Downloads

Download report PDF

PDF | 638.98 KB

Executive summary

This report is one of two reports on the management of pension wealth in retirement conducted as part of the Pensions Review, led by the Institute for Fiscal Studies in partnership with the abrdn Financial Fairness Trust. In this report, we examine the decisions that older individuals face as they draw on and manage their private pension wealth through retirement. In particular, we highlight the growing importance of defined contribution (DC) wealth, fuelled by automatic enrolment into (predominantly) DC workplace schemes, we document how retirees currently draw down on their wealth and we provide evidence for the wide range of financial risks that older people face. We utilise data provided by the Association for British Insurers, the Financial Conduct Authority, and the Office for National Statistics, as well as conducting our own new empirical analysis of household surveys. We have also benefited from insights provided by focus groups which have been run alongside this project by Ignition House.

The accompanying report (Boileau, Cribb and Emmerson, 2025) uses the evidence drawn together in this report in discussing potential policy improvements to help people make good financial decisions through their retirement.

Key findings

The importance of defined contribution pension wealth

- The share of retirees who will have to decide how to draw on their defined contribution (DC) pension wealth is set to grow significantly. Among 55- to 64-year-olds in 2021–23, six in ten (59%) had some DC pension wealth, up from around 44% fifteen years earlier. Meanwhile, the fraction with defined benefit (DB) pension wealth has fallen from 45% to 38%. This rise of DC wealth and fall of DB wealth will continue.

- The average size of individuals’ DC private pension wealth at retirement is set to rise as well. We estimate that, on current trends, median DC wealth at retirement (amongst those with some DC wealth) for people born in the early 1970s will be more than a third (38%) higher than among those born ten years earlier in the early 1960s (£102,000 compared with £74,000). A quarter of those born in the early 1960s with some DC wealth are projected to have more than £215,000; this rises by a third to having more than £286,000 among those born a decade later. A quarter, though, of those born in the early 1960s will have £25,000 or less, rising to £36,000 or less among those born in the early 1970s. These birth cohorts are likely to face particular challenges – resulting from the decline of DB pensions, combined with the fact that they did not experience a full career under automatic enrolment.

- DC pension wealth is likely to be considerable among those who have worked and contributed to a DC pension pot their whole adult lives – even for low earners. A lower earner (currently earning £18,000, e.g. working 30 hours a week on the 2024–25 minimum wage) working every year from age 22 to state pension age might expect to accumulate a pot of £150,000 given reasonable assumptions about economy-wide earnings growth and asset returns. An average earner (currently earning around £37,000) might accumulate a pot of £320,000. Therefore many, including relatively low earners, will need to make complex decisions about how to draw upon consequential amounts of DC pension wealth in the future.

- However, at the moment, most (although by no means all) current retirees’ decisions about DC pension wealth are relatively low-stakes. This is because a minority rely on DC pensions as a significant source of retirement income. For example, 19% of those aged 55–64 have more than £50,000 of DC pension wealth and less then £50,000 of DB pension wealth.

- Many of those with DC pension wealth do not know how they will access their pots, and the take-up of advice and guidance is low. Around four in ten 50- to 64-year-olds with DC wealth report not knowing how they will access this wealth. Nearly three-quarters (73%) of those in their late 50s with DC wealth had not encountered any sort of information on pensions or retirement choices in the last three years, and the majority of DC pots accessed for the first time were accessed by people who had not used any guidance or advice.

Patterns of wealth drawdown at older ages

- The ways in which people access DC pension wealth have changed dramatically since ‘pension freedoms’ were announced in 2014 and introduced in 2015. Annuitisation rates have plunged, with the number of annuity purchases falling by three-quarters between 2013 and 2024 (despite a partial recovery as annuity rates have risen since 2022). Remaining in active drawdown implies that retirees will have more complex financial decisions to take at older ages compared with if they have an annuitised income stream.

- Most DC pension pots are accessed before turning 65. In 2023–24, two-thirds of pension pots accessed for the first time were accessed by people aged under 65. This proportion was much lower among the minority purchasing annuities, among whom only 35% were aged under 65. Most of those with particularly valuable pots (worth £250,000 and above) also accessed them before turning 65, consistent with the fact that retirement before the state pension age is (increasingly) concentrated among the wealthiest.

- Non-annuitised wealth tends to be drawn down relatively slowly in retirement. In the case of DC pension wealth, a quarter (26%) of DC pots worth £250,000 and above from which regular withdrawals were being made (representing 124,000 pots in 2023–24) were withdrawn at annual rates of less than 2% in 2023–24, and a further 30% at rates of between 2% and 4%. Some of this slow drawdown is likely to have been due to the (soon to be withdrawn) inheritance tax benefits of keeping wealth in DC pensions. Financial wealth held outside of pensions is also drawn upon very slowly. Median real net financial wealth for those born in 1930–34 declined by just 13% between the ages of 75 and 89, and among those born in 1940–44 it declined by just 5% between the ages of 66 and 79.

- Significant fractions of older people’s wealth are held in owner-occupied housing – but downsizing, or other forms of equity release, are uncommon. In 2018–20, almost three-quarters of people in Great Britain in their 40s and 50s were homeowners, with the median value of their main property around £250,000. Both downsizing and equity-release products were unpopular among retired homeowners in our focus groups, implying that this wealth is unlikely to be accessed during retirement. Only 3% of non-retired homeowners in their 40s and 50s planned to use equity-release products to help fund their retirement in 2018–20.

Financial risks at older ages

- There are a set of important and interrelated risks people face in old age, which have consequences for their retirement incomes and material standard of living. These include longevity risk, investment risk and the risk of cognitive decline. Compared with a world with widespread DB pensions and where DC pensions had to be annuitised, people are exposed to these risks to a much greater extent.

- Longevity has improved dramatically in recent decades – in particular, the chances of living to very old ages have risen rapidly. Among men, the probability a 60-year-old will live to 95 has more than tripled between 1981 and 2024, rising from 4% to 14%. The probability a 60-year-old woman will live to 95 has more than doubled over this period, from 10% to 23%. This means people face the risk that they will live much longer than they expect and, as a result, exhaust their private financial resources and rely only on income from the state (and any owner-occupied housing they own).

- Relative uncertainty over life expectancy rises with age. 60-year-olds are much less likely to live 25% or 50% longer than their median life expectancy than are 75-year-olds or 90-year-olds. 16% of female 60-year-olds and 21% of male 60-year-olds in 2024 were expected to live 25% longer than their median life expectancy, compared with 31% of female and 36% of male 90-year-olds. In general, the more uncertainty over life expectancy, the higher the case for insuring against that uncertainty, so the potential value of annuitisation is higher at older ages.

- Investment risk has important consequences for outcomes in retirement. Those who actively manage their DC pension through retirement, rather than buying an annuity, leave themselves exposed to fluctuations in the rate of return on the investments they hold. These can result in large differences in the age at which DC wealth is exhausted. Those withdrawing 5% initially from a £100,000 pot at 67, and then keeping withdrawals fixed in real terms thereafter, might exhaust their pot at around age 93 if they enjoy a gross real return of 3%. But if the real return is 0%, this could be at age 86 – below median life expectancy for both men and women.

- Cognitive decline is another key risk at older ages. Memory tends to decline through retirement, particularly at later points. One measure of cognitive function declined by 18% between the ages of 66 and 79 for those born in the early 1940s. The decline was higher at older ages – a decline of 26% between the ages of 75 and 89 for those born in the early 1930s. These declines mean it is harder for people to manage their own (potentially complex) financial decisions at later points in retirement.

- Those who are widowed may face particular difficulties managing their finances. The risk of being widowed rises with age, and is higher for women (reflecting higher life expectancy for women and average age gaps within couples). 7% of men born in the mid 1930s were widowed by their early 70s, rising to 18% by age 85. Among women, the equivalent figures are 27% rising to 55%. Being widowed can have greater financial consequences where the deceased partner is the one who was better at, and took more responsibility for, managing finances. This is particularly likely to be the case among widowed women.

1. Introduction

Managing the combination of longevity and investment risks through retirement has been described by Nobel Prize-winning economist William Sharpe as the ‘nastiest, hardest problem in finance’.1 There used to be fewer risks associated with managing pension wealth in retirement for most people in the UK. In the mid 1990s, the majority of employees saving into workplace pensions were saving into a defined benefit (DB) pension, which offered a regular, lifelong income through retirement. For those in defined contribution (DC) arrangements (where pension contributions are held in a tax-efficient account and invested for later life, but provide no promise of a particular income in retirement), it was near-compulsory that three-quarters of accumulated DC wealth be annuitised by the age of 75.2 Again, this would ensure a known income stream that would last until the end of life.

While public sector employees still have access to DB pension arrangements, private sector employers have become increasingly likely to offer DC instead of DB pensions. The introduction of automatic enrolment has further increased the share of employees contributing to DC arrangements. And ‘pension freedoms’, introduced in April 2015, allow people to access their DC pension wealth flexibly, rather than being required to annuitise any of it, radically expanding the options available to people as to how and when to use their pension wealth.3

Since the introduction of pension freedoms, annuity purchases have rapidly declined. More people are choosing to purchase ‘drawdown’ products – or to access their pension in other ways, such as withdrawing their pension pot in full. This greater flexibility could allow people to make decisions better suited to their particular spending needs: perhaps to support a phased retirement prior to the state pension age, or to spend more of their pension wealth earlier in retirement when their health is better. Added flexibility also, though, adds significant complexity and risk to the decision-making process during retirement.

Various risks are faced when managing pension wealth over this period. Most attention has probably been paid to longevity risk – the risk that someone runs out of private resources before death. There are also risks related to inflation, investment returns, health outcomes, cognitive decline, and the health and lifespan of a partner. The increase in financial risks that people face, especially in retirement, has been noted by a diverse range of different stakeholders including the House of Commons Work and Pensions Select Committee (2022), the Institute and Faculty of Actuaries (2021) and the Joseph Rowntree Foundation (Barnard, 2023).

This report draws together evidence on how people in or approaching retirement are making decisions over their pension wealth, and how this is likely to change in the future. We set out and discuss ten ‘key facts’ throughout the report that we think are the most important issues in this area. To do this, we draw on evidence from government and industry statistics, existing research, our own new empirical analysis, and focus groups of newly retired individuals run by Ignition House alongside the Pensions Review.

