Downloads

Download report PDF

PDF | 1.23 MB

Foreword

This eighth annual report from the Institute for Fiscal Studies provides another authoritative picture of education spending in England at a time of significant change. While overall public spending on education remains close to historic lows as a share of national income, the demands on the system are anything but static. The government has set ambitious goals for opportunity and social mobility, but these commitments must be delivered against a backdrop of tight fiscal constraints and rising costs.

Demographic trends are reshaping pressures across the system. Falling pupil numbers in primary schools contrast with continued growth in student numbers in post-16 education and higher education, creating uneven challenges for budgets and infrastructure. These shifts present choices for policymakers. They must decide whether to use smaller numbers in some phases to make savings, or to reinvest in improving quality and reducing class sizes. At the same time, the expansion of early years entitlements represents one of the most significant policy shifts in a generation: transforming the scale of government support for childcare to enable parents to work, while raising questions about sustainability and the balance between universal and targeted provision.

Perhaps the most acute pressure lies in special educational needs and disabilities (SEND). Spending on high needs provision has almost doubled over the past decade, driven by rising numbers of pupils with Education, Health and Care Plans and shortages of places in state-funded special schools. The Office for Budget Responsibility forecasts a £6 billion gap between expected spending and funding by 2028–29. The White Paper on schools and SEND – likely to be published soon after this report – will be pivotal in determining whether reforms can slow this growth while improving provision for children with the greatest needs. Action will be essential: without it, these pressures risk crowding out resources for mainstream schools and constraining the system’s ability to deliver a broad, balanced and high-quality education for all.

Higher education faces its own set of challenges. The indexation of tuition fees and the planned reintroduction of maintenance grants will bring some relief for students, yet the long-term balance between public and private contributions remains contested. Meanwhile, further education and skills – long the relative loser in funding settlements – must adapt to new policy ambitions and rising demand.

This report, as with its predecessors, does more than track spending. It illuminates the hard choices policymakers face in aligning resources with priorities. It shows where funding growth is concentrated, where it falls short of costs, and how these patterns shape opportunities for children and young people. For those designing policy, the evidence here is indispensable. But it is also an invaluable resource for those involved in various ways in holding policymakers to account.

The Nuffield Foundation is proud to support this project as part of our overall mission to advance social well-being and create a fairer, more inclusive and more prosperous society. This requires an ambitious and well-functioning education system. These annual reports are part of a wider body of work, with regular deeper-dive reports collated on the programme’s microsite. This analysis of the funding of education provision is an important backbone for our large portfolio of research on early childhood development, school improvement, skills and transitions to adulthood. Understanding how resources are deployed is fundamental to improving outcomes.

The annual reports have a strong track record in changing the terms of public debate and informing decision-making at critical moments. This report is particularly well timed in that respect. The challenges are substantial, but so too is the opportunity to ensure that investment in education delivers for all learners, especially the most vulnerable children and young people.

Josh Hillman

Director of Education, Nuffield Foundation

Preface

This report is the eighth in a series of annual reports on education spending in England. The authors gratefully acknowledge the support of the Nuffield Foundation, which has funded this series of annual reports (grant number EDO /FR-000024394). The Nuffield Foundation is an independent charitable trust with a mission to advance social well-being. It funds and undertakes rigorous research, encourages innovation and supports the use of sound evidence to inform social and economic policy, and improve people’s lives. The Nuffield Foundation is the founder and co-funder of the Nuffield Council on Bioethics, the Ada Lovelace Institute and the Nuffield Family Justice Observatory. This project has been funded by the Nuffield Foundation, but the views expressed are those of the authors and not necessarily the Foundation. Find out more at: nuffieldfoundation.org; Bluesky: @nuffieldfoundation.org; LinkedIn: Nuffield Foundation.

The authors also thank the Economic and Social Research Council for support via the ESRC Centre for the Microeconomic Analysis of Public Policy (grant number ES/Z504634/1), which underpins much of IFS’s research.

The authors would like to thank the members of the advisory group, officials from the Department for Education and colleagues at IFS, who have commented on and greatly informed the analysis in this report.

This report uses a range of data releases from the Department for Education, its predecessors, related agencies and non-departmental bodies. These are all listed in the sources below individual figures and/or in the methods section of our microsite, which houses all our analysis of education spending (https://ifs.org.uk/education-spending). The IFS student finance model draws on National Pupil Database data linked to data from the Higher Education Statistics Agency (HESA). It also uses data from the Family Resources Survey and the University of Essex’s British Household Panel Survey. Several chapters use data from the Office for National Statistics (ONS) Quarterly Labour Force Survey. The National Pupil Database is Crown Copyright and made available by the Department for Education. HESA data are Copyright Higher Education Statistics Agency Limited. Neither the Department for Education nor Higher Education Statistics Agency Limited nor HESA Services Limited can accept responsibility for any inferences or conclusions derived by third parties from the data.

The views and analysis presented in this report are those of the authors alone. Any errors or omissions are also their responsibility.

Executive summary

This is the eighth IFS annual report on education spending in England funded by the Nuffield Foundation. It provides consistent comparisons of the level of and changes in spending per student across different stages of education. We also analyse the resource pressures and choices facing policymakers for each stage of education. Our dedicated website further provides easy access to our latest analysis, figures and methodology (https://ifs.org.uk/education-spending). All figures quoted are in 2025–26 prices and relate to England unless otherwise stated.

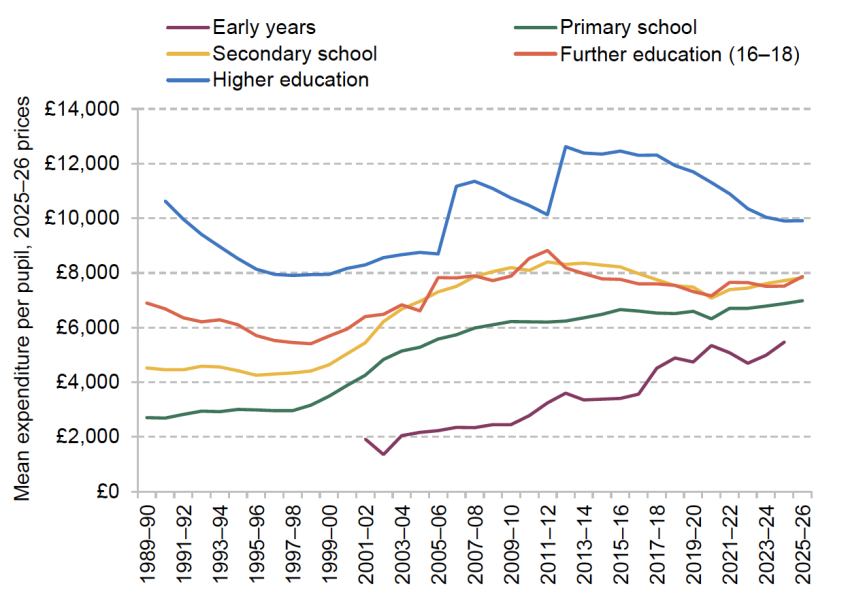

Looking at spending per pupil for the most recent year of data (2025–26, unless otherwise stated):

- Early years: £5,500 per child in 2024–25 (double compared with 2010–11)

- Primary schools: £7,000 per pupil (+12% since 2010–11)

- Secondary schools: £7,800 per pupil (–3% since 2010–11)

- All school spending (including wider spending): £8,400 per pupil (same as in 2010–11)

- Further education: £7,900 per student aged 16–18 (–8% since 2010–11)

- Higher education (up-front spending on teaching only): £9,900 (–5% since 2010–11)

Spending per pupil or student per year at different stages of education (2025–26 prices)

Total public spending on education

- The latest data (for 2024–25) show that total public spending on education in the UK was £122 billion (in 2025–26 prices). This represents a 10% or £14 billion fall since 2010–11, with this drop mostly reflecting a shift in the cost of higher education from the taxpayer to graduates.

- Public spending on education has also fallen as a share of national income, from about 5.6% of national income in 2010–11 down to about 4.1% in 2024–25. This equals the historic lows seen in the late 1990s, late 1980s and mid 1960s. There has been no long-run increase in the share of national income devoted to public spending on education, despite rises in post-compulsory education participation over the long run.

Early years

- Total public spending on the ‘free entitlement’ to funded childcare hours reached £8.7 billion in 2025-26 – double the total spending envelope from two years earlier. This increase in spending reflects the introduction of major new entitlements covering children under 3 in working families. This is the latest, and biggest, step change in early years policy. Spending is more than eight times as high as in the early 2000s – a significant change in the scope of the state over the last 25 years.

- Taking in all public spending on childcare support (including support through the tax and benefit systems as well as support for students), childcare spending reached £8.4 billion in 2024–25 and will be around £10.5 billion in 2025–26. After falling sharply during the late 2010s, spending through the tax and benefit systems has stabilised.

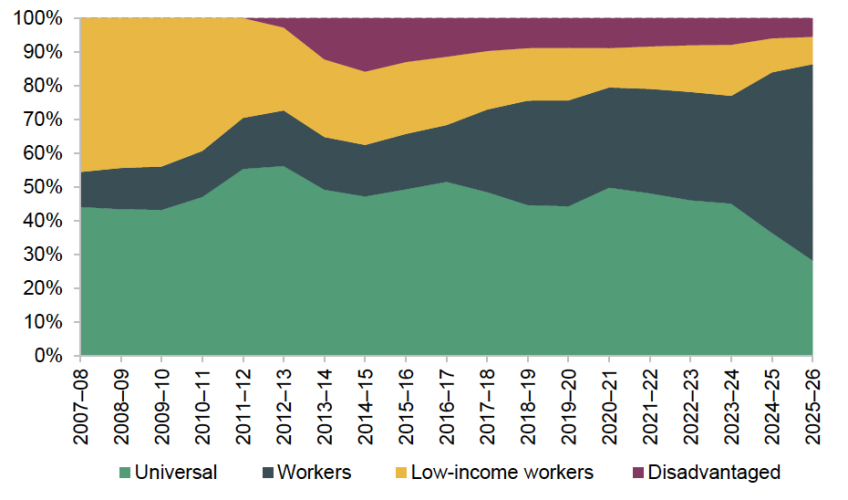

- New childcare entitlements, targeted at working families, are reshaping how early years spending is targeted. The share of spending targeted at working families has risen from 15% in 2014–15 to 48% in 2024–25, and is on track to reach 58% in 2025–26. This is in the context of a growing total budget. At the same time, tighter eligibility criteria for the disadvantaged 2-year-old offer (which in 2024–25 covered 24% of children, down from 38% in 2014) have seen spending on this group fall both as a share of the early years budget and in absolute terms. In 2024, spending of £480 million was less than half its level a decade earlier.

- While rolling out new entitlements for working parents was a significant undertaking, most early indications suggest that the system has by and large coped well. Nationwide, over 90% of parents who applied and were approved for the entitlements secured a place. However, there may be signs of additional pressure on supply in some parts of the country (notably in London).

- Take-up of the new entitlements has been significantly higher than initially expected. The 2024 budget for the new entitlements was revised upwards by 28% after take-up exceeded initial expectations by a quarter. Top-ups set out at the 2025 Spending Review will go some way to meeting this pressure in future years – but if the new entitlements continue to be as popular as they are now, the government is on track for perhaps £350 million (in today’s prices) in extra spending in 2028–29.

- The per-hour funding rates set by central government remained essentially flat in real terms between 2024–25 and 2025–26. This followed a big (34%) real-terms increase in the core funding rate for 2-year-olds in 2024, as part of a proposal to more tightly link funding to underlying costs of delivery for different age groups. But childcare providers’ costs have risen more quickly than economy-wide inflation (mostly due to upwards pressure from a rising minimum wage, employer National Insurance and pension contributions). Once these sector-specific costs are accounted for, per-hour funding for 3- and 4-year-olds is 22% lower than its peak in 2017–18 – with a 4% decline just in the last year. Effective resources per hour for 2-year-olds are 12% higher than their 2017 peak.

- In the 2025 Budget, the government committed to a review of the early years system. This is a welcome step: the system is complex and difficult to navigate. The first step in this review should be to work out the aims the government wishes to achieve with its early years investment – for example, improving children’s development, increasing parents’ ability to work, or easing cost-of-living pressures. That will allow for principled discussions about the outcomes achieved in the early years system as a whole, rather than attempting to make each individual policy achieve all of these distinct goals.

