Downloads

Download report PDF

PDF | 535.83 KB

Executive summary

The current system of private pension savings in the UK is based on employers choosing a workplace pension provider, to which contributions from the employee and employer are sent, and which invests the contributions on behalf of the employee. This means that when an individual leaves their employer (or otherwise ceases to participate in the pension), pots become ‘deferred’ (not contributed to) and must still be administered by the pension provider. A substantial number of these deferred pots are very small, meaning that they are expensive to administer. And when an individual moves to a new employer, it is often the case that this leads to a new pension being opened. So over a lifetime an individual could end up with several deferred small pension pots, which are therefore hard for individuals to keep track of and to manage well. This report discusses the problems with this system and the merits of different potential policy responses.

Key findings

- The number of deferred small private pension pots is large and growing. In 2023, there were around 20 million defined contribution (DC) pension pots worth under £10,000 which are no longer being contributed to. In aggregate, these contained almost £30 billion. Over half of these pots, 12.1 million, were worth under £1,000, containing, in aggregate, over £4 billion of investments. These numbers have increased rapidly in recent years and are likely to continue to grow without policy action. For example, based on information from five large pension providers, the number of deferred pots worth less than £1,000 increased by almost two million from 2020 to 2023.

- The proliferation of these deferred small pension pots is burdensome for savers and pension providers. Smaller pots are uneconomical for pension providers, with there being some fixed costs of administering pots, leading to higher charges and therefore lower returns for savers. In addition, having several, or potentially many, small pension pots, rather than one big pension pot, makes managing saving and drawdown decisions harder for individuals, and increases the likelihood of them losing track of a part of their savings. The introduction of Pensions Dashboards, an online tool being developed by the government for people to access information about all their pensions in one place, should help people keep track of how much they have saved, but will not necessarily lead them to consolidate their pensions appropriately and make good saving and drawdown decisions.

- Lower earners and women are particularly likely to accumulate small pension pots. Our illustrative modelling exercise suggests that, over a nine-year period, almost three-quarters of pension pots accumulated by the lowest third of earners will be worth under £5,000, compared to one-fifth of pots accumulated by the highest third. Over half of pots accumulated by women will be worth under £5,000 compared to one in three pots accumulated by men. The key drivers of the generation of small pots are low levels of earnings (for example, through working part-time), low rates of pension contributions, and individuals moving from one employer to another.

- The status quo is not fit for purpose. We judge there is a strong case for deferred small pension pots to be consolidated by default, with people being given the option to opt out of this consolidation if they wish. This would reduce the stock of uneconomical pension pots, benefiting savers and providers. It could also make it easier for individuals to manage their pensions as they would be spread over fewer pots and, importantly, it need not change the administrative burden on employers. This could be implemented through the creation of a central clearing house.

- Individuals who have more than one pot with the same pension provider should have these pots automatically consolidated together. Individuals can have multiple pension pots administered by the same pension provider, for example relating to two or more different employment spells for different employers. These different pots can have different fee structures and individuals should ideally have all funds, regardless of pot size, consolidated into the pot that represents the best value for money. The case for this same-provider consolidation will become even greater if the DC pension market becomes more concentrated over time.

- Besides same-provider consolidation, there are a number of decisions to make about the implementation of automatic consolidation of deferred small pension pots, including which size of pots should be automatically consolidated. As smaller pension pots are typically more uneconomical to provide, the case for consolidation is strongest for the smallest pots. But also consolidating larger pots would lead people to have their savings spread across fewer pots as they approach retirement, which would help them make sensible decumulation decisions. There would nevertheless be a benefit to limiting the number of pots that are automatically consolidated initially to assess any potentially anti-competitive effects of the reforms on the market, as well as the costs associated with moving pots. Therefore, only deferred pots below £1,000 should be automatically consolidated initially, but this limit should ideally be raised over time and should also, in the long run, be subject to regular and frequent increases to avoid it falling behind inflation. It should also be easy for individuals to choose to opt into having their larger deferred pots consolidated too.

- Another key question for implementation is which pot the deferred small pots should, by default, be consolidated with. The two most sensible policy choices are either to use one of a set of government-approved consolidator arrangements (often referred to as ‘default consolidator’), or to consolidate into a member’s current pension (often referred to as ‘pot follows member’). Ultimately, these options have many similarities. In our judgement, both pot follows member and the default consolidator approach would be a significant improvement on the status quo.

- The choice between default consolidator and pot follows member interacts with the size limit for deferred pots. A higher size limit in the default consolidator model would lead to more pots being consolidated into a small number of funds – this anti-competitive effect might limit how high the limit can be set under this approach. Under pot follows member, raising the size limit indefinitely would eventually lead a member’s pension pot to always follow them when they change employer. This might have the benefit of increasing members’ engagement with their current pension, and it would ensure that their pension was not with an outdated provider, but there could be issues with the associated flow of funds between providers. This could be mitigated by having the limit increase once individuals are within, for example, ten years of reaching their state pension age, although it is not clear that the pension fund associated with the final employment spell would necessarily be the best destination for everyone’s pension savings. There are definitely advantages to the pot follows member approach, but the preferred policy will depend on the weight policymakers put on ensuring all individuals end up with a single pot by retirement as well as the government’s aims for the future structure of the DC market.

