Downloads

Download the report as a PDF

PDF | 599.27 KB

Executive summary

Since its inception, the Welsh Government has had powers over local taxation – determining the structure of council tax (with councils then setting the headline tax rate) and the structure and level of business rates. The late 2010s saw the Welsh Government gain powers over a number of other taxes, including the power to vary income tax rates on non-savings, non-dividends income. Devolved taxes now account for around 21% of the Welsh Government’s budget for day-to-day (resource) spending.

The Welsh Government has made only modest changes to tax policy during the current Senedd term. But more is scheduled to come, with a visitor levy and regular revaluations of council tax legislated for, and the potential for broader reforms to Wales’s local tax regime.

The Welsh Government has only relatively limited powers over benefit policy, but has the ability to make somewhat bigger changes than it has to date, if it so wished.

Key findings

- Decisions by Welsh Governments, including during the current Senedd term, have resulted in only modest differences in tax and benefit policy compared with England. To a large extent, this reflects the fact that the powers devolved to Wales are limited in scope – certainly by comparison with Scotland. However, even for policies that have been fully devolved, such as property transaction tax and business rates, changes made by the UK government in England and Northern Ireland have often been mirrored in Wales – including those with questionable economic rationale, such as higher transaction taxes on second or rental properties. This suggests UK government policy remains a key reference point for Welsh policy. However, influence is not all one way – the UK government has recently followed Wales in allowing councils to set second-home council tax premiums, and is consulting on plans for a ‘tourism tax’. And hopefully other parts of the UK will follow Wales’s lead with plans for a full revaluation of council tax.

- The largest devolved tax power is the power to set the Welsh rates of income tax. The Welsh Government is able to vary income tax rates on non-savings, non-dividend income, but not the bands. This allows the Welsh Government to increase or reduce revenue, but means less scope to target tax rises or cuts than in Scotland, where powers over tax bands are devolved too. Perhaps as a result, the Welsh Government has not yet made use of its income tax powers. However, it has benefited from additional revenue as a result of income tax devolution because UK government freezes in tax thresholds rates increase revenues from each tax band in Wales by more in percentage terms than in England due to the shape of the Welsh income distribution.

- After a revaluation in 2005, Welsh council tax bands are not as out of date as those in England and Scotland – but are still based on relative property values in 2003, almost a quarter of a century ago. As a result, it is welcome that the Welsh Government has legislated for a council tax revaluation in April 2028 and every five years thereafter. This is intended to be revenue-neutral. Further changes to the tax could be made at the same time, including adding additional bands, and a less regressive structure. While it is a shame reforms were pushed back from 2025 (the initial date proposed), the Welsh Government deserves credit for grasping what is clearly a thorny political issue.

- Policy on land transaction tax since the last Welsh election has continued two previous trends: cutting rates at the bottom while raising them at the top, and increasing the surcharge for second and rental properties. The latter – penalising the rental sector in a particularly harmful way – is an especially unwelcome trend shared in the rest of the UK. But more generally, taxing land transactions is ill-conceived. While the Welsh Government has pursued sensible reform of housing taxation, it is a shame that has not extended to this most damaging property tax.

- The Welsh Government has made business rates more complicated by introducing a higher tax rate for high-value properties, a lower tax rate for low-value retail properties and a temporary relief for food and drink hospitality businesses. Although superficially appealing, the case for such differentiation is not clear. The effects of business rate changes are likely to be felt mainly by landlords rather than tenants in the long run. Research commissioned into the feasibility of land value taxation points towards a more promising direction for reform in the future.

- Legislating to allow councils to introduce ‘visitor levies’ on overnight accommodation has given them another (modest) revenue-raising option. There are arguments for and against imposing such levies, but there is some logic to making it a local decision based on local circumstances and views on the costs and benefits of visitors to the area. Indeed, there is an argument for giving councils somewhat more flexibility than the legislation currently does.

- No further tax powers are currently confirmed for devolution, but the current Welsh Government appears interested in acquiring modest additional powers. It has recently resurrected its request for powers to levy a tax on land with planning permission but where development fails to take place for several years (a ‘vacant land tax’). It has also commissioned research on the options for further income tax devolution. Devolving income tax rates on savings and dividend income would allow the Welsh Government to apply any changes in rates it made in future to all forms of income, closing down some tax avoidance opportunities (although opening up others). Giving it powers to vary bands, as in Scotland, would allow more targeted tax rate changes, but the Welsh Government would need to take care to avoid over-complicating the tax rate structure, as has happened there.