The remainder of this report proceeds as follows. In Chapter 2, we illustrate the changing prevalence and size of DC pension wealth and how important that will be for people’s retirement finances. In Chapter 3, we examine how current retirees are drawing down on their wealth and discuss the extent to which this can be a guide to the future. In Chapter 4, we quantify various risks that individuals face in retirement. Chapter 5 provides a short conclusion. In addition, this report provides the basis for the accompanying report (Boileau, Cribb and Emmerson, 2025) which sets out our conclusions for public policy in this area.

2. The importance of defined contribution pension wealth

The rise in defined contribution (DC) pension wealth, and the end of near-compulsory annuitisation in 2015, have increased the challenges people face when managing their retirement income. Defined benefit (DB) pension arrangements remain relatively easy to manage, with few decisions required from individuals other than the age at which to start drawing their pension. In this chapter, we therefore focus on DC pension wealth, discussing its changing prevalence, and how the shift from DB to DC pension participation is likely to affect current and future retirees.

Key fact 1. While relatively low amongst current retirees, defined contribution pension wealth is growing in prevalence and value.

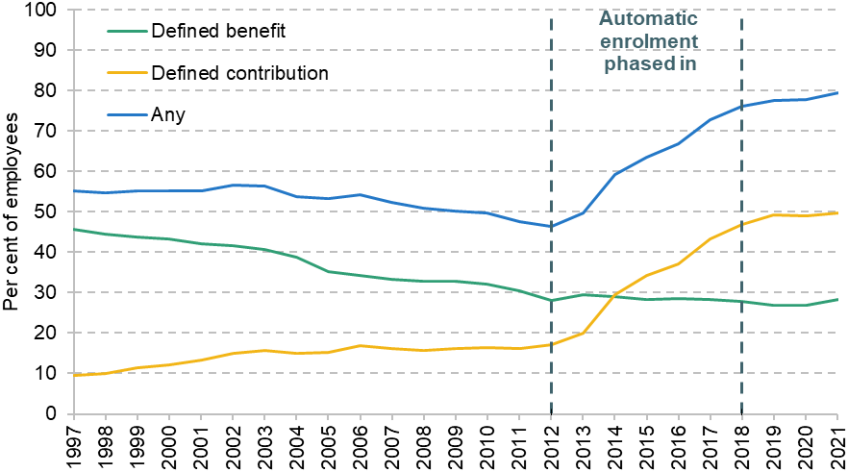

Over the last 30 years, the pension provision of private sector employees in the UK has changed dramatically. Figure 2.1 shows the share of employees saving in different types of workplace pensions between 1997 and 2021. Overall participation in a workplace pension rose between 2012 and 2018, from around half (47%) to more than three-quarters (76%) of employees, a rise entirely driven by the rise in the share participating in a DC pension. Meanwhile, between 1997 and 2021, the share of employees in a DB pension has fallen by almost two-fifths, from 46% to 28%. Among employees participating in a DB pension, almost all are in the public sector. In 2021, only 7% of private sector employees were participating in a DB pension scheme, compared with 82% of public sector employees (Office for National Statistics, 2022b).

Figure 2.1. Share of UK employees participating in a workplace pension by type of pension, over time

Source: ONS analysis using the Annual Survey of Hours and Earnings (https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/workplacepensions/bulletins/annualsurveyofhoursandearningspensiontables/2021provisionaland2020finalresults).

The initial rise in the share of employees contributing to DC pensions was driven by a couple of key factors. In 1988, employees were first allowed to opt out of the State Earnings-Related Pension Scheme (SERPS) into a DC scheme (previously, opting out of SERPS was only possible into a DB pension). As was shown in the first report of the Pensions Commission (2004), membership of DC pensions started to rise in the late 1980s, and subsequently rose slowly throughout the late 1990s and 2000s as private employers were also shifting their workplace pension offerings to DC, rather than DB, schemes. However, in 2012, still only 17% of employees (22% of private sector employees) were participating in DC pension arrangements.

Between 2012 and 2018, automatic enrolment was gradually rolled out in the UK, increasing the share of employees contributing to a DC scheme substantially. Automatic enrolment requires employers to enrol eligible employees into a workplace pension scheme. While employees can opt out, the vast majority do not, driving a substantial increase in the numbers saving into DC pensions, and thus an increase in the prevalence and amount of DC wealth (Cribb and Emmerson, 2020).

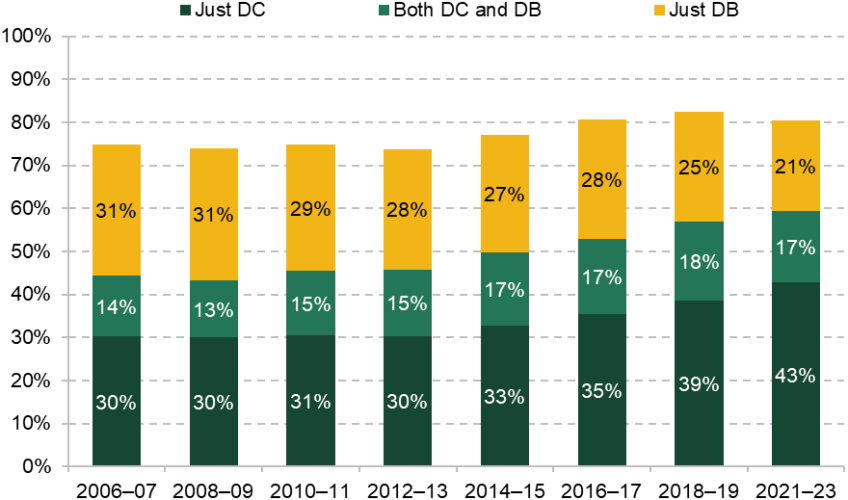

This rapid change in the landscape of workplace pension provision has much-slower-moving effects on the level of pension wealth with which people reach retirement, since pension wealth at retirement reflects a history of contributions through working life. As is shown in Figure 2.2 – which shows the share of 55- to 64-year-olds with different types of pension wealth, between 2006–07 and 2021–23 – the rise in the proportion of 55- to 64-year-olds with some DC pension wealth is relatively slow compared with the changes in workplace pension provision over the same period.

Figure 2.2. Share of 55- to 64-year-olds with (a) just defined contribution, (b) both defined contribution and defined benefit and (c) just defined benefit pension wealth

Source: Authors’ calculations using the English Longitudinal Study of Ageing, Waves 1–10.

As Figure 2.2 shows, less than half (44%) of 55- to 64-year-olds in 2006–07 had any DC pension wealth. Of this group, a third also had some DB pension wealth, further reducing dependence on DC pensions. Since the mid 2000s, the fraction of those approaching their mid 60s with DB wealth has fallen and the fraction with DC wealth has risen. Putting aside the roughly constant fraction of this age group with both DB and DC wealth, the share of 55- to 64-year-olds who only have DB wealth has fallen from 31% to 21% between the mid 2000s and the early 2020s, while the fraction with only DC pension wealth has risen from 30% to 43%.

Amongst those who are currently close to retirement, amounts saved in DC pensions are relatively low, on average. Table 2.1 shows the shares of 55- to 64-year-olds with different levels of pension wealth in more detail. We categorise people here on the basis of how much DC and DB pension wealth they have, a categorisation we can use to think about which people have higher-, or lower-, stakes decisions to make about their private pension wealth.

Table 2.1. Share of 55- to 64-year-olds with different levels of pension wealth in 2018–20

Note: Percentages are from the Wealth and Assets Survey (WAS), adjusted using a scaling factor from the English Longitudinal Study of Ageing. Defined benefit pension wealth in WAS is calculated using an adjusted discount and annuity rate.

Source: Authors’ calculations using the Wealth and Assets Survey, Round 7 (2018–20), and the English Longitudinal Study of Ageing, Wave 9 (2018–19).

Those with the lowest-stakes decisions to make are people who have little or no DC pension wealth and significant DB pension wealth – these are the cells in Table 2.1 shaded in the darker blue. In contrast, the stakes are much higher if you have significant DC pension wealth but little or no DB pension wealth, the groups highlighted in darker red in the table. Here, we have chosen to describe ‘significant’ wealth as having more than £50,000 in DC or DB pension wealth. Of course, there are no precise definitions here, but while the numbers would differ if different thresholds were used, the principle remains the same.

Table 2.1 shows that only a minority – albeit a significant one – have DC wealth that is consequential both in relative terms to DB pension wealth and in absolute terms. Under a fifth (19%) of 55- to 64-year-olds have both more than £50,000 in DC pension wealth and less than £50,000 in DB pension wealth. In contrast, a plurality – 44% (highlighted in light blue) – had DB pension wealth below £50,000 but also had less than £50,000 of DC pension wealth. 29% had significant DB wealth (above £50,000) but below £50,000 in DC wealth, implying no significant decisions to be made. The remaining 8% had both significant DB and high DC wealth.

All this implies that while DC pension wealth has risen over time, and will continue to do so, most people currently approaching retirement do not look like they are having to make high-stakes decisions over how they draw their DC pension wealth, due to the combination of low average amounts and the fact that some already have non-trivial levels of DB wealth.

Key fact 2. In future, the share of people with consequential decisions to make about DC wealth in retirement will rise.

Figure 2.1 implies that the share of retirees with some DC wealth is set to rise, driven by a rising share of people approaching retirement who have spent time employed since 2012 (when DC pension participation increased).

The average amount of DC wealth at retirement is also on course to increase over time. We use projections based on the Wealth and Assets Survey, as described more fully in a previous report of the Pensions Review (O’Brien, Sturrock and Cribb, 2024), to estimate how average DC wealth at retirement is likely to change in the medium term. We look at people born between 1960 and 1979, who will reach their mid 60s between now and the mid 2040s.4

These projections, summarised in Figure 2.3, imply that median DC wealth (meaning that half of people have less than this and half more) at retirement among those with some DC wealth born in 1960–64 will be around £74,000. This rises to £102,000 among those born a decade later, in 1970–74, and to £131,000 among those born in 1975–79.

Figure 2.3. Projected 25th percentile, median and 75th percentile DC pension wealth at retirement among those with some DC wealth, by birth cohort

Source: Authors’ calculations based on projections using the Wealth and Assets Survey, 2018–20 (described more fully in O’Brien, Sturrock and Cribb (2024)).