Schools

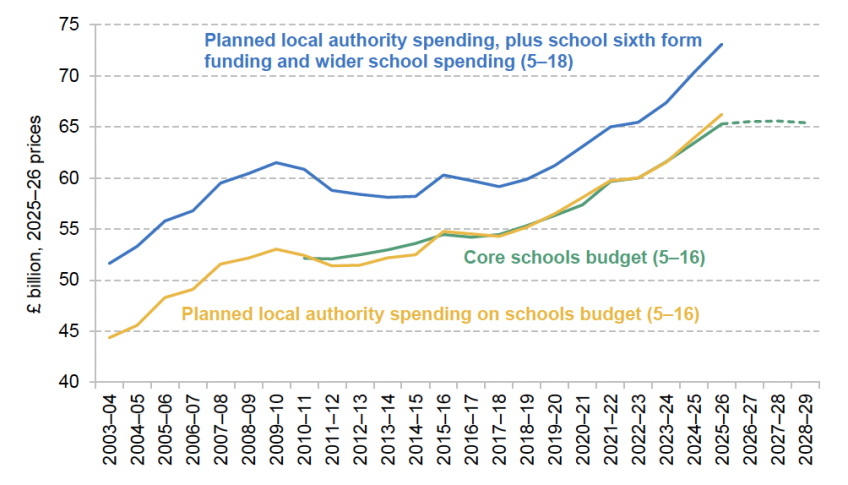

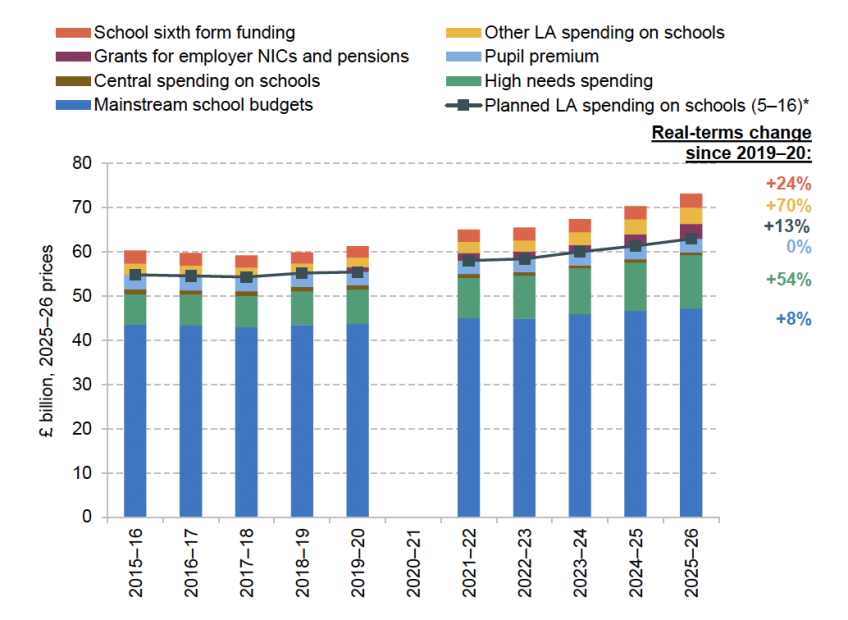

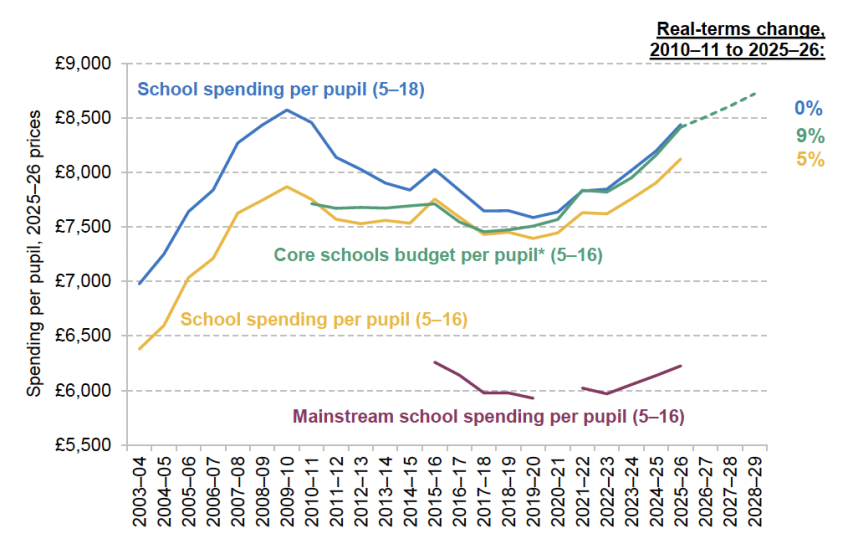

- Total school spending per pupil aged 5–18 in England fell by 10% in real terms between 2010–11 and 2019–20. Recent funding increases have reversed these cuts and mean that it is now back to 2010–11 levels.

- Between 2019–20 and 2025–26, total school spending for pupils aged 5–16 grew by £7.5 billion or 13% in real terms. This drove a 10% real-terms increase in spending per pupil aged 5–16. Over half of this increase in school funding can be explained by growth in spending on special educational needs and disabilities (SEND).

- After accounting for planned spending on SEND, we estimate that mainstream school funding per pupil aged 5–16 only grew by 5% in real terms between 2019–20 and 2025–26. In fact, mainstream school spending per pupil is currently about the same level it was in 2015–16.

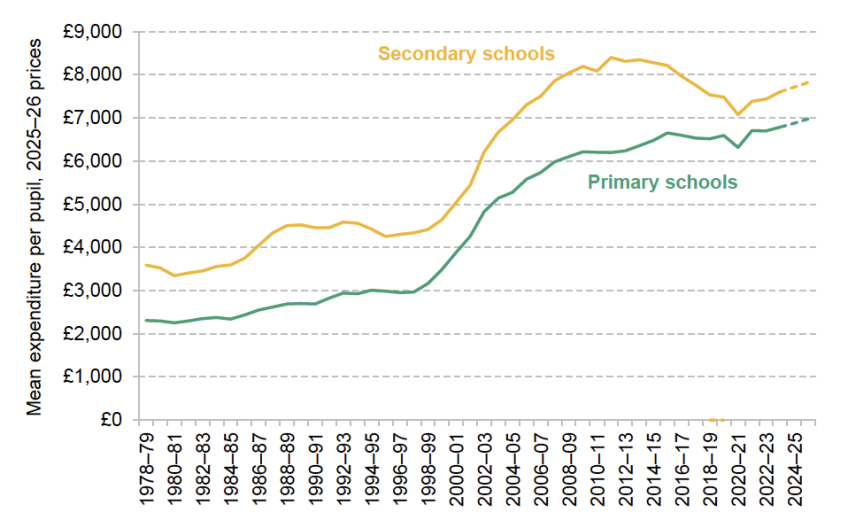

- Secondary school spending per pupil in England in 2025–26 is due to be about £7,800, which is 12% higher than in primary schools (£7,000). This is down from a difference of about 30% in the 2000s and over 50% during the early 1990s. This represents a very significant reduction in the secondary:primary funding ratio over time.

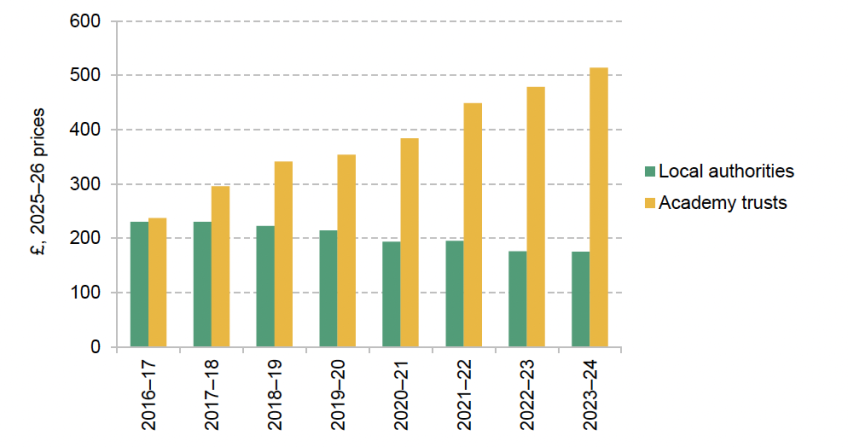

- Academy trusts can hold back some funding to spend centrally, which is not included in spending by individual primary and secondary schools. This is partly to deliver services that would otherwise be provided by councils, but they can also spend money centrally on some things that would be provided by individual maintained schools, such as teachers. Central spending on academies is now £510 per pupil, more than double the level in 2016–17. This reflects a shift towards larger academy trusts and increasing central spending per pupil among academy trusts of all sizes.

- The Office for Budget Responsibility (OBR) forecasts that spending on special educational needs and disabilities will have more than doubled in real terms by 2028–29 as compared with 2015–16, including real-terms growth of 13% in 2025–26. This reflects rapid growth in the number of pupils with Education, Health and Care Plans (EHCPs), which are reserved for high-cost needs, and high growth in demand for special school places. A shortage of places in state-funded schools has forced councils to pay for high-cost places in independent special schools, with the cost of fees nearly doubling in real terms between 2018–19 and 2024–25 and now standing at over £2 billion.

- OBR forecasts imply a £6 billion gap between expected funding and spending on SEND in 2028–29. The government is due to publish a schools white paper, including SEND reforms, which may help close this gap by slowing the growth in spending. The other options to fill this gap include topping up the schools budget or reducing mainstream school budgets. To set these in context, £6 billion represents about 9% of the schools budget and about 11% of existing mainstream school budgets.

- In the 2025 Spending Review, the government set out plans to keep core school funding largely constant in real terms between 2025–26 and 2028–29. Falling pupil numbers will reduce pressure on this budget to some extent. If policymakers choose to keep per-pupil spending fixed in real terms, they could generate savings of about £1.8 billion in the total schools budget by 2028–29, which could be used to partly fill the £6 billion funding gap between SEND funding and spending.

- Only increasing mainstream funding per pupil in line with general inflation also creates a number of risks. First, in order to generate any savings, policymakers would actually need to reduce resources, such as through cutting staff numbers or closing schools. Second, in this scenario, we project that actual growth in schools’ costs would exceed funding growth by about 0.5–1 percentage points per year. This would place mainstream schools in a very tight position.

Further education and skills

- Total public spending on further education and skills – covering 16–19 education, adult skills and apprenticeships – is around £14 billion in 2025–26. In the 2025 Spending Review, the government set out plans to increase total further education and skills funding by £300 million in real terms between 2025–26 and 2028–29, but did not specify how this funding will be allocated across the system.

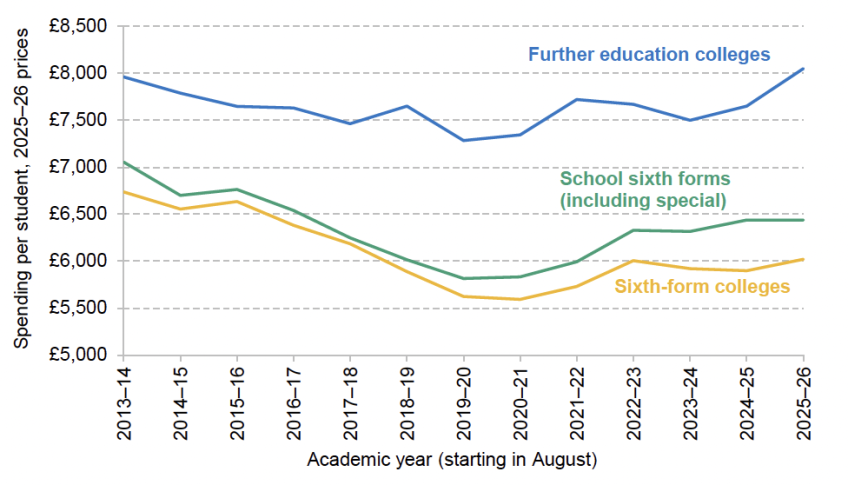

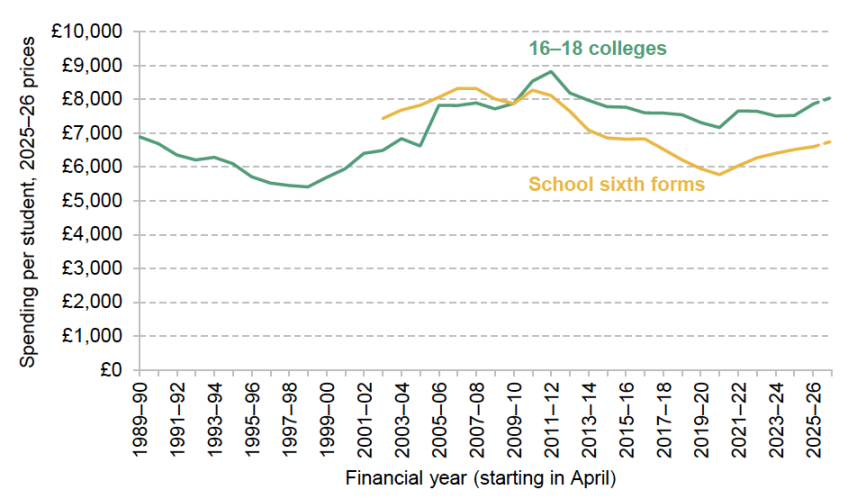

- Between 2010–11 and 2019–20, real-terms funding per student aged 16–18 fell by 14% in colleges and 28% in school sixth forms. Although funding has risen since 2019–20, this has only partially reversed earlier cuts. In 2025–26, funding per student in colleges is around 8% lower than in 2010–11 and around 20% lower in school sixth forms. The recent Post-16 Education and Skills White Paper implies a further 2.5% real-terms increase in spending per student in 2026–27, funded from within the Department for Education’s Spending Review settlement.

- In the 2025–26 academic year, spending per student aged 16–18 in further education colleges is £8,000, compared with £6,400 in school sixth forms and £6,000 in sixth-form colleges. Higher funding for further education colleges mostly reflects higher levels of funding for costly technical programmes and extra funding for students from more deprived areas.

- The number of 16- to 18-year-olds in England is projected to increase by around 70,000 (3%) between 2025 and 2028. Maintaining spending per student at its 2026–27 level in real terms would require total 16–18 funding to increase by a further £150 million (in today’s prices) by 2028–29.