- Allowing employees to choose where their employer should send their pension contributions – ‘member choice’ – would also help prevent the creation of new small pension pots as employees using this option would likely ask their employers to send pension contributions to an existing pot if they have one. A ‘lifetime provider’ model takes this further by automatically having contributions for each employee sent to a ‘lifetime’ pot. These policies have merit if savers can choose a more appropriate pension plan for themselves than their employer. The lifetime provider model would ensure people end up with one DC pot at retirement without a significant constant flow of funds between providers. However, they would create extra hassle for employers, and could lead to increased fees, particularly for those with smaller pots. And there will be concerns that, left to their own devices, some will end up with a worse deal than what their employer would have been able to negotiate on their behalf. We judge that member choice and lifetime provider solutions should only be considered after fully implementing policies to consolidate deferred small pots automatically.

1. Introduction

The introduction of automatic enrolment into workplace pensions in the UK since 2012 has led many more private-sector employees to save into defined contribution (DC) pensions, with over 14 million employees saving in a DC pension plan in 2021.1 Under the current system, employers choose where to send their employees’ pension contributions, often enrolling all their employees into a plan with the same pension provider. This keeps the burden of arranging and administering pensions low for employers, which is especially important for smaller employers who might find this relatively more costly.

A consequence of this arrangement is that when an employee changes employer, their new employer will often enrol them into a plan with a different pension provider, creating a new pension pot. In fact, a new pension pot is still often created even if the new employer uses the same pension provider as the previous employer. As a result, and as discussed from the outset with the introduction of automatic enrolment (Emmerson and Wakefield, 2009), most private-sector employees are likely to accumulate several DC pension pots over the course of working life, some with relatively small amounts of money in them.

The proliferation of deferred small pension pots creates several issues. They are costly for providers to administer due to fixed costs for each pot, pushing up charges for individuals, and eroding the values of the pots. In addition, making sensible decisions during working life around how much to save and where to invest becomes more difficult if savings are scattered across several pots, some of which may not have been contributed to for several years. Deferred small pots are also easier to lose track of completely, with research from the Pensions Policy Institute (2024a) estimating that there are over three million ‘lost’ pension pots containing over £31 billion in assets, an increase from £19.4 billion in 2018.2 While the introduction of Pensions Dashboards, an online tool being developed by the government for people to access information about all their pensions in one place now scheduled for completion in 2026, should make it easier for savers to keep track of all their small pots, it does not solve the problem that they are costly for providers to administer.

Deciding how to access pension wealth through retirement is also made more complicated if it is spread across several pots. More than four in ten individuals in their 50s and early 60s with DC pension pots already report that they ‘don’t know’ how they plan to use them (Cribb and Karjalainen, 2023). With more people accumulating more deferred pots over time as they spend a greater proportion of careers under automatic enrolment, these decisions on how to access pension wealth become more consequential, and more difficult as the average number of pots that people have rises.

The scale of the small pots problem is large, as shown in Figure 1, and growing over time. Evidence reported to the Department for Work and Pensions by pension providers suggests that there were 12.1 million deferred pension pots worth less than £1,000 as of 2023, and another 7.8 million worth between £1,000 and £10,000 (Department for Work and Pensions, 2023a). In aggregate, the value of assets in these deferred small pension pots is not trivial, at just over £4 billion for pots worth less than £1,000 and over £25 billion for pots worth between £1,000 and £10,000. In comparison, aggregate assets in the DC pension market as a whole are estimated at around £650 billion (Pensions Policy Institute, 2024b).

Figure 1. Number and value of deferred pension pots worth under £10,000, in 2023

Source: Provider data from Department for Work and Pensions (2023a).

The number of deferred small pots has grown over time: between 2020 and 2023, the number of deferred pots worth less than £1,000 held with five large pension providers increased from 8.3 million to 10.2 million (Department for Work and Pensions, 2023a). This growth could accelerate should the government make use of legislation passed last year – the Pensions (Extension of Automatic Enrolment) Act 2023 – to reduce the minimum eligibility age for automatic enrolment from 22 to 18, although reducing the lower threshold of qualifying earnings would increase the size of pots created in future.3

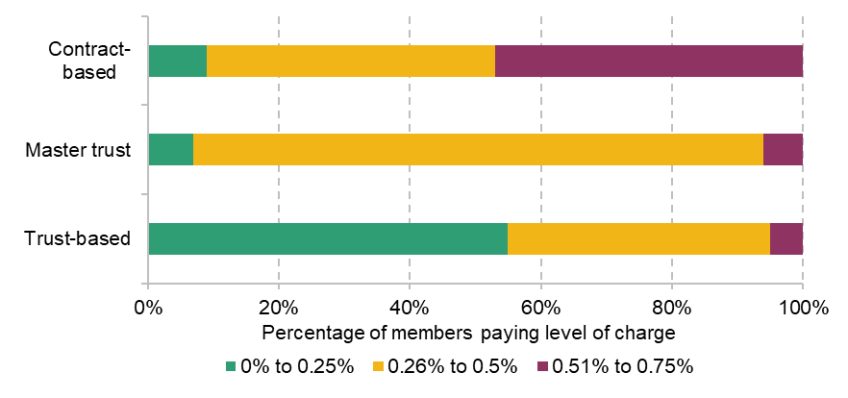

The pension provider that administers an individual’s pension savings is important, in particular as management fees and investment performance vary. The variation in fees arises despite the cap on charges for pension providers that can be used for automatic enrolment (qualifying arrangements) to 0.75% of funds under management since 2015. While this led to a reduction in fees overall, there is still variation in the fees charged by different pension plans, as shown in Figure 2 (Department for Work and Pensions, 2021). Almost half of members of contract-based qualifying arrangements had ongoing charges of between 0.51% and 0.75% of funds under management, while over half of members of trust-based arrangements had ongoing charges of no more than 0.25%.

