Downloads

Download the report as a PDF

PDF | 1.51 MB

The Chancellor, Rachel Reeves, is likely to raise taxes in the upcoming Budget. In the spring, she decided to meet her borrowing rule by just £10 billion. The subsequent dilution of planned reductions to the generosity of disability benefits, and the partial reversal of recent cuts to pensioners’ winter fuel payments, will reduce this slender margin. A downgrade to the Office for Budget Responsibility’s economic forecasts could easily eliminate it. If that happens, the Chancellor will face three options: borrow more in breach of her fiscal rules, reduce spending or increase taxation. The first of those options seems unlikely: the Chancellor has (understandably and repeatedly) stated that she will not loosen the fiscal rules. As for spending reductions, unpicking detailed departmental spending plans up to 2028–29 set out in June’s Spending Review seems unlikely. Pencilling in cuts to total spending in 2029–30 (the year in which her fiscal rules bind) in order to meet the letter of her targets would be possible but would stretch credulity to breaking point. Cutting benefits has proven to be difficult politically. There is, therefore, a widespread expectation that tax rises will be the key feature of the Budget. For that reason, this chapter sets out the options for tax increases, but such increases are not inevitable. Any changes to tax policy should be done in a way that, ideally, improves the design of the tax system and that, at a minimum, does not worsen it.

Key findings

- Tax revenue as a share of national income is set to reach a UK record high of 37.4% in 2026–27. This is still lower than in many other Western European countries. It would be feasible for the Chancellor to raise more tax revenue if desired.

- Raising the rates of income tax, National Insurance contributions (NICs) or VAT – the three largest taxes – could straightforwardly raise large sums, but break Labour’s manifesto promise not to ‘increase National Insurance, the basic, higher, or additional rates of Income Tax, or VAT’. Extending the ongoing freeze in personal tax thresholds would also raise a significant amount but (if it included a freeze to NICs thresholds) would also break the manifesto pledge and would leave real-terms tax thresholds – and the size of the tax rise – to be determined by the vagaries of future inflation.

- A new tax on income, hypothecated to a particular spending stream, may be a more politically attractive way to increase tax on a large tax base, but would add unnecessary complexity to the tax system. Hypothecation would either be unjustifiably restrictive (such that spending on a particular item was tied to a specific revenue stream) or economically meaningless (in the sense that the amount raised from the tax bore no direct relation to the amount spent on an area).

- Restricting income tax relief on pension contributions would raise large sums but should be avoided. It would be unfair and distortionary to restrict up-front relief but continue to tax pension income at the taxpayer’s marginal rate. It would also be practically very difficult to attribute employer contributions to defined benefit arrangements to specific individuals so that they could be taxed. There are better options for increasing tax on pensions, including levying some NICs on employer pension contributions and/or reforming the 25% tax-free element of pension income.

- Labour’s pledge not to raise the biggest three taxes, if adhered to, seriously constrains options. Raising significantly more revenue from the next four largest taxes – corporation tax, council tax, business rates and fuel duties – would also bring challenges.

- The government has ruled out increasing the main or small profits rates of corporation tax or reducing the main corporation tax reliefs. It has previously stated its intention to shift some business rates from small retail properties to large properties, in the context of the Labour party manifesto’s intention to ‘raise the same revenue but in a fairer way’. Making tweaks to the current system rather than moving to a land value tax for commercial property is a missed opportunity.

- Council tax rates are already assumed to rise by 4.3% per year for the rest of the parliament; larger increases would be needed to bring in additional revenue. An alternative to raising all rates further would be to increase rates on homes in higher value bands. This would make council tax less regressive. But because council tax bands in England and Scotland are still based on 1991 valuations, the increases would not accurately target the properties that are most valuable today. A sensible goal would be to move to a tax that is proportional to up-to-date property valuations.

- Current forecasts assume that rates of fuel duties (which are lower in cash terms than they were in 2009) will in future keep pace with RPI inflation and that the current ‘temporary’ 5p per litre cut will come to an end – a combined cash increase of more than 20% by 2029–30 on current forecasts. Anything less than that would lose the government revenue relative to current forecasts.

- Higher tax rates on income from capital – including rental income, dividends, interest and self-employment profits – could raise money. So too could removing capital gains forgiveness at death. But simply raising rates would discourage saving and investment. The case for genuine reform is clear: improving the design of the tax base (entailing some giveaways) and then more closely aligning overall tax rates across different forms of income and gains would produce a fairer and more growth-friendly system.

- We caution against introducing an annual wealth tax, which would face huge practical challenges. It would also penalise saving and, the more it was concentrated on the very wealthy, the more it would incentivise them to leave (or not come to) the UK. It would not be a well-targeted way to tax the large returns that wealth can generate and, as such, would be no substitute for well-functioning taxes on capital income and gains. If the Chancellor wants to raise more from the better-off, a better approach would be to fix existing wealth-related taxes.

- The Chancellor should not increase stamp duties (because they lead to asset misallocation and lower labour mobility, dragging on growth in the process) or insurance premium tax (which creates damaging distortions to production decisions that weigh on productivity).

- The overall tax gap (between taxes owed and revenues collected) has fallen, but the tax gap for small companies has ballooned; reducing it should be a priority. The approach should include compliance activities and improving policy design.

- It would be difficult, but not impossible, for the Chancellor to raise tens of billions of pounds more revenue without breaking Labour’s manifesto promise not to increase National Insurance, the basic, higher or additional rates of income tax, or VAT. Just because large sums could be raised elsewhere does not mean it would be sensible. Many of the tax-raising options outside the ‘big three’ would have particularly damaging effects on growth and welfare.

- However much revenue she seeks to raise overall, the Chancellor could create a fairer, simpler, more growth-friendly tax system. That means grasping the nettle and pursuing genuine tax reform (property and capital taxes would both be good places to start). At a minimum, the Chancellor should avoid measures that worsen the design of the tax system.

4.1 Introduction

UK tax revenues have risen substantially in recent years and are forecast to reach an all-time high of 37.4% of national income next year. Even so, if the Chancellor wants to raise more revenue from taxes, that would be possible – as evidenced by the many Western European countries that raise substantially more tax relative to the size of their economies than the UK does.

The tools available to a tax-raising Chancellor are many and varied. This chapter lays out the main levers for raising revenue – which are summarised in Table 4.1 at the end – and discusses the key features of different options. We consider the taxes that the Chancellor can control and, for those taxes that are devolved, account for the effects of adjustments to devolved government finances. A theme throughout is that the poor design of the tax system makes tax rises more damaging than they need to be. However much revenue the Chancellor wishes to raise, we urge her to take steps towards a fairer and more growth-friendly tax system.

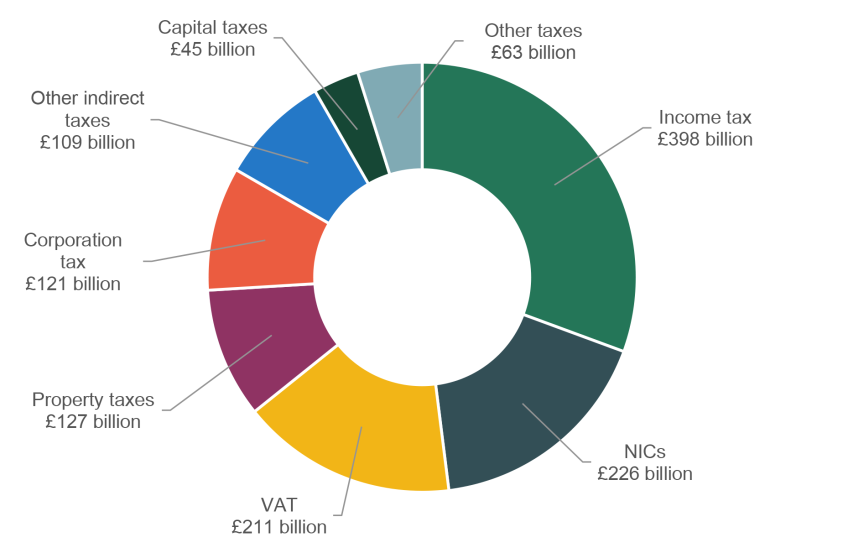

The most straightforward way to raise large sums of revenue would be to increase the main rates of income tax, National Insurance contributions (NICs) or value added tax (VAT). This should not be surprising. These are by far the three largest taxes – together accounting for two-thirds of total tax revenue (see Figure 4.1) – because they are levied on large tax bases. It is well known, however, that Ms Reeves’s ability to raise these taxes will be seriously hampered by Labour’s (self-imposed) political constraints. The party’s 2024 manifesto states that ‘Labour will not increase taxes on working people, which is why we will not increase National Insurance, the basic, higher, or additional rates of Income Tax, or VAT’.

