Downloads

Download report PDF

PDF | 726.59 KB

Executive summary

This report discusses how public policy should change to bring about better outcomes in retirement for employees through their accumulation of private pension wealth. In doing so, we draw on new modelling undertaken as part of the Pensions Review (O’Brien, Sturrock and Cribb, 2024) as well as new evidence from public engagement and focus groups undertaken as part of the Review. We focus entirely on policies that affect private sector employees, leaving to one side potential issues with the design of public service pensions. We examine policies that affect the accumulation of defined contribution pension wealth that could be used to fund retirement income, focusing on the parameters of the automatic enrolment system as these have been shown to be powerful in influencing the retirement saving outcomes of private sector employees (Cribb and Emmerson, 2020).

New modelling published alongside this report (O’Brien, Sturrock and Cribb, 2024) shows the scale of the challenge facing private sector employees in trying to accumulate private pension wealth. The economic and policy environment has changed significantly over the last two decades, with substantial consequences for retirement saving decisions. Specifically:

- Big increases in the flat-rate part of the state pension relative to average earnings, and enhanced universality, mean the state pension provides a much stronger foundation level for retirement incomes. This is particularly the case for women, the self-employed, and other groups with lower lifetime incomes, for whom the flat-rate component of the state pension is an especially important source of retirement income.

- Automatic enrolment has successfully brought millions more private sector employees – especially those on average and below-average earnings – into workplace pensions. However, even with automatic enrolment, at any point in time around one-quarter of private sector employees are not contributing to a workplace pension. These people are roughly evenly split between not being in the automatic enrolment target group (e.g. because they earn too little) and being in the target group and choosing to opt out. Most of those brought into workplace pensions by automatic enrolment contribute relatively low amounts: fewer than half of private sector employees saving in a defined contribution pension have pension contributions of more than 8% of their total earnings.

- Changes in the economic environment have made it more difficult to prepare for retirement: lower earnings growth and asset returns make it harder to accumulate pension wealth, and higher longevity at older ages means that those who are not retiring later will need to draw on their pensions over a longer period. This is particularly the case for those on middle and higher lifetime incomes, who are more reliant on private pensions.

Our analysis suggests that more than half of private sector employees who are saving in a defined contribution (DC) pension are on course to meet standard benchmarks of retirement income adequacy. But we find that a substantial minority are not. The exact proportions are sensitive to some of the assumptions made, particularly regarding future investment returns. Which groups appear most at risk of undersaving depends on the chosen benchmark.

A widely used absolute benchmark is the PLSA’s ‘minimum standard’ – a single measure of the annual amount of expenditure needed to obtain a ‘minimum’ standard of living in retirement – where we find that one-third of DC pension savers are falling short in retirement. This increases to two-thirds when we focus solely on those with low earnings (the lowest earnings quarter). That being said, over one-third of working families do not have incomes that meet an equivalent ‘minimum standard’ in working life. This makes it less clear that they would be made better off by saving more now in order to have a higher retirement income. Throughout this report, we stress that there are trade-offs. It is the case that many people will need more money in retirement, but many people also struggle to make ends meet during their working lives, and it is not obvious that reducing their disposable income now in order to increase their income in retirement is desirable.

When considering a ‘target replacement rate’ – specifically that chosen by the Pensions Commission (2004) in its landmark analysis, where an individual’s retirement income is ‘adequate’ if it maintains a certain proportion of their pre-retirement income – we find that it is a majority of higher-earning DC pension savers who will see their retirement incomes fall short. This is because the flat-rate state pension provides a greater degree of earnings replacement for lower earners than for those on middle and higher earnings.

Given the changes set out above, our new empirical estimates, and the fact that the automatic enrolment defaults are extremely powerful tools for changing private pension saving behaviour, the government should look again at how automatic enrolment works to generate good outcomes for people both in retirement and during working age. Automatic enrolment is not compulsory saving – employees are free to opt out if they want to – and therefore it should set defaults in place that are considered to be a reasonable guide to how much an employee with a certain amount of earnings should be saving for retirement.

This report sets out and discusses our policy suggestions given the findings of our modelling work, the views of focus groups of private sector employees, and conclusions from discussion with stakeholders. We balance carefully the benefit to many of saving more – that is, higher retirement incomes – against the cost – namely, lower take-home pay leading to lower living standards during working age. We do this by targeting higher pension contributions at points in life when people should find it easier to save more, and by looking for ways to limit affordability concerns for lower earners, including by proposing increases in employer pension contributions in ways that are less likely to lead to reductions in their take-home pay.

Our policy suggestions are:

- Any employee who earns enough should be eligible for automatic enrolment from age 16 up to age 74 (before and after which people are not allowed to contribute to a tax-favoured private pension), rather than from 22 to state pension age (as it is now). This is a simplification to the system. While those aged 16 to 21 and from state pension age to 74 can request to be enrolled into their employer’s pension scheme and, if they have sufficient earnings, receive an employer contribution, this change would mean more workers would be automatically enrolled if they earn over £10,000.

- There is a strong case for employees to receive an employer pension contribution of at least 3% of total pay, irrespective of whether they contribute themselves. This would prevent many from missing out on an employer pension contribution if they are not eligible or if they opt out, particularly benefiting lower earners. Compared with other ways of increasing employer pension contributions for the lower-paid, this is less likely to push down on lower earners’ wages, as any resulting reduction in wage growth cannot easily be targeted at those who would otherwise have opted out of their workplace pension. A risk is that making the employer contribution non-contingent would lead to many more choosing to opt out of making an employee contribution. Our reading of the available evidence is that the numbers responding in this way would be small. But a government worried about this issue could trial this system amongst a group of employers prior to implementation to provide greater evidence. To prevent some monthly contributions being exceptionally small (and very small pension pots potentially proliferating), some minimum level of earnings would need to be defined, above which employer contributions become required. We suggest an appropriate figure could be around £4,000 per year.

- There is a good case for being particularly careful with policies that aim to increase the proportion of their current earnings that lower earners save in a private pension. Higher pension saving would lead to higher incomes in retirement, but this must be balanced against the potential cost of lower take-home pay now, which may be harder for lower earners to bear. This lower take-home pay would be the direct result of higher employee contributions, and could also arise from higher employer contributions if these lead to lower growth in wages. For people currently earning between £10,000 and £15,000, almost two-thirds (63%) are in households with below-average incomes, 22% are in income poverty and 20% are in ‘material deprivation’. They also face other financial pressures: half of them have less than £1,500 in accessible savings.

- If the government utilises legislation passed in 2023 (for Great Britain, with the Northern Ireland Assembly currently considering an equivalent bill for its jurisdiction) allowing it to reduce the lower limit for qualifying earnings to zero, default pension contributions (from employees, employers and tax relief) would increase by around £500 a year for everyone currently targeted by automatic enrolment. This would imply a much larger increase in contributions as a proportion of earnings for low earners. A person earning £10,000 on minimum contributions would see employee pension contributions rise by £250 per year, pushing down take-home pay by 2.5%. Any reduction in wages arising from employers passing on the costs of increased employer contributions to their employees would increase this fall in take-home pay further. If the new government is to proceed in this direction, it should therefore give serious consideration to diverting the additional contributions from this policy initially into a liquid savings account, similar to the NEST sidecar account. While this would reduce the extent to which the policy ultimately boosted retirement incomes, it should also reduce adverse consequences for working-age living standards.

- Additional pension contributions are easier to bear when incomes are higher. Increases in the default pension contribution above 8% of earnings should therefore be targeted at average – and above-average – earners. Additional pension contributions are also easier to bear when day-to-day expenditures are lower. For many, this happens once children are older, mortgages are less of a burden and student loans are paid off, perhaps after age 50 or 55. There is therefore also a case for increasing default contributions above 8% more broadly among those aged over 50 or 55. In either case, these targeted higher total contributions should not involve higher default employer contributions. Increases for higher earners and older employees would also help many who are low earners at some points in their life – either by encouraging them to save more at a later point when their earnings are higher or through boosting the pension saving of a higher-earning partner.

- Around a fifth of employees in DC pensions earning around £50,000 are on minimum pension contributions. But employees earning above the upper limit for qualifying earnings of £50,270 currently face a declining minimum pension contribution (as a percentage of their pay) as they earn more. These people should, in general, be saving higher fractions of their earnings as they earn more, so the current automatic enrolment minimums are less good at guiding them to make good decisions. The upper earnings limit for qualifying earnings should therefore be raised. There is a case for increasing this to £90,000, which would mean that, even with a rise in default minimum contributions to 12% for the portion of earnings above average earnings, default minimum contributions would remain below the ‘money purchase annual allowance’ (the limit for tax-relieved pension saving for those who have made a flexible withdrawal from a private pension). An alternative would be to restore this limit to its real-terms value in 2021–22 (from when it has been frozen in cash terms): this would increase it to just over £60,000 today. Indeed, the freezing of the upper earnings limit for qualifying earnings had the consequence of reducing minimum saving levels for those on £60,000 or above by around £800 a year. This limit could be increased for total contributions. One concern with raising the upper earnings limit could be that this would increase the up-front income tax relief going to high earners, at a cost to the exchequer. Much of the additional relief would be tax deferred rather than tax avoided. And while there would be some overall cost to the public finances, using automatic enrolment parameters to steer employees away from making good retirement saving decisions in order to limit those reliefs would be very poor policymaking relative to tackling overgenerous reliefs directly.