Figure 2. Percentage of qualifying-plan members paying different levels of ongoing charge (% of funds under management), by pension type

Source: Table 3.5 of Department for Work and Pensions (2021).

Crawford, Emmerson and Ogden (2022) show that fees for deferred pensions are typically much higher than fees of qualifying arrangements today. The average annual fee for deferred pensions taken out in the 1990s is over 1.1% of fund value, and this is not offset by better returns for these pensions. A 50-year-old with a deferred pot of £21,000 might be expected to have £2,000 less in their pension when they reach their state pension age of 67 with an annual fee of 1% compared to 0.75%, assuming annual investment returns of 7.7% in both cases.

The rest of this report proceeds as follows. In Section 2, we provide new evidence on which employees are more likely to accumulate deferred small pension pots based on analysis of longitudinal individual-level data. In Section 3, we discuss the merits of different options facing policymakers looking to solve the small pots problem, and provide our judgements on which might be most appropriate, with maintaining the status quo not being seen by us as a sensible way to proceed. Section 4 provides a short conclusion.

2. Which groups accumulate more small pots?

The scale of the proliferation of deferred small pension pots is widely appreciated thanks to information supplied by pension providers; however, these data generally do not allow us to link pension pots from different providers to the same individual, nor do they provide demographic information on savers. As a result, relatively little is known about which groups of employees consistently tend to accumulate more deferred small pots, and therefore might find it more difficult to manage their pension saving during working life and retirement.

In this section, we present the results from new analysis of household-level microdata to help address this knowledge gap. We first examine which groups are particularly likely to join a new pension pot over the course of a year, before estimating the distribution of accumulated pot sizes over a longer time period by various characteristics. To do this, we use Understanding Society (see University of Essex, 2024), a household survey dataset of around 40,000 UK households that collects detailed information on respondents’ demographic characteristics and their employment situations. Importantly, this dataset is longitudinal, meaning we can follow the same respondents over time as they move in and out of employment and change employer.

We begin by showing which employees are more likely to have contributed to a new DC pension pot over the course of a year. To do this, we focus on wave 10 of Understanding Society, which contains data from 2018 to early 2020, to avoid any temporary changes to the share of people changing employer that occurred during, or in the immediate aftermath of, the COVID-19 pandemic. We take a sample of private-sector employees aged 22–65 who are eligible for automatic enrolment (AE-eligible; i.e. earning over the equivalent of £10,000 per year and have worked for their employer for at least three months), who also responded to wave 9 of the survey, and we plot the share who started working for their wave-10 employer in the past year. This will proxy the share of employees who accumulated a new DC pension pot over the course of a year, although it will slightly overstate this share as it does not account for people opting out of (or otherwise not joining) a pension plan.4

Figure 3 shows that there are significant differences in the proportion of different groups who started working for their employer in the past year, and therefore who will likely have accumulated a new pension pot. There are particularly large differences by age, with 22% of AE-eligible private-sector employees aged 22–34 having joined their employer in the past year, compared to 11% of those aged 50–65. Lower earners and women are also more likely to have joined their employer recently than higher earners and men, respectively. This suggests that these groups (younger employees, lower earners and women) are more likely to accumulate new DC pension pots.

Figure 3. Share of AE-eligible private-sector employees who joined their employer in the past year

Source: Authors’ calculations using Understanding Society, waves 9 and 10.

We now turn to estimating the distribution of accumulated DC pension pot sizes over a longer time period, and how this varies for different groups. This analysis accounts for the fact that people can spend periods when they are not saving in a workplace DC pension, for example when they are out of paid work, working in the public sector (where defined benefit pensions are prevalent) or working in self-employment (where levels of private pension participation are very low). It might also be the case that some who change employers one year are also more likely to change employers the next year, and these employer changes can also be correlated with how much people earn, all of which can affect the distribution of accumulated pension pots.

We take the set of people who answered all waves 2 to 10 of Understanding Society (i.e. from 2010 to 2020), were initially aged between 22 and 58 in wave 2, and who worked as an AE-eligible private-sector employee in at least one wave.5 We follow them over time, modelling contributions into DC pension pots as 8% of their annual qualifying earnings in periods where they work as an AE-eligible private-sector employee. We assume a new pot starts every time the individual starts work with a new private-sector employer in an AE-eligible role.

These numbers are somewhat illustrative for three reasons. First, we only observe people yearly in Understanding Society. As a result, we miss some of the shortest employment spells, where an individual works for a few months for a given employer between survey interviews. This will cause us to underestimate the number of particularly small pots, although this will be mitigated by the fact that employers can delay automatically enrolling new employees for three months. Our assumption that employees work for their employer at the time of interview for the whole year might also lead us to underestimate the number of very small pots.

Second, these numbers assume that no employee opts out of automatic enrolment, and that all employees contribute the minimum default amount. The latter assumption will cause us to underestimate the size of pots, as average contributions to DC pensions are higher than the automatic enrolment minimums. Third, we only model contributions made during a nine-year period. We do not model whether contributions made during this period flow into a pot that already existed before the start of the nine years, or that will continue to be contributed to after the end of the period.