- Limited devolution of benefit policy constrains the extent to which Wales can diverge from the system that operates in England. Where powers are devolved and have been used, the Welsh Government has generally chosen to be more generous. The most significant example is the council tax reduction scheme, but the Welsh Government has also used its powers to extend access to free school meals and to fund a number of payments administered by councils (including one-off means-tested energy cost support during winter of 2022–23). Unlike in Scotland, in Wales the power to create new ‘social security’ benefits, or to top-up existing benefits, is explicitly reserved to the UK government, which means that creating a Welsh equivalent of the Scottish child payment may not be possible. However, the Welsh Government could use discretionary housing payments administered by councils to mitigate the bedroom tax or benefit cap, as is the case in Scotland, if it so chose.

1. What tax and benefit powers are devolved to Wales?

The Senedd and Welsh Government have had powers over local tax policy since the advent of devolution in 1999, determining the structure of council tax, and the structure and rates of business rates.1

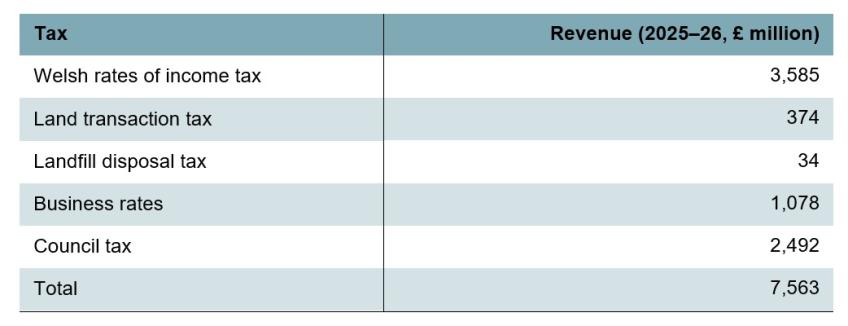

Following the Silk Commission (Commission on Devolution in Wales, 2012, 2014) and Wales Act 2016, the late 2010s saw the Senedd and Welsh Government gain and subsequently make use of a wider range of powers over tax. Table 1 summarises the most recent forecasts for revenues from devolved taxes for the year just ending, 2025–26.

Table 1. Forecast revenue for devolved taxes

Source: Office for Budget Responsibility (2026) and Welsh Government (2025a).

Specifically, the Senedd and Welsh Government have powers over:

- 10 percentage points of each income tax rate for income other than savings and dividend income. These Welsh rates of income tax are forecast to raise £3.6 billion in 2025–26, and the power to set these rates was first devolved in 2019–20.

- The taxation of land and property transactions. In Wales, this is enacted via land transaction tax (LTT), which is forecast to raise £374 million in 2025–26. This power was devolved in 2018–19.

- Taxation of landfill disposal, via the landfill disposal tax. This tax is forecast to raise £34 million in 2025–26 and was also first devolved in 2018–19.

- Business rates, which councils collect and the Welsh Government then redistributes between them on the basis of population, are forecast to raise £1.1 billion in 2025–26.

- Council tax, which Welsh councils set the headline (‘Band D’) rate of, collect and retain the revenues from, is forecast to raise £2.5 billion in 2025–26.

Taken together, these represent approximately 19% of all tax revenue raised in Wales.2 The four taxes which flow to or via the Welsh Government rather than directly to councils make up 21% of its funding for day-to-day (resource) spending as of 2025–26 (Brogaard and Phillips, 2026).

Using its powers over local taxation, the Welsh Government has also legislated for a tourism accommodation tax which councils will be able to choose to implement from April 2027.

On the benefits side, the vast majority of benefits remain the responsibility of the UK government but the Welsh Government does have powers over the design of several payments administered by councils. This includes means-tested reductions to council tax bills via the Council Tax Reduction Scheme, and discretionary payments for households facing hardship or at risk of homelessness. As we discuss later, the Welsh Government also has powers to make payments akin to those that councils in England are able to make – whether directly itself or through Welsh councils. The precise limits of these powers are not well defined, but it seems like it would be possible for the Welsh Government to use these powers more than it has so far.