- If higher default total pension contribution rates are introduced for all earners, or for specific groups of the population such as average and above-average earners or older workers, employees should be presented with the option to ‘opt down’ to the minimum pension contribution rates currently in operation.

- The values of parameters in the current system, such as the ‘earnings trigger’ above which employees are automatically enrolled, have been eroded by inflation and grown much less than earnings. The earnings trigger (£10,000) is also now 13% below the annual value of a full new state pension (£11,502), whereas on its introduction in 2012 it was 45% higher than the then annual value of a full basic state pension (£8,105 and £5,587, respectively). To prevent further erosion, the earnings trigger for automatic enrolment, the upper limit for qualifying earnings, and the lower limit for qualifying earnings (if it is retained) should be increased over the longer run in line with growth in average earnings.

- The experience of the past 20 years highlights that the saving landscape can change significantly over a fairly short period. Given how powerful they are in influencing saving decisions, automatic enrolment default rates should be subject to a regular and frequent review – perhaps aligned with the periodic review of the state pension age and certainly not occurring less than once a decade – to ensure that they are set up to best support current savers.

In summary, this package of policy suggestions would:

- Boost private pension saving for all (or nearly all) employees who currently miss out on any contribution from their employer (e.g. because they are not currently eligible for automatic enrolment or because they have chosen to opt out) who are disproportionately on lower earnings. This would be done in a way that is less likely to depress their take-home pay. Overall, this non-contingent employer contribution is estimated to boost aggregate employer pension contributions for those employees not saving into a pension by around £4.0 billion per year.

- Help employees to save more for retirement at the points of their working lives when they are most able to do so: when they have above-average earnings and when they are at older working ages. Many currently on low earnings would benefit from this because they will save more when they earn more later in life or because they have a higher-earning partner who would save more.

- Mitigate concerns about the affordability of higher default contributions by allowing additional pension contributions to be diverted into a liquid savings account, and allowing employees to ‘opt down’, rather than ‘opt out’, with no loss of employer contribution.

- Help ‘future-proof’ the system by ensuring that over the longer term, thresholds in the automatic enrolment system keep up with average earnings growth.

The suggestions here are complementary to those previously made by the Pensions Review with regards to the state pension. Indeed, making the state pension system more predictable, as is proposed in Cribb et al. (2023a), would reduce one layer of uncertainty for those making private saving choices. Specifically, ensuring that the state pension is not means-tested, that it maintains its value relative to earnings over the longer term, and that the vast majority of those spending their whole working lives in the UK qualify for the full flat-rate amount, makes it clearer how much additional saving – if any – different individuals might want to save privately for retirement during their working lives

1. The outlook for retirement income adequacy

There are widespread concerns about how prepared many working-age people are for retirement. Indeed, it was one of the key challenges that we highlighted upon launching the Pensions Review in April 2023 (Cribb et al., 2023b). Drawing on our new findings on how well prepared current employees are for retirement (O’Brien, Sturrock and Cribb, 2024) and on public engagement work undertaken by Ignition House as part of our Review, we set out some new suggestions for policy around private pension saving.

Our suggestions very much take the current structure of the private pensions landscape as given: private sector employees are automatically enrolled into (mainly) defined contribution pension arrangements. We focus on how the very powerful levers operating within this existing system can be made to work better for private sector employees. We do not – for now – consider more structural changes to the private pensions landscape such as any widespread move towards collective defined contribution (CDC) schemes, nor any mechanism for consolidation of smaller defined contribution (DC) pension pots; nor do we consider reforms to public service pension schemes. These issues will be considered later in the Review. We also do not consider in this report changes to the tax system designed to encourage more saving, though we note where we think the approach of relying on defaults is unlikely to be enough.1

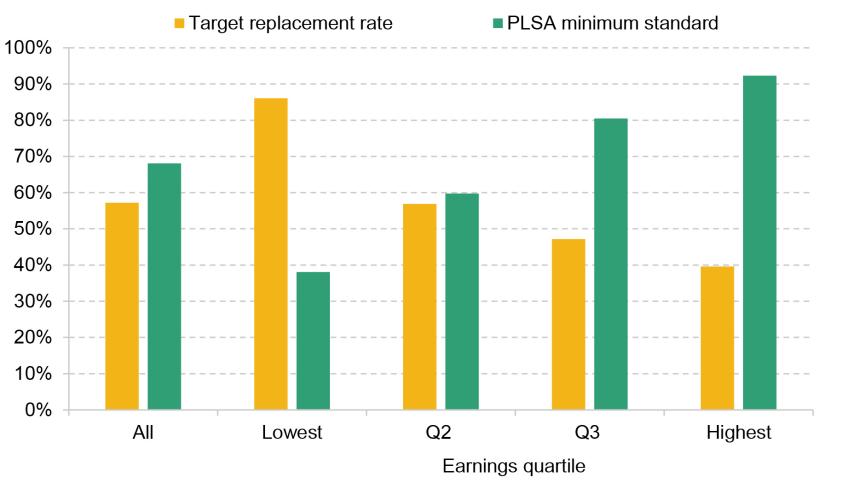

Our new modelling of the adequacy of employees’ private wealth accumulation (O’Brien, Sturrock and Cribb, 2024) identifies a number of key challenges facing private sector employees saving for retirement that provide important context for our suggested policy changes – most notably that falls in asset returns and earnings growth over the last 20 years make it harder for people to accumulate wealth. This is compounded by the fact that the expected longevity of the current working-age population is higher than the longevity of the working-age population 20 years ago, so that unless retirement ages increase in lockstep with increased longevity, accumulated pensions will have to cover more years of retirement. These concerns are combined with the fact that most of the large number of employees brought into workplace pensions by automatic enrolment are not making contributions above the minimum default levels. O’Brien et al. (2024) suggest that more than half of private sector employees who are saving in a DC pension are on course to meet standard benchmarks of retirement income adequacy. But, as shown in Figure 1.1, which considers individual incomes (therefore not considering incomes from a partner or spouse), we find that a substantial minority are not. The exact proportions are sensitive to some of the assumptions made – in particular regarding future investment returns. And which groups appear most at risk of undersaving depends on the chosen benchmark.

Figure 1.1. Retirement income adequacy: percentage of private sector employees saving into a defined contribution pension projected to reach selected benchmarks

Note: Earnings quartiles are defined as the quartiles of pre-retirement earnings (measured between the ages of 50 and 59). PLSA = Pensions and Lifetime Savings Association.

Source: Reproduced from figure 4.6 of O’Brien, Sturrock and Cribb (2024).

A widely used absolute benchmark is the PLSA’s ‘minimum standard’, where we find that one-third of DC pension savers – equivalent to 5 million people – are falling short in retirement. This rises to two-thirds of those on low earnings. When considering a ‘target replacement rate’ – specifically that chosen by the Pensions Commission (2004) in its landmark analysis2 – we find that it is a majority of higher-earning DC pension savers who will see their retirement incomes fall short. Our results here are similar to those from other modelling undertaken by the Pensions Policy Institute (Pike, 2022) and the Department for Work and Pensions (2023).

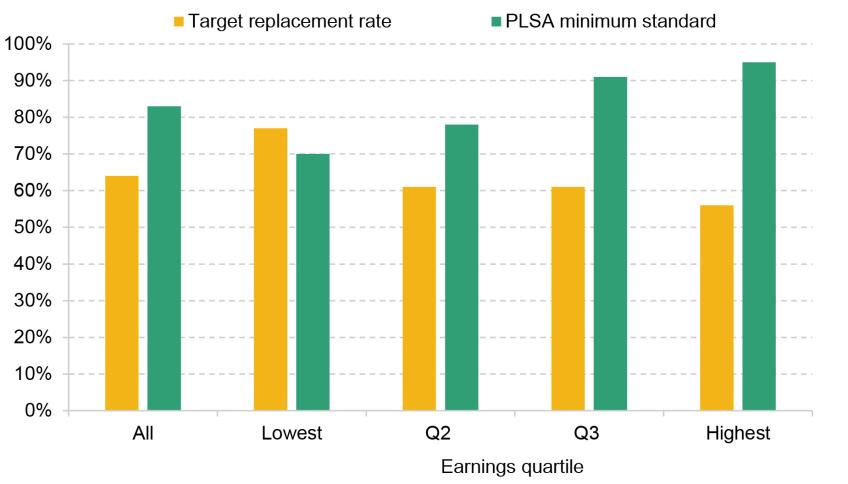

Considering individual incomes is not the only way of considering retirement income adequacy, particularly as most people share income with a partner or spouse. Figure 1.2 provides analysis of whether people reach these adequacy benchmarks if we assume that couples share their incomes in retirement, and additionally accounts for the fact that some people may continue to live in private rented accommodation in retirement and therefore have significant housing costs. More people reach the adequacy benchmarks on this basis, with 64% reaching their target replacement rate (up from 57% when considered individually) and 83% reaching the PLSA minimum standard (up from 68% when considered individually).

Figure 1.2. Retirement income adequacy: percentage of private sector employees saving into a defined contribution pension projected to reach selected benchmarks, including projected retirement income of partners and rental costs

Note: These results model couples jointly, assuming they share their incomes in retirement, and incorporate housing costs for those living in private rented accommodation in retirement. Earnings quartiles are defined as the quartiles of pre-retirement earnings (measured between the ages of 50 and 59). PLSA = Pensions and Lifetime Savings Association.

Source: Reproduced from tables 4.5 and 4.6 of O’Brien, Sturrock and Cribb (2024).

