Downloads

Download report PDF

PDF | 2.45 MB

Executive summary

This report takes a fresh look at the prospects for the future of retirement incomes for employees in the UK. Since the Pensions Commission reported around 20 years ago, much has changed in the economic and pensions policy environment. While the introduction of automatic enrolment has been in many respects a great policy success – and the level and coverage of the flat-rate component of the state pension have increased markedly – lower-than-expected growth in earnings and depressed returns to saving make the private saving landscape more challenging.

This report undertakes new modelling for those in paid employment today, simulating their future earnings until retirement and assuming that they continue to place the same share of those earnings in a pension as currently and that the new state pension will rise in line with earnings. We assess the outlook for whether people will reach the replacement rate targets set out by the Pensions Commission and whether they will reach the retirement living standards set out by the Pensions and Lifetime Savings Association (PLSA). We also show results from an economic model of when and how much people should save at different points in life.

Key findings

1. There have been several changes to the economic environment since the Pensions Commission reported two decades ago, some making it harder for employees to reach an adequate retirement income and others making it easier. On the one hand, since 2004, the level, coverage and indexation of the flat-rate component of the state pension have become considerably more generous. We take a stylised individual spending a lifetime (from age 22 to state pension age) on close to full-time median earnings (£38,500) and calculate the amount they would have to save privately each year to hit a retirement income gross replacement rate of 67%, which would give them a gross retirement income of around £25,800. We estimate that changes to the state pension would – all else equal – reduce their required saving by roughly one-third from around 9% to around 6% of their earnings. This assumes the state pension is earnings indexed; were it to remain ‘triple locked’, the required private saving rate would fall further.

2. However, other changes to the economic environment – namely, longer life expectancy at older ages, lower earnings growth and lower returns to saving – have more than offset the effects of a more generous flat-rate state pension. Accounting for these changes as well as the more generous state pension, we find that for someone spending their lifetime as a low, middle or high earner, the saving rate required to hit the targets that the Pensions Commission set out is approximately 1–3% of earnings higher than was expected when it concluded its study.

3. In aggregate, private sector employers are contributing a similar amount (as a fraction of total earnings) to their employees’ private pensions in 2021 to what they were in 2005 – approximately 6% of total pay. There have been increases in pension contributions for smaller employers (fewer than 100 employees) over this period (from 2.9% of pay to 3.5%), while among larger employers (at least 1,000 employees) overall pension contributions are almost unchanged at around 8% of pay. We cannot make this exact comparison going further back due to a lack of consistent data before 2005; however, we can be sure that, as a fraction of earnings or GDP, employer pension contributions are around their highest levels since the mid 2000s and are probably higher than they were in the 1990s. Having said that, deficit reduction payments from employers to defined benefit pension funds have fallen in recent years.

4. Projecting forward the savings and retirement incomes of current workers, our baseline model finds that over half (57%) of current private sector employees saving in a defined contribution pension are projected to have an ‘adequate’ replacement rate (as defined by the Pensions Commission) on current trends. This means that a significant minority – around four in ten of this group – appear to be ‘undersaving for retirement’ on this metric. The same modelling implies that over two-thirds (68%) of private sector employees are projected to have an income that would allow them to meet a ‘minimum’ retirement living standard (expenditure of £14,400 per year in today’s terms, assumed to rise with the growth in average earnings).

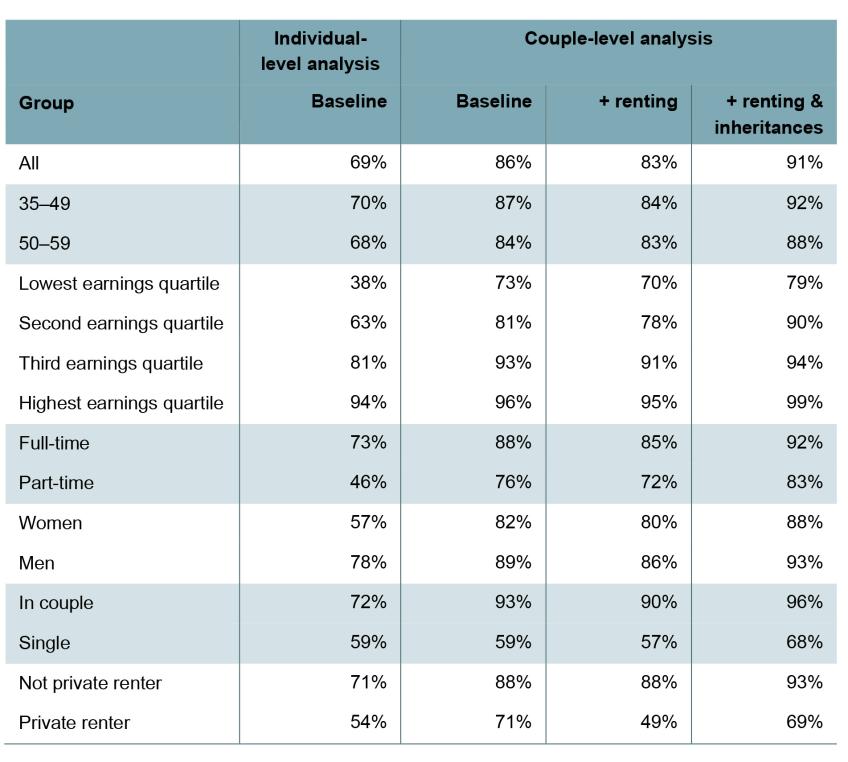

5. By their nature, these estimates are very sensitive to some of the assumptions made. Our downside scenario, where the return achieved on pension saving is lower by 1 percentage point, implies that over half of individuals are saving too little to hit a target replacement rate and that around 40% would not hit the ‘minimum’ living standard. On the other hand, a 1 percentage point higher rate of return (meaning a return comparable to that anticipated by the Pensions Commission) and a 10% higher state pension, plus the inclusion of predicted inheritances as a source of future retirement resource, reduces projected rates of undersaving to just under two in ten, with almost 90% expected to achieve at least a ‘minimum’ income.

6. Certain groups appear more likely to be undersaving than others. For example, compared with the Pensions Commission replacement rate measure of retirement income adequacy, those on higher levels of earnings are more likely to be undersaving than lower earners. While 86% of those in the bottom quarter of earners when in their 50s are projected to hit their target replacement rate, this is so for just 40% of those in the top quarter of earners. This is because the flat-rate nature of the state pension means it provides more income replacement (in percentage terms) for lower earners.

7. However, lower earners are less likely to reach a ‘minimum’ living standard, reflecting the fact that they have lower lifetime incomes and therefore typically save smaller amounts for their retirement. The combination of lower earners being more likely to reach target replacement rates, but less likely to hit ‘minimum’ retirement incomes implies that the key issue facing many of these employees is low lifetime incomes, rather than not transferring enough of their working-age income to provide for their retirement. Indeed, many working families currently have incomes below the equivalent of the PLSA ‘minimum’ living standards: 32% of working couples and 44% of working single people have an income below these ‘minimum’ retirement income targets. In this context – where significant shares of working-age households do not appear to be enjoying a ‘minimum’ standard of living – boosting their retirement income without risking eroding their current low living standards further would require redistribution of income towards them, either via higher state pensions, more generous total compensation from their employment, or more generous treatment by the tax and benefit system. In addition, measures to help lower earners remain in paid work up to (or at least up to) state pension age would also increase retirement incomes without reducing take-home pay during working life.

8. Women are slightly more likely to meet replacement rate measures of adequacy but less likely to meet ‘minimum’ income standard measures. This is because they typically have lower levels of earnings than men. Again, this suggests that appropriate policies to reduce the gender pension gap would require redistribution of income towards women rather than any move to encourage women to save more of their own earnings than men.

9. Within the group of individuals aged 35–59, if we assume that retirement resources will be shared within current couples, then the overall outlook for adequacy is improved. Those on higher incomes are more likely to be on track to hit a replacement rate defined at the couple level instead of the individual level. A much higher proportion of women (82% compared with 57%) are on track to have at least a ‘minimum’ retirement income, if their retirement resources are equally shared with their partner. People who live on their own in retirement cannot benefit from this resource sharing, and are projected to be much less likely to have a ‘minimum’ retirement income than those living in couples (59% compared with 93%).

10. When measuring incomes after adjusting for housing costs, those who will be private renters in retirement are much more likely to be undersaving than those who are not privately renting. Just under half of private renters are on track to meet the Pensions Commission replacement rate target compared with around two-thirds of those not privately renting. Almost 90% of those not privately renting are projected to hit a ‘minimum’ retirement living standard, compared with just under half of private renters.

11. Results from an economic ‘life-cycle’ model of when during working life people should be saving indicate that there are good reasons for many people to save a greater proportion of their earnings for retirement in the later stages of their working life when their earnings are typically higher and their outgoings – such as mortgage payments, childcare costs and student loan repayments – are lower.

1. Introduction

The recommendations of the Pensions Commission (2004, 2005) led to the introduction of automatic enrolment into workplace pensions and a dramatic shift in the private pension saving landscape in the UK. Millions more private sector employees have workplace pensions than would otherwise have been the case (Cribb and Emmerson, 2020). Alongside, the new state pension provides a much higher basic retirement income than was expected in 2004 and, combined with means-tested benefit entitlement, is enough to keep most types of pensioner households out of standard measures of relative income poverty in retirement (Cribb et al., 2023a).

While there has clearly been progress in improving the outlook for future retirement living standards, there is a consensus that many are still not on track to have ‘enough’ or ‘adequate’ income in retirement (e.g. Pike, 2022; Pensions and Lifetime Savings Association, 2022; Department for Work and Pensions, 2023). The essential reasoning here is that automatic enrolment default rates are set at a level that will still leave many with insufficient retirement savings. The second report of the Pensions Commission (2005) described a system in which typical contributions to workplace pensions of 8% of earnings above the ‘Primary Threshold’ (then £4,888) provided a ‘base load’ of private saving, with the expectation that many would then save more to secure an adequate retirement income. Since then, changes in the economic outlook, in particular terrible average growth in earnings and the decline in expected returns to pension savings, have potentially made the environment for savers more challenging. In addition, while automatic enrolment has boosted pension participation, there remains a group of around one in ten employees who opt out of saving in a private pension, and approximately another one in ten employees do not participate as they are not automatically enrolled due to their age or earnings. The result of these considerations is that policymakers, the pensions industry and stakeholders focused on future retirement living standards are broadly of the view that further action to boost private saving for retirement is required.

