Downloads

Download report PDF

PDF | 1.26 MB

Executive summary

There have been widespread concerns about the patterns of retirement saving amongst self-employed workers, who now make up just over one in eight of the whole labour force. Most strikingly, the fraction of self-employed workers earning over £10,000 who are making contributions to a private pension has been around 20% since the early 2010s. That compares with over 80% among employees. Self-employed workers who want to save in a pension must arrange their own personal pension, in contrast to most employees who will be automatically enrolled into a workplace pension by their employer. However, many self-employed workers have private pensions from previous employment, save in other forms of wealth, or are married to or cohabiting with someone who does have a workplace pension. The state pension system has also become more generous for the self-employed since the introduction of the new state pension in 2016. This report summarises the patterns of saving and wealth among the self-employed, including new modelling on the potential adequacy of saving for the self-employed compared with standard benchmarks. From the concerning trends we uncover, it is clear that reform is overdue; we therefore also set out some policy options for policymakers to choose between.

Key findings

1. The distribution of total wealth of the self-employed is similar to that of employees who are not currently saving into a defined benefit (DB) pension, while both of these groups have accumulated much less wealth than employees currently saving into a DB pension. A key difference is that the self-employed hold less of their wealth in private pensions and more of it in property wealth, financial wealth and, towards the top of the wealth distribution, business wealth. As with employees, there is substantial variation in the amount of wealth that self-employed workers have accumulated to date, with around a quarter of self-employed workers having no more than £10,000 in total wealth.

2. It is of particular concern that the direction of travel for the self-employed is quite different from that for employees. Among self-employed workers making annual profits of more than £10,000, only one in five is saving into a pension, down from three in five in 1998. Meanwhile, automatic enrolment has boosted workplace pension participation among employees earning more than £10,000 a year to over four in five. Many of the self-employed who do save in a pension make the same cash-terms contributions for many successive years, rather than increasing them as earnings grow, as typically happens with employees.

3. If the self-employed were to continue building up private pension wealth at their current rate, we project that around 55% of the self-employed would not have any pension savings to supplement their state pension entitlement in retirement. Consequently, in the absence of other private resources to fund retirement, two-thirds would not reach their Pensions Commission replacement rate benchmark (a percentage of pre-retirement income that is thought to approximate ‘smoothing’ of living standards from working life into retirement) and three-quarters would not achieve the ‘minimum income’ standard produced by the Pensions and Lifetime Savings Association. An important caveat to these results is that they assume that all today’s self-employed workers continue to save the same proportion of earnings into a pension as today for the rest of their career. This is unlikely to be the case for self-employed people spending significant time in future working as employees, for whom pension saving rates are higher.

4. These inadequacy rates are markedly higher for the younger self-employed than for those at older ages, with only one-fifth of 25- to 34-year-olds projected to reach their target replacement rate, compared with almost half of those in their 50s. This partly reflects the falling rate of pension participation over time among the self-employed. Adequacy in terms of replacement rates is lower for higher earners, reflecting the fact that the state pension replaces a lower share of their earnings and that private pension saving is not sufficient to bridge the remaining gap for most.

5. Although a larger proportion of younger age groups are currently not on track to hit adequacy benchmarks, the saving rates required to get back to those benchmarks typically appear to be more achievable for the young than for older people because they have a longer period over which to make up any saving shortfall. On average, self-employed workers not currently saving into a pension, aged 25–34 and in the third quartile of earnings (annual earnings of £22,200 to £39,000) would need to save 9% of their income to hit their replacement rate target. That compares with 18% for those in their 50s and in the same quartile.

6. An important point to bear in mind alongside these results is that the self-employed accumulate wealth in forms other than pensions. For those in their 50s, we find that including non-main-property wealth, financial wealth and business assets as sources of retirement income leads to 20% more of the self-employed being on track to hit their target replacement rate. Much of this increase comes from people higher up the wealth distribution who hold larger amounts of this other wealth. This means that the outlook for higher earners in younger age groups is in all likelihood better than the outlook in our central projections because they may subsequently accumulate these other types of wealth and use them to fund their retirement.

7. Once the resources of the partners, and the potential future inheritances, of the self-employed are taken into account, a larger proportion reach adequacy benchmarks, particularly among those with lower earnings. While individuals – and for that matter policymakers – may not want to rely on these resources being available and shared with the self-employed once they reach retirement, it does indicate that for a substantial proportion the outlook may not be as stark as individual-level modelling implies.

8. Together, this provides some concerning and some more reassuring evidence on the prospects for the retirement incomes of the self-employed. Reasonable people can differ on how much policy action is needed to make it easier for the self-employed to save for retirement. Nevertheless, in our judgement the status quo, in which self-employed people have to arrange their own pension plans without assistance, is no longer fit for purpose, particularly given the effort the state has put into making pension saving easy for employees and the extent to which the self-employed are no longer engaging with personal pensions.

9. We suggest policymakers choose between one of two options. One is to require all self-employed individuals filling out a self-assessment tax return to make an active choice about the level of pension contributions to make at that point (with zero being an option). Any contributions made would then go into either a nominated private pension plan, a government-chosen default pension plan or a Lifetime ISA. Evidence suggests this would boost pension participation, though there is some uncertainty about how much. While the increase would be expected to be smaller than under automatic enrolment, this might be considered appropriate given that for some – or indeed many – self-employed individuals, private pensions might not be the right saving option.

10. A second option would be a form of automatic enrolment, again operationalised through the self-assessment tax return, with HMRC selecting a pension provider if no decision was made by the individual. As defaults can be powerful, this should be limited to those with self-employment income above a certain trigger, perhaps set at the level of the equivalent trigger for employees or at the level of the new state pension. Default contributions could be introduced at a moderate level and increase over time to equal the default total contributions for an employee with the equivalent level of earnings. A straightforward way to opt out should be available for those who do not wish to make a pension contribution. Those declaring to be already making pension contributions on their self-assessment form could either be not enrolled or be enrolled with contributions equal to the default level minus their declared contributions. An option to instead divert savings to a Lifetime ISA could also be introduced.

11. To help self-employed people who are saving in a private pension save a more appropriate amount, the defaults on direct debit contributions should be changed. At the moment, contributions typically remain fixed in cash terms. A range of options for automatically increasing contributions each year should be provided, perhaps with a default of rising in line with the Consumer Prices Index.

1. Introduction

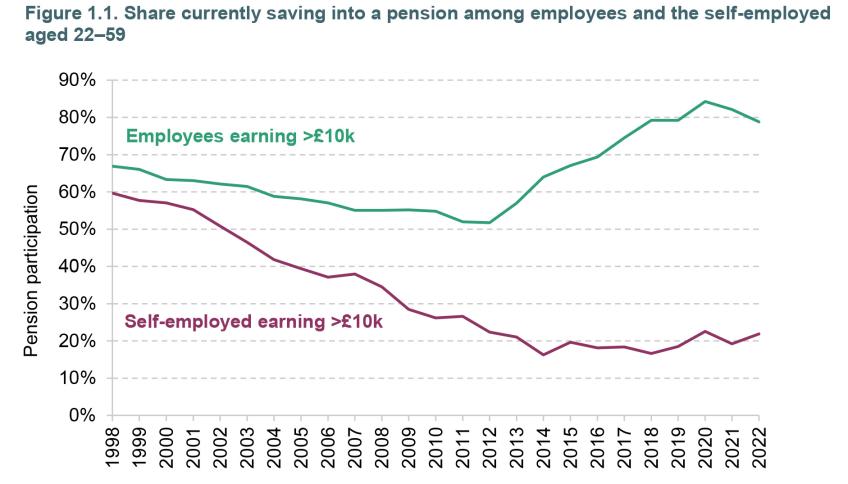

The self-employed make up an important part of the UK workforce. Around 13%, or just over one in eight, workers in the UK are self-employed and a much larger fraction of the workforce will spend some period of their working life in self-employment. However, there is a well-known challenge facing the retirement saving of self-employed workers: whereas the introduction of automatic enrolment has massively boosted the private pension participation of employees, there is no equivalent mechanism in place for the self-employed. And even concentrating only on those earning over £10,000 per year (who would therefore be targeted by automatic enrolment if they were employees), in 2022 only 22% of self-employed workers were saving in a private pension, as is shown in Figure 1.1. This is down from 60% in 1998 (though unchanged since around 2012, having fallen sharply between 1998 and 2012). In comparison, around 80% of employees earning over £10,000 per year were saving in a private pension in 2022. As Karjalainen (2023) showed, only a third of the decline in pension saving between the mid 2000s and mid 2010s can be explained by the changing composition of the self-employed workforce, such as the fact that they have lower levels of income, with two-thirds of this drop remaining unexplained.

Source: Authors’ calculations using the Family Resources Survey, 1998–2022. People with strictly positive earnings are defined as employees or self-employed based on their own self-reported main economic activity.

Given these trends, at the launch of the Pensions Review in April 2023, we identified the challenge of low levels of private pension saving among the self-employed to be one of the key challenges facing the UK pension system. And a challenge that was much more important than at the time of the Pensions Commission two decades ago, when self-employment was less prevalent and more of the self-employed saved in a private pension. This report seeks to understand better how prepared for retirement the self-employed workforce is likely to be based on current trends, and examine the case for policy reform to ensure adequate living standards in retirement.

This report presents the latest evidence on the potential retirement resources of the self-employed, looking not only at private pension wealth but at other assets too, including financial, housing and business wealth. We undertake new modelling to project retirement incomes for the self-employed on current trends, using the methodology set out in an accompanying report (O’Brien, Sturrock and Cribb, 2024), and judge these projected retirement incomes against commonly used adequacy thresholds. We examine how the fraction of the self-employed meeting these thresholds might change if they saved at levels closer to those undertaken by employees. Our findings suggest that reform is needed and therefore we also set out some policy options for policymakers to choose between.

2. The wealth and saving of the self-employed

In this chapter, we present key facts about the earnings, wealth and pension saving of the self-employed. Our sample for this analysis is self-employed workers aged 25–59 – consistent with the analysis we have undertaken on UK employees in O’Brien, Sturrock and Cribb (2024). Our key source of data is the Wealth and Assets Survey, supplemented by analysis from Cribb and Karjalainen (2023) which draws on HMRC’s self-assessment tax records data. In particular, we show how levels of wealth and private pension saving vary for those of different ages and with different levels of earnings.