The biggest difference compared with the individual results is for the lowest earnings quarter, where 70% are modelled to reach the PLSA minimum standard (compared with 34% on an individual basis). This is in large part because less private income is needed to supplement two full new state pensions in order to reach the PLSA minimum standard for couples than is needed in addition to a single full state pension in order to reach the PLSA minimum standard for singles.

The 17% of people (and 30% of low earners) modelled to not reach the PLSA minimum on this basis in retirement compares with over one-third (35%) of working families (6.7 million families) that do not have incomes that are equivalent to that ‘minimum standard’ in working life.3 This rises to around 50% for employees in the lowest quarter of the earnings distribution.

The rest of this report proceeds as follows. Chapter 2 discusses potential changes to the automatic enrolment system, highlighting where we think there is a strong case for reform. Chapter 3 sets out modelling that shows the effects of our suggested set of reforms and compares them with the effects of two other proposed reforms. We examine in particular how these potential reforms affect retirement incomes and how that differs across the retirement income distribution, how they affect take-home pay, and how they affect the estimated proportion of private sector employees meeting retirement income adequacy benchmarks. Chapter 4 provides a short conclusion.

2. Changes to the automatic enrolment system

This chapter discusses potential changes to the automatic enrolment system, which uses defaults to encourage employees to save for retirement in private pensions; these defaults have been shown to be very powerful. We discuss some of the different options and set out where we have concrete proposals.

Currently, the system of automatic enrolment requires that employees aged between 22 and state pension age who have been employed in a job for three months or more and whose earnings in that job are equivalent to at least £10,000 per year (the ‘trigger level’) are enrolled into a private pension by their employer. Total default contributions into this scheme must be at least 8% of the value of the part of the employee’s annual salary between £6,240 (‘lower limit for qualifying earnings’) and £50,270 (‘upper limit for qualifying earnings’), with employer contributions making up at least 3 of the 8 percentage points.

The previous government stated an ambition to reduce the lower earnings limit to zero in the ‘mid 2020s’ and to lower the starting age from 22 to 18. And while legislation was passed in 2023 that would enable the government to make these changes across Great Britain (with the Northern Ireland Assembly currently considering equivalent legislation that would apply to its jurisdiction), these new legal powers are yet to be exercised. Employees can choose to opt out of pension saving, in which case their employer can also opt not to make contributions to their workplace pension. Those earning below the trigger level can choose to opt in and, if they meet the age and job tenure criteria and earn above the lower limit for qualifying earnings, they must receive at least the minimum employer contribution. Employers can choose to enrol workers who are outside the automatic enrolment target group, and many enrol workers into arrangements with higher contributions (in particular, employer contributions, but often also employee contributions) than the minimum default level.

In making policy suggestions to change these parameters of the automatic enrolment system, we balance carefully the benefit of saving more for many – that is, higher retirement incomes – against the cost – namely, lower take-home pay leading to lower living standards during working age. We do this by targeting higher pension contributions at points in their life when people should have greater capacity to save and by looking for ways to limit affordability concerns for lower earners. We take seriously the idea that following the defaults in the system should generally produce good outcomes – and certainly not steer towards bad outcomes – for employees saving for retirement, which is why we are suggesting changes to defaults in the pension saving system. There is a wide range of evidence that such defaults in the retirement saving system are very powerful. This is reflected in a comment from a member of the public in our public engagement work, shown below, which indicates that many people expect the default saving to produce good outcomes in retirement.

‘People will naturally think if you’re putting in the 8% auto-enrolment contribution it will be OK. And when they eventually go to retirement at 20, 30, 40 years and they’ve always been putting in the 8%, they’ll be sitting there saying, well, hold on a minute. I fully expected to be able to retire and retire comfortably on my 8% contribution for the last 40 years. Why didn’t you tell me 20 to 30 years ago that actually it needed to be 12% or 14%?’

– Male, aged 45–54

Despite this aim, it is difficult to set defaults that are likely to generate optimal outcomes for all. People face very different circumstances and those who appear quite similar in many ways today can be on very different trajectories, as highlighted in our modelling published alongside this report (O’Brien, Sturrock and Cribb, 2024). We therefore highlight the groups for which defaults may be a poor guide as to how to prepare effectively for retirement, and what might be done about this.

This chapter proceeds as follows. First, we examine potential changes to some of the current key parameters in the automatic enrolment system: who is targeted in terms of earnings and age, and how qualifying earnings are determined. In Section 2.4, we discuss the case for altering the structure of automatic enrolment to make employer pension contributions not contingent on employees making their own contributions to a scheme. In Section 2.5, we examine the case for higher default minimum pension contributions at least for some employees – or at some point in employees’ working lives – and discuss other potential changes to default contribution rates. Finally, we examine the accessibility of private pension savings.

2.1 Employees targeted for automatic enrolment

Automatic enrolment currently applies to those aged 22 to state pension age. Following the Pensions (Extension of Automatic Enrolment) Act 2023, the government now has, within Great Britain, the power to reduce the lower age threshold to 18. However, it is not clear why the age limits to automatic enrolment should exclude some of those who are allowed to save into a tax-favoured pension (all those aged 16–74). While there will be few people earning above the trigger at ages 16–21 and state pension age to 74, if someone is earning above the trigger there is a case that they should be defaulted in, for the same reasons as people are defaulted in at other ages. We therefore suggest abolishing any age restriction such that employees aged from 16 to 74 are subject to automatic enrolment. One concern with this may be that it would increase the number of small pension pots. Were an effective solution to reduce the small pots problem implemented then the case for expanding the age range would be further strengthened.

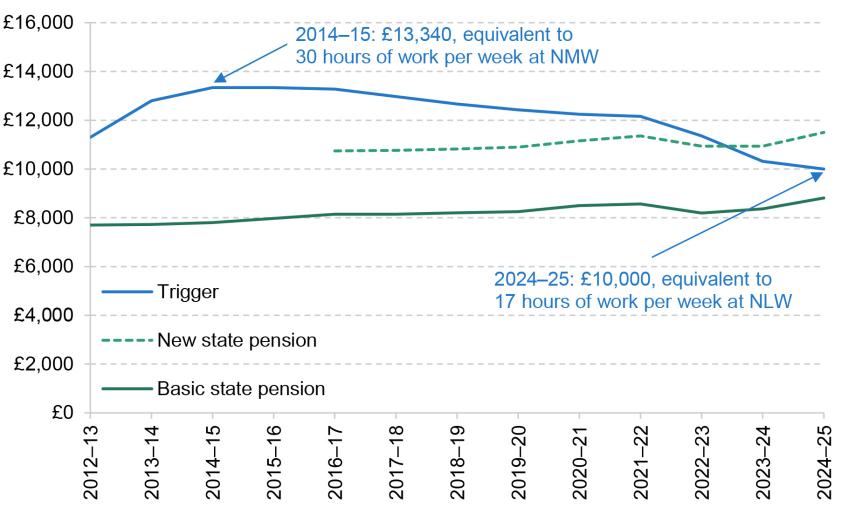

The level of annual earnings above which someone must be defaulted into pension saving is currently set at £10,000 and has been fixed at this level in cash terms since 2014. This means that it has fallen by 25% in real terms over the past 10 years (see Figure 2.1). While the trigger was substantially higher than the new state pension in 2016, it has fallen significantly below it now. The trigger was even further above the level of the full basic state pension in 2012. It has also fallen sharply relative to minimum wage levels: in 2014 it was set at the equivalent of 30 hours a week of work at the national minimum wage whereas it is now equivalent to 17 hours a week at the national living wage.

Figure 2.1. Level of the trigger and annual value of a full new state pension and a full basic state pension in March 2024 prices

Note: Figures are expressed in real terms using the Consumer Prices Index.

Source: Authors’ calculations using ONS CPI index (series D7BT).

There is no universally right answer to the question of when people ought to be defaulted into saving, but in general the presence of the flat-rate new state pension means that the case for saving for retirement is weaker for those currently on lower incomes. Encouraging employees who consistently have low living standards during working life to reduce their living standards further to have higher income in retirement can be hard to justify. And employees with temporarily low earnings would be better served saving more when their earnings are higher, rather than when they have low earnings. These observations in general would indicate setting the trigger at a level – perhaps closer to the level of the new state pension – that ensures that people are not inappropriately transferring resources from a period when they have low incomes to a period when their income is likely to be higher.4