Automatic enrolment and the outlook for private pensions policy

Currently, employees aged between 22 and state pension age who earn at least £10,000 per year must be automatically enrolled into a workplace pension plan.1 Total default contributions into the pension must be at least 8% of total ‘qualifying earnings’, with at least 3 of the 8 percentage points contributed by the employer. ‘Qualifying earnings’ are gross earnings between £6,240 and £50,270; these lower and upper limits on qualifying earnings tend to increase each year. Individuals can choose to leave their workplace pension plan, in which case there is no obligation for their employer to contribute anything to their pension. If someone earns more than £6,240 but less than £10,000 per year and is aged between 16 and 74, they can ask to join their employer’s pension plan and receive minimum employer contributions.

There are several directions for possible reform of automatic enrolment that have seen widespread discussion. Legislation was passed last year that gives the government the power to reduce (for those in England, Scotland and Wales) the age at which employees must be automatically enrolled and scrap the lower limit for qualifying earnings – i.e. have contributions paid from the ‘first pound’ – following the recommendation of these changes by the 2017 Automatic Enrolment Review (Department for Work and Pensions, 2017). The previous Conservative government committed to consulting on the move to first pound in the ‘mid-to-later part of this decade’, but it is not yet clear if and when the current government intends to implement this change.

One of the major questions for automatic enrolment policy is whether default contribution rates should rise, for whom and by how much, and how any rise should be split between employer and employee contributions. A number of industry bodies and commentators have called for an increase in default contributions, with a proposal of 12% minimum contributions, with at least 6% coming from employers, often cited (e.g. Association of British Insurers, 2022; Standard Life, 2023). The basis for this proposal is the assessment that, on current trends, many individuals are on track not to meet adequacy benchmarks and that increased contributions are an obvious way to avoid undesirable shortfalls in retirement incomes (e.g. Pensions and Lifetime Savings Association, 2022; WPI Economics, 2024).

Outside of the framework of automatic enrolment, a recent direction of travel for private pension saving policy has revolved around attempts to increase returns to pension savings and encouraging a greater investment of UK pension savings in ‘high-growth’ UK companies. Former Chancellor Jeremy Hunt’s Mansion House speech of July 20232 set out ambitions to consolidate poor-performing defined contribution (DC) plans and encourage greater investment of pension assets into unlisted UK companies. The speech came alongside a commitment by some large DC pension providers to allocate ‘at least 5% of their default funds to unlisted equities by 2030’. The government thereafter set out an approach to consolidating small DC pots, a consultation on the ‘pot for life’ and a consultation on broadening collective defined contribution pension provision. Labour has indicated an intention to continue with this broad direction of travel both in its 2024 election manifesto and in the subsequent King’s Speech, and although a review of policy in this space is promised, as yet detail is limited.

This report

In this report and the accompanying report on policy recommendations (Cribb et al., 2024a), we focus on the outlook for the adequacy of employees’ retirement incomes and changes to automatic enrolment. We do not here consider reforms that we broadly define as aimed at changing investments, costs and returns (including ‘pot for life’ and collective defined contribution pensions) but will return to consider these later in the Pensions Review. A separate report also published in September 2024 considers the outlook for self-employed workers and potential policy solutions to trends in their saving that are of concern (Cribb et al., 2024b).

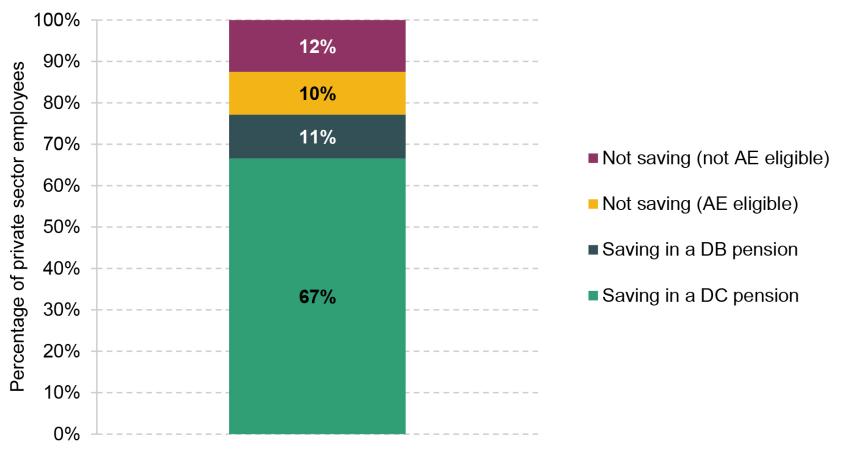

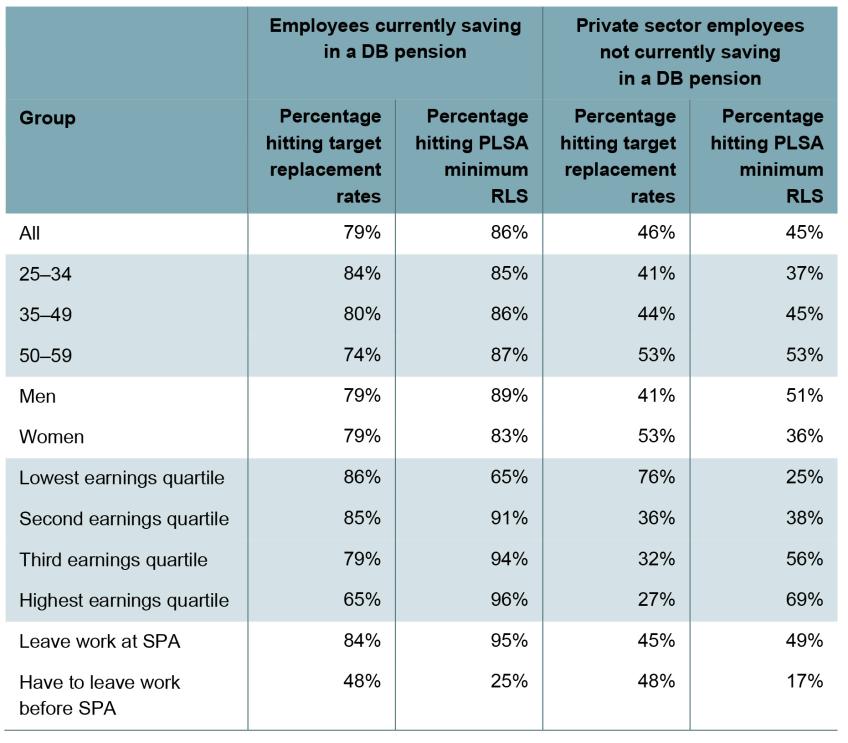

We mainly focus on the outlook for private sector employees who are saving into a DC pension, corresponding to around 16.5 million people. As shown in Figure 1.1, this corresponds to 67% of private sector employees, or half of all employees. It is therefore important to keep in mind who is not in this sample. On the one hand, we do not tend to focus on private sector employees saving in a defined benefit (DB) pension (or public sector employees, who also tend to save in DB pensions). These pensions tend to be more generous and, indeed, Cribb et al. (2024b) highlight that employees saving into a DB pension tend to have significantly higher levels of overall wealth than other employees. We therefore do not focus on these employees as there are likely fewer concerns about their accumulation of retirement savings, although we do show some of our headline results for this group.

Figure 1.1. Distribution of private sector employees by workplace pension saving status

Note: AE = automatic enrolment.

Source: Authors’ calculations using the Annual Survey of Hours and Earnings, 2021.

The other significant group that is not typically in the sample we analyse is employees who are not currently saving in a pension. This is principally because of difficulties with modelling their future saving behaviour. However, given they are not currently saving in a pension, there may well be worries about the levels of their retirement income. Almost a quarter of private sector employees are currently not saving in a pension, split almost equally between those not eligible for automatic enrolment and those who have chosen to opt out of pension saving. Our policy suggestions in Cribb et al. (2024a) include some measures that would boost the retirement saving of this group.

Throughout this report, and the accompanying report on the resulting policy options and our suggestions, in addition to empirical analysis we draw on quotes from individuals interviewed by Ignition House as part of our public engagement work on private pension accumulation conducted as part of the Pensions Review.

The remainder of this report proceeds as follows. Chapter 2 provides a short introduction to the concept of retirement income adequacy and the potential measures of it. Chapter 3 provides an update on some of the influential modelling undertaken by the Pensions Commission on the level of private saving needed for adequate pension incomes. Chapter 4 conducts new modelling using data on individuals’ assets and current saving behaviour to project retirement incomes for current private sector employees, including testing for sensitivity to incorporating partners, housing and inheritances. Chapter 5 provides some additional results from an economic life-cycle model, updating work published in Crawford, O’Brien and Sturrock (2021). A short conclusion is provided in Chapter 6.

2. How to measure adequacy

This report estimates the adequacy of the income that today’s employees will have when they retire. Before we present projections for future retirement incomes, we first consider how we should define and measure income adequacy.

There are different ways of conceiving of retirement income adequacy. These lead to different benchmarks against which to compare retirement incomes and therefore lead to different conclusions about current and future levels of adequacy. This makes it crucial to consider carefully the assumptions behind each concept and benchmark.

There are two broad approaches to conceptualising adequacy. One compares an income with some absolute standard such as a poverty line or particular ‘living standard’. A second approach considers how an individual’s retirement income relates to the income they had during their working life. Both approaches are useful in different ways and so we use them both in our modelling.3

2.1 Poverty line or ‘living standard’ approach

This approach identifies individuals as having adequate resources if their income exceeds a level deemed necessary to purchase a certain standard of living. Previously, work has focused on whether people reach a poverty line (e.g. Crawford and O’Dea, 2012). More recently, with pensioner poverty at much lower levels, and a more comprehensive foundation level of income provided by the new state pension, pensioner poverty in the future – at least for most singles, and couples where both members are above state pension age – is likely to be very low. Cribb et al. (2023a) show that essentially all groups receiving the new state pension in full, but no other income, will be above the poverty line, with the exception of some single people living in the private rented sector in some parts of England.

