Downloads

Download report PDF

PDF | 658.92 KB

Executive summary

The Post-16 Education and Skills White Paper sets out the government’s proposals for how England’s post-16 education and skills system should be organised, governed and funded. It brings together a wide range of policies across further and higher education, including curriculum reform, changes to institutions and adjustments to funding and finance. This report focuses primarily on the funding and finance elements of the White Paper and their implications for learners, providers and public spending.

Key findings

- The White Paper sensibly considers the entire post-16 education system – further and higher education – together. This is a step in the right direction, but while the scope is broad, the paper mostly focuses on individual policy measures and the proposals do not always add up to a coherent overall strategy. There is insufficient indication of how the different reforms connect, or strategic vision for how key trade-offs in the system will be resolved.

- The government has set a headline target of two-thirds of young people participating in higher-level learning (degrees and advanced technical courses), but with no deadline. Currently, about half of young people participate in higher-level learning. Based on existing trends, the goal would be met by the late 2030s. Achieving the target earlier, by 2030, would mean around an extra 50,000 young people participating in higher-level training relative to current trends. The government should set a clear deadline for the target as this will determine how ambitious it is.

- The White Paper confirms that funding for 16–19 education will increase by £450 million in real terms between 2025–26 and 2026–27, with the extra coming from within the Department for Education’s budget set out in the 2025 Spending Review. This translates into a 3% increase in real-terms spending per student between 2025–26 and 2026–27. That is a significant increase given the overall 1.8% increase in day-to-day spending implied by the Spending Review over this period. Even so, funding levels will remain below those of the early 2010s – with real-terms funding per pupil around 4% lower in colleges and 18% lower in school sixth forms.

- The government has committed to increasing the cap on tuition fees for domestic undergraduates in line with inflation each year. This will arrest the decline in real-terms per-student teaching resources, which had been steadily eroded by successive cash-terms freezes to the tuition fee cap since the tripling of fees in 2012/13. Although the fee cap was already increased with inflation this year (to £9,535), confirming an ongoing path of inflation-linked increases provides some much-needed certainty for universities and prospective students alike.

- The new Lifelong Learning Entitlement is expected to be available from September 2026. This will give adults from age 18 a flexible loan entitlement equivalent to four years of post-18 study (worth £38,140) to use across further and higher education – including, in some subjects, for individual modules of larger courses. This has the potential to make it easier to mix academic and vocational study, as well as supporting those retraining later in life. But its success will depend on learners and employers seeing value in individual modules. Early evidence underscores the delivery challenge with the Lifelong Learning Entitlement: in a recent trial of short courses, only 125 people enrolled compared with an expectation of around 2,000.

- Living-cost support for students – which is provided in the form of maintenance loans – has become substantially less generous in real terms over the last decade. The maximum loan has been increased in line with forecast inflation each year, but inflation has been higher than expected, and fewer students have been entitled to the maximum each year as a result of a long-running freeze in the household income thresholds that determine the amount of loan people are eligible for. The government intends that the maximum loan will continue to rise in line with inflation, but if it maintains the freeze in income thresholds, by 2029/30, some students may be able to borrow over £1,000 (around 15%) less in real terms than equivalent students would be entitled to this academic year.

- The government will reintroduce maintenance grants for low-income students studying ‘priority subjects’ by the end of this parliament. It has said little about the design of the new grants, with more detail promised at the Budget. Limiting the grants to those on ‘priority courses’, as the government plans, and who are also currently eligible for the maximum student loan would lead to about 10% of England-domiciled students being eligible. If, for example, the government awarded a flat grant worth £4,000 a year to this group, the total cost would be around £500 million. Restoring the system of maintenance grants that was in place until 2016/17 – where more than half of students received grants – would cost around £2.6 billion in today’s prices.

- The government plans to introduce a new levy on tuition fees paid by international students, with further details expected in the Autumn Budget. If the levy were applied at the 6% modelled in the immigration White Paper, it would likely have raised slightly less than £600 million if it had been in place in 2023/24. The government should be clear on the economic rationale for such a levy, which would constitute a tax on the UK’s exports. There is no meaningful sense in which the revenues raised from this levy will “pay for” the reintroduction of maintenance grants for some students, as government has claimed.

- Labour’s 2024 manifesto proposed broadening the apprenticeship levy into a growth and skills levy, allowing employers to use levy funds for a wider range of training. The White Paper confirmed that this will go ahead from April next year, but there are still big questions over design. The government has so far only indicated that new ‘apprenticeship units’ will fall within scope, without defining what these are. For employers and learners planning their training, greater clarity is needed sooner rather than later.

1. Introduction

Few areas of public policy have experienced as much change as skills policy. Successive governments have sought to reshape the system, often arguing that it fails to deliver the skills the economy demands or the opportunities individuals need. Reforms have typically been presented as ways to boost productivity, drive growth and expand opportunity. Since taking office, the current government has announced a series of skills initiatives, including the creation of Skills England, reforms to the apprenticeship levy and the transfer of responsibility for skills policy from the Department for Education to the Department for Work and Pensions. It has also signed up to some of the major reforms announced by previous governments, most notably the Lifelong Learning Entitlement.

The Post-16 Education and Skills White Paper, published on 20 October, marks the most wide-ranging statement of this agenda to date. The document brings together a mixture of previously announced policies, new proposals and broader ambitions. Its measures span the full post-16 landscape – from support for young people at risk of becoming NEET (not in education, employment or training) to adults engaged in lifelong learning, and including both academic and vocational routes – and draws on a wide range of policy levers, including curriculum reform, institutional structures, regulation and funding.

Taken together, the proposals amount to a broad programme of reform, but they vary considerably in their level of development. Some build on years of policy work, while others are presented as early-stage ambitions that will require substantial further design. More importantly, the White Paper offers limited explanation of how its different strands are intended to fit together or how the government plans to navigate the trade-offs that any skills strategy must confront. Many proposals touch on long-standing tensions in the system – for example, between national direction and local autonomy – but do not always resolve them. The result is a programme that is wide in scope but not yet clearly prioritised, and whose effectiveness will depend heavily on the (strategic) choices made during implementation.

This report is structured as follows. We begin in Section 2 by reviewing the overarching aims of the White Paper, and the government’s new targets for post-16 education participation. The remainder of the report then focuses on the funding and finance elements of the White Paper. These are central to understanding what the government’s ambitions on skills will mean in practice: how resources will be distributed across sectors, who will ultimately bear the costs of education and training, and whether the incentives created by the skills system for learners and providers align with the government’s stated objectives. Section 3 analyses the government’s funding decisions; Section 4 examines the proposed changes to student finance; Section 5 explores the evolving role of levies within the skills system; and Section 6 concludes.

2. The government’s post-16 reform package

The reforms in the White Paper sit within a broader set of decisions that governments must make when shaping post-16 education and training. Skills policy has to support a wide range of aims, involve many different institutions and respond to changing economic conditions. Any attempt to reshape the system therefore requires taking positions on several underlying judgements about how post-16 education should be organised, governed and funded. These decisions influence the incentives facing learners, providers and employers, and help determine whether the system functions in a coherent and effective way.

There are several important choices that shape how the post-16 system operates. In many cases, the question is not which of two opposing options to select, but where along a spectrum the system should sit. These include:

- How the costs of education and training are shared between government, employers and learners. All three groups stand to gain from investment in skills, but they face constraints: learners may be uncertain about the returns, employers may be reluctant to fund skills at risk of employees leaving, and government must balance skills spending against other priorities. This can lead simultaneously to underinvestment across the system, and to risks of subsidising activity that would have taken place anyway.

- Central direction and local autonomy. National coordination can support consistency, clear priorities and a coherent offer for learners – as well as supporting wider national priorities such as an industrial strategy. Greater local autonomy can help provision reflect local labour market needs and make better use of existing institutions.