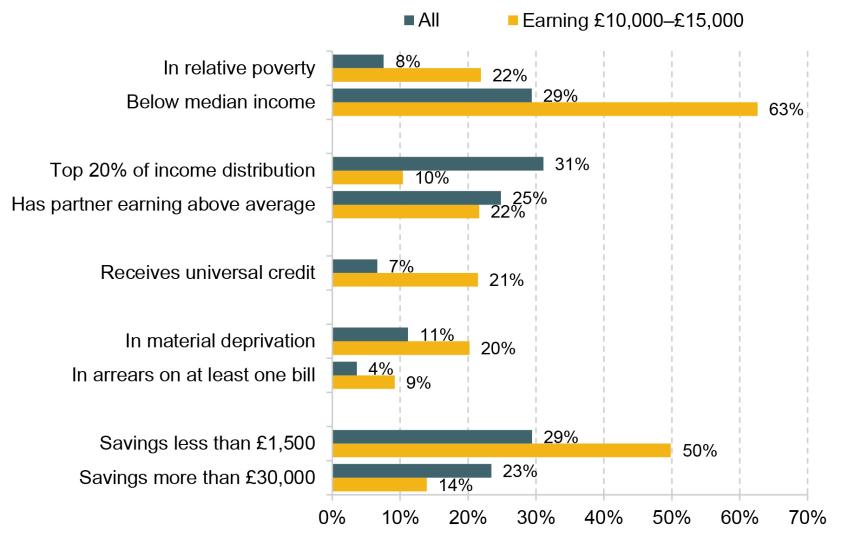

Concerns regarding the potential for people on lower earnings to oversave for retirement at the expense of higher take-home pay today are supported by Figure 2.2. It shows that low-earning people who are currently targeted for automatic enrolment (i.e. earning between £10,000 and £15,000 per year) are mostly on below-average household income (63%), with almost a quarter (22%) in relative poverty and a fifth ‘materially deprived’ (unable to afford a set of important material goods and services). Around a fifth (21%) receive universal credit (UC), and while that is much higher than the average for employees in DC schemes (7%), it means that most of the targeted low earners do not benefit from the fact that higher pension contributions lead to higher UC payments. They also have low levels of accessible wealth, with half having less than £1,500 in savings. Previous research from the roll-out of automatic enrolment in the UK has found that, as well as successfully generating additional pension savings, it led to a reduction in other types of savings (Choukhmane and Palmer, 2024) and an increase in debt (Beshears et al., 2024). This highlights how further reducing the earnings trigger could have adverse effects on the financial well-being of some of those affected.

Figure 2.2. Characteristics of employees who are participating in a workplace pension scheme, 2022–23 (all and employees earning £10,000 to £15,000)

Note: Incomes are measured at the household level after deducting housing costs and are equivalised to account for differing household size and structure. The relative poverty line is 60% of median equivalised household income. Partner earning above average is defined as a cohabiting partner or spouse earning over £35,000 (full-time median earnings in 2023). ‘Receives universal credit’ includes those receiving legacy benefits.

Source: Authors’ calculations using the Family Resources Survey, 2022–23. Updated from a similar chart in Cribb, Karjalainen and O’Brien (2024).

While there is a diversity of experiences for any group in the labour market, it is notable that very few lower earners currently targeted by automatic enrolment have high household income (only 10% are in the top fifth of the household disposable income distribution) and few have a high level of savings. There could be an argument that if someone has a higher-earning partner, with whom they share current income, then this individual ought to save to maintain their living standard at older ages. 80% of employees earning £10,000 to £15,000 are women, and higher-earning partners are therefore particularly likely to be men.

This argument might hold particularly given the risk of divorce or separation, which could mean that the lower-earning partner has a higher standard of living today (while in a couple) than in retirement (when potentially living alone). Indeed, research has highlighted that only a minority of couples actually split their assets in half upon divorce, with private pensions particularly unlikely to be shared equally; this primarily affects women, particularly those with children, who tend to have accumulated lower levels of pension wealth (Hitchings et al., 2023). This is one reason why the lower earner in a couple might want to build up their own private pension, particularly if they have a high-earning partner. However, only 22% of the low earners targeted by automatic enrolment have a partner earning above the national median for a full-time worker (around £35,000).

The fact that – currently – the earnings trigger affects not just which people make employee contributions to private pensions, but also who receives employer contributions, provides an argument against a higher earnings trigger. If the earnings trigger is raised, a set of lower earners will no longer be defaulted into making employee contributions but they will also not by default receive an employer contribution. With such a change concentrated on a small set of earners, they may be unlikely to receive higher pay to make up for the lower remuneration through employer pension contributions.

Irrespective of the level of the threshold, it should be automatically increased over time, preferably in line with average earnings, so as to prevent the divergence of the trigger and the value of the new state pension and to stop increasingly lower-paid employees being automatically enrolled over time.

2.2 Lower limit for qualifying earnings

Currently set at £6,240, the lower limit for qualifying earnings has also fallen in real terms over time, being worth around 20% less in real terms now than it was in 2012–13. This means that the default minimum pension contributions under automatic enrolment for most earners are larger than was envisaged when it was introduced, with the percentage increase in contributions greater for lower earners.

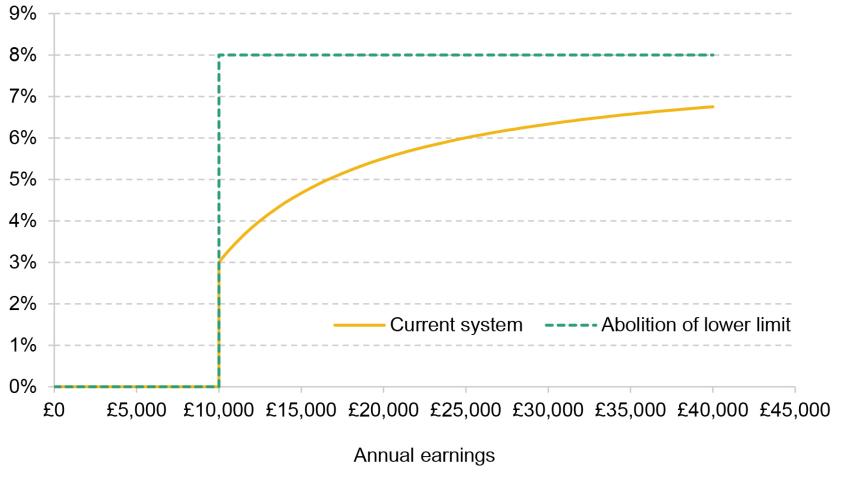

When setting the level of the lower limit for qualifying earnings, there are some key trade-offs to be considered. For each £100 fall in the lower limit, minimum default contributions for those above the trigger rise by £8, with at least £3 of this having to come in the form of an employer contribution. Among those above the trigger, this implies a larger percentage increase in saving for those on lower earnings. Figure 2.3 shows this graphically, as the largest (percentage) increase in pension contributions when reducing the lower limit to zero is for those earning the trigger level of £10,000. The higher contributions that would result from a decrease in the lower limit might particularly be considered a good thing for middle and higher earners, among some of whom there is a good case for more saving. For those earning just above the trigger, who would see the largest rise in contributions in percentage terms, our modelling is suggestive that more saving may not in many cases be advisable. Such people are either lifetime low earners, who should only be saving at most a modest fraction of their earnings in order to smooth their income, or temporary low earners, who would preferably be saving for retirement at other times in their life.

Figure 2.3. Schedule of default total contribution rates under current system and under abolition of the lower limit for qualifying earnings

Source: Authors’ calculations.

There is another aspect of this trade-off. Decreasing the lower limit might also be considered beneficial for those whose earnings are split over multiple jobs. For someone who is working in multiple jobs, the trigger applies separately to the earnings from each job, so the current system means they will save a lower proportion of their total earnings than someone earning the same amount but in a single job. For someone who has multiple jobs and is earning above the trigger level in at least one of those jobs, reducing the lower limit will take their overall saving rate closer to that of someone earning the same amount from one job.

Two further considerations point in favour of reducing the lower limit. One is that, particularly if it is set to zero, it may make it easier for employees to understand how much they are saving under default contributions, improving the transparency of the system. Currently, the default rate of total contributions as a share of total pay (for someone with one job) is increasing for earnings up to the upper limit for qualifying earnings (and then declining). Reducing the lower limit takes this closer to a simple 8% of total earnings for most of those above the trigger (all except those over the upper limit for qualifying earnings). It seems possible that currently, if they are unaware of the lower limit, an employee may believe their pension contributions total 8% of their salary; a switch to contributions ‘from the first pound’ would eliminate any such confusion.

A second reason for having a lower limit that is lower than the earnings trigger is so that those earning just above the trigger are not making small contributions and therefore creating small pension pots, which might be uneconomical due to administrative costs. However, the gap between the lower limit and the earnings trigger has expanded in real terms over time, meaning that this concern should have receded. But it could be that other reforms – either to reduce the number of ‘small pots’ or to reduce the costs of providing small pots – would be sensible. These will be considered in a later part of the Pensions Review.

In contrast, one consideration points towards raising the lower limit for qualifying earnings. If employees do not value a pound of employer contributions equally to a pound of normal pay (due to a lack of awareness or a lower value placed on future income than on current income), then employer contributions operate in part like a tax. In this case, there is a cliff-edge in the effective tax rate at the trigger level, and this becomes larger when the lower limit is reduced and as default employer contributions are increased. This provides an unwelcome incentive for employers to offer employment contracts at just below the trigger in order to avoid automatic enrolment, with this incentive being greater the lower the lower limit is, though analysis of the Annual Survey of Hours and Earnings as automatic enrolment was rolled out found no strong evidence of additional employment concentrated just below the trigger.

Overall, there is a trade-off between, on the one hand, the transparency and simplicity of reducing the lower limit and the benefits of the additional contributions that brings and, on the other, the potential cost of oversaving by some low earners and an increase in the effective cost of employment at the trigger. Of course, as we come onto later, a reduced lower limit is only one way to increase saving rates for middle and higher earners.

2.3 Upper limit for qualifying earnings

The upper limit for qualifying earnings has been set equal to the upper earnings limit (UEL) for National Insurance contributions since 2012–13. As the UEL is also tied to the higher-rate threshold, this means that the government’s income tax policies have led to changing levels of minimum default contributions for higher earners in recent years – first with real increases in the UEL from 2015 to 2019, pushing up real minimum default contributions for higher earners, and then with cuts in the UEL as tax thresholds have been frozen, reducing real minimum default contributions.