With these caveats in mind, Figure 4 shows the distribution of accumulated DC pension pot sizes for different groups. Overall, we find that 7% of accumulated pots are worth less than £1,000 and 35% are worth between £1,000 and £5,000. The current stock of deferred pots, shown in Figure 1, has a higher share of pots worth less than £1,000. In part, this will be because we miss some particularly small pots, which are accumulated between survey interviews. In addition, some of the difference could come from some of the current stock of DC pension pots worth less than £1,000 being accumulated when minimum automatic enrolment contributions were very low – in particular, from 2012 to early 2018, minimum total contributions were only 2% of qualifying earnings.

Figure 4 also highlights that women and lower earners are more likely to accumulate small DC pension pots. Around half of pots accumulated by women over the nine years are worth less than £5,000, compared to 32% of pots accumulated by men. In addition, 72% of pots accumulated by those in the lowest earning third are worth less than £5,000, compared to just 21% of pots accumulated by those in the highest earning third. Younger adults are also slightly more likely to accumulate small pots than older people, although the differences are not as stark as the differences in job mobility between age groups displayed in Figure 3.

Figure 4. Distribution of accumulated DC pension pots over a nine-year period, based on minimum pension contributions

Source: IFS calculations using Understanding Society.

Overall, the evidence in this section highlights that women and lower earners are more likely to accumulate smaller pension pots and so could be particularly likely to benefit from policies that lead to consolidation. People are also particularly likely to change employers at younger ages, thereby accumulating more deferred pots. A reduction in the lower age limit for automatic enrolment eligibility – which an earlier report from the Pensions Reviewhas suggested would be beneficial and therefore should take place – would thus, under current arrangements, further exacerbate the small pots problem.

3. Potential policy responses

In response to the problems created by the proliferation of deferred small pension pots, two types of policies have been put forward. The first includes policies to consolidate – at least by default – the existing stock, and subsequently the future flow, of deferred small pots. As we discuss, there are different models for this. The second type of policy aims to reduce the creation of new pension pots more directly, by giving employees the right to have their employers send pension contributions to a nominated pension plan. This is referred to as ‘member choice’ and can be strengthened by specifying nominated arrangements to be existing pension pots by default. In this section, we discuss these two types of policies in turn, discussing options for implementation and the trade-offs they bring.

Consolidation of deferred small pots

The first type of policy proposal would address the stock of deferred small pots. This would consolidate the current stock of deferred small pots, and future small pots would also then eventually be consolidated once they became deferred (i.e. inactive for at least a given period, generally considered to be one year). This consolidation would happen by default, with savers having the option to opt out. In practice, this might mean that once a small pot has been inactive for a year, savers would be sent a letter informing them that their pot will be automatically consolidated unless they respond within, say, three months, to opt out. There are several other decisions to make about how this policy would be implemented, which we now discuss.

Which pot are they consolidated with?

A decision would need to be taken on which pot to consolidate deferred small pots with. There are two main options that have been put forward on this.

The first option is to consolidate deferred pots with savers’ current active pension pot. This is commonly referred to as the pot follows member or ‘magnetic pensions’ approach (Webb, Myers and Box, 2024). The Pensions Act 2014 gave the government powers to implement this system; however, it was never actually put into effect.6

One advantage of this approach is that it could increase member engagement with their current pension pot, as it will increase the amount of money, and the share of the member’s total pension savings, contained in the pot. One potential disadvantage is that some members could lose out if their deferred pensions are consolidated into worse-value arrangements. Of course, by the same token, members could also gain if their current pension provides better value for money than the deferred pot that is consolidated into it. Indeed, average fees have fallen over time, suggesting that current pots should, on average, have lower charges than deferred pots (Department for Work and Pensions, 2021). However, should this remain a concern, current pots could be restricted to be consolidated only into arrangements meeting certain value-for-money requirements.

The second option is known as the multiple default consolidator model. The previous Conservative government indicated this to be its preferred approach to solving the small pots issue in its response to a public consultation in 2023 (Department for Work and Pensions, 2023b). Under this approach, the government defines a set of authorised pension plans to act as default consolidators. Then, when a pot becomes deferred, it is by default consolidated with one of these approved default consolidator plans. By only consolidating pots with an approved list of arrangements, this should ensure that deferred small pots are not consolidated with one that provides poor value for money.

If the member does not have a pot with one of the default consolidator arrangements, then the proposal was that the pension into which to consolidate the pot would be chosen randomly. If the member already has one pot with one of these providers, then the deferred pot would be consolidated into this existing pot. If the member has more than one pot with an authorised provider, then under the previous government’s proposal, the deferred pot would be consolidated with the largest of these. However, another option would be for the member’s currently active pot to take precedence in this scenario, conditional on this pot being administered by an authorised provider. This then becomes more similar to the pot follows member approach suggested earlier in this section.

Under the multiple default consolidator model, a decision would have to be made on the number of authorised providers. If this number is small, then increasing the limit for which pot sizes are eligible for automatic consolidation could start to have an anti-competitive effect on the pensions market, as more and more pots would be moved into a small number of different arrangements, leading to a very small number of providers dominating the market. This could limit the scope for the threshold for automatic consolidation to be increased (which would help bring about a single – or at least a small number of – DC pension pot(s) for each individual upon retirement). More broadly, both the multiple default consolidator model and the pot follows member model would affect existing providers relative to the status quo in different ways, depending on their current and past market share, the extent to which their members tend to accumulate small pots, and whether or not they were an authorised consolidator or not.