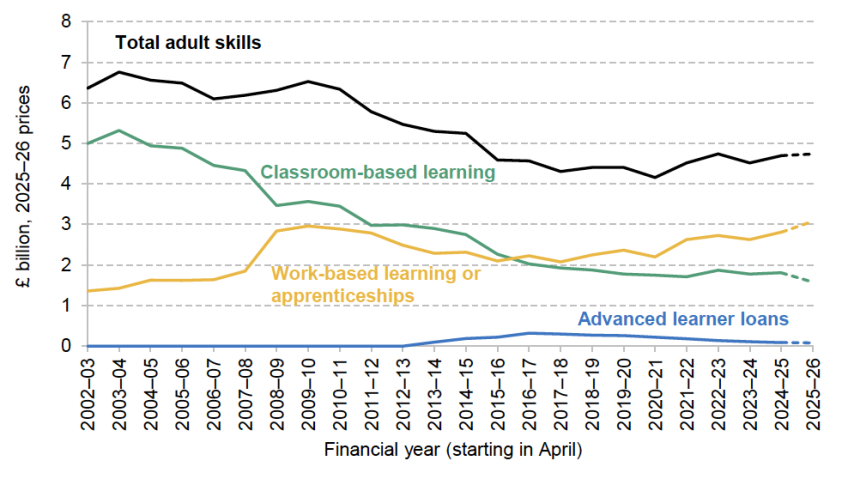

- Total spending on adult skills and apprenticeships increased by 7% in real terms between 2019–20 and 2025–26. However, this only reverses a fraction of past cuts: total spending in 2025–26 will still be 25% below its 2010–11 level. The long-run decline has been particularly pronounced in classroom-based adult education, where falling learner numbers and sustained real-terms reductions in funding rates mean spending is projected to be around 54% below its 2010–11 level in 2025–26.

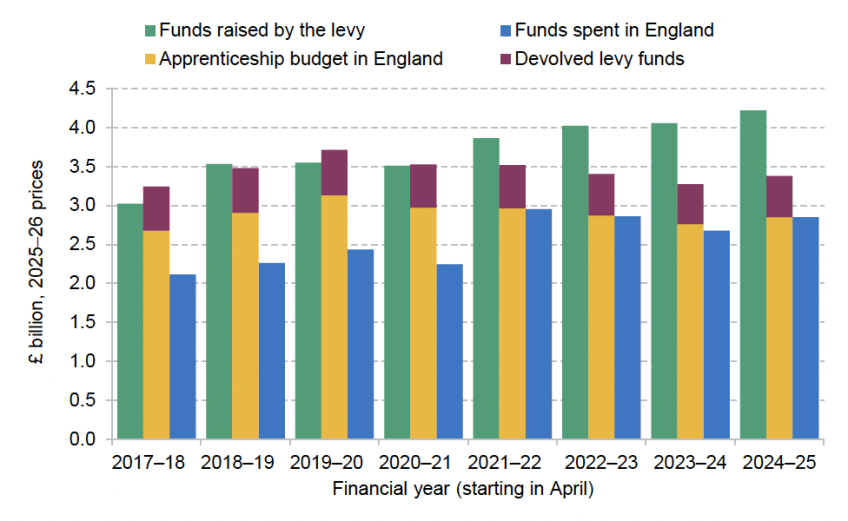

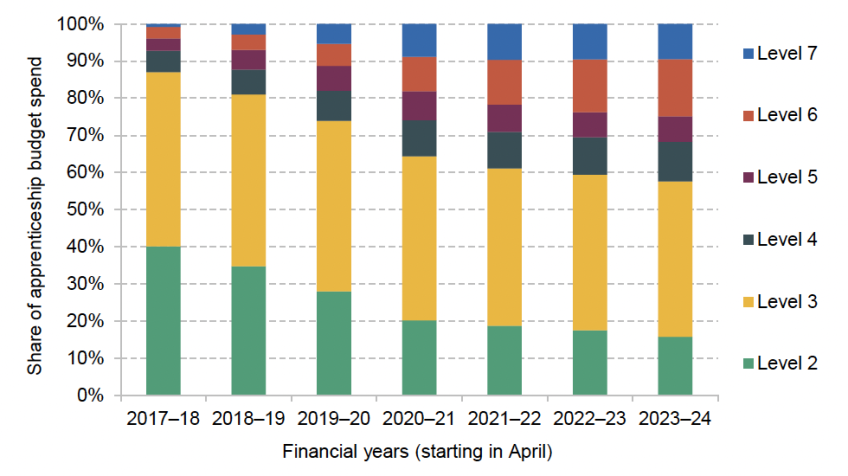

- Since 2021–22, revenues from the apprenticeship levy have consistently exceeded the funding allocated to the apprenticeship budget, with the surplus rising to almost £840 million in 2024–25. Over the same period, underspends against the apprenticeship budget have largely disappeared, meaning that most allocated funding is now being spent. This shift reflects, in part, a sharp increase in spending on higher-level apprenticeships (level 4 and above), which rose from 13% of total apprenticeship spending in 2017–18 to 39% in 2021–22.

- Looking ahead, if the government chooses to hold spending per student in 16–18 education constant in real terms, much of the increase in total further education and skills funding implied by the Spending Review would be absorbed by rising student numbers. Even allowing for the planned increase in growth and skills levy funding announced at the Autumn Budget – around £50 million in real terms by 2028–29 – public spending on adult education and skills (i.e. outside the 16–19 budget) would be broadly unchanged in real terms between 2025–26 and 2028–29.

Higher education

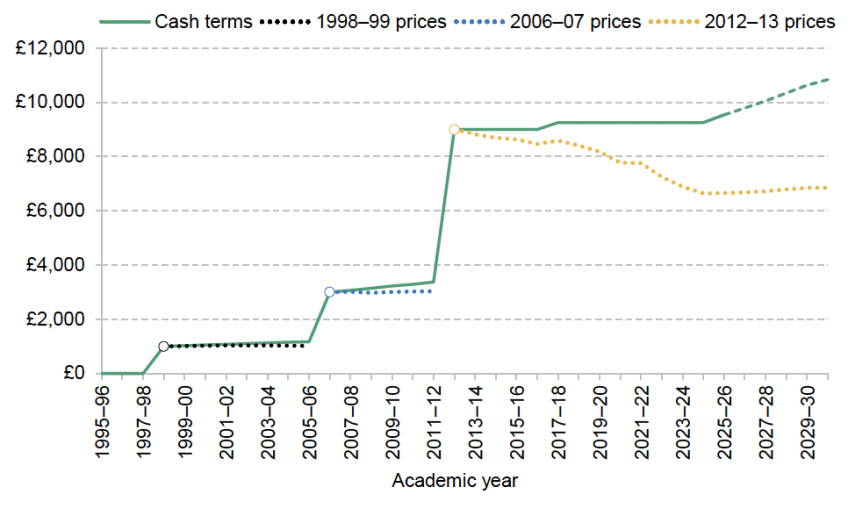

- Up-front spending on teaching resources per higher education student has declined steadily, standing at £9,900 per year for the 2024–25 university entry cohort. This is around £2,700 or 22% lower in real terms than for those who started courses in 2012–13, who were the first to pay much higher tuition fees, largely because of successive cash-terms freezes to the fee cap since then. The government increased the fee cap with inflation this year (to £9,535) and has committed to increase the cap in line with inflation each year. This will arrest the decline in real-terms per-student teaching resources, and provides some much-needed certainty for universities and prospective students alike.

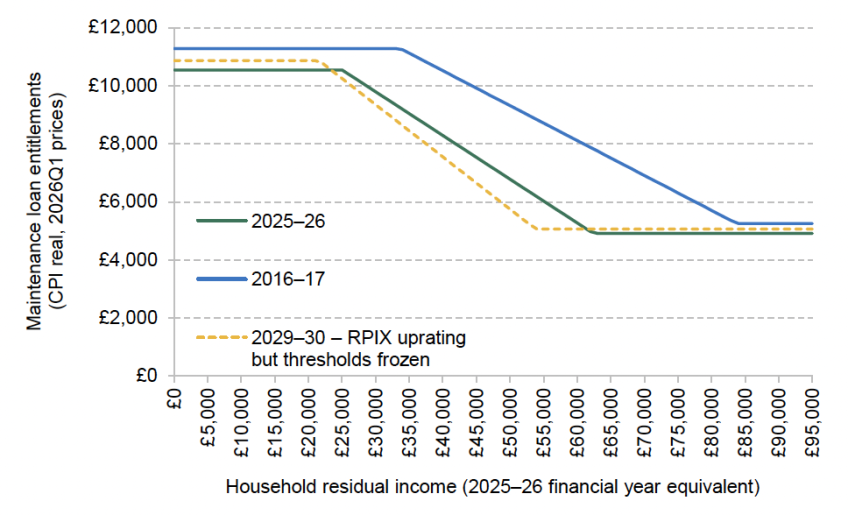

- Since 2016–17, living cost support for students has only been provided in the form of loans. The maximum amount students are entitled to borrow has been increased each year in line with forecast inflation, but the generosity of support has still declined substantially in real terms, with some students eligible for over a third (around £2,900) less in 2025–26 in today’s prices than equivalent students in 2016–17. This has resulted partly from a long-running freeze in the household income thresholds that determine how much individual students can borrow. If this freeze continues, we estimate that by 2029–30, some students may be eligible for over £1,100 (around a sixth) less in real terms than equivalent students this academic year.

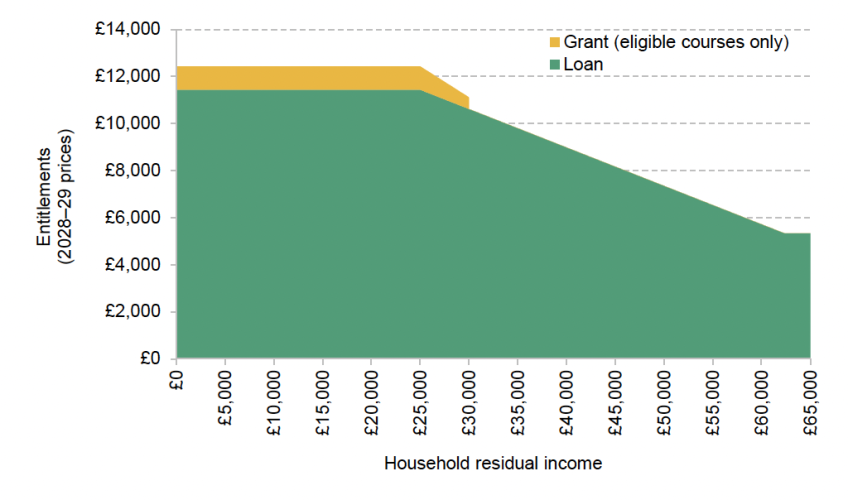

- By the end of this parliament, the government proposes to introduce maintenance grants – which do not need to be repaid – for low-income English students. Grants of between £500 and £1,000 will be provided in addition to existing loans. If they had been available in 2022–23, we estimate 47% of students may have met the means-testing criteria for the new grants, at a cost of approximately £520 million. However, only students on particular courses will be eligible for the new grants, and the government has yet to confirm which these courses will be.

- Until 2015–16, undergraduate students from England were entitled to means-tested maintenance grants whichever subjects they studied. They were worth over four times as much in real terms as the new grants proposed by the government, and were awarded to 57% of all students who received any living cost support. Low-income students from other parts of the UK still are entitled to maintenance grants regardless of subject studied, with maximum grants of £2,000 for Scottish Young Students, £3,475 for Northern Irish students and £8,100 for Welsh students living away from home, outside London this academic year.

- Unlike fees for domestic undergraduates, tuition fees paid by international students are not subject to a fee cap, and now account for more than a fifth of higher education providers’ overall income. The government plans to introduce a levy of £925 per student on these fees from 2028–29. The levy is expected to raise £445 million in its first year and to reduce provider income by around £270 million. There is no meaningful sense in which the revenues raised from this levy will ‘pay for’ the introduction of maintenance grants for domestic students, as government has claimed.