Figure 4.1 Forecast composition of UK tax revenue (2029–30)

Note: Taxes sum to total national account taxes. Figure for VAT excludes receipts refunded to public bodies. These refunds (which are still classed by the Office for National Statistics as taxation) are included in the ‘other taxes’ category. Figure for property taxes includes business rates, council tax and stamp duty land tax (and its devolved equivalents). Corporation tax includes receipts from the bank surcharge, energy profits levy and petroleum revenue tax. ‘Other indirect taxes’ includes fuel duties, tobacco duties, alcohol duties, air passenger duty, insurance premium tax, the climate change levy, vehicle excise duties, environmental levies (including the emissions trading scheme), customs duties, betting and gaming taxes, the landfill tax, the aggregates levy, the soft drinks industry levy, the plastic packaging tax, vaping tax, the residential property developer tax and the carbon border adjustment mechanism. Figure for capital taxes includes capital gains tax, inheritance tax and stamp duties on shares. Northern Ireland business and domestic rates are included in the ‘other taxes’ category.

Source: Table A.5 of Office for Budget Responsibility (2025).

What is perhaps less well known is that Ms Reeves also faces significant constraints if she wants to raise money from any of the next four largest taxes – corporation tax, council tax, business rates and fuel duties. She has made pledges that rule out raising the main corporation tax rate and has signalled an intent to make revenue-neutral reforms to business rates. Council tax and fuel duties are already assumed to rise significantly across the parliament, meaning that even greater increases would be needed to improve the public finances.

This is not to say that the Chancellor cannot raise significant sums without raising the ‘big three’ taxes. As an illustration (but not a recommendation), she could raise £20 billion if she: introduced a new council tax surcharge that acted to double council tax rates on band G and H properties (£4.4 billion); abolished the residence nil-rate band within inheritance tax (£6 billion); increased the bank surcharge to 6% (£1.2 billion); ended forgiveness of capital gains tax at death (£2.3 billion); abolished business asset disposal relief (£0.9 billion); and reduced the small companies tax gap by £5 billion. But if the Chancellor wants to raise large sums – and wants to do so without having to raise many smaller taxes – she will likely need to turn to a tax on a large base and therefore break, at least in spirit, her previous pledges.

Despite the focus on whether the Chancellor will break one of her tax pledges, and more broadly on how she will navigate the politics of tax rises, it should be remembered that there are other important issues to consider when changing tax policy. We highlight two.

The first is the effects of tax on outcomes other than revenue.

People commonly ask how much revenue a tax can raise. We should also always ask what the cost of the tax rise is. Almost any increase in tax will create disincentives. Depending on the specific tax rise in question, these will include some combination of disincentives to work, to save or invest, to move house, to spend money on one thing rather than another, or to live, work or invest in the UK (rather than abroad). The list of potential disincentives could go on.

While some taxes – such as those on pollution – are explicitly aimed at changing behaviour, most taxes influence people’s behaviour in unhelpful ways and all reduce the welfare of those who bear their economic burden. As a result of poor tax design, almost all of our taxes create more distortions than are necessary given any reasonable set of policy goals. Conversely, by improving tax design, we could achieve our social and economic objectives with fewer welfare-reducing side effects. Said more plainly: for a given level of revenue, and a given set of preferences over redistribution, taxes could be raised in ways that do less to reduce economic growth and well-being.

Precisely what good design looks like varies from tax to tax. Nevertheless there are some rules of thumb that can offer useful guidance (discussed in detail in Mirrlees et al. (2011)). In general – and unless there are good reasons to deviate from this – the tax system should treat similar activities in similar ways. Not doing this usually creates unfairness and inefficiency as people make decisions based not purely on what is the most productive activity, or what makes them happiest, but rather on what reduces their tax bill the most. We will highlight some of the very many ways in which the UK tax system treats similar activities very differently, and in doing so puts a brake on growth. The complexity of the UK’s tax system, and the instability of tax policy, also act to reduce growth. Tax reform – by creating a less distortionary, simpler, more stable system – offers a real prize.

Yet if experience proves any kind of guide, concerns that we will see moves that take us further away from a well-designed system are likely to be well founded. Some of the most damaging taxes we have – notably including stamp duties and insurance premium tax – have (regrettably) been increased multiple times in the recent past.

The second issue to consider when changing taxes is the context in which policy is being made. One important piece of context is the policy measures that have come before. Direct taxes (income tax and National Insurance contributions) are now lower for middle earners than at any time since the mid 1970s. But since around 2010, governments have been increasing taxes at the top of the income distribution (Adam, Miller and Upton, 2024). The result is that the government is increasingly reliant on a relatively small number of taxpayers for a large share of revenue. These individuals tend to be more internationally mobile and responsive to tax changes. Considering incentive effects – including incentives to stay in (or come to) the UK – is important.

The remainder of this chapter proceeds as follows. In Section 4.2, we discuss the ‘big three’ (income tax, NICs and VAT), detailing the various ways in which additional revenues could be raised from these taxes as well as opportunities for reform. In Section 4.3, we briefly discuss corporation tax, including the growing tax gap for small companies. In Section 4.4, we discuss the taxation of wealth and savings, assessing the merits of a new tax on wealth as well as describing opportunities for reforms that would facilitate more efficient revenue-raising from capital incomes. In Section 4.5, we discuss property taxation. In Section 4.6, we discuss indirect taxation outside the VAT system, covering (amongst other things) the taxation of fuel and carbon emissions. Section 4.7 concludes.

4.2 The ‘big three’

The most straightforward course of action for a Chancellor seeking to raise substantial sums is to turn to the UK’s three largest taxes: income tax, National Insurance contributions (NICs) and value added tax (VAT).

Changes to headline rates

Because the bases of these taxes (broadly, people’s income, their earnings and their expenditure) are large, relatively small changes in their rates yield relatively large amounts of revenue:

- Increasing all rates of income tax by 1 percentage point would yield an estimated £10.9 billion a year by 2029–30 – with the bulk of this revenue coming from increasing the basic rate (charged on the portion of a person’s income falling between £12,570 and £50,270 a year).1

- Increasing individual (i.e. employee and self-employed) rates of NICs by 1 percentage point would yield £8.5 billion a year by 2029–30. This is somewhat less than an equivalent increase in income tax, due primarily to the fact that NICs are charged only on earnings (which excludes, for example, rental income, pension income and interest income). A 1 percentage point increase in the rate of employer NICs would yield £6.0 billion if employers passed the increase on in full to employees in the form of lower earnings.

- Increasing the main rate of VAT by 1 percentage point would yield £9.9 billion a year by 2029–30.

Increases in the rates of income tax and NICs would both be progressive: higher-income households would pay more both in absolute terms and as a proportion of their incomes. This is primarily because – for both income tax and individual NICs – individuals’ first £12,570 a year of income is tax-exempt, considerably dampening the impact of rate increases on lower-income households. For the same reason, an increase in employer NICs, from which only the first £5,000 of salary is exempt, would (if fully passed on to employees) be somewhat less progressive than an increase in either income tax or individual NICs.

Contrary to popular belief, increasing VAT would also be slightly progressive. The progressivity of an expenditure tax such as VAT is best measured by looking at VAT payments as a percentage of expenditure, not income;2 items not subject to VAT (such as most food) make up a bigger share of poorer households’ spending, making the tax slightly progressive. Nevertheless, a VAT rise would be – at least with respect to future income – nowhere near as progressive as an income tax or NICs rise, because there is no VAT-free allowance on the first tranche of household expenditure analogous to the allowances in income tax and NICs. On the other hand, increasing VAT, unlike income tax or NICs, effectively imposes a tax on the stock of existing wealth as well as future income, since both will be subject to VAT when they come to be spent.