An upper limit for qualifying earnings means that the required minimum default total contributions reduce as a percentage of salary for earnings levels above that limit. That seems inadvisable in light of the findings that higher earners should generally save more than they are currently saving to provide a reasonable replacement rate in retirement. Given the projected shortfall in saving among some middle and high earners (see Figure 1.1), we think there is a strong case to raise the upper limit. Whatever level it is set at it should then be indexed in line with earnings.

There is a principled argument for abolishing the upper limit for qualifying earnings altogether on the basis that this would help high earners reach target replacement rates. One argument for having an upper limit is to claim that above a certain point – perhaps where an individual is very unlikely to be reliant on means-tested benefits or will have reached some objective benchmark standard of living – it is not the government’s responsibility to ensure that someone is saving to smooth their living standards from working life into retirement. This is reinforced by the fact that high-income individuals will typically be better placed to take and act on financial advice. A counterpoint would be to argue that as automatic enrolment is only a default (though a rather powerful one) and not mandatory saving, this default ought to be set in a way to make it easy for as many people as possible to save in a way that would be good for them.

A more practical point is that the annual allowance for pension saving is tapered away from £60,000 to £10,000 per year for those with taxable income plus pension contribution of more than £260,000. Further, for those who have already made flexible DC pension withdrawals, their ‘money purchase annual allowance’ is £10,000 per year. There could therefore be a case for setting the upper limit for qualifying earnings such that no one would have default contributions of more than £10,000. With the other changes to automatic enrolment rates and thresholds we suggest, this would imply an upper limit of around £90,000.5 An alternative would be to restore this limit to its real-terms value in 2021–22 (from when it has been frozen in cash terms): this would increase it to just over £60,000 today.

A different option to increase the upper limit for qualifying earnings would be to create two upper earnings thresholds for qualifying earnings: a lower one that determines qualifying earnings for minimum employer contributions and a higher one that determines qualifying earnings for total contributions. While this would introduce some additional complication into the system of qualifying earnings, it would encourage higher employee contributions, but not directly change employer contributions, meaning additional default saving for high earners could come – nominally – only from employees, and not employers. This could potentially ease political difficulties with a straightforward increase in the upper limit if that were seen to benefit higher earners by defaulting higher minimum employer contributions, even though in reality these higher employer contributions would be likely to reduce their pay in the medium run. If two separate upper limits (for employer and for total contributions) were introduced, they should both be indexed in the long run to rise in line with average earnings.

2.4 Contingency of employer contributions

Currently, opting out of a pension typically means losing out on an employer contribution. This creates an incentive for employees to remain in a pension and, to the extent to which it is effective, the incentive may be seen as a positive. On the other hand, it might be seen as a double hit to someone who is forced to opt out of pension saving due to a short-term increase in their spending needs. Specifically, employees who opt out are likely to be disproportionately those who are struggling to meet their current spending needs, and it might be seen as unfair that by opting out they lose part of their remuneration. Once you include the approximately 12% of private sector employees who do not participate in a pension and are not automatically enrolled, just over a fifth of all private sector employees are not receiving an employer pension contribution. Furthermore, the contingent nature of the employer contribution provides an undesirable incentive for employers to want their employees to opt out of their workforce pension, and it is not far-fetched to think that some unscrupulous employers might act upon such an incentive.

‘I think that if the employer is paying in it is like a wage. So if you had to stop, they should still pay in because it’s part of your wages.’

– Female, aged 45–54

One attractive option is to make default employer contributions universal for almost all employees, rather than being contingent on the employee making contributions themselves. The most straightforward change would be to make a baseline level of employer contributions (such as 3% of all earnings) mandatory for all except the lowest earners (in order to prevent extremely low contributions being made). If this earnings threshold were set at £4,000 per year, it would mean that contributions made were at least £10 per month. Those earning above the ‘earnings trigger’ (£10,000) would still be defaulted into making a total contribution of at least 8% of qualifying pay (plus 3% on earnings up to the lower limit for qualifying earnings), but would have the option to reduce their employee contributions to zero and maintain employer contributions of 3% of earnings. Employers could choose to make non-contingent contributions in excess of 3% of pay, or to implement ‘matching’ functions where higher employee contributions would lead to employer contributions higher than 3%.

The standard concern about making employer pension contributions non-contingent is that substantially more people would stop making employee contributions in response to the diminished financial incentive to make such payments. Our judgement on the available evidence is that the fraction of people making employee contributions would likely fall slightly, but not dramatically. Cribb and Emmerson (2020) find increases in pension participation of 36 percentage points after automatic enrolment in the UK, with 12% not participating after the reform. Beshears et al. (2023) review the effects of automatic enrolment in a wide range of settings and generally find similarly large effects.

In contrast, the effect of the financial incentive from ‘employer matched contributions’ is estimated to be much smaller, as we would expect. For example, Beshears et al. (2010) study a match schedule where the employer contribution equals half the employee contribution (up to a 6% employee contribution), and find it only increases pension participation by around 5–11 percentage points compared with no employer contribution at all. This is similar to the findings of Duflo et al. (2006) and Engelhardt and Kumar (2007). Indeed, Beshears et al. (2010) also study a US firm’s introduction of non-contingent contributions at 3% of pay and find the fraction making no employee contributions rises by 8 percentage points from 11% to 19%. While this is not a trivial increase, it is dwarfed by the size of the increases arising from automatic enrolment.

It is worth being explicit about the trade-offs here. The key benefit of non-contingent employer contributions is to those who currently leave their pension scheme after automatic enrolment or who are never automatically enrolled in the first place. They would no longer ‘miss out’ on part of their remuneration. Because they are a fairly small group compared with the workforce as a whole, and because a key reason for being ineligible for automatic enrolment is low weekly hours of work, we think that any incidence on wages of these higher employer contributions is likely to be spread out across the workforce as a whole, and it is unlikely to materially reduce the hourly wages of people on low earnings. The cost of such a change would be the potential for slightly lower wages spread across the rest of the population who already receive an employer pension contribution.

As discussed, another downside is the potential for higher fractions of people not making employee contributions to their pension. This would be particularly the case if individuals are short-sighted and therefore generally avoid saving for retirement but are only convinced to remain in a pension plan because of the contingent employer contribution. On the other hand, there may be others who only participate in a pension because they do not want to lose the employer contribution but who would have a very high value to higher take-home pay, to finance current spending or to pay down high-interest debt, for example. If they opted out from making employee pension contributions after non-contingent contributions were introduced, this is less likely to be a bad outcome for them.

A government that was concerned about the extent to which a non-contingent employer contribution would lead to fewer employees making employee contributions could run a trial to evaluate such a system. This could take the form of the government asking firms to offer to participate and then randomising which firms enact such a system. Implementing a system of an (at least) 3% non-contingent employer contribution might necessitate a separate solution for people (in the public or private sector) who are offered defined benefit (DB) pension schemes; these generally have much higher employer and employee contributions, and receiving the employer contribution is contingent on making the employee contribution. A potential option could be for any employee opting out of the DB scheme to be enrolled in a DC scheme where the employer contribution is at least 3% of pay. A different option would be to exempt employers that offer defined benefit schemes (with a minimum level of generosity) from these suggested rules.