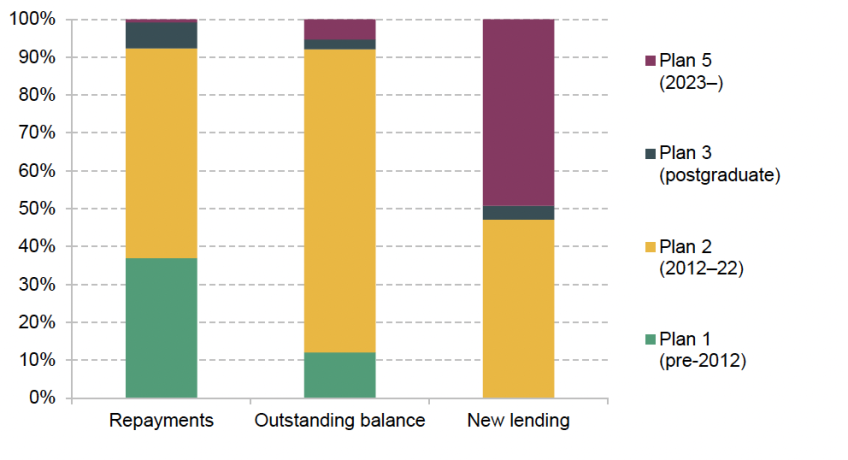

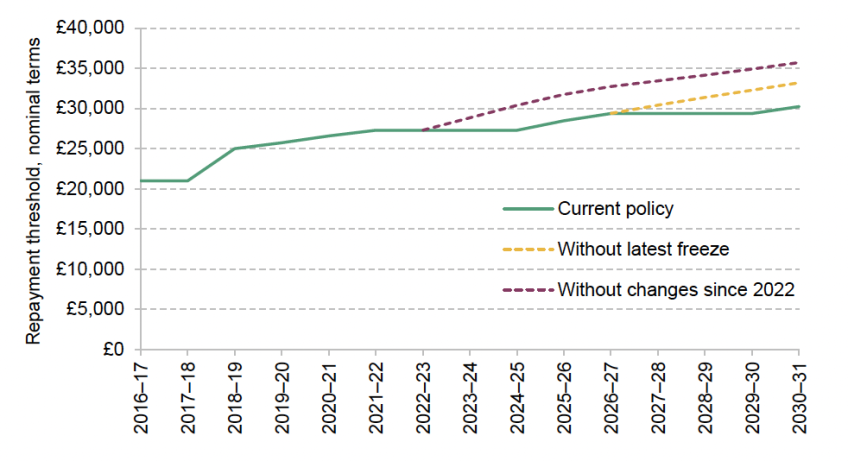

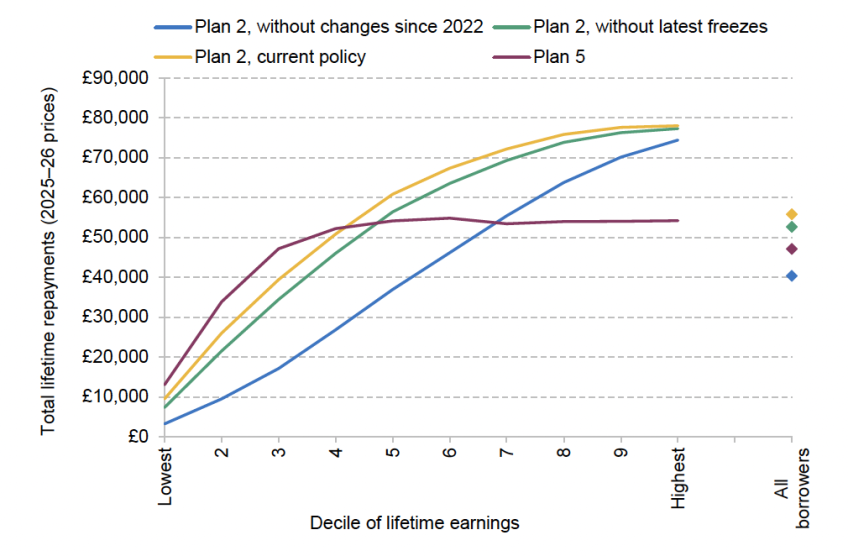

- How much graduates go on to repay towards their student loans determines how the cost of higher education is shared between the taxpayer and graduates themselves. In the 2025 Budget, the government announced that the repayment threshold for ‘Plan 2’ student loans will be frozen for three years from April 2026. As a result, we expect millions of graduates – who started courses between 2012 and 2022 – will repay £93 more towards their loan in 2027–28 and £259 more in 2029–30. Many of these graduates will also be affected by freezes to personal tax thresholds. The interest rate thresholds – which determine how much interest is added to these student loans – are also being frozen for three years. Although less appreciated, this freeze will be more important for many high-earning graduates in the long run than the freeze in the repayment threshold.

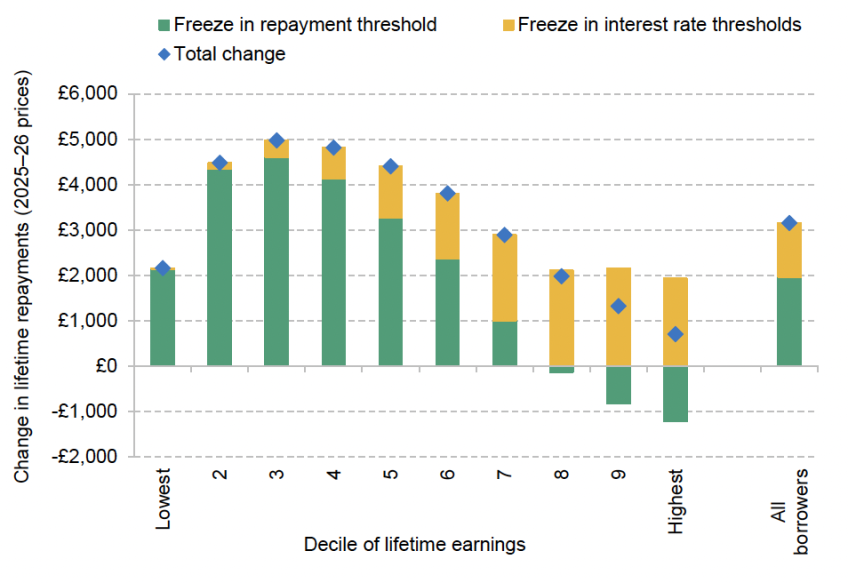

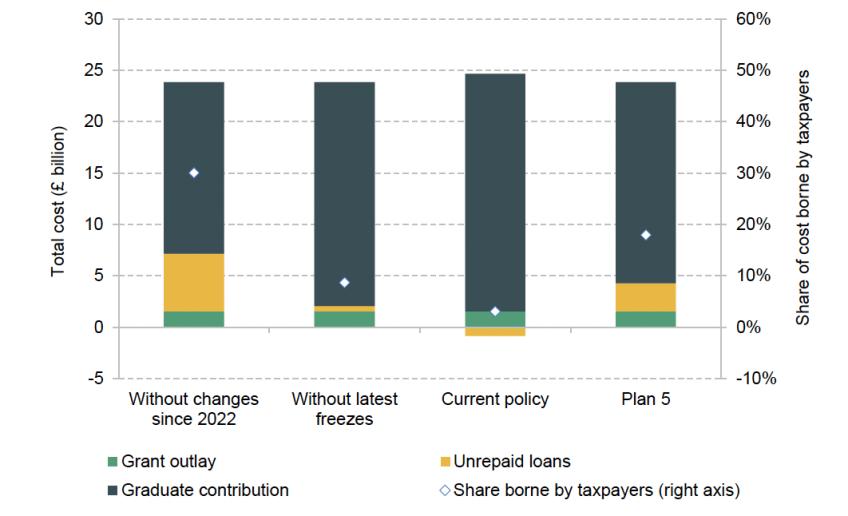

- The combined effect of the freezes announced at the Budget will be to increase expected lifetime loan repayments from those who started courses in 2022–23 by around £3,200 (6%) on average, from £52,600 to £55,800 in today’s prices. Borrowers in the third decile of lifetime earnings can expect to repay around £5,000 (14%) more over their lifetimes. We estimate that this will reduce the long-run cost to the taxpayer of financing higher education for this single cohort by £1.3 billion, with the taxpayer now set to bear only 3% of the total cost, down from 9% before the latest freezes.

1. Introduction

Education spending is the second-largest element of public service spending in the UK behind health, representing £122 billion in 2024–25 in today’s prices or about 4.1% of national income. In order for policymakers to be able to make well-informed policy choices, it is crucial to have a clear, consistent picture of how the level of spending at each phase of education has changed over time, what the expected future changes are and the factors driving these changes.

This is of particular importance given evidence showing how education investments at different ages combine to drive long-run outcomes. Evidence tends to show that earlier investments have larger effects than later ones (Cunha, Heckman and Schennach, 2010). There is also now an extensive literature on the effects of school spending. Much of this is from the US and finds that a $1,000 increase in school spending over three to four years can improve test scores by about 0.03 standard deviations (Jackson and Mackevicius, 2024). Effects tend to be larger for children from disadvantaged backgrounds and when school spending is preceded by high-quality early years provision (Johnson and Jackson, 2019).

In a series of annual reports on education spending in England funded by the Nuffield Foundation, we have sought to cast light on this subject by illustrating how spending per pupil (or student) across different stages of education has changed over time. We also publish a range of smaller outputs throughout the year to provide more timely and rapid analysis of the resource challenges facing different phases of education. This analysis is housed on a dedicated website (https://ifs.org.uk/education-spending), providing easy access to the latest figures and the underlying methodology.

The Department for Education is leading the new government’s ‘Opportunity Mission’, with overall goals to improve social mobility by improving support in the early years, narrowing inequalities in the school system and improving skills to increase economic growth.1 The government has set a specific milestone goal to increase the share of 5-year-olds demonstrating a ‘good level of development’ from its current level of 68% to 75% by 2028.

The overall funding available to the Department for Education to meet these and other objectives was largely set in the 2025 Spending Review, though these plans can be topped up and revised. Under current plans, the Department for Education is due to see a 1% per year real-terms increase in day-to-day funding for services in England (resource departmental expenditure limit or RDEL) between 2025–26 and 2028–29. This is similar to overall plans for growth in day-to-day public service spending across government as a whole.

The government has already begun to set out spending priorities across different stages of education in order to meet its objectives and the various challenges it faces. Public spending on the early years has already risen significantly in order to deliver the new extended entitlement to free early years education and childcare from the age of 9 months through to when children start school, which was gradually rolled out from April 2024 onwards. The government now faces the continuing challenge to make sure this is delivered effectively and to assess what else it can do to meet its milestone to improve school readiness, such as through new ‘Family Hubs’.

The core schools budget is set to be held constant in real terms between 2025–26 and 2028–29, plus extra funding to cover an extension to free school meals to all those on universal credit. With falling pupil numbers, this equates to a small real-terms rise in funding per pupil. However, the government faces huge pressures from ever-rising spending on special educational needs and disabilities (SEND) in schools, which has almost doubled in real terms over the past decade. This has been driven by rapid rises in numbers of pupils entitled to statutory support through Education, Health and Care Plans (EHCPs). The Office for Budget Responsibility forecasts that such pressures are likely to intensify, with a £6 billion gap between forecast spending by local authorities and funding from central government in 2028–29. The government is set to publish a White Paper with proposals to reform the SEND system early in 2026. If such proposals slow the growth in spending, this would help close the £6 billion expected funding gap. Either way, how the government seeks to reform the SEND system will be the most important factor shaping the budget pressures on all schools in England in coming years.

Over much of the last 40 years, the budget for further education and skills has tended to be a relative loser from spending changes. When there have been increases in education spending, these areas have generally seen smaller rises. When there have been cuts, they have tended to see the largest cuts. Somewhat unusually, the government is currently implementing faster rises in funding for further education colleges and sixth forms than in overall education spending in England.

The government has also published a White Paper setting out proposals for how England’s post-16 education and skills system should be organised, governed and funded (Department for Education, 2025b). This includes a headline target of two-thirds of young people participating in higher-level learning (degrees and advanced technical courses). But with no deadline for this target, it is hard to judge the significance of this. The White Paper also confirmed plans to convert the apprenticeship levy into a ‘growth and skills levy’, providing subsidies to all employers to fund a wider range of training. Our special report provides further analysis of proposals in this White Paper (Ogden and Tahir, 2025).

Following a period of uncertainty and concern for university finances, the government has recently provided more certainty by committing to index tuition fees in line with inflation, so that their real value does not, by default, decline with inflation (as happened in all but one year between 2012 and 2024). However, living cost support for university students – mainly provided in the form of maintenance loans – has become substantially less generous in real terms over the last decade. From the 2028–29 academic year, the government is planning to reintroduce maintenance grants, which students would not need to repay, although these will be smaller and available to far fewer students than was the case for the grants that were scrapped in 2016. The government also plans to introduce a new levy on tuition fees paid by international students, although it has not been clear about the economic rationale for such a levy, which would constitute a tax on an element of the UK’s exports.

Before we turn to individual areas of education, the rest of this introduction provides overall context on total spending, pupil numbers across each sector over time and the overall methods.

1.1 Total public spending on education

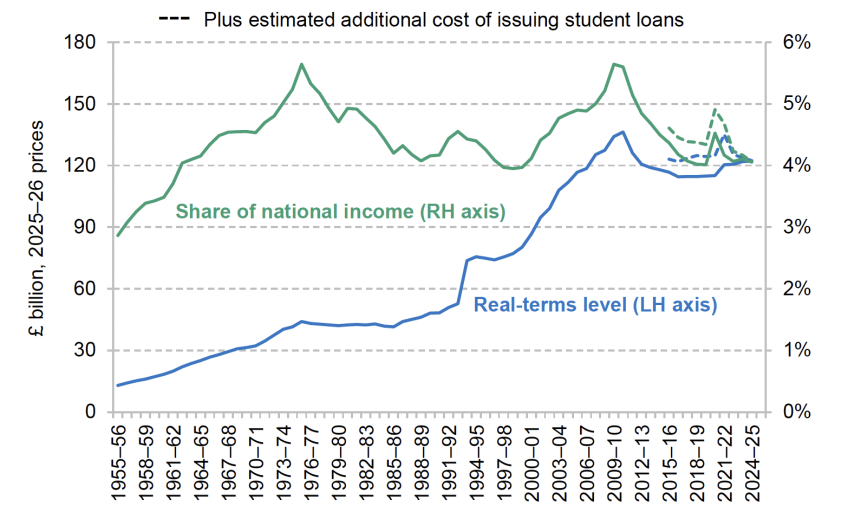

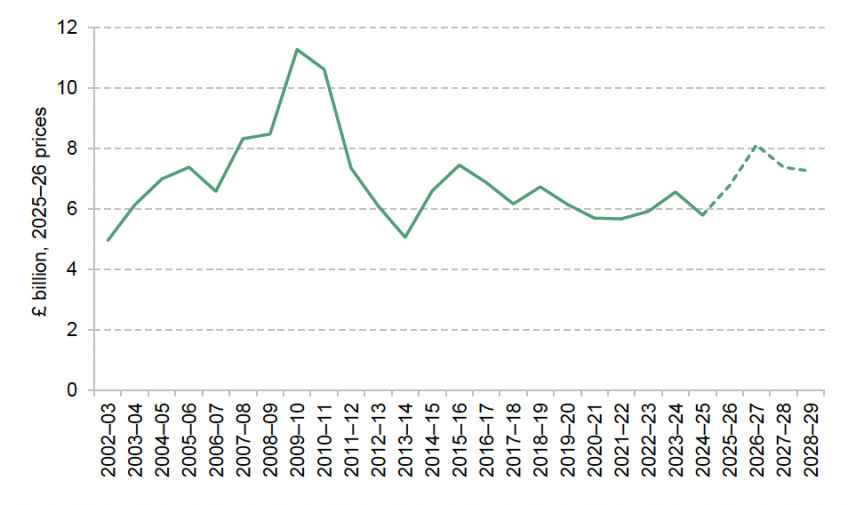

The total level of public spending on education in the UK rose significantly up to about 2010. As shown by the blue line in Figure 1.1, growth in official spending on education was particularly fast from the late 1990s through to the late 2000s, with real-terms growth averaging about 5% per year between 1998–99 and 2010–11. Education spending then fell as public spending cuts began to take effect from 2010 onwards. Between 2010–11 and 2019–20, official education spending fell by 16% in real terms. Since then, it has risen slightly, but in 2024–25 it remained 10% below its 2010–11 level.