In all three cases, rate increases would come at the cost of exacerbating economic distortions and would weigh on growth. Higher taxes on earnings (whether through income tax or NICs) would make work less attractive, as would higher rates of VAT: a tax that increases prices reduces the real value of earnings just like a tax on earnings does. Each of the three tax rises would also exacerbate other existing tax-induced economic distortions, in different ways:

- Increasing income tax rates would discourage saving in taxed forms (such as investing in companies or property) and would increase the bias towards putting savings in relatively tax-favoured forms such as private pensions, ISAs and owner-occupied housing.

- Increasing NICs would not have these effects since NICs are not levied on savings income, but for the same reason it would increase the existing incentive to shift the form in which income is taken away from earnings and towards capital income (for example, through setting up a company and taking income as dividends rather than earnings).

- Increasing the main rate of VAT would increase the scale of the distortion towards buying zero- and reduced-rated goods and services instead of standard-rated ones.

Income tax and NICs thresholds

Instead of increasing rates of income tax and NICs, the Chancellor could choose to change the thresholds at which those rates begin to apply.

In general, reducing thresholds is less progressive (and correspondingly weakens work incentives less) than increasing rates, as reducing a threshold takes the same cash amount from everyone above the initial threshold, rather than an amount increasing in proportion to their income above the threshold (at least up to the next threshold). It can still be somewhat progressive over much of the income distribution, for three reasons: (i) people below the new threshold are unaffected; (ii) households with two people above the threshold, who tend to be better off, lose twice over; and (iii) in the case of the tax-free allowances, many of those above the threshold but still with relatively modest incomes will be receiving means-tested benefits and see the reduction in their after-tax income (as a result of the rise in the threshold) offset by an increase in their benefit entitlement. But the cash loss will be a declining share of income for those with the highest incomes.

One well-trodden path to achieving this would be to freeze thresholds in cash terms, leaving inflation to reduce their real level over time and accelerating the process of ‘fiscal drag’, whereby incomes’ growing faster than tax thresholds brings more income into higher tax bands. The thresholds at which the basic and higher rates of income tax begin to apply have already been frozen in cash terms since April 2021 and, under plans inherited from the previous government, will remain so until April 2028. Taken together with a similar freeze to NICs thresholds, that will represent an estimated £51.1 billion a year tax increase by 2029–30, relative to a scenario where thresholds were uprated annually in line with inflation (as is the default).3 Under the Office for Budget Responsibility’s latest inflation forecasts, extending the freeze in all income tax and NICs thresholds for two more years (until April 2030) – a real-terms reduction of 3.9% – would be expected to raise £10.4 billion a year from 2029–30. Note that this would increase NICs, breaking Labour’s manifesto pledge.

Reducing the real value of tax thresholds is a reasonable way to raise revenue. Doing so via a cash freeze, however, is a highly unsatisfactory means of achieving that aim. It abdicates control over the real value of thresholds, leaving it to the vagaries of inflation. The current threshold freeze provides a stark case study. When first announced by then-Chancellor Rishi Sunak at the March 2021 Budget, freezes to income tax thresholds were expected to yield £10.5 billion a year of additional revenue by 2025–26.4 It is now estimated that that figure will in fact be £26.8 billion – a tax rise, in other words, more than twice as large as that originally planned.5 The shape of the tax system should be the result of deliberate, thought-through decisions. If the government thinks the personal allowance, higher-rate threshold and so on should be X% lower in real terms, it should announce that it will reduce real-terms tax thresholds by X% and explain why it thinks that is the appropriate choice. It should not announce a tax rise of an unknown size to be determined by whatever inflation turns out to be in four years’ time.

While reducing the real value of tax thresholds generally increases revenue, an unusual feature of the upper earnings limit (UEL) for employees and upper profits limit (UPL) for the self-employed in NICs is that the marginal tax rate above these thresholds, 2%, is lower than that below the thresholds (8% for employees and 6% for the self-employed). Reducing the UEL/UPL, unlike other thresholds, therefore costs money rather than raising it, since it brings more earnings into being taxed at a lower (2%) rate. Since 2009–10, the UEL and UPL have been aligned with the income tax higher-rate threshold, currently £50,270 a year. Since the gap between income tax rates above and below the threshold (40% versus 20%) is bigger than the gap between NICs rates, reducing the aligned thresholds is still a net revenue-raiser. But one revenue-raising option available to the Chancellor would be to break that alignment and increase the level of the UEL and UPL, or even abolish them entirely.

Abolishing the UEL/UPL would mean charging the main rates of NICs on earnings above the current UEL/UPL as well as below it – essentially a 6 (4) percentage point increase in the employee (self-employed) NICs rate on earnings above £50,270 a year, and (given the similarities between NICs and income tax) somewhat akin to a 6 percentage point increase in the higher and additional rates of income tax. This would raise £14 billion a year by 2029–30 – mostly from the highest-income tenth of households. Behavioural responses would be likely to reduce this yield significantly, however. There is undoubtedly scope to raise substantial additional revenue from the bulk of higher-rate taxpayers. But the combined effective rate of income tax and individual NICs on earnings between £100,000 and £125,140 is already 62% (or 69.5% in Scotland), before accounting for the effects of employer NICs and indirect taxes.6 This substantially weakens incentives for individuals to increase their taxable income in that range, and a higher top rate of NICs would only weaken them further. The very highest earners, meanwhile – perhaps those earning, say, more than twice that much – appear to be highly responsive to taxation, and further increasing the tax rate on those earnings would raise the realistic prospect of actually reducing revenue raised from the highest-income taxpayers. There is enormous uncertainty about the responsiveness of top incomes to tax, however.7 If the Chancellor wanted to go down the route of increasing the UEL/UPL, stopping short of £100,000 might be more prudent than abolishing it altogether.

Individual NICs on pensioners' earnings

Currently, the earnings of those above the state pension age are exempt from employee and self-employed (although not employer) NICs. One possible extension would be to end this exemption, or at least impose some level of individual NICs on pensioners’ earnings. £1.3 billion of NICs revenue is forecast to be forgone as a result of the exemption in 2029–30, although its abolition would raise less than that thanks to behavioural responses. The argument in favour of such a change is fundamentally one of fairness – why should older workers face a lower level of taxation than younger ones? The historical reason for the exemption is that National Insurance was conceived of as a contributory system, with individuals contributing during working life to build up rights to a state pension in retirement (and other benefits at times of need). But in reality there is now barely any connection at all between the amount of NICs paid and the amount of state pension (or indeed any other benefit) received (see Chapter 8 of this Green Budget for further discussion of the dwindling role of contributory benefits in the UK). NICs are essentially just a second income tax, and it is hard to see a principled reason for an age cut-off.

There are practical reasons to be cautious about such a change, however. It is generally easier for workers who are already closer to retirement to change their work decisions in response to additional taxation (for example, by retiring earlier). This means that increasing tax rates for those over the state pension age would be likely to cause a relatively large reduction in work done – eating into the £1.3 billion potential yield. There is a good argument for disincentivising work less for more responsive groups. At a time when the government is seeking to encourage individuals to work longer, to help manage the fiscal pressures of an ageing population, this change would push in the opposite direction.

Broadening the VAT base

The Chancellor could raise significant revenue by broadening the VAT base. By international standards, the UK VAT makes plentiful use of zero-rating. Most food, for example, is zero-rated (representing an estimated £30.6 billion of forgone annual revenue in 2029–30) as are new homes (costing another £19.0 billion) and an array of other goods and services including domestic passenger transport (£6.1 billion), prescription drugs (£4.4 billion) and children’s clothing (£2.6 billion). Internationally, the zero-rating of children’s clothes is unusual (although Ireland follows a similar policy), while the blanket zero-rating of most food also marks the UK out – France, Germany and Italy all charge a reduced (rather than a zero) rate. The UK also applies a reduced (5%) rate to domestic energy (costing £7.8 billion). In total (relative to a world in which VAT were charged at a standard 20% on all consumer sales), the government will lose an estimated £83.1 billion in 2029–30 from zero and reduced rates of VAT.