Perhaps as a result of this, interest has grown in more ambitious metrics that compare individuals’ retirement incomes against a higher fixed income line, most notably the ‘retirement living standards’ benchmarks produced by Padley (2024), based on the Minimum Income Standard benchmark (Padley and Stone, 2023), for the Pensions and Lifetime Savings Association (2024). There are three PLSA retirement living standards levels – minimum, moderate and comfortable – and for each level separate figures are produced for single households and for couple households. The idea of these figures is to give an annual amount of expenditure that achieves a living standard reflective of those terms. Crucially, these expenditure amounts assume no spending on housing costs, care costs or tax. That means that the pre-tax income required to reach those levels will be higher. A household with housing costs – whether mortgage repayments or rental payments – will require a higher income still to reach each benchmark, as will a household that wants to put aside resources to pay for care. Figures for couples are lower (on a per-person basis) because some items can be shared within a household, making it cheaper to achieve a certain standard of living. Separate figures are also produced for those living in London, where costs are expected to be higher.

Other living standard benchmarks exist, on top of poverty lines and the PLSA lines. In particular, the Living Pensions project (Finch and Pacitti, 2021; Cominetti and Odamtten, 2022; Broome, 2024) aims to calculate the size of the pension pot – and corresponding saving rates – needed to meet the Minimum Income Standard benchmark (Padley and Stone, 2023), taking into account both housing costs and income tax. To avoid proliferation of different benchmarks, in this project we focus on the PLSA levels (as well as the replacement rate methodology set out in Section 2.2).

The figures for each PLSA benchmark are produced by researchers in consultation with focus groups. The approach is ‘bottom-up’: the discussions with focus groups aimed to establish which sorts of goods people think are required to reach each of these three standards of living. The total expenditure number is then the cost of acquiring these. Updates in the standards over time reflect both changes in the costs of goods and services and changes in the expectations of retirees about what each standard requires. In 2024, the benchmarks were ‘rebased’ – i.e. established again from scratch – for the first time since their introduction in 2019.

Published in early 2024, the current minimum standard for a single individual is £14,400 per year. The moderate and comfortable standards are £31,300 and £43,100, respectively. The equivalent figures for couples are £22,400, £43,100 and £59,000.

As a definition of retirement income adequacy, these objective benchmarks are helpful in telling us how well off we would expect someone to be and which groups are on track to fall short of a certain standard of living. They are also relatively transparent and easy to interpret and may therefore be helpful for individuals looking to target a particular lifestyle in retirement. This is set out in the following quote from an individual in a focus group considering private pension accumulation undertaken as part of the Pensions Review:

‘I find the retirement living standards easier to understand as it is visual with less information and just the most important. It is easier to refer to and is not overwhelming.’

– Male, aged 45–54

However, living standards benchmarks may, alone, not be a good guide to which groups should be saving more. The reason for that is many households will not reach a given living standard in their working life. In that case, even if they look set to fail to reach a certain benchmark during retirement, it might not be in their best interest to respond by saving more, as it will impact their current standard of living.

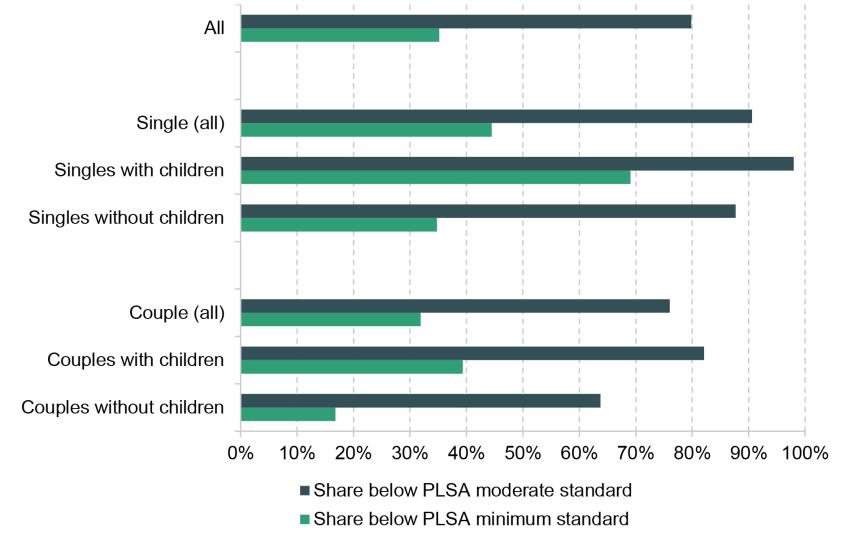

This consideration is relevant because the current PLSA retirement living standards are set at rates that many working families do not reach. This is particularly the case for the moderate and comfortable levels, but Figure 2.1 shows that once you take into account people’s housing costs (mortgage repayments or rents), 35% of working households do not reach even the ‘minimum’ standard and 80% do not reach the moderate standard. Single people and those with children are particularly unlikely to meet these levels. In addition, accounting for other costs that working people face but retired people do not, such as childcare costs or commuting costs, would further push up the fraction of working-age people who do not meet these metrics.

Figure 2.1. Share of working households with income net of housing costs below the minimum and moderate PLSA retirement living standards

Note: Single/couple households with children have their income equivalised to the level of a single/couple household without children before being compared with the PLSA standards. Equivalisation uses the OECD modified scale. Working-age households with someone in paid work are included.

Source: Authors’ calculations using the Family Resources Survey, 2022–23.

For those households not on track to reach certain living standards benchmarks in retirement but that also have lower living standards in working life than in retirement, increasing private saving may not be the appropriate response. It is still important to measure progress against these benchmarks because this may indicate where other forms of support – most obviously, greater redistribution through either a higher state pension or a more extensive means-tested pensioner benefit system – would be the appropriate response for policymakers with certain distributional preferences. Because the moderate and comfortable living standards are not reached by the vast majority of working-age households, we focus in this report on performance against the minimum benchmark.

One important consideration when measuring projected future retirement incomes against these benchmarks is how they should be assumed to increase over time. Today’s savers presumably should aim to achieve what will be deemed an ‘adequate’ retirement income at the point when they retire, not what was deemed to be adequate sometime in the past. One option would be to increase the PLSA benchmarks in line with inflation. This would embody an assumption that the same basket of goods would be deemed sufficient to meet a minimum/moderate/comfortable living standard in the future. In reality, the basket of goods will also likely change as expectations for minimum living standards rise over time. We assume that these expectations rise in line with living standards in the economy at large, and therefore assume that the PLSA benchmarks rise in line with average earnings over time.

2.2 Replacement rate approach

The replacement rate approach considers retirement income adequate if it maintains a certain proportion of the individual’s pre-retirement income, thus avoiding significant drops in living standards at the point of retirement. This concept is grounded in the idea that people would want to use private saving into pensions to smooth their standard of living over their lifetime. It might be natural to expect that smoothing living standards would mean having the same income in retirement as in working life. However, there are several reasons to expect that a retirement income lower than working-life income can maintain the same standard of living.

First, the same level of expenditure may achieve a higher standard of living in retirement than in working life. Expenses associated with employment, such as commuting and work attire, typically decline or cease entirely at retirement. Housing costs for those buying a home with a mortgage may similarly decline with age. With more free time, retirees might engage more in cost-saving activities such as cooking at home instead of eating out, or shopping around for better prices (Aguiar and Hurst, 2005). That said, some costs – most notably, healthcare and social care costs – tend to rise in retirement, potentially offsetting these other factors.

Second, a given level of expenditure can be achieved with a lower gross income in retirement. One reason for this is that pensioners face a more favourable tax system than those of working age. In particular, pensioners do not pay National Insurance contributions on any of their income, while up to a quarter of any private pension withdrawals can be taken free of income tax. In addition, saving for retirement will end at retirement, meaning that a portion of income is freed up for expenditure.

In principle, we could use empirical evidence to work out what level of income replacement provides a smooth standard of living from working life into retirement. Empirical studies of replacement rates of income in the UK, such as Banks, Blundell and Tanner (1998), find average net replacement rates in the UK around 80%, with higher rates for lower pre-retirement incomes. However, using such studies to set benchmarks requires an assumption that retirees’ incomes are just adequate, which may not always be true. Surveys that seek to elicit desired replacement rates directly, such as Mayhew (2002), reveal varied perceptions. Many on lower incomes desire higher replacement rates, while those on higher incomes often accept lower rates. Binswanger and Schunk (2012) conducted similar studies in the US and the Netherlands, finding that perceived adequate replacement rates decline with higher income levels.

When operationalising replacement rates, one needs to decide over which period to measure retirement and working-life incomes. The perspective of smoothing living standards would suggest looking over the whole of retirement and working life. Often, empirical analysis is restricted by the time frame of datasets and compares the first year of retirement income with some average income over a small number of pre-retirement years. We compare predicted income at retirement with projected pre-retirement incomes, measured at ages 50–59.

Combining theoretical arguments and empirical evidence, there is no single clear definition of an adequate replacement rate. The Pensions Commission (2004) provided one set of benchmark replacement rates. The rates are expressed in terms of gross retirement income as a percentage of pre-retirement gross income and decrease with higher pre-retirement incomes. These are reasonably well established and accepted as useful metrics within the realms of policy and private pensions analysis. We therefore uprate the Pensions Commission benchmarks to today according to earnings growth since 2004, as shown in Table 2.1.

