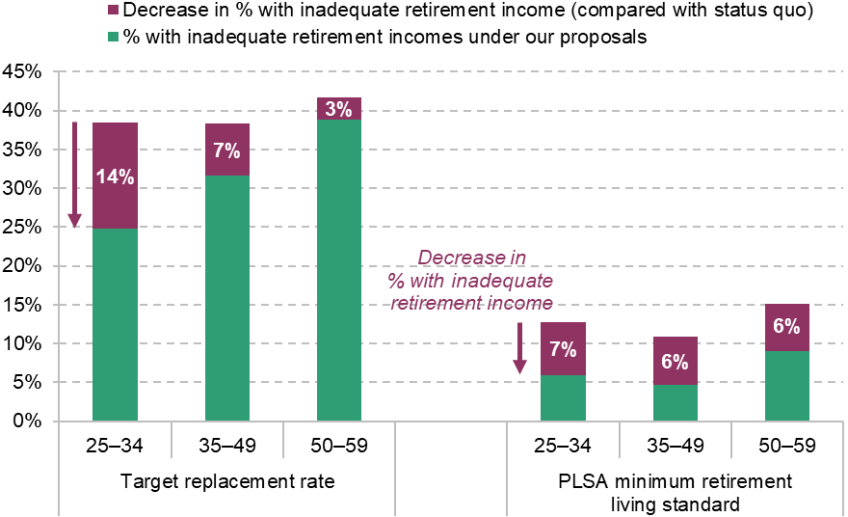

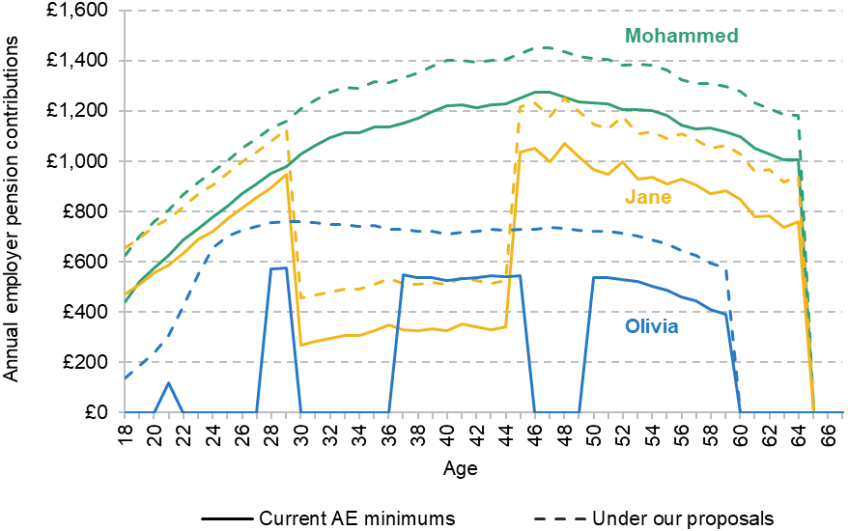

Our proposed reforms to private pensions would result in more private saving – our modelling suggests around £11 billion a year – on top of the foundation provided by the state pension. Our suggested enhancements to automatic enrolment would reduce the share of people with an ‘inadequate’ income in retirement, and the largest percentage increase in retirement incomes would come for those currently most at risk of low retirement incomes. Importantly, the effects would be substantial for younger adults, who would see the benefits of our proposals over the whole course of their working lives (see Figure ES.2). The share of 25- to 34-year-old employees saving in defined contribution pensions who are projected to miss their target replacement rates would fall by 14 percentage points, from 38% to 25%, while the share predicted to fall short of the PLSA minimum retirement living standard would more than halve under our proposals, from 13% to 6%.

Figure ES.2. Share of 25- to 34-year-old employees saving in defined contribution pensions projected to be on course for an inadequate retirement income, under current system and under our proposed reforms to automatic enrolment

Note: The sample contains 25- to 34-year-old private sector employees saving into a defined contribution pension in Round 7 of the Wealth and Assets Survey. We simulate their projected future retirement income under their current saving rate, and under our automatic enrolment proposals, modelling everyone at the individual level and without accounting for future housing costs or receipt of inheritances.

The effects on pension adequacy for older working-age adults are smaller, as they have fewer years before retirement to save more. This highlights the cost of delay. Acting swiftly ensures more generations have time to benefit for longer from increases in private pension saving. By implementing these policies sooner rather than later, the pension system can better help more of today’s working-age population build a more financially resilient retirement.

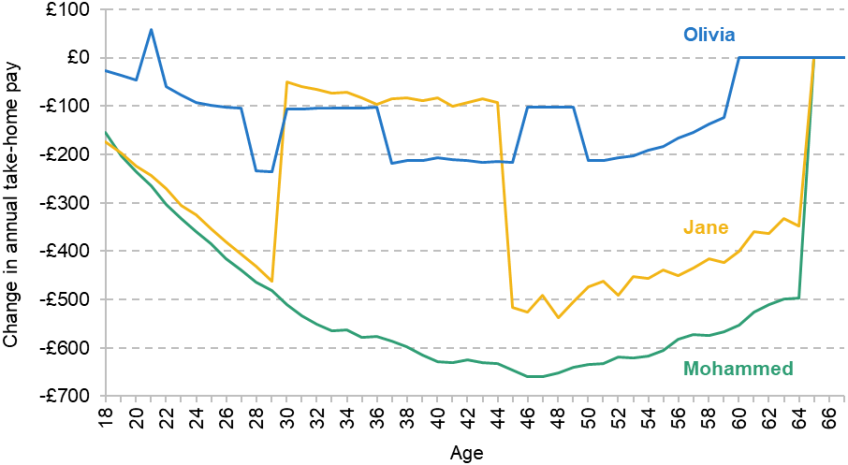

In addition to reducing the fraction of workers facing inadequate retirement incomes, what really sets our proposals apart is that, by carefully targeting increased saving, we would achieve this while mitigating falls in working-life take-home pay for those struggling on lower earnings. And, by both increasing the level and extending the reach of minimum employer contributions, we would ensure this extra saving is the shared responsibility of both employees and their employers. Our automatic enrolment proposals would boost private pension saving by around £11 billion a year, with roughly half of this coming from increased employer contributions and half from increased employee contributions. This increase in contributions would attract around £3 billion a year of additional up-front tax relief. Our proposals to facilitate pension saving for the self-employed would also benefit this group which has particularly – and worryingly – low pension participation.

However, just helping people to accumulate more savings is not enough. Currently, people are reaching retirement with too little assistance in how to put the savings they have built up to good use. Our proposals would reduce the risk of people making poor financial decisions with their retirement savings by helping them consolidate their pension pots, thereby simplifying the problem, and guiding them towards good decisions – for example, through default product offers – without necessarily having to access expensive ongoing financial advice.

Finally, there will always be some who need extra financial support from the state in old age. Our proposed reforms would help these people in a well-targeted way by boosting means-tested support for some of those hardest hit by increases in the state pension age and the growing numbers living in the private rented sector in retirement.

Detailed summary of proposals

1. Our proposed reforms can help move towards a pension system that will: (1) provide a secure and stable state pension; (2) provide increased support to many hit hardest by state pension age rises and others particularly at risk of poverty in retirement; (3) increase the number of people saving into a private pension and help many others save more; and (4) offer solutions to help people manage their pension wealth through retirement.

The state pension

2. The current flat-rate state pension, first claimable from a single age and with a simple structure, has many benefits. However, the state pension system faces significant challenges. The ageing population will add considerable additional pressure on the public finances in coming decades, and ‘triple lock’ indexation ratchets up the value of the state pension over time, increasing the cost of the system in a way that creates additional uncertainty compared with increasing the state pension in line with earnings growth. Relying only on raising the state pension age to rein in spending would hit those with lower life expectancy – disproportionately including many on lower incomes – harder. And despite its new-found simplicity, there is a mixture of confusion and pessimism about the state pension.