Ultimately, however, these two approaches share many similarities, and they can be modified to incorporate the advantages of each. They would both reduce the stock of expensive-to-administer small pots, benefiting members as lower costs lead to lower fees, without imposing large extra costs on employers. Either option could be rolled out starting with only the smallest pots, and then increasing the level below which pots are consolidated, as discussed in a subsequent section; though, as noted above, choosing the multiple default consolidator approach might limit how high this level can be raised if the number of authorised consolidators is small, given the impact it would have on market structure. On the other hand, if the limit below which pots are consolidated remained low in pot follows member, people might be more likely to end up with several pots worth just more than the consolidation limit, as the pots would stop following them once they passed the limit. This would be less likely under the multiple default consolidator approach, where all small pots would be consolidated into the same consolidator pot.

Other options for which pot to consolidate with have larger downsides. Consolidating deferred pots into the first pension pot the member ever had is unlikely to be a good option, as charges were typically higher in the past, and because the first pension a member had may have been from several decades ago and might not reflect the type of arrangement the member would want to save into today. For example, it could lead to many graduates accumulating, at least by default, their DC pension wealth in an arrangement that was set up by an employer for whom they worked part-time while studying. Another approach is the single default consolidator model, which is similar to the multiple default consolidator model, except there is only one authorised default consolidator plan. While this would share some of advantages of the multiple default consolidator model approach, the anti-competitive effect on the market would be larger with a single authorised provider, further limiting how high the limit for pot consolidation could be raised. While either of these options has attractions relative to the status quo, we suggest that a better option should be pursued.

How would consolidation work?

A key practicality to consider is how the consolidation process would actually work. At present, a pension provider cannot see the deferred or active pots its member might have with other providers, making automatic consolidation of pots infeasible under current infrastructure. There are two possible options to overcome this hurdle and support the consolidation process.

The first option is the creation of an independent central clearing house responsible for matching deferred pots and communicating with members and pension providers. Alternatively, a central registry could be created, which would act as a database allowing providers to observe all the pension pots a saver has with other providers. Providers could then access this information in order to match their member’s deferred pot to the relevant consolidator plan themselves, with providers retaining responsibility for communicating all relevant information with members. There would be costs to creating and maintaining a central clearing house that would need to be funded appropriately. However, it would make the consolidation process simpler for providers in the long run.

Whichever option is chosen, it would seem sensible to build on the work done as part of the Pensions Dashboard in matching savers’ pots across providers. This has been far from straightforward because, although in principle it should be possible to link pension pots to the same person through names, dates of birth and National Insurance numbers, errors and incompatibilities in how these are put into different pension providers’ data systems can hinder the matching exercise. It would therefore be wasteful to repeat all the work done for the Pensions Dashboard when creating a clearing house or central registry, rather than utilising this platform.

What size of pots should be consolidated?

One of the key points of discussion in the Department for Work and Pension’s 2023 consultation on ending the proliferation of deferred small pots was how to define which pots are sufficiently small that they should be automatically consolidated. The consultation asked whether the size limit for automatic consolidation should be £1,000, £2,000, £5,000 or £10,000, and some respondents suggested other limits too.

Given that one of the key motivations for consolidating small pots is that they can be uneconomical to provide, thereby leading to higher charges for members, the case for consolidation is strongest for the smallest pots. In addition, there might be a benefit to setting a relatively low limit to consolidation initially to ensure that the system works well and to assess the effect of reform on the market and the costs associated with consolidating pots. These considerations therefore point to starting with a relatively low limit, of, say, £1,000. Even this low level would require 12.1 million pension pots, with an aggregate value of £4.2 billion to be consolidated safely.

This limit should increase over time, at the very least periodically, to account for inflation. But there are good reasons to go further than this. Part of the rationale for the consolidation of deferred pots is to facilitate good decisions when saving for retirement and when drawing down this saving at older ages. This might still be difficult if people have pension savings spread over several, or many, different pots worth over £1,000.7

Indeed, given how complicated decisions over how to draw down wealth in retirement are, there is an argument that it should be made as easy as possible for people to end up with all their DC savings in one pot as they reach retirement. This points towards – once the system is up and running and has been seen to be working well – increasing the limit for automatic pot consolidation substantially, and potentially even eventually scrapping the limit entirely so that all pots are consolidated by default.

One issue that is raised, especially with a high (or infinite) limit, is that individuals could be consolidated into a scheme that has higher fees than their previous scheme, which would lead to lower accumulation of pension wealth over time.8 Although there would also be people who would benefit, having been consolidated into schemes with lower fees, there may be more concern from those who face higher fees than appreciation from those who see lower fees. There are a number of potential mitigations here, discussed below, including the potential for higher limits at older ages (meaning that larger pots are only automatically consolidated at older ages) as the compounding effects of higher fees are less stark over shorter time periods; and the potential for same-scheme consolidation of pension pots into the arrangement with lowest fees (see below).

Another potential concern is that, under a pot follows member model, this would then mean members’ entire pension savings would – again by default – move with them every time they changed employer and were enrolled into a new DC pension pot. Having this amount of money constantly moving through the system could create some problems and hinder long-term investments. However, there are two reasons to suggest this might not be a large issue. First, in a world with a smaller number of master trusts, the net balance of transfers between providers, which ultimately matters for pension investments, might not be so substantial in comparison to the overall inflows and outflows. Second, the workplace DC pension market in the UK is still relatively immature, meaning most funds are experiencing significant net inflows and have access to a large amount of liquidity. As a result, the flows caused by the pot follows member model would be unlikely to prevent them from investing in illiquid assets.

One option here would be to have a smaller pot size limit until, say, age 55, and then a much higher – or perhaps even no – transfer limit after this age, allowing pensions to be consolidated before retirement without a large number of transfers earlier in people’s careers. A key question then is whether the pension pot associated with an individual’s last employment spell would typically be a good destination for people’s pension savings.