Table 2.1. Target replacement rates for different levels of pre-retirement average earnings

| Target replacement rate | Pre-retirement gross earnings range in 2004 | Pre-retirement gross earnings range in 2023 |

| 80% | £0 to £9,499 | £0 to £16,999 |

| 70% | £9,500 to £17,499 | £17,000 to £31,499 |

| 67% | £17,500 to £24,999 | £31,500 to £44,999 |

| 60% | £25,000 to £49,999 | £45,000 to £89,999 |

| 50% | £50,000 and above | £90,000 and above |

Note: We uprate the pre-retirement gross earnings range from Pensions Commission (2004) based on the change in average weekly earnings for total pay between April 2004 and April 2023 (and then round the resulting earnings ranges). The earnings ranges are then uprated in line with average earnings growth (assumed to be 1.8% per year) for people retiring in future years.

Source: Figure 4.11 in Pensions Commission (2004) and ONS average weekly earnings series EARN01.

These replacement rate benchmarks have limitations and should be used cautiously. They are inevitably somewhat arbitrary. This is particularly the case for higher earners, where changes in the tax system and levels of saving should in principle imply changes in the replacement rates required to smooth living standards. Inevitably, these benchmarks cannot reflect the wide variety in individual circumstances that would be expected to lead to differences in the replacement rate required to smooth living standards. These benchmarks also do not give any indication of when in life any private saving should take place. For these reasons, it can also be useful to look at the outputs from a model that explicitly attempts to calculate what level and timing of saving will smooth living standards and therefore maximise welfare over an individual’s whole lifetime.

The replacement rate benchmarks can be seen as helpful in guiding saving decisions based on the idea of smoothing living standards. As expressed in the quote below, they can be more difficult for some people to understand, given that they are expressed as a percentage of working-life income and do not have an immediate interpretation in terms of a standard of living. Someone reaching adequacy on the replacement rate benchmark can have income that is deemed inadequate by one or more of the living standards benchmarks. These are all reasons for viewing the two types of measure together.

‘From the moment I looked at Replacement Rates my eyes glazed over. Sorry, my issue here! But I am sure lots of other people would feel the same. I like to have financial information presented to me in the simplest of forms, which is done on the Living Standards. I know it’s broad and approximate but I find this so much easier to digest than trying to interpret percentages.’

– Male, aged 45–54

3. What has changed since the Pensions Commission?

When the Pensions Commission reported in the mid 2000s, the landscape for retirement savers was very different from today’s. We therefore update some analysis first conducted for the Pensions Commission to illustrate the implications of the changed saving environment for how much today’s employees might need to save for retirement compared with 20 years ago. We also discuss changes in employer contributions to pensions over time.

3.1 Changes in the landscape for savers

In 2004, a full basic state pension was £79.60 per week, at that point worth 19% of median full-time earnings, equivalent to £139 per week in today’s prices, and it was formally indexed to growth in prices as measured by the Retail Prices Index (RPI). There have been major changes to the outlook for the state pension for today’s savers since 2004, including the introduction of the new state pension for those reaching state pension age from 2016 and the set of reforms implemented from April 2010 that reduced the number of qualifying years needed for a full state pension and treated years spent with certain formal caring responsibilities more favourably. Importantly, the indexation of the state pension is much more generous too, with flat-rate state pensions being indexed in line with the ‘triple lock’ formula since 2011.

The new state pension is paid at a rate depending on the number of years of eligible activities and is much more generous to those with lower levels of earnings than the system it replaced. A full new state pension is now worth £221.20 a week, 59% more in real terms than the basic state pension in 2004 and, at 30% of average full-time earnings, 11% of average earnings more than it was 20 years ago. The DWP forecasts that by the mid 2030s, over 80% of those reaching state pension age will receive a full new state pension (Department for Work and Pensions, 2013). These state pensions will, though, begin to be paid from a later age than may have been expected in 2004, given actual and legislated future increases in the state pension age since then.

Happily, longevity at older ages has improved significantly since 2004. At the time of the Pensions Commission in 2004, a woman aged 65 was expected to live for a further 20.2 years on average. That compares with 21.2 years now expected for a woman aged 65 in 2024. For men, the rise is from 17.4 to 18.6 years. While improvements in longevity have slowed and even showed signs of going into reverse for some groups in recent years (Office for National Statistics, 2024), and there is always significant uncertainty about the future evolution of life expectancy, a central expectation is that people of working age today will tend to live to older ages than was expected 20 years ago for the generation of working-age people then. Longer lives have come alongside more years spent in paid work. At least up until the eve of the pandemic, employment rates for both men and women in their 50s and 60s were rising steadily (Cribb, 2023), with the big rise in the female state pension age one significant factor behind this. Expectations for the number of years spent in retirement for someone retiring at the state pension age have risen from 17.4 to 17.6 for men (despite the one-year increases in the male state pension age from 65 to 66). Given the six-year increase in the state pension age for women, the expected number of years after state pension age for women has fallen from 25.4 to 20.1.

The years leading up to 2004 saw much higher rates of growth in earnings than have been seen since and are now expected in the future. Over the 20 years up until 2004, average annual earnings for someone of working age grew at an annualised rate of 2.8%. Since then, average earnings have barely grown. While some of the poor performance of earnings over the period since 2004 is attributable to economic shocks – most notably, the financial crisis and its aftermath – economists, including the Office for Budget Responsibility (OBR), have consistently downgraded forecasts for future productivity growth, and most long-term expectations are that productivity growth going forward will be lower than over the latter decades of the 20th century.

The final, and perhaps most important, change since 2004 – albeit one closely related to the poor productivity performance mentioned above – is the change in the outlook for returns to saving. Over the 20 years up to 2004, total real returns to UK equities averaged just under 8% per year.4 In the period from 2004 to 2020, they have averaged 4%. The real returns to 15-year government bonds have fallen from a little under 6% per year over the 20 years up to 2004 to 1.5% over the period up to 2020. While UK pension savers do not only save into UK equities and bonds, this illustrates the scale of the changes seen recently. The outlook for returns going forward is of course uncertain. Returns to government bonds have risen substantially in nominal terms in the period since 2022, but the medium-term outlook for the real rate of return to safe assets has changed less. Expectations of financial markets are that real gilt rates will be between 0% and 2% over the coming decades.5

3.2 The implications for required saving rates

We illustrate the importance of this changed saving landscape by estimating the saving rate required to hit a target replacement rate for an individual with certain illustrative earnings levels. These illustrative earnings levels are based on the Pensions Commission analysis and updated to today’s terms.

The calculations are made as follows. We assume that earnings grow at the same rate in each year, and that people work in all years from age 22 until state pension age. We define the individual’s pre-retirement income as their earnings in the year before they reach state pension age, and then multiply this by their target replacement rate (see Table 2.1) to get their target retirement income. We model income at state pension age from state benefits, either following the methodology in Pensions Commission (2004) or, for our updated 2024 analysis, assuming that everyone gets the full new state pension (and no other state benefits). The difference between the individual’s target retirement income and their retirement income from state benefits gives us their target ‘private’ retirement income, and we assume they achieve this by buying an inflation-linked annuity, following the methodology in Pensions Commission (2004). We then calculate the saving rate the individual would need in order to have enough wealth to purchase such an annuity upon reaching state pension age, assuming that the individual saves the same amount in each year of working life.

Key assumptions that feed into this modelling are summarised in Table 3.1. Our earnings growth assumption is line with the OBR’s long-run expected economy-wide earnings growth.6 The assumption on rates of return during accumulation mainly comes from Financial Conduct Authority (2017), although we update the expected rate of return on bonds underlying this calculation in line with current UK gilt curves. To obtain the expected rate of return for annuity providers, we subtract 0.7 percentage points from the return on government bonds (to account for fees). We compare our assumptions with the equivalent ones made by the Pensions Commission in its 2004 analysis.

Table 3.1. Comparison of earnings growth, rate of return, and state pension indexation assumptions

| Pensions Review, 2024 | Pensions Commission, 2004 | |

| Real earnings growth | 1.8% | 2.5% |

| Real rate of return during accumulation | 3.3% | 4.8% |

| Real rate of return for annuity providers | 1.8% | 2.3% |

| Indexation of the state pension | Earnings growth | Inflation |

Note: See Section A.13 for details on our 2024 assumptions. The Pensions Commission assumed an average earnings growth rate of 1.5% above RPI and rates of return of 3.8% above RPI during accumulation and 1.3% above RPI for annuity providers. We assume a wedge of 1 percentage point between the Retail Prices Index and Consumer Prices Index and an average (CPI) inflation rate of 2% per year7 to obtain real rates for the Pensions Commission numbers.

Source: Pensions Commission, 2004.

The results of the analysis are shown in Table 3.2. We show projections for the required saving rates using the Pensions Commission’s assumptions for someone starting their working career at age 22.8 We then show the impact of updating the state pension environment, life expectancy, and rates of return and earnings growth to today’s assumptions. As we work across the columns, the changes are cumulative so that the final column shows the saving rates based on our 2024 assumptions. We show projections for low, middle and high earners (as defined below), all of which are the same levels as shown in Pensions Commission analysis, although uprated in line with average earnings growth to today.

Table 3.2. Required contribution rates to an occupational pension to reach target replacement rates, by earnings, 2004 and 2023

| Earnings (2023 terms) | 2004 environment | Updating state pension | + updating life expectancy | + updating earnings growth and returns: 2023 environment |

| £16,000 | 0% | 2.0% | 2.5% | 3.3% |

| £38,500 | 9.2% | 6.5% | 7.9% | 10.3% |

| £90,000 | 8.5% | 6.4% | 7.7% | 10.0% |

Note: Authors’ calculations updating Pensions Commission (2004) analysis for an individual aged 22 today and working until state pension age. The leftmost column shows their earnings at age 22, which are assumed to grow at a constant rate each year. The individual is assumed to save a constant fraction of their earnings in each year in order to reach their target replacement rate (80% for the lower earner, 67% for the middle earner and 50% for the higher earner). The table shows the saving rate they need to achieve these replacement rates under different economic environments.