Figure 2.1 shows the distribution of annual earnings for our sample of self-employed workers, measured in Round 7 of the Wealth and Assets Survey. For comparison, we also show the distributions of earnings among employees currently saving into a defined benefit (DB) pension and among employees not saving into a DB pension. This graph highlights that self-employed workers tend to have lower earnings than employees. Almost 20% of self-employed workers earn less than £10,000, compared with only 10% among employees not saving into a DB pension and 3% among employees saving into a DB pension. At the top end of the distribution, 16% of self-employed workers have earnings above £50,000, compared with over 20% of employees.

Figure 2.1. Distribution of earnings for employees saving into defined benefit (DB) pensions, employees not saving into DB pensions and the self-employed

Note: ‘Employees DB’ includes employees saving into a defined benefit scheme. ‘Employees not DB’ includes those saving in defined contribution pension arrangements and those who are not currently in any pension plan. People with strictly positive earnings are defined as employees or self-employed based on their own self-reported main economic activity.

Source: Authors’ calculations using the Wealth and Assets Survey, Round 7.

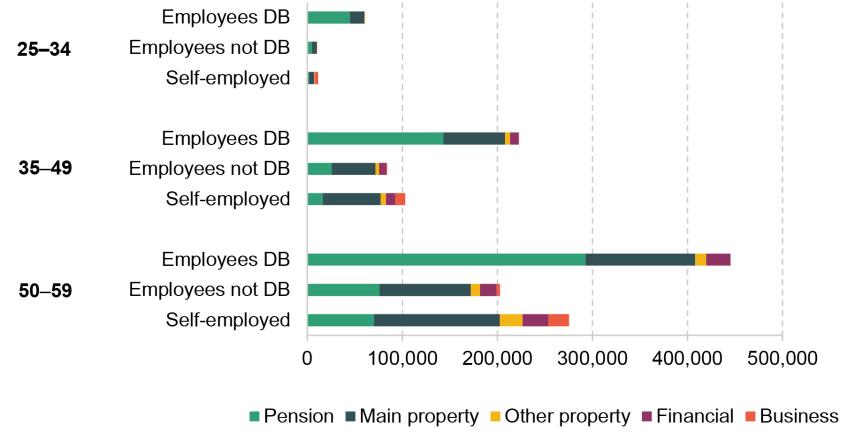

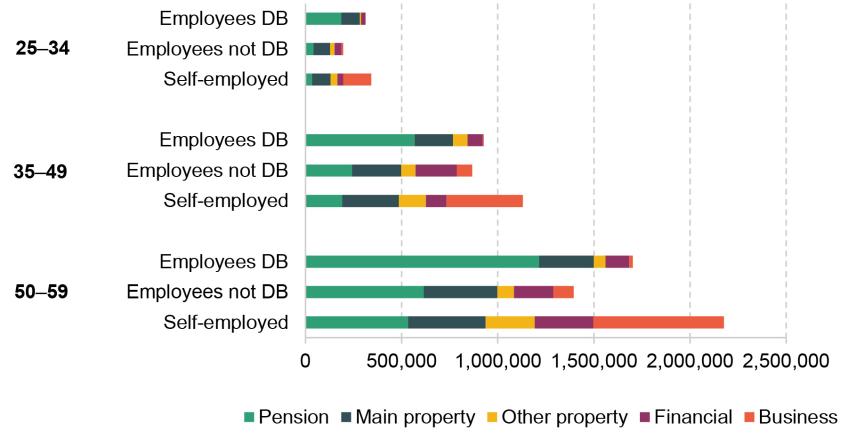

We move on to look at differences in average net wealth among these three groups in Figure 2.2, separately for three different age groups and splitting out different sources of wealth. As we would expect, older individuals have more wealth on average. Within all three age groups, the group of employees currently saving in a DB pension has significantly higher mean wealth than both employees not currently saving in a DB pension and the self-employed. This is mostly driven by high levels of pension wealth among employees saving in a DB pension, which is unsurprising given the generosity of most DB pensions.

Figure 2.2. Mean individual wealth among employees saving into DB pensions, employees not saving into DB pensions and the self-employed, by age group

Note: Property wealth is measured net of any mortgages on the property, and financial wealth is net of any non-mortgage debt.

Source: Authors’ calculations using the Wealth and Assets Survey, Round 7.

For all three age groups, mean wealth among self-employed workers is similar to and, if anything, slightly higher than among employees not saving in a DB pension. This is potentially surprising given that self-employed workers tend to have lower current earnings. Digging into the sources of wealth, we see that the self-employed have lower levels of pension wealth than employees who are not currently saving in a DB pension; however, they offset this with higher levels of average property wealth (particularly in additional properties) and business wealth. Figure A.1 in Appendix A shows average wealth by source for these three groups and three age groups, split separately for those in the bottom three-quarters of the wealth distribution and those in the top quarter of the wealth distribution. Business wealth is particularly concentrated at the top of the wealth distribution for the self-employed. However, even when ignoring business wealth, and looking at those in the bottom three-quarters of the wealth distribution, we find that average levels of wealth are similar for self-employed workers and employees not currently saving in a DB pension.

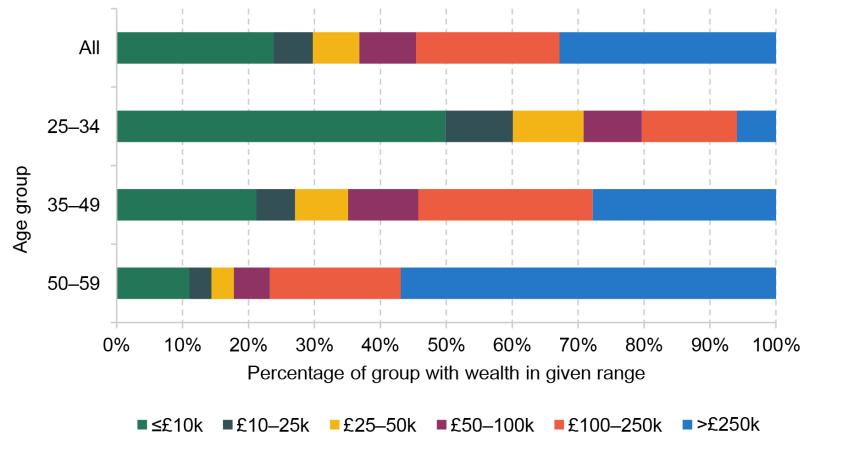

Figure 2.3 goes beyond looking at mean wealth and shows that there is a significant degree of dispersion in total wealth among self-employed workers. Overall, around a quarter of self-employed workers have no more than £10,000 in total net wealth, while a third have total wealth of over £250,000. This graph also shows how the distribution of total net wealth varies by age. Younger self-employed workers are particularly likely to have low levels of wealth, with almost half of the 25–34 age group having no more than £10,000 in wealth. In contrast, 57% of self-employed workers in their 50s have over £250,000 in total net wealth.

Figure 2.3. Distribution of total wealth among the self-employed, by age group

Note: Total wealth includes private pension wealth, property wealth (net of mortgages), financial wealth (net of financial debt) and business wealth.

Source: Authors’ calculations using the Wealth and Assets Survey, Round 7.

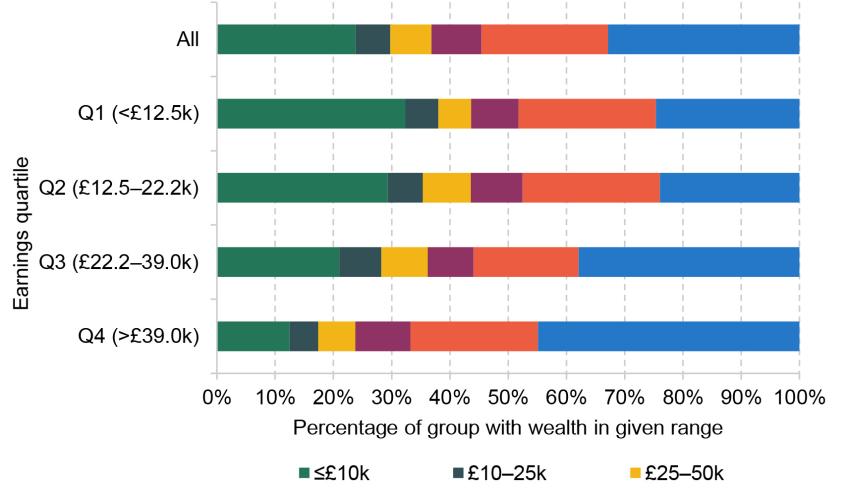

Figure 2.4 shows how the distribution of total net wealth varies for different quartiles of the earnings distribution among self-employed workers. The distribution of wealth is similar for the bottom and second-bottom quartiles of the earnings distribution, with around three in ten having no more than £10,000 in wealth. Those in the top quartile of the earnings distribution tend to have higher levels of wealth.

Figure 2.4. Distribution of total individual wealth among the self-employed, by earnings group

Source: Authors’ calculations using the Wealth and Assets Survey, Round 7.

Thus far, therefore, we have shown that self-employed workers have fairly similar levels of wealth to the set of employees who are not saving in a DB pension, despite tending to have lower levels of earnings. Underlying this average, there is a substantial degree of variation in wealth, even when comparing self-employed workers of similar ages or similar levels of earnings. Levels of wealth today reflect the accumulation of saving decisions in previous years (together with decisions on where to invest savings). Consequently, levels of wealth today might not be a good indicator of future trends in retirement wealth if saving decisions today and in the future differ from those in the past.

As was shown in Chapter 1, the fraction of self-employed workers currently saving into a private pension scheme has fallen to low levels. To examine the saving behaviour (rather than the stocks of wealth) of self-employed people in more detail, we show analysis undertaken by Cribb and Karjalainen (2023) using self-assessment tax data.1 Two key points emerge from their analysis, shown in Figures 2.5 and 2.6.