The graph also shows that 25th and 75th percentile DC pension wealth among those with some DC pension wealth are set to rise. The 75th percentile of DC pension wealth – above which a quarter of people have higher levels – is projected to rise by a third, from £215,000 to £286,000, comparing those born in the early 1960s with those born in the early 1970s. The 25th percentile will rise by more in proportional terms (43%), although less in absolute terms, increasing from £25,000 among those born in the early 1960s to £36,000 among those born in the early 1970s.

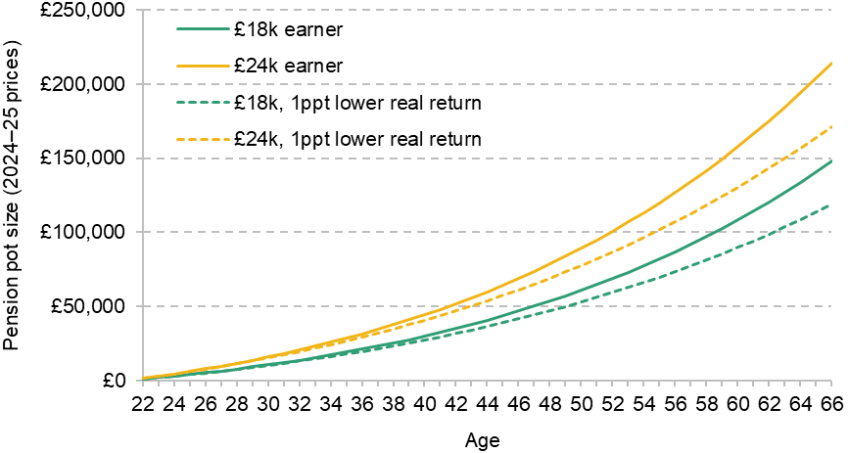

In the longer term, DC pension wealth is likely to become considerable even for relatively low earners if they work full-time (as they will be automatically enrolled into a DC pension throughout their adult lives). Even the youngest generation examined in Figure 2.3 – those born in the late 1970s – were already in their mid 30s upon the introduction of automatic enrolment in 2012, and compounding returns mean that savings made earlier in adult life can have a particularly large effect on people’s retirement finances. To illustrate the potential for the future importance of DC wealth, Figure 2.4 shows illustrative projections for the size that DC pots could reach under existing minimum automatic enrolment contributions.

Figure 2.4. Pension pot size at each age for someone who works every year from ages 22 to 66, assuming 1.8% earnings growth per year and 3.3% real rate of return

Note: We assume that individuals work each year, that 8% of earnings between the lower and upper earnings limit (£6,396 to £50,270) is contributed to their pension each year, that they receive a 3.3% real rate of return on their savings, and that their earnings growth is 1.8% each year in real terms. We assume that the lower earnings limit (LEL) and upper earnings limit (UEL) rise with inflation each year.

Source: Authors’ projections based on automatic enrolment parameters.

A lifetime lower earner, working every year from ages 22 to 66, and currently earning £18,000 a year – representing someone currently working 30 hours a week on the 2024–25 minimum wage – might expect to accumulate a pot of £150,000 by age 66 given reasonable assumptions about economy-wide earnings growth (1.8% annually) and asset returns (3.3% annually).5 If they retire at 60, their pot could still be worth £110,000. If they retire at 60 and asset returns are 1 percentage point lower, they could still have a £90,000 DC pot over which to make decisions. Those who earn £24,000 (currently around the 30th percentile of the annual earnings distribution) might accumulate a pot of £215,000 by 66, or £160,000 if they stop work much sooner at age 60. Among average earners, numbers will be (much) larger; those earning around £37,000 (median full-time annual earnings in 2024) might accumulate a pot of £320,000 by 66 (assuming they made minimum pension contributions).

In practice, gaps in labour market activity will reduce the amount saved for many. This is likely particularly to be the case for women, who have lower employment rates than men, which largely drives current differences in pension participation rates (Cribb, Karjalainen and O’Brien, 2023). It is also the case, though, that many low earners will have periods of higher earnings, and while they may have some years where they have opted out of a workplace pension, they could have some, or indeed many, years where they contribute more than the minimum default amount. What is clear is that many relatively low earners will need to make complex decisions about how to draw upon consequential amounts of DC pension wealth in the future. There is therefore potential for serious financial mistakes to be made.

Key fact 3. DC pension wealth is increasingly likely to be spread across multiple pension pots.

Under the current system of automatic enrolment, employers typically enrol all their eligible employees into a DC pension plan with the same provider. As a result, when employees change their employer and enrol in a new scheme, this will generally create a new pension pot. Over time, this means that most private sector employees will accumulate multiple DC pension pots through their working lives. Polling in 2024 showed that one in five 18- to 34-year-olds already had five or more pension pots, with an average of three pots across the age group (Guy, 2024). A Pensions Review report published in February showed that some groups – women and lower earners – are particularly likely to accumulate small pension pots (Cribb et al., 2025).

It is likely that individuals with multiple pension pots will find managing their total pension wealth more challenging. Individuals must aggregate the value of all their pots to understand their total DC wealth, which may be particularly difficult if some pots have been forgotten about or even lost, with pension providers unable to contact the pot’s owner. The introduction of pensions dashboards could improve this situation somewhat for individuals seeking to understand their total pension wealth.

Pension schemes will not have access to the information held in pensions dashboards, though, and are likely to continue only to have pot-level, rather than individual-level, data on their members’ pension wealth. This is likely to cause issues if and when any default solutions or options for accessing DC pension pots in retirement are introduced, particularly if these solutions are based on features such as pot size. For example, the NEST Guided Retirement Fund, which NEST manages for members in retirement drawing on their pension, has a lower limit of £10,000.6 Someone with five pension pots with NEST worth just under £10,000 each would therefore not be able to access this fund – designed for pension drawdown – at least without consolidating their pension wealth. Meanwhile, someone with the same level of pension wealth with NEST, but as a single pension pot worth £50,000, would be automatically moved into this fund by NEST.

Savers may also hold pots in both trust- and contract-based DC schemes,7 which can complicate matters further. In 2022, there were 10.5 million active savers in trust-based schemes, compared with 5.6 million active savers in contract-based schemes in 2021 (The Pensions Regulator, 2023). This may exacerbate problems of management associated with multiple pension pots, as trust- and contract-based DC schemes may end up with different default requirements. Even if individuals are able to opt out of these defaults – which seems very likely, at the time of writing – finding out about the various options offered by different sorts of schemes and making an informed choice between schemes is a relatively high burden to place on those drawing down on their pensions. In the next key fact, we document existing low levels of engagement and information about DC pensions, underlining the difficulty of relying on individuals carefully shopping around for retirement solutions.

Beyond just making decisions more difficult for individual savers, the growth of multiple DC pots can create challenges for stakeholders interested in retirement outcomes. Industry data on key measures of how people are drawing on their pension, such as withdrawal rates, are typically collected at a pot, rather than individual, level. This means that as individuals accumulate increasing numbers of pots, the amount of data which could tell us how people are managing their income and wealth in retirement falls. This makes it harder for policymakers, analysts and the pension industry to design effective policies, recommendations and (potentially) default retirement income paths.

Key fact 4. Many with DC wealth report not knowing how they will access their pots, and there is low take-up of advice and guidance.

It is relatively common for those with some DC wealth not to access information, guidance or regulated financial advice – whether in their late 50s and early 60s, or at the point of accessing a pension specifically – and a large share do not know, even close to retirement, how they will access their wealth.

Around four in ten 50- to 64-year-olds with DC wealth report not knowing how they will access this wealth, as shown in Figure 2.5. Perhaps this is unsurprising given that people may not make plans until they get close to retirement, and given generally low levels of engagement with pensions – according to a survey run by the Financial Conduct Authority (2023), only half of people with DC pensions had reviewed their pension savings in the last year, and a survey commissioned by the Department for Work and Pensions (2022) showed that one in four 40- to 75-year-olds saving into a workplace pension did not know the rate of their contributions.

Figure 2.5. Share of those aged 50–64 who report that they do not know how they will access their largest DC pension pot, by wealth and age group

Note: Non-proxy respondents aged 50–64 with some unannuitised DC wealth. Wealth thirds defined among those with any DC wealth aged 50–64. Wealth is defined as total net private wealth at the individual level (excluding non-housing physical wealth and state pension).

Source: Reproduced from Cribb and Karjalainen (2023).

Not knowing how DC wealth would be accessed was most common among the lowest-wealth third of 50- to 64-year-olds, among whom 60% did not know how they would access their largest DC pot (perhaps less concerningly, since DC income will make up a very small share of overall income for this group (Cribb and Karjalainen, 2023)). But even among the highest-wealth third, 31% did not know how they would access their largest DC pot. Looking at just those in their early 60s, so closest to the point of access, low levels of planning also held true: 39% said they did not know how they would access their largest pension pot when asked.

At the same time, most of those in their late 50s have not accessed any sort of information or advice about pension choices or about retirement. Figure 2.6 shows that 62% of those in their late 50s had not accessed any information or advice from any source in the last three years, rising to 73% of those with DC pension wealth. 10% of those with DC pension wealth had accessed information from an independent financial advisor, while 8% had accessed information from an employer.

Figure 2.6. Share of those aged 55–60 who had accessed information or advice about retirement or pension choices in the last three years from various sources, among (a) everyone and (b) those with DC pension wealth

Note: Percentages do not sum to 100, since people can give multiple answers to these questions and because not all answers are included.

Source: Authors’ calculations using the English Longitudinal Study of Ageing, Wave 10.