2. Income tax unchanged but is raising additional revenue

Since 2019–20, income tax has been partially devolved to Wales. For income other than savings and dividend income, the UK government has reduced the rates of income tax it applies to Wales by 10 percentage points. This means that the basic, higher and additional rates applied by the UK government are 10%, 30% and 35%, respectively. The Senedd and Welsh Government are then able to set Welsh rates of income tax on top of these, and retain the revenues. From a Welsh taxpayer’s perspective, this effectively means the Welsh Government is able set the basic, higher and additional rates – albeit it is not able to cut rates by more than 10 percentage points relative to UK rates. In contrast to the Scottish Government, it has no powers to vary income tax thresholds, or to introduce new thresholds.

So far, the Welsh Government has not made use of its income tax powers to increase or reduce tax rates. It has set 10% rates on each band, meaning a taxpayer in Wales pays the same income tax rates as they would in England or Northern Ireland. This also contrasts with the Scottish Government, which has made extensive use of its powers.

In this section, we first set out how the Welsh Government’s limited powers constrain its options to vary income tax. We then analyse options that the next Welsh Government has to raise or lower income tax, including their effects on revenues and individuals’ tax liabilities. Finally, we discuss how UK government policy has affected Wales’s devolved income tax revenues.

Limitations of the Welsh powers

The Welsh Government does have the ability to raise more or less tax revenue, and to make the income tax system more or less progressive by changing different rates differently. However, only being able to set rates, rather than vary band thresholds too, does impose limits on how targeted tax changes can be: for instance, a change in the basic rate of tax must apply to all basic rate taxpayers. For example, increasing all rates of income tax by 1 percentage point would be a broadly progressive tax rise across the population as a whole (because of the tax-free personal allowance), and raise a meaningful amount of additional revenue (see below). Increasing just the higher and top rates of tax is also possible, but would raise only modest sums (again, see below). However, it is not currently possible to increase tax on, for example, individuals with incomes above £30,000 (roughly halfway up the basic rate tax band), which would again raise a meaningful amount, but protect lower-income taxpayers.

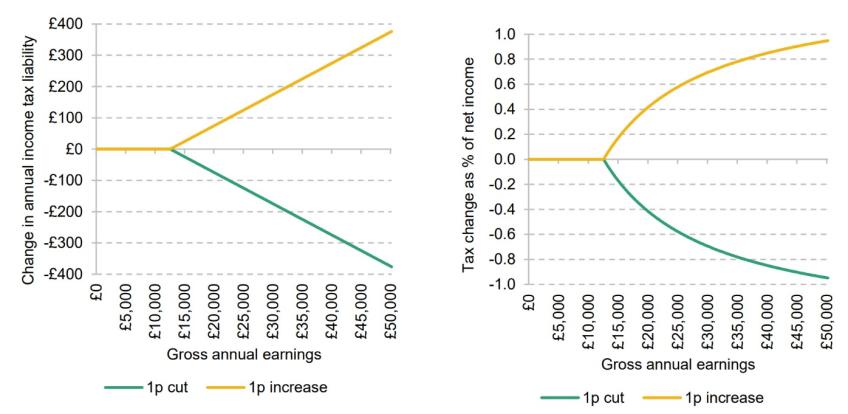

Options for cutting taxes are similarly constrained. For example, if the Welsh Government wished to cut taxes for lower-income taxpayers, it could only do so by cutting the basic rate. This would deliver a bigger tax cut to higher-paid individuals within the basic rate band – with the maximum gains from 1 percentage point reductions in the basic rate being highest in both cash terms (£377 a year) and as a proportion of income (0.9%) for someone at the top of the basic rate band (with income of £50,270). The gain for someone working full-time on the national living wage (earning £24,785 a year) would be smaller (£122 or 0.6% of net income, at most, and less if they are in receipt of universal credit). This is illustrated in Figure 1, which shows the change in income tax bill in cash terms and as a percentage of net income for a 1 percentage point change in the basic rate of income tax for taxpayers with different income levels. Just as it is impossible for the Welsh Government to exempt lower-paid basic-rate income taxpayers from an increase in income tax, it is impossible for it to target income tax cuts at this group.