First, Figure 2.5 shows the share of long-term self-employed workers and employees who are saving in a pension for different levels of earnings, separately for 2011–12, before the boost to employees’ pension participation from automatic enrolment, and for 2014–15 (the latest year of data available at the time of the analysis). Middle- and higher-earning self-employed workers are more likely than their lower-earning counterparts to save in a pension. However, when it comes to the differences in pension participation between the self-employed and employees, the biggest gaps are not at the bottom of the earnings distribution, but across a broad swathe of the earnings distribution above £10,000. For those on earnings between £10,000 and £40,000, pension participation is at least 40 percentage points higher amongst employees than amongst similarly-earning self-employees in 2014–15. And the gap grew between 2011–12 and 2014–15 as automatic enrolment boosted employees’ workplace pension membership while participation in personal pensions by the self-employed continued to fall. This gap will likely have narrowed further since, as employees’ pension participation continued to grow with the continuing roll-out of automatic enrolment.

Figure 2.5. Share of self-employed workers and private sector employees saving in a pension, by earnings

Note: The self-employed are defined as of working age (ages 22–64) who have been self-employed for at least five years with no employment income.

Source: Reproduced from figure 2.1 of Cribb and Karjalainen (2023), which uses Annual Survey of Hours and Earnings and HMRC self-assessment data.

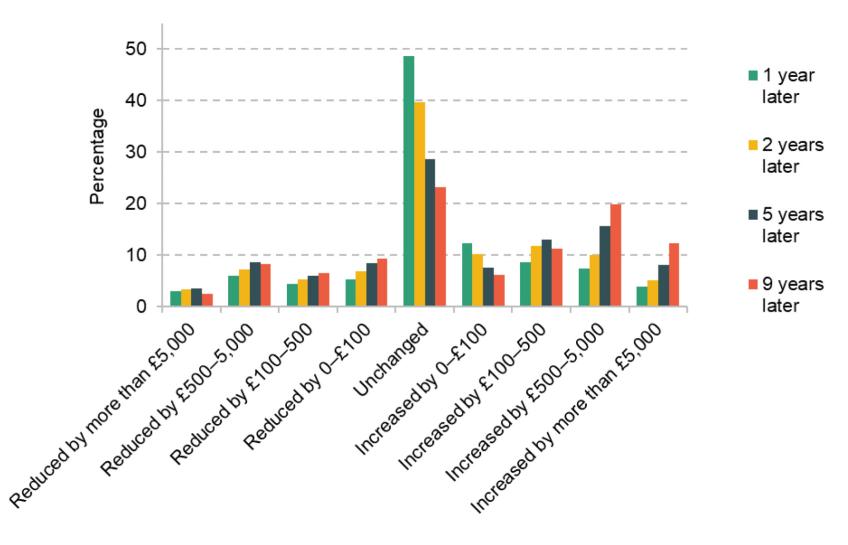

Second, Cribb and Karjalainen (2023) also identify a number of concerns with the contributions of self-employed people who do save in a private pension, as shown in Figure 2.6. It shows that, amongst self-employed people who do continue saving in a private pension scheme over time, large fractions of people keep saving the exact same cash amount. Nearly 50% of those saving in two consecutive years save the same amount in both years, and astonishingly around a quarter of those saving nine years apart still contribute the same amount. This is likely to be due to direct debits with defaults having cash-flat contributions over time – Cribb and Karjalainen (2023) find that almost a quarter of people have a ‘round number’ contribution (with £50 or £100 per month the most common) and that people with these ‘round number’ contributions are particularly likely not to change their contributions. 60% of those making ‘round number’ contributions who are saving nine years apart make the same cash-terms contribution in both years. This is in stark contrast to employees, whose contributions will tend to rise as (nominal) earnings rise. The fact that many people make contributions which stay the same over time was also something highlighted by some members of the focus group of self-employed workers that Ignition House ran as part of this project, as shown below.

‘I’ve kept the same since it started, but to be fair, I started quite low. It was only £60 so, you know, it was more like a top up.’

– Male, aged 35–44, homeowner

Figure 2.6. Change in contributions among self-employed workers saving in a private pension, over different periods

Note: The self-employed are defined as of working age (ages 22–64) who have been self-employed for at least five years with no employment income.

Source: Reproduced from figure 3.6 of Cribb and Karjalainen (2023), which uses HMRC self-assessment data from 2005–06 to 2014–15.

In summary, this chapter has shown that average levels of wealth among self-employed workers are broadly similar to average levels among employees, once we exclude those who are saving in defined benefit pension schemes. This is despite the self-employed having lower earnings than employees. However, the compositions of the wealth of the two groups are markedly different, with less private pension wealth and more additional property wealth on the part of the self-employed. This implies that, to some extent, self-employed people save in different ways from employees. Nevertheless, the trends in pension participation are concerning, not just because of much lower rates of pension participation compared with employees (and these rates have fallen significantly over time), but also because even amongst those who do participate in a pension, many self-employed people make the same cash contribution year after year.

3. Adequacy projections for the self-employed

In this chapter, we take the current saving situation and undertake new modelling to predict the distribution of future retirement incomes for today’s self-employed workers. We also compare these future retirement incomes with two measures of retirement income adequacy: the target replacement rates of the Pensions Commission (2004) and the PLSA ‘minimum retirement living standard’ (Pensions and Lifetime Savings Association, 2024). As discussed in detail in chapter 2 of O’Brien, Sturrock and Cribb (2024), under the target replacement rate approach, someone’s income in retirement is considered adequate if it maintains a certain proportion of the individual’s pre-retirement income, while the PLSA minimum retirement living standard is a single measure of the annual amount of expenditure needed to obtain a ‘minimum’ standard of living in retirement (and does not vary by pre-retirement income).

The key things to remember are that the replacement rate approach sets a target income that is a given fraction of pre-retirement income, meaning that if you have higher income in working life, you are expected to want to be on course for a higher income in retirement too. The exact percentage of income that is targeted decreases for those with higher levels of earnings. This accounts for the fact that those who earn more have, for example, higher tax rates and save more, and so can maintain their living standard even with some drop-off in (pre-tax) income at retirement. In contrast, the ‘minimum retirement living standard’ asks whether income is above or below a fixed line, though it is important to remember that just over one-third of working households do not have incomes that meet these lines in their working life.

At a high level, the modelling involves taking the set of 25- to 59-year-old self-employed workers in Round 7 of the Wealth and Assets Survey and simulating how much pension wealth they will have at retirement based on the pension wealth they have accumulated to date plus future pension wealth they are currently on course to accumulate in the rest of their working life. We assume that in all future years people save the same proportion of their earnings into their pension as they are currently. Importantly, this modelling also means that if an individual is not currently participating in a pension arrangement, ‘on current trends’ they will not make any further pension contributions. But – working in the other direction – those currently making pension contributions are assumed not to take a break from these at any point up to retirement, except for when they are not in paid work. Once people reach retirement, they are assumed to annuitise their private pension wealth and this annuitised income, together with state benefits (including the state pension), comprises their future retirement income.2 A more detailed explanation on how we project future retirement incomes is contained in section 4.2 and appendix A of O’Brien, Sturrock and Cribb (2024).

One caveat to this modelling is that, in our baseline approach, we do not model the accumulation of non-pension sources of wealth that could be used to fund living standards in retirement. We will therefore understate the future retirement resources of those individuals who accumulate more retirement wealth in non-pension sources. This is likely to be a more significant issue for the self-employed than for employees because, as shown in Chapter 2, the self-employed are more likely than employees to have significant wealth in non-pension assets, including housing, financial assets and business wealth. We therefore show how sensitive the results for 50- to 59-year-old self-employed workers are to including other sources of wealth at the end of Section 3.2.

3.1 Baseline projections

We start by showing the distribution of future retirement incomes under our baseline model. We do this for the sample of all 25- to 59-year-old self-employed workers in Round 7 of the Wealth and Assets Survey, where we model people at the individual level (rather than at the couple level) and do not yet account for future housing costs or the possibility of receiving an inheritance to fund living standards in retirement.

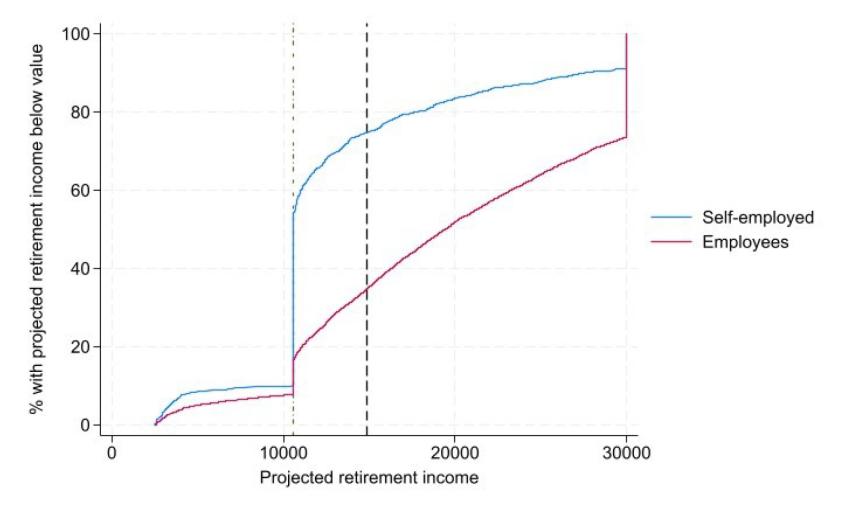

Figure 3.1 shows the distribution of projected (state plus private) pension income for the self-employed and for all employees. Each line in this figure shows the share of the group that have projected income below the value on the horizontal axis. The dashed vertical line shows the value of the PLSA minimum retirement living standard (just under £15,000 annually in pre-tax terms). The blue line for the self-employed crosses this dashed line at 75%, which means that three-quarters of self-employed workers are projected to have a retirement income below the PLSA minimum retirement living standard. In contrast, only around a third of employees are projected to have pension income below this level on current trends.

Figure 3.1. Distribution of projected pension income for the self-employed and employees

Note: Retirement incomes are measured in the first year of retirement (modelled to be between 60 and state pension age if modelled to be forced to leave work due to health problems or unemployment; otherwise at the state pension age). Those leaving work before state pension age may have an income below the level of the full new state pension upon leaving work (though their incomes will subsequently increase when they reach state pension age). The black dashed vertical line shows the value of the PLSA minimum retirement living standard. The green dashed-and-dotted vertical line shows the value of the new state pension. Retirement incomes are deflated to 2023 prices by the rate of average earnings growth.

Source: Authors’ calculations using the Wealth and Assets Survey, Round 7.