Under the 2004 assumptions, the low earner (£16,000 in today’s terms) actually did not need to do any private saving for retirement to meet the target replacement rate benchmark: income from the basic state pension, SERPS (State Earnings-Related Pension Scheme) and pension credit (guarantee credit) were sufficient for them to replace 80% of their pre-retirement earnings.9 Moving to the new state pension system, all else equal, means an increase in the required saving rate for the low earner, due to the loss in SERPS income. In contrast, the middle (£38,500 in today’s terms) and high (£90,000) earners have a required saving rate of around 9% under 2004 assumptions. As a proportion of their pre-retirement income, they receive significantly less income from SERPS and means-tested benefits in retirement than the lower earner. Moving to the new state pension system decreases the required saving rate to around 6.5% as they now receive the new state pension, which we assume is indexed to average earnings growth, meaning a much more generous state pension in the long run than an RPI-indexed state pension as assumed by the Pensions Commission.

Increases in life expectancy push up required saving rates by slightly over 1% of earnings for the middle and higher earners as, essentially, all else equal, longer retirements mean more private saving is needed. Longer life expectancy leads to a much smaller increase in the required saving rate of the lower earner, for whom private saving is a much lower proportion of their retirement income. The lower rates of return and lower growth in earnings lead to an even larger increase in required saving rates, of almost 2.5% of earnings, for the middle and higher earners. The increase is again more muted for the lower earner, who relies much less on private income in retirement. Overall, the increase in required saving rates is larger for the lower earner than for the middle and higher earners, although even today they only have to save a very modest proportion of their earnings.

There is of course significant uncertainty around the future evolution of earnings growth, rates of return and the level of the state pension. Table 3.3 illustrates how our results change when we alter the key assumptions. The rate of return matters for the required saving rates. A 1 percentage point (ppt) higher return and 1ppt higher rate of earnings growth reduces the required saving rate by around 1% of earnings for middle and higher earners. This effect is primarily driven by the change in returns. Changes to the outlook for the state pension matter more for lower earners, as the state pension is a larger proportion of their retirement income. If we assume that the triple lock remains in place (meaning here that the state pension grows 0.58ppts faster than earnings in each year, as assumed by the Office for Budget Responsibility (2023)), this reduces the required saving rate for low and middle earners by around 3% and 2% of earnings, respectively.

Table 3.3. Effect of different assumptions on state pensions and rates of return on required contribution rates to an occupational pension to reach target replacement rates, by earnings

| Earnings | Baseline projection | Higher growth and returns | Lower growth and returns | 10% higher state pension | Triple lock state pension |

| £16,000 | 3.3% | 2.8% | 3.9% | 1.5% | 0% |

| £38,500 | 10.3% | 9.2% | 11.7% | 9.6% | 8.1% |

| £90,000 | 10.0% | 9.0% | 11.3% | 9.7% | 9.1% |

Note: Triple-lock ratchet assumed to be 0.58ppts above earnings indexation as assumed by OBR (2023). Higher/lower earnings growth and asset returns are 1ppt higher/lower compared with the baseline set out in Table 3.1.

Source: Authors’ calculations.

3.3 Changes over time in employer contributions to pensions

Another key trend in the UK pension saving landscape over the last few decades has been the declining prevalence of defined benefit pensions in the private sector. Among private sector employees not working in non-profit institutions, 7% were saving into a defined benefit pension in 2021 (Office for National Statistics, 2022), compared with around 30% in the early 1990s and 35% in the early 1980s (Pensions Commission, 2004). This is important given that employer contributions to defined benefit pensions tend to be substantially higher than contributions to defined contribution pensions.10

Reliable data on employer contributions to pensions in the Annual Survey of Hours and Earnings only go back to 2005, when 24% of all private sector employees were saving in a defined benefit pension. Figure 3.1 shows the aggregate employer pension contribution rate between 2005 and 2021 for private sector employees, calculated as total employer contributions to pensions (excluding one-off payments such as deficit reduction contributions which we discuss below) divided by total gross earnings. Overall, total employer contributions to pensions fell from 5.9% of total earnings in 2005 to 5.1% in the mid 2010s, before rising to 6.0% in 2021 (the latest year for which we have data). This is mainly driven by the fact that many more employees are saving in a workplace pension and receiving an employer contribution now than 20 years ago (though increases in minimum contributions in 2018 and 2019 are likely to have driven some of the rise in the late 2010s).

Figure 3.1. Employer pension contributions to private sector employees’ private pensions, as a percentage of total earnings, split by employer size

Note: Average employer contribution is calculated across all private sector employees, not restricting to those who participate in a workplace pension scheme.

Source: Authors’ calculations using the Annual Survey of Hours and Earnings, 2005 to 2021.

We do not have consistent data before 2005. But the first report of the Pensions Commission (2004) reported a slightly different metric (occupational pension contributions as a percentage of GDP) from the early 1970s to the early 2000s. This has the disadvantage of including public sector and excluding non-occupational DC plans (such as ‘Group Personal Pensions’).11 The Pensions Commission analysis suggests that employer pension contributions rose by about 1% of GDP from the early 1970s to the early 1980s, reaching 2.5% of GDP, before falling to 1% of GDP by the early 1990s, and with a nascent recovery in the late 1990s. It is hard to say exactly where private sector employer pension contributions are (compared with total employee earnings or GDP) relative to recent history given these data limitations – they are certainly at their highest level since the mid 2000s, are probably higher than in the early-to-mid 1990s, but may or may not be as high as they were in the early-to-mid 1980s.

It is also worth looking at how these changes have occurred since 2005, split by employer size. Larger employers were more likely to offer defined benefit pensions in the past, and typically had more of their employees participating in a pension than smaller employers, so we might have expected a drop in their aggregate employer pension contributions as they switched to defined contribution pensions. Despite this, we see that even for the set of employers with at least 1,000 employees, aggregate employer pension contributions were, at 8% of average earnings, around the same level as a fraction of pay in 2021 as they were in 2005. For small employers (fewer than 100 employees), the changes are more marked, particularly in recent years. In 2021, average employer contributions were 3.5% of pay, up from 2.9% in 2005.

These figures only refer to the employer pension contributions made for current employees – they explicitly exclude other employer ‘lump-sum’ contributions to pension schemes. For many years, many employers have had to make ‘deficit reduction contributions’ to their defined benefit pension schemes because of deficits in these schemes. With most private defined benefit schemes closed to new accrual (or at least to new members), these payments helped secure the retirement incomes of (mostly) current pensioners or other previous employees, rather than being a form of remuneration for current work of employees.

However, there have been large falls in these payments in recent years. Data from the Pension Protection Fund (2024) show that the fraction of defined benefit schemes in deficit has fallen from around 60% in 2020 to below 10% in 2024 as nominal interest rates have risen, which has cut pension scheme liabilities by more than the fall in the value of their assets. Data from HM Revenue and Customs (2024) show that the tax relief applied to deficit reduction payments fell from £5.1 billion in 2020–21 to £2.8 billion in 2022–23 as interest rates rose.

There is some evidence on how the obligation to fill pension deficits affects firms and workers. Adrjan and Bell (2018) find that most of the burden has fallen on the firms themselves, although there was evidence of some incidence on employees’ wages (about 10% of the cost of deficit payments fed through into lower wages). If there is symmetry in the responses to the (broadly unexpected) decline in pension deficits over the last few years, then we would in general expect firms (and therefore shareholders) to be the key beneficiary from the reduction in pension deficits, but employees to benefit modestly too through slightly higher wages.

3.4 Summary

There have been substantial changes to the pension saving environment since 2004, including reforms to the state pension system, increases in life expectancy, and lower expected rates of return and earnings growth rates. The analysis in this chapter suggests that, in all, these changes likely mean that people would need to do slightly more saving for retirement than suggested in the Pensions Commission reports, by slightly over 1% of earnings for middle and higher earners. This is driven by increases in life expectancy and lower expected rates of return on saving. We also find that lower earners might need to do more private saving for retirement today than in the world as it was 20 years ago to hit target replacement rates; however, in both periods, required saving rates are very low as the state replaces a large proportion of pre-retirement earnings.

Importantly, there is a significant degree of uncertainty about future earnings growth, rates of return and the level of the state pension, and our assumptions on how much people need to save are relatively sensitive to assumptions about these parameters. Employers are contributing more (as a fraction of total earnings) to their employees’ private pensions in 2021 than in 2005. This is particularly the case for smaller employers (who in the past will have been less likely to offer relatively generous defined benefit pensions and more recently will have been more greatly affected by automatic enrolment), but is also the case amongst larger employers.

4. What is the outlook for adequacy on current trends?

As discussed in the previous chapter, changes in the saving landscape – in particular, a lower expected rate of return on pension saving and higher life expectancy – mean that people will generally have to save more to hit their target replacement rates than was the case 20 years ago. Of course, there have also been large changes in how much employees are saving for their pension since the early 2000s, due to, for example, automatic enrolment.

In this chapter, we therefore take stock of the pension saving position of current private sector employees. As explained in Chapter 1, we mostly focus on our main sample of private sector employees, aged 25–59, currently saving in a defined contribution pension. The focus on those saving in DC pensions means our work is comparable to that of others who have undertaken similar exercises, such as Pike (2022).

In this chapter, we document the distributions of pension saving and pension wealth among this group, and how these vary with earnings and age. Then we undertake new modelling to project future retirement incomes for our sample of interest, highlighting the uncertainty associated with our estimates, and how the results differ for different groups and with different modelling assumptions. Throughout, we compare these projected future retirement incomes with both the incomes needed to hit target replacement rates and the PLSA minimum retirement living standard, as described in Chapter 2.

4.1 Current trends in pension saving

Before diving into the modelling, we first show the distributions of both current pension wealth and pension contribution rates among our analysis sample in Round 7 of the Wealth and Assets Survey. We uprate wealth to 2023 prices using the Consumer Prices Index.

Figure 4.1 shows the distribution of total private pension wealth (including both defined contribution and defined benefit pension wealth) by age.12 Clearly, there is a wide dispersion in the amount of private pension wealth that employees have accumulated to date. Around 40% of private sector employees currently saving in a DC pension have accumulated less than £10,000 of pension wealth, while another 20% have pension wealth of over £100,000. Unsurprisingly, younger employees are particularly likely to have low levels of pension wealth, with almost two-thirds of 25- to 34-year-olds having pension wealth of less than £10,000. However, even among 50- to 59-year-old employees, over one in five have less than £10,000 in pension wealth. On the other hand, more than a quarter of this older age group have pension wealth of over £250,000. This highlights that the dispersion of pension wealth is particularly wide among those in their 50s; some of these employees will have missed out on many years of pension saving as pension participation fell during the 2000s, while others might have accrued a large defined benefit pension either from a private sector employer (when these schemes were more prevalent) or from a spell working in the public sector.