Figure 1. Changes in income tax liabilities for basic-rate taxpayer resulting from 1p cut/increase to basic rate

Source: Authors’ calculations.

If the Welsh Government had the ability to vary and introduce bands, then more options would be available to vary the progressivity of the system, including while raising or cutting taxes overall. For example, it could target tax rises at higher-earning basic-rate taxpayers, by lowering the higher-rate threshold, or by accompanying an increase in the basic rate of income tax with the introduction of a zero-rate band above the personal allowance (which would more than offset the higher tax rate for lower-income taxpayers). The ability to introduce a zero band would also allow the Welsh Government to target tax cuts at lower-income taxpayers, without cutting the taxes of higher-income taxpayers (within a band), by suitably varying other rates and thresholds.

This inflexibility is compounded by the fact that Wales has a lower distribution of income than England. In 2023–24, over 89% of Welsh taxpayers were basic-rate taxpayers (HMRC, 2025), compared to 78% in England (UK government, 2025a), and over 82% of the Welsh Government’s tax revenue in 2026–27 is set to come from the basic-rate tax band (Office for Budget Responsibility, 2026). This means that, unless the Welsh Government were willing to increase the higher and top rates substantially, increasing the basic rate – thereby affecting even the lowest-income taxpayers – is the only way it can currently raise significant sums from changes to income tax.

The current Welsh Government has cited these precise limitations as the reason it has not made use of its existing income tax powers (Senedd, 2025), though it also did not support a Plaid Cymru motion in the Senedd calling for devolution of powers over rates and bands in 2023 (Senedd, 2023).

Behavioural and revenue effects of potential tax rate changes

Changes to taxes using the existing powers are nevertheless an option open to the next Welsh Government. For example, the Welsh Conservatives have promised a 1 percentage point cut to the basic rate in their manifesto (Welsh Conservatives, 2026), and Reform UK have proposed a 1 percentage point cut to all rates and bands by the end of the upcoming Senedd term in 2030 (Reform UK, 2026).

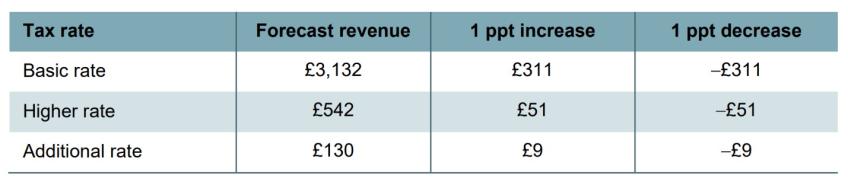

Table 2 sets out the revenue forecast to be raised from the Welsh rates of income tax from each of the basic, higher and additional rate bands in 2026–27. Each of those rates is currently 10%. The table also sets out official estimates of the additional revenue that would be raised for the Welsh Government by increasing each rate by 1 percentage point, and the (roughly symmetric) costs of cutting each rate by 1 percentage point. The table shows that raising the basic rate is the only lever available to deliver substantial additional revenue to the Welsh government, with a 1 percentage point increase raising £311 million per year (with a cut costing the same) – this is equivalent to around 1.3% of the Welsh Government’s budget for day-to-day (resource) spending. Conversely, an increase in the higher rate of income tax would raise £51 million – around 0.2% of resource spending.

Table 2. Revenue effects of 1p changes in tax rates (2026–27, £ million per year)

Source: Welsh Government (2026a).

Behavioural responses to tax policy changes would affect the revenue effects of tax policy changes. These responses could take several different forms, including: reductions in hours of work or effort; (legal) tax avoidance and (illegal) tax evasion; and migration out of Wales (or discouraged migration into Wales). Because Welsh rates of income tax do not apply to savings and dividends income, some individuals could also avoid any tax increase by setting up an incorporated business, and taking income in the form of dividends rather than salary or self-employment profits. A range of evidence suggests such responses are highest for high-income taxpayers; see Phillips (2024) and Saez, Slemrod and Giertz (2012) for a review. It is for this reason that the gap between the estimated revenue effect of a 1 percentage point change in tax rate and 10% of current revenue forecasts is proportionately largest for the additional rate (£9 million versus £13 million) – behavioural responses are assumed to have the biggest impact on revenues from this tax rate.