2.5 Default contribution rates

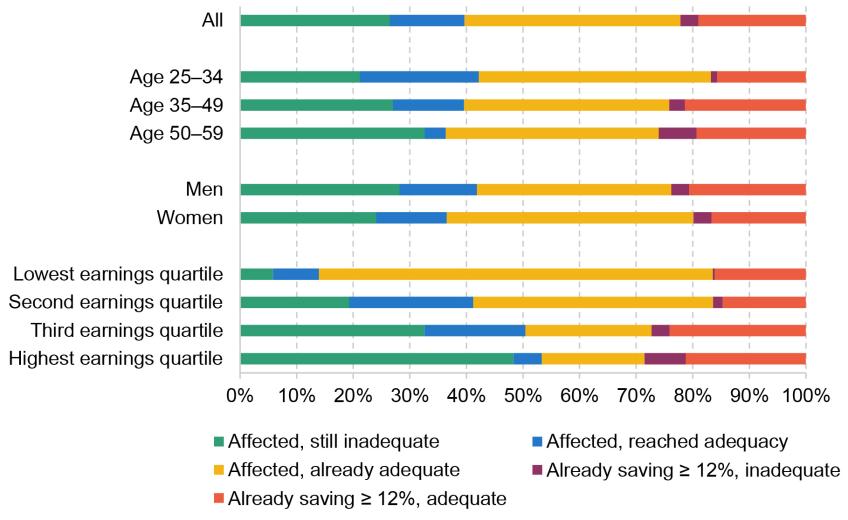

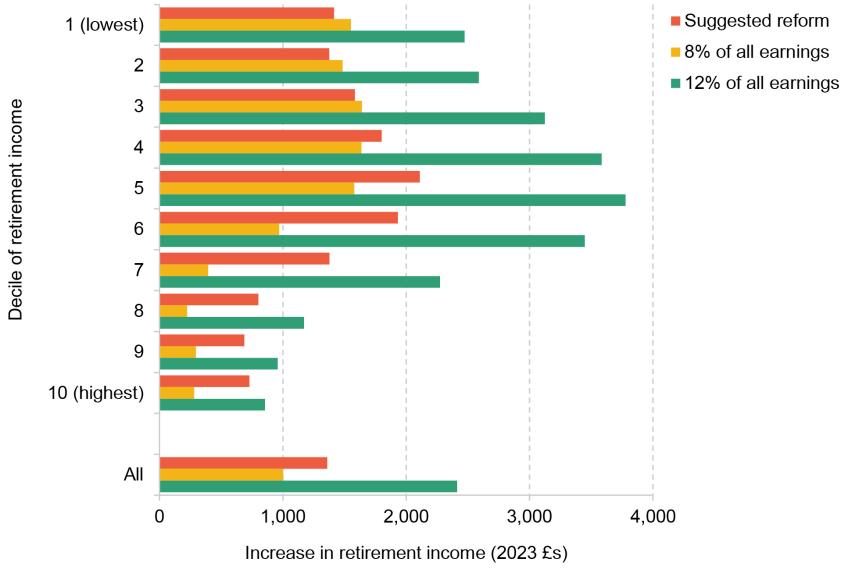

There is no one-size-fits-all answer to how much people should be saving. Our modelling suggests that a single minimum default total contribution rate may therefore not be right for everyone. For example, Figure 2.4 shows that increasing default contribution rates to 12% of total earnings – and assuming that there is no increase in opt-out rates and no change in saving behaviour among those already saving at least 12% of their salary in a pension – would lead to about one in eight more employees who are currently saving in a DC scheme reaching an adequate retirement income relative to their target replacement rate (the blue bars). These are clustered among younger employees, for whom this increase in default contribution rates would halve the rate of undersaving. It would also substantially reduce undersaving among those in the middle (the second and third quarters) of the earnings distribution. Figure A.1 in Appendix A shows the corresponding graph relative to the PLSA minimum retirement living standard.

Figure 2.4. Who is affected by an increase in total contributions to 12% and who reaches (or exceeds) their target replacement rate in this scenario?

Note: The sample contains 25- to 59-year-old private sector employees saving into a DC pension in Round 7 of the Wealth and Assets Survey. We simulate their projected future retirement income under their current saving rate, and assuming that everyone saves at least 12% of total pay in all periods when above the earnings trigger, modelling everyone at the individual level and without accounting for future housing costs or inheritances. The graph then plots the share who are ‘affected’ (i.e. saving less than 12% of total pay currently), split by whether they are projected to reach their target replacement rate under both saving rates, and the share who are already saving at least 12% of total pay currently, again split by whether they are on track to reach their target replacement rate. The target replacement rate is based on those in Pensions Commission (2004). Earnings quartiles are based on pre-retirement earnings, i.e. simulated average earnings between ages 50 and 59.

However, the change would risk substantially increasing the proportion of people ‘oversaving’ compared with standard replacement rates, as shown by the yellow bars in Figure 2.4. This increase represents 38% of all private sector employees in DC schemes and 70% of those in the lowest quartile of the earnings distribution. Therefore, if the government were to go ahead with such a blanket increase in default minimum saving rates, we think there would be a strong case for making it possible – and relatively straightforward – for employees to opt back down to the current default rates of minimum total and employer contributions.

Instead of a blanket increase in minimum contributions, we think there is a strong case for saving at a higher rate than current defaults for some people in periods when they are on above-average earnings and for individuals in later working life who will tend to have relatively higher earnings and lower living costs. This is because an increase in contribution rates that also applied to lower earners and those at younger ages would in a majority of cases lead to oversaving relative to replacement rate benchmarks. We therefore suggest policymakers consider minimum default contribution rates that increase with earnings and potentially with age. Although this would add extra complexity to the schedule of contribution rates with respect to earnings, we think this extra complexity is needed to best help people make more appropriate saving decisions given the lack of a one-size-fits-all answer to how much people should be saving.

If certain groups are to be defaulted into higher rates of pension contributions (but not others), there is a strong case that any ‘extra’ should come on the part of higher total contributions and is not associated with a rise in employer contributions. This avoids any unfairness – whether real or only perceived – from some groups getting more of an increase in contribution rate from their employer than others. People facing higher minimum default contribution rates should have the ability to opt back down to the current minimum total contribution while maintaining an employer contribution of at least 3% of earnings.

Giving exact numbers for thresholds above which default rates should rise will always be somewhat arbitrary and there is much uncertainty around what default rate would be appropriate. This stems not only from uncertainty about the future but also from the difficulty of choosing one set of defaults to apply to a very diverse population and from uncertainty about how opt-outs will and should respond to any change.

Our modelling suggests that higher total contribution rates (i.e. including employer contributions), perhaps in the region of 10–12% of total earnings on the portion of earnings above £40,000 or £50,000, could be appropriate. There is a case for extending such an increase further down the distribution of earnings, to cover all those earning above the median (around £35,000) but this is less clear-cut. Generally speaking, there will always be a trade-off between bringing some undersavers up towards adequate levels of saving and defaulting some into rates that would result in them oversaving. In this context, the option to opt back down to the current defaults is key to ameliorating the downside risk.

It is worth nothing that this kind of change is basically a form of auto-escalation, where people are defaulted in to contributing higher fractions of their pay to a private pension when they receive a pay rise. Evidence from our public engagement work suggests that auto-escalation is a popular way to encourage people to save more, as indicated in the quote below.

‘I think it should be an option for all. It would be frustrating if this scheme was appealing to you but unfortunately your employer was not interested’

– Male, age 25–34

We further suggest that policymakers consider an additional increase in the default rate of total contributions for high earners aged 50 or over. For example, above-average-earning individuals could see their contribution rate escalate by 2% of earnings by default at age 50. We note that such an increase could result in people’s take-home pay falling after reaching the age threshold, so any such increases should be implemented with care.

As noted in O’Brien, Sturrock and Cribb (2024), there is a wide variety in preparedness for retirement of those currently over age 50. This may be due to the specific circumstances of their working life (significant DB provision for some but no automatic enrolment for most of their working life). But we do not know to what extent this divergence of circumstances may also characterise the saving trajectories of younger generations. Consequently, automatic enrolment default rates should be subject to a regular and frequent review – perhaps aligned with the periodic review of the state pension age and certainly not occurring less than once a decade – to ensure that they are set up to best support current savers.

Comparison with others’ proposals

Our proposals for higher default pension contributions for those on above-average earnings and above the age of 50 are a rather different way of encouraging saving compared with other proposals, such as a proposal from the Pensions and Lifetime Savings Association, or Broome et al. (2023), amongst others, for minimum contributions to be raised to 12% of all earnings, 6% from the employee and 6% from the employer.6 It is worth examining the differences between this proposal and our suggested way forward, focusing on the differences regarding employee contributions and employer contributions separately.

Regarding employee contributions, our suggested way forward focuses higher employee contributions on people who are earning at least median earnings. This does not mean that current low earners do not make higher contributions over their lives. In fact, many of them will do so because in the future they will become higher earners. Our proposal leaves lower earners with higher take-home pay to spend on current needs, put in a savings account or pay down debt. But it is also fair to say that our suggestion comes with some additional complexity relative to a more straightforward increase in contribution rates.

Compared with the proposal of 12% minimum contributions, our suggestion does not include a broad-based increase in employer contributions – though, as set out above, it does suggest some increases in employer contributions, to 3% of all earnings for (almost) all employees, most importantly affecting most of those who are not currently in a pension scheme at all.

Effects of increased employer pension contributions

It is important to carefully assess the potential impacts of increased employer contributions on employers and their employees. What might be the economic effects of higher minimum employer pension contributions? First, if there were no changes in wages or other forms of remuneration as a result of mandating higher pension contributions, this would mean a rise in the total compensation that employees receive and a rise in the cost of employing workers. This would benefit many employees, though it could also reduce demand for employees, leading to lower employment. One way it might lower employment is by increasing the incentive for employers to contract with self-employed workers instead of employing people directly.

However, there are likely to be at least some changes to wages following increases in mandated employer pension contributions. The extent to which wages do fall can be hard to predict, in terms of both theory and evidence. We first touch on the theory, before turning to the evidence in Box 2.1. The classic prediction emphasised in Gruber (2008) is that if the mandated benefit (such as an employer pension contribution) is valued as much as take-home pay by employees, then the cost of the additional benefit is likely to pass through entirely into lower wages. In the case of pension contributions, we might think that, on average, employees value these less than the equivalent value in take-home pay – for example, because some employees might be short-sighted and tend to undervalue the future, or because some have low earnings and do not want to save at that time. In this case, an increase in mandated employer contributions would not pass through one-to-one into lower wages. Manning (2001) also points out that mandated benefits might not pass through entirely into lower wages if employers have market power in the labour market.7

Box 2.1. Empirical evidence on incidence of mandated employer pension contributions

There is not a huge amount of evidence specifically on the effect of mandating higher pension contributions on wages. Here we summarise the evidence that is available.

Scarfe, Schaefer and Sulka (2024) study the roll-out of automatic enrolment in the UK between 2012 and 2016 to estimate effects on wages. They find that around half of the cost of higher pension contributions passes through into lower pay (particularly into lower overtime and other forms of additional pay, rather than basic pay). However, there is a lot of uncertainty around the magnitude of this pass-through into wages. Moreover, the effect on wages between 2012 and 2016, at the time when individuals are enrolled, is likely to be a lower bound on the pass-through into wages because it does not take into account any adjustments to wages that may have happened between the announcement of the reform and its implementation in late 2012, nor any impact after 2016. The central estimates from this study are therefore likely consistent with pass-through of employer contributions to wages of more than 50%, but there is considerable uncertainty around the magnitudes here.