We can also see from Figure 3.1 that a large share – 44% – of self-employed workers are projected to have a pension income of exactly the level of the new state pension (at £10,600, given the analysis is based on the 2023–24 system), and another 10% have projected retirement income even below this level.3 This is mainly because a significant share, 52%, of self-employed workers in Round 7 of the Wealth and Assets have no private pension wealth and are not currently saving in a private pension. Therefore in this baseline version of the model, these workers will accumulate no private wealth with which to fund their retirement. This is a caveat to keep in mind when interpreting results from this baseline model for groups who we might expect to accumulate retirement wealth in other sources. We turn to this issue later.

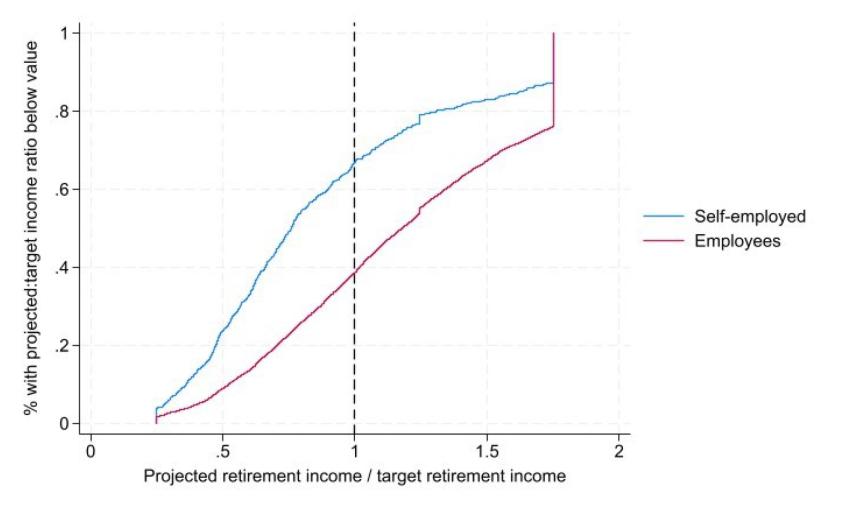

As shown in Chapter 2, the self-employed tend to have lower levels of earnings than employees. This could be one reason why the self-employed have lower projected pension incomes than employees. Figure 3.2 presents the distribution of the ratio of projected pension income to target retirement income under the target replacement rate measure, again both for self-employed workers and for employees. Reading up the dotted vertical line to the line for self-employed workers, we see that 67% of self-employed workers have a ratio of projected to target retirement income of less than 1; in other words, only 33% of self-employed workers are on track to achieve their target replacement rate. This compares with 61% of employees meeting their target replacement rates, highlighting that the lower retirement incomes for self-employed workers are not just because of their lower earnings, but also because they save less in pensions as a percentage of their income.

Figure 3.2. Distribution of pension income as a share of target retirement income for the self-employed and employees

Source: Authors’ calculations using the Wealth and Assets Survey, Round 7.

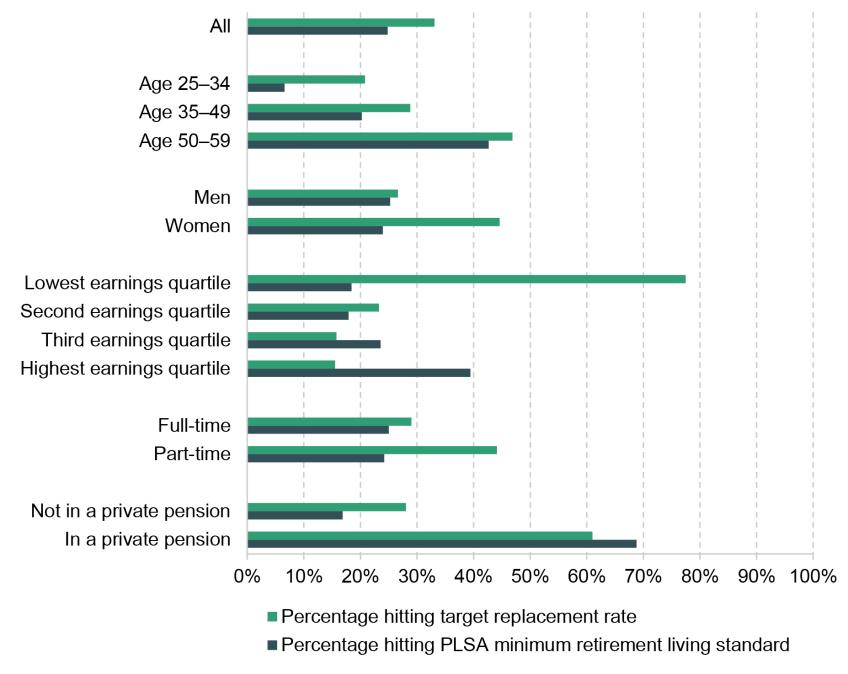

Figure 3.3 shows how the share of self-employed workers projected to reach measures of retirement income adequacy varies for different groups under our baseline modelling. Self-employed workers in their 50s are projected to be more likely than younger self-employed workers to hit both measures of adequacy. Indeed, only 7% of self-employed workers aged 25–34 are on track to hit the PLSA minimum retirement living standard in this baseline model specification, compared with 43% of 50- to 59-year-olds. This is consistent with younger self-employed workers having accumulated particularly low levels of pension wealth to date (as shown in Figure 2.2) and being especially unlikely to be saving into a pension (Cribb and Karjalainen, 2023).

Figure 3.3. Percentage of self-employed workers projected to hit different measures of retirement income adequacy, by group

Note: The sample includes 25- to 59-year-old self-employed workers in Round 7 of the Wealth and Assets Survey. We simulate their projected future pension income under our baseline assumptions, modelling everyone at the individual level and without accounting for future housing costs or inheritances. We then compare these future retirement incomes with the two measures of retirement income adequacy. Earnings quartiles are based on pre-retirement earnings, i.e. simulated average earnings between ages 50 and 59.

Source: Authors’ calculations using the Wealth and Assets Survey, Round 7.

There are different patterns in the shares meeting the two measures of adequacy by pre-retirement earnings. Those with lower levels of pre-retirement earnings are more likely to meet their target replacement rates, with around 80% of those in the lowest earnings quartile projected to be on track. This is because the flat-rate nature of the new state pension means that it will bring lower earners closer to achieving a given replacement rate than it does for middle or higher earners. On the other hand, those with higher levels of pre-retirement earnings are more likely to hit the PLSA minimum retirement living standard. The flat-rate new state pension will lift lower, middle and higher earners towards such a minimum threshold in a similar way, and any remaining shortfall is easier for higher than lower earners to make up through additional private pension saving. Nevertheless, the share of those in the top quartile of pre-retirement earnings achieving the PLSA measure is still only 39%. Only 27% of male self-employed workers are on track to hit their target replacement rate, compared with 45% of women, consistent with the fact that women tend to earn less than men.

Unsurprisingly, self-employed workers who are currently saving into a pension are significantly more likely to reach both measures of adequacy: 61% of self-employed workers currently saving into a pension are on track to hit their target replacement rate, compared with just 28% of self-employed workers not currently saving into a pension. This difference is even larger when comparing the share projected to have retirement income above the PLSA minimum retirement living standard (69% compared with 17%). However, as emphasised earlier, these shares might be underestimates, particularly for the group not saving into a pension, if they are accumulating resources for retirement in other forms of wealth.

Table 3.1 shows how much self-employed workers would on average need to save to achieve these measures of adequacy. It shows the median required pension contribution rate (as a percentage of total gross earnings) to reach both measures. We show this for all self-employed workers and also separately for those currently saving and not saving into a private pension. Among everyone, the median required pension contribution rate to achieve their target replacement rate (TRR) is 7%, while the median required rate to achieve the PLSA minimum retirement living standard is 6%. The median pension saver does not actually need to save any of their earnings to reach the PLSA minimum retirement living standard according to our modelling, and would only need to save 2% of earnings to reach their target replacement rate. This is because those self-employed who are saving in a pension tend to be older and to have already accumulated a fairly substantial level of pension wealth. However, even among those who are currently not saving into a private pension, median required saving rates are only 7–8% of earnings. This demonstrates that the key reason we find such low projected adequacy shares is not that the self-employed would have to save a large amount into their pension to reach these, but simply that so few are actually doing any pension saving at all.

Table 3.1. Median required pension contribution rate (as a percentage of earnings) to achieve adequate retirement income for everyone and separately for those currently saving and not saving into a private pension, by earnings quartile and age group

| Age group | Age 50–59 earnings quartile | Everyone | Pension savers | Not pension savers | |||

| TRR | PLSA minimum | TRR | PLSA minimum | TRR | PLSA minimum | ||

| All | All | 7% | 6% | 2% | 0% | 8% | 7% |

25–34 35–49 50–59 | All All All | 7% 9% 4% | 5% 6% 8% | - 3% 0% | - 2% 0% | 6% 9% 7% | 5% 7% 11% |

25–34 35–49 50–59 | Q1 Q1 Q1 | 0% 0% 0% | 11% 19% 22% | - 0% 0% | - 9% 11% | 0% 0% 0% | 10% 20% 22% |

25–34 35–49 50–59 | Q2 Q2 Q2 | 5% 7% 4% | 6% 9% 13% | - 2% 0% | - 3% 2% | 5% 7% 6% | 6% 9% 16% |

25–34 35–49 50–59 | Q3 Q3 Q3 | 9% 11% 17% | 4% 6% 9% | - 8% 12% | - 2% 0% | 9% 11% 18% | 4% 6% 10% |

25–34 35–49 50–59 | Q4 Q4 Q4 | 14% 16% 23% | 3% 3% 0% | - 15% 16% | - 0% 0% | 14% 16% 25% | 3% 4% 0% |

Note: TRR = target replacement rate. The sample contains 25- to 59-year-old self-employed workers in Round 7 of the Wealth and Assets Survey. We simulate the share of income they need to save to reach adequacy measures under our baseline assumptions, modelling everyone at the individual level and without accounting for future housing costs or inheritances. This table shows median required saving rates by age and pre-retirement earnings quartile across everyone in the group, and also separately for those currently saving and not saving into a private pension. Cells with fewer than 20 underlying observations have been suppressed and are shown as ‘-’.

The median required saving rates to hit the two adequacy benchmarks are not markedly different across age groups. This is despite the fact that older self-employed workers are much more likely to be on track to have an adequate retirement income (as shown in Figure 3.3). This is because older workers who are not on track to reach adequacy have higher required saving rates than younger workers, as they have fewer years of saving in which to make up the shortfall.