However, if the Welsh rates of income tax were changed, then the expected effects of behavioural responses to those changes on Welsh Government revenues would be smaller than in the case of either the UK government or Scottish Government. This is because the Welsh Government only retains a proportion of the revenue from each band (10 percentage points), with the remainder going to the UK government. For example, if the Welsh additional rate of income tax was increased by 1 percentage point, and some affected taxpayers reduced their taxable income (for example, by saving more into a pension) in response, then the Welsh Government would bear the impact of this reduced income on its 11 percentage points of income tax (10 + 1 percentage point increase). But the UK government would bear the effects on revenues from its 35 percentage point additional income tax rate in Wales. As a result of this, while the Welsh Government bears the full mechanical revenue effects of changes in the Welsh rates of income tax (holding behaviour fixed), it bears only part of the revenue effects of changes in behaviour – with the UK government bearing the behavioural effect on its portion of income tax revenues.

In contrast, in Scotland, the Scottish Government bears all effects on income tax revenues on non-savings, non-dividends income tax – it does not bear the effects on other taxes such as dividends and savings tax, National Insurance contributions (NICs) or capital gains tax, for example. And in England and Northern Ireland, the UK government bears all effects on all income tax revenues (plus NICs and other revenues). As we discuss in Section 6, the partial devolution of revenues from each tax band to Wales and the fact that revenue effects of behavioural responses to Welsh income tax policy are only partially borne by the Welsh Government may affect its tax-setting behaviour in future.

Recent changes in income tax revenue in Wales

The real-terms income tax revenues received by the Welsh Government have increased over the current Senedd term despite it making no changes to tax rates. In large part, this is due to cash-terms freezes in the tax-free personal allowance and higher-rate threshold, and a reduction in the additional-rate threshold, by the UK government. These policies have meant more people have started paying income tax, or higher rates of income tax, as their incomes have grown in cash terms. The Welsh Government expects to receive over £3.8 billion in income tax revenue in 2026–27, which represents a 9% real increase relative to 2024–25, and a 27% real increase relative to 2021–22 (HMRC, 2023).

The net effect of devolved income tax revenues on the Welsh Government’s budget (the so-called ‘net income tax revenue position’) depends not only on how Welsh income tax revenues themselves evolve, but also on how revenues from each tax band evolve compared to revenues from the same tax band in England and Northern Ireland. This is because the block grant adjustments (BGAs) subtracted from the Welsh Government’s block grant funding to account for income tax devolution, after initially being set equal to income tax revenues in Wales in each band in 2019–20, have been indexed according to the rate of growth in revenues from the same tax bands in England and Northern Ireland in subsequent years.3

Freezes in the personal allowance and tax thresholds mean that revenues from each tax band have grown at a faster percentage rate in Wales than in England and Northern Ireland, and so faster than the offsetting BGAs subtracted from the Welsh Government’s block grant funding. This is because typically lower incomes in Wales mean that more of the taxpayers and taxable incomes in a given tax band are closer to the bottom of each tax band than in England and Northern Ireland. Freezing the thresholds therefore drags proportionately more taxpayers and income into a tax band, and results in proportionately larger percentage increases in the amount of income tax in each tax band. This means that the income tax net revenue position has been increasingly positive – meaning a growing positive contribution to Welsh Government funding over time – despite relatively weak employment figures in Wales compared with England and Northern Ireland (Office for Budget Responsibility, 2026). Outturns and forecasts show the net income tax revenue position increasing from £72 million in 2021–22, to a forecast £360 million in 2026–27 (HMRC, 2023; Office for Budget Responsibility, 2026). This increase is just over 1.5% of the Welsh Government’s resource funding for 2026–27 (Welsh Government, 2026b).