- Structured programmes and flexible pathways. Full programmes provide clarity, strong signalling and well-defined progression routes, and it can be easier to demonstrate the returns to training and study. Modular or credit-based approaches can support adult learners, retraining and part-time study.

- Responsiveness and stability. A system that evolves too slowly may fail to keep up with technological and economic change, while one that changes too frequently can create uncertainty and make long-term planning difficult for providers and learners.

- Broad participation and targeted investment. Policymakers must balance widening access with the fact that returns vary significantly by course and sector. Some routes deliver high wage and productivity gains; others provide broader social value or support inclusion.

These choices interact and the stance taken on one can reinforce or constrain decisions taken elsewhere. They also provide an important backdrop for interpreting the White Paper, which is summarised in Box 1.

Box 1. Overview of key reforms in the Post-16 Education and Skills White Paper

1. Qualification and curriculum reform

- Curriculum reform at Level 2 (GCSE or equivalent) and below, introducing two new post-16 pathways (occupational and further study).

- Comprehensive reform of Level 3 (equivalent to A levels) vocational qualifications, replacing existing vocational qualifications with new qualifications (‘V levels’) as the main alternative to A levels and T levels.

2. System coordination and oversight

- Skills England established as a national coordinating body, working with strategic authorities, employer groups and government agencies through the Labour Market Evidence Group.

- Additional oversight of higher education delivered in colleges, with the Office for Students and the Department for Education jointly responsible for ensuring consistent standards, accountability and quality.

3. Greater employer involvement in shaping provision

- Sector skills packages and Jobs Plans in priority industries (e.g. construction, digital, engineering), setting out how government and local partners will build the skills these sectors need and providing targeted funding to support this.

- Replacing the apprenticeship levy with a growth and skills levy from April 2026, with identical revenue-raising conditions but allowing employers to use levy funds for short, non-apprenticeship training courses.

4. Funding announcements

- Recommitting to the Spending Review settlement, which offers an additional £1.2 billion (cash terms) per year by 2028–29 for 16–19 education and adult skills. Allocations from within this envelope will see the total 16–19 budget increase by £450 million in real terms between 2025–26 and 2026–27.

- Tuition fee caps to increase in line with inflation in 2026/27 and 2027/28, with plans to increase tuition fees automatically in future academic years subject to quality conditions.

- No specific announcements on grant funding for universities, but a commitment to reform the Strategic Priorities Grant to ensure funding aligns with the government’s priority sectors.

5. Changes to student support and entitlements

- A Youth Guarantee offering an automatic place in further education (FE) for school-leavers without a post-16 study plan, and a guaranteed job for young people (up to age 24) on universal credit who remain unemployed for more than 18 months.

- Introduction of the Lifelong Learning Entitlement (LLE) from 2026/27, allowing adults to access loan funding equivalent to four years’ worth of education and training for courses at Levels 4–6, which is worth £38,140 (equal to four years of higher education study based on 2025/26 fee rates).

- Maintenance loans to rise annually with inflation.

- Introduction of new means-tested maintenance grants for disadvantaged students, targeted at those on specific priority courses at Levels 4–6, which will be funded by a new levy on international students.

6. Workforce development

- Introduction of a new professional development pathway for FE teachers and strengthened training standards across the FE workforce.

Assessing the government’s overall post-16 reform package

The White Paper brings together a wide range of reforms across further and higher education, adult learning and employer engagement. It is best understood as a collection of small- to medium-sized interventions rather than a single, transformative overhaul of the system. Some policies, including the Lifelong Learning Entitlement, have undergone years of policy development; others, such as V levels, are only just being announced and are likely to require extensive consultation. A number of proposals also read more as statements of ambition than as immediately deliverable plans.

What the White Paper does not provide is a clear account of how its many strands are intended to work together. The document sets out changes across qualifications, funding, oversight and learner support, but offers little sense of which elements are most central, how they will interact or how the government intends to manage the trade-offs between them. As a result, the package does not yet read as a coherent or clearly prioritised strategy. Instead, it risks becoming a set of initiatives that may improve parts of the system, but that could also pull in different directions without a clearer overarching framework.

On the balance between central direction and local autonomy, for example, the Adult Skills Fund has been progressively devolved to local areas since 2019 (Drayton et al., 2025), in principle giving them greater scope to shape provision in line with local labour market needs. In practice, however, a large share of the budget is tied up in statutory entitlements that reflect national priorities and leave limited room for local discretion. The White Paper also strengthens the role of Skills England as a national coordinating body, setting expectations for how provision should align with wider economic objectives. These developments need not be incompatible, but they do mean that the headline shift towards local autonomy sits alongside clear constraints on what local areas can meaningfully change.

There are similar tensions in the White Paper’s approach to questions of which types of training are prioritised. The document signals an ambition to give employers a stronger role in shaping the skills system, with greater autonomy over – for example – the types of training that can be subsidised by levy funds. Set against that, there are also clear signals of a desire for greater government involvement in choosing the mix of training to support, with several new initiatives that focus on a new category of ‘priority’ courses.

The White Paper proposals also arrive against a long-standing backdrop of frequent change across the skills system, even as policymakers emphasise the need for greater stability. Since 2020 alone, there have been four major changes to the post-16 vocational education system. These include the introduction of T levels, the proposed move to the Advanced British Standard, the withdrawal of funding for large parts of the applied general qualification system (e.g. BTECs), and now the creation of V levels. This level of churn carries significant transitional costs for providers, who must redesign curricula and retrain staff. But the more enduring burden falls on learners and employers, who have to navigate a system in which pathways and qualification labels change repeatedly.

Introducing such a large set of reforms simultaneously will also place significant pressure on implementation, particularly in a context where delivery relies on dozens of universities, thousands of colleges and training providers, and hundreds of thousands of employers. The reforms set out in the White Paper cannot simply be delivered from the centre, and without good coordination there is a risk that individual changes progress on their own rather than adding up to a genuinely joined-up system.

A headline target for skills

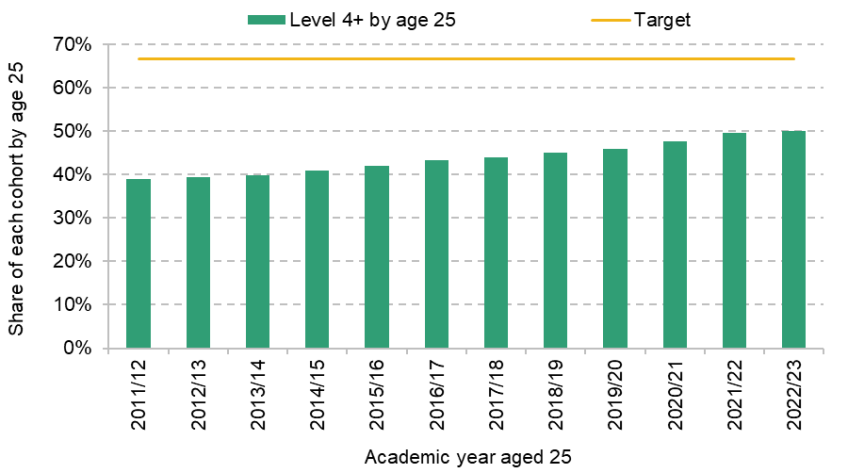

In addition to policy proposals, the White Paper sets out a number of system-wide targets intended to measure progress. In principle, setting clear goals is sensible: it helps define what success looks like and provides a basis for monitoring change over time. However, the specific targets in the White Paper raise several questions. The headline participation goals illustrate this clearly. The government aims for 10% of young people to enrol in Level 4 or Level 5 courses by 2040 (up from 5.8% in 2022/23) and for two-thirds of young people to be participating in higher-level learning (Level 4 and above).