Figure 1.1. UK education spending (2025–26 prices and as a share of national income)

Source: HM Treasury, Public Expenditure Statistical Analyses 2025; previous PESAs; HM Treasury, GDP deflators, November 2025; Office for Budget Responsibility, Economic and Fiscal Outlook, various editions (https://obr.uk/efo/); Office for National Statistics, ‘Student loans in the public sector finances: a methodological guide’, January 2020.

Some of the decline in education spending during the 2010s reflects initially large declines in capital spending just after 2010 (Sibieta, 2023a). The declines also reflected a deliberate shift in the financing of higher education, with greater reliance on contributions from graduates repaying student loans later in life, particularly from the 2011–12 financial year onwards. Unfortunately, these official figures do not fully account for the cost to the taxpayer of issuing student loans.2 We estimate that if official measures of education spending had reflected the eventual taxpayer cost of issuing student loans, education spending would have been around £6 billion higher in 2015–16, as shown by the dashed blue line in Figure 1.1.3 We estimate it would have been £2 billion higher in 2023–24 and about £0.2 billion higher in 2024–25, with this more recent decline in spending on student loans reflecting changes to repayment terms which have increased expected graduate contributions. As a result, while for many years official figures would have been overstating cuts to education spending since 2010–11, the overall decline in education spending between 2010–11 and 2024–25 is now around 10% across both series. The decline in spending over this period mostly reflects the shifting of most of the cost of higher education from taxpayers to graduates. Accounting for this, the real-terms level of public spending on education in 2024–25 was about the same as it was just before the financial crisis of 2007 to 2008.

Irrespective of whether we adjust for the additional cost of issuing student loans, education spending represented about 4.1% of national income in 2024–25. This follows a temporary peak of 5% during the height of the COVID-19 pandemic in 2020–21, when spending was boosted and the size of the economy was depressed. The underlying picture, however, is a significant decline in education spending as a share of national income over the last 15 years. Following a significant rise over the 2000s, education spending as a share of national income reached a peak of 5.6% of national income in 2010. Since then, it has declined to its current level of 4.1% of national income. Since the early 1960s, education spending has ranged between 4% and 5.5% of GDP. Having fallen for the last 15 years, we are now back at the low end of this range, similar to what was spent between the mid 1980s and late 1990s. Indeed, it is clear that education spending as a share of national income has not seen a sustained rise since the early 1970s. This is despite large rises in participation in post-compulsory education over time, both in schools and in higher education, as well as the creation of a publicly funded early years sector.

1.2 Student numbers over time

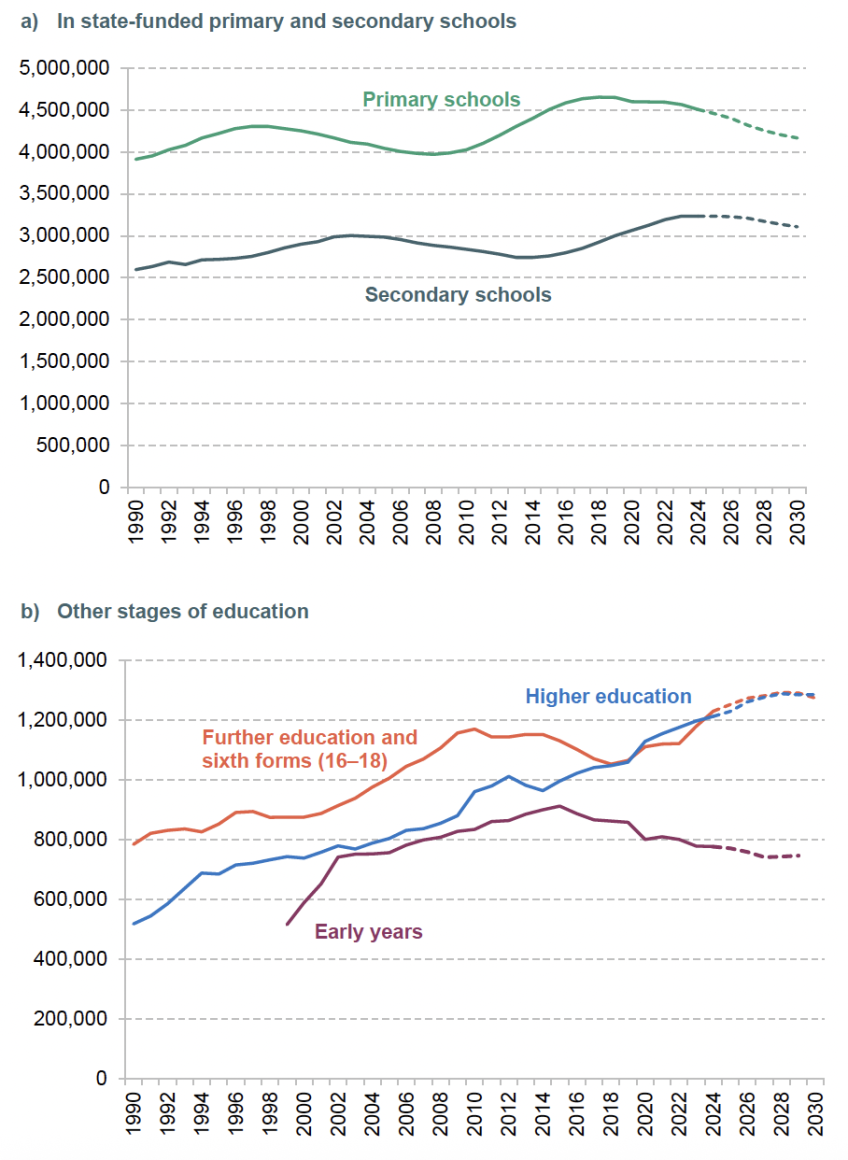

Total spending figures can obscure the impact of changes in the number of pupils or students, which are often one of the most important factors driving changes in the total and per-pupil level of spending over time. There have also been some fairly substantial changes in recent times, which are due to continue over the next decade. Changes in pupil numbers in schools are shown in Figure 1.2a, and will largely just reflect changes in cohort size over time. Changes in numbers in early years education, further education and sixth forms, and higher education are shown in Figure 1.2b. In addition to changes in cohort size, these figures will also reflect (rising) participation levels over time. Actual figures are shown up to 2024–25, with projections for 2025–26 and beyond.

Figure 1.2. Pupil numbers in education in England (including projections from 2025 to 2030)

Note and source: Years refer to academic years starting from September, i.e. 2002 refers to the 2002–03 academic year. Early years numbers present the total number of children taking up any of the universal 3- and 4-year-old entitlement (excluding 4-year-olds in infant classes) and are taken from Department for Education, ‘Funded early education and childcare’ (2025) as well as predecessor series ‘Education provision: children under 5 years of age’. Primary and secondary school numbers are taken from Department for Education, ‘Schools, pupils and their characteristics’, January 2025 and earlier years, and ‘National pupil projections: July 2025’. Projections for primary and secondary school children for 2030 are based on Office for National Statistics (ONS) population projections by single year of age (https://www.nomisweb.co.uk/datasets/ppsyoala). Further education and sixth forms figures refer to 16- to 18-year-olds in state-funded schools or colleges as measured at the end of each calendar year in Department for Education, ‘Participation in education, training and employment: 2024’. Higher education figures relate to full-time England-domiciled students on first undergraduate degrees and other undergraduate courses from Higher Education Statistics Agency, ‘Who’s studying in HE?’, and also use ‘Historical statistics on the funding and development of the UK university system, 1920–2002’. Forecasts for the early years are based on ONS 2022-based forecasts for 3- and 4-year-olds, applying the average take-up rate from the post-pandemic period (2022–23 to 2024–25). Forecasts for 16–18 education are similarly based on the ONS population projections for 16- to 18-year-olds. Forecasts for higher education are based on Department for Education forecasts of entrants up to 2029 (https://explore-education-statistics.service.gov.uk/methodology/student-loan-forecasts-for-england) and then on ONS forecasts for the number of 18- and 19-year-olds.

Figure 1.2a shows the numbers of pupils in state-funded primary and secondary schools in England over time. Numbers in primary schools grew by 17% between 2009–10 and 2019–20, the equivalent of an extra 700,000 pupils – or effectively a full school year of children. With falling numbers of children being born during the 2010s, primary pupil numbers have since fallen, with a 3% or 100,000 drop between 2019–20 and 2024–25. In contrast, pupil numbers in secondary schools fell from the early 2000s through to about 2014–15. Between 2014–15 and 2024–25, they then grew by nearly 18% or 500,000.

Looking beyond 2024–25, the primary pupil population is currently expected to fall by over 300,000 more between 2024–25 and 2030–31, or about 8%. The secondary pupil population is expected to fall by about 100,000 or 4%, with these falls only starting from about 2026–27. This implies a fall in the total pupil population of only about 6% or just under 500,000 between 2024–25 and 2030–31.

As was detailed in a separate IFS report on demographic change and schools, the number of children is expected to continue to decline after 2030 (Sibieta, 2025). These falls in the number of pupils and children leave policymakers with a choice. They could use the drop in the number of pupils as an opportunity to make savings by reducing the numbers of schools and teachers in the system. Alternatively, they could choose to increase per-pupil funding and increase the overall intensity of resources, such as by reducing class or school sizes.

As Sibieta (2025) discussed in detail, policymakers facing changing pupil numbers have made different choice across time. During the 1970s and 1980s, policymakers across the UK often chose to make savings in the face of large drops in pupil numbers. In contrast, during the 2000s, there were increases in per-pupil funding and lower class sizes in response to falling pupil numbers. Over the last 10 years, rapid falls in primary school pupil numbers in London have been accompanied by falling numbers of teachers, though not much change in the number of schools, whilst there is more evidence of school closures in Wales, Scotland and Northern Ireland.

In Figure 1.2b, we show how pupil numbers have changed over time in the early years (where we focus here on the universal entitlement for 3- and 4-year-olds), further education, and higher education (where we focus on full-time English-domiciled undergraduate students).

The burgundy series in Figure 1.2b shows big increases in the number of pupils taking up at least some of the universal entitlement to an early education place at ages 3 and 4. This reflects both a rise in the take-up rate (in the earliest years) and changes in the underlying cohort size. The number of 3- and 4-year-olds peaked in 2015–16, and is projected to have fallen by over 15% by 2029–30.

There have been a range of policy reforms in the early years system that mean the number of children under 5 receiving some funded childcare – and, even more so, the number of hours of support on offer – have increased sharply, with significant extensions to the generosity of the free entitlement system in 2004, 2010, 2014, 2017 and – most recently – between 2024 and 2025. These reforms have changed the system in different ways, from increasing eligibility to entitlements to increasing the number of hours on offer. We return to these policy decisions, and their implications for education spending, in Chapter 2.

The number of students in 16–18 education (shown by the red line in Figure 1.2b) grew by almost 50% between 1990–91 and 2010–11, from about 800,000 to 1.2 million full-time-equivalent (FTE) students. After 2010–11, numbers fell by about 10% to just over a million in 2018–19, reflecting reduced cohort sizes rather than falls in participation at this stage of education. Since then, numbers have started to rise again and the number of students is 17% or 200,000 higher in the latest year of data (2024–25) than in 2018–19. Again, this mostly reflects growth in cohort sizes.

Further rises are expected over the next few years due to population growth, with numbers currently projected to rise by a further 5% between 2024 and 2029, before then starting to fall slightly. After this point, the 16–18 student population is likely to drop in the way that we are currently seeing for primary and secondary schools.

The number of full-time undergraduate students in higher education in England increased by over 130% between 1990 and 2024, to reach 1.2 million (as shown by the blue line on Figure 1.2b). The latest forecasts imply a further increase in higher education student numbers to a peak of nearly 1.3 million by 2028. The number of 18-year-olds in England is then expected to decline – by around 10% over the course of the 2030s – as the smaller cohorts currently driving declines in numbers of school pupils reach the age where they might enter higher education. However, unlike for schools, this may not necessarily translate into fewer England-domiciled undergraduate students. The potential impact of similar population declines in the early 1990s and during the 2010s on student numbers was more than outweighed by the impact of increases in the proportion of each age cohort participating in higher education. The proportion starting a first degree by age 20 increased steadily from 29% in 2006–07 to 40% amongst those aged 20 in 2017–18 and 46% amongst those aged 20 in 2022–23.4 If this upward trend continues, this would suggest undergraduate numbers may continue to increase year-on-year, albeit at a slower rate.

1.3 Methods and approach

The rest of this report mainly focuses on day-to-day (‘current’) spending on different stages of education in England. This is primarily for data availability reasons, though we have also previously undertaken analysis comparing school spending per pupil across the four nations of the UK, which indicates higher levels of school spending per pupil in Scotland in particular (Sibieta, 2023b; Sibieta and Snape, 2025a). We also briefly examine capital spending as part of Chapter 3 on schools.