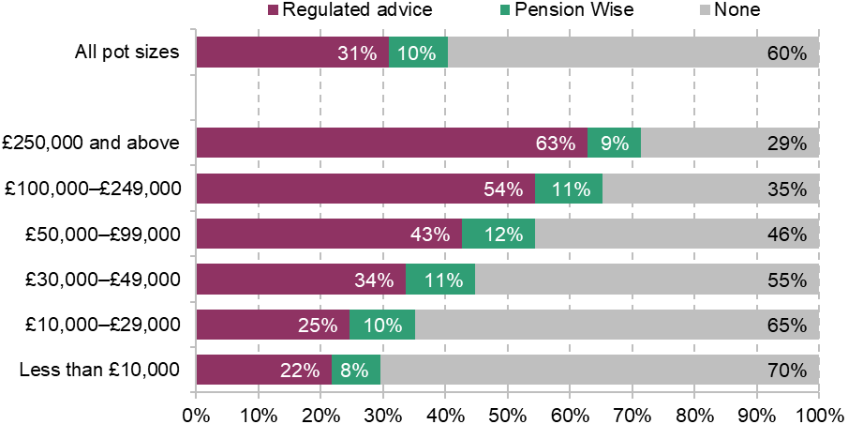

At the point of accessing a pension, the majority of people do not use either regulated advice or guidance from Pension Wise (a free government service offering guidance on pension options for people aged 50+), despite the complexity of the access decision, and the adverse consequences of making poor decisions. Six in ten DC pots accessed for the first time were accessed by people who had not used any guidance or advice, as Figure 2.7 shows. While the share accessing guidance or advice rises with pension pot size, a significant proportion even of those with the highest-value pots do not use advice. Three in ten DC pots worth £250,000 or more were accessed by people who had used neither guidance nor advice.8

Figure 2.7. Use of advice or guidance when first accessing pension, 2023–24

Source: Authors’ calculations using Financial Conduct Authority retirement income market data, September 2024.

In a focus group of 20 people who had recently retired, run by Ignition House in parallel to the Pensions Review, only around half had heard of Pension Wise. Their opinions of the service when told about it were generally positive, suggesting that one factor pushing down the share of people who access guidance might be a lack of awareness.

I am totally unaware of Pension Wise. So I’m not sure how it works exactly but if it is impartial and free, it cannot be a bad option to take in the first instance.

Male, aged 70–74, retired, homeowner

The lack of knowledge about Pension Wise is also apparent in other focus groups run among those in their 50s and 60s (e.g. Overton and Smith, 2022). This other qualitative research does reveal some limitations experienced by those who have actually used Pension Wise, though, with dissatisfaction that Pension Wise – as guidance – cannot use personal information about users to give any recommendations or personalised support. We discuss these limitations – and proposed ‘middle way’ solutions between impersonal guidance and expensive regulated advice – in our accompanying policy report (Boileau, Cribb and Emmerson, 2025).

Summary

The rise in participation in defined contribution pension arrangements, particularly since the introduction of automatic enrolment, is well known. But while the fraction of people approaching retirement with DC pension wealth has been rising, the importance of DC pension wealth is growing much more gradually. Most, but not all, people currently approaching state pension age will make only low-stakes decisions with their DC pension wealth. Perhaps partly as a result of this, most people accessing these pensions do not use either regulated advice or government guidance when doing so. Over time, however, average levels of DC pension wealth upon retirement will continue to rise, and the reliance on DB pensions, which guarantee an income through retirement, will fall for those who do not spend significant periods of their careers in the public sector. Importantly, even people on relatively low earnings are likely to accumulate significant amounts of DC pension wealth to draw upon at older ages.

3. Patterns of wealth drawdown at older ages

The previous chapter documented key facts about the rise in DC pension wealth. Since 2015, upon reaching the age of 55 people have had complete freedom over how they can draw this DC wealth. Financial wealth and housing wealth can also be drawn on relatively flexibly in retirement; housing wealth in particular is important in understanding overall trajectories of wealth through retirement (Blundell et al., 2016). In this chapter, we consider evidence on how different types of wealth are currently being drawn down in retirement.9

When examining patterns of wealth drawdown, it is worth noting there are two big-picture concerns about how people draw down on unannuitised pension wealth. The first is that people, particularly if they are present-biased or have unduly pessimistic expectations about how long they are likely to live, may draw down on their pension wealth too fast. In our experience, this is the primary policy concern in this area amongst UK stakeholders. However, there are also a set of concerns about people drawing down pension wealth too slowly, with people potentially being unnecessarily austere. In the United States, where people have historically held more unannuitised pension and financial wealth than in the UK, this has often been a key concern.10 We discuss in more detail the financial risks that individuals face in Chapter 4.

Key fact 5. Pension freedoms changed patterns of drawing on DC wealth. Few buy annuities and most access their pots before state pension age.

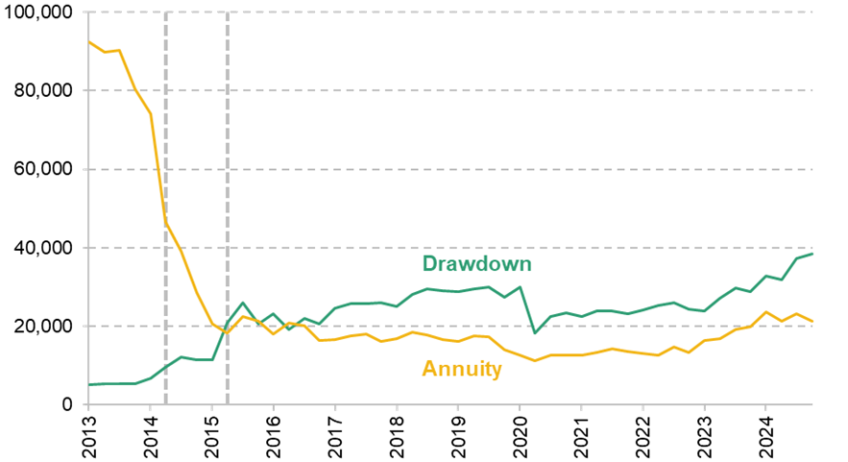

Since the announcement of ‘pension freedoms’ in 2014 and their introduction in April 2015, annuity purchases have fallen significantly.11 Figure 3.1 shows that annuity purchases declined in particular following the announcement (but before the introduction) of pension freedoms. Overall, the number of annuities sold fell by three-quarters between 2013 and 2024, while drawdown purchases have rapidly increased. Unsurprisingly, annuity purchases show some relationship with annuity prices – as interest rates and government bond yields have risen since 2021, and annuity rates have commensurately improved, the number of annuities purchased has risen, increasing by 56% from the final quarter of 2021 to the same quarter in 2024, but levels are still very low compared with the early 2010s.

Figure 3.1. Number of annuity and drawdown purchases

Note: Dotted lines show the announcement of pension freedoms in April 2014 and their subsequent introduction in April 2015.

Source: Authors’ calculations using Association of British Insurers quarterly pension annuities 2024Q4 and quarterly new long-term business (pensions) 2024Q4. Copyright of the ABI.

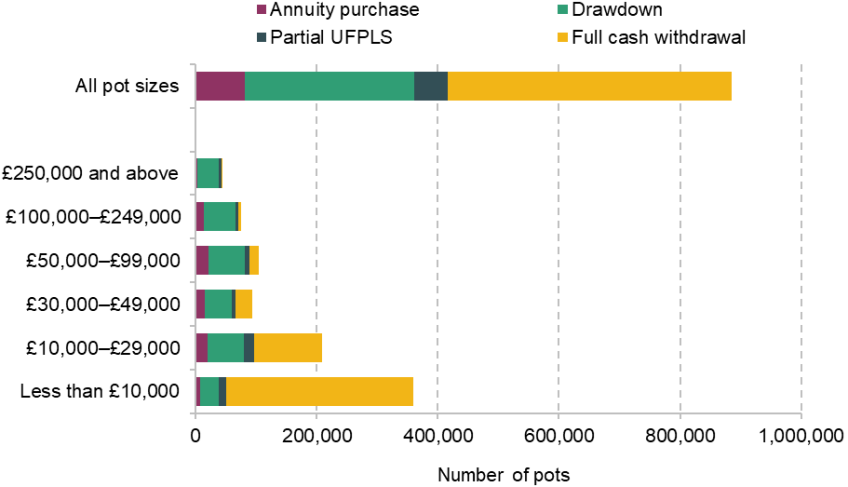

In 2023–24, withdrawing DC pensions in full represented the most common method of accessing pensions for the first time. More than half (53%) of pensions accessed for the first time were fully cashed out. A further 32% were used to buy a drawdown product, with 9% used for annuity purchase. The remaining 6% of pensions accessed for the first time were accessed as an ‘uncrystallised funds pension lump sum’ (UFPLS), a way of drawing down on pension wealth while receiving tax relief on 25% of each withdrawal. As is shown in Figure 3.2, these patterns differed considerably by pot value. Across the pot value distribution, the prevalence of annuity purchase rose from 2% of pots worth less than £10,000 to 21% of pots worth between £50,000 and £100,000, falling again for more valuable pots (to 8% of pots worth £250,000 and more).

Figure 3.2. Method of first accessing DC pension pot, by pot size, 2023–24

Note: Partial UFPLS (uncrystallised funds pension lump sum) is where individuals take out a set of lump sums from their pension pots, receiving tax relief on 25% of each withdrawal (and paying their marginal rate of tax on the other 75%).

Source: Authors’ calculations using Financial Conduct Authority retirement income market data, September 2024.

The prevalence of both drawdown purchase and partial UFPLS purchase also rose across the pot value distribution – 8% of pots first accessed worth under £10,000 were used to purchase a drawdown product, rising to 81% of pots first accessed worth £250,000 or more, while 4% of pots first accessed worth less than £10,000 were used for a partial UFPLS withdrawal, compared with 10% of pots worth £250,000 or more. Meanwhile, the share of pots first accessed in 2023–24 and fully cashed out fell from 86% of pots under £10,000 to 1% of pots over £250,000.

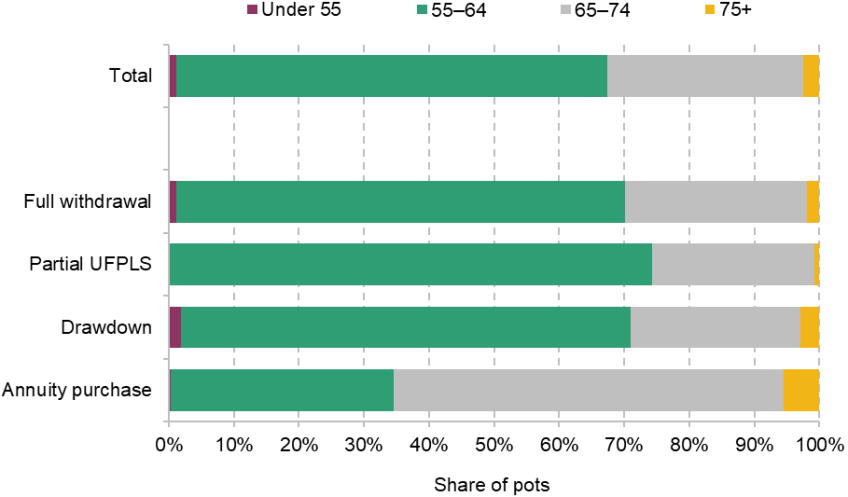

Figure 3.3 shows that around two-thirds of DC pension pots first accessed in 2023–24 were accessed by those aged under 65. Those purchasing an annuity were typically older – only 35% of those first accessing their pension and buying an annuity were under 65. Between 70% and 74% of those accessing their pension in other ways accessed their pension before age 65. 70% of those who fully withdrew their pension pots were under 65.