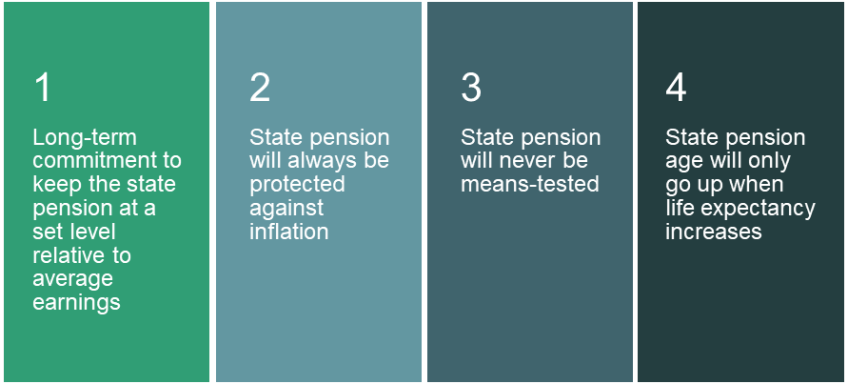

3. To help with these challenges, we propose a ‘four-point guarantee’ for the state pension. This is designed to give people more confidence and certainty over what they can expect their state pension to provide; help them avoid old-age poverty; and provide a bedrock on top of which private pension saving can be built.

4. The four points are:

4.1 There will be a government target level for the new state pension, expressed as a share of median full-time earnings. Increases in the state pension will in the long run keep pace with growth in economy-wide average earnings, which ensures that pensioners benefit when the incomes of working-age households rise.

4.2 Both before and after the target level is reached, the state pension will continue to increase at least in line with inflation every year. Together with the first point, this means that the state pension will follow a ‘smoothed earnings link’, as is used in Australia.

4.3 The state pension will not be means-tested.

4.4 The state pension age will only rise as longevity at older ages increases, and not by the full amount of that longevity increase. To increase confidence and understanding, the government will write to people around their 50th birthday stating what their state pension age is expected to be. Their state pension age would then be fully guaranteed 10 years before they reach it.

5. A key feature of this guarantee is for the government to set a target level of the state pension, expressed as a fraction of average (median full-time) earnings. A full new state pension is currently worth 30.2% of average earnings. As an illustration, a 9% boost to its value would mean a full new state pension being worth 33% of average earnings – and on average give a bigger percentage boost to the incomes of lower-income retirees. But it would cost around £15 billion more per year in 2050 than if the target was the current level of 30.2%.

6. The target level will ultimately be based on political priorities, but under our guarantee the government would not have to move away from the triple lock immediately. Rather, it could communicate what level it wants the state pension to reach, and commit to keeping the triple lock in place until then, introducing the Australian-style smoothed earnings link set out above from the point the target is reached.

7. The smoothed earnings link is an important improvement to the system. Retaining the triple lock while raising the state pension age would hit poorer people more because the loss of a year of state pension income is more important for those with lower life expectancy, as they spend fewer years above the state pension age. On the other hand, those with a higher life expectancy benefit relatively more from the triple lock, as they are more likely to be receiving a generously indexed state pension in their 90s and beyond.

Means-tested benefit system

8. We do not think that early access to a state pension at an actuarially reduced rate is desirable, as it would add complexity to the system and increase individuals’ risk of income poverty at older ages. Instead, there is a case for enhancing the working-age means-tested benefit system, especially as the state pension age continues to rise.

9. We therefore propose additional means-tested support for those within a year of their state pension age, i.e. those aged 66 from 2028 onwards. This support could either be offered to everyone with low incomes and assets (those receiving universal credit) or targeted only to those with low incomes and assets who are also receiving health-related benefits (alongside universal credit). This type of additional support comes at a cost to public finances (costing £600 million or £200 million, respectively). It also reduces work incentives and potentially increases the incentive to apply for health-related benefits if that is the basis of targeting. However, these kind of mitigation measures can play an important role in helping groups that are most harmed by a higher state pension age, as well as in maintaining political and public support for state pension age increases (which significantly increase employment). The public finance costs are a small fraction of the approximately £6 billion annual saving from increasing the state pension age by a year. And to the extent to which such mitigation boosts public support for increases in the state pension age, it might make such increases more likely to be successfully implemented.

10. For pensioners entitled to means-tested benefits, low take-up of pension credit remains an issue. It is essential that the government delivers its plans to integrate pension credit and housing benefit to help with the take-up issues. Private renter pensioners face higher poverty rates and risks due to lower housing security, and the fraction of privately renting retirees is set to grow significantly. We propose that the government increases the maximum housing benefit for private renter pensioners by allowing an extra bedroom in setting the maximum allowance (initially costing around £150 million per year). This would mean that, for example, a pensioner couple would be entitled to housing support that was always based on (at least) the local rents for two-bedroom properties, which would bring the treatment of privately renting pensioners closer to that of social renters. Furthermore, focus groups run alongside this Pensions Review revealed much support for pensioners being entitled to have a ‘spare’ bedroom.

Private pension saving – employees

11. Our modelling shows that many average and higher earners are not on track to reach commonly used benchmark retirement income replacement rates. A significant fraction of lower earners are not saving in a pension. Even if they are saving in a pension, a significant minority of employees are projected to fall short of their ‘target replacement rate’ – a benchmark for avoiding large falls in standards of living at retirement (as defined by the 2002–06 Pensions Commission). A smaller minority are on track for a retirement income that falls short of the ‘minimum standard’ defined by the Pensions and Lifetime Savings Association (£13,400 per year for a single person and £21,600 for a couple, measured after tax and after housing costs, living outside London). There is a clear challenge with two competing priorities: we need policies to help employees reach adequate levels of retirement income, while also mitigating concerns around lower take-home pay in working life. These concerns exist irrespective of whether increases in private pension saving come from employee or employer contributions, as evidence shows that a large fraction of mandated employer contributions are passed on to employees in the form of lower wage growth.

12. There is a strong case for employees to receive an employer pension contribution of at least 3% of their pay, regardless of the employee’s contribution. This would ensure that (most of) those who currently earn too little to have to be automatically enrolled, and those who opt out from saving for affordability reasons, do not miss out on an employer pension contribution. We think this should apply to anyone earning at least £4,000 per year, and for the contribution to be based on total earnings up to the annual equivalent of £50,270 (the higher-rate income tax threshold).

13. As the new state pension provides the same flat-rate amount to everyone with the full number of qualifying years, it alone takes lower earners much closer to their target replacement rates (though it alone does not ensure single people reach the PLSA ‘minimum standards’). Many middle and higher earners will need more significant private savings to ensure that they do not see a large fall in their material standards of living upon retirement. Thus, increases in minimum default total (i.e. employee plus employer) contributions should be targeted in particular at average – and above-average – earners. Those with low earnings in some years, but higher in others, would also (by default) end up saving more – but importantly targeted towards when they were more able to do so.

14. There are many ways in which this could be achieved, and in this report we propose a new set of rules for minimum default total contributions. For employees earning at least £10,000 per year, the minimum default total contribution would equal 3% of £9,000 (£270), plus 10% of the portion of earnings between £9,000 and £90,000. For a middle-earning employee on £35,000 per year, minimum default total contributions would rise by around £570 per year, from £2,300 to £2,870.

15. People should have the ability to contribute less, as well as more, than these defaults if they wish to. We also think the age range targeted by automatic enrolment (currently 22 to state pension age) should be extended to all who are eligible to make tax-relieved pension saving (i.e. all aged 16–74). To future-proof the system, thresholds should be uprated over time in line with earnings.

16. Our proposals would reduce the share of current 25- to 34-year-old employees saving in defined contribution pensions who are projected to fall short of their target replacement rates by more than a third (from 38% to 25%). There would also be falls in the share of employees failing to reach that standard for older groups, though they are much smaller (e.g. from 42% to 39% for current 50- to 59-year-olds) as they have less time to benefit from increased saving rates.

17. These proposals would boost private pension saving by around £11 billion per year. Roughly half of this increase would come from higher employee pension contributions, with the remaining half coming from higher employer pension contributions. Higher pension saving comes at a cost to the exchequer because of the tax advantages attached to private pensions. These proposed changes would result in a short-term cost to the public finances of up to £3.7 billion per year, falling to (at most) £2.1 billion per year in the long run. With a gradual implementation, these exchequer costs would not be realised for a few years. Small broad-based tax rises, or carefully designed reductions in some elements of pensions tax relief, could – if desired – be implemented to make these reforms revenue-neutral.

Private pension saving – self-employed

18. Pension saving rates of the self-employed have declined dramatically over time, with only around one-in-five of the self-employed now saving into a private pension. This fraction is worryingly low. Even among those who are saving in a private pension, over a quarter make unchanged regular contributions (in cash terms) after five years. Most self-employed people are on track for an inadequate retirement income if relying only on their own pensions, although the picture is improved once we include incomes of partners, inheritances and other wealth.