The required saving rates differ by pre-retirement earnings in line with the results on the shares meeting adequacy in Figure 3.3. The median required saving rate in the bottom quartile of the pre-retirement earnings distribution to achieve their target replacement rate is actually 0%, as the state pension already replaces a significant share of earnings for this group. On the other hand, required saving rates to achieve the PLSA minimum retirement living standard are fairly high for this group, at between 11% and 22%. We see the opposite picture for those in the top quartile of the pre-retirement earnings distribution: required saving rates to achieve the PLSA minimum retirement living standard are between 0 and 3%, compared with required rates of between 14% and 23% to achieve their target replacement rates.

3.2 Results accounting for partners, inheritances, the costs of private renting and other sources of wealth

In this section, we extend the baseline model in several ways to improve our understanding of the saving situation of today’s self-employed workers. The first extension is to account for the fact that many people live with a partner in retirement, and some of these partners are employees who are accumulating more substantial pension savings (particularly those with defined benefit pensions). In the previous section, we modelled everyone on an individual basis; however, in this section, we show what happens to our modelling results if we assume that people who are in a couple in retirement share their resources equally. To do this, we first restrict our sample of interest to self-employed workers currently aged between 35 and 59 (because of difficulties associated with modelling whether younger people will become part of a couple – and, if so, who with) and assume that those currently in a (cohabiting or married) couple will remain in the same couple into retirement. Overall, 80% of our sample of 35- to 59-year-old self-employed workers are in a couple (as measured in the Wealth and Assets Survey). Among these, 85% have a partner who is in paid work, 54% have a partner who is an employee and 61% have a partner who is saving into a pension.

The second extension is to show how our adequacy calculations might be affected by people living in private rented accommodation during retirement. We do this by first simulating which individuals will live in private rented accommodation in retirement. Then we assume that simulated future private renters will spend the same share of their income on rent in retirement as they do now and adjust the adequacy measures accordingly.4 Overall, 16% of our sample of 35- to 59-year-old self-employed workers are projected to rent privately in retirement, and on average they spend 30% of their income on rent.

We also show how sensitive the model results are to including inheritances. We model whether people might receive an inheritance in the future, and the value of these inheritances, based on work from Bourquin, Joyce and Sturrock (2020), and we assume that people use all the inheritance to finance their retirement. This will likely give an upper bound for the impact of inheritances on people’s retirement incomes, given that some people will, for example, leave some of the inheritance that they receive to their children.

For more detail on how we incorporate couples, housing costs and inheritances in the modelling, see appendix A of O’Brien, Sturrock and Cribb (2024).

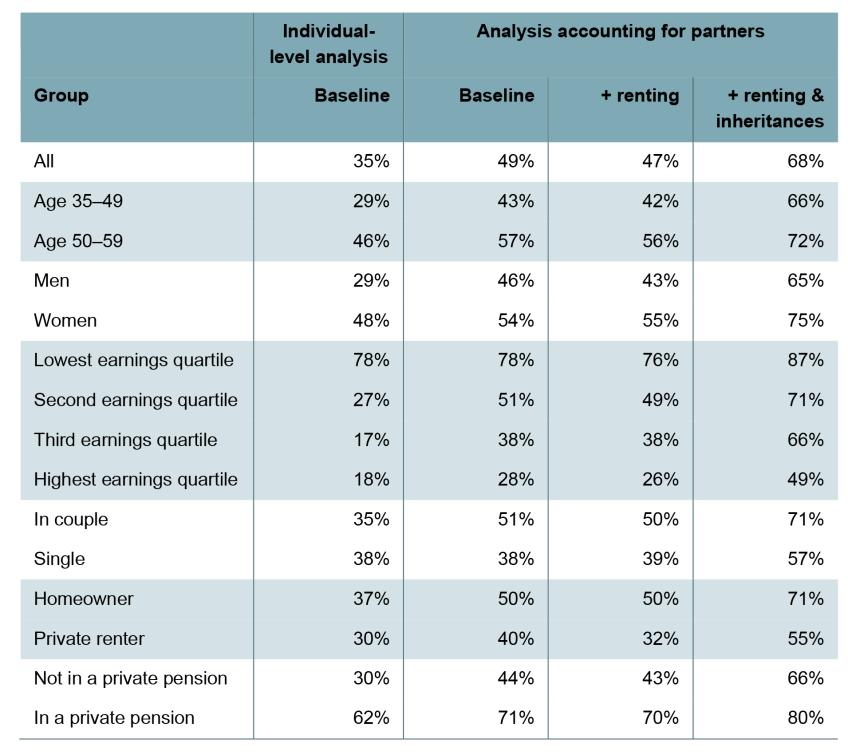

Table 3.2 shows how the share of self-employed workers (aged 35–59) projected to meet their target replacement rate is affected by these model extensions. In our baseline individual-level model, this share is 35%; however, moving the analysis to the couple level increases this to 49%. We see the largest increase in adequacy among those in the middle of the pre-retirement earnings distribution, but no change in adequacy for those in the bottom quartile consistent with this group tending to have a higher-paid partner, and people with higher earnings being less likely to reach their target replacement rate.

Table 3.2. Shares meeting target replacement rates when accounting for partners, and additionally private renting and likely receipt of inheritances

Note: The sample contains 35- to 59-year-old self-employed workers in Round 7 of the Wealth and Assets Survey. We simulate their projected future retirement income under our baseline assumptions. The first column shows the results when everyone is modelled at the individual level. The next column instead models couples jointly, assuming they share their incomes. The next column also incorporates housing costs for those living in private rented accommodation in retirement. The final column also includes the effects of future inheritances. We then compare future retirement incomes with the income needed to achieve their target replacement rate. Quartiles of age 50–59 earnings are measured across the population of self-employed people in the sample.

Source: Authors’ calculations using the Wealth and Assets Survey, Round 7.

Incorporating housing costs into the analysis for those modelled to live in private rented accommodation in retirement has only a small negative impact on the overall share on track to meet their target replacement rate. This is mainly because only a minority of the self-employed are projected to live in private rented accommodation in retirement. In addition, adequacy among specifically the group of future private renters only falls by 8 percentage points, from 40% to 32%. This decrease is somewhat tempered because people who are projected to rent privately in retirement are also modelled to rent privately during their 50s, and so they have low pre-retirement income (measured after housing costs), reducing the target income they have to aim for in retirement.

Incorporating future inheritance receipt into the modelling increases the shares modelled to reach their target replacement rate significantly: from 47% to 68% overall. The increase is larger for those aged 35–49 (42% to 66%) than for those in their 50s (56% to 72%), consistent with inheritances making up a larger proportion of lifetime income for later-born generations (Bourquin, Joyce and Sturrock, 2020). Three groups stand out as still having relatively low levels of adequacy in this specification: those in the top quartile of the pre-retirement earnings distribution (49%), single people (57%) and future private renters (55%).

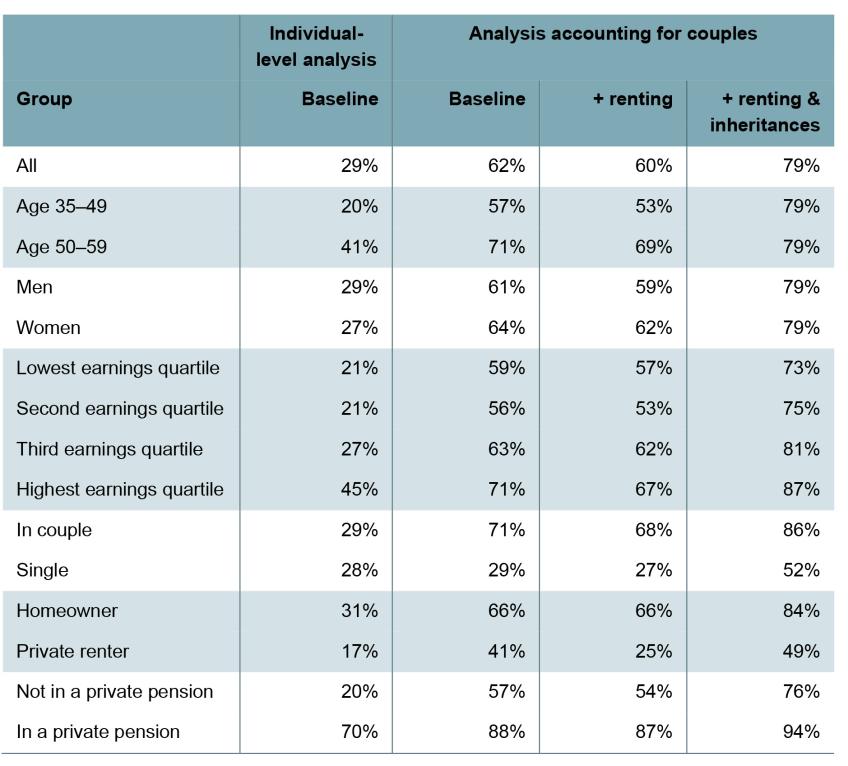

Table 3.3 shows the equivalent results for the PLSA’s minimum income standard. Moving the analysis from the individual to the couple level increases the shares reaching this measure of adequacy by even more than for the target replacement rates: from 29% to 62%. The increases are slightly larger for those in the bottom three-quarters of the pre-retirement income distribution, at 35–38 percentage points compared with an increase of 26 percentage points in the top quartile. We also see slightly larger increases in adequacy for homeowners (35 percentage points) than for future private renters (24 percentage points) and for those not currently saving in a pension (37 percentage points) than for those currently saving in a pension (18 percentage points).

Table 3.3. Shares meeting PLSA minimum income standard when accounting for partners, and additionally private renting and likely receipt of inheritances

Note: The sample contains 35- to 59-year-old self-employed workers in Round 7 of the Wealth and Assets Survey. We simulate their projected future retirement income under our baseline assumptions. The first column shows the results when everyone is modelled at the individual level. The next column instead models couples jointly, assuming they share their incomes. The next column also incorporates housing costs for those living in private rented accommodation in retirement. The final column also includes the effects of future inheritances. We then compare future retirement incomes with the PLSA minimum retirement income standard (which is uprated with average earnings growth). Quartiles of age 50–59 earnings are measured across the population of self-employed people in the sample.