Figure 3.3. Age at first accessing pension, by mode of withdrawal, 2023–24

Note: Partial UFPLS refers to a partial uncrystallised fund pension lump sum.

Source: Authors’ calculations using Financial Conduct Authority retirement income market data, September 2024.

These access rates also differed for pots of different values. 69% of pots worth less than £10,000 were accessed by those aged under 65 – this fell for more valuable pots, to 61% of pots worth between £100,000 and £249,000, before rising again to 68% of pots worth £250,000 and above. The fact that a high share of the most valuable pension pots were being accessed by those aged under 65 is consistent with the fact that retirement before the state pension age is particularly concentrated among the wealthiest 20% of the population (Cribb, 2023).

In general, DC pensions are accessible from age 55 (rising to 57 by 2028). Although it is impossible from these data to know the exact age of access and how this has changed with the introduction of pension freedoms, there is a risk that private pensions become detached from the primary aim of financing retirement at older ages if pensions continue to be accessed at relatively young ages. Ideally, better data would be available for assessing this risk.12 If the majority are accessing their pensions at age 64, there would be fewer concerns than if many are accessing them at age 55.13

Overall, most people accessing DC pensions are accessing them before age 65 and are not using them to purchase annuities. Instead, they are accessing their pension wealth in ways that imply continuing active management of DC wealth over retirement. However, large pots are much more likely to be drawn down upon gradually, or annuitised, compared with the very large number of small pots that are accessed by withdrawing them in full.

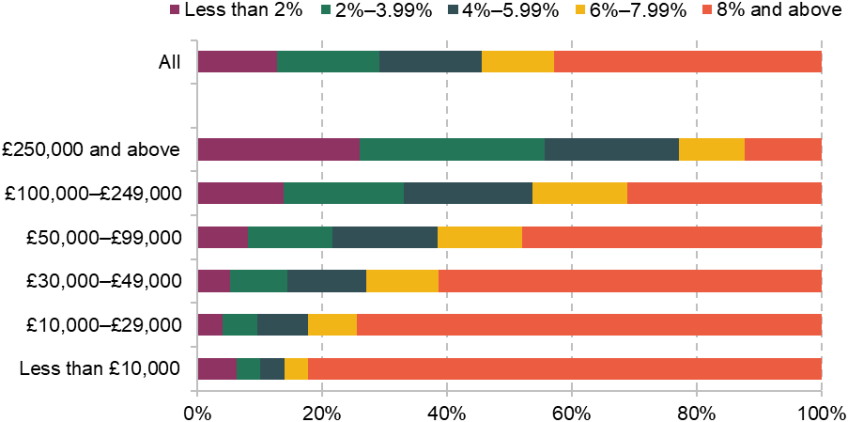

Key fact 6. Unannuitised pension and financial wealth is spent down slowly on average.

Drawdown rates for DC pensions vary a lot, as is shown in Figure 3.4. Overall, 13% of DC plans from which regular partial withdrawals were being made (around 528,000 plans) were being withdrawn at rates of less than 2%, and a further 16% were being withdrawn at rates of between 2% and 4%. This differed significantly by pot size: there were around 124,000 plans worth £250,000 and above from which regular withdrawals were being made in 2023–24. More than a quarter (26%) of these pots were being withdrawn at annual rates of less than 2% in 2023–24, and a further 30% were being withdrawn at rates of between 2% and 4%. If maintained, these rates are unlikely to lead to the exhaustion of a pension pot at or around death.

Figure 3.4. Share of plans from which regular partial withdrawals were being made, by rate of withdrawal, 2023–24

Source: Authors’ calculations using Financial Conduct Authority retirement income market data, September 2024.

12% of people with pots over £250,000 – relatively few, although a non-trivial minority – are withdrawing their pots at a rate of 8% or more. If maintained in real terms, starting at an 8% withdrawal rate would, on reasonable assumptions, be expected to exhaust a pot within around 15 years. This kind of risk is much less concerning for people with small pots (who are much more likely to have a high drawdown rate) where the absolute amount of income involved is small.

The question of the ‘right’ withdrawal rate from a DC pot is not one with a single correct answer. This will be determined by each person’s level of other wealth: for example, any other DC pots they have, whether they own their home outright, whether they have substantial DB pension wealth and their level of non-pension savings. It will be determined by their health, and – relatedly – their life expectancy, with higher withdrawal rates more suitable for those who expect to live for less long. It will be determined by whether they have a partner, and – if so – their partner’s own wealth and health. It will be determined by whether they have received, or expect to receive, an inheritance – and if so, how much they might receive and at what point. There are many other factors, too, that determine an appropriate withdrawal rate. Reflecting this complexity, the focus groups run by Ignition House revealed considerable uncertainty as to what drawdown rate might be sustainable, with several mentioning worries about running out of money too fast (which might drive some of the cautious withdrawal behaviour we observe in the data).

I’d like information on how long your money is going to last, and perhaps communication from the providers if it looks like you are taking out too much, too soon.

Female, 65–69, retired, homeowner

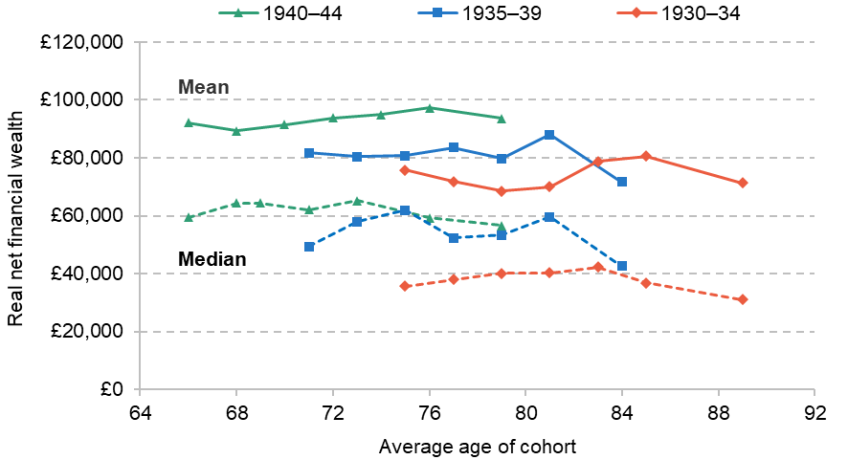

To some extent, the high share of the most valuable DC pension pots from which people are withdrawing at low rates might be motivated by the inheritance tax treatment of DC pension pots in 2023–24; at that point in time, DC pension wealth bequeathed at death was not subject to inheritance tax, creating an incentive to preserve pensions as bequests (Adam et al., 2022). However, as shown in Figure 3.5, non-annuitised financial wealth (held outside of pensions), which is not affected by the same distortionary tax incentives, is also drawn down slowly through retirement in the UK.

Figure 3.5. Mean and median net financial wealth, by age

Note: Solid lines connect mean wealth. Dashed lines connect median wealth. Each point represents data from a particular wave of ELSA, with average wealth plotted against the average age for each five-year birth cohort. For the calculation of mean wealth, only the middle 90% of the wealth distribution is included. All figures are in October 2024 prices. Our panel is balanced, including only individuals observed each wave.

Source: Authors’ calculations using the English Longitudinal Study of Ageing, Waves 4–10.

Figure 3.5 shows the trajectory of financial wealth at older ages among people born in the 1930s and 1940s, based on our analysis of data from the English Longitudinal Study of Ageing, an update of earlier work at IFS on financial wealth in retirement (Crawford, 2018a). The graph shows that median real net financial wealth for those born in 1930–34 declined by 13% between 2008–09 and 2021–23, and among those born in 1940–44 it declined by just 5%.

This pattern of slow wealth drawdown at older ages fits well with international evidence, such as from Australia, the US and other countries with significant DC wealth (see Pensions Policy Institute (2023) for a survey). International research often highlights the importance of bequest motives. In the Australian context, Asher et al. (2017) find that rates of drawdown are often slow, with the median pensioner passing away during their sample bequeathing 90% of the wealth with which they were first observed. In the US, new research from De Nardi et al. (2025) finds that bequest motives are the key driver of slow drawdown of wealth in retirement.

Key fact 7. Lots of wealth is tied up in owner-occupied housing.

Almost three-quarters of Britons in their 40s and 50s were homeowners in 2018–20, as Figure 3.6 shows. Although rates differed by region, with a higher share of those living in the South of England owning their own home (at 76% in the South East and South West), homeowners were the majority in each region. Even in London, which had the lowest share of homeowners, 60% of those in their 40s and 50s were homeowners.

Figure 3.6. Homeownership rates among people in their 40s and 50s, by region

Note: The data source covers Great Britain only.

Source: Authors’ calculations using the Wealth and Assets Survey, Round 7 (2018–20).

Homeownership, of course, has important implications for the level and composition of people’s wealth – and patterns of housing wealth have previously been identified as a key driver of why trends in drawdown of wealth in retirement have differed between the UK and the US (Blundell et al., 2016). As Figure 3.7 shows, the median value of homeowners’ main property among those in their 40s and 50s was around £250,000 in 2018–20. The differences by region are perhaps more substantial here, with London – unsurprisingly – standing out, but across all regions the value of homeowners’ main property was substantial.

Figure 3.7. Median value of main property among homeowners in their 40s and 50s, by region

Note: Data source covers Great Britain only. Prices are expressed in October 2024 terms.

Source: Authors’ calculations using the Wealth and Assets Survey, Round 7 (2018–20).

If drawn on, this housing wealth could have important implications. Drawing on housing wealth through retirement would increase the level of financial resources available; alternatively, the option to draw down on housing wealth in extremis could reduce some of the risks of running down private pension wealth faster than expected or of living longer than expected.