19. To help the self-employed, more should be done to facilitate their pension participation, drawing on lessons from the success of automatic enrolment. We propose that at a minimum, the self-employed should be required to make an active choice about the level of pension contributions when filling out a self-assessment tax return. Going further, they could be automatically enrolled into a private pension, or potentially a Lifetime ISA, at the point of self-assessment, with the option to opt out. For those who set up direct debits for pension saving, these should by default increase automatically over time.

Small pots consolidation and managing retirement incomes

20. The number of small, deferred private pension pots is large and growing. In 2024, there were around 23 million deferred defined contribution pots worth under £10,000. The number of deferred pots worth less than £1,000 increased by almost one million between 2023 and 2024 (to 13 million). Low earners and women are particularly likely to accumulate small pots. This proliferation of small, deferred pension pots is burdensome for savers as they are difficult to keep track of, and uneconomical for pension providers, thereby reducing the net returns available within pensions.

21. It is welcome that the government has announced it will move forward with small pots consolidation. It will do this by introducing a ‘multiple default consolidator approach’ in which small deferred pots (£1,000 or less) are by default consolidated into one of a small number of nominated pension schemes, with the option to opt out. This is a significant improvement on the status quo. While only deferred pots of £1,000 or less will be automatically consolidated initially, the Pensions Minister Torsten Bell has described the reforms as ‘the starting point’, which we hope indicates an ambition to increase this limit over time. However, as the size limit for automatic consolidation increases, more and more pots would flow into a small number of approved consolidator funds. This anti-competitive effect might cap how high the size limit can be set. People should typically end up with one, or a small number of, defined contribution pension pots at the point of retirement. Many will still need to consolidate their own pots to achieve this, and it needs to be made as easy as possible for individuals to do this sensibly.

22. There are stark challenges for people managing defined contribution pension wealth through retirement, with risks over how long they are going to live (longevity risk), asset returns (investment risk), inflation risk, risk related to the loss of a spouse, and risk of becoming less able to make good decisions at older ages due to cognitive decline. Together, these mean people risk either drawing on their wealth ‘too slowly’ or depleting their pension too quickly.

23. Most people are likely to need more protection against longevity risk than is currently provided by the state pension alone, as their living standards would see sharp falls if they were solely reliant on this. The recently published Pension Schemes Bill would require many pension schemes to introduce default retirement income solutions. A ‘flex then fix’ product, where people have the flexibility of drawdown earlier in retirement and the security of an annuity later in retirement, is likely to be a good model for many. However, the defaults should be carefully designed. They should be ‘soft’ so that they are easy to opt out of, and there should be the potential for different defaults for different types of individuals. The ability to deviate from the default will likely be particularly important for those with other annuitised income streams (such as defined benefit pensions) and those with a low life expectancy. For those who want to make a more active decision around decumulation, people should be able to receive high-quality information on their options without ongoing commitment to expensive financial advice, along the lines of the Financial Conduct Authority’s proposals for targeted support.

24. It is also important that people view pensions as pensions, rather than just another accessible savings pot. To ensure this, the age at which people are able to start to access their defined contribution pension pots should be gradually increased over time so that it reaches age 60 by the time the state pension age reaches 68 in the mid 2040s. In addition, the way in which tax benefits of private pensions are described should not accidentally encourage people to withdraw large amounts from their pensions early in retirement. The 25% tax-free element is invariably described as a ‘tax-free lump sum’. This risks inadvertently – and inappropriately – steering people towards taking 25% of their pension up front as a lump sum. It would be better if it were instead called the ‘tax-free component’ or ‘tax-free element’.

Implementation

25. There is a strong case for urgent action. Reforms to encourage more private pension saving can do more to support the future retirement incomes of those who are younger as they will spend more time under the improved system. Each year that passes without policy changes to help people spend their wealth wisely in retirement means an extra set of retirees being more likely to make mistakes in using their pension wealth, with potentially long-lasting adverse financial consequences.

26. While reform is urgently needed, that does not mean it all has to be implemented immediately. Changes to automatic enrolment should first be consulted on with schemes and employers to ensure a smooth implementation. Piloting some changes with larger employers – as was the case with the initial roll-out of automatic enrolment – is an additional option. Reforms should be announced as soon as possible but with a gradual phase-in period to allow employers and individuals time to adjust. There is a good case for announcing the target goal of the state pension sooner rather than later. Other reforms, in particular to help people use their wealth sensibly in retirement, should come more quickly, as there are fewer near-term barriers to implementation and the problems are more acute.

1. Introduction

In April 2023, the Pensions Review – led by the Institute for Fiscal Studies in partnership with abrdn Financial Fairness Trust – was launched, with the aim of comprehensively assessing the consequences of current pension policy, the economic environment and individual behaviour for the future of living standards in retirement. While the Pensions Commission’s final recommendations in 2005, and the subsequent implementation of these proposals, marked a change in direction, and improvement, in UK pensions policy, it has been around two decades since the publication of its final report, and much has changed in the intervening period.1

From the outset of this project, we argued that there was complacency about the retirement living standards of future pensioners (Cribb, Emmerson, Johnson, Karjalainen and O’Brien, 2023). Average pensioner incomes – after tax and after accounting for housing costs and household size and structure – are currently similar to those for people below state pension age. But many of today’s retirees benefited from generous final salary pensions, rising earnings and asset prices, and very high levels of homeownership, none of which is likely to apply to the next generations of retirees (although the next generation are more likely to receive a significant inheritance in their lifetime).

We outlined concerns about many employees making only modest pension contributions and about low pension participation for the self-employed. We set out the large number of risks that people face in the pension system, including the risk of running out of private resources at older ages, and the risk of poverty if people are still living in the private rental sector upon retirement. And these challenges are exacerbated by ongoing demographic pressures on the public finances, with an ageing population pushing up state spending both on state pensions (and pensioner benefits) and on health and social care.

In this context, as part of this Review, we have systematically reviewed the evidence on the challenges facing future pensioners and undertaken careful empirical analysis to understand recent economic trends and how people have responded to previous pension reforms. We have published a large number of reports (see Appendix D for a full list) and held events to publicise our findings and policy proposals.

We have also extensively engaged with policymakers and other stakeholders representing different groups in society to understand their views on the key challenges and trade-offs. We have worked with abrdn Financial Fairness Trust to commission opinion polling and public engagement activities, undertaken by Ignition House, to understand how people from across the country see the challenges of funding their own retirements and gather their thoughts on potential routes for reform. Summaries of findings from this work and quotes from participants are included throughout this report.

This report brings together our policy proposals which have been informed by the analysis conducted since the launch of this project. In this report, we provide recommendations for reform to improve outcomes for future generations of pensioners across the UK. Importantly, rather than looking at only one part of the pension system at a time, we look at the different aspects of the pension system together. In a system where a combination of public support and private saving is needed to ensure adequate standards of living for retirees, it is important to consider the big picture, rather than focusing on individual parts of the system on their own. The rest of this report proceeds as follows. Chapter 2 sets out our key proposals for improvements to the pensions system. Chapter 3 sets out analysis of the package of reforms, focusing on the effects on both employees and their employers. Chapter 4 sets out considerations regarding implementation of these proposals, including an indicative timeline for the different elements of the package, and the public finance consequences of the reforms. Chapter 5 provides a short conclusion.

2. Reforms needed to improve the current system

The building blocks of the UK pension system are strong – in particular, the flat-rate state pension and an automatic enrolment system that helps employees build private savings on top of it. But, as illustrated in the executive summary, urgent reform is needed to ensure that the pension system works better for those at risk of not achieving adequate standards of living in retirement. In this chapter, we introduce our proposed reforms which build on the successes of past policy reforms.

Most of these proposals were introduced in previous reports published as part of this Review, which provide a great deal of background analysis and detail for the reasoning behind them.2

2.1 Reforms to state support

State pension four-point guarantee – a better way forward

In the past, the UK’s state pension system was overly complicated, and it was difficult for people to understand how much state pension entitlement they had built up or were expected to build up (e.g. Bozio, Crawford and Tetlow, 2010). Too many people – in particular, too many married women – did not qualify for a full state pension. Successive reforms improved things for many groups, culminating in the introduction of the flat-rate new state pension for those reaching the state pension age from April 2016 onwards. Projections show that most new retirees (80%) will receive the full new state pension by 2030 (Department for Work and Pensions, 2013). It is commendably simple, and we believe it can, and should, provide a strong and reliable foundation for private saving decisions.