Figure 1 shows historical progress against the latter measure, tracking the share of each academic cohort in England who have undertaken higher-level learning by age 25. In 2022/23, the most recent cohort for which data are available, around half of young people had reached this milestone – meaning the two-thirds target represents a substantial increase. Participation has risen steadily since 2011/12, and if growth were to continue at a similar pace, the government’s target would be reached by around 2038. If the government wanted to achieve the target earlier, by 2030 for example, this would require around an extra 50,000 young people participating in higher-level training by then relative to current trends.

Figure 1. Percentage of each English academic cohort participating in higher-level learning by the age of 25

Source and note: Department for Education, 2025e. Higher-level learning covers all Level 4+ qualifications including higher education and work-based learning, such as higher apprenticeships.

The target considers higher-level learning in the round – across academic, technical and work-based routes – which is welcome. The difficulty is that, while both targets imply sizeable increases in participation, they offer only a limited guide to whether the skills system will genuinely change. The Level 4–5 target could, in principle, be met without any real shift in behaviour. For example, this could happen if existing degree programmes were modularised so that their early stages count as Level 4 or Level 5 learning. The higher-level learning target is similarly constrained: it includes no time frame, and on current trends would be reached by the late 2030s even in the absence of new policy. As a result, the targets themselves are relatively weak tools for driving or assessing system-wide reform: they lack clear milestones, can be met through presentational changes, and reveal little about whether learners are accessing high-quality pathways. What will ultimately matter far more is whether the wider package of reforms creates a post-16 system that offers a coherent set of attractive routes for learners.

3. The funding of colleges and universities

The capacity of further education providers and universities to deliver the reforms set out in the White Paper will ultimately depend on the resources available to them. Funding shapes what providers can offer, the pace at which they can adapt and the incentives they face. The White Paper sets out important changes to both further and higher education funding – including additional public funding for 16–19 education, delivered primarily by further education colleges and school sixth forms, and an increase in the university tuition fee cap. This section outlines the broader context for these commitments and assesses what the planned funding changes mean for resource levels across each sector.

Public funding for further education and skills

At the Spending Review in June, the government set the overall funding envelope for post-16 education for the remainder of this parliament. It announced an additional £1.2 billion per year in annual day-to-day funding for further education by 2028–29 in cash terms. This settlement appears to apply across the main elements of the further education and skills budget – 16–19 education, adult skills and apprenticeships – which together account for around £13.5 billion of public spending in 2025–26. Once adjusted for inflation, the Spending Review settlement equates to a real-terms increase of just over £400 million (in today’s prices) between 2025–26 and 2028–29, or around 3% over the period (Tahir, 2025). However, the Spending Review did not specify how this funding would be allocated across different parts of the skills system.

The White Paper sets out further detail for 16–19 education, which represents nearly 60% of college funding (Moura and Tahir, 2024). It confirms that £800 million will be added to the 16–19 budget in 2026–27 from within the Spending Review envelope. After consolidating £190 million already announced in May, this amounts to a £610 million cash-terms increase between 2025–26 and 2026–27. This means that the total 16–19 budget will increase by around £450 million in real terms over this period.

Figure 2 shows funding per student aged 16–18 in school sixth forms and colleges from the early 2000s, with projections for 2026–27 based on these announcements. Throughout the 2010s, funding per student fell sharply in real terms across both types of provider. Between 2010–11 and 2019–20, college funding per student declined by 14%, while school sixth forms experienced a far steeper 28% fall. This period has also seen a substantial increase in learner numbers: between 2018 and 2024, the population of 16- to 18-year-olds in England grew by 230,000 (13%), with a further 110,000 (5%) expected by 2028, when the cohort is projected to peak. These demographic pressures mean that additional investment is needed simply to maintain real-terms funding per student (Sibieta, Snape and Tahir, 2025).

Figure 2. Spending per student in 16–18 colleges and school sixth forms (actual and projected for 2026–27)

Source and note: Update of figure 4.2 in Drayton et al. (2025). We use HM Treasury’s GDP deflators, September 2025, and assume an equal percentage change for college and school sixth form spending between 2025–26 and 2026–27. For more information, see https://ifs.org.uk/education-spending/methods-and-data.

Recent years have seen some recovery in funding levels. Since 2020, increases in 16–19 funding have contributed to a modest rise in spending per student: across all institutions, real-terms funding per student grew by around 4% between 2019–20 and 2024–25 (Drayton et al., 2025). The funding set out in the White Paper for 2026–27 implies a 3% real-terms increase in spending per student aged 16–19 between 2025–26 and 2026–27. This would return college funding per student roughly to its 2012–13 level, and school sixth-form funding to levels last seen in the mid 2010s. Even after these increases though, college funding would remain around 4% below its 2010–11 level and school sixth-form funding around 18% below. In effect, the recent increases reverse some – but not all – of the real-terms decline seen during the 2010s. At the same time, the White Paper introduces a range of new expectations for colleges, including delivering new qualifications and strengthening the further education workforce, which will put additional pressures on college resources.

University tuition fees and teaching grants

A growing number of higher education providers are facing financial challenges, with around 45% of institutions forecasting a deficit in the 2024/25 academic year (Office for Students, 2025a). In recognition of these challenges, the government announced in November 2024 (Department for Education, 2024) that the cap on tuition fees for England-domiciled undergraduate students – which had been set at £9,000 from 2012/13 and increased only once, to £9,250 in 2017/18 – would increase by 3.1% to £9,535 for the 2025/26 academic year, in line with forecast inflation as measured by RPIX.1

In the post-16 White Paper, the government announced that the cap on tuition fees will be increased with inflation for the next two academic years. If these increases are based on the same measure as in 2025/26, we might expect the fee cap to increase to £9,800 in 2026/27 and £10,070 in 2027/28, as shown in Figure 3. The government plans to legislate to make increases in the tuition fee caps in line with inflation (‘indexation’) automatic in future years (from 2028/29 onwards). Making such rises the policy default is one way to make them less politically costly for the government – although, as in the case of fuel duty rates, scheduling future rises is no guarantee that they will actually happen.

Figure 3. Tuition fee cap for full-time undergraduate courses, per year

Note: Maximum tuition fees that UK universities can charge for home fee students starting or continuing full-time courses. Assumes fee cap increases from 2026/27 onwards in line with the Office for Budget Responsibility’s March 2025 forecasts for RPIX in the first quarter of each academic year. Dotted lines show evolution of fees in real terms since the rises in 1998/99, 2006/07 and 2012/13, using the financial year GDP deflator applying for the first half of the relevant academic year.

Source: Historical fee levels taken from relevant secondary legislation; Office for Budget Responsibility’s Economic and Fiscal Outlook, March 2025; HM Treasury’s GDP deflators, September 2025.

Providing clarity now on the government’s policy on future fee rises gives some welcome certainty to universities attempting to plan, and to prospective students making decisions, who would otherwise have little sense of how much their fees may be when they can still expect to be studying (and paying them) in three or four years’ time.