For the most part, we focus on public spending on education. This is due to a lack of reliable data on total private spending on each stage of education over time. For schools, Sibieta (2023c) produced additional analysis comparing state school spending per pupil and private school fees over time, including the likely effects of removing tax exemptions from private schools. For higher education, we also consider expected graduate contributions to higher education spending through student loan contributions later in working life, although our main estimates of higher education spending consider the up-front resources available for teaching and ignore both living cost support and eventual loan repayments.

In Chapters 2–5, we examine trends in spending on the early years, schools, further education and skills, and higher education. In Chapter 6, we compare trends in spending per pupil across different stages of education over time. In each case, our methodology for calculating spending per student is detailed in full on the dedicated website (https://ifs.org.uk/education-spending/methods-and-data). In most cases, figures relate to core education spending and exclude temporary support during the pandemic, though it is not always possible to separate this out. Chapter 7 concludes.

In most cases, we calculate real-terms changes by adjusting for economy-wide inflation as captured by the GDP deflator. This is the standard practice used for analysing public spending in the UK. Across long periods of time and in stable economic environments, the GDP deflator is likely to provide a close approximation to the input costs faced by education providers. We also analyse the likely costs faced by providers. This allows us to consider how the actual funding available to providers compares with their actual cost pressures.

2. Early years

Early childhood sets the foundations for children’s later development through the education system. In view of this, the government has set itself a target for 75% of children to reach a ‘good level of development’ at the end of Reception by 2028.

In the earliest years especially, children’s development is holistic: health, emotional well-being and early skills are interrelated, and different dimensions of development build on one another. This means that the definition of ‘education’ is less clear in the early years than at other stages: programmes such as formal childcare or integrated early years services can promote children’s educational development, but may have wider goals such as supporting parents to work, increasing families’ disposable incomes or improving parents’ mental health.

In this chapter, for comparability with other stages of education, we largely focus on public support for formal childcare that happens outside the home. These ‘early childhood education and care’ settings can – though by no means always do – promote children’s development, though they also contribute directly to wider policy aims.

2.1 The scale of spending on funded childcare entitlements

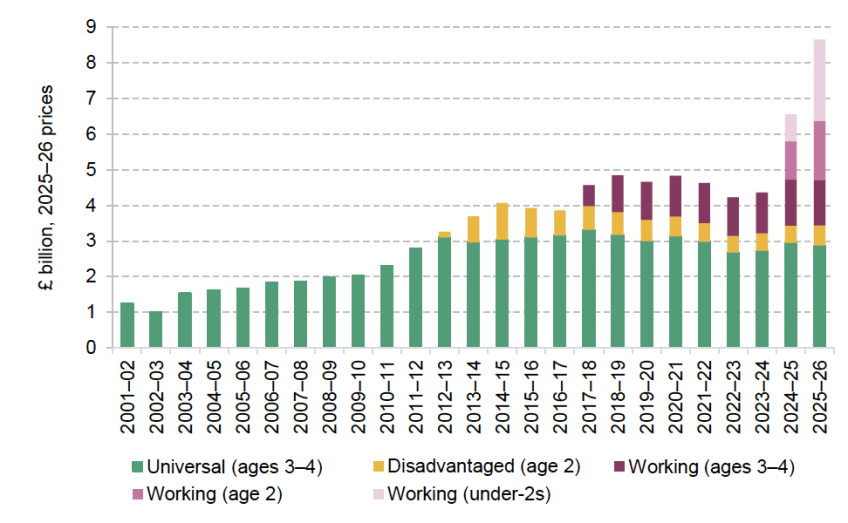

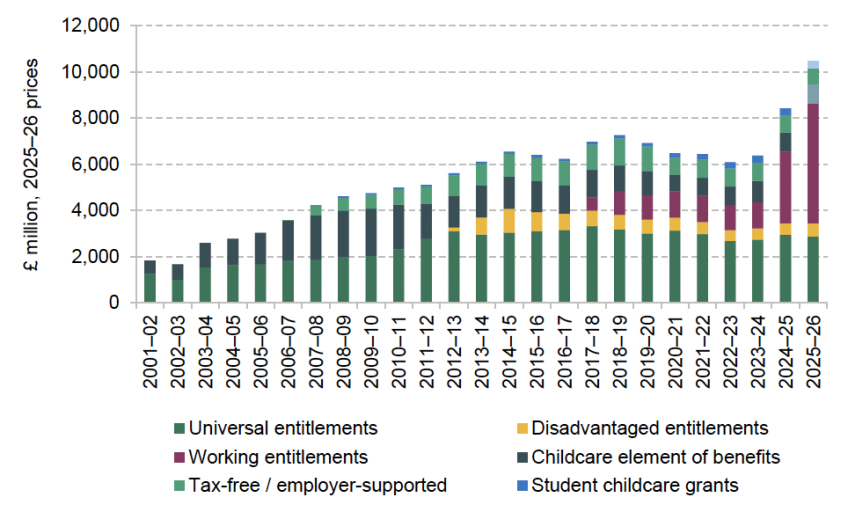

Over the last 25 years, public support for early childhood education and childcare has become a major part of England’s educational system. As Figure 2.1 shows, in the early 2000s spending on the ‘free entitlement’ to a funded childcare place amounted to just over £1 billion (in today’s prices). By 2009–10, this had doubled; by 2014–15, it had doubled again; and this year, with the introduction of new childcare entitlements, spending doubled once again. Total spending on the free entitlement now stands at £8.7 billion.

Figure 2.1. Total spending on the ‘free entitlement’ to a funded childcare place

Note: Because our data on total spending do not split out the universal and extended entitlements, we allocate total spending proportional to their budgets from the Dedicated Schools Grant (DSG).

Source: See https://ifs.org.uk/education-spending/methods-and-data.

To put this in context, in 2010–11, free entitlement spending was 4% of the level of the core schools budget. This year, the free entitlement budget is 13% of core school funding. This is a transformation in the scale of government support for early years education.

The free entitlement is not one single programme; different offers are available to children of different ages, with different eligibility requirements. These include:

- a universal offer of up to 15 hours a week5 for all 3- and 4-year-olds;

- a disadvantage offer of 15 hours a week for the most disadvantaged 2-year-olds;

- an extended entitlement to up to 30 hours a week for 3- and 4-year-olds in working families (combining the 15-hour universal offer with a 15-hour top-up).

Alongside these schemes is the new ‘expanded’ entitlement announced at the March 2023 Budget by the previous government (and subsequently implemented by the current government). These expanded entitlements have been rolled out over the last two years; since September 2025, they offer up to 30 hours a week for children aged 9 months to 2 years in working families.6

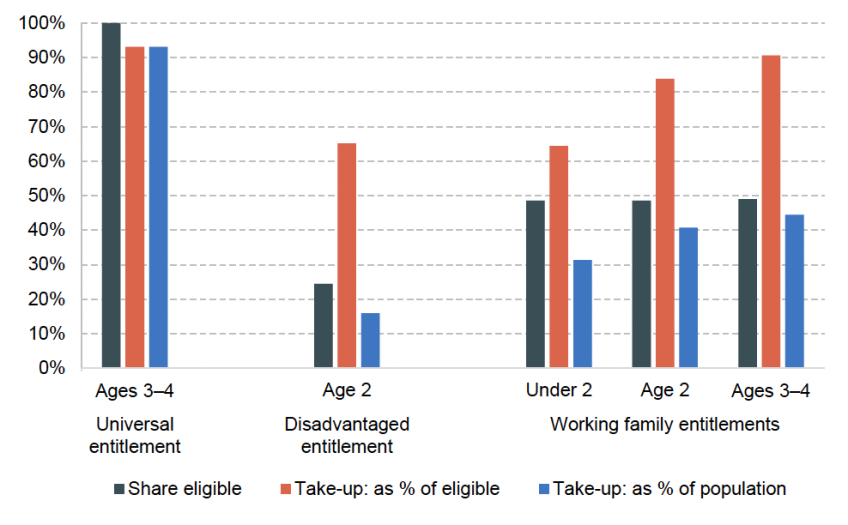

As Figure 2.2 shows, eligibility for and take-up of funded childcare vary quite a lot across the different entitlement programmes. Eligibility for the universal 3- and 4-year-old entitlement is, of course, universal across this age group. Just under half of children live in families that are estimated to be eligible for the working family entitlements.7

Figure 2.2. Eligibility and take-up for different elements of the free entitlement, 2025

Note: Based on data as at January 2025, when under-3 working family entitlements covered part-time rather than full-time places. Data are based on headcounts (number of children using any of each entitlement) rather than part-time-equivalent places. Eligibility for working family entitlements for 3- and 4-year-olds stops when children enter Reception (or reach compulsory schooling age). This means the share of all 3- and 4-year-olds (including those in Reception) that are eligible for the working family entitlement is estimated to be 34%. For comparability across ages and entitlements, we instead present eligibility and take-up rates as a share of the population not in Reception as at January 2025. Eligibility for working family entitlements is estimated by the Department for Education using data from the Family Resources Survey. Because of small sample sizes, DfE assumes the proportion of children eligible is constant across families with a 1- to 4-year-old.

Source: Department for Education, ‘Funded early education and childcare: 2025’ (https://explore-education statistics.service.gov.uk/find-statistics/funded-early-education-and-childcare/2025). See also methodology note (https://explore-education-statistics.service.gov.uk/methodology/funded-early-education-and-childcare).

Eligibility for the disadvantaged 2-year-old offer is much lower, at just under a quarter. This is notably low: when these entitlements were introduced in their current form, in 2014–15, eligibility was close to 40%, but years of cash-terms freezes in eligibility criteria have meant that eligibility has fallen. We return to these trends, and what this means for the shape of the early years system, in Sections 2.3 and 2.4.

Among 3- and 4-year-olds that are eligible for funded childcare, take-up rates are quite high: 93% of 3- and 4-year-olds take up at least part of their universal entitlement, and 91% of eligible 3- and 4-year-olds take up at least part of their working family extended entitlement. Take-up rates are lower among younger age groups, with 84% of eligible 2-year-olds and 64% of eligible under-2s taking up the working family entitlement. Take-up amongst disadvantaged 2-year-olds is considerably lower than take-up of the 2-year-old working entitlement (65% versus 84%), though this might in part reflect issues with children who are eligible for both entitlements being recorded as using the working rather than disadvantaged offer.8

In the next section, we analyse the take-up of the new ‘under-3’ working family entitlements, which were rolled out during 2024 and 2025, as well as spending on these new programmes. We then examine how spending on and take-up of existing early years programmes have changed over time (Section 2.3). Finally, we take a step back to look at the wider landscape of public support for formal childcare, analysing what these changes mean for the overall shape of childcare support in England (Section 2.4). These questions will be particularly important over the coming year as the government embarks on a major review of the shape of England’s childcare and early years system.

Of course, funded childcare entitlements – and wider childcare subsidies through the tax and benefit system – are only part of the early years picture, though they are very much the largest part in terms of spending. In Box 2.1, we summarise some of the key policies announced in the government’s July 2025 ‘Best Start in Life’ strategy (Department for Education, 2025c), which aims to look at the wider landscape of early years services in addition to support for formal childcare.

Box 2.1. Best Start in Life strategy and the government’s missions

In July 2025, the government released its ‘Best Start in Life’ strategy, which aims to present a framework for supporting children’s development until the end of Reception year. In addition to prenatal investments in maternal physical and mental health, the strategy covered three pillars: family support, increasing access to subsidised early education and childcare, and support for quality early education (in both childcare and Reception settings).

Of all the policy reforms discussed in the strategy, by far the biggest in terms of spending implications were the commitments – inherited from the previous government – to go ahead with rolling out the expanded entitlements for children under 3 in working families. However, these new expanded entitlements will do very little to close gaps in children’s early development: there is little robust evidence that formal childcare in the very earliest years has significant benefits for children’s development. Even if there are benefits to be had, by prioritising children in working families this policy steers support away from the poorest children (who typically benefit the most from formal childcare). This reflects the fact that the new expanded entitlements are aimed much more strongly at increasing labour supply among parents – in the government’s parlance, contributing to the growth mission (rather than necessarily helping to meet its opportunity mission aim to increase good levels of development at the end of Reception).

The other strands of Best Start in Life are more clearly linked to the opportunity mission – though the funding announced, of about £500 million a year, is around a tenth of the £5 billion a year we are set to spend on the expanded childcare entitlements by 2028–29.

One important step in the strategy was a commitment to expand access to Family Hubs, which aim to bring together evidence-based services in health, education and childcare as well as additional targeted support. This model is based on the Sure Start model of the 2000s, which research at IFS has found had wide-ranging and long-lasting benefits for children’s development (Carneiro et al., 2025). But even with the top-up funding announced as part of the strategy, total spending on integrated early years services will be less than half as high as peak Sure Start spending, and is meant to cover a much wider age group.

The final pillar of the strategy looked at the early years workforce and the quality of provision in childcare and Reception. A simplified and improved training system could deliver real benefits, though it comes against a backdrop of quite high turnover amongst staff.