The government will also forgo a further £45.8 billion as a result of sales that are exempt from VAT. VAT exemptions differ from zero rates in that, while in both cases there is no VAT charged on sales, producers of exempt goods or services (examples of which include financial services, (some) education and healthcare) cannot reclaim any VAT paid on inputs they buy. This makes exemptions particularly economically damaging, because they distort production patterns as firms try to minimise their purchases of taxed inputs.

VAT is, in principle, a well-designed tax, but zero and reduced rates and exemptions make it less so. As noted above, zero- and reduced-rated items are consumed disproportionately by poorer households. But zero and reduced rates are not well-targeted tools for redistribution. Income-related taxes and benefits can be used to fine-tune how much we redistribute from richer to poorer households. It is harder to see why we should redistribute to those who spend more than others with the same total income/expenditure on food or children’s clothes. As the Mirrlees Review noted, ‘we subsidize those who spend large amounts of money on designer clothes for their children but tax those who spend similar amounts on, perhaps rather educational, toys. Those with a taste for music are taxed; those with a taste for magazines are not’ (Mirrlees et al., 2011). That is not only unfair but distorts people’s consumption decisions, making them worse off. What is more, much time, money and human ingenuity are currently wasted on questions such as (to take just one case recently brought before the courts) whether mega marshmallows should be zero-rated (in line with mini-marshmallows) or taxed at the main rate (to match their standard-sized counterparts). One cannot help but wonder whether the time and expertise of those engaged in such disputes might be more productively deployed elsewhere.

A move towards greater uniformity would therefore be welcome. Since richer households typically spend more in cash terms than poorer households on zero- and reduced-rated items, a more uniform VAT would raise more than enough revenue to compensate poorer households on average, though inevitably some households would lose out. And while broadening the VAT base, like increasing the rate, would weaken work incentives (by reducing the real value of earnings), it would be possible to design a package of reforms that would provide the desired compensation without weakening work incentives (Mirrlees et al., 2011, chapter 9). There are benefits to be reaped here, but it is not an ‘easy win’: as elsewhere, to raise significant net revenue, the government would need to accept some losses for poorer households and/or a weakening of work incentives.

A new tax on income?

One means by which past Chancellors have sought to raise revenue while keeping to the letter (if perhaps not the spirit) of their party manifestos has been to create a new tax altogether. In 2015, then-Chancellor George Osborne announced the creation of the apprenticeship levy on big employers’ wage bills – essentially an employer NICs supplement (with little meaningful connection to apprenticeships) – conveniently circumventing a manifesto pledge (made just a few months before) of ‘no increases in VAT, National Insurance contributions or Income Tax’.8 In 2021, meanwhile, then-Chancellor Rishi Sunak announced the introduction of the health and social care levy – more or less a carbon copy of an increase in employee and self-employed NICs9 – after a similar manifesto commitment not to ‘raise the rate of income tax, VAT or National Insurance’.10 The levy was later scrapped under the brief premiership of Liz Truss (although the planned spending on the NHS for which the majority of the revenue was earmarked was left untouched).

Ms Reeves may be tempted to follow a similar course. A new ‘defence and security levy’ or ‘national health charge’ or similar could be a means of, in effect, increasing income tax or NICs rates while still adhering to the precise wording of Labour’s promise on those taxes (though it would, of course, still represent a tax increase on working people). One substantial drawback of such an approach would be its opacity. The UK already has two separate major taxes on income (income tax and NICs), each applying to slightly different (but very much overlapping) tax bases. A new tax on income would make an already overly complex system even harder to understand. Box 4.1 considers broader arguments around hypothecation: the earmarking of revenues from a particular tax (rise) for a specific, identified purpose.

Box 4.1 Hypothecation: ring-fenced revenues for the NHS or defence?

The hypothecation of a tax – sometimes referred to as ring-fencing or earmarking – refers to a situation where the revenue raised from a particular tax (or tax increase) is dedicated to a specific spending stream (or spending increase). From an economic perspective, the idea of hypothecating a tax is problematic for one of two reasons.

If total spending on a particular area is genuinely tied to a specific income stream, it is unjustifiably restrictive. Were the amount spent on the NHS each year linked to the revenues from a dedicated ‘NHS tax’, for example, this would imply that if tax revenues fell in a recession, the NHS budget would need to be cut by a commensurate amount, or the tax rate increased. Neither option is likely to represent good policy. One could imagine some sort of smoothing mechanism, with top-ups from or payments into some kind of fund, but this would introduce additional complexity and weaken the link between the hypothecated tax and the spending it is intended to fund. There is very little to commend such an approach.

Or, if the amount raised from a hypothecated tax does not affect the amount spent on an area, then the hypothecation is effectively meaningless. Take the example of the Health and Social Care Levy announced in 2021 alongside a matching increase in funding for the NHS and social care. The amount raised by the tax bore no relationship to the overall amount spent on health and social care. If the tax raised more or less than expected, there would be no corresponding change in spending. It was not clear whether all future increases would be funded via the new levy – and this would have been impossible to verify in any case, given that funding for health and social care comes out of the general tax pot, along with all other spending programmes. In the end, the Health and Social Care Levy was scrapped – but the NHS budget was not correspondingly reduced, thereby underlining the absence of a meaningful link between the two.a

It is, of course, completely reasonable and desirable for government to convey why it wants to raise taxes. It might want to explain, for example, that tax is being increased in order to increase spending in a specific area. Some polling suggests that tax rises whose revenues are intended for certain public services such as the NHS are more acceptable to the public.b But, crucially, explaining why taxes are increasing need not come with any form of hypothecation – i.e. with either an actual formal link, or the illusion of a link, between particular taxes and particular spending items.

Ultimately, politicians might determine that linking the revenues from a particular new tax to NHS or defence spending in the public’s mind might help to obtain voter consent. But by introducing a new tax to ‘pay for’ something, the government: adds needless complexity to the tax system; could make it more likely that the tax will become the go-to policy measure in future if spending pressures in that area grow (even if it is not the most economically efficient means of raising revenue); and may in fact reduce, rather than aid, transparency by creating a misperception that there is a mechanical link between the amount raised and the amount spent (including the misperception that by paying the tax, voters have ‘paid for’ the entirety of whatever it is labelled as). This kind of hypothecation would be firmly into the world of second- (or third- or fourth-) best policy, and should be avoided.

a. The reforms to the adult social care funding system announced alongside the Health and Social Care Levy were eventually abandoned, but not until July 2024, almost two years after the levy itself was scrapped by then-Chancellor Kwasi Kwarteng in the September 2022 ‘mini-Budget’.

b. See, for example, https://www.survation.com/70-brits-pay-extra-1p-tax-pound-went-nhs/, but note that the polling evidence is not clear-cut (as discussed here, for example: https://taxpolicy.org.uk/2024/03/17/tax_and_nhs_spending/).

4.3 Corporation tax

Corporation tax, a tax on company profits, has become an increasingly important contributor to the Treasury’s coffers in recent years. Over the course of the 2010s, revenue averaged 2.4% of national income; in 2025–26, that figure is forecast to reach 3.3% (£99.4 billion). Nevertheless, more revenue could be raised from corporation tax. Increasing the main rate by 1 percentage point, for instance, could raise around £4.1 billion in 2029–30 – although it would do so at the cost of making investment in the UK less attractive, reducing that potential yield. A political obstacle to raising revenue from this source, however, is the commitments set out in the government’s ‘Corporate Tax Roadmap’ (HM Treasury, 2024b) which was published alongside this government’s first Budget in the autumn of 2024. The Roadmap not only commits to keeping both the main and small profits rates at their current levels but also shuts down other potential sources of revenue, pledging, for example, to maintain much of the current system of investment reliefs, research and development (R&D) incentives and loss reliefs.11 Given the importance of certainty and stability for business investment decisions, having made such commitments there are strong arguments for sticking to them.