The optimal level of the fee cap will depend on political judgements about how much funding to allocate to universities, and on how the costs of tuition should ultimately be shared between students and taxpayers. However, as noted in the White Paper, sector estimates suggest that universities are not recovering their costs on publicly funded teaching activity (i.e. the teaching of domestic, or UK-domiciled, students). Given that the cost of delivering the same quality of teaching would be expected to increase over time as a result of inflation, an indefinite cash-terms freeze in the fee cap was unsustainable – at least without a greater contribution from the taxpayer through direct grants to universities. A funding model that relied on ever-increasing income from international fees to offset declining resources for domestic students would also not be sustainable in the long run – as highlighted by recent declines in international student recruitment.2

Prior to 2012/13, annual increases in fees of a few percentage points were standard. As shown in Figure 3, this meant that in the years following major rises (in 1998/99 and 2006/07) the value of fees was roughly maintained in real terms. It was only after the tripling of tuition fees to £9,000 that freezing fees in cash terms became the norm. During periods of freezes, the real-terms value of the fee cap was determined by inflation out-turns rather than an active policy decision by government about the right level – and higher-than-expected inflation, particularly after 2021/22, meant that the real-terms value of the cap fell by much more than government had anticipated when announcing the freezes. Indexation will not reverse the real-terms erosion in the fee cap over this period – which would take an above-inflation rise – but should mean fee levels are not further eroded.

The White Paper also announced that future fee uplifts (but not those in 2026/27 or 2027/28) will be conditional on providers ‘achieving a higher quality threshold through the Office for Students’ quality regime’. The idea of having fee caps that differ by provider is not new. From 2012, universities were able to charge the maximum of £9,000 only if they met requirements for improving access and participation, through access agreements with the Office for Fair Access (a predecessor of the Office for Students). From 2017, only those with a Teaching Excellence Framework award were able to increase fees to £9,250.3 The impact of the proposed conditionality from 2028/29 onwards will depend on the details of how this is implemented, and the Office for Students (2025e) is currently consulting on its approach to regulating quality.

What does this mean for resources for teaching?

Funding for teaching England-domiciled undergraduates comes from two main sources: tuition fees charged to students and direct grants paid to universities by the Office for Students for teaching particular high-cost courses. Crucially, increases in teaching grants – which now account for around 10% of overall teaching resources – have not made up for the substantial real-terms cuts in the fee cap. This has meant universities’ resources for undergraduate teaching have been eroded in real terms since around 2017/18. For students starting courses in 2022, teaching resources per year were £10,321 – just barely higher in real terms than for those starting courses in 2011, the year before the tuition fee cap was tripled (see Figure 4).

Figure 4. Up-front resources for teaching domestic undergraduate students (2025–26 prices)

Note: Cohort-based numbers divided by 3 – an approximate course length in years. Assumes overall funding for high-cost courses is maintained in real terms after 2025/26, and nets off estimated spending by universities on fee waivers and bursaries, which is assumed to be flat in cash terms per student after 2022/23.

Source: Authors’ calculations following same methodology as in Drayton et al. (2025), described at: https://ifs.org.uk/education-spending/methods-and-data.

Compared with a continued cash freeze, Drayton et al. (2025) estimated that the increase in fees in 2025–26 would spare the higher education sector a further real-terms cut to teaching resources of £350–400 million that academic year. Partly offsetting this, there was a £87 million (8.3%) cash-terms cut in the funding allocated to providers for delivering high-cost courses in the same academic year, from £1,043 million to £956 million. This followed a substantial cut in the funding that the Department for Education provided to the Office for Students through the Strategic Priorities Grant in the 2025–26 financial year (Office for Students, 2025b).

The tuition fee rises now announced are likely to be worth somewhere in the region of £700 million across the sector as a whole by 2027–28, compared with if there had been no further increase in fees. Unlike for 16–19 education, the post-16 White Paper did not make specific commitments on funding for higher education teaching from within the Spending Review envelope.4 Given much of the increase in the Department for Education’s budget announced at the Spending Review in June has already been allocated to other areas (notably schools, early years and further education), there is unlikely to be any substantial increase in overall teaching grants to universities during the Spending Review period (to 2028–29).

If there are no further real-terms cuts in funding for high-cost courses, we estimate per-student teaching resources will be roughly maintained at the same level in real terms for the next few cohorts of students as a result of tuition fee indexation, remaining around a fifth lower than the 2012/13 peak.

Who will ultimately pay more as a result of the indexation of fees?

The vast majority of eligible students take out government-backed student loans for the cost of tuition and make student loan repayments from their earnings. The amount students can borrow will increase in step with the fee cap. Under the loan terms applying for new student loan borrowers (Plan 5), we expect that around a quarter of any additional tuition fee loans extended will eventually be written off (40 years after graduation), with the expected cost of this met up front by government. Delivering the same increase in teaching resources through increasing teaching grants would be around four times as expensive for the taxpayer as delivering higher loans, as the whole cost of grants would be borne by the taxpayer.

For students who take out tuition fee loans, the increase in tuition fees will lead to higher loan balances in cash terms (compared with a continued freeze). But for most students, the impact on actual student loan repayments will not be felt for many years. This is because until the loan is paid off, monthly loan repayments only depend on a borrower’s earnings and not on their outstanding loan balance. For those borrowers who can expect to repay their loans in full before they are written off, the tuition fee rises will mean they continue making loan repayments for a few more months than they otherwise would have, typically in their 40s. Around one-in-five borrowers will never repay any more, as they would never clear their loans even if fees had been frozen again.

4. Post-16 education student finance

The extent to which learners can take up post-16 education depends not only on the courses on offer but also on the financial support available to them. The Lifelong Learning Entitlement – originally announced in 2020 – represents a potentially major shift in how higher-level education will be financed. As a result, individuals will have access to a loan entitlement worth the equivalent of four years of post-18 study. Alongside the Lifelong Learning Entitlement, the White Paper includes changes to maintenance support, with uprated maintenance loans and new targeted maintenance grants for low-income students studying priority subjects. These measures will play an important role in determining who is able to take up study and under what conditions. This section examines each element in turn.

Lifelong Learning Entitlement

The government has reaffirmed its plan to reform student finance through the introduction of the Lifelong Learning Entitlement (LLE), which will give ‘each individual access to 4 years’ worth of loan funding for higher level education or training to use over their working lives’ (Department for Education, 2025a). This represents a significant change in how higher-level courses are funded. First announced in 2020, the first LLE-funded courses are expected to open for applications in September 2026.

The LLE can be viewed as a package of three connected reforms to the post-18 loan system (Tahir, 2023). First, it will unify the two existing loan schemes – higher education student loans and advanced learner loans for further education – into a single integrated system, simplifying what is currently a fragmented set of arrangements. Second, it will remove the ‘equivalent or lower qualification’ (ELQ) rule, allowing adults to access funding for courses at the same level as one they already hold or lower. Third, it will introduce modular funding, enabling learners to take out loans for individual modules or short courses rather than only for full qualifications. All eligible learners will receive access to their full entitlement from age 18, and existing adult learners will transition onto the new system with a residual entitlement based on the funding they have previously drawn down. Although at least initially, learners will be able to access modular funding only in subject groups that address priority skills gaps and align with the government’s Industrial Strategy.

The White Paper sets the ambition of the LLE as ensuring ‘that everyone can upskill throughout their working life, with access to short, modular courses or longer periods of training’. Removing ELQ restrictions and extending loan funding to modular study at Levels 4–6 should, in principle, make it easier for adults to retrain or update their skills. Yet whether this happens in practice will depend on both learner demand and provider participation, each of which presents distinct challenges.

On the learner side, it is difficult to gauge how much unmet demand exists for modular study and the extent to which access to loans is an important barrier to study. The Learning and Work Institute’s Adult Participation in Learning Survey (Phipps et al., 2025) shows that the share of adults citing cost as a barrier to learning rose from 8% in 2019 to 24% in 2025.5 Yet adults also point to time pressures, work or caring commitments, low confidence, feeling ‘too old’ or difficulty identifying suitable courses. Making modular courses eligible for loans is unlikely to address these broader constraints.