We can also potentially learn from studies in other countries or for other forms of mandated benefits, such as mandated sick pay or maternity pay. On the one hand, Bosch et al. (2022) find that only about 30% of the cost of higher pension contributions in the Netherlands was passed through into lower pay. In contrast, Gruber’s (2008) review article summarised the literature then, which pointed towards the mandated benefits being passed entirely into wages in the long run. The evidence reviewed by Gruber (2008) includes studies that find that the entire cost of mandatory maternity health insurance (Gruber, 1994) and of general health insurance (Olson, 2002) passed through into lower wages.

There would also not be direct pass-through of increased contributions to lower wages for workers currently earning the minimum wage.8 In this case, increasing default employer contributions would make those minimum wage employees who remain in work better off, but there could be a potential reduction in the demand for these employees. In the medium run, the potential effects of the employer contributions would be a factor that would be relevant to the setting of the minimum wage and may well lead to slower increases over time.

Is there a case for increased employer pension contributions?

Given all this, what case is there for mandating that employers offer much higher levels of employer pension contributions?9 The answer will depend on how much the higher employer contributions lead to lower wages or employment of targeted workers and how much of the cost is passed on to others, through changes in wages, firm profits and prices. But, crucially, the case will also depend on how much weight a policymaker puts on any such effects – and risks of these effects – and how they trade these off against the boost to future retirement incomes from higher pension saving.

If increased employer contributions are offset one-for-one by lower wages, then the question at hand is relatively simple: is it a good idea to transfer a higher fraction of pay to retirement? If there is less than one-for-one offset of higher contributions by lower wages, then the trade-off is more nuanced. Is a total increase in compensation (pay plus employer pension contributions) worth a reduction in current pay? This will clearly depend on the extent that wages are reduced when contributions rise. But it also depends on how much current pay is valued versus pension contributions. We would expect that a smaller effect on wages is more likely when employees themselves value the pension contributions less. However, a policymaker might take a view that employees are placing insufficient weight on those pension contributions (perhaps due to myopia) and that the trade-off in terms of higher future retirement income in exchange for lower current pay is a good one.

If total compensation for targeted employees does increase, this must come at the expense of either lower demand and therefore employment of these employees, or lower wages or employment for other employees, or higher prices for consumers, or lower profits for firms. There is therefore a trade-off here, with the best option depending on how much weight the policymaker places on the redistribution towards those workers getting higher compensation. An additional consideration would be whether higher employer pension contributions are the best way to increase compensation, as opposed to – say – a higher minimum wage, or increased mandation of other benefits or rights such as paid annual leave.10

In sum, the more confident policymakers are (a) that employees need to transfer more resources to retirement, (b) that employees ought to value pension contributions at least as much as current pay, (c) that employers have significant market power, (d) that they are willing to risk the potential for lower employment and (e) that higher employer pension contributions are a better way to increase total remuneration compared with other policy options, the stronger the case for higher mandated employer pension contributions. Given the evidence is not clear-cut, different policymakers are likely to come to different judgements about the merits of higher mandated employer pension contributions.

Another consideration is the potential structure of employer pension contributions. Our suggested way forward is a fixed proportion of salary (3% of earnings), which means higher contributions in cash terms for higher earners. Policymakers could decide to have a different structure, such as a higher percentage minimum employer contribution for lower earners.11 While this has the possibility of redistributing towards low earners, with all the trade-offs set out above, it would have the additional unwelcome effect of incentivising employers to employ fewer people on higher hours, relative to more people on lower hours.

Finally, there is the question of timing of any increase in minimum (or default) employee or employer pension contribution rates. This has been considered by others before, including in a joint report from WPI Economics and Phoenix (2023). They sensibly suggest that increases in contribution rates should happen slowly over time, and that oversaving concerns would need to be examined or addressed. They also express concerns about increasing pension contributions when incomes have been falling following the cost-of-living crisis and suggest that increases could be paused during difficult economic conditions.

In addition to this, it is worth thinking about the potential timing for introducing our proposals for non-contingent employer pensions and higher default pension contributions for above-average earners and those over the age of 50. On the one hand, non-contingent employer contributions may need to be introduced more slowly than other increases in employer contributions as the former involve a slightly different automatic enrolment structure from the current one and would involve significantly more people saving in a pension plan. Employers and pension providers may need some time to adjust. This could provide time for the government to run a trial of the policy, if it so desired. A trial could potentially help policymakers understand the extent to which employers might need more guidance administering a reformed system.

On the other hand, because the increased default contributions we suggest only affect those on above-average earnings, who are more financially resilient, there is a good case for the government introducing these much more quickly than more broad-based increases that would affect lower earners. Either way, increasing contributions may be easier when earnings are growing faster than inflation.12 It may also be wise to increase them in April, as part of the fall in take-home pay from one month to the next could then be offset by slightly lower tax payments if tax thresholds were increased in line with inflation.

2.6 Accessibility of pension savings

There is a good case that some individuals would benefit from increased levels of liquid assets and some saving should be channelled towards this rather than retirement saving (Beshears et al., 2020). This is particularly important to consider because evidence suggests that higher minimum employee pension contributions have led to lower savings deposits and higher credit card debt (Choukhmane and Palmer, 2024). Given these concerns, there have been proposals for automatic enrolment to be used to divert income to an accessible savings pot (up to some limit, after which contributions go into an inaccessible pension), with the intention that this can be drawn on during periods of need (e.g. Broome, Mulheirn and Pittaway, 2023). The National Employment Savings Trust has piloted programmes like this as part of its sidecar savings trials (NEST Insight, 2023).

Such schemes could increase individuals’ abilities to weather some financial shocks, as they are more likely to build up a ‘rainy day’ fund that they could draw upon during working life, and it would only lead to additional pension saving if the liquid savings account reached a particular limit. Some who saved in NEST’s sidecar savings pilot did draw upon their accumulated pots and report that participating made them financially better-off (NEST Insight, 2023). However, defaulting employees into an increase in liquid saving funded through an increase in employee or employer contributions that applies to those on low levels of earnings has the disadvantage that for some (but not all) people it will mean reduced levels of take-home pay and reduced living standards if they do not draw on the liquid savings account – for example, if some employees are not aware of it or find it hard to access.

If there is a desire to use automatic enrolment to increase liquid savings then ideally this needs to be balanced against the need for incomes to fund current expenditures. A clear option to help achieve this balance is that some portion of contributions under the current set of defaults be first allocated to fill a liquid savings pot up to some cap (such as £1,000) before contributions instead then flow into their workplace pension. If there is a strong desire not to reduce levels of pension saving then, if the lower limit for qualifying earnings was reduced to zero, the resulting increase in contributions could be channelled into this accessible pot.

The taxation of contributions to these accessible pots would need to be considered. Given that contributions into these pots are not going into pension pots, which are inaccessible to individuals until at least 55, it would be most appropriate for these contributions to be treated like other pay and therefore not receive up-front tax relief. This would mean that withdrawals from these savings accounts could then be made without any further tax liability. Contributions into the pension pot, once the liquid savings account reached its cap, would attract up-front tax relief in the same way as other pension contributions.

3. The effects of our policy suggestions

In the previous chapter, we set out a range of suggestions on changes to the structure of automatic enrolment that different policymakers could pick from. In this chapter, we simulate the effect of one set of our suggested reforms on the distributions of retirement incomes and of take-home pay during working life, and compare its effects with those of two other commonly suggested reforms to automatic enrolment. There are, of course, other suggested reforms to automatic enrolment, including ones we suggest in this report and those suggested by other people; however, we restrict our attention to three different reforms to keep our analysis clear. We make the simplifying assumptions that no employee opts out of automatic enrolment as a result of the suggested policy changes and there is no employer non-compliance; in other words, all private sector employees saving into a defined contribution scheme save at least the default minimum contribution rates.13

The three reforms are:

- reducing the lower limit for qualifying earnings to zero (i.e. contributions ‘from the first pound’); this would mean default minimum contributions of 8% of earnings (with at least 3% coming from the employer);

- reducing the lower limit for qualifying earnings to zero and increasing the default minimum total contribution rate to 12% of earnings (with at least 6% coming from the employer);

- a set of the suggestions made in this report,14 i.e.

- everyone earning more than the new ‘employer contribution earnings trigger’ (suggested to be set at £4,000 per year) receives an employer contribution worth at least 3% of earnings between zero and the ‘upper limit for qualifying earnings for employer contributions’ (suggested to be set at the current upper limit for qualifying earnings, £50,270);

- everyone earning more than the ‘employee contribution earnings trigger’ (suggested to be set at £10,000 per year) has a minimum default total contribution rate of:

- 3% of the lower limit for qualifying earnings (£6,240 a year), i.e. £187.20, plus

- 8% of earnings between the lower limit for qualifying earnings and a new ‘AE upper-rate threshold’, which we set at £35,000 as that is around average full-time earnings, plus

- 12% of earnings between the AE upper-rate threshold and the ‘upper limit for qualifying earnings for employee contributions’ (suggested to be set at £90,000 per year).

Under all three reforms, all monetary parameters are assumed to be indexed over time in line with growth in average earnings.