Given this, drastic changes to the structure of the state pension are not needed. However, we propose a set of reforms to help improve the sustainability and reliability of the state pension system. Our proposals are summarised in the four-point pension guarantee, first discussed in Cribb, Emmerson, Johnson and Karjalainen (2023), and illustrated in Figure 2.1.

Figure 2.1. The four-point pension guarantee

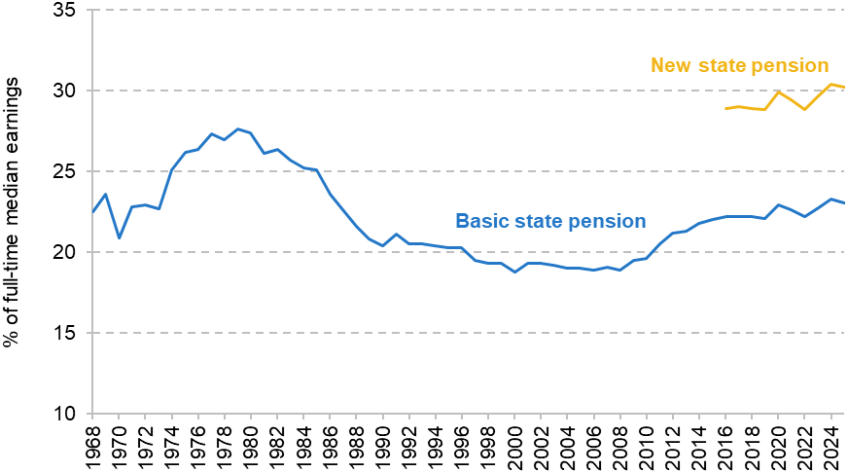

The first part of the guarantee states that the government should decide the level of state pension relative to economy-wide average earnings, which could be at or higher than the current level (of 30% of full-time median earnings). This target for state pension would then be maintained over the long run, providing people and government finances certainty over the level and cost of the state pension in the future. This would also ensure that pensioners’ incomes are boosted over time as standards of living more generally rise.

This would be an improvement over the current system, where the triple lock (by which the state pension rises each year by the highest of average earnings growth, inflation as measured by the CPI and 2.5%) boosts the value of the state pension relative to earnings, but does so in an unpredictable way, and only in periods of poor economic performance when average earnings growth is low (Cribb, Emmerson and Karjalainen, 2025). We estimate that under the triple lock, in 2050 a reasonable range (i.e. between the 10th and 90th percentiles, occurring 80% of the time) for the value of the new state pension in 2050 is between 31% and 37% of median full-time earnings. This creates uncertainty when it comes to future spending on the state pension. Based on our calculations, a reasonable estimate (taking place 80% of the time) for additional spending on the state pension in 2050 due to the triple lock, above and beyond earnings indexation, would be between £5 billion and £40 billion a year in today’s terms.

While some have argued that the triple lock should be supported to generate a higher state pension (e.g. Portes, 2023), if the government wants a more generous state pension relative to average earnings then it would be better to set that as an explicit goal than to use the triple lock which is a mechanism that may or may not deliver the sought-after higher state pension by any given future date.3

The second part of the guarantee states that the state pension will always be protected against inflation. This means that when average earnings growth is below the rate of inflation, the state pension should increase in line with inflation until the target level of the state pension is reached again. This is the system used to index the state pension in Australia and is illustrated in Figure 2.2. It protects the incomes of pensioners when inflation outpaces average earnings growth, while ensuring that the level of the state pension relative to average earnings remains stable over time. This is sometimes known as the ‘smoothed earnings link’, because of the way in which it maintains the link between the state pension and average earnings, while also making sure that the state pension rises in line with inflation in every period. This is also the type of indexation for the state pension that was recommended by the House of Commons Work and Pensions Committee (2015), which proposed that this form of indexation be introduced starting in 2020.

Figure 2.2. Illustration of how our suggested new style of indexation would operate

Note: Assumes inflation of 2% and average earnings growth of 5% in years 1–5 and 3% in years 6–9. In the first period of negative real earnings growth, average earnings growth falls to 0% for one year. In the second period of lower average earnings growth, which lasts four years, the rates are 0%, 1%, 2% and 3%. Between the periods of negative real earnings growth, the nominal average earnings growth rate is 4%, as it is in the final three years.

The third part of the guarantee is a promise that the state pension will never be means-tested. The temptation of an apparently lower-cost means-tested approach should be resisted as it would disincentivise saving for many and therefore risk undermining the success of automatic enrolment. This promise would help working-age people in planning their retirement, as they could have trust in the state pension being available to them in retirement. It is also worth noting that the state pension makes up a large part of incomes even for people on higher incomes. For recent retirees, the state pension on average accounts for 71% of income for low-income pensioners (bottom fifth of income), but even for the richest fifth the state pension makes up 23% of their overall income (Cribb, Emmerson, Johnson and Karjalainen, 2023). In the public engagement work commissioned for this Pensions Review, people tended to agree with not means-testing the state pension, with the state pension seen as an essential element of the welfare system.

‘[The state pension has] always been there and is part of the country’s DNA; as is the NHS. People need structure in their lives and to feel that the Government has their back when it comes to their working life, if they get ill, and retirement.’

Male, aged 65–74, homeowner

The final point of the guarantee relates to the state pension age. When longevity at older ages increases, the state pension age should also rise, but it should not increase by the full amount of that increase in longevity. Communicating the state pension age clearly and effectively is also important. To increase confidence and understanding, we propose that the government should write to people around their 50th birthday stating what their state pension age is expected to be. Their state pension age should then be guaranteed 10 years before they reach it.

Choosing the level of the state pension and phasing it in

A key part of our vision for the state pension is that the government should choose a level for the state pension relative to average earnings. It is worth noting that if the state pension is indexed to average earnings in the medium run, the value of the state pension rises over time as living standards improve, meaning real pensioner incomes should rise over time. In choosing this level of the new state pension, the government has to consider the trade-off between a higher income for pensioners and the public finance implications – namely, higher taxation or lower government spending on other items – that would have. Spending on the state pension is currently (in 2025–26) £146 billion per year.4

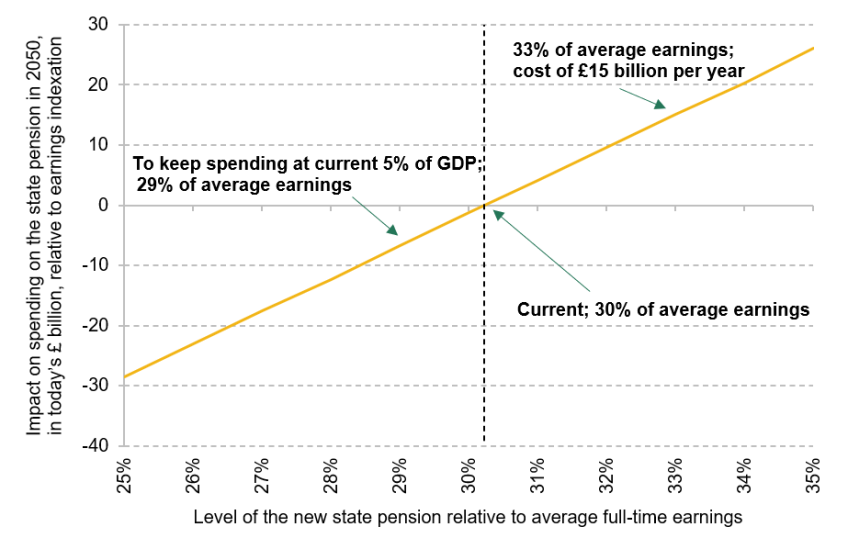

To illustrate the cost of increasing the value of the state pension relative to average earnings, Figure 2.3 shows the cost in 2050 of different levels of the state pension (measured in today’s terms) relative to keeping the state pension, as today, at 30% of median full-time earnings. We also show in Table 2.1 how much the target levels of the state pension would save the government in 2050, relative to the central expected path of the triple lock. Any target level up to 34% would be expected to lead to a public finance saving in 2050 relative to the triple lock – although due to the nature of the triple lock there is a lot of uncertainty around this, as the additional cost of the triple lock in 2050 is uncertain. The table illustrates the central scenario, but the savings could be much more (or less) than this based on how the economy performs over the next 25 years.