The LLE may reduce financial constraints for adults, but learners taking out loans will still need good information on the likely returns to the courses they are taking. In general, there is a distinct lack of evidence on the labour market returns to modular or ‘micro-credential’ learning. While the UK has extensive evidence on the returns to full qualifications, particularly degrees, there is almost none on the value of short-course study. A recent OECD review of short courses in higher education across different countries concludes that there is ‘very limited evidence’ on the value of these courses ‘to learners and the wider society’ (OECD, 2021, p. 31). In the absence of clear evidence on returns, learners may be reluctant to take on debt for modular courses whose economic value is uncertain. Indeed, early evidence from the Office for Students (2024) on its short-course trial in 2022/23 illustrates the challenge. Around 2,000 people were expected to enrol in short courses funded by loans, but in reality only 125 people enrolled in these courses. This low uptake highlights the need for clear communication and effective promotion of modular provision under the LLE to achieve meaningful scale.

The incentives for providers are also uncertain. Even where modules could, in theory, be carved out of existing degree programmes, delivering them as standalone units can be costly. Providers may need new systems for credit accumulation and transfer, additional quality assurance processes, and redesigned curricula that were originally built around longer, sequential programmes. As a result, the supply of modular provision may expand slowly, potentially limiting the choices available to learners in the early years of the LLE.

Loans for students’ living costs

As well as loans for tuition fees, government provides support for students’ living costs. For higher education students, these are in the form of maintenance loans, with most students entitled to borrow an amount each year which reflects their living situation (whether they live at home and whether they study in London) and their household income. In the White Paper, the government confirmed that maximum maintenance loan entitlements will continue to increase each year in line with forecast inflation. On current forecasts, this could mean maximum loan entitlements for those living away from home and studying outside of London will increase from £10,544 in 2025/26 to £10,833 in 2026/27 and £11,132 in 2027/28.

Increasing maximum maintenance loan entitlements in this way has been long-standing government policy, with entitlements increasing by between 2.3% and 3.2% in each academic year for the last nine years. Despite this policy, the real-terms generosity of student maintenance support has still declined substantially over the last decade. This has been a result of two features of how maintenance loan entitlements are set:

- Increases in loan entitlements are set based on forecasts for inflation. In recent years, higher-than-expected inflation has led to a real-terms loss of value in the maximum amount the poorest students can borrow of around 10% since 2020/21. Failing to correct for the impact of inflation forecast errors has left these cuts baked in for subsequent years.

- The income thresholds that determine eligibility for maintenance loans have been frozen in cash terms for many years despite substantial growth in households’ nominal earnings. This has meant fewer students have been eligible for the maximum support each year, and loan entitlements have been withdrawn more quickly from students from higher-income households.

As shown in Figure 5, the amount students with equivalent household incomes have been entitled to borrow has declined between 2016/17 (blue) and 2025/26 (green). The largest cuts have been for those with household incomes of around £59,000, who were entitled to borrow £5,300 in 2025/26 – nearly £3,000 (36%) less in real terms than equivalent students would have been able to borrow nine years earlier.

Figure 5. Maintenance loan entitlements per year, by household income

Note: For England-domiciled students living away from home and studying outside London. Entitlements for students starting courses each academic year in CPI real terms (2026Q1 prices). Household residual income thresholds are expressed in 2025–26 financial year prices, and changes over time reflect growth in average earnings between the relevant financial years upon which entitlements are based (e.g. 2023–24 tax year for entitlements in the 2025/26 academic year). 2029/30 schedule assumes maximum entitlements are increased in line with consumer prices and income thresholds are frozen in cash terms. (In practice, we would expect government to increase entitlements in line with forecasts for RPIX. These are typically higher than forecasts for CPI, although they have not been higher than actual CPI in recent years.)

Source: Authors’ calculations using student finance guides (Student Finance England, 2016; Student Loans Company, 2025) and Office for Budget Responsibility’s Economic and Fiscal Outlook, March 2025.

Whereas the government plans to increase the maximum maintenance loan each year in line with inflation, it has not indicated that it plans to apply any indexation to these income thresholds. If they remain frozen in cash terms then we can expect further declines in the generosity of maintenance support in the coming years. By 2029/30, we estimate that some students may be able to borrow over £1,000 (around 15%) less in real terms than they would be entitled to this academic year. If the government deems that the living support available to students in 2025/26 is at the appropriate level, it should also increase the income thresholds, for instance by indexing them with average nominal earnings growth.

Reintroducing maintenance grants

Until 2015/16, undergraduate students from low-income households were entitled to maintenance grants, which did not need to be repaid. For the last decade – since these grants were abolished for new students from 2016/17 – living-cost support for England-domiciled students has been provided entirely in the form of loans.6 The latest official forecasts suggest that more than half of current students can be expected to repay these loans in full (Department for Education, 2025b).

In a speech at the Labour Party Conference in September, Education Secretary Bridget Phillipson announced that the government would introduce new, targeted maintenance grants. The post-16 White Paper made the more specific commitment to introduce ‘targeted means-tested maintenance grants by the end of this Parliament, to help students from the lowest income households who are studying courses that support our missions and Industrial Strategy’. More detail on the grants will be set out at the Autumn Budget, but this commitment suggests that the new grants will be targeted in two ways.

The first is that – unlike the grants that existed up to 2015/16 – the new grants will only be available to those studying on priority courses, specifically those studying subjects that ‘address priority skills gaps and align with the government’s Industrial Strategy’. We estimate that around 390,000 full-time England-domiciled undergraduates were enrolled on courses in these priority subjects in 2023–24, accounting for around 30% of all such students.7 As shown in Figure 6, this included 77,000 students on nursing and midwifery courses, 73,000 studying computing and 64,000 studying engineering and technology. Amongst those not studying in ‘priority subjects’, by far the largest number were studying business and management (242,000), followed by design, and creative and performing arts (106,000).

Figure 6. Number of full-time England-domiciled undergraduates enrolled in priority and non-priority subjects in 2023/24

Note: Figures include all UK providers, and are full-person equivalents, reflecting the proportion of each student’s course that related to each subject. Subject groups that will be eligible for LLE-funded modules, mapped onto closest subject at CAH level 1 except for economics (CAH 15-02), health and social care (CAH 15-04), nursing and midwifery (CAH 02-06), allied health (CAH 02-06), physics (CAH 07-01) and chemistry (CAH 07-02). Architecture, building and planning excludes landscape design (CAH 13-01-03). Other includes agriculture, veterinary sciences, combined and general studies, and landscape design.

Source: Authors’ analysis of HESA students (DT051 Table 52) and Department for Education (2025c).

The second main eligibility criterion will be means-testing, with the new grants only set to benefit ‘students from the lowest income households’. We expect that students’ eligibility is likely to be assessed based on the same measure of ‘household residual income’ (HHRI) that is used to assess entitlements to maintenance loans currently.8 However, this means-testing could still be applied in many different ways. Some of the many options for how this could be done – alongside retaining some maintenance loan entitlements for low-income students – are illustrated in Figure 7.

Figure 7. Potential options for means-testing of new maintenance grants

Note: Illustrations of potential options for means-testing new grants. Value of grant and loan entitlements are shown on the vertical axis, and depend on household income, which is shown on the horizontal axis.

One important choice will be whether all eligible students will be entitled to the same amount of grant (as in Panel A of Figure 7), or whether the amount of the grant will also be means-tested, with entitlements tapered away smoothly as household income increases (Panels B, C and D). In Scotland, where low-income students are still entitled to non-repayable grants of up to £2,000, there are sharp cliff-edges such that the total amount of support a student is entitled to falls by £1,500 if their household income goes from £33,999 to £34,000, for instance. In contrast, as described above, current maintenance loan entitlements for England-domiciled students are tapered away smoothly with HHRI. A single headline amount of grant that is received by all eligible students may be easier for government to communicate to prospective students, but introducing cliff-edges would worsen the design of the English student support system. It would see students in almost-identical circumstances awarded different levels of support, and risks disincentivising some households close to the income threshold from work as they could lose out on a substantial amount of support if their earnings increased just slightly.