2.2 Spending on and take-up of the under-3 childcare entitlements

Take-up of the new entitlements

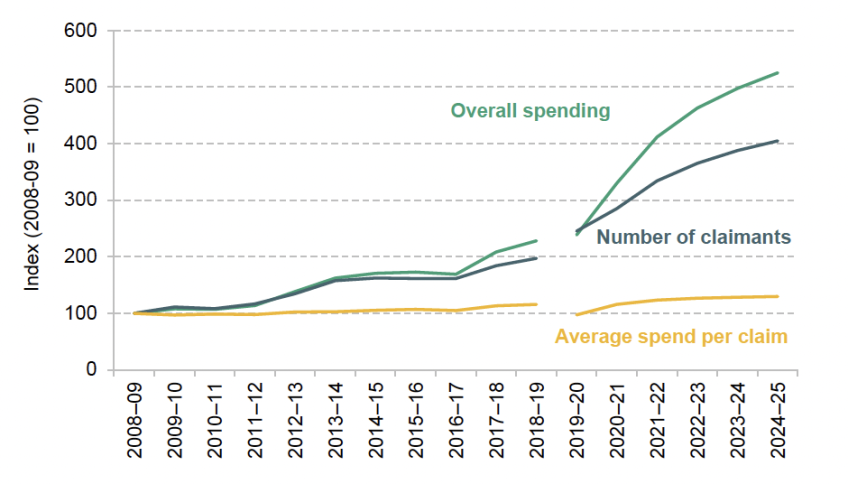

The new childcare entitlements for working families with a child under 3 represent a major change in the landscape of early years and childcare support in England. As Figure 2.2 suggests, these entitlements have proven popular, with two-thirds of eligible children under 2 and five in six eligible 2-year-olds using at least some of their entitlement.

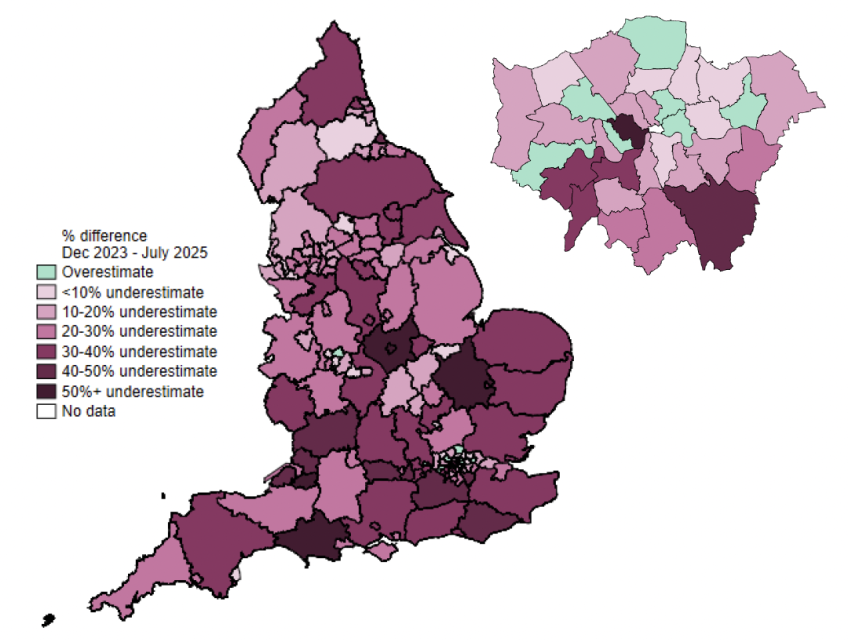

Indeed, as we discussed in Farquharson (2025), the new entitlements have proven much more popular than initially expected. Figure 2.3 shows, for each local authority, the change in part-time-equivalent places between the first version of the 2024–25 Dedicated Schools Grant budget (issued in December 2023) and the latest estimates (issued in July 2025). Across most of England, take-up of the new entitlements turned out to be substantially higher than initially estimated: the number of part-time-equivalent places taken up under the new entitlements was revised upwards by 26% over the course of 2024–25.

Figure 2.3. Percentage change in predicted take-up of the new childcare entitlements in 2024–25, from initial estimates (December 2023) to latest estimates (July 2025)

Note: Map shows the percentage change in expected take-up of the new working family entitlements for 2024–25 between the first version of the 2024–25 Dedicated Schools Grant budget (December 2023) and the final version (July 2025). Areas where expected take-up has fallen (an initial overestimate of take-up) are shown in green; other areas had an initial underestimate. Greater London is shown separately for visibility.

Source: Adapted from figure 2 of Farquharson (2025). Based on data from the December 2023 and July 2025 versions of the Dedicated Schools Grant for 2024–25.

There are good reasons why initial estimates of the take-up of these new entitlements would need to be revised. First, there is considerable uncertainty as to how many families would have been eligible even if the entitlements had had no effect on working patterns or how they organised their childcare. The best current estimates are based on data from the Family Resources Survey, but there will always be a degree of uncertainty in using survey data (especially when looking at sub-national estimates). On top of this, local-authority-specific population forecasts are uncertain and subject to change, and this might be particularly true of the youngest age groups.

Take-up rates might also have turned out to be higher than initially expected because more families changed their behaviour than initially expected. For example, if more working families switched from using informal care (such as grandparents) to formal care once they gained access to funded hours, this would drive up take-up rates. It is also possible that higher-than-expected take-up rates reflect greater-than-expected labour supply responses – that is, that more parents are moving into work or working more (and so becoming eligible for the new entitlements or increasing the amount of childcare they use). Disentangling these different drivers will be central for understanding what impact the new entitlements are having on families’ employment patterns and disposable incomes.

That said, the scale of the change – more than 75,000 more part-time-equivalent places than initially expected – is nevertheless remarkable. And that has had significant fiscal implications: total spending plans for the new entitlements in 2024–25 were revised up within the year by £440 million, or 28%. This was partly offset by underspends elsewhere in the early years budget, so overall early years funding from central government was revised upwards by £315 million. Like many other education programmes (including pupil premium, free school meals and high needs funding), childcare entitlements fall under the ‘Departmental Expenditure Limits’ set at the Spending Review. This means that, when demand outstrips expectations, it creates spending pressure on the department’s budget as a whole that must be met by either spending less elsewhere in education or having overall budgets topped up.

What this means for spending going forward is not yet clear. One area of uncertainty is what effect the September 2025 move from part-time (15-hour) to full-time (30-hour) entitlements will have. Estimates from the Office for Budget Responsibility’s March 2023 Economic and Fiscal Outlook, based on previous research at IFS (Brewer et al., 2022), suggest that impacts on parents’ labour supply will largely kick in only with the full-time offer. This might suggest that take-up rates will increase further.

Previously, we set out how total spending on the new entitlements might change based on different scenarios for take-up and per-hour funding (Farquharson, 2025). We estimated that spending in 2028–29 could reach between £4.8 billion and £5.3 billion (in current prices). On a central estimate, that is around £1 billion more than would be implied by a real-terms freeze in the allocations set out in the 2023 Budget, when these policies were first announced. A top-up announced at the Spending Review in June this year (worth £640 million in today’s prices for 2028–29) will go some way to closing this gap, but could still leave additional funding pressure if these new entitlements continue to prove popular.

Provision of the new entitlements

At the time the new entitlements were announced, one widespread concern was around the deliverability of a big expansion: would childcare providers be willing to offer the new publicly funded entitlements, and would they be able to expand to offer more places to the under-3s?

Higher-than-expected take-up rates are one sign that, across much of the country, providers are indeed offering free entitlement places. Importantly, most of the places will not be ‘new’ – based on estimates from the Office for Budget Responsibility, we estimated at the time of the 2023 Budget that perhaps five in six places funded by the new entitlements would have existed even without the expanded entitlements, with parents rather than government paying (Farquharson, 2023). And data from the Childcare and Early Years Survey found that the share of 0- to 4-year-olds using formal childcare ticked up just 1 percentage point between 2023 and 2024, from 63% to 64% – a relatively small change, and well within the margin of error.9 While there is lots of uncertainty about the precise amount of ‘new’ childcare being delivered, what is clear is that a large majority of the childcare funded by the new entitlements would have happened anyway, lessening the delivery challenge.

The government also incentivised providers to offer these new entitlements by introducing funding rates for 2-year-olds and under-2s that were much more generous than the fees that parents were paying on the private market. This was partly to ensure that funding rates more closely mirrored costs (which are much higher for younger children), a change to providers’ previous practice of charging similar amounts for all pre-school children (Drayton et al., 2025). But this also gave a clear incentive for providers offering places to under-3s to opt into the publicly funded free entitlement system.

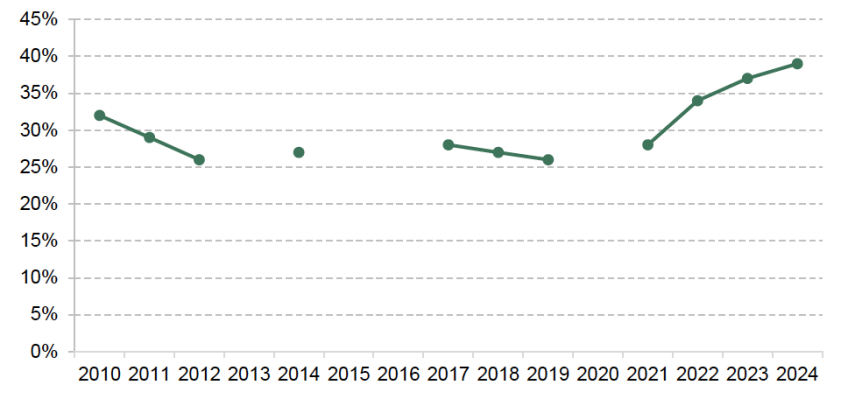

This is not to say there are no pressures in the system. Figure 2.4 shows the share of parents of 0- to 4-year-olds reporting that there are not enough childcare places in their local area. For most of the 2010s, between 25% and 30% of families with a pre-schooler felt that there was not enough childcare availability in their local area. Following the COVID-19 pandemic, that has increased to nearly 40% in 2024. Despite this, only 4% of families with a pre-school child not in childcare cited inability to find a place as a reason for not using childcare.10

Figure 2.4. Share of parents of 0- to 4-year-olds reporting a lack of childcare availability in their local area

Source: Department for Education, Childcare and Early Years Survey of Parents (various years).

Local childcare markets: pressures in bigger cities?

One factor that helps to explain why some parents perceive a lack of availability in their local area is that childcare is a very local market: a surplus of places in Barnsley is no help to a family living in Birmingham (and even within Birmingham, a family living in Erdington might not benefit from additional places in Edgbaston). And there are some indications of pressure in particular parts of the country, especially London and other major urban areas.

Figure 2.3 shows that take-up of the new entitlements generally exceeded initial expectations. London (and some other urban areas) is a notable exception: in 7 out of 32 London boroughs, take-up was lower than initially expected. And while nationally 91% of parents who applied and were approved for the new entitlements had successfully found and taken up a childcare place, that validation rate was 85% in London.11

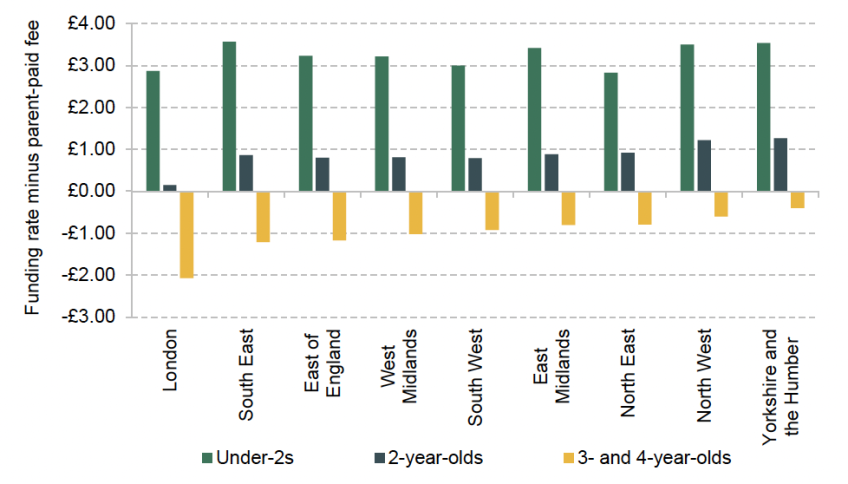

One possible contributing factor is that funding rates in London have been less generous (compared with market prices) than in other regions. Figure 2.5 shows the difference between the average hourly funding rate and the average hourly price charged to parents in each region of England in 2025. Funding rates always exceed market prices for under-2s and for 2-year-olds, while funding rates are less than market prices for 3- and 4-year-olds. This reflects a policy decision to have funding rates more closely reflect underlying costs (rather than ‘smoothing’ across ages so that parents pay a similar amount regardless of their child’s age).

Figure 2.5. Difference between average government funding rate and average parent-paid fees, by region, 2025

Note: Positive numbers indicate that average hourly funding in the region is greater than the price charged to parents; negative numbers indicate that prices are higher than funding rates.

Source: Department for Education, Childcare and Early Years Provider Survey, 2025, https://explore-education-statistics.service.gov.uk/find-statistics/childcare-and-early-years-provider-survey/2025.

But in London, the gap between funding and fees is smaller for the younger children, while the shortfall between fees and funding for 3- and 4-year-olds is larger. This suggests that funding rates in London are less generous compared with market prices than in other regions of the country.

2.3 Trends in take-up of and spending on existing free entitlement programmes

While much of the policy and delivery focus has been on the new expanded entitlements for working families with children under 3, as Figure 2.1 shows, these account for a little less than half of total free entitlement spending in 2025–26. In this section, we therefore examine changes in the take-up of and eligibility for other childcare entitlements, as well as effects on the wider market.