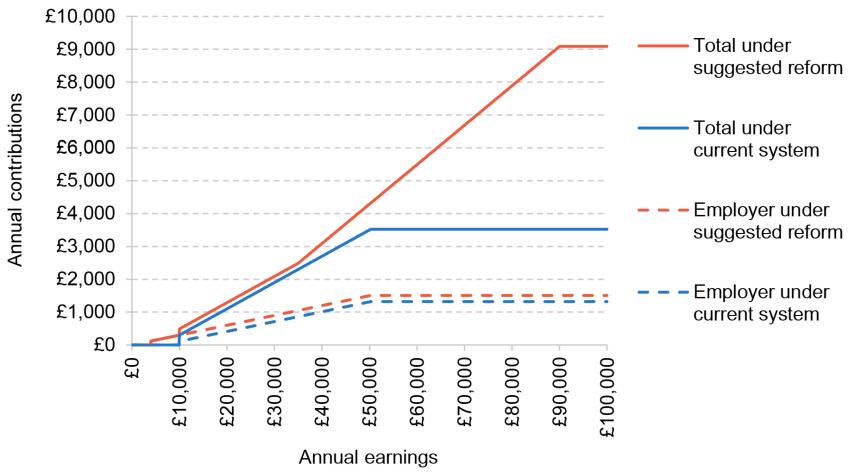

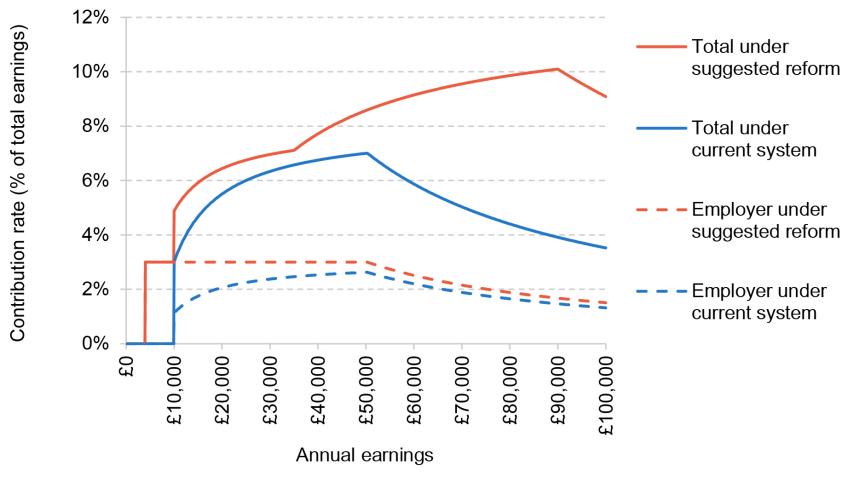

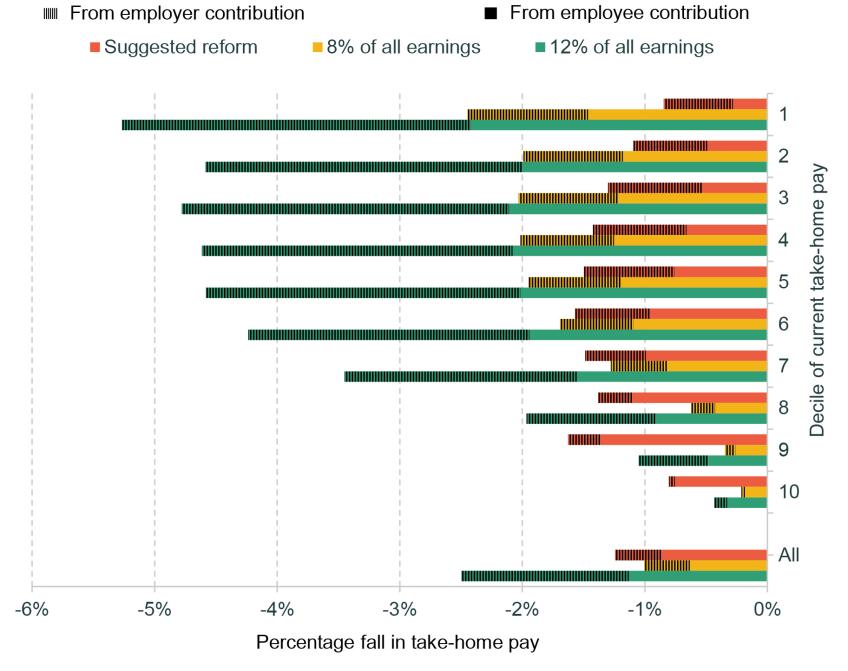

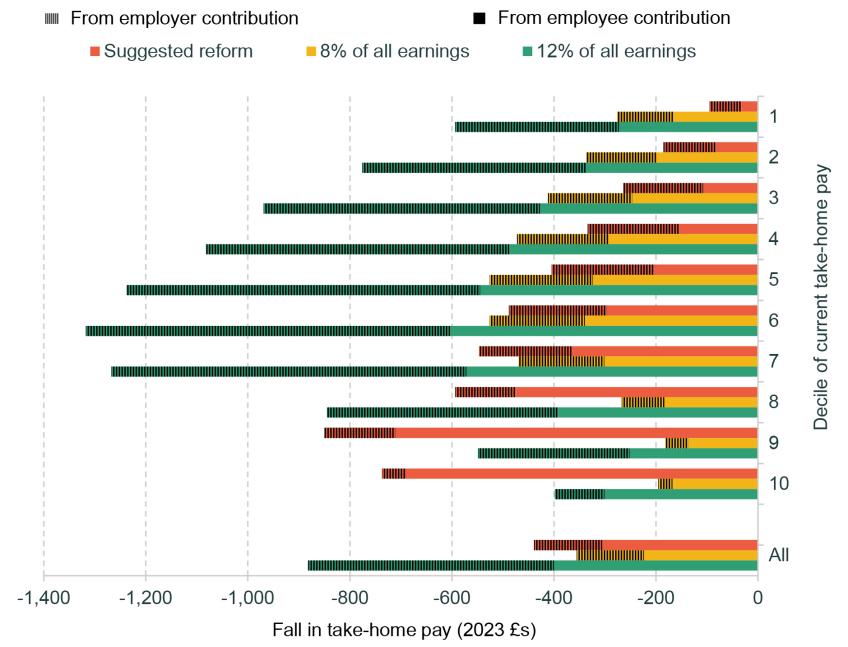

Figure 3.1 shows default minimum total and employer contributions, by earnings, under the policy suggestions in this report and under the current automatic enrolment system. We show the same graph but expressed as contribution rates as a proportion of (total) earnings in Figure 3.2. Two things stand out from these graphs. First, the suggested changes lead to larger increases in minimum default total contributions above median earnings than below. Second, the suggestions lead to an increase in minimum default employer contributions worth £187.20 per year for all employees above the earnings trigger (£10,000).15

Figure 3.1. Default minimum total and employer pension contributions, by earnings: current automatic enrolment system and policy suggestions in this report

Note: This figure shows default minimum total and employer contributions by annual earnings (for an employee with one job) under the current automatic enrolment system and under the policy suggestions in this report.

Figure 3.2. Default minimum total and employer pension contributions as a percentage of total earnings, by earnings: current automatic enrolment system and policy suggestions in this report

Note: This figure shows default minimum total and employer contributions, as a percentage of total earnings, by annual earnings (for an employee with one job) under the current automatic enrolment system and under the policy suggestions in this report.

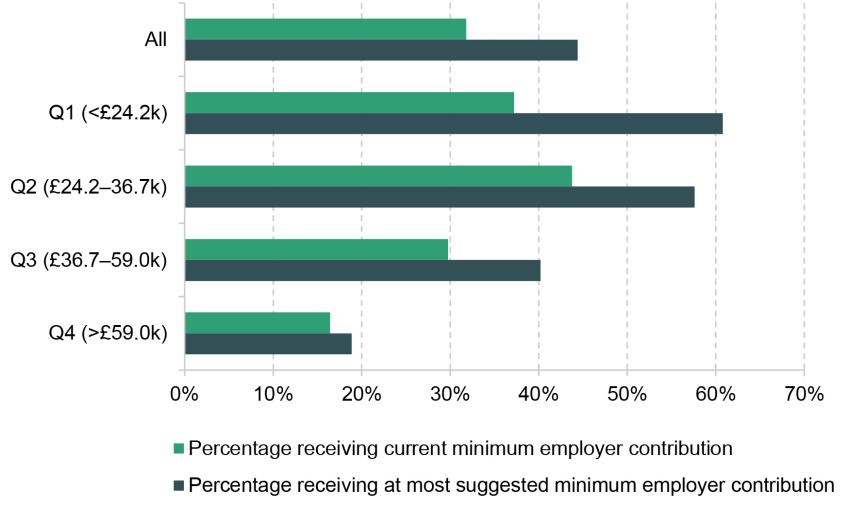

However, this does not mean that actual employer contributions will increase by the same cash amount for all levels of earnings. This is because those in the top quarter of the earnings distribution are much more likely to currently receive an employer contribution worth more than the current, and suggested, minimum amount than those in the bottom half of the distribution, as shown in Figure 3.3. This is consistent with the findings of Cribb et al. (2023b), who found that the average employer contribution rate was already (in 2019) 8% for the highest-earning fifth of private sector employees. Similarly, higher earners are also more likely to have total pension contributions above the current minimum: around four-fifths of private sector employees earning between £50,000 and £70,000 are saving more than current automatic enrolment minimum contributions, compared with fewer than three-fifths among those earning between £10,000 and £40,000.

Figure 3.3. Percentage of private sector employees saving into a defined contribution pension receiving an employer pension contribution of the current minimum and less than or equal to the suggested minimum, by current earnings quartile