Another policy choice will be whether any awards of maintenance grant would be in addition to students’ existing loan entitlements (as in Panels A and C of Figure 7) or would be offset by a reduction in the amount of loan students would be entitled to. If this offsetting were 1:1 (as in Panel B) then there would be no increase in the total amount of living-cost support provided to low-income students when grants were introduced. In England until 2015/16, a student’s maintenance loan entitlements were reduced by 50p for every £1 of maintenance grant they received (Panel D).

The optimal design for the new grant will depend on the government’s policy aims. These were not specified in the White Paper, but are likely to be some combination of:

- providing additional living-cost support for disadvantaged students, to increase their standard of living in the short run and increase their ability to participate and succeed in higher education (e.g. through supporting them to undertake fewer hours of paid work);

- reducing student loan borrowing amongst low-income students, either by reducing how much they are entitled to borrow or as a by-product if those receiving a grant opted to take up less of their loan entitlement; and

- encouraging more students to study courses in priority subjects, who would otherwise have studied a different (non-priority) course or not have participated in higher education.

At the margin, the introduction of maintenance grants could well induce some individuals to enter higher education who might not otherwise have done, although there is mixed evidence in the academic literature on the effectiveness of financial incentives in influencing students’ participation decisions. For prospective students facing liquidity constraints, the total amount of up-front support available to them is likely to have more impact than whether it is provided in the form of grant or loan. There may still be some positive impact on participation even if the grants were offset 1:1 by a reduction in loan entitlements, if prospective students anticipate the impact of lower loan borrowing on their eventual loan repayments or they are sufficiently debt-averse.

There is little directly relevant evidence on the extent to which a targeted grant may influence students’ subject choices. Evans (2017) found that financial incentives were not effective in persuading low-income students in the US to major in STEM fields, and English students have typically decided which subject to specialise in at an earlier stage. Any grant is likely to be more impactful if students are aware of the conditions under which they would be eligible for it, and if this awareness comes early enough to shape their choices of GCSE and A level subjects. There is some evidence that once they have started a course, providing low-income students with bursaries may have a positive effect on continuation, course scores and final degree classification, with high-ability students likely to benefit the most (Murphy and Wyness, 2023).

How many students might be eligible for the new grants?

To understand how many students might be eligible for the new grants under different potential policies, we can look at the share of low-income students who are enrolled on undergraduate courses in priority subjects currently. This gives a sense of how many students might have received the grants if they had been available in the 2023/24 academic year, although it will underestimate take-up if the grants are effective in inducing more potentially eligible students to study these courses.

As shown in Figure 8, the share of students studying priority subjects did vary slightly with household income in 2023/24. The proportion of undergraduates studying priority subjects varied from 26% amongst those reporting zero household income, to 30% amongst those with household income between £1 and £25,000, up to 32% amongst those not responding (who have not applied for income-dependent financial support – typically suggesting they have a high enough income that they knew they would only be entitled to the minimum loan).9 Of the priority subjects, those with the lowest household incomes are more likely to study nursing and midwifery, and allied health, but are notably less likely to study engineering, maths, chemistry and physics. The starkest difference in subject choices across these groups is that students from low-income households are much more likely to study business and management – which is not a priority subject – than better-off students.

Figure 8. Estimated share of full-time undergraduate students enrolled in priority and non-priority subjects, by household residual income, in 2023/24

Note: Includes England-, Wales- and Northern-Ireland-domiciled full-time undergraduate students enrolled at UK higher education providers in 2023/24. Where CAH level 1 subject areas include both priority and non-priority subjects, assumes shares who are enrolled across priority and non-priority are the same across household income and match those amongst England-domiciled students only. Economics and health and social care are both from ‘social sciences’. Percentages are of full-person equivalents.

Source: Authors’ analysis of Office for Students (2025c).

One way to target students from low-income households would be to provide the new grants only to those with a household income of between zero and £25,000 – the group of students who are currently eligible for the maximum maintenance loan. In total, we estimate that of England-domiciled undergraduate students who were awarded any form of student support in 2023/24, around 40% (440,000) would be classified as ‘low-income’ on this measure. Of these students, around 124,000 were also studying priority subjects – 28% of all such ‘low-income’ students, and around 10% of all English undergraduate students.10

The government has not yet indicated how large the new maintenance grants will be. To give some sense of potential spending, awarding a grant worth £4,000 per year to all students on priority courses with household incomes below £25,000 would have implied spending around £500 million on maintenance grants in 2023/24. If such a grant were provided in addition to existing maintenance loan entitlements (as in Panel A of Figure 7), it would have increased the total support provided to low-income students by 40%.11

In a government press release in September, the policy was framed as the reintroduction of the grants abolished in 2016, but in a targeted, means-tested format (Department for Education, 2025d). As described in Box 2, these grants were available to low-income England-domiciled students up to 2015/16, with students higher up the income distribution awarded partial grants and, crucially, no restriction on eligibility to those studying specific subjects. A total of £1.6 billion was spent on maintenance grants in 2015/16, with more than half of England-domiciled undergraduates (and 57% of those eligible for any living-cost support) awarded at least some maintenance grant and 40% receiving the full award of £3,387 (equivalent to £4,487 in today’s prices). Reflecting inflation and growth in the number of students, operating a similarly generous system might have required spending around £2.6 billion on maintenance grants in 2023/24.12 Roughly matching the per-student generosity of the grants awarded in 2015/16, but restricting them to those studying priority subjects, might have cost around £750 million in 2023/24. This is equivalent to around 7.5% of total international student fee income in the same year.

Box 2. How did maintenance grants work before they were abolished in 2016/17?

In 2015/16, new students from families with annual incomes of £25,000 or less were entitled to the maximum maintenance grant of £3,387, while students with household incomes up to £42,620 received a partial maintenance loan. Students’ maintenance loan entitlements were reduced by 50p for every £1 of maintenance grant they received, as shown in Figure 9. Some students – including those eligible for some disability-related benefits or with caring responsibilities – were instead eligible for a special support grant. This was also worth £3,387 but did not reduce students’ maintenance loan entitlements.

Figure 9. Entitlements to maintenance support for students starting undergraduate courses, by household residual income, in 2015/16 and 2016/17

Note: Entitlements and household incomes expressed in cash terms in the relevant years.

Of full-time England-domiciled students awarded student finance in 2015/16, 43% (413,000) received a full award of maintenance grant or special support grant, with £1.4 billion spent on these full awards. A further 14% (136,000) received a partial award, accounting for a further £240 million of spending. This means that 53% of all full-time England-domiciled undergraduate students (57% of those who were awarded any form of student support) received at least some maintenance grant.

When maintenance grants were abolished for new students in 2016/17, the total amount better-off students were entitled to borrow was increased with inflation, but loan entitlements for poorer students were increased by around 10% in cash terms. This meant students who were no longer entitled to maintenance grants nonetheless saw an increase in total up-front support.

Note: Number and value of awards are from table 3A of Student Loans Company (2016) and include the special

support grant

5. Levies in the post-16 education and skills system

Levies have long been used as a tool within skills policy to facilitate investment in skills. A levy is a charge used to raise funds for a defined purpose, such as education and training. In skills policy, levies are typically hypothecated, meaning the revenue is reserved for training rather than being absorbed into general government spending. They are used both to create a stable funding stream and to address underinvestment. The UK has a long history with skills levies, dating back to the Industrial Training Act 1964, which required employers in many sectors to pay compulsory levies to support industry-wide training. The White Paper discusses two skills levies – the apprenticeship levy and the proposed international student levy – which similarly aim to raise dedicated resources while shaping behaviour within the post-16 education and skills system (although it is not clear that the international student levy will, or should, be truly ‘hypothecated’).