Note, though, that if the personal allowance and tax bands were unfrozen and increased faster than incomes, this process would reverse, and Welsh revenues from each band would grow proportionately less quickly (or fall by more) than in England and Northern Ireland and hence the offsetting BGAs. The net income tax revenue position would then fall, and act as a drag (rather than a boost) to the Welsh Government’s budget. Income tax devolution, while beneficial financially to the Welsh Government so far (despite no changes having been made to income tax rates), could in future reduce Welsh Government funding – highlighting how tax devolution brings risks as well as opportunities.4

3. Taking the lead on council tax revaluation and reform

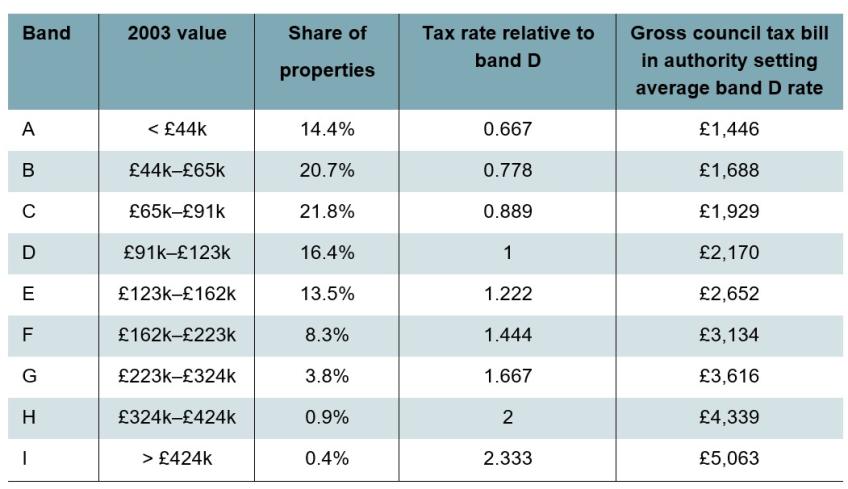

Households pay council tax on the property they occupy. Since 1999, the Welsh Government has determined the structure of the tax – including the relative tax rates for different properties – while individual local councils and police authorities set the overall level of the tax in each area. The current system is summarised in Table 3.

Table 3. Summary of the Welsh council tax system in 2025–26

Source: Average band D rate and share of dwellings in each band calculated using data from Welsh Government (2025b).

Comparison across nations of the UK

It is difficult to compare council tax rates in Wales to those in England and Scotland.5 Comparing the average rate for a band D property, for example, is not very meaningful because properties are not allocated to bands on the same basis. A band D property in Wales is not necessarily worth the same as one in England or Scotland; indeed their values cannot even be compared like-for-like, as council tax bands in England and Scotland are still based on 1991 property values, while in Wales they are based on 2003 property values. And there are differing proportions of properties in each band: 43% of properties in Wales are in band D or above, compared to just 35% in England, for instance.

More informative is a comparison of the average net council tax bill. In 2025–26, the average bill in Wales is similar to that in England (about £1,800) and considerably higher than in Scotland (a little under £1,300).6 But property prices in Wales are significantly lower than in England, though higher than in Scotland; as a proportion of average property value, the average council tax bill in Wales (around 0.75%) is considerably higher than in either England or Scotland (both around 0.5%).7

A process of welcome reform

Although the 2021–26 Senedd term has seen significant increases to council tax rates in cash terms, there has been rapid inflation in this period as well, so in real terms the average band D rate is only 1% higher in 2025–26 than it was in 2021–22 (Welsh Government, 2021a, 2025b). However, this is in the context of real-terms reductions in council tax rates over this period in both England (3%) and Scotland (5%) (UK government, 2025b; Scottish Government, 2025c). Most councils in Wales are proposing to increase council tax by a little more than inflation in 2026–27 (Wightwick, 2026).

The more important development over the course of this Senedd term has been the significant progress that has been made towards council tax revaluation and reform.

Reform of council tax was a 2021 manifesto pledge of both the governing Welsh Labour Party and Plaid Cymru, with which Welsh Labour had a co-operation agreement for certain policy and legislative priorities for much of this Senedd term (Plaid Cymru, 2021; Welsh Labour, 2021). This agreement included reform of council tax, with a stated aim of making the tax ‘fairer’ and less regressive (Welsh Government, 2021b).8 Between 2022 and 2024, the Welsh Government undertook two consultations (Welsh Government, 2023a, 2024a) on possible directions for reform – the latter accompanied by an IFS report (Adam, Phillips and Ray-Chauduri, 2023) commissioned to analyse some specific illustrative options. This was followed later in 2024 by legislation to revalue all properties for council tax in 2028 and to regularly revalue every five years after that.