Figure 4.1. Distribution of total pension wealth among private sector employees saving into a DC pension, by age group

Note: Sample contains private sector employees aged between 25 and 59 currently saving into a defined contribution pension. Pension wealth is uprated to April 2023 prices.

Source: Authors’ calculations using Round 7 of the Wealth and Assets Survey.

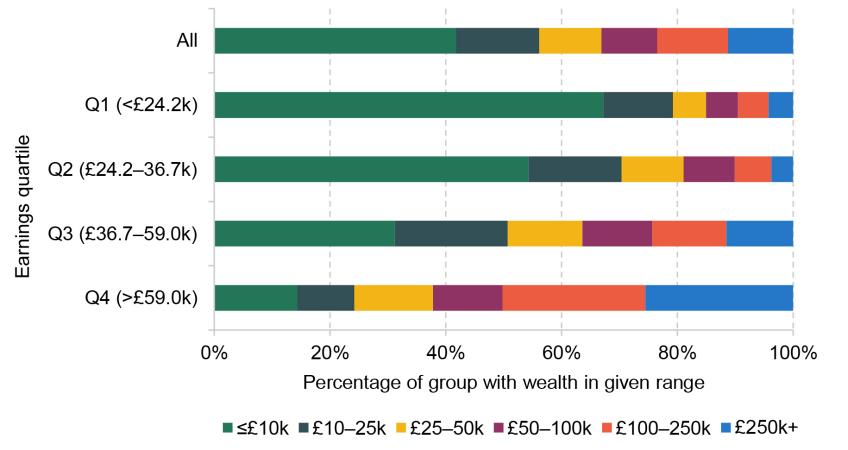

Figure 4.2 shows the distribution of pension wealth for different quartiles of the current earnings distribution. There is again a large spread of pension wealth among middle and, especially, higher earners. A quarter of those earning more than £59,000 annually have pension wealth of less than £25,000, while another quarter have pension wealth of over £250,000. Lower earners typically have lower levels of pension wealth than higher earners, as expected.

Figure 4.2. Distribution of total pension wealth among private-sector employees saving into a DC pension, by current earnings quartile

Note: Sample contains private sector employees aged between 25 and 59 currently saving into a defined contribution pension. Pension wealth is uprated to April 2023 prices.

Source: Authors’ calculations using Round 7 of the Wealth and Assets Survey.

Of course, earnings and age are related: employees in their 50s tend to earn more than those at the start of their career. Table 4.1 therefore shows median total pension wealth in our sample by both age group and earnings quartile. This highlights that the patterns in Figures 4.1 and 4.2 are not driven solely by earnings or solely by age, but that both are important for pension wealth. For a given level of earnings, older workers tend to have higher pension wealth, while for a given age group, higher earners tend to have higher pension wealth. Median pension wealth is just £1,800 among lower earners aged between 25 and 34, compared with around £280,000 for higher earners in their 50s.

Table 4.1. Median total pension wealth among private sector employees saving into a DC pension, by age group and earnings quartile

| Earnings quartile | Age 25–34 | Age 35–49 | Age 50–59 | All |

| Q1 (<£24.2k) | £1,800 | £4,200 | £19,600 | £3,700 |

| Q2 (£24.2–36.7k) | £3,900 | £11,500 | £38,200 | £7,800 |

| Q3 (£36.7–59.0k) | £8,900 | £34,800 | £114,900 | £24,200 |

| Q4 (>£59.0k) | £23,500 | £120,500 | £278,000 | £101,000 |

| All | £4,800 | £26,300 | £77,000 | £17,000 |

Note: Sample contains private sector employees aged between 25 and 59 currently saving into a defined contribution pension. Pension wealth is uprated to April 2023 prices. Figures rounded to the nearest £100.

Source: Authors’ calculations using Round 7 of the Wealth and Assets Survey.

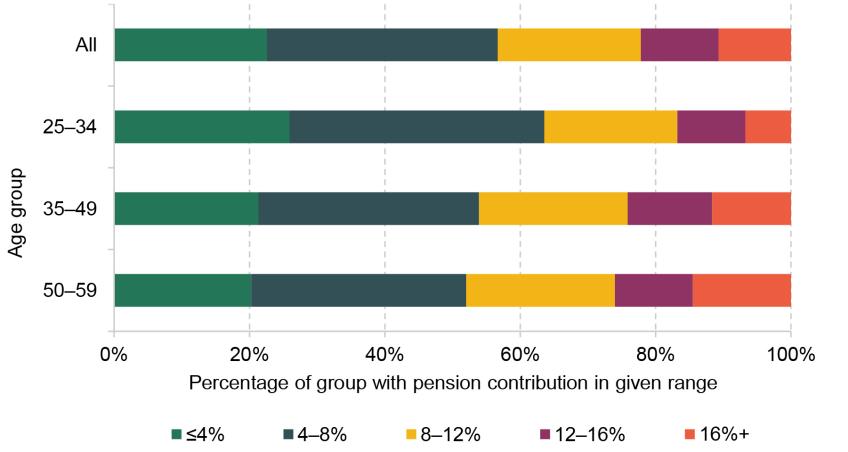

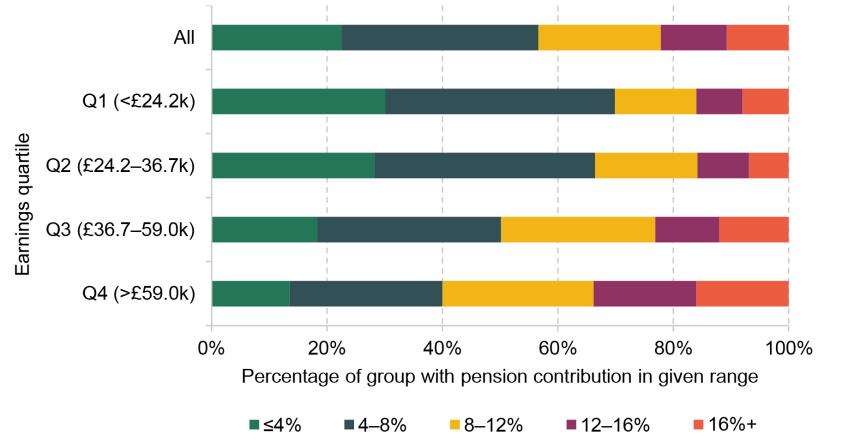

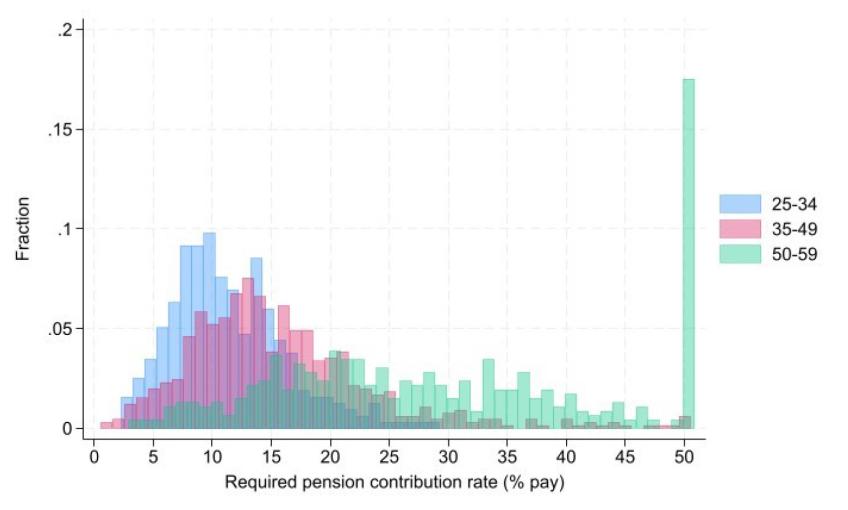

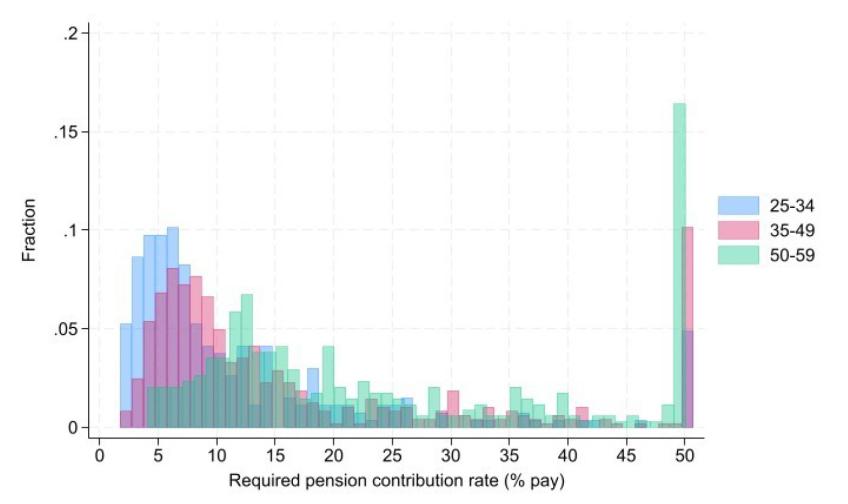

Figures 4.3 and 4.4 show the corresponding relationships between current total (employee + employer) pension contribution rates, as a proportion of gross pay, and age and earnings. Again, there is substantial variation in pension contribution rates; however, there is much less correlation between contribution rates and earnings or age than for pension wealth.

Figure 4.3. Distribution of total pension contribution rates (% of earnings) among private sector employees saving into a DC pension, by age group

Note: Sample contains private sector employees aged between 25 and 59 currently saving into a defined contribution pension. Total pension contribution rates are calculated as employee + employer pension contributions divided by total (gross) earnings.