This section examines the White Paper’s proposals to reshape the apprenticeship levy into a growth and skills levy, and considers the implication of introducing an international student levy for universities and the wider post-16 skills system.

Reforming the apprenticeship levy

The apprenticeship levy has been a central feature of England’s skills system since its introduction in 2017. Large employers – those with annual pay bills above £3 million – pay a tax of 0.5% on their pay bill above this threshold. In England, the funds from this levy can be used by all employers (both those that pay the levy and those that do not) to subsidise the training and assessment costs of apprentices. Any unspent levy revenues are rolled into the government’s wider budget, while any excess demand for apprenticeships (over and above levy revenues) is paid for out of general revenues.

Despite the name, the apprenticeship levy is not really a hypothecated tax, where the revenue collected goes directly into a separate funded dedicated solely to apprenticeships. Instead, the Treasury sets an apprenticeship budget in England. While the revenue from the levy is an important factor in setting the apprenticeship budget, other considerations such as broader policy objectives can also play a part. The devolved governments of Scotland, Wales and Northern Ireland receive a corresponding amount via the Barnett formula. The level of allocated funding can be, and has been, different from the amount of money raised through the apprenticeship levy.

Figure 10 shows the revenue generated by the apprenticeship levy, the funds allocated to England’s apprenticeship budget and the amount allocated to devolved nations, as well as the actual expenditure from England’s apprenticeship budget.

Figure 10. Funds raised by, allocated to and spent from the apprenticeship levy

Source: Funds raised by the levy from the Office for Budget Responsibility’s ‘Economic and fiscal outlook – supplementary fiscal tables: receipts and other’. Funds spent in England and apprenticeship budget in England from Freedom of Information request. Funds allocated to devolved nations between 2017–18 and 2019–20 from HM Treasury (2016) and calculated using Barnett formula for remaining years.

In the early years of the apprenticeship levy, the amount raised was broadly in line with the funding allocated for apprenticeships (the sum of the apprenticeship budget in England and transfers to the devolved nations). Since 2021–22, however, levy receipts have consistently exceeded allocations, with the surplus rising from around £345 million in 2021–22 to almost £840 million in 2024–25. In total, the levy has generated around £2.2 billion more (in today’s prices) than has been allocated across the UK since its introduction in 2017. It is also important to distinguish between the apprenticeship budget in England and actual expenditure. The apprenticeship budget sets out what government has allocated to fund apprenticeships, but spending depends on employers’ demand for apprenticeships. In the first four years of the levy, only around 75–80% of the budget was actually spent each year; this gap has narrowed more recently, with a small overspend in the latest year.

The basic structure of the levy has remained unchanged since 2017, but successive governments have made incremental adjustments, and suggestions have been raised about whether the system should allow employers to subsidise a broader set of training options (Tahir, 2023). Prior to the election, the Labour Party set out proposals to broaden the levy into a growth and skills levy, enabling employers to use up to 50% of their contributions to fund approved non-apprenticeship training (Farquharson et al., 2024). The intention was to address underinvestment in training that is not currently eligible for support. But widening the scope of subsidised training also brings challenges, including the risk of deadweight – funding activity that would have taken place anyway – and the need for quality assurance across a more diverse set of courses.

Since taking office, the government has begun to make changes to the levy system, though the steps taken up until now have focused on controlling costs rather than widening flexibility. Shortly after the election, the Department for Education announced that levy funds could no longer be used to support Level 7 apprenticeships for adults aged 22 and over.13 This change reflects mounting pressure on the apprenticeship budget. Figure 11 shows that spending on higher-level apprenticeships (Level 4+) has risen from 13% of total spending in 2017–18 to 39% in 2021–22, and Level 7 programmes alone increased from 1% to 10% over the same period. These apprenticeships are predominantly taken up by adults who already hold degrees, with 74% of higher-level starts in 2024/25 by individuals aged 25 and over. This shift has placed growing strain on the apprenticeship budget and helps explain why the government has sought to restrict the use of the budget for higher-level apprenticeships.

Figure 11. Share of apprenticeship budget spent in England on each apprenticeship level

Source: Freedom of Information request.

There is now some indication of how the apprenticeship levy is intended to evolve into a growth and skills levy. The White Paper confirms that, from April 2026, employers will ‘be able to use the levy on short, flexible training courses’. These courses will take the form of ‘apprenticeship units’ and will be available in a set of designated critical skills areas.

What this approach means in practice is still uncertain. It is not clear what ‘apprenticeship units’ will look like. In addition, by restricting eligibility to courses in critical skills areas, the government appears to be adopting a narrower model than the broader flexibility proposed before the election. There are sound reasons for targeting subsidy towards regulated, high-quality provision in areas of clear labour market need. But many employers also invest in training that falls outside these categories, and limiting eligible courses may reduce the extent to which the levy supports wider workforce development. The challenge for the government will be to strike a balance between expanding flexibility, managing costs and ensuring that public funds support training with genuine economic value.

A new levy on international students

The government first proposed a new levy on international student fees in a White Paper on the immigration system published in May 2025 (Home Office, 2025b). In a speech at the Labour Party Conference in September (Department for Education, 2025d), Education Secretary Bridget Phillipson confirmed the new levy would be used to ‘pay for’ the reintroduction of maintenance grants for some domestic students – a claim reiterated in the recent post-16 White Paper. The government has promised further details on the levy itself at the Autumn Budget.

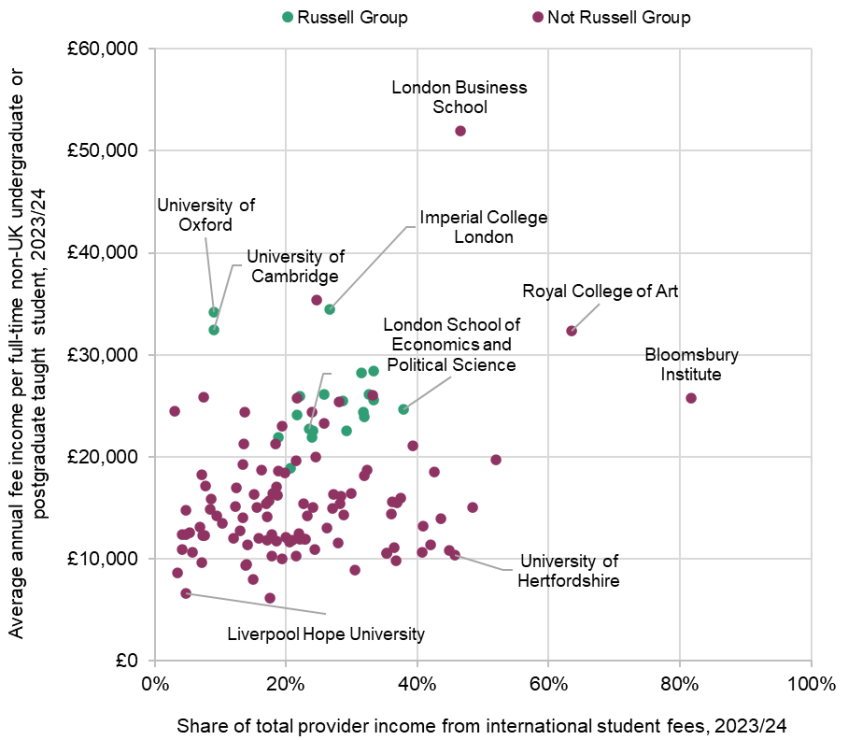

The context for this proposal is a substantial increase in income from tuition fees paid by international students, which were worth £10 billion across England in 2023/24, accounting for 22% of all higher education providers’ income, up from 17% in 2017/18. International students are not subject to the same tuition fee cap as domestic students and typically face much higher fees. Across universities in England, average tuition fee income per full-time international student per year was around £19,000 in 2023/24, but this ranged from more than £30,000 at some of the most prestigious universities (Imperial College London and the Universities of Oxford and Cambridge) to less than £10,000 at York St John University, Edge Hill University and Liverpool Hope University, for example. As shown in Figure 12, Russell Group universities are over-represented amongst those with the highest per-student fee income.