This problem would not exist to the same extent in the multiple default consolidator approach, as deferred pots would be moved into people’s largest pot with an authorised provider, which would presumably change less over time. On the other hand, an infinite limit in the multiple default consolidator approach would have a greater anti-competitive effect because all pots would be consolidated into arrangements offered by a small number of approved providers.

Alternatively, the limit for automatic consolidation could remain fairly low, with individuals instead relied upon for making their own consolidation decisions. If this route is taken, policies should be put in place to help people consolidate their pots. For example, when people are informed about the automatic consolidation of a deferred small pot, as well as providing a method for opting out, they could also be given the chance to opt into having their larger pots consolidated too.

Even if the process of consolidating pension pots is not administratively difficult for individuals, people often have low confidence in what they are doing with pensions. This is not a financial decision that is made frequently, which means that most people consolidating their pensions will never have done it before. Given this, if the government decides to stick with a relatively low pot size limit for automatic consolidation, relying on individuals to make their own decisions on consolidating their pots further, there should be a simple step-by-step guide of how to do it on a trusted government website such as gov.uk.

Same-scheme consolidation of pension pots

The discussion above implicitly assumes that an individual’s different pension pots are administered by different pension providers. However, in practice, some individuals may have multiple pension pots administered by the same pension provider. This is most likely to occur due to an individual having employment spells with two or more separate employers who both use the same provider for their workplace pension scheme. While some providers may already be consolidating pots for individuals with multiple pension pots, others – potentially most – are not (as is discussed by the Department for Work and Pensions in its 2023 consultation).

Having multiple pots with the same provider can be confusing for individuals managing their pension wealth, and some may face different charges on their different pension pots with the same provider. And it can only be more expensive for the provider to administer than having the pensions combined – if only because separate statements have to be regularly issued. Such a situation seems rather ridiculous. Where there are two or more deferred pots with the same provider, there is an extremely strong case that these are automatically consolidated, ideally into the arrangement that represents the best value for money. Where this pot is not the one that is currently being contributed to, those contributions should just be rerouted into the pot that represents the best value for money. For same-scheme consolidation, it should not just be the smallest pots that are consolidated, but all pots. If it was felt that some people might not want this to happen, then individuals could be given the ability to opt out.

In November 2024, the government announced a consultation on proposals to legislate for a minimum size and maximum number of DC pension scheme default funds, with the aim of creating a small number of pension ‘megafunds’ (Department for Work and Pensions and HM Treasury, 2024). The case in favour of same-scheme consolidation will only increase if this happens, as more people would have multiple pots with the same provider. However, this would not obviate the need for a broader system of automatic consolidation of deferred pots, because, unless there were only one or two ‘megafunds’ with over 90% of the market, individuals could still easily build up a small pot with one provider, move employer, and never work for an employer using the same original provider.

Member choice and lifetime provider model

Automatically consolidating deferred small pots is one way to reduce the problems associated with their proliferation. However, it is not the only potential way forwards. In their 2023 consultation about ending the proliferation of deferred small pension pots, the previous Conservative government also indicated an interest in pursuing a ‘member choice’ or ‘lifetime provider’ approach for addressing the small pots problem (Department for Work and Pensions, 2023b). In this subsection, we describe these approaches and their potential benefits and drawbacks.

Member choice

Under member choice, workers would be given the right to tell their employers to send pension contributions to their nominated arrangement. This could prevent a new pot being created every time an employee changes employer, as they could tell their employer to send their pension contributions to an existing pension pot. This differs to the current model, where employers choose a pension scheme for their employees.

Member choice on its own could have some benefits. Individuals might be better placed than employers to choose a pension arrangement that fits their preferences, and they could become more engaged with their current pension if they have more choice over where their contributions are going. However, on its own, it is unclear whether many employees would actually take the option to send their pension contributions to an existing pot rather than sticking with the default suggested by the employer, especially given the relatively high current level of disengagement with pensions among the UK workforce. This approach is therefore unlikely to do much to improve the small pots problem on its own, although it could be combined with automatic consolidation of deferred pots.

There are, however, some drawbacks to member choice. First, it would lead to higher costs for employers, who would potentially have to send their employees’ pension contributions to several different pension providers. This might be particularly burdensome for smaller employers, although this could be alleviated with the creation of a central clearing house responsible for receiving pension contributions from employers and sending them to the right pension plans. Employers do already have to send salaries to the bank accounts chosen by their employees, and it is not obvious that pensions should be any more complicated. Member choice could also lead to higher marketing costs, as providers compete to attract savers’ pension pots. As Webb et al. (2024) point out, average member fees in the Australian system, where savers can choose their superannuation plan, are over double those in the UK. There is also a worry that those with the largest pension pots could be particularly likely to deviate from their employer’s default pension arrangement, if they are inherently more active with their finances or particularly targeted by marketing (Ahern et al., 2024). This could lead to higher fees in default plans offered by employers, as employers lose bargaining power and there is less cross-subsidisation from higher earners with larger pots (which are cheaper to administer) to lower earners with smaller pots (which are more expensive to administer) within arrangements.

Lifetime provider model

The previous government opened a consultation about going further than member choice to a ‘lifetime provider’ model. This would still entail employees being given the right to tell their employees where to send their pension contributions; however, it also specifies a default nominated arrangement where all contributions would be sent for a worker’s entire career, rather than the default being left to the employer. Individuals might be allocated a pension by their first employer, but would be given the option to switch if they wanted.