Even so, some avenues (albeit relatively minor ones) for revenue-raising remain compatible with the commitments set out in the Roadmap. For instance, both the bank levy (a tax on the balance sheets of large banks and building societies) and the bank surcharge (a corporation tax surcharge on their profits) are described by the Roadmap as being kept ‘under review’. Taken together, these two taxes will raise a total of £2.4 billion in 2025–26. Increasing rates would yield supplementary revenues (albeit on a modest scale) – a 1 percentage point increase in the bank surcharge, for instance, would raise around £0.4 billion in 2029–30 (not accounting for any behavioural response).

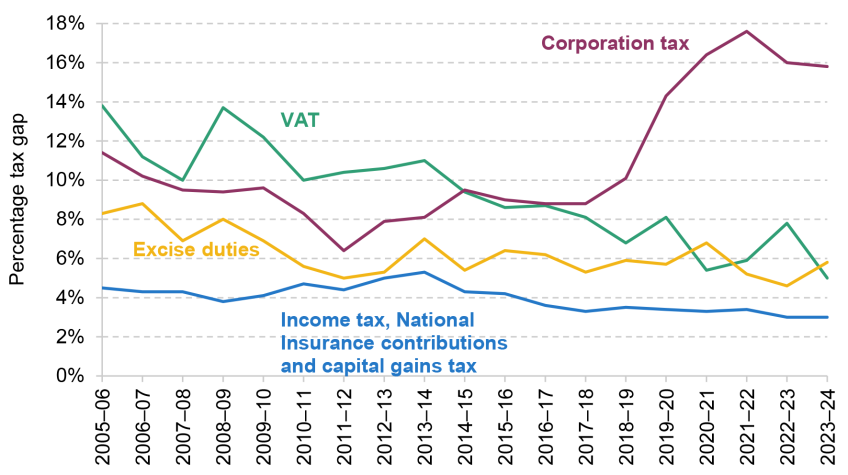

Another means by which additional revenue could also be raised from corporation tax is by improving compliance. The overall HMRC ‘tax gap’ – the difference between the amount of tax HM Revenue and Customs (HMRC) thinks theoretically ought to be paid and the amount it actually collects – has been on a downward path over the last 20 years, falling from 7.4% in 2005–06 to 5.3% in 2023–24. Bucking that broader trend, however, the corporation tax gap has widened sharply in recent years, with the estimated share of liabilities going uncollected jumping from 8.8% in 2017–18 to 15.8% in 2023–24 (the most recent year for which data are available; see Figure 4.2). This is driven entirely by a burgeoning tax gap (40% in 2023–24) amongst smaller companies (HM Revenue and Customs, 2025a). In 2029–30 terms, a corporation tax gap of that size would represent more than £24 billion of forgone revenue; just returning the gap to 2017–18 levels could raise more than £10 billion.

Figure 4.2 Estimated tax gaps

Note: The tax gap is defined as ‘the difference between the amount of tax that should, in theory, be paid to HMRC, and what is actually paid’.

Source: HM Revenue and Customs, 2025a.

The Chancellor is no stranger to seeking additional revenues by bolstering compliance. Taken together, compliance measures announced at the 2024 Budget and 2025 Spring Statement are forecast to increase revenues by £7.5 billion in 2029–30. Of that, however, the Office for Budget Responsibility expects just £0.3 billion to come in the form of increased corporation tax revenue. That suggests that closing the corporation tax gap remains a relatively untapped source of potential revenue.

While the sums involved make tackling non-compliance a substantial prize, claiming that prize would not be straightforward in practice. HMRC random audits suggest that 53% of small businesses submitting a corporation tax return under-declared their tax liability in 2021–22 – up from just 15% in 2017–18. More work is needed to understand why so many small companies are submitting incorrect tax returns. It is likely that tackling the gap would require targeted compliance activities from HMRC, such as auditing small businesses. Improved policy design would also help. The taxation of small business – like the tax system in general – has grown ever more complex. This in turn makes it harder for business owners to know how much tax they owe and to fill in their tax return correctly. We also have a tax system that incentivises people to operate through companies (rather than through self-employment or employment); see Box 4.2 later. There has been a rise in the number of people working through companies, which in turn gives rise to more risk that company directors do not understand their corporation tax liabilities. The government should adopt the dual approach of improving the design of taxes as they apply to small businesses and increasing compliance activities.

4.4 Taxes on wealth and savings

Additional revenue could be raised by increasing tax on capital incomes, on capital gains or on stocks of wealth. But this is an area where the design of the tax base – the definition of what is actually taxed – is crucial. Simply raising tax rates on capital incomes or gains – or, for that matter, introducing a new wealth tax – would increase disincentives to save and invest. That would be a drag on economic growth. Importantly, and as we will highlight in this section, better alternatives are available to a Chancellor willing to reform how we tax wealth and the returns that flow from it. Reducing the harmful distortions created by the poor design of the UK’s capital taxes should be a key focus of policy, however much revenue the Chancellor would like to raise.

In this section, we cover: taxes on capital incomes and gains; the tax treatment of pensions; inheritance tax; and the idea of a new tax on wealth.

Taxation of capital incomes and gains

Returns to capital can take many forms. Most straightforwardly, they include interest income, (actual and imputed) rental income, dividends and capital gains; all of which are subject to different tax regimes. Some returns will stem from investments within companies (and therefore be subject to corporation tax), some from investments in unincorporated businesses (and therefore be subject to the personal taxes that apply to self-employment income) and others from investments held within pensions or ISAs. Broadly, there are two problems with how the UK taxes the returns to capital investment.

First, effective tax rates on different forms of capital income and gains vary wildly; they can sometimes be below zero (an effective subsidy to saving) or above 100%. Usually, returns to capital are taxed at lower overall rates than employment income, producing a tax penalty on employment relative to other forms of income (see Box 4.2).

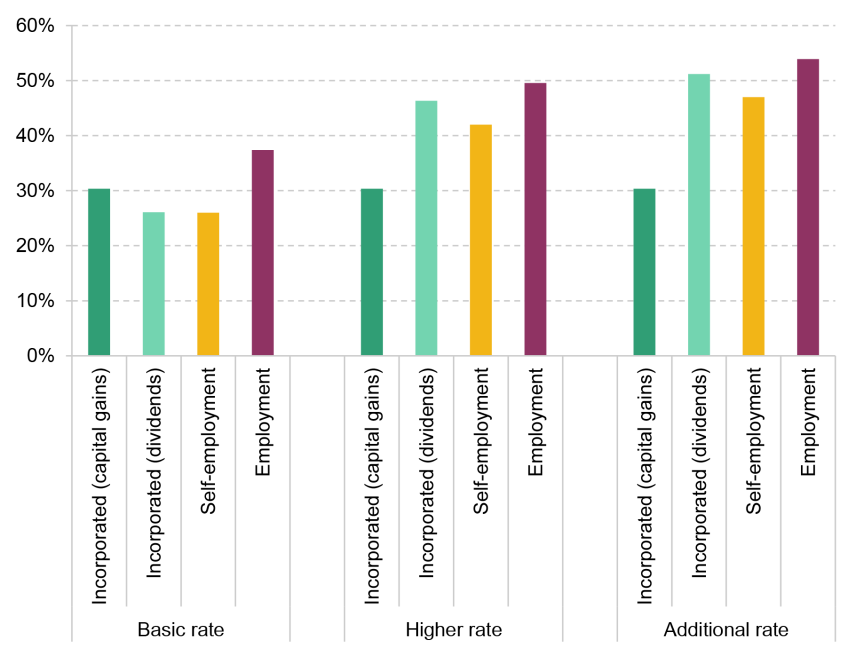

Box 4.2 How tax rates vary across different types of income and gain

Tax rates vary wildly across different forms of income and gain. Figure 4.3 gives a flavour of these differences, showing the overall marginal tax rates applied to income depending on whether it is derived from employment, self-employment or working as an owner-manager of a limited company (incorporated). Note that the overall rates include all layers of tax (business and personal), since this is what drives incentives over how to work or what to invest in. The gaps between rates charged on employment income and on capital income has narrowed in recent years,a but there is clearly still a tax penalty on employment. Tax rates on income from business (received as dividends or self-employment profits) are lower – largely (but not only) because there is no equivalent of employer National Insurance contributions on these incomes.