There are various ways of drawing down on housing wealth, including downsizing and formal equity-release products. Crawford (2018a) found that many people do release equity from their homes when they move at older ages, even if they are not moving for explicitly financial reasons (perhaps to be close to family). In addition, Crawford (2018b) found that around 40% of owner-occupiers moved home between age 50 and death. However, the actual amounts of wealth released when moving house at older ages tend to be fairly low: at the median, only 9% of property value is released, some of which will be taken up with moving costs. Even downsizing by buying a house with fewer bedrooms does not necessarily free up a lot of capital, though it could for some. Data released by the Office for National Statistics (2022a) suggest the median two-bedroom home was worth £45,000 less than the median three-bedroom home in 2021. In Northern Ireland and Wales in particular, the gap was even smaller – at £30,000 and £35,000 – though much more capital could potentially be released by downsizing within London or the South East, from a four-bedroom to a three-bedroom home, or by moving away from the high housing cost areas of Southern England in particular.

Formal equity release itself is relatively rare, with surveys showing only around 5% of retired households use equity release (Legal & General, 2022). Consistent with this, the prospect of downsizing, as well as other equity-release products, was unpopular in the focus groups that Ignition House ran, with interviewees typically viewing it as a ‘last resort’ rather than a popular plan for drawing upon wealth in retirement. Concerns about inheritance, and about the poor value represented by equity-release products, both came up in discussion in these focus groups. In 2018–20, our analysis of the Wealth and Assets Survey finds that only 2% of homeowners in their 40s and 50s who had not yet retired said they were planning to use a formal equity-release scheme to fund their retirement (while 23% planned to move to a less expensive property to release equity).

With high interest rates at this time, in my opinion, you could have nothing left to pass on. I believe equity release is the last resort.

Male, 70–74, retired, homeowner

Summary

We have set out key facts about how people draw down wealth in retirement in the UK. Since the abolition of near-compulsory annuitisation, few buy annuities, and instead they access defined contribution pension wealth typically either by withdrawing their (relatively small) pots in full or by going into drawdown. Pots are generally accessed before the age of 65. For those making withdrawals, significant numbers of people draw down on their larger pots relatively slowly, as financial wealth held outside pensions is also spent down slowly, consistent with evidence from other comparator countries. Housing is a large and important asset for many, and provides a potential ‘last resort’ for people who run out of other funds. But formal equity release is rare and, although a large minority move after the age of 50, in general the amounts of wealth released when people move are low.

4. Financial risks at older ages

The shift from DB to DC pensions, as discussed in Chapter 2, combined with the changes in DC access patterns associated with pension freedoms, as discussed in Chapter 3, create – or increase the importance of – a set of risks related to drawing down wealth in retirement. The increase in the risks borne by individuals in the pension system has been described by one professional body – the Institute and Faculty of Actuaries – as ‘the Great Risk Transfer’ (Institute and Faculty of Actuaries, 2021).

This chapter mainly examines the key risk relevant to individuals’ management of their wealth in retirement: longevity risk (the risk of living longer than expected such that individuals run out of private resources). It also briefly summarises some of the other risks faced, including those related to investment returns, cognitive decline, and the death of a spouse.

Key fact 8. Longevity is a key risk. Longevity is also improving, but with lots of heterogeneity.

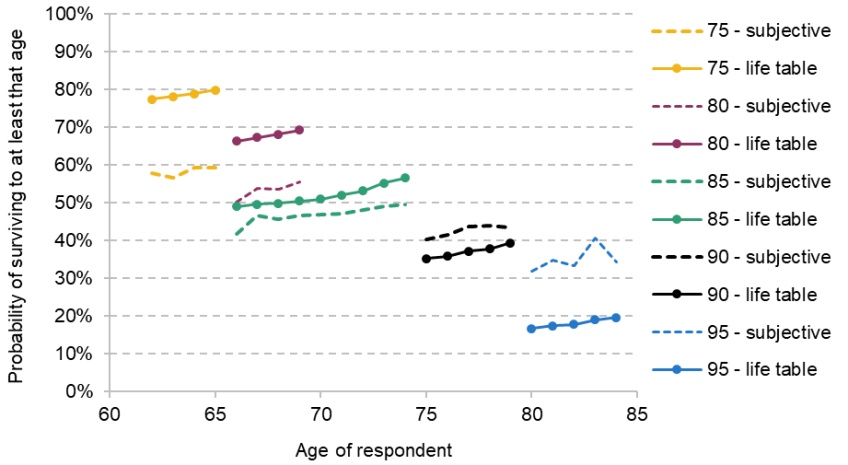

Life expectancy is one of the most important factors determining the management of resources in retirement. People’s subjective survival rate – the length of time they expect to live – will bear on the rate at which they should draw down from their pension, as will the uncertainty with which they expect to live to that age.

A key difficulty here in sensibly managing wealth in retirement is that people systematically misperceive their longevity during retirement (O’Dea and Sturrock, 2023). This is illustrated in Figure 4.1, which shows average subjective survival rates – the average probability individuals assign to living to a certain age – among men born in the 1930s, as well as showing ‘objective’ survival rates as given by ONS life tables. As shown, in these men’s 60s and early 70s, they underestimate their longevity, assigning a lower probability to surviving to a given age than is given by life tables. After their early 70s, though, they begin to overestimate longevity on average, assigning a higher probability of surviving to a given age than life tables imply. We see similar patterns among women born in the 1930s.

Figure 4.1. Average subjective survival rates compared with life-table survival rates, for men born 1930–39

Source: O’Dea and Sturrock, 2023.

This has implications for how these individuals might choose to manage their resources through retirement. Those in their 60s and early 70s might spend down resources ‘too fast’, if the aim is to exhaust their DC pot by the end of life, and might be especially reluctant to purchase an annuity priced based on life-table expectations of survival given that their expectations of survival are lower than these.

Over time, longevity is increasing, resulting in an increase in the number of years spent in retirement. Managing a pension pot over a longer period increases the complexity of decisions faced, since there are more potential outcomes in terms of inflation and rates of return (among other factors).

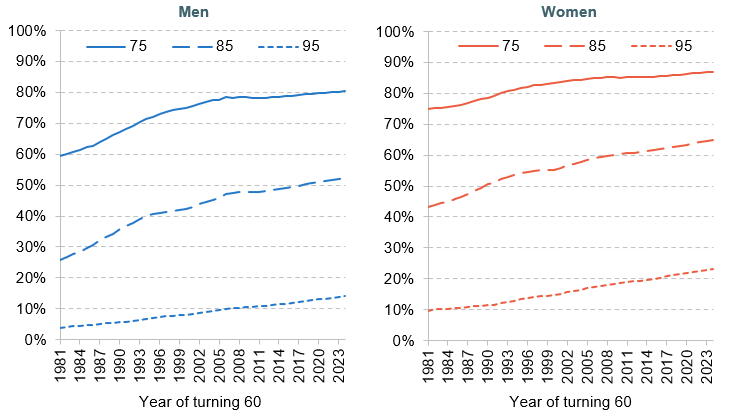

In particular, the probability of living to very old ages is rising rapidly. Figure 4.2 shows the probability that a 60-year-old will live to 75, 85 and 95, split by sex. The probability a 60-year-old man will live to 95 has more than tripled between 1981 and 2024, rising from 4% to 14%. The probability a 60-year-old woman will live to 95 has risen less dramatically, but has still more than doubled over this period, from 10% to 23%.

Figure 4.2. Probability that a 60-year-old survives to (a) 75, (b) 85 and (c) 95, by year of turning 60 and sex

Source: Authors’ calculations using ONS cohort life tables (2022-based).

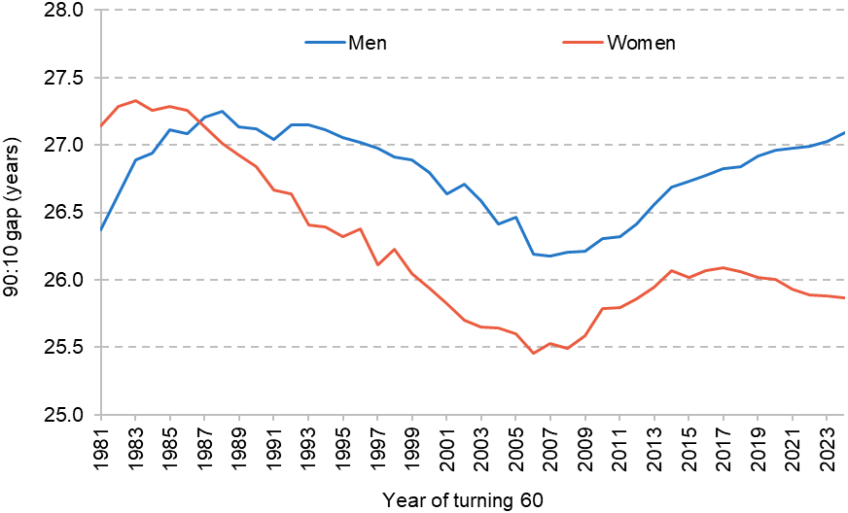

As well as the rising probability of living to these older ages, there have been changes over time in the uncertainty around life expectancy. One measure of this uncertainty is the gap between the 10th and 90th percentiles of life expectancy – i.e. the ages between which 80% of the population are expected to die. The wider this gap, the more uncertain (on this measure) is life expectancy.

Figure 4.3 shows the change in this gap between 1981 and 2024. Following a long period of this gap reducing from the 1980s to the mid 2000s, driven by the reduced probability of dying in people’s 60s and early 70s, the variation in life expectancy has been increasing since around 2007, notably for men. Growth in this gap since 2007 has been driven by the fact that the probability of living to much older ages (e.g. 95) has risen more rapidly in the last 15–20 years than the probability of living to relatively younger ages (e.g. 75) – conditional on being alive at 60 of course.

Figure 4.3. Gap between the 10th and 90th percentiles of life expectancy, by year of turning 60 and sex, among 60-year-olds

Source: Authors’ calculations using ONS life tables (2022-based).

With more variation in life expectancy, it is harder for decision-makers (whether those be individuals or anyone else) to choose appropriate drawdown rates for unannuitised pension assets. The implications for individuals turning 60 over time depend on how private information held at 60 about life expectancy has changed over the same period – but the wider variation may lead to greater uncertainty over remaining life expectancy.