Source: Authors’ calculations using the Wealth and Assets Survey, Round 7.

Accounting for housing costs for future private renters again only has a fairly small impact on the overall share reaching the PLSA minimum retirement living standard. However, this extension does lead to a larger decrease in the share of future private renters meeting the PLSA adequacy measure (16 percentage points, from 41% to 25%) than the 8 percentage points decrease (from 40% to 32%) we saw in Table 3.2 for the target replacement rate measure. This is because the PLSA measure is not affected by the fact that private renters in retirement will also be private renters during working life and so also have a lower level of disposable income then.

Finally, adding in the effect of future inheritances again leads to a significant increase in the share reaching adequacy. Overall, the share reaching the PLSA minimum income standard increases from 60% to 79%. Self-employed workers currently saving into a pension are particularly likely to be projected to achieve this standard, with an adequacy share of 94%. In contrast, single people and people projected to live in private rented accommodation in retirement have particularly low adequacy shares, at 52% and 49%, respectively. These two groups also stood out for being particularly unlikely to reach their target replacement rates in the previous table.

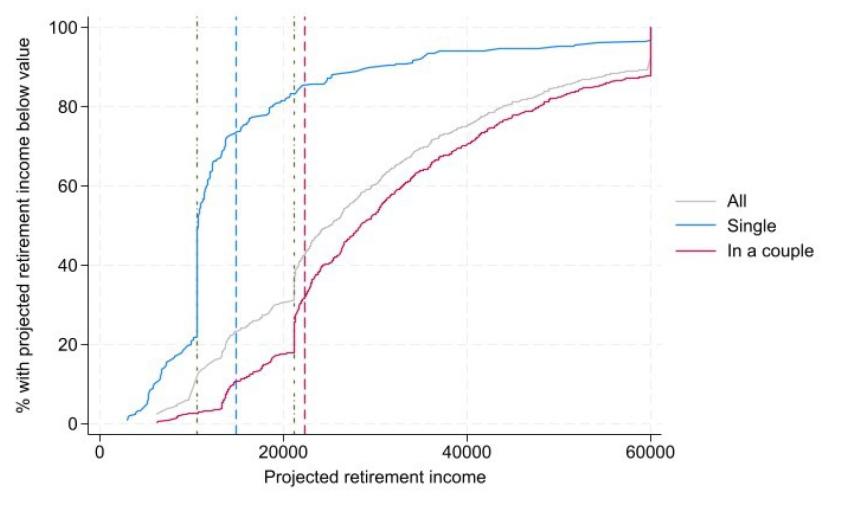

In Panel A of Figure 3.4, we show the distribution of future retirement incomes, both overall and separately for single people and people in a couple. This graph includes the impact of future housing costs, but not inheritances. The dashed vertical lines show the levels of the PLSA minimum retirement living standard, and the green dashed-and-dotted vertical lines show the levels of the new state pension, for single people and couples. This panel shows that a significant share of people, especially among single people, are projected to have a retirement income at the level of the new state pension on current trends. However, receiving just the full new state pension, but no private retirement income, is not enough to reach the PLSA minimum retirement living standard, whether the household has one or two members. On the other hand, as shown in Cribb et al. (2023), the full new state pension is set a level high enough for the vast majority of pensioner households – with the notable exception of single private renters in some parts of the country – to live above the poverty line. This highlights that the shares reaching adequacy are sensitive to the level of the income standard chosen, which will always be somewhat arbitrary. Choosing a slightly lower level for the PLSA minimum retirement income standard, or slightly increasing the level of the full new state pension, could lead to a significant change in the shares projected to reach the income standard.

Figure 3.4. Distribution of retirement incomes compared with PLSA standards and TRR incomes, combining incomes for partners, including private renting and excluding inheritances

Panel A. Projected retirement incomes compared with PLSA standards

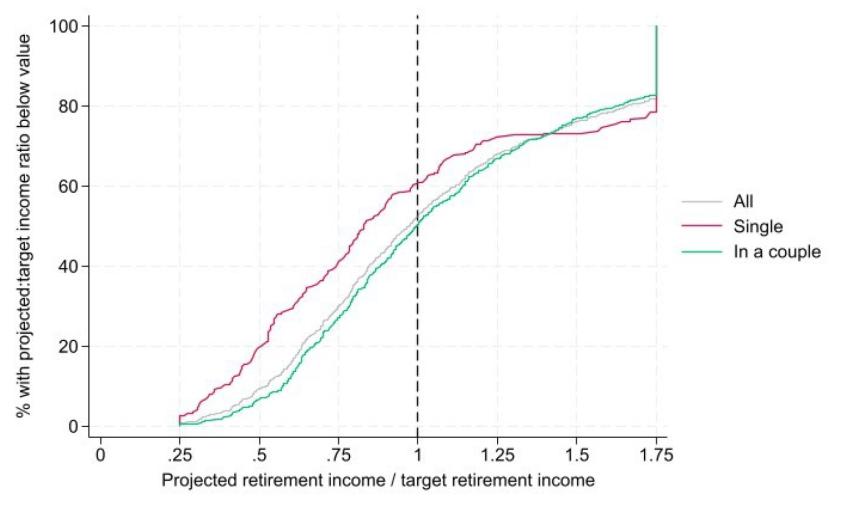

Panel B. Projected retirement incomes as a share of target retirement incomes

Note: The sample contains 35- to 59-year-old self-employed workers in Round 7 of the Wealth and Assets Survey. We simulate their projected future retirement income under our baseline assumptions, combining income for couples and accounting for housing costs for future private renters. Panel A plots the empirical cumulative distribution function of retirement incomes, deflated to 2023 by average earnings growth. The dashed vertical lines show the value of the (pre-tax) PLSA minimum retirement living standards, and the green dashed-and-dotted vertical lines show the levels of the new state pension, for singles and couples. Panel B plots the empirical cumulative distribution function of projected retirement incomes divided by pre-retirement income (average between ages 50 and 59 and again combined for couples).

Panel B of Figure 3.4 shows the distribution of the ratio of projected retirement income to the retirement income needed to achieve their target replacement rate, including income of the partner where appropriate. Again it includes the effect of future housing costs but not inheritances. It shows that a significant share of both single people and people in couples are projected to have retirement income significantly below that needed to reach their target replacement rate. Around two-fifths of single people and a quarter of people in a couple have projected retirement income at least 25% lower than that needed to reach their target replacement rate.

However, as emphasised throughout this section, these results only include pension saving (as well as future inheritances) and do not model the effects of retirement saving done through other means. This is potentially a problematic assumption for the self-employed, who are more likely than employees to have significant non-pension wealth. The results thus far can therefore be considered a lower bound on the shares likely to reach adequacy for the self-employed.

In Figure 3.5, we give a sense of how incorporating other types of saving and wealth into the analysis affects our results. Modelling the accumulation of all types of assets over people’s working lives is beyond the scope of this report. We therefore look at those aged 50–59, who are later in working life, and assume that the non-pension and non-primary-residence assets they hold at that age will also be used to fund retirement. To do this, we take the stock of wealth they have accumulated and assume this grows in line with asset-specific rates of return until retirement, and then assume all this wealth is used to fund retirement income. Our measure of wealth includes non-primary-residence properties, financial assets and business assets and is net of all debt other than any mortgage relating to a primary residence. To the extent that self-employed workers accumulate wealth for retirement after we see them in the survey, we will understate their retirement incomes, and vice versa if wealth is spent down before retirement. See O’Brien, Sturrock and Cribb (2024) for full details on this modelling extension.

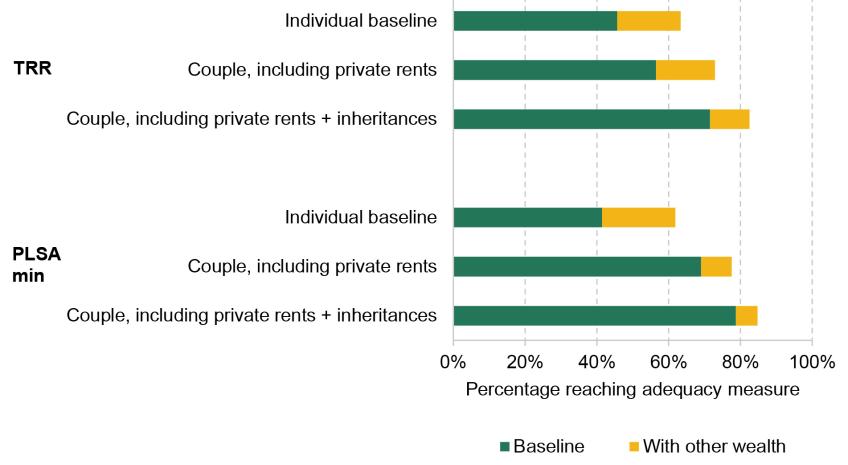

Figure 3.5. Effect of including other types of accumulated wealth in modelled adequacy for self-employed workers aged 50–59

Note: The graph shows the share of 50- to 59-year-old self-employed workers who are projected to achieve their target replacement rate or the PLSA minimum retirement living standard. The green bars show the share meeting these measures of adequacy when only including (state plus private) pension income, while the yellow bars show the extra share meeting adequacy when also allowing people to accumulate retirement wealth in non-main properties, financial assets and businesses. We show this for our individual baseline model, and also show the effects of including partners’ income and future housing costs, and including inheritances too.

Figure 3.5 shows the share of 50- to 59-year-old self-employed workers who are projected to reach both measures of adequacy with and without the inclusion of other wealth. We do this for the individual baseline model, the model incorporating the effect of couples and housing costs, and the model incorporating the effect of couples, housing costs and inheritances. For the individual-level model, the incorporation of other wealth into the analysis increases the share reaching both measures of adequacy by around 20 percentage points, with adequacy shares of just over 60% in both cases.

We see smaller increases in adequacy for the couple-level analysis, particularly for the PLSA minimum retirement living standard, and after the inclusion of inheritances, partly because the shares reaching adequacy are higher before incorporating other types of wealth. In the version without inheritances, including other types of wealth increases the share reaching their target replacement rate by 16 percentage points, from 56% to 73%, and the share reaching the PLSA minimum retirement living standard by 9 percentage points, from 69% to 78%. When including inheritances, the increases are 11 percentage points for the target replacement rate measure (from 72% to 83%) and 6 percentage points for the PLSA standard (from 79% to 85%).