Figure 12. Average fee income per full-time international student per year, and international fee income as a share of total provider income, 2023/24

Note: Includes England Approved (fee cap) providers for which both finances and student data were available, which had at least 100 students enrolled, of whom at least 50 were full-time non-UK students on undergraduate or postgraduate taught courses. Excludes University of Suffolk as implied fee income per student was implausibly low. International student fee income as a share of total provider income includes all tuition fees paid by non-UK students at any level or mode of study. Average fee income per student is restricted to undergraduate and postgraduate taught (including PGCE) students.

Source: Authors’ analysis of HESA finances DT031 Table 6 and DT031 Table 7, HESA students DT051 Table 1 and HESA provider metadata.

The extent to which universities recruit internationally also varies substantially, with international students making up around a quarter of all enrolled students across the sector in 2023/24, but more than half of students enrolled at Imperial College London, UCL and the University of Hertfordshire, for instance, and closer to two-thirds (64%) at LSE. Together these patterns mean that income from international fee income is very unevenly distributed across providers.

As well as additional income, recruiting additional students also means higher expenditure for providers. Sector estimates submitted to the Office for Students (2025d) suggest that non-publicly funded teaching (mainly of international students) on average costs universities around 70% of the income they receive for this teaching. There are good reasons to be cautious in interpreting these estimates. In particular, if providers have spare capacity that they fill with international students, average cost figures will substantially overstate the true costs of taking on these additional students. However, based on the simplifying assumption that each £1 of income from international student fees translated into a 30p increase in university surpluses in every academic year, we estimate that if international fee income had not risen, there may have been an aggregate sector deficit of 1.4% of income in 2023/24, instead of a small surplus.14

While government has said little about the potential design of the new levy, illustrative modelling in the immigration White Paper was for a 6% levy on the tuition fees paid by all international students, including undergraduates and postgraduates. If such a levy had been in place in 2023/24 (the latest year for which HESA data are available), and if there had been no change in the number of international students as a result of the levy, it might have been expected to raise around £600 million.15 Recent reports suggest that the government may instead be considering imposing the levy as a flat fee of £1,000 per student.16 Again assuming no behavioural response, such a levy might have been expected to raise a very similar amount across the sector in 2023/24 (£615 million). Given wide variation in fee income per student, a 6% levy would raise much more on average from Russell Group universities (£1,550 per year, and more than £2,000 at Imperial College London and the University of Oxford) than a flat fee of £1,000, and much less – only £550 on average – from students at the 10 universities with the lowest fee income per student.

What impact might an international student levy have and how much might it raise?

In practice, the impact of such an international student levy on universities’ recruitment and finances, and the revenue raised, depends on the extent to which such a levy affected the demand and supply of international student places. Economic theory suggests it would be likely to lead to both an increase in the levy-inclusive tuition fee (price) charged to international students, and to a fall in numbers (quantity), relative to a counterfactual in which no such levy was introduced. The more responsive international students’ demand is to the fees they pay (more price-elastic demand) or the more responsive universities’ supply of places is to the fee income they receive (more price-elastic supply), the larger the likely fall in the number of students as a result of a levy. It is this impact on the quantity of students which will be most important for determining the revenues raised by a levy.17 The more price-elastic is demand relative to supply, the smaller the rise in post-levy fees. It is this which will determine the incidence of the levy: whether it is ‘paid’ by international students or reduces universities’ income from any international students they do recruit.

There is limited evidence on the price sensitivity of international students considering study in the UK, particularly as their composition (country of origin and level of study) has changed markedly in recent years. This makes it difficult to estimate potential responses based on past changes in fee levels. There is even less evidence on how universities set fee levels and determine how many international students to recruit. One estimate used in modelling for the immigration White Paper suggests that a 1% increase in the level of tuition fees charged to EU students may be associated with a decrease of 0.26% in student numbers in the short run (Conlon et al., 2021). Another more recent estimate suggests student numbers are more elastic, with a 1% increase in fees associated with a 0.57% fall in non-EU student numbers (Public First, 2025). There is clearly still a lot of uncertainty, and the true value may end up being higher or lower than either of these. However, based on these estimates, a 6% levy on international student fees might be expected to lead to 1.6% or 3.4% fewer international students studying at English universities. For context, this would have been equivalent to having 9,600 or 21,000 fewer non-UK students in 2023/24.18 Compared with potential revenues of £600 million in the absence of any behavioural responses, such declines would reduce revenues from the levy by similar amounts (£10 million and £20 million respectively) each year.19

These estimates – of the elasticity of student numbers with respect to prices – do not provide direct evidence as to where the incidence of any potential levy would fall. If universities absorbed the full cost of the levy, those international students who did enrol would face the same fees post-levy and be no worse off financially. The entirety of revenues from the levy (£600 million) would come from a decline in universities’ surplus. At the opposite extreme where the fees universities charged students increased by the full amount of the levy, the impact on universities’ finances would be through the decline in student numbers, i.e. through the loss of fee income from any students who did not enrol. Falls in student numbers of the magnitudes described above would have implied losses of £160–340 million in fee income in 2023/24. The impact of this on universities’ surplus would depend on the extent to which they would also face lower costs as a result of needing to teach fewer international students. If these students were as costly to teach as the average across non-publicly funded teaching activity, these falls may have amounted to a loss of surplus of £50–100 million across the sector. If the cost of teaching these marginal students was much lower, the lost surplus would be consequently greater. The decline in universities’ surplus would only equal the value of the lost fee income if it were not possible for universities to make any cost savings – which may be more plausible in the very short term.

In practice, we would expect the impact of the levy to be somewhere between these two extremes, with universities likely to increase their fees by less than the full 6% on average, passing some of the cost on to international students and absorbing some of the cost themselves. Given differences in existing fee levels – and evidence that the price elasticity of student numbers varies between students from EU and non-EU countries, and between undergraduate and postgraduate students – we would expect the impacts of any levy to be very different across providers and across different types of international student.

Why introduce an international student levy?

The government has not yet set out any strong economic rationale for the introduction of an international student levy. Providing education to international students counts as one of the UK’s export activities, and any lost fee income from prospective international students deterred from studying in the UK would amount to a reduction in UK exports. While taxes on imports (tariffs) are fairly common, it is unusual for a country to tax its own exports.20

If the government’s aim is to reduce the overall number of international students, a levy on international student fees would be one way to achieve this. Another option would be to ration the number of student places through quotas (rather than prices) – for example, by restricting the number of student visas. This would not raise revenues, but would give the government more certainty as to the size of the quantity reduction achieved. It may also allow government to target particular types of international students or providers. A further alternative would be to restrict the number of student visas but to auction them off (a ‘cap and trade’ system). This would both raise revenues and give the government certainty about the number of international students.

In both the immigration and post-16 White Papers, the government recognises the contribution that international students make to the UK, suggesting that reducing overall student numbers is not government’s primary aim with this policy. There may well be positive externalities from recruiting more international students: they may make universities more diverse and vibrant, increase rates of innovation of technological transfer or increase the UK’s soft power, for instance. There may be positive fiscal externalities from having more international students, if they spend foreign earnings on goods and services other than tuition, which may be taxable. This would be offset by any demands placed on public services, although we might expect these to be fairly limited given the age profile of students.21