Figure 2.3. The trade-off between the level of the state pension and the cost to public finances

Table 2.1. Level and cost of the state pension, for different relativities to average earnings

| 2025 | 2025 | 2025 | 2050 | 2050 |

|

Value of new state pension relative to average earnings | Weekly nSP (£) | nSP difference relative to current | Cost relative to current (£bn) | Cost relative to earnings indexation from now (£bn) | Expected saving relative to triple lock central case (£bn) | When triple lock central case would achieve this level |

31% | 236 | +2.5% | 3.1 | 4.2 | 16.4 | 2030 |

32% | 244 | +5.8% | 7.2 | 9.7 | 11.0 | 2037 |

33% | 251 | +9.1% | 11.3 | 15.1 | 5.5 | 2043 |

34% | 259 | +12.5% | 15.4 | 20.3 | 0.3 | 2050 |

Memo: current level (30.2%) | 230 | N/A | Current cost: £146bn | N/A | 20.6 | N/A |

Note: nSP refers to the new state pension.

Figure 2.3 shows that, for example, increasing the state pension to be at 33% of average earnings in 2050 would cost an additional £15 billion per year in today’s terms (about 0.5% of national income), compared with keeping the state pension at its current share of average earnings. That would be a saving of £5.5 billion compared with our central expectation of spending under the triple lock. It would also deliver a state pension equivalent (in terms of today’s earnings) to £251 per week, i.e. £21 (or 9%) higher than today’s full new state pension of £230 per week. More options are illustrated in Table 2.1.

Setting the level of the state pension is ultimately a question of political priorities. The government needs to decide how high a foundation level of income in retirement it wants to provide, and hence what level of taxation it is willing to impose in order to achieve that, and the resulting balance between state and private pensions.

One aspect of the state pension is that it helps protect most people from income poverty in retirement. But – unlike over the 1970s and 1980s when most pensioners were low-income – using a higher state pension to achieve further pensioner poverty reduction is a blunt tool (a point also recently made by others, such as Otto (2025)). Increasing the state pension benefits not only pensioners on low incomes, but those on middle and higher incomes, whose incomes are well above the poverty line. Increasing the level of the state pension is therefore an expensive way of reducing pensioner poverty. The state pension should also not be considered in isolation as the only possible way to target pensioner poverty in a system where private pensions and the means-tested benefit system also play a key role (though the effectiveness of the means-tested system at reducing pensioner poverty would be boosted by further addressing long-standing issues of far from complete take-up of pension credit).

Most parties across the political spectrum have stated their commitment to the triple lock in election manifestos including at the 2024 general election. The Pensions Minister Torsten Bell also reiterated the current government’s support for the triple lock in April 2025.5 There may be political costs from moving away from the triple lock, especially in this parliament, given the Labour party manifesto committing to it in 2024.

However, assuming that the government desires a higher level for the state pension (relative to average earnings) than we have currently, it can still choose a pre-specified target that would allow it simultaneously to: increase the value of the state pension (in real terms and relative to earnings); keep the triple lock in the short run (e.g. during this parliament); and move to the ‘smoothed earnings link’ when it has achieved its announced aim of reaching its target.

Table 2.1 shows the central estimate for when the triple lock is expected to lead to specific levels of the state pension relative to average earnings. However, this central estimate is based on economic outcomes from 1992 to 2025 and, depending on how the economy performs in the future, reaching any specific level could take more – or less – time than anticipated. It is also worth noting that even with earnings indexation from 2025, spending on the state pension would rise by 0.2% of GDP, or £5 billion in today’s terms, by 2050, in particular due to the rising number of pensioners.

As part of this Pensions Review, public engagement work was commissioned, where people were asked for their views on a higher state pension (32% or 34% of average earnings). Overall, people tend to prefer the highest state pension presented; but when confronted with the public finance costs, many then opted for the more moderate increase. Many seemed surprised at how expensive even small increases in the level of the state pension are for public finances – the expense follows from the fact that the state pension is received by 13.2 million pensioners.6 Increasing the level of the state pension by 1% of average earnings (which is around a 3% increase in the state pension) costs an additional £4 billion per year.

When people were asked in our public engagement work how they would like to pay for a higher state pension, most had negative reactions to funding a higher state pension through increasing the state pension age – many believe it is already too high.

‘It should not be raised. People cannot work as well in their 60s. I know because I know how much my own skills have reduced. People should not have to work until they die. It will create an even bigger rich poor divide – with the poor working till 70 and then dying and the rich retiring early cos they don’t really need the state pension to retire.’

Female, aged 55–64, homeowner

When pushed, people preferred tax rises over a higher state pension age, in particular VAT increases (rather than income tax rises) as they believed that would mean everyone pays more, which is seen as appropriate as everyone will benefit from a higher state pension. However, people expressed surprise at the cost associated with any pension increase and recognised it was a difficult situation. Most people were looking for a ‘third way’ of finding savings rather than tax rises, mentioning MPs’ expenses for example. However, spending on categories such as MPs’ expenses is only a tiny fraction of the cost of a higher state pension.

‘[A higher state pension should be paid for by increases in] VAT because everyone will get a pension, so everyone should help pay for it.’

Male, aged 35–44, homeowner

‘This is a nightmare choice either way.’

Female, aged 35–44, homeowner

The state pension age

The state pension age was 65 for men and 60 for women from 1940 to 2010. Since 2010, it has risen to age 66 for both. Longevity at older ages during the late 20th century and early 21st century has increased dramatically. For example, between 1975 and 2020 life expectancy of men at age 50 increased by 8 years, while the state pension age (for men) increased by just 1 year, meaning that the time for which men aged 50 could expect to receive the state pension age increased by 7 years. And even though the state pension age for women rose by 6 years over this period, women are still expected to spend on average 20 years receiving the state pension (Cribb, Emmerson, Johnson and Karjalainen, 2023).

The state pension age is legislated to rise further to 67 between 2026 and 2028, and to 68 between 2044 and 2046. The government is also required to conduct periodic independent reviews of the state pension age, to be published within six years from the previous report. There have been two such reports so far, undertaken in 2017 and 2022 (Department for Work and Pensions, 2017 and 2023a), which both recommended that the SPA should rise to 68 earlier than currently legislated, but governments have not made any changes to state pension age legislation as a result of either of these.

Increasing the state pension age is a reasonable way for a government to control the increased public finance pressures arising from rising longevity at older ages. Our modelling (Cribb, Emmerson and Karjalainen, 2024) shows that increasing the state pension age by one year would save the exchequer around £6 billion per year, which is about one-and-a-half times the increase in spending from a 1 percentage point increase in the value of the state pension relative to average earnings.7

However, state pension age increases will also have a different distributional effect from that of other tools for controlling the rising cost of the state pension, especially a policy change of moving away from the triple lock. Retaining the triple lock while raising the state pension age would hit poorer people more because the loss of a year of state pension income is more important for those with lower life expectancy (which poorer people tend to have), as they spend fewer years above the state pension age. On the other hand, those with a higher life expectancy benefit relatively more from the triple lock, as they are more likely to be receiving a generously indexed state pension in their 90s and beyond.

Modelling in the 2022 Independent Review (Department for Work and Pensions, 2023a) shows that the increases in the state pension age required to keep spending on the state pension below a certain level of national income would also have to be substantial. That modelling shows that to keep public spending on the state pension below 6% of national income while retaining the triple lock, the state pension age would have to rise to 69 by 2048–49 and 74 by 2068–69.

While we think that the state pension age should rise as longevity at older ages rises, but not by the whole increase in longevity, this still leaves room for different political parties to prioritise increasing, or holding down, the state pension age to different extents. Our proposal is also consistent with, for example, the principle of keeping the ratio of adult life spent above the state pension age constant.

In this report, we do not take a view on the exact degree to which the state pension age should rise in coming decades. As with the choice around the level of the state pension, the state pension age is just one parameter to consider in a system where other factors such as availability of private resources and the generosity of the working-age means-tested benefit system will also change the way in which increases in the state pension age affect people’s outcomes. However, given that in 2017 the Conservative government accepted the recommendation of the 2017 Independent Review of bringing the state pension age rise to 68 forward, but did not legislate this change, the current government should clearly set out a plan for when we will get to a state pension age of 68 – and specifically whether this should be brought forward. This is particularly timely and important now, as both independent reviews of the state pension age have sensibly recommended that any changes to the state pension age be communicated to people at least 10 years in advance.