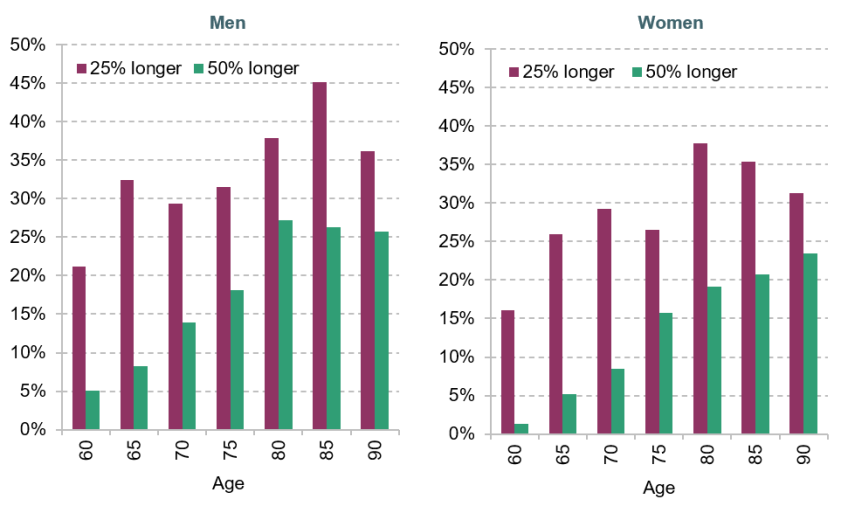

Relative uncertainty over life expectancy, based solely on sex and age, rises with age, as has been pointed out by LCP (2021). What do we mean by relative uncertainty? Figure 4.4 shows that 60-year-olds are much less likely to live 25% or 50% longer than their median life expectancy than are 75-year-olds or 90-year-olds. 16% of female 60-year-olds and 21% of male 60-year-olds in 2024 were expected to live 25% longer than their median life expectancy, compared with 31% of female and 36% of male 90-year-olds. This has important implications for drawdown strategies, and for the desirability of annuitisation at different ages. It means that the case for annuitisation is much higher at older ages than earlier in retirement because the probability of living much longer in relative terms than your life expectancy is much higher.

Figure 4.4. Probability of surviving (a) 25% longer and (b) 50% longer than median life expectancy, by age and sex, 2024

Source: Authors’ calculations using ONS life tables (2022-based).

Key fact 9. People with unannuitised wealth face investment risk through retirement.

People who do not purchase an annuity with their DC pension pot, but instead choose to draw down on it in other ways through retirement, leave themselves exposed to changes in the value of their investments. The extent of this investment risk will of course reflect the riskiness of the assets held. Different investment returns can have a considerable effect on how long a DC pot lasts through retirement, therefore interacting with longevity risk. The management and reduction of investment risk, alongside longevity risk and inflation risk, were recognised by NEST (2015) as crucial in its six guiding principles for a retirement income strategy.

To illustrate investment risk, Figure 4.5 considers a 67-year-old individual with a £100,000 DC pension pot, who chooses to withdraw their DC pot at an initial rate of 4%, 5% or 6% and keeps the amount withdrawn constant in real terms thereafter. Crucial in determining the outcome they experience will be the rate of return they experience on their invested pot. The graph shows the age at which they would exhaust their pot, assuming they receive a gross real annual rate of return of 3% (the squares) or 0% (the circles) and that charges effectively reduce these rates of return by 0.7 percentage points a year.

Figure 4.5. Age at which a pension pot is exhausted, based on different withdrawal rates and rates of investment return, assuming drawdown starts at age 67

Note: Circles represent a real rate of return of 0% and squares a real rate of return of 3%. Fees and charges are represented by subtracting 0.7 percentage points from the real rate of return, consistent with the modelling of O’Brien, Sturrock and Cribb (2024). Median life expectancy is measured at 67, using 2022 cohort-based life tables.

Source: Authors’ calculations using Financial Conduct Authority long-term return projections and ONS 2022-based life tables.

As shown, the different rates of return result in vastly different expected ages at which the £100,000 pot would be exhausted. Those withdrawing at an initial rate of 5% would exhaust their pot at age 93 if receiving returns of 3%, well above median life expectancy at age 67 for both men and women. Around 30% of 67-year-old women, and 20% of 67-year-old men, would be expected to reach age 93 and thus exhaust their pot before death. In contrast, if returns were 0%, those withdrawing at an initial rate of 5% would exhaust their pot at around age 86 – slightly below median life expectancy for men aged 67 (and well below median life expectancy for women aged 67).

If gross real rates of return were instead around 6%, those withdrawing at an initial rate of 6% would only exhaust their pot were they to reach around age 102. Those withdrawing at 5% or 4% would never exhaust their pot; their annual withdrawals would be smaller than their annual returns on investment.14 Being exposed to investment risk therefore allows for a much wider range of financial outcomes in retirement compared with annuitising wealth.

Key fact 10. Other risks increase with age – for example, cognitive decline and the death of a spouse/partner.

Older individuals face a range of other risks, including the risk of experiencing cognitive decline and the risk of losing a spouse.15 As well as harming their quality of life and well-being, these experiences can also affect their ability to manage their finances, which may make the management of unannuitised retirement wealth considerably more difficult.

To examine how cognitive function changes at older ages, we undertake a cohort-based analysis of individuals who have undertaken cognitive function tests in the English Longitudinal Study of Ageing (ELSA).16 Our first measure of cognition is a test of immediate and delayed word recall (see Figure 4.6).17 The mean number of words remembered in a memory test (out of 20) declined by 18% between ages 66 and 79 for those born in the early 1940s. From age 75 to 89 this cognition score declined by 26% (for those born in the early 1930s). This indicates a potential concern around people’s ability to manage complex decisions at older ages in retirement.

Figure 4.6. Average number of words remembered (out of 20), by age and birth cohort

Note: Each point represents data from a particular wave of ELSA, with the mean word test score plotted against the average age for each five-year birth cohort. Panel is balanced.

Source: Authors’ calculations using the English Longitudinal Study of Ageing, Waves 4–10.

Another measure of cognition is reading comprehension – measuring whether people can understand a set of instructions – which bears on whether people can shop around or can choose a reasonable strategy for managing their wealth, for example. Figure 4.7 shows that the average literacy score among those born in 1930–34 declined by almost a fifth between the ages of 71 and 89, and it declined by a tenth among those born in 1935–39, who aged from 67 to 84 on average, providing more evidence of within-cohort declines in cognition as people age.

Figure 4.7. Reading comprehension score (out of 4), by age and birth cohort

Note: Each point represents data from a particular wave of ELSA, with the mean reading comprehension score plotted against the average age for each five-year birth cohort. Panel is balanced.

Source: Authors’ calculations using the English Longitudinal Study of Ageing, Waves 2, 5 and 10.

The decline we find here means it is harder for people to manage their own financial decisions at later points in retirement. It matches a set of academic evidence, which has noted a worsening of financial mistakes with age (Agarwal et al., 2009). Angrisani and Lee (2019) chart an association between a household financial decision-maker experiencing cognitive decline and reductions in wealth. This is moderated somewhat among those with some annuity income.

Those who are widowed may face particular difficulties managing their finances. Crawford, Karjalainen and Sturrock (2022) find that when one partner in a couple passes away, the surviving spouse’s per-person spending may rise since shared costs, such as housing, remain unchanged. This places pressures on the surviving spouse’s finances. Poterba, Venti and Wise (2010) find in an American context that people in married couples tend to experience a large decline in wealth at the time of a divorce or the death of a partner, and wealth tends to grow more slowly thereafter than among those who have not experienced a separation. Asher et al. (2017) chart in the Australian context a similar association between losing a partner and experiencing large falls in assets.

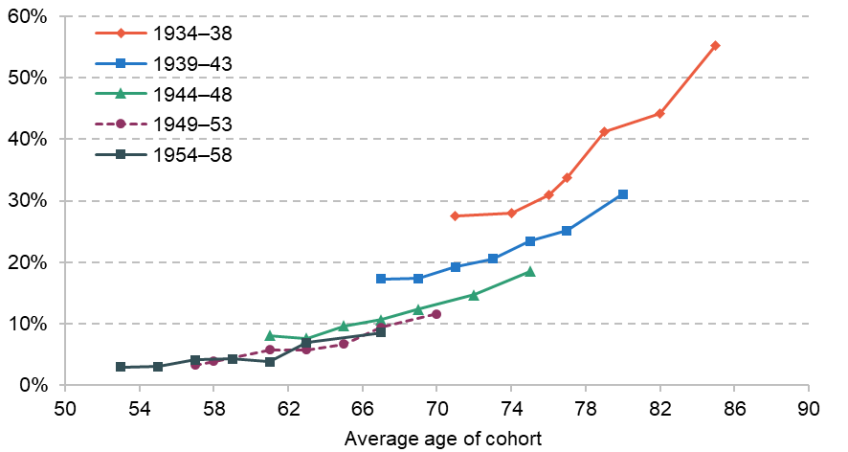

Figure 4.8 shows how the risk of being widowed rises with age, and differs considerably by sex, reflecting higher life expectancy for women as well as the fact that women tend to be the younger member of a couple. Among men born in the mid 1930s (1934–38), the proportion widowed rose from 7% to 18% between the ages of 71 and 85, whereas for women the proportion widowed rose from 27% to 55% over the same age range. This is particularly important because women are also less likely to be the key financial decision-maker within the household (Fonseca et al., 2012; Bertocchi, Brunetti and Torricelli, 2014). In a context with DB (or annuitised) wealth with survivor benefits, this problem is likely to be less severe, but in a context of rising levels of unannuitised wealth, it implies there may be more older people in the future who are less well equipped to handle complex finances.

Figure 4.8. Share of people widowed over time, by age, birth cohort and sex

Men

Women

Note: Each point represents data from a particular wave of ELSA, with the average share widowed plotted against the average age for each five-year birth cohort. Data are a balanced panel, including only those present in Waves 4–10.

Source: Authors’ calculations using the English Longitudinal Study of Ageing, Waves 4–10.

Concerns about the potential financial situation when a spouse dies were also mentioned in the focus groups that we are drawing on in this report, as shown below. Consistent with previous research, men were found to be more likely to take responsibility for household finances.