Figure 4.3 Combined marginal tax rates by legal form, 2025–26

Note: We show marginal combined rates including (where relevant) corporation tax at the 19% rate charged on small profits. Employment income includes employee and employer National Insurance contributions. Unincorporated self-employment includes self-employed National Insurance contributions. Income tax rates are different in Scotland, meaning that employment and self-employment bars are accurate only for taxpayers in England, Wales and Northern Ireland.

Preferential tax rates for business incomes and gains cannot be justified by differences in social security benefits or employment rights and are poorly targeted at incentivising entrepreneurship (Adam and Miller, 2019). The differential tax rates create inefficiency, unfairness and complexity. The uneven tax treatment also makes revenue-raising more challenging. One important reason why increasing the additional rate of income tax would raise little (see Table 4.1 later), for example, is that some taxpayers have the opportunity to take their money in alternative ways in response to higher rates.

Looking beyond income and gains that relate to how people work, the full variety of different tax rates and regimes applying to different returns to capital is bewildering. Tax rates (and regimes) vary across interest income earned in bank accounts, rental income, dividend income, capital gains (the rate of which varies by assets), returns earned in ISAs or pensions, and so on. Effective tax rates depend not only on the asset but also on a variety of other factors such as the rate of inflation, how long the asset is held for and whether a landlord has a mortgage. Adam and Shaw (2016) discuss effective tax rates on different forms of saving.

a.That is a result of a number of factors including increases to dividend rates of income tax, a higher main rate of corporation tax (which is charged on company profits before they are distributed as dividends), increases to rates of capital gains tax and a narrowing of the gap between employee and self-employed National Insurance contribution rates.

Second, the design of the tax base creates a long list of distortions. A key example is that saving and investment incentives vary depending on the asset type, source of finance and legal structure/vehicle involved and range from large subsidies to large penalties. The list of resulting problems includes (but is by no means limited to) a disincentive to invest (equity) in companies, a bias towards investing in some assets rather than others, a disincentive to take risks, and an incentive to hold onto assets for longer than commercial considerations would dictate.

This system is unfair: similar people doing similar activities can attract very different tax bills depending on how they arrange their work and investments. It is also inefficient: by distorting a range of decisions, including how to work, how much to save and which investments to make, our tax system ultimately reduces society’s aggregate output and well-being. The complexity of the system also creates a huge and costly burden.

Simply raising tax rates on capital incomes and gains would raise revenue. It would also exacerbate the problems caused by the poor design of the tax base. If the Chancellor were minded only to change tax rates, here is what she could expect in terms of revenue (although the likely revenue consequences of behavioural responses are hard to predict):

- A 1 percentage point increase in the basic rate of income tax on dividends would raise £0.4 billion in 2029–30 (before behavioural response). Note that the higher and additional rates of dividend tax already result in distributed UK corporate profits being taxed at similar rates to income from employment.12

- A 1 percentage point increase in the rates of income tax charged on interest income would raise around £0.2 billion in 2029 (before behavioural response).

- According to HMRC estimates, a 1 percentage point increase in the higher rate of capital gains tax would actually reduce revenues by about £30 million in 2029–30, while a 10 percentage point increase would reduce revenue by about £3.7 billion in the same year. Our view is that these estimates are not a good guide to the revenue effect over a longer time horizon and that a rise in capital gains tax rates would, up to a point, raise revenue in the medium run. Most importantly, however, the revenue raised would depend crucially on whether the tax base was reformed. Adam et al. (2024) discuss capital gains tax in detail.

- The abolition of business asset disposal relief, which provides a preferential rate of capital gains tax for certain business assets, would raise around £0.9 billion in 2029–30 (before behavioural response).

- Ending the forgiveness of capital gains at death13 would raise around £2.3 billion a year by 2029–30 (before behavioural response).

Any of these tax rises would reduce the difference in the tax rate relative to employment income. Note, however, that they would all also increase the bias towards tax-exempt assets such as ISAs and owner-occupied housing, and in some cases make other tax rate differentials worse. For example, increasing the basic rate of tax on dividends would increase the gap relative to capital gains. This is a key reason why the tax system should always be recognised as just that, a system. All of the above tax rises would also weaken incentives to save and invest – and exacerbate a range of other problems. When increasing capital gains tax rates, those problems include discouraging people from trading one asset for another.

Policymakers could largely escape this trade-off (whereby higher tax rates make some problems better and others worse) by also reforming the tax base.

In a nutshell, we propose the following big-picture solution to fixing the design flaws in capital taxes: the tax base should be changed so that there are full deductions for any amounts of money saved or invested. This should be true for all investments – including, for example, when landlords are investing in property, or business owners in their businesses. There is more than one way this could be done. Fixing the tax base would also require being more generous in the treatment of losses and removing forgiveness of capital gains tax at death. With a reformed tax base in place, tax rates could be increased with little concern about weakening incentives to invest and take risks (at least domestically: international movement of people and capital would still be a concern). Ultimately, we advocate that overall tax rates – i.e. including all layers of tax – be aligned across all forms of income and gains in order to remove the problems caused by differential rates. This solution was originally set out in Mirrlees et al. (2011). Adam and Miller (2021a) describe the solution in detail and apply it to the taxation of business owners. Adam et al. (2024) discuss how to reform capital gains tax.

We do not expect that the government would make such wide-ranging changes in one Budget. But with a clear end goal in mind, the Chancellor could take steps in the right direction. Both Adam and Miller (2021) and Adam et al. (2024) discuss in detail some specific packages of measures that the government could implement to move towards a sensible system.

Taxation of pensions

Pensions are taxed differently from most other forms of saving. Individuals’ pension contributions (up to a limit) receive full income tax relief (but no NICs relief) while employer pension contributions receive both income tax and NICs relief. Any investment returns made are also free of personal tax while the money remains in the pension fund. Income tax (but not NICs) is instead charged on pension withdrawals, with the caveat that 25% of individuals’ pension pots can be taken tax-free (up to a limit of £268,275).

The basic approach taken to applying income tax to pensions (contributions and investment returns exempt, withdrawals taxed) has a number of desirable features. First (and unlike many tax treatments of saving), it does not discourage saving. Second, it allows individuals with more volatile incomes to ‘smooth’ their taxable incomes over time – reducing the tax penalty on volatility caused by having an annual progressive income tax.14 Third, taxing pension income rather than pension contributions means that the timing of revenues is more closely aligned to spending pressures on the public finances (as retirees make greater use of the NHS and social care).

One change that the Chancellor might be tempted to make would be to restrict income tax relief on pension contributions. This could raise a lot of revenue. For example, capping relief at the basic rate of 20% could raise as much as £22 billion in 2029–30 (this is before accounting for behavioural responses; individuals’ choosing to reduce their pension saving could act to increase revenues further, at least in the short term). That is an attractive sum for a Chancellor who has left herself with limited options for significant revenue-raising. But Ms Reeves would do well to think twice.

A coherent tax treatment of pensions must consider both the treatment of pension contributions and the treatment of pension income. Providing relief for pension contributions and taxing pension income is a coherent approach (although not the only coherent approach available). Earnings put into a pension are taxed once – at the time they are withdrawn from the pension. Limiting tax relief on contributions while continuing to tax withdrawals at the taxpayer’s marginal rate, on the other hand, follows no clear logic. For one, higher-rate taxpayers would see pension savings taxed at 20% (or more) at the point of contribution and then, if they remain higher-rate payers in retirement, taxed again at 40% at the point of withdrawal – creating a strong disincentive to save. Limiting up-front relief might come as a particular shock to those who are currently basic-rate taxpayers but whose pension contributions would, if taxable, make them a higher-rate taxpayer – a group that includes many teachers and nurses, for example.