Source: Authors’ calculations using Round 7 of the Wealth and Assets Survey.

Figure 4.4. Distribution of total pension contributions (% of earnings) among private sector employees saving into a DC pension, by current earnings quartile

Note: Sample contains private sector employees aged between 25 and 59 currently saving into a defined contribution pension. Total pension contribution rates are calculated as employee + employer pension contributions divided by total (gross) earnings.

Source: Authors’ calculations using Round 7 of the Wealth and Assets Survey.

One thing that stands out from these figures is that a significant fraction of private sector employees saving in DC pensions have low contribution rates. Over 20% are contributing at most 4% of total earnings, and over half are contributing no more than 8% of total earnings. On the other hand, nearly a quarter have a contribution rate of over 12% of earnings. Older employees are slightly more likely to have higher contribution rates than those aged between 25 and 34, and higher earners also tend to have higher contribution rates than lower earners. Indeed, almost 70% of those in the bottom half of the earnings distribution are contributing at most 8% of earnings to their pension.

Despite this, we still find that the share contributing less than or equal to 8% of earnings to their pension is 45% among those in the top half of the distribution, and 52% among those aged between 50 and 59. Even among those in the top half of the distribution and aged between 50 and 59, 36% have a contribution of at most 8% of earnings. This is likely a particularly good time in working life for many of these individuals to do their pension saving, when their earnings are high and when their outgoings are often lower due to lower mortgage repayments and lower childcare costs (Crawford, O’Brien and Sturrock, 2021).

It is important to remember that the previous graphs in this section on pension contributions have focused on the sample of private sector employees saving in a defined contribution pension. As emphasised in Chapter 1, there are also many private sector employees who are not currently contributing to a pension at all. Figure 4.5 shows that, overall, 27% of all private sector employees are not saving in a pension in Round 7 of the Wealth and Assets Survey, with around half of these non-savers eligible for automatic enrolment (and therefore, presumably, opting out of their workplace pension) and half not eligible.

Figure 4.5. Percentage of working-age private sector employees not saving in a pension, by automatic enrolment eligibility and group

Note: AE = automatic enrolment. SPA = state pension age. The sample contains all private sector employees aged between 16 and 63 (for women) and between 16 and 64 (for men), inclusive, in Round 7 of the Wealth and Assets Survey.

This graph also shows the share not saving in a pension for different groups of private sector employees. Those aged between 16 and 24 are particularly likely to be ineligible for automatic enrolment and not saving in a pension, which is unsurprising given that the current lower age limit for automatic enrolment eligibility is 22. Private sector employees aged between 60 and state pension age are also slightly more likely not to be saving in a pension than those of other ages, both due to slightly higher rates of ineligibility (with many working part-time earning below the earnings trigger) and of opting out. Over half (54%) of those in the bottom quarter of the earnings distribution are not saving in a pension, with most of them not eligible for automatic enrolment (principally due to the £10,000 earnings trigger). In addition, women are more likely not to be saving in a pension than men as they are less likely to be eligible for automatic enrolment, consistent with results in Cribb, Karjalainen and O’Brien (2023). Groups with lower levels of formal education qualifications are more likely not to be saving in a pension, as are part-time workers compared with full-time workers. All these results on who is not saving in a pension are important to keep in mind when interpreting the modelling results, which focus on the sample of 25- to 59-year-old private sector employees currently contributing to a defined contribution pension. We do show results for the sample of all private sector employees (who are not saving in a defined benefit pension) in Table B.3 in Appendix B, but we do not include non-pension-savers in our main sample given more uncertainty about how their pension saving might evolve in the future.

4.2 Overview of modelling approach

Our modelling takes the current position of employees and projects forward the retirement incomes they may expect on current trends. In this section, we provide a high-level overview of how this modelling works and the main assumptions we have made. Appendix A contains a full, self-contained, description of the modelling.

The underlying data for our model come from the Wealth and Assets Survey (Round 7), where respondents report their earnings, total pension wealth, current pension contribution rate, sex, age and education level. We simulate forward earnings and employment for each employee until they permanently leave the labour force. These simulations are based on observed data from Understanding Society (also known as the UK Household Longitudinal Survey), and we allow people with different education levels, people from different generations, and men and women to have different earnings trajectories. Our method allows people to move up and down the earnings distribution and to move into and out of paid work in a way broadly consistent with what has happened in the past. In addition, the earnings processes are consistent with future economy-wide earnings growth of 1.8% per year, in line with OBR long-term assumptions.

As well as allowing for movements into and out of paid work during working life, we also model when people permanently leave the labour force. We assume that people aim to retire at state pension age; however, some people are forced to retire earlier than this (as early as age 60) – for example, due to health problems, because they have to care for a family member or because they lose their job and are unable to find another one. We do not allow people to work past state pension age in our modelling, nor do we allow people to retire before state pension age because they think they have already accumulated enough wealth to enjoy a comfortable standard of living in retirement.

We assume that people save a constant fraction of their earnings – as defined by their current total (employer + employee) contribution rate – into their pension in all future years in which they are in paid work. People then access their pension pot (coming from any defined contribution wealth they had already accumulated by the time they were surveyed, plus future saving, plus returns they get on their saving) once they permanently leave the labour force. An individual’s retirement income is calculated in the first year after they permanently leave work. As well as their defined contribution pension income, an individual’s retirement income will also be made up of either state pension income or means-tested state support (depending on whether they leave work at state pension age or earlier), any defined benefit income they had already accrued rights to in a previous job, and, in some specifications, annuitised income from other forms of wealth (e.g. from future receipt of inheritances or existing financial wealth held outside of pensions).

We assume all pensioners receive a full new state pension from state pension age. If someone leaves paid work before state pension age, we assume they draw down their defined contribution (and other) wealth more quickly in the period before they reach state pension age, before annuitising the rest upon reaching state pension age in order to smooth their income over their whole retirement. The state pension is assumed to grow in line with average earnings (1.8% per year in real terms) in the baseline model, while the generosity of working-age means-tested support is increased in line with prices.

We then compare the individual’s projected retirement income with a given measure of adequacy. The PLSA minimum retirement living standard is worth £14,400 per year currently; we convert this to a pre-tax measure and then uprate it in line with average earnings – this implicitly assumes that society’s view of a minimum acceptable standard of living in retirement (as judged by this measure) rises as the country becomes more prosperous. For the target replacement rate measure of adequacy, we define pre-retirement income as the individual’s average income between ages 50 and 59. We then multiply this by the relevant target replacement rate to get a measure of target retirement income (the target replacement rates are outlined in Chapter 2 – see Table 2.1).

As well as assessing whether an individual’s projected retirement income is on track to hit a given measure of adequacy on current trends, we can also calculate the share of future earnings that they would need to save in order to reach adequacy under different metrics. In addition, we can project what might happen to their retirement income if parameters of the automatic enrolment system were changed, such as an increase in minimum default contribution rates.

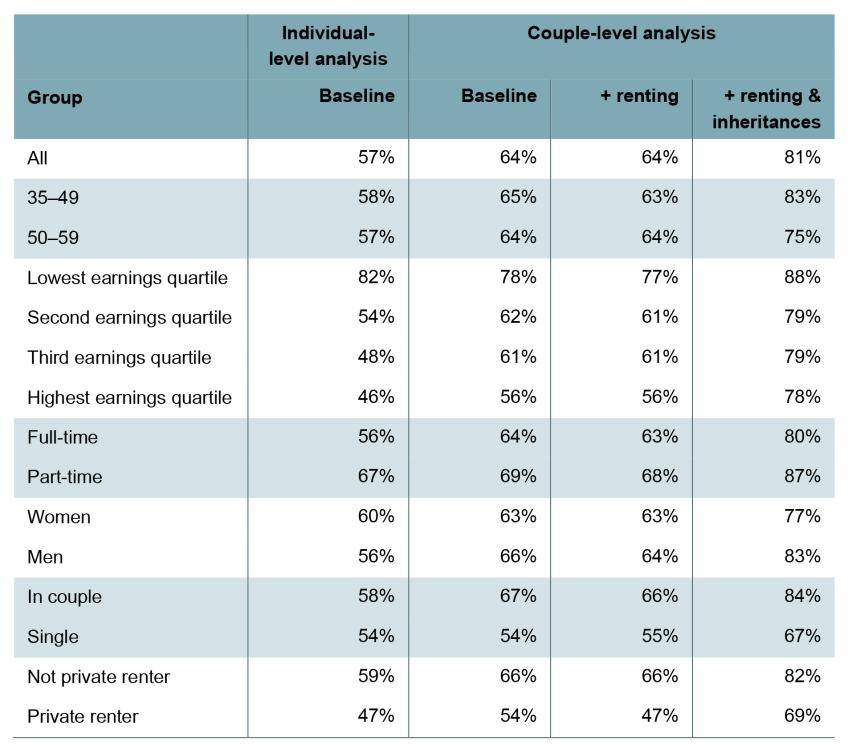

In an extension to the model, we also show what happens if we model individuals as couples rather than as individuals, assuming that earnings and retirement resources are shared equally between both members. To do this, we focus on people aged at least 35, given that the share of people with a cohabiting partner or spouse is much less stable before this age, and we assume that couples remain married/partnered at least until retirement.13 When doing this, we compare single people with the PLSA minimum retirement living standard for single people and we compare couples with the PLSA standard for couples.