Summary

There have been concerns about the retirement saving of the self-employed in the UK in recent years, given low levels of private pension participation. Unsurprisingly, we find very low shares of the self-employed are on track to have an adequate income in retirement when considering only their individual private saving in pensions and the state pension. We project that only a third of self-employed workers are on track to achieve their target replacement rate and that this fraction is higher among those with low earnings (for whom the state pension is a larger share of their earnings). Only a quarter are on track to hit the PLSA minimum retirement living standard (concentrated amongst higher earners). We find particularly low shares reaching these measures of adequacy for self-employed workers aged under 35.

There are some important caveats to these results, which means that looking at individual private pension wealth of the self-employed presents at best a partial picture. First, many self-employed workers have a partner who is saving into a pension. Accounting for the fact that people may share resources with their partners, the shares reaching adequacy rise to 49% for the target replacement rate measure and 62% for the PLSA minimum living standard (although this analysis is restricted to those aged 35 and over). Second, our headline numbers are based only on pension saving and we assume that people who are not saving in a pension today will not ever save into a pension, which might not be a good assumption for those who spend time working as employees in the future. Self-employed workers might fund their retirement incomes through means other than pension saving. For example, they may receive an inheritance before retiring, or save in other, non-pension, forms of wealth. Incorporating inheritances into the analysis for those aged 35–59 increases the shares reaching their target replacement rate to 68% and reaching the PLSA minimum living standard to 79%.

For those in their 50s, we also show that including non-pension wealth in the analysis can further boost adequacy shares. Overall, while the concerns about low pension saving rates of the self-employed are justified, there is a great degree of uncertainty about exactly what the distribution of future retirement incomes among today’s self-employed workers might look like.

3.3 The effects of increasing retirement saving

In this section, we show the effects of higher saving rates on the proportion meeting adequacy benchmarks. Unlike with employees, who are often subject to automatic enrolment, there is no single obvious saving rate to consider. However, we show the impact of moving all self-employed individuals who earn more than £10,000 and who are making pension contributions of less than 8% of their total earnings up to that level.

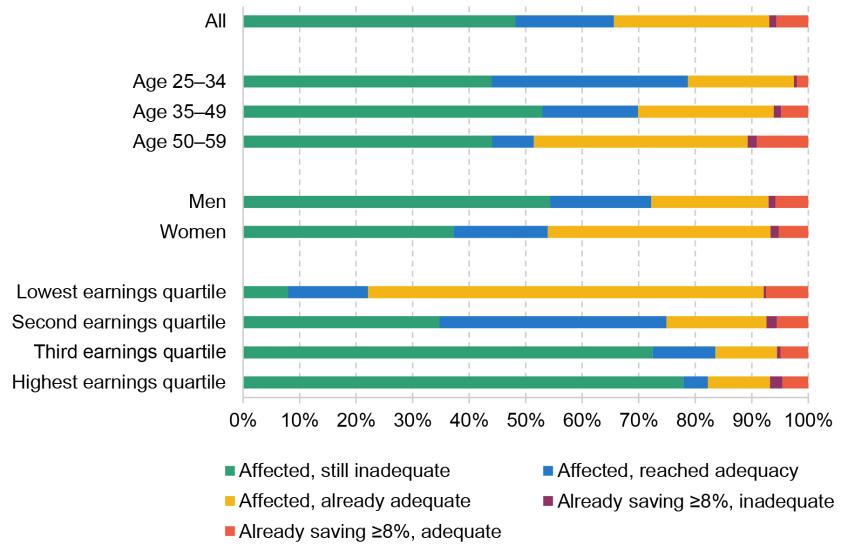

Figure 3.6 shows the impact that bringing all self-employed people earning over £10,000 up to a saving rate of 8% would have on a target replacement rate measure of adequacy. This modelling is on an ‘individual baseline’ basis, therefore not considering the impacts of partners’ incomes, renting, inheritances or other assets. Looking at the overall results, the yellow bar shows that almost 30% of individuals would be affected by such an increase but are already reaching adequacy, while around 15% (the blue bar) would be brought up to meeting their target replacement rate.

Figure 3.6. Who is affected, and who reaches (or exceeds) their target replacement rate, if all self-employed people save at least 8% of total earnings when earning more than £10k (earnings-indexed) per year: individual baseline model results

Note: This figure shows how the shares achieving their target replacement rates would change if all self-employed workers had to save at least 8% of total earnings into their pension when earning more than £10,000 per year. These calculations are based on our ‘individual baseline’ model simulation for the sample of 25- to 59-year-old self-employed workers in Round 7 of the Wealth and Assets Survey. Those who currently contribute less than 8% of total earnings to their pension are affected by the reform; we calculate whether they would reach their target replacement rate if they instead saved exactly 8% of total earnings when earning at least £10,000 per year. The green bar shows the share who are not projected to achieve their target replacement rate in this scenario, the blue bar shows the share who are projected to achieve it under this scenario but not under the status quo with their current saving rate, and the yellow bar shows the share who are projected to reach it even under the status quo. The purple bar shows the share who are already saving at least 8% of earnings into their pension (and so are not affected by the reform), but are not projected to achieve their target replacement rate. The last (red) bar shows the share who are already saving at least 8% of earnings into their pension and are projected to achieve their target replacement rate. Earnings quartiles are based on modelled pre-retirement earnings, i.e. average earnings between ages 50 and 59.

Almost half of individuals would not meet their target replacement rate even after their saving rate was increased to 8% (the green bar). Those who are saving less than 8% but already reaching their target replacement rate are primarily low earners, while those for whom 8% is not ‘enough’ are predominantly middle and high earners. A large part of those who would be brought up to their replacement rate are those in the second quartile of earnings, for this moderate amount of private saving is around the level required to meet their target replacement rate.

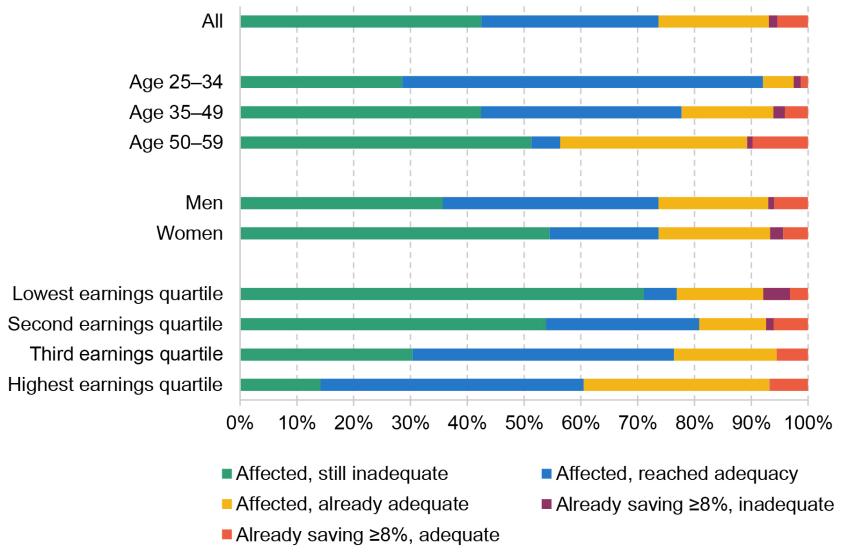

When considering the PLSA minimum income benchmark (Figure 3.7), bringing saving rates up to at least 8% once someone is earning over £10,000 would substantially increase retirement income adequacy for higher-earning self-employed people but have only a small impact among the lowest earners. Indeed, Table 3.1 shows that the median required pension contribution to achieve this benchmark is between 11% and 22% for those in the bottom earnings quartile. There are particularly large impacts of moving to 8% among those aged 25–34. Relatively modest amounts of pension saving have the potential to bring the majority of this group up to a minimum income standard in retirement.

Figure 3.7. Who is affected, and who reaches (or exceeds) PLSA minimum retirement living standard, if all self-employed people save at least 8% of total earnings when earning more than £10k (earnings-indexed) per year: individual baseline model results

Note: This figure shows how the shares achieving the PLSA minimum retirement living standard (RLS) would change if all self-employed workers had to save at least 8% of total earnings into their pension when earning more than £10,000 per year. These calculations are based on our ‘individual baseline’ model simulation for the sample of 25- to 59-year-old self-employed workers in Round 7 of the Wealth and Assets Survey. Those who currently contribute less than 8% of total earnings to their pension are affected by the reform; we calculate whether they would reach the PLSA minimum RLS if they instead saved exactly 8% of total earnings when earning at least £10,000 per year. The green bar shows the share who are not projected to achieve the PLSA minimum RLS in this scenario, the blue bar shows the share who are projected to achieve it under this scenario but not under the status quo with their current saving rate, and the yellow bar shows the share who are projected to reach it even under the status quo. The purple bar shows the share who are already saving at least 8% of earnings into their pension (and so are not affected by the reform), but are not projected to achieve the PLSA minimum RLS. The last (red) bar shows the share who are already saving at least 8% of earnings into their pension and are projected to achieve the PLSA minimum RLS. Earnings quartiles are based on modelled pre-retirement earnings, i.e. average earnings between ages 50 and 59.

Figures A.2 and A.3 in Appendix A show the results when including partners and housing costs in the analysis. As highlighted previously, a higher share reaches adequacy benchmarks under current projections on this basis (this is partly because this modelling also omits the youngest age group). Overall, the impacts of bringing saving rates up to 8% are more modest than when considering only individual resources. The differences across groups are less marked, reflecting the fact that the partners of those in each group will be diverse in their pension provision.

4. Policy responses

The analysis in the previous chapters has shown that self-employed workers have relatively similar levels of wealth to private sector employees (excluding those currently saving in defined benefit schemes), though less of it is contained in private pensions. But the trajectory of saving implies less future accumulation of private pension wealth than among employees, as over half of self-employed workers neither have any retained private pension wealth nor are currently saving in a private pension. Those who do participate in private pension schemes often make the same cash contributions year after year. Concern around these trends will be more significant for those who are long-term self-employed and therefore spend little time as (automatically enrolled) employees.