The government should promptly conduct a new review of the state pension age, using the latest projections of longevity, and make a swift decision on when (not if) these increases should come in, to provide more guidance to people on what they can expect. This review should also assess the latest data to see how evenly recent changes in mortality have been felt.

The means-tested benefit system in the lead-up to state pension age

A higher state pension age will not affect all groups to the same extent. Lower-income people are more reliant on a state pension in retirement and have less private savings to fall back upon. Moreover, people with lower lifetime earnings and incomes have, on average, lower life expectancies, so for those who survive to pension age, missing out on a year of state pension payments reduces their expected receipt of the state pension by a much greater proportion than it does for better-off groups. Many find it hard to remain in paid work up to the state pension age – the employment rate at age 65 (i.e. just below the current state pension age of 66) is 44% for men and 34% for women. While some of those not in paid work will have made a voluntary choice to retire, a significant minority (12% of 65-year-olds) report being economically inactive due to ill health (Cribb, 2023). When the state pension age is increased, more should be done to support those who are at risk of being left behind on a low income. Without action, we can expect the gap between income poverty rates among those just below, and those just above, the state pension age to continue to rise.

Despite this, in our judgement, the UK should maintain a single universal state pension age, rather than introduce an ‘early access’ age in return for an actuarially reduced award as is possible in many countries. This often occurs in settings with much more generous state pensions – and less reliance on private savings for retirement incomes – than is the case in the UK. In contrast, opting for early access at a permanently reduced rate of state pension in the UK would mean receiving a potentially fairly low state pension throughout retirement, increasing individuals’ risk of income poverty at older ages. We therefore think that rather than allowing early access, additional support for those hardest hit by increases in the state pension age should come from enhancements to the working-age benefits system.

We therefore recommend that a small fraction of the fiscal savings from any future increase in the state pension age should be recycled into making universal credit (UC) more generous for those in the run-up to that age. In our Pensions Review report on the means-tested benefit system around state pension age (Cribb, Emmerson and Karjalainen, 2024), we discussed two broad options – targeting additional support to those aged one year below the state pension age who are in receipt of UC, or to those in the year before state pension age who are receiving UC as well as disability benefits.

There are good reasons for providing additional support for this specific group. People in the year below state pension age are close to being able to access the pensioner benefit system. This means that while additional support would affect the work incentives for this group, we may worry less about the long-run effects of this as they are close to the state pension age in any case. It is also the case that there is a big step up in the amount of out-of-work financial support available at the state pension age – our proposal replaces this large step up with two steps up which are each half as big.

We modelled the cost of these two policies as £600 million a year (for the reform where increases apply to all receiving UC) or £200 million a year (for those receiving UC and disability benefits) – these are relatively modest costs in that they are equivalent to around 10% and 3% of the savings from a one-year increase in the state pension age. It is worth noting that the final cost would, of course, depend on the exact uplift the government chooses. In the Spring Statement in March 2025, the government also proposed changes to working-age health-related benefits which will reduce these costings. In particular, the government is making it more difficult for some to receive personal independence payment (PIP). While the Office for Budget Responsibility (OBR) has estimated this will reduce the number of claimants by 800,000, this estimate is highly uncertain as it will depend on how claimants and assessors change their behaviour, which may also vary by age. The balance of how much the basic element of UC is worth relative to the health element is also changing – the government has suggested an increase in the UC basic element and a reduction in the health-related benefit. These changes will also affect the costing of our proposed policies, if the adjustments to support for those below the state pension age change.

The qualitative research commissioned alongside our Pensions Review suggests that the public also support additional help for some of those most affected by state pension age increases. Increased support was particularly favoured for those with disabilities, as this group was seen to require more support and be more reliant on state benefits. International evidence from the IMF (International Monetary Fund, 2025) also indicates that pension age rises are more publicly acceptable – and politically easier to implement – when accompanied by such mitigation measures. This means that dedicating some of the savings from raising the state pension age to targeted support for poorer groups could also improve political sustainability of the principle of increasing the state pension age as longevity at older ages rises.

‘People who suffer from disabilities or ill health should not be penalised, and should have access to the equivalent pension rate. Ten years is a long time to wait for your state pension if you are too ill to work. The worry and having to live on a reduced income cannot help with their health issues.’

Male, aged 75–84, private renter

The means-tested benefit system for pensioners

The means-tested benefit system for pensioners is much more generous than that for working-age people. However, two changes should be made that would improve state support for low-income pensioners. First, means-tested benefits for pensioners should be streamlined so that they are made easier to claim. It is therefore welcome that the government is working on integrating pension credit and housing benefit for pensioners, which should increase take-up of both as people only have to submit one (higher-stakes) application for most state support.

Second, pensioners should be entitled to more generous housing benefit. The maximum housing benefit that people can receive is based on the distribution of local rents and the size of the household – for example, the maximum housing benefit for couples and single people is (typically) based on the 30th percentile of rents of one-bedroom properties in the local area. We propose that pensioners’ maximum housing benefit should be based on an additional bedroom. This means that for couples and singles, pensioners’ maximum housing benefit would be based on the distribution of local rents of (at least) two-bedroom properties rather than of one-bedroom properties. This would immediately benefit all pensioners whose housing benefit does not fully cover their rents. Support for an additional room compared with working-age individuals can be justified on the basis that pensioners often spend more time at home than working-age people. They may also have adult children, and/or disabilities, which make a second bedroom particularly useful, especially if they require care. It would also more closely align support with housing benefit for those in the social rented sector, where pensioners are not subject to the so-called ‘bedroom tax’. We model the current cost of the policy as £150 million per year, although this would likely rise in the future as more retirees enter retirement as private renters (Cribb, Emmerson and Karjalainen, 2024).8 However, the relatively modest cost reflects the targeted approach of our proposal. As illustrated by the quote below, we found widespread support for this proposal in the public engagement work.

‘An extra bit of space for carers/relatives to stay in times of ill health would be good.’

Male, aged 65–74, homeowner

We think this policy should be introduced in addition to LHA rates being permanently linked to the 30th percentile of local rents for all of those receiving state support with their housing costs, as has been highlighted by other advocacy groups (e.g. Independent Age, 2025).

2.2 Reforming the private pension system

The majority of private pension saving in the UK is done in workplace pensions that are facilitated by employers. All employers have to enrol ‘eligible’ employees automatically into a workplace pension with at least minimum levels of contributions. Eligible employees are those aged between 22 and state pension age and earning at least £10,000 per year. Employers can also delay automatically enrolling new employees for up to three months.

Under automatic enrolment, there is both a minimum default employer contribution of 3% of qualifying earnings (the portion of earnings between £6,240 and £50,270 per year) and a minimum default total (i.e. employee plus employer contribution) of 8% of qualifying earnings. Employees can choose to opt out of workplace pension saving entirely, meaning neither the employee nor the employer contributes to the pension. Employers choose a workplace pension provider for their employees, meaning that when people move employer they generally start saving into a new pension pot. Private pensions can be accessed, in any way that the individual wishes, from age 55 (rising to 57 in Apil 2028).

How to help employees not saving enough

Irrespective of the exact level that the flat-rate state pension could reasonably be set at, we need a private pension system that facilitates many to have a higher income in retirement than that provided by a full state pension. Large numbers of private sector employees – our modelling suggests a majority – are on course to achieve commonly used benchmarks for retirement saving adequacy. But a substantial minority (39%) – and in our view too many – appear on course to fall short of their target replacement rate (as shown in Figure ES.1 in the executive summary). A smaller, but still important, minority, appear on track to fall short of a ‘minimum’ standard of living in retirement. For any realistic value of the new state pension, more private saving for retirement is needed to help more middle- (and higher-) income people achieve a standard of living in retirement that does not fall well short of what they experienced in working life. More pension saving will mean some combination of lower take-home pay for working-age households and increased obligations for employers, and it will mean more tax relief which is attracted by those higher pension contributions.

The obvious lever to facilitate more pension saving among employees is through enhancements to automatic enrolment. Public engagement work shows that there is a great deal of support for automatic enrolment, with many employees acknowledging they would not be saving otherwise.

‘I think if left to me I would not be disciplined enough to save for retirement. I think I would always find something more important at the time to spend the money on. In the current economic climate, there is little disposable income, and paying for something now is a greater need than investing in the future.’