A commonly cited concern is that it is ‘unfair’ for people to get higher-rate relief on contributions and pay only basic-rate tax on withdrawals. But by the same logic, it is equally ‘unfair’ for people to get basic-rate relief on contributions and pay no tax on withdrawals if their income in retirement was below the personal allowance – yet that argument is never made. If the real aim of reform is simply to increase income tax on higher earners, then this should be done directly, through increases in income tax rates or cuts in income tax thresholds.

Principled arguments aside, moving away from up-front income tax relief at the taxpayer’s marginal rate would raise major practical challenges for defined benefit pensions as the value of employer contribution that should be assigned to each individual employee is not straightforward to measure. This is not a minor issue: HM Revenue and Customs (2025d) estimates that almost half (45%) of all up-front income tax relief is attributable to defined benefit schemes.

A better option for raising revenue from pension saving would be to review the substantial subsidy that pension saving receives as a result of its NICs treatment. Employer pension contributions escape both employer and employee NICs entirely (incurring no liability at either the point of contribution or the point of withdrawal). This fact leads many employees to enter into ‘salary sacrifice’ arrangements with their employers where they agree to a reduction in salary in return for their employer making (NICs-exempt) contributions to their pension. The annual cost of NICs relief on employer pension contributions is around £30 billion in 2029–30 terms. While there is certainly a case for subsidising pension saving, there are legitimate questions as to whether the subsidy needs to be so large. The current subsidy is also opaque and oddly targeted – for example, it provides no encouragement for the self-employed to save in a pension since, by definition, they cannot receive an employer pension contribution. Numerous possibilities exist for moving towards a system in which at least some NICs are charged on employer contributions (see Adam et al. (2023) for details). To give a sense of scale, however, a 1% employer NICs charge on all employer pension contributions could be expected to raise up to £1.5 billion in 2029–30 (although again this figure does not account for behavioural responses). More radically, employer NICs could be levied in full on all employer pension contributions, and replaced with (an arguably more salient) 10% subsidy on all employer pension contributions. This would raise around £6 billion a year (because the rate of employer NICs is 15%, which is bigger than 10%) – and it would also provide an increased subsidy on employer pension contributions in cases where employer NICs are not levied.

Another feature of the system that is ripe for reform is the tax-free 25% offered on all pension withdrawals up to a cap of £268,275. (This is commonly called the tax-free lump sum, but no longer needs to be taken as a lump.) This currently provides the largest benefit to those with the highest incomes in retirement (as income tax exemption is more valuable to those facing the higher rate of income tax in retirement). It also subsidises saving for those who have already accumulated big pension pots and are at no risk of under-saving. One attractive option for reform would be to replace the tax-free 25% with a (taxable) cash top-up on pension withdrawals. This would provide more even benefits than the current system – which favours pensioners with the highest incomes. It could be done in a way that also raised meaningful amounts of revenue while still strengthening saving incentives for those most at risk of under-funding their retirements. Less radically, the current cap of £268,275 – which was introduced by the last Chancellor, Jeremy Hunt, in his March 2023 Budget alongside the abolition of the lifetime allowance – could be cut. An IFS report from February 2023 – i.e. just prior to Mr Hunt’s announcement – set out an option for a cap along the lines that was introduced, but with the example provided of a cap of £100,000 (Adam et al., 2023).

Inheritance tax

Given the strength of feeling it is apt to provoke, inheritance tax currently raises a relatively modest amount of revenue – just over £9 billion in 2025–26 – though that is high by modern historical standards and set to rise further in the years ahead. There are a number of ways in which the Chancellor could increase that figure. One obvious option would be to increase the rate of inheritance tax from its current 40%. An increase of 1 percentage point would raise £0.3 billion in 2029–30. Another would be to reduce the threshold at which the tax begins to be paid, bringing a larger share of the population into scope of the tax (in 2025–26, 6.2% of UK deaths are expected to result in an inheritance tax charge, though that is already forecast by the Office for Budget Responsibility to rise to 9.7% by 2029–30, the highest level for more than half a century). Currently, individuals are allowed to pass on up to £325,000 of wealth tax-free, with an additional £175,000 tax-free allowance that can be used only when passing on a primary residence (or the value of a previously sold primary residence, if higher) to a direct descendant. Abolishing the second of these allowances (known as the residence nil-rate band), for example, would raise something in the region of £6 billion in 2029–30 (before behavioural response).

Another means of raising revenue would be to bring more gifts made during people’s lifetimes into the scope of the tax. For example, the length of time (currently seven years) within which gifts made prior to death have some inheritance tax applied to them could be extended. More radically, the Chancellor could seek to tax gifts across people’s entire lives (rather than just those made in the years immediately preceding death). The annual flow of gifts is around a fifth of the value of the annual flow of non-spousal inheritances, with the largest 5% of gifts making up more than half of the total value of gifts received over 2018–20 (Boileau and Sturrock, 2023). Gift taxes are not uncommon internationally, although no jurisdiction raises large amounts of revenue from such a tax. It is hard to find a principled rationale for taxing lifetime gifts less than bequests at death. The taxation of gifts does, however, raise some additional practical challenges, aside from the potential unpopularity of extending inheritance tax at all (inheritance tax frequently tops polls as the most unpopular tax). For a detailed discussion of options for reforming inheritance tax, see Advani and Sturrock (2023).

A new tax on wealth

One suggestion recently raised is that additional revenue could be raised through a new annual tax on wealth.15 Support for a wealth tax is often motivated by the observation that wealth inequality has been rising and that a significant proportion of wealth at the top stems from business income, which tends to be taxed at lower rates than labour income.

It may seem obvious that taxing wealth is a good way to create a progressive tax system: aren’t wealthy people better off almost by definition? And shouldn’t we, therefore, tax stocks of wealth? In fact, making the case that an annual wealth tax is part of a well-designed tax system is much less straightforward. The economic arguments for and against a wealth tax are discussed in detail in Adam and Miller (2021b). In short, making the case for a recurrent tax on wealth requires explaining why it is better to tax the same wealth every year rather than raising the same revenue by taxing all sources of wealth once when they are received (and/or when they are spent). An annual tax on stocks of wealth would penalise saving and create an incentive to move wealth out of the UK (or not bring it here in the first place). At the same time, a wealth tax would not be effective at taxing those who receive very high returns on wealth but spend them quickly – a wealth tax is not a good substitute for a well-functioning tax on capital income and gains.

Even if a wealth tax is deemed desirable in principle – either because policymakers decide they want to target tax at people who save, or because reform of other taxes is deemed not to be possible – the practical issues involved in designing and implementing a tax on wealth stocks should not be underestimated. It would require the government to value wealth each year. This would be a huge undertaking. It would be extremely difficult – conceptually and in practice – to value certain kinds of assets, such as private businesses (which are a large share of wealth for the very wealthy) and defined benefit pension rights.

Any specific wealth tax proposal would need to specify which assets would be subject to the tax, at what rate(s) and above what threshold. The precise design of a wealth tax would be key to determining its effects. Taxing millionaires and taxing billionaires are very different propositions, and both are very different from taxing ordinary people’s houses and pensions. Not only are the taxpayers themselves different, but so are the assets involved and the likely behavioural responses. Importantly, any tax that did not apply to all assets would allow opportunities to avoid the tax – but valuing all assets in order to apply a comprehensive wealth tax would, as mentioned above, pose enormous practical challenges.

How a wealth tax was designed would also determine how much revenue could be raised. The Wealth Tax Commission analysed a wealth tax that would apply to virtually all assets and estimated16 (using data for 2016–18) that a 1% tax would raise £33 billion if applied above a threshold of £1 million, or £10 billion if applied above a threshold of £10 million, before allowing for any behavioural response to the tax.17 In practice, however, the yield would be significantly reduced by a variety of behavioural responses (from reduced wealth creation and accumulation to avoidance and emigration); quite how much the yield would be reduced is highly uncertain and contentious.

International experience of annual wealth taxes is not encouraging: they have been abandoned in most of the developed countries that previously had them. While details vary across countries, the typical experience was that – among other problems – large-scale reliefs and exemptions (introduced for a combination of practical and political reasons) undermined the revenue yield, meaning they brought in little revenue in return for the economic, administrative and political headaches they caused (Perret, 2021).