Assuming that they continue to save at their current low rates, many self-employed workers are therefore likely to have little pension income in excess of the state pension. Our modelling suggests that if this were the only source of retirement income resources, most self-employed workers would not be on track to meet the PLSA’s benchmark for a ‘minimum’ standard of living in retirement. This is especially true for the many self-employed workers who have low incomes during working life. On the other hand, this group will have a reasonable replacement rate generated by the new state pension, which is much more generous to the self-employed than the pre-2016 state pension system that it replaced. Furthermore, many self-employed people also accumulate wealth (on top of any main property wealth) in forms other than private pensions, or have a partner with a private pension, or stand to receive a substantial inheritance.

These findings are nuanced and, for people interested in the retirement income adequacy of the self-employed, there are both worrying and reassuring elements to them. Given this, there is likely to be a range of reasonable opinions on the appropriate policy response.

One reason that there will be different judgements on this is that it is less clear (compared with the situation for employees) that private pensions are the best savings product for self-employed people. Many self-employed workers may want to hold savings in an accessible form as they face more income volatility than employees and they may want to invest in their business. Indeed, Karjalainen (2023) finds that self-employed people with more volatile incomes are less likely to save in private pensions. This is also highlighted in the quote below, from a self-employed worker who participated in one of the focus groups Ignition House ran for us as part of this project. Lifetime Individual Savings Accounts (LISAs) in particular may be a better long-term savings product for many basic-rate taxpaying self-employed workers, both because they are more liquid and because self-employed people are not able to receive employer contributions to pensions.

‘If you’re employed, you’re on a fairly fixed monthly income or weekly income, whatever it might be. So you know roughly what’s going to be coming each month. If you know what your income’s going to be for the next six months or 12 months, you can start to make plans for what you want to do with it. In my position, I don’t know what my income’s going to be in the next couple of months, let alone six months, because it’s up and down. So, I don’t have that certainty of what’s coming in the longer term.’

– Male, aged 35–44, private renter

In addition, there is more hassle cost for self-employed savers setting up a private pension than there is for employees. Currently, self-employed people who want to start saving in a private pension have to choose and approach a firm that offers personal pensions, and set up a personal pension with it, whereas automatically enrolled employees can save in a workplace pension without having to make any decisions at all. Personal pensions also typically have higher fees than workplace pensions.5

That being said, private pensions are still in many ways a good savings product for many self-employed workers: they are a (significantly) tax-advantaged way of saving for retirement – even for basic-rate taxpayers not receiving an employer contribution6 – and help people with savings ‘commitment’ problems by locking away some of their savings until a later age. By investing in an appropriate mix of assets including equities and bonds, they allow individuals to have a diversified portfolio in a way that can generate much higher returns than available in a cash ISA, though a similarly diversified portfolio can be arranged in a ‘stocks and shares’ ISA or a LISA. Investing in additional property is much less tax advantaged, and involves much less diversification of risk, than saving in a private pension.

The remainder of this chapter sets out the key options that policymakers face regarding how to help increase pension participation amongst the self-employed, which includes setting out our judgement on the appropriateness of each of these options. We additionally highlight some recommendations for helping those self-employed people who are saving into a pension to save an appropriate amount.

The status quo

Keeping with the status quo might be justified by a policymaker stressing the fact that many self-employed people are well served by the new state pension (in particular in comparison with the pre-2016 state pension system), that they on average accumulate similar amounts of wealth to employees not in defined benefit pension arrangements and that private pensions may not be the best savings product for the self-employed.

However, our judgement is that staying with the status quo would not be appropriate. While pensions are not the right product for everybody, they can play an important role in locking away wealth to help fund expenditure in retirement, and the assets typically invested in provide an appropriate balance of risk and return for most people. And for most they are tax-favoured. Low rates of private pension participation – and much lower than was seen in the late 1990s – particularly amongst the long-term self-employed, are therefore concerning.

Moreover, there is a fairness argument about how the structure of the private pension system treats employees and the self-employed. Government legislation has made it easy for an employee who should be saving in a private pension scheme: if they do nothing, they will save into a workplace pension. In contrast, the hassle cost, and the number of decisions (which company to go with; how much to save; potentially which assets to invest in) needed, are much higher and more complicated for the self-employed. We therefore judge that the status-quo can, and should, be improved upon.

Option 1: requiring an active choice

As noted in the quote below, self-employed people face hassle costs to participate that employees do not. The first option we suggest is for government to introduce reforms to reduce the hassle cost for the self-employed to participating in a private pension plan. For example, HMRC could require self-employed people to make an ‘active choice’ as to whether they make a pension contribution when filling out their self-assessment tax return. Under this option, for those with self-employment income, a section on the self-assessment form would require individuals to decide whether they want to make any (additional) contributions to a private pension plan. There could be no default value filled in on the form; instead, the box would be empty and self-employed people would have to enter a number for how much they wish to contribute. But the form could tell them what the minimum default pension contribution for an employee with the same level of income would be (and how that compares with any pension contributions they had already reported on their self-assessment return). If an individual were to choose to make contributions, funds would be withheld by HMRC and invested in the plan chosen by the individual. Where the individual did not make a choice of plan, a government-chosen default provider would be used. This would be similar to what was in the past done with Child Trust Funds in cases where the parent did not open an account. These plans should have appropriate default investments so that self-employed individuals are not obliged to make their own investment decisions (although they should be free to move away from the defaults). There would also need to be a minimum level of contributions for those who did decide to participate (i.e. contributions would have to be at least a certain amount in cash terms). And, of course, the individual would be free to select that they wished to make no pension contribution that year. Individuals could be offered the option of saving into a Lifetime ISA instead of a pension; this may be a good option for basic-rate taxpayers, for whom a Lifetime ISA is a particularly tax-advantaged form of savings.

‘If you’re employed, somebody basically says: here’s a pension scheme set up for you – do you want to opt-out - yes or no? I appreciate it can’t be quite that straightforward for self-employed, but ideally, for me it’d be something similar where I don’t have to worry about setting the scheme up. I don’t have to consider various options. It’s a case of here’s a basic scheme, do you want it?’

– Male, aged 35–44, private renter

A key benefit of integrating this within the self-assessment scheme would be that HMRC could highlight how much less tax the individual was paying as a result of contributing, and indeed the individual would immediately face a lower tax bill upon completing self-assessment. However, making pension contributions at this point would lead to an additional outgoing at the same time as paying their income tax and National Insurance bill. But with low incomes for most self-employed people, tax bills are generally not enormous and those who do pay income tax are used to keeping funds aside to pay them. Median pre-tax self-employment income for the self-employed in 2022–23 was around £18,000, meaning an income tax and National Insurance bill of around £1,400 (under the 2024–25 tax system). Making a pension contribution of 8% of their earnings would equate to £1,440 but would reduce their up-front income tax bill by £288. A significant fraction of self-employed people will owe almost nothing in tax each year upon completing their self-assessment tax return due to their low incomes.

There is mixed evidence on the extent to which active choice frameworks lead to higher rates of pension or savings participation, although it is clear that effects on participation are lower than for automatic enrolment, which generally leads to participation rates of between 70% and 95% (see table 1 of Beshears et al. (2023) for a summary). There is evidence of ‘active choice’ leading to a substantial boost in participation in at least two cases. Carroll et al. (2009) find that new hires into a US firm are 28 percentage points more likely to save in a defined contribution pension plan if they have to make an ‘active choice’ compared with standard ‘opt in’ enrolment. Patterson and Skimmyhorn (2022) study an active choice framework in the US army defined contribution pension plan and find it increases pension participation by 11 percentage points compared with a baseline of ‘opt in’ enrolment of 11%. An example of a less successful boost to savings is found in a paper by Holmes Berk et al. (2024), who find that compared with ‘opt in’, the active choice framework boosted participation by only 2–3 percentage points for a few months, but effects diminished after that. A difference here is that the savings plan was not a pension scheme but instead a short-term liquid savings account.

In sum, requiring self-employed people who are filling out their self-assessment tax return to make an active choice on whether they want to make contributions to a private pension scheme would be a light-touch way of facilitating pension saving for the self-employed. It should be seriously considered by policymakers. Prior evidence is unclear as to the size of the increase in participation it would generate. But irrespective of the exact effects, there is a good case for policymakers to at least make it much easier for those who do want to save in a pension scheme to do so.

A final benefit of the active choice system is that policymakers would not be obliged to choose default contribution rates, and they could make this option available to all self-employed people irrespective of their earnings, with little worry that they are nudging low earners into inappropriate saving decisions. This could be considered particularly important for the self-employed given their extremely varied circumstances and trajectories. Under this option, the only default would be that the self-employed would be required to make a choice over whether or not to participate in a pension (or LISA).

Option 2: automatic enrolment

An alternative option would be for the government to use the HMRC self-assessment to implement a form of automatic enrolment for self-employed individuals. There are various ways that this could work, from more light-touch ways to ways that would introduce much more hassle cost to opting out, or indeed introduce financial incentives into the mix.

The way to do this would be to introduce a new part of the self-assessment form (as described above) and to have private pension participation as the default, with a pre-calculated default contribution (based on the profits they declare) filled in, which could be changed up or down by the individual. Again, the individual would be able to nominate a scheme, and where this was not done they would use a government-chosen default provider. As discussed earlier, policymakers could alternatively choose to make enrolment in a Lifetime ISA a default, or make it an option for people to choose instead of a pension.

Given how strong default options and automatic enrolment are (see discussion earlier and the evidence in Beshears et al. (2023)), this would need to be targeted only at self-employed individuals for whom the government was confident it was appropriate that they should be saving for retirement. This could imply introducing a ‘trigger’ for automatic enrolment that was similar to the level of the employee earnings trigger in automatic enrolment (currently £10,000). Or it could be higher than this – a key reason currently not to raise it substantially for employees is that they may lose an employer contribution from doing so, but this would not be a concern for the self-employed, who do not receive an employer contribution. An appropriate trigger could therefore be close to the level of the full new state pension (currently around £11,500).

Policymakers would also have to decide on what an appropriate default contribution rate for the self-employed could be. They may want to start lower and then consider increasing it over time as evidence comes in on behaviour, as was done during the roll-out of automatic enrolment for employees. A good starting point could be 4% of self-employed profits (which would attract tax relief, therefore topping it up to 5%). Over time, the objective could be to increase this to the same minimum level of default contributions in place for employees (currently 8% of qualifying earnings), though this could be revised in the light of how well the initial introduction lands and how the self-employed respond. For those declaring some private pension contributions on their self-assessment form, the default contribution amount could be reduced by the amount of their declared contributions.