Female, aged 55–64, homeowner

However, any enhancements to the current system need to be carefully designed. Increasing the saving – and therefore reducing the spending – of working-age households who are currently on a low income and struggling would create greater hardship today. This is true even when extra contributions come from employers, as the majority of higher employer pension contributions would likely be passed through to lower wages.9 Among lower earners who are currently targeted by automatic enrolment (i.e. earning between £10,000 and £15,000 per year), over a fifth are in relative poverty and half have less than £1,500 in liquid savings (Cribb, Karjalainen and O’Brien, 2024). Some of this group will have low living standards consistently throughout working life, but will have the state pension to rely on in retirement. Encouraging these people to save more – and spend less – in working life, and for those savings to be locked away in a pension, is hard to justify. Other low earners will only have low earnings temporarily, but would be better served by saving more for retirement at other points of life when their earnings are higher rather than saving more when their earnings are low.10

These considerations point towards targeting higher minimum default pension contribution rates at those on middle (and higher) earnings, and potentially those at older ages, who are often more able to bear increased saving due to lower costs of living (e.g. due to lower (or no) mortgage payments, and children often having moved out of the family home). In addition, employees earning more than the upper limit for qualifying earnings (£50,270) currently face a declining minimum pension contribution rate (as a percentage of their pay) as they earn more. These people should generally be saving a higher share of their earnings as they earn more, to help them smooth their incomes over their lifetime, so the current automatic enrolment minimums are not guiding them to make good savings decisions. One-in-six of those earning between £50,270 and £70,000 are making minimum contributions currently – and this is the case for only 2% of those earning £70,000–£100,000 (see Figure C.4 in Appendix C).

Despite the success of automatic enrolment, around 20% of private sector employees are not saving in a workplace pension (O’Brien, Sturrock and Cribb, 2024). Roughly half of this group are not in the target group for automatic enrolment (which includes many women who work part-time and so earn below the ‘earnings trigger’ of £10,000 per year), while the other half are targeted but have chosen to opt out. These employees do not receive an employer pension contribution.

Making the minimum employer pension contribution almost universal for employees, as first suggested in Cribb, Emmerson, Johnson, O’Brien and Sturrock (2024), so that employees receive it whether or not they themselves contribute, would boost employer pension contributions particularly for lower earners. And it would do so in a way that is less likely to depress their wages, as any resulting slowdown in wage growth cannot easily be targeted at those who would otherwise have opted out of their workplace pension. Arguably, this increases the fairness of the system – those who perhaps cannot afford their own contributions do not lose out on employer contributions. This reform would, though, reduce the financial incentive for some employees to save in a pension and might therefore lead to a fall in the share of employees making contributions themselves. However, as discussed in Cribb, Emmerson, Johnson, O’Brien and Sturrock (2024), previous evidence suggests that the fall in employees making contributions would likely be limited. If the government was particularly worried about an increase in opt-outs, it could trial the ‘non-contingent’ employer contribution in a limited number of employers before universal roll-out.

In addition, there are good reasons to extend the age range eligibility for automatic enrolment to boost saving and to simplify the system. Indeed, it is not clear why the age range for automatic enrolment should exclude some employees who are allowed to save into a tax-advantaged pension (all those aged 16–74). Extending the age range for eligibility would also further expand the number of employees benefiting from the minimum employer contribution: we estimate that around 1.5 million employees who are younger than 22 or older than 65 would benefit from an increase in employer pension contributions.

There are several potential reforms to automatic enrolment that could achieve our aims of higher total contribution rates for middle and higher earners alongside introducing a ‘non-contingent’ element to the employer pension contribution. Below is one set of parameters:

- age range for eligibility: 16–74;

- earnings trigger for eligibility: those earning at least the equivalent of £4,000 per year;

- minimum employer pension contribution: 3% on the band of earnings from £0 up to £50,270 and irrespective of whether the employee contributes;

- minimum default total (i.e. employee plus employer) pension contribution:11

- 3% of earnings for employees earning at least £4,000 and less than £10,000 per year;

- 3% of £9,000 (i.e. £270) plus 10% of earnings between £9,000 and £90,000 for employees earning at least £10,000 per year;

- employees have the option to ‘opt down’, reducing their total contribution below the minimum default total contribution without losing the minimum employer pension contribution.