My wife is creative and a teacher. My background was financial. Accordingly, she managed the household, and I managed the money.

Male, aged 65–69, retired, homeowner

My husband used to say to me you’ll be okay when I die. My pensions will cover you. But it doesn’t pay anything now. And I was so surprised to find that out. I didn’t take a lot of notice of stuff like that, to be honest.

Female, aged 75–79, retired, private renter

Summary

Longevity at older ages has increased significantly over the last 45 years. Combined with the decline of annuitised pension wealth, this means people are increasingly at risk of outliving their financial resources and relying on state income and housing wealth. As people age, uncertainty over life expectancy grows, making financial planning more complex. Longevity risk is not the only important risk faced in retirement: other risks include investment risk, and the risk of cognitive decline which also makes it hard to make financial decisions. And widows often face additional financial difficulties, especially if their late spouse was primarily responsible for financial decisions.

5. Conclusion

This report has brought together key evidence – from government and industry statistics, existing research, focus groups, and new microdata analysis – showing the landscape people face when managing their financial resources in retirement. Managing defined contribution pension wealth in retirement presents significant challenges. Retirees must navigate multiple risks that can substantially impact their standard of living, most obviously longevity risk. These risks can lead either to financial hardship in later life or to overly cautious spending due to fears of running out of money.

Most people are currently making fairly low-stakes decisions with their defined contribution pension wealth. But as defined contribution pension wealth becomes more prevalent relative to defined benefit pensions for younger generations (Cribb, 2019), more people will face complex and important financial decisions at retirement. The number of people making high-stakes choices about their pension drawdowns is set to rise. Additionally, automatic enrolment has led to most pension wealth accumulating passively, meaning many individuals reach retirement with little prior engagement with their pension savings.

In this context, policymakers face multiple challenges in creating a framework to support good pension withdrawal decisions. The options available to policymakers, including some concrete suggestions, are discussed at length in the accompanying report (Boileau, Cribb and Emmerson, 2025).

Appendix. List of advisory group organisations

Age UK

Association of British Insurers

Behavioural Insights Team

Department for Work and Pensions

Financial Conduct Authority

Generation Rent

HM Treasury

Institute and Faculty of Actuaries

Institute for Government

Lane Clark and Peacock

Pensions and Lifetime Savings Association

Pensions Policy Institute

Trades Union Congress

Which?

References

Adam, S., Delestre, I., Emmerson, C. and Sturrock, D., 2022. Death and taxes and pensions. IFS Report, https://ifs.org.uk/publications/death-and-taxes-and-pensions.

Agarwal, S., Driscoll, J., Gabaix, X. and Laibson, D., 2009. The age of reason: financial decisions over the life-cycle with implications for regulation. SSRN Electronic Journal, https://doi.org/10.2139/ssrn.973790.

Angrisani, M. and Lee, J., 2019. Cognitive decline and household financial decisions at older ages. Journal of the Economics of Ageing, 13, 86–101, https://doi.org/10.1016/j.jeoa.2018.03.003.

Asher, A., Meyricke, R., Thorp, S. and Wu, S., 2017. Age pensioner decumulation: responses to incentives, uncertainty and family need. Australian Journal of Management, 42, 583–607, https://doi.org/10.1177/0312896216682577.

Banks, J. and Crawford, R., 2022. Managing retirement incomes. Annual Review of Economics, 14, 181–204, https://doi.org/10.1146/annurev-economics-051420-014808.

Barnard, H., 2023. How do we defuse the pensioner poverty timebomb? Joseph Rowntree Foundation, https://www.jrf.org.uk/savings-debt-and-assets/how-do-we-defuse-the-pensioner-poverty-time-bomb.

Bertocchi, G., Brunetti, M. and Torricelli, C., 2014. Who holds the purse strings within the household? The determinants of intra-family decision making. Journal of Economic Behavior & Organization, 101, 65–86, https://doi.org/10.1016/j.jebo.2014.02.012.

Blundell, R., Crawford, R., French, E. and Tetlow, G., 2016. Comparing retirement wealth trajectories on both sides of the pond. Fiscal Studies, 37, 105–30, https://doi.org/10.1111/j.1475-5890.2016.12086.

Boileau, B., Cribb, J. and Emmerson, C., 2025. Policies to help people manage defined contribution pension wealth through retirement. IFS Report, https://ifs.org.uk/publications/policies-help-people-manage-defined-contribution-pension-wealth-through-retirement.

Bonsang, E., Adam, S. and Perelman, S., 2012. Does retirement affect cognitive functioning? Journal of Health Economics, 31, 490–501, https://doi.org/10.1016/j.jhealeco.2012.03.005.

Cannon, E., Tonks, I. and Yuille, R., 2016. The effect of the reforms to compulsion on annuity demand. National Institute Economic Review, 237, R47–54, https://doi.org/10.1177/002795011623700116.

Crawford, R., 2018a. The use of financial wealth in retirement. IFS Report, https://ifs.org.uk/publications/use-financial-wealth-retirement.

Crawford, R., 2018b. The use of housing wealth at older ages. IFS Report, https://ifs.org.uk/publications/use-housing-wealth-older-ages.

Crawford, R., Karjalainen, H. and Sturrock, D., 2022. How does spending change through retirement? IFS Report, https://ifs.org.uk/publications/how-does-spending-change-through-retirement-0.

Cribb, J., 2019. Intergenerational differences in income and wealth: evidence from Britain. Fiscal Studies, 40, 275–99, https://doi.org/10.1111/1475-5890.12202.

Cribb, J., 2023. Understanding retirement in the UK. IFS Report, Pensions Review, https://ifs.org.uk/publications/understanding-retirement-uk.

Cribb, J. and Emmerson, C., 2020. What happens to workplace pension saving when employers are obliged to enrol employees automatically? International Tax and Public Finance, 27, 664–93, https://link.springer.com/article/10.1007/s10797-019-09565-6.

Cribb, J., Emmerson, C., O’Brien, L. and Sturrock, D., 2025. Small pension pots: problems and potential policy responses. IFS Report, https://ifs.org.uk/publications/small-pension-pots-problems-and-potential-policy-responses.

Cribb, J. and Karjalainen, H., 2023. How important are defined contribution pensions for financing retirement? IFS Report, https://ifs.org.uk/publications/how-important-are-defined-contribution-pensions-financing-retirement.

Cribb, J., Karjalainen, H. and O’Brien, L., 2023. The gender gap in pension saving. IFS Report, https://ifs.org.uk/publications/gender-gap-pension-saving.

De Nardi, M., French, E., Jones, J. B. and McGee, R., 2025. Why do couples and singles save during retirement? Household heterogeneity and its aggregate implications. Journal of Political Economy, 133, 750–92, https://doi.org/10.1086/733421.

Department for Work and Pensions, 2020. Pension freedoms: a qualitative research study of individuals’ decumulation journeys. DWP Research Report 995, https://www.gov.uk/government/publications/pension-freedoms-a-qualitative-research-study-of-individuals-decumulation-journeys.

Department for Work and Pensions, 2022. Planning and preparing for later life. https://www.gov.uk/government/publications/planning-and-preparing-for-later-life/planning-and-preparing-for-later-life.

Financial Conduct Authority, 2023. Financial Lives 2022 survey: pensions (accumulation and decumulation). https://www.fca.org.uk/publication/financial-lives/fls-2022-pensions.pdf.

Financial Conduct Authority, 2024. Retirement income data: April 2018 - March 2024, https://www.fca.org.uk/data/retirement-income-market-data-2023-24#full.

Fonseca, R., Mullen, K. J., Zamarro, G. and Zissimopoulos, J., 2012. What explains the gender gap in financial literacy? The role of household decision-making. Journal of Consumer Affairs, 46, 90–106, https://doi.org/10.1111/j.1745-6606.2011.01221.x.

French, E., Jones, J. B. and McGee, R., 2023. Why do retired households draw down their wealth so slowly? Journal of Economic Perspectives, 37(4), 91–114, https://doi.org/10.1257/jep.37.4.91.

Guy, A., 2024. Don’t wait for ‘pot for life’ pension reforms. interactive investor, https://www.ii.co.uk/analysis-commentary/dont-wait-pot-life-pension-reforms-ii531707.

House of Commons Work and Pensions Select Committee, 2022. Protecting pension savers – five years on from the pension freedoms: accessing pension savings. Fifth Report of Session 2021–22, https://committees.parliament.uk/publications/8514/documents/86189/default/.

Huppert, F., Gardener, E. and McWilliams, B., 2006. Cognitive function. In J. Banks, E. Breeze, C. Lessof and J. Nazroo (eds), Retirement, Health and Relationships of the Older Population in England: The 2004 English Longitudinal Study of Ageing, Institute for Fiscal Studies, https://ifs.org.uk/books/retirement-health-and-relationships-older-population-england-elsa-2004-wave-2.

ILC UK, 2021. Slipping between the cracks? Retirement income prospects for Generation X. https://ilcuk.org.uk/wp-content/uploads/2021/03/ILC-SLIPPING-BETWEEN-THE-CRACKS-3rd-March-Final.pdf.

Institute and Faculty of Actuaries, 2021. The great risk transfer: campaign recommendations. https://actuaries.org.uk/media/31hbykda/campaign-recommendations-april-2021.pdf.

LCP, 2021. Is there a right time to buy an annuity? Lane Clark & Peacock, https://www.lcp.com/media/1150053/is-there-a-right-time-to-buy-an-annuity.pdf.

Legal & General, 2022. The equity economy. Produced in association with the Centre for Economics and Business Research, https://cms.legalandgeneral.com/globalassets/adviser/over-50s-mortgages/document-library/articles/da1445.pdf.

NEST, 2015. The future of retirement: a retirement income blueprint for NEST’s members. National Employment Savings Trust, https://www.nestpensions.org.uk/schemeweb/dam/nestlibrary/the-future-of-retirement-blueprint.pdf.

O’Brien, L., Sturrock, D. and Cribb, J., 2024. Adequacy of future retirement incomes: new evidence for private sector employees. IFS Report, https://ifs.org.uk/publications/adequacy-future-retirement-incomes-new-evidence-private-sector-employees.

O’Dea, C. and Sturrock, D., 2023. Survival pessimism and the demand for annuities. Review of Economics and Statistics, 105, 442–57, https://doi.org/10.1162/rest_a_01048.