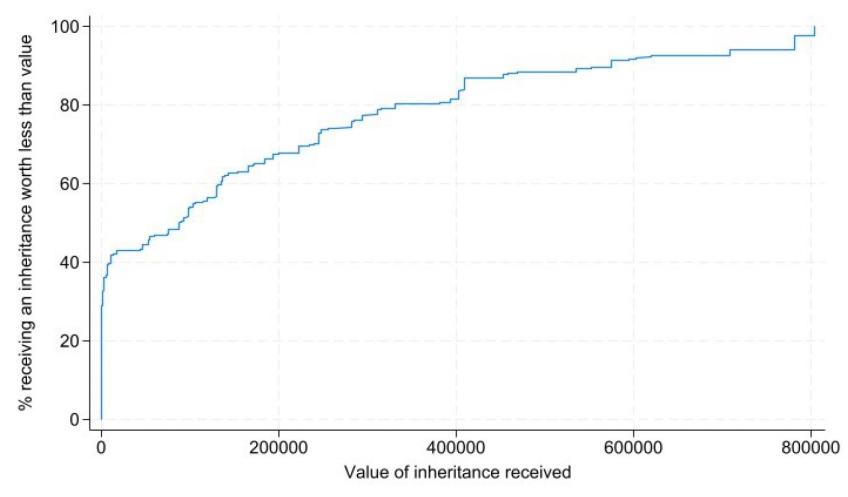

We also show the potential effect of future inheritance receipt on projected retirement incomes and the shares reaching adequacy. To do this, we model people as receiving an inheritance from a distribution consistent with previous work by IFS researchers (Bourquin et al., 2020) depending on their education level, their generation and whether their parents are homeowners – see Figure A.1 in Appendix A for the distribution of inheritances received in our model. We assume inheritances are received at age 60 and are used to fund their retirement living standards. This can be thought of as an upper bound of the effect of inheritances – for example, some may decide to pass the wealth on to their children.14

In another extension, we account for the extra living costs brought about by private renting in retirement. To do this, we assume that anyone aged at least 45 who rents their home privately in the survey will also be a private renter in retirement. For private renters aged between 35 and 44, we estimate the probability of moving out of private renting for this age group based on data from Understanding Society, where we allow the probability to vary by earnings, region and marital status. We then scale these probabilities such that the overall private renting share for this age group matches the overall private renting share for people born in the early 1970s. Once we have determined who will be privately renting in retirement, we adjust our measures of target retirement income for these individuals and calculate the share who reach these adjusted targets, taking into account that some renters will receive housing benefit which will cover at least part of their rent.

As noted in Chapter 2, there have been several other attempts to model future retirement incomes, such as Pike (2022) and Department for Work and Pensions (2023) in recent years. As well as sharing similarities, the modelling in all these reports differ in several important ways. Different modellers make different assumptions about how various factors might evolve in the future, and make fundamentally different choices about how to model the world. Despite this, many of the results in this report are broadly consistent with these previous modelling exercises, lending credibility to our (and, by extension, their) results.

4.3 Projections at the individual level

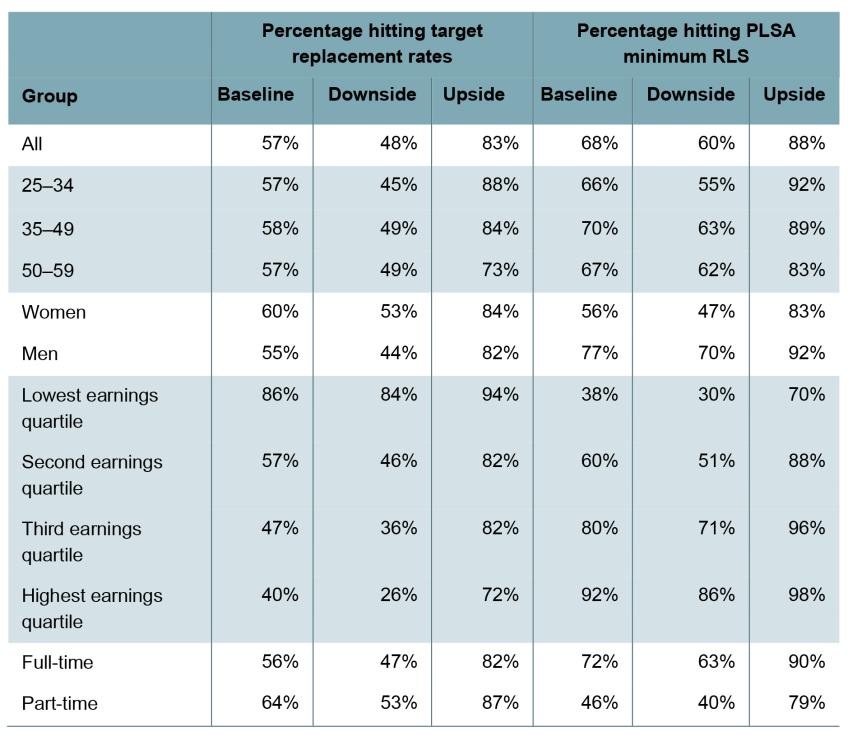

We first set out the baseline results from our modelling. This is for our entire sample of 25- to 59-year-old private sector employees saving into a DC pension, modelled at the individual (rather than couple) level, and without taking into account housing costs or the possibility of receiving an inheritance. Our baseline assumptions for how the economy will evolve in the future are as in Chapter 3: average real earnings growth is assumed to be 1.8% per year, people achieve a real rate of return of 3.3% per year on pension saving during the accumulation phase, and the real rate of return during the decumulation phase (used for calculating annuity rates) is 1.8%. The state pension is assumed to be indexed in line with average earnings growth.

Figure 4.6 shows that, in this baseline model, 57% of our sample are on track to hit their target replacement rate and 68% are on track to achieve the PLSA minimum retirement living standard. In other words, over two in five individuals (7 million people) are projected to be ‘undersaving’ relative to the target replacement rate metric, and one in three (5 million) are relative to the PLSA minimum metric. So in both cases a substantial minority appear to be undersaving.

Figure 4.6. Percentage of private sector employees saving into a DC pension who are projected to hit different measures of retirement income adequacy, by group

Note: The sample contains 25- to 59-year-old private sector employees saving into a DC pension in Round 7 of the Wealth and Assets Survey. We simulate their projected future retirement income under our baseline assumptions, modelling everyone at the individual level and without accounting for future housing costs or inheritances. We then compare these future retirement incomes with the two measures of retirement income adequacy. Earnings quartiles are based on pre-retirement earnings, i.e. simulated average earnings between ages 50 and 59.

This graph also highlights that the groups projected to achieve ‘adequacy’ are quite different for the two metrics, especially when we look at the patterns by earnings. On the one hand, over 85% of those in the bottom quartile of pre-retirement earnings are on track to achieve their target replacement rate, compared with only around 40% of those in the top quartile. In contrast, only 38% of those in the lowest pre-retirement earnings quartile are on track to hit the PLSA minimum retirement living standard, compared with over 90% in the top quartile.

This difference fundamentally arises because target retirement incomes are higher for those with higher pre-retirement earnings under the target replacement rate metric, while the PLSA minimum retirement living standard does not vary with earnings. Higher earners find it easier to reach the minimum standard because relatively low pension saving rates might still be sufficient for them to reach this benchmark, which will not be the case for lower earners. The proportion achieving their target replacement rate is particularly high for lower earners because they almost replace a sufficient proportion of their pre-retirement income with the state pension alone. In fact, the only lower earners who do not reach their target replacement rate on this measure are those who have to leave work before state pension age. These people do not have any state pension income in their measured retirement income, since we measure these in the first year after permanently leaving the labour force. Once they reach the state pension age, the value of a new state pension is sufficiently large relative to their earnings when working for their replacement rate to be reached.

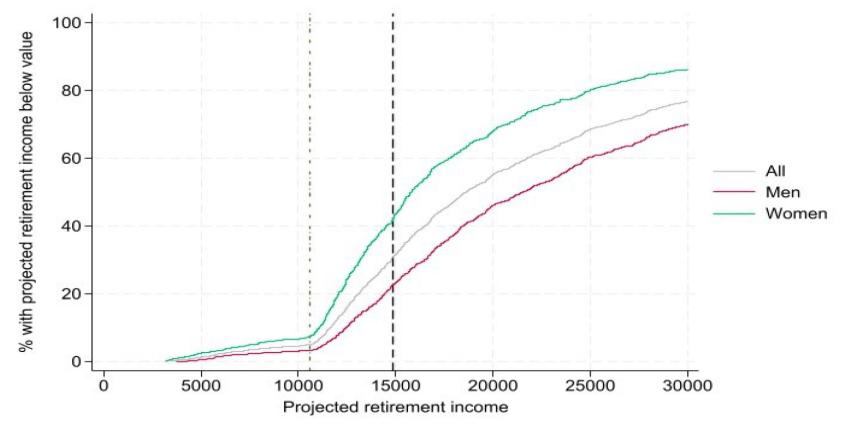

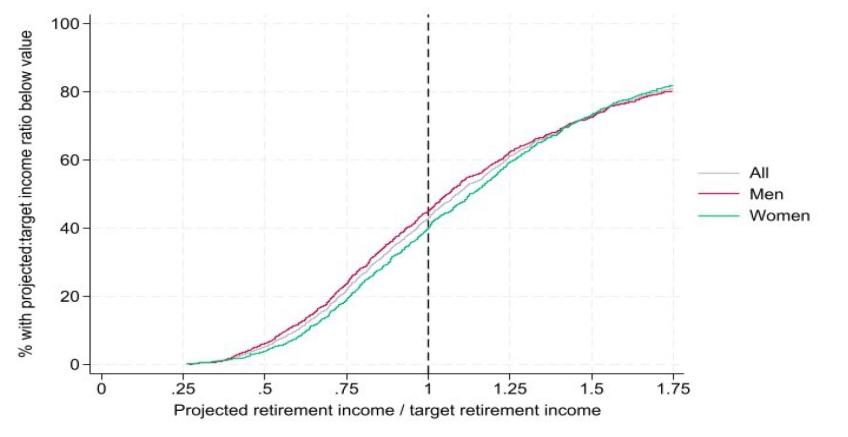

There are further differences in the patterns of who reaches adequacy between the two metrics, principally driven by differences in earnings between different subgroups. Women, who tend to earn less than men, are slightly more likely to reach their target replacement rate but are less likely to reach the PLSA minimum retirement living standard. Similarly, a higher proportion of part-time workers than full-time workers achieve their target replacement rate, while a lower proportion reach the PLSA minimum standard. Interestingly, the proportions hitting both types of adequacy vary little with age.