We caution against introducing an annual wealth tax. Our view is that the government’s priority should be to fix current taxes – including capital gains tax and inheritance tax (as discussed above). We should not underestimate the (potential) radicalism of possible reforms to existing wealth-related taxes. To take just one example, aligning tax rates on capital gains (after fixing the tax base) with tax rates on earnings would imply a top rate of over 40%, compared with the 18% rate (from 2026–27) under business asset disposal relief and 0% where capital gains are unrealised at death. Reforming existing taxes could involve a very big tax rise for many of the best off.

Finally, while there are serious drawbacks to a recurring wealth tax, a tax based on an unexpected and credibly one-off assessment of existing wealth could in principle be an economically efficient way to raise revenue, since tax liabilities based only on past wealth could not be reduced by changing future behaviour. The potential efficiency of such a tax could be undermined, however, if announcing a one-off tax created expectations of, or uncertainty about, other future taxes (whether a repeat of the ‘one-off’ wealth tax or something else entirely) which led people to change their behaviour – though other tax rises can also affect expectations and uncertainty. Whether such a tax is considered fair (for example, whether it is fair that a one-off tax would fall mainly on the particular generation that happened to be at the peak of their wealth – typically around retirement age – at the time it was assessed, and on those within that generation who had saved rather than spent their money) is something on which reasonable people will differ. Again, Adam and Miller (2021b) discuss this in detail.

4.5 Property taxes

A Chancellor seeking to raise revenue could turn to existing property taxes. In this section, we consider those levied on the occupiers of domestic properties (council tax) and of non-domestic properties (business rates), as well as on the purchase of land and buildings (stamp duty land tax).18

Council tax

Levels of council tax are set by local authorities but, in England, annual increases are typically capped (at 5% in recent years for authorities with responsibility for social care services).19 Pressure on local government finances has seen local authorities in England bumping up against that cap, and the OBR forecast currently assumes increases of 4.3% a year for the remainder of the parliament (Office for Budget Responsibility, 2025).20 Council tax increases would need to go above and beyond that 4.3% a year in order to strengthen the public finances relative to current forecasts.

The simplest option would be to remove or relax the current cap on increases in England. Local authorities would not be obliged to increase rates by the maximum allowed amount, but if all did increase their council tax rates (beyond what they would otherwise have set), each additional 1% increase in council tax would collectively raise them about £0.5 billion in 2029–30.

Another option would focus council tax increases on the highest-band properties by increasing the relative tax rates applied in those bands.21 Council tax (before any discounts) is currently a lower percentage of property value for high-value properties than for low-value properties. For example, properties in England in the top council tax band, band H, are charged three times as much as band A properties in the same local authority, despite being worth (in 1991) at least eight times as much and usually far more.22 This regressive rate structure is hard to justify. The government could change those relativities to increase the relative rates for high-band properties, making the tax more proportional to (1991) property values. Scotland introduced a modest reform of that kind in 2017.23 Again, local authorities need not necessarily raise more revenue from council tax as a result: they could choose to respond by setting a lower band D rate than they otherwise would, to keep average bills the same but with liabilities rebalanced so that those in high-band properties paid more and those in lower-band properties paid less. But if local authorities set the same band D rates as in the absence of reform, copying Scotland’s 2017 reform in England would raise about £1.9 billion in 2029–30; doubling the top two rates of council tax in England (those applying to bands G and H, around 4% of properties) would raise £4.2 billion in 2029–30. Either of these options would make council tax less regressive, but the latter would be more radical, with much sharper increases for a smaller set of properties. In a council that set its band D rate at the 2025–26 England average, band G and H properties would attract an additional £3,800 and £4,560 a year respectively in council tax, taking their total bills to £7,600 and £9,120.

Any additional revenue from council tax rises would flow to local authorities, not central government. This might be worth considering, given the severe financial pressures facing many local authorities; but it would not directly help the Chancellor meet her fiscal rules. If Ms Reeves wanted to bolster central government’s finances, she could reduce the grants paid out to local authorities – essentially using any council tax changes of the kind described above as a way to enable local authorities to make up the revenue lost from grants. But reducing grants to local authorities would mean altering the Spending Review settlement made in June, which the government might be loath to do. Any changes to the structure of council tax would also affect the implementation of reforms the government is currently planning to the local government finance system.24

Alternatively, a new national tax could be introduced that would act as a top-up to council tax but would be paid to central government. One possibility would be a national supplement to council tax rates, broadly analogous to that levied in London by the Greater London Authority, for example. Another would be a new surcharge on band G and H properties, charged at flat rates across the country.25

A major downside of a council tax increase or supplement – especially one targeted at the highest bands – is the fact that tax bands in England (and Scotland) are still based on the values of properties in April 1991. Properties in the highest bands are not those that are worth most today, but those that were worth most in 1991 – a very different set. In particular, properties in areas such as London (where average house prices are around seven times higher than in April 1991) are under-represented in top bands and properties in areas such as the North East (where average prices have increased only fourfold in the same period) are over-represented (HM Land Registry, 2025). A tax rise on band G and H properties would therefore not be hitting the most valuable properties. A revaluation is long overdue. On its own, bringing assessed values up to date would not raise revenue, but it would distribute the tax burden more fairly and make tax rates – and increases – less arbitrary. 26, 27

Business rates

Business rates are one of the few areas of the tax system where Labour’s manifesto signalled interest in genuine reform, stating that Labour would ‘replace the business rates system, so we can raise the same revenue but in a fairer way’.28 The reality has proved less ambitious, with published proposals reading more like tweaks to the status quo than replacement (HM Treasury, 2024a). Regardless, with both the manifesto and subsequent proposals indicating that any changes will be on a revenue-neutral basis, it is hard to see business rates providing any significant extra revenue at the coming Budget.

Stamp duty and land tax

Stamp duty land tax (SDLT)29 is levied on the purchase of land and buildings. It has been gradually increased over the course of this century and is forecast to bring in £24.5 billion in 2029–30. That is regrettable. Taxing asset transactions impedes mutually beneficial exchanges. Instead of allowing assets to be sold to those who value them most, SDLT effectively throws sand in the gears, leading to an inefficient allocation of property. Imagine, for instance, an elderly couple living in a large suburban house with more rooms than they need but which is in need of doing up, and a young family living in a small urban flat that has been recently refurbished and is of the same value. It may be that both families would be happier in each other’s homes, and in an uninhibited market they would be able to transact. But SDLT adds a cost to the transaction, which may stop it from taking place – despite the fact that it would have made both families better off. One consequence of people choosing to move house less often than they would do otherwise is that they are less likely to relocate to get (better) jobs, acting as a drag on growth. SDLT on rental housing and on commercial property is similarly damaging.

SDLT certainly should not be increased. But a well-designed tax system would have no place for SDLT at all. The IFS-led Mirrlees Review (Mirrlees et al., 2011) argued that SDLT should be abolished as part of a wholesale reform of property taxation – arguably the part of the tax system that needs it most. Council tax should be turned into a tax proportional to up-to-date property values, set at a rate that would replace the revenue from SDLT on housing as well as existing council tax revenue. The revenue from both business rates and SDLT on commercial property would then (ideally) come instead from a tax on the value of non-residential land (i.e. excluding the value of the buildings themselves, unlike business rates) – feasibility of accurate valuation permitting – so as not to discourage the development and use of property for business purposes. There is a case for raising a larger share of tax revenue from taxes on land and property – since land is in fixed supply and cannot move, and taxing it therefore causes less economic distortion (and is more growth-friendly) than other taxes, such as taxes on income. But the priority should be to reduce the damage and unfairness caused by our existing property taxes. More sensible property taxes could be increased, if desired, with fewer reservations.

4.6 Other indirect taxes

In this section, we discuss the scope for the Chancellor to raise revenues through indirect taxes (that is, taxes levied on goods and services) other than VAT. Taken together, taxes of this kind represent a meaningful source of revenue and are forecast to raise £109 billion in 2029–30.

Motoring taxation