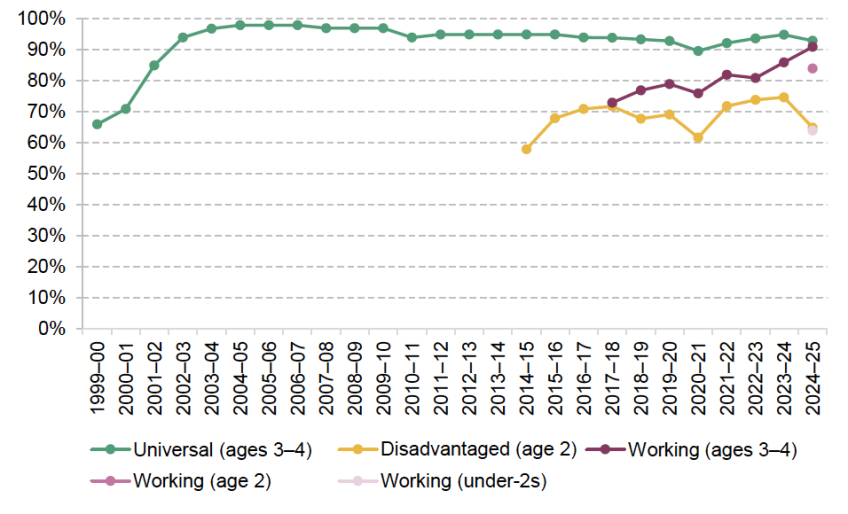

Figure 2.6 shows the take-up (as a share of the eligible population) of the different childcare entitlements over time. Take-up of the universal entitlement (shown in green) has been very high since the early 2000s. After a dip during the COVID-19 years, take-up has largely recovered, with 93% of 3- and 4-year-olds taking up at least some of their free hours in 2024–25 (equal to the pre-pandemic take-up rate).

Figure 2.6. Take-up of funded childcare entitlements (as a share of eligible population)

Note: Take-up reflects headcounts as a share of the relevant eligible population.

Source: Department for Education, ‘Funded early education and childcare’, 2025 (https://explore-educationstatistics.service.gov.uk/find-statistics/funded-early-education-and-childcare/2025) and its predecessors.

Take-up rates of the working family entitlement for 3- and 4-year-olds (shown in burgundy) have been rising fairly steadily. When the offer was introduced in 2017, just over 70% of eligible families took up at least some of their extended hours. Before the pandemic, take-up rates were around 80%. In the last two years, take-up rates have jumped up again and by 2024–25 stood at 91% – just 2 percentage points shy of the take-up rate for the universal entitlement. This growth in take-up could reflect the policy ‘bedding in’ (with take-up rates rising as parents become more familiar with it and some of the operational challenges are resolved). It could also reflect the greater value of these new entitlements: as childcare prices have risen (relative to economy-wide inflation), it becomes more expensive for families to purchase their own care, so the incentives to use free entitlement places are greater. Regardless of the drivers, rising take-up rates among this age group suggest that families with 3- and 4-year-olds are not being ‘crowded out’ of the childcare market by new publicly funded hours for the under-3s.

By contrast, take-up rates for the 2-year-old disadvantage offer (shown in yellow on Figure 2.6) had been slowly rising before 2024–25 (outside of the COVID-19 pandemic). But in 2024–25, take-up rates fell by 10 percentage points, from 75% to 65%. Partly, this will reflect some changes in data collection: perhaps around 5% of 2-year-olds are eligible for both the disadvantaged and the working family entitlements (Farquharson, 2024). While the guidance from central government was that a child eligible for both entitlements should be registered as claiming the disadvantage entitlement, this guidance was not universally followed. So there will be some disadvantaged children who are still receiving publicly funded childcare, but are registered as claiming a working family entitlement – contributing to lower take-up rates of the disadvantaged offer.

Even so, a 10 percentage point fall in take-up in one year is large, and probably too large to be fully explained by changing coding. One concern is that providers could be opting to offer places to 2-year-olds in working families, making it more difficult for those in disadvantaged families to find an early years place. The core funding rate for 2-year-olds is the same for both offers, worth on average £4,930 per year for a child taking up the full 570 hours a year in 2024–25 (though low-income families accessing either scheme also attract £570 a year in top-up funding from the early years pupil premium, which was extended to cover 2-year-olds in 2024–25). This means that if 2-year-olds in working families are more attractive to providers for other reasons (e.g. if these families are more likely to take up full-year places with parents paying the difference), then providers may be incentivised to offer places first to these working families.

Another possible – though longer-running – explanation is that the characteristics of families who are eligible for the 2-year-old disadvantaged entitlement have changed. The eligibility criteria for the 2-year-old disadvantaged offer have remained essentially the same since the programme was introduced in its current form in 2014–15. For families who are eligible because they claim certain means-tested benefits, the income cap (above which they lose eligibility) has also remained frozen in cash terms over this period.12 This means that the eligibility criteria have become more stringent over time, as the income cap does not keep pace with rising prices or earnings – meaning that eligible children are now, on average, more disadvantaged than they were a decade ago.

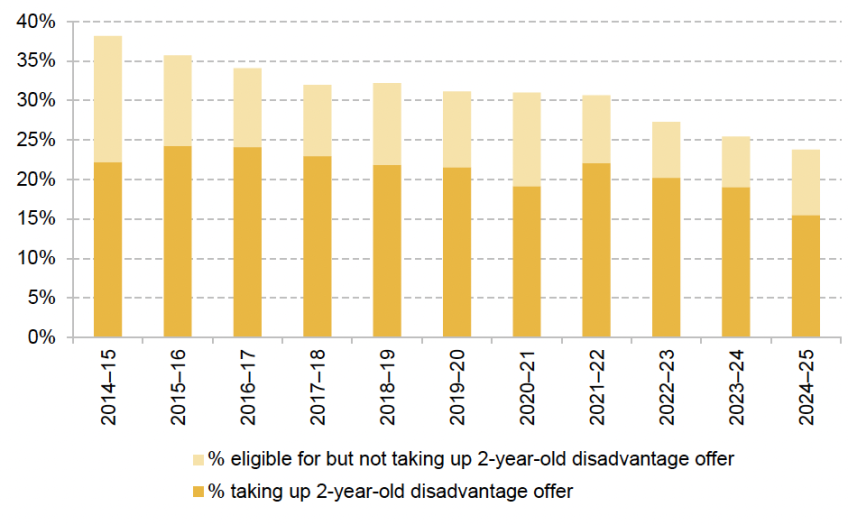

This is evident in Figure 2.7, which shows the shares of 2-year-olds who are eligible for and taking up the disadvantage offer in each year. When the entitlements were introduced in their current form in 2014–15, 38% of children were eligible for this offer. This had fallen to 31% by 2021–22. With rapid inflation following the pandemic pushing up (cash-terms) earnings, eligibility has fallen by 7 percentage points in the last three years, and now 24% of 2-year-olds are eligible for the entitlement.

Figure 2.7. Share of 2-year-olds eligible for and using the 2-year-old disadvantage offer

Source: Department for Education, ‘Funded early education and childcare’, 2025 (https://explore-education-statistics.service.gov.uk/find-statistics/funded-early-education-and-childcare/2025) and its predecessors.

Spending on existing childcare entitlements

For childcare providers delivering the free entitlement, the key input into their financial picture is the core per-hour funding rate. Core funding per hour has been set by the Department for Education through the Dedicated Schools Grant. It governs the amount of funding received by each local authority. Every individual local authority then allocates its total early years budget through its own Early Years Single Funding Formula; we discuss this process in more depth in Drayton et al. (2025). Core funding per hour differs from the spending measures used earlier in this chapter, which capture spending through other elements of the funding formula (such as targeted uplifts) as well as any wider spending done by local authorities.

In cash terms, core funding per hour has increased by 36% in the last decade for 3- and 4-year-olds (from £4.50 in 2016–17 to £6.14 in 2025–26). For 2-year-olds, cash-terms funding has increased twice as quickly, from £5.03 in 2016–17 to £8.65 in 2025–26. The difference in growth rates was largely down to a big adjustment to 2-year-old funding rates announced in the 2023 Budget, alongside the announcement of the new entitlements: funding rates for 2-year-olds rose by nearly 40% in cash terms between 2023 and 2024. In addition, from April 2024, 2-year-olds (claiming either the disadvantaged or the working family entitlements) became eligible for the early years pupil premium (EYPP), worth 68p per hour that year. This will have increased effective funding rates for providers delivering the disadvantaged 2-year-old offer, since most children receiving that entitlement will attract EYPP.

Of course, cash-terms increases are not the best measure of the resources providers have to deliver these entitlements: costs have risen over this period, too. And this is particularly true of childcare providers’ costs. Relative to the economy as a whole, a higher proportion of childcare providers’ costs comes from staffing (75% of total costs), with rent and premises costs (7%), food (3%) and energy (3%) making up most of the remainder.13 Many of these costs have been rising more quickly than economy-wide inflation. There have been particularly big rises in the costs of employing staff on low wages, as the national living wage for adults aged 25 and up rose by 70% between April 2016 and April 2025 (and lower rates for younger workers are increasingly being removed). The increase in employer National Insurance contributions – which, for the childcare sector, were not offset by a more generous employment allowance – have also pushed up costs significantly this year.

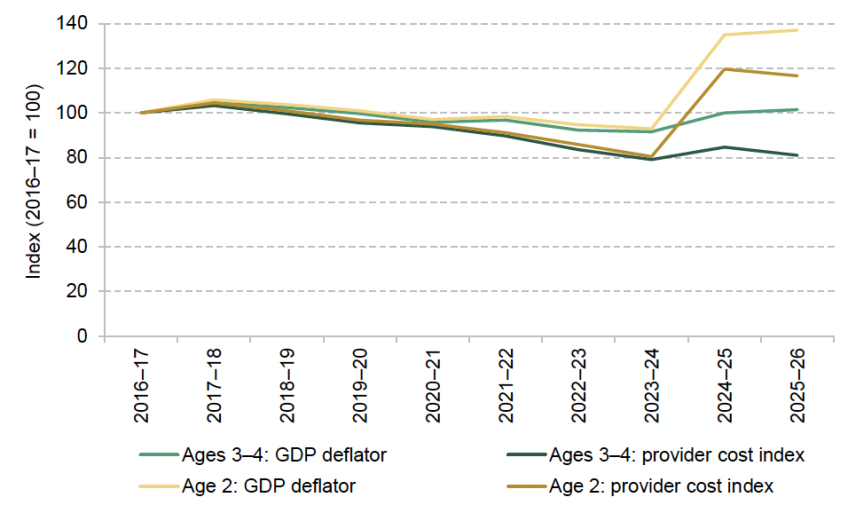

Figure 2.8 therefore shows how core funding per hour has changed after adjusting for two measures of inflation: economy-wide inflation (as measured by the GDP deflator) and childcare-provider-specific cost increases (based on our index of childcare providers’ costs).14 Since 2016–17, economy-wide inflation has increased costs by 35%. On our measure, childcare providers have instead seen their costs rise by 55% over the same period. This puts considerable additional pressure on hourly funding rates.

Figure 2.8. Core funding per hour for 2-year-old and 3- and 4-year-old entitlements, compared with economy-wide inflation and provider costs

Note: Childcare provider cost index captures growth in labour costs (employer cost of workers on full-time minimum wage and on average earnings); rent and energy costs; food costs; and other costs (proxied by economy-wide inflation). We follow the methodology in Drayton and Farquharson (2022), updating the labour costs elements to account for employer costs (employer National Insurance and pension contributions) in addition to gross earnings. Weights are determined by provider cost shares as reported in the 2019 Survey of Childcare and Early Years Providers.

Source: National Living Wage for workers aged 25+; Office for National Statistics, Average Weekly Earnings (EARN01), whole economy adjusted for seasonality. Costs for food and property costs come from relevant sub-series of the Consumer Prices Index. ‘Other’ costs are proxied by the GDP deflator (November 2025).

Taking economy-wide inflation into account, core funding per hour for 3- and 4-year-olds has recovered its real-terms value and now sits at about the same level as in 2016–17; it is still about 3% below its peak in 2017–18. But taking childcare-provider-specific costs into account, core funding rates for 3- and 4-year-olds remain 19% lower than a decade ago. Effective resources per hour fell by 4% just in the last year, largely due to big increases in employer costs.

By contrast, the big cash-terms increases in core funding per hour for 2-year-old entitlements have translated into substantial increases in resources per hour. Even after accounting for childcare providers’ rising costs, funding per hour is 17% higher than it was a decade ago. This largely reflects a policy decision to see childcare funding more closely reflect underlying costs at different ages. Prior to 2024–25, funding rates for 2-year-olds were around 13% higher than rates for 3- and 4-year-olds. But costs are much higher for younger children: the maximum staff-to-child ratio for 2-year-olds was 1:4 for most of this period (since increased to 1:5), while for 3- and 4-year-olds the ratio can be 1:8 or 1:13 depending on the staff’s qualifications.

2.4 The shape of England’s childcare system

New childcare entitlements for working families with children under 3 represent the latest, and biggest, step in the transformation of England’s early years system. But England’s system of support for childcare encompasses an even wider range of programmes, stretching across three government departments. In addition to the various free entitlement policies, the Department for Education also runs a programme to subsidise childcare expenses for full-time English students (with family incomes below a cap) – see Box 2.2. There are subsidies for childcare costs for working families receiving benefits (managed by the Department for Work and Pensions), and a wider set of policies offering subsidies to working families higher up the income distribution (run by HM Revenue and Customs).

Box 2.2. Childcare grants for students

An additional channel of public spending on childcare comes through subsidies for students. This applies to full-time student parents in higher education, through a system of childcare grants. Student parents in further education can also receive support with childcare costs through the ‘Care to Learn’ scheme; this is a much smaller programme (just £5 million of spending in 2021–22a), so below we focus on childcare grants for university students. Parents are eligible for the grant if:

- they are taking out (or are eligible for) undergraduate ‘student finance’ such as tuition fee loans for full-time English university courses;

- they are not taking out a postgraduate loan;

- they have children under 15 (or under 17, if the children have special educational needs); and