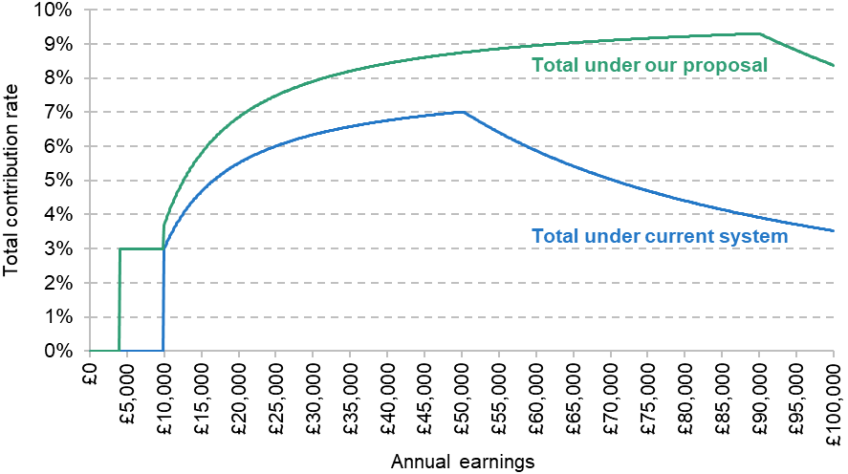

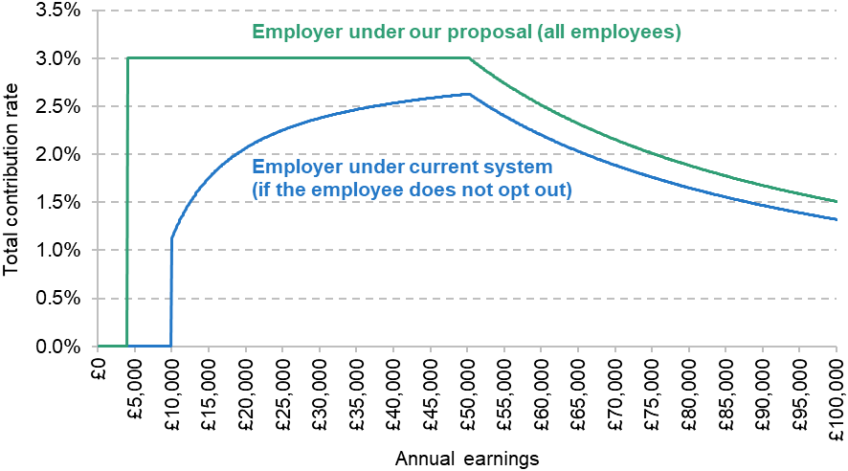

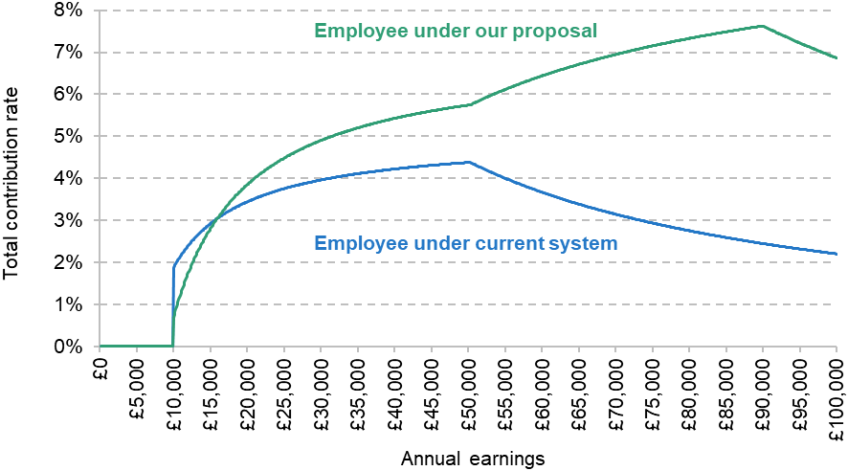

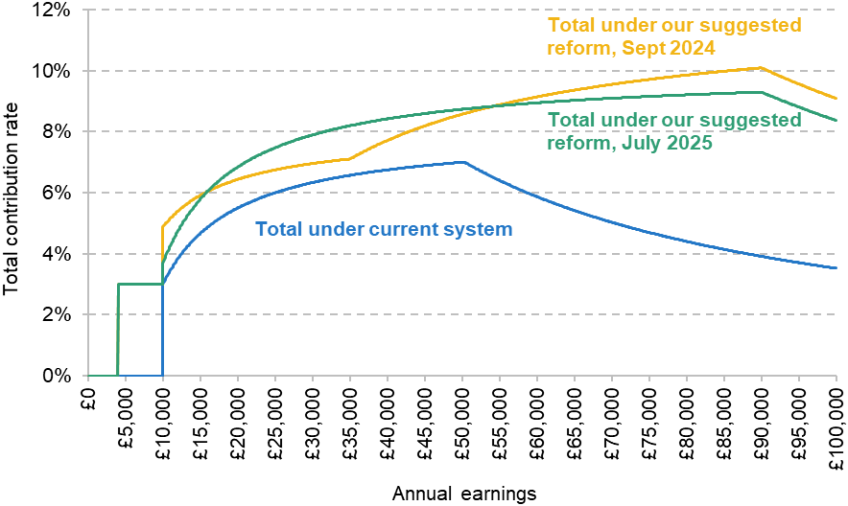

Figure 2.4 shows the minimum default total contribution rate, as a percentage of total earnings, for different levels of earnings under both the current automatic enrolment system and our proposals. The corresponding graphs for the minimum employer contribution rate, and the implied default employee contribution rate when employers make minimum contributions, are Figures C.1 and C.2. Our proposals imply an increase in the minimum default total contribution rate at all levels of earnings, and indeed increases that are larger (both in cash terms and as a percentage of earnings) for people on middle and higher earnings than for people on lower earnings, with the exception of people earning between £4,000 and £10,000 who would under our proposals receive an employer pension contribution for the first time.

Figure 2.4. Minimum default total (employee + employer) contribution rate, % of total earnings, under different potential automatic enrolment systems

How these proposals impact incomes and savings is determined both by the change in the minimum default contributions and by the extent to which different groups are actually affected by these changes. Middle and higher earners are much more likely than lower earners to contribute more than the current default minimum amounts, meaning middle and higher earners are typically less affected by changes to these minimums. Among private sector employees currently saving in a defined contribution pension, over half of those earning between £10,000 and £20,000 have (current) minimum pension contributions, compared with only one-in-six of those earning between the higher-rate tax threshold (£50,270) and £70,000, as shown in Figure C.4. In Chapter 3, we show explicitly how this set of reforms would affect different groups of employees and employers.

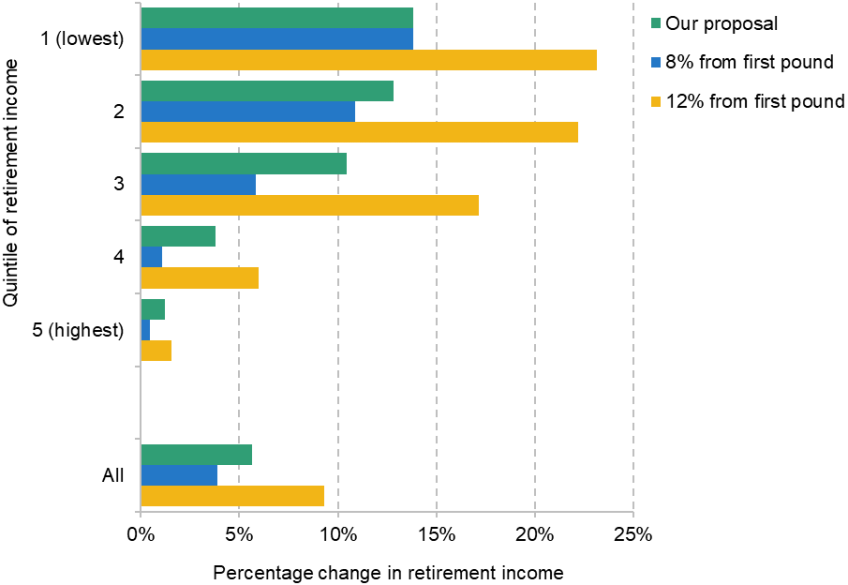

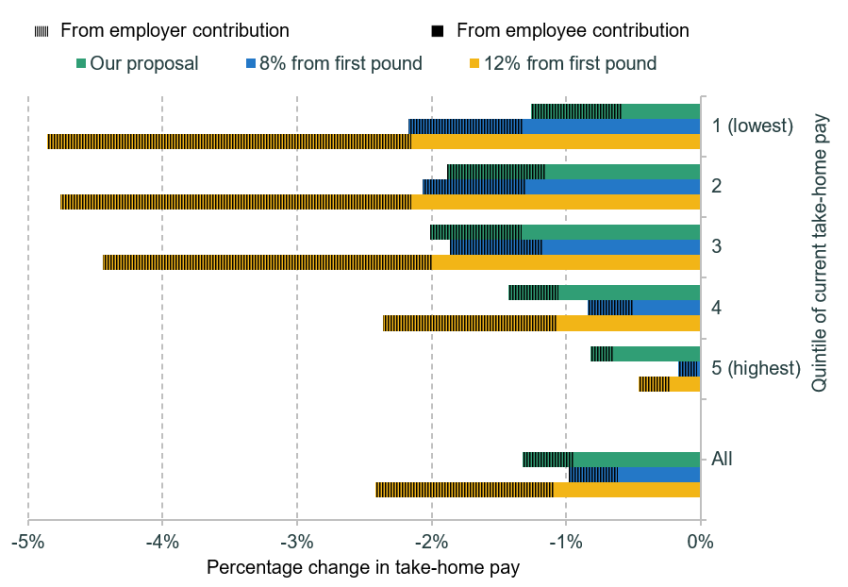

It is also worth emphasising why we are not recommending some reforms that are commonly suggested by others. One such suggestion is to reduce the lower limit for qualifying earnings to zero, so that contributions are calculated from the ‘first pound’. Indeed, enabling legislation for this change to be made in England, Scotland and Wales was passed in 2023.12 However, this change would lead to the highest percentage increase in contributions for those earning just over £10,000 per year (as discussed in Cribb, Karjalainen and O’Brien (2024)), and many in this group might struggle to afford the associated reduction in take-home pay. Others have suggested increasing the minimum total contribution rate to 12% (of which 6% would come from the employer) alongside reducing the lower limit for qualifying earnings to zero as a way of increasing pension saving (e.g. Pensions and Lifetime Savings Association, 2022a). This would risk an even larger fall in take-home pay for lower earners. Improving pension outcomes for lower earners is important, but it is crucial that this is done in a way that minimises hardship during working life. And neither extending to the first pound, nor increasing the minimum contribution rate to 12%, would do anything to help the fifth of employees who are not a member of their workplace pension. In contrast, it might lead to more employees opting out of pension saving altogether if they cannot afford the higher employee contribution. We model the effects of our proposals relative to these other suggestions in Chapter 3 and show that, while the reforms have similar distributional effects on retirement incomes – although the magnitude of the increase is larger for the move to a 12% contribution rate – the reductions in take-home pay arising from our proposals are much less focused on lower earners.

Our proposals take as given that most private sector employees currently save into defined contribution pension arrangements. Some stakeholders are enthusiastic about the potential for collective defined contribution pensions (‘CDC’), with proponents highlighting they can potentially generate higher returns for savers and help manage longevity risk. But there is a great degree of uncertainty around the development of these schemes, such as if (or when) these products will be available at a large scale, whether the products would be more likely to be whole-life or ‘decumulation-only’, and how well they can actually provide insurance against investment and inflation risk (in addition to longevity risk) across successive generations (while retaining pension freedoms). We see the prospect of CDC becoming more widely available as ‘complementary’ to our other proposals, but it seems likely that defined contribution schemes will remain the predominant form of private pension provision in the coming years.

Other measures have also been suggested to mitigate or balance concerns about affordability and increased retirement savings. In particular, Nest Insight has run extensive trials on ‘sidecar’ models of saving where some of the automatic workplace savings initially go to liquid savings products rather than being locked away in a pension for retirement. These have shown promising results in terms of effects on building up financial resilience (e.g. Nest Insight, 2023). While not a core part of this report, in our previous work (Cribb, Emmerson, Johnson, O’Brien and Sturrock, 2024) we suggested that the government should consider these types of hybrid saving options especially if automatic enrolment is amended so that employee contributions are calculated from the first pound of earnings.

How to help self-employed workers not saving enough