Practically, the lifetime provider model is member choice with a member’s single ‘lifetime’ pension nominated by default. As a result, the benefits and drawbacks associated with member choice, as outlined in the previous section, would also apply to the lifetime provider model.

However, there would also likely be advantages to implementing a lifetime provider model over and above member choice. First, it would simplify the system significantly for savers, who would know where to find all their pension savings and would only have them move around when they wanted to switch provider. Second, pension providers would have better information about their customers’ total amount of pension wealth, and where it is invested, allowing them to provide better information and communication to members. Third, it could support the development of collective defined contribution pensions, as outlined in the government’s call for evidence, as individuals would by default have all their savings in a single pot that is not automatically transferred between providers.

It is important to point out that implementing a system of pot follows member, with no transfer limit, would achieve a similar outcome, in the sense that individuals would by default have all their pensions pots consolidated into their active pension. This approach would also lead to simplicity for the member, while avoiding some of the downsides associated with member choice, in terms of extra costs for employers, potentially higher marketing costs, and issues regarding lower cross-subsidisation. Nevertheless, it would also involve more transfers between pension providers, which could reduce the viability of investing in longer-term assets, which the government has indicated it would like to promote, and the suitability of the system for collective defined contribution pensions.

4. Conclusion

The proliferation of deferred small pension pots in the UK makes pensions costlier to provide, more expensive for savers, and harder to manage than they need to be, as pension savings are spread over several different pots. The number of deferred small pots is large, with over 12 million worth less than £1,000, with this number growing swiftly. While the introduction of the Pensions Dashboard will help some savers manage their pension savings better, this will not solve the costs associated with the large number of small pots in the system. Individuals can also – rather ridiculously – by default end up with multiple pensions held with the same pension provider, and be paying higher fees in some of those pensions than others. The status quo is therefore not fit for purpose.

One potential policy solution is to give employees the right to tell their employers where to send their pension contributions. This is known as member choice. This could help prevent the creation of a new pension pot every time an employee moves employer, as individuals could direct pension contributions into an existing pension pot. Indeed, this could be the default, with employees always contributing to a single pension pot throughout their career under the lifetime provider model. While these policies might prevent the creation of new small pots, they would not on their own consolidate the stock of deferred small pots that already exists. They would be a more radical departure from the current status quo than other approaches and there would be some potential downsides that would need to be carefully considered.

Instead, we suggest the government should bring in legislation to consolidate deferred small pots automatically, with employees given the option to opt out. As well as consolidating the stock of deferred small pots that already exists, this approach would help solve the problem going forwards, as any future small pots that are created would also by default be consolidated. And it would do this without altering the fundamental structure of the system today, where employers choose where to send their employees’ contributions, which minimises costs for employers. It would likely also not alter any cross-subsidisation from members with larger pots to those with smaller pots that currently exists within a given workplace arrangement.

There would be important decisions to make about the implementation of automatic consolidation, in particular around which pot to consolidate deferred small pots into. The two main suggestions that exist here are either to consolidate into the member’s current pot (known as pot follows member), or to consolidate into one that is listed within a set of authorised arrangements, choosing the biggest pot if a member already has a pot with one of these providers (known as the multiple default consolidator approach).

Ultimately, these two approaches share many similarities, and both would be a significant improvement on the status quo. One benefit of consolidating deferred pots into a member’s active pension pot is that it could increase engagement with the current pot, whereas under the multiple default consolidator model, pots could potentially be consolidated into a pot that the member stopped actively contributing to decades ago. Our view is that this points in favour of the pot follows member approach. The lower costs of provision under this system should reduce charges faced by individual members. To the extent to which this does not occur, the government should review and consider lowering the charge cap for those arrangements to be eligible under automatic enrolment.

A concern about the multiple default consolidator approach is that, if a fairly small number of consolidators are chosen, then there would be anti-competitive effects of raising the threshold for auto-consolidation. This would likely be much less of a concern in the pot follows member approach.

Policymakers would also need to specify which size of pots are eligible for automatic consolidation, and how this consolidation would be carried out in practice. Regarding the former, we judge there is a good case for starting with a fairly low upper limit for the size of pots to be consolidated, of potentially £1,000. Even this low level would capture over 12 million deferred small pots and would not have a large adverse impact on the structure of the market. However, this limit should then be raised over time, both to consolidate a greater number of deferred pots and to avoid it falling behind inflation. The ultimate level of the limit could then be informed by the experience of the initial implementation of the policy. But it could be that the limit should eventually be increased very substantially, or perhaps even removed.

One issue about raising the limit substantially could be that some people might be automatically consolidated into schemes that have higher fees than their current deferred pots. While there would also likely be people consolidated into schemes with lower fees, the concerns of those facing higher fees may outweigh the appreciation of those facing lower fees. One way to mitigate this would be to have a high (or no) limit for automatic consolidation only for those approaching state pension age – this would mean that any change in fees would (for better or for worse) only apply for a shorter period.

Whatever form of consolidation is pursued, it should also be noted that the case for same-scheme consolidation is even stronger. We suggest that individuals who have multiple pension pots with the same pension provider should see those pots automatically consolidated into the arrangement representing the best value for money. And any ongoing contributions should also be routed into that pot. This would simplify pension-saving decisions and generate better value for money.

Irrespective of which pots are subject to automatic consolidation, it should be made simple for individuals to be able to opt into having their other pension pots consolidated too. To implement the consolidation, the two main options are to do this through a central clearing house, or to have a central registry allowing pension providers to carry out the transfer themselves. The majority of respondents to the 2023 government consultation preferred the central clearing house option, and indeed the creation thereof could have longer-term benefits should the government move to allow member choice at a later date.

The desirability of a member choice or a lifetime provider approach is less clear cut, in our opinion. These approaches would entail a more fundamental change to the pension-saving system, imposing extra costs on employers, and the benefits relative to a world where small pots are already automatically consolidated are uncertain. Therefore, we suggest that policymakers should first fully implement automatic consolidation of deferred small pots, either through a multiple default consolidator approach or through – in our view, preferably – a pot follows member approach, before revisiting the case for member choice and a lifetime provider model at a later date.

References

Ahern, J., Oakley, M., Wyjadlowska, J. and Brazzill, M. (2024). Understanding the impact of ‘pot for life’ proposals. A WPI Economics Report for the ABI, https://wpieconomics.com/publications/understanding-the-impact-of-pot-for-life-proposals/.

Crawford, R., Emmerson, C. and Ogden, K. (2022). The risk of pension inattention in a DC world. IFS Briefing Note BN338, https://ifs.org.uk/publications/risk-pension-inattention-dc-world.

Cribb, J., Emmerson, C., Johnson, P., O’Brien, L. and Sturrock, D. (2024). Policies to improve employees’ retirement resources. IFS Report R332, https://ifs.org.uk/publications/policies-improve-employees-retirement-resources.

Cribb, J. and Karjalainen, H. (2023). How important are defined contribution pensions for financing retirement? IFS Report R261, https://ifs.org.uk/publications/how-important-are-defined-contribution-pensions-financing-retirement.

Department for Work and Pensions (2021). Pension charges survey 2020: charges in defined contribution pension schemes. Research report no. 996, https://www.gov.uk/government/publications/pension-charges-survey-2020-charges-in-defined-contribution-pension-schemes/pension-charges-survey-2020-charges-in-defined-contribution-pension-schemes.

Department for Work and Pensions (2023a). Ending the proliferation of deferred small pots. Consultation outcome, https://www.gov.uk/government/consultations/ending-the-proliferation-of-deferred-small-pension-pots/ending-the-proliferation-of-deferred-small-pots.

Department for Work and Pensions (2023b). Government response to ending the proliferation of small pots. Consultation outcome, https://www.gov.uk/government/consultations/ending-the-proliferation-of-deferred-small-pension-pots/outcome/government-response-to-ending-the-proliferation-of-deferred-small-pots.

Department for Work and Pensions and HM Treasury (2024). Pensions Investment Review: unlocking the UK pensions market for growth. Closed consultation, https://www.gov.uk/government/consultations/pensions-investment-review-unlocking-the-uk-pensions-market-for-growth.

Emmerson, C. and Wakefield, M. (2009). Amounts and Accounts: Reforming Private Pension Enrolment. IFS Commentary C110, https://ifs.org.uk/publications/amounts-and-accounts-reforming-private-pension-enrolment.

Pensions Policy Institute (2024a). Lost Pensions 2024. PPI Briefing Note 138, https://www.pensionspolicyinstitute.org.uk/research-library/research-reports/2024/briefing-note-138-lost-pensions-2024/.

Pensions Policy Institute (2024b). The DC Future Book 2024. https://www.pensionspolicyinstitute.org.uk/research-library/research-reports/2024/the-dc-future-book-2024-in-association-with-columbia-threadneedle-investments/.

Webb, S., Myers, L. and Box, T. (2024). Magnetic pensions – a new blueprint for the DC landscape. LCP On point paper, https://www.lcp.com/en/insights/on-point-paper/magnetic-pensions-a-new-blueprint-for-the-dc-landscape.

Data

University of Essex, Institute for Social and Economic Research (2024). Understanding Society: Waves 1–14, 2009–2023 and Harmonised BHPS: Waves 1–18, 1991–2009. [data collection]. 19th Edition. UK Data Service. SN: 6614, http://doi.org/10.5255/UKDA-SN-6614-20.

Acknowledgements

The abrdn Financial Fairness Trust has supported this project (grant reference 202206- GR000068) as part of its mission to contribute towards strategic change which improves financial well-being in the UK. Its focus is on tackling financial problems and improving living standards for people on low to middle incomes. It is an independent charitable foundation registered in Scotland. Co-funding from the ESRC-funded Centre for the Microeconomic Analysis of Public Policy at IFS (grant number ES/T014334/1) is also gratefully acknowledged. We are grateful for comments and advice from our Steering Group members, David Gauke (Chair), Jeannie Drake, David Norgrove and Joanne Segars, and from Karen Barker and Mubin Haq at the abrdn Financial Fairness Trust. Comments and advice from Paul Johnson have been invaluable, as was research assistance from Mahima Sabberwal. Understanding Society is an initiative funded by the Economic and Social Research Council and various government departments, with scientific leadership by the Institute for Social and Economic Research, University of Essex, and survey delivery by the National Centre for Social Research (NatCen) and Verian (formerly Kantar Public). The research data are distributed by the UK Data Service.

Endnotes

Authors

Jonathan Cribb

Jonathan joined IFS in 2011. His research areas includes: pensions, ageing and demographic change, public sector pay, housing, and inequalities.

Laurence O'Brien

Laurence is in the Retirement, Savings and Ageing sector. His work focuses on people’s savings decisions and on economic activity in later life.

More from IFS

Understand this issue

Policy analysis

Academic research