Revaluation is important because, since 2003, the values of different properties have increased by very different amounts. Properties now worth similar amounts can face bills that differ by hundreds of pounds because they used to be worth different amounts in 2003; conversely, properties now differing in value by hundreds of thousands of pounds can face the same tax bill because they were in the same (broad) value range in 2003. This unfairness is resolved by regular revaluations, which ensure that equally valuable properties in the same local authority are taxed at the same rate.

Revaluation need not mean a net tax increase just because the properties have risen in value since 2003. Thresholds can be set higher to reflect higher property values; if councils (collectively) wish to spend the same amount on public services and receive the same amount of grant from the Welsh Government, then they will need to raise the same amount in council tax revenue to make up the difference (i.e. set the same average bills). The Welsh Government intends the revaluation to be revenue-neutral, though it cannot control that, as the revenue ultimately raised will depend on the tax rates chosen by councils and police authorities, not on the Welsh Government’s policy design.

The Welsh Government’s original plan was to proceed with revaluation in 2025. The delay to 2028 was disappointing: revaluation was already long overdue and there was no obvious economic or administrative need for, or benefit from, delay. But to legislate for a revaluation at all was a major achievement, sadly unmatched so far by the UK and Scottish governments.

The council tax bands and the relative tax rates that will apply to them after the 2028 revaluation have not yet been announced. The minimal option would be a ‘pure revaluation’: to keep nine bands as there are now, with the same relative tax rates for different bands and with the thresholds chosen to keep the same proportion of properties in each band as now but based on up-to-date rather than 2003 values, so that the highest-value properties are in the highest bands. In our view, there is a strong case for going beyond a pure revaluation. Council tax has other problems besides out-of-date valuations:

- The use of a small number of wide bands means that properties just either side of a threshold, with very similar values, attract very different tax liabilities; while properties at opposite ends of a band can have very different values yet attract the same tax.

- Council tax is regressive with respect to property value: it is a higher percentage of property value for low-value properties than for high-value properties (at least before means-tested discounts). As Table 3 shows, band I properties have a (2003) value at least 9.6 times as high as band A properties but attract only 3.3 times as much council tax. Not every tax needs to be progressive: what matters is the effect of the system as a whole. But if we want to levy higher tax rates on those with more resources in general, then it seems odd to levy lower tax rates on those with more of one particular resource (housing) as the current regressive structure does. Moreover, the fact that it is harder to hide or move housing than it is to hide or move income means that combining a regressive council tax with a progressive income tax is likely to increase the economic distortions and costs of redistribution. Even if one did not want to increase the progressivity of the overall tax system, there is a case for making council tax less regressive (and other parts of the tax system, such as income tax, less progressive) to redistribute in a less economically costly way.

- The way the 25% discount for single-adult households is designed – worth more if living in a high-band property than a low-band property – makes it cheaper for single-adult households, and more expensive for multi-adult households, to live in higher-band properties, contributing to both underoccupation and overcrowding.

On the last of these, the Phase 2 consultation document unfortunately proposed to ‘retain the one-adult discount and to keep the level of discount at 25%’. On the structure of tax rates and bands, the three illustrative options discussed in the consultation ranged from a pure revaluation to options that would also make the tax rates applied to properties in different bands somewhat less regressive and add three more bands to distinguish more finely between properties with different values. The Welsh Government did not consult on more radical options, such as making the tax rates proportional to property value (rather than just a little less regressive) and moving away from a banded system altogether. One might reasonably (though debatably) argue that bringing valuations up to date after almost a quarter of a century is radical enough on its own, and further reform should be pursued only after that has been accomplished. But it will be for whoever is in power after May’s election to decide.

The current Welsh Government has not indicated any intention to follow England’s and Scotland’s lead by introducing a ‘mansion tax’ on the highest-value properties. But if the Welsh Government in power after the election did want to increase tax on high-value properties, it could do so simply by building it into the rate-band structure it chose for post-revaluation council tax. By virtue of doing a revaluation for all properties, it avoids the incoherent mess that England and Scotland are getting themselves into by revaluing the highest-value properties but not the rest. Scotland plans to levy council tax based on up-to-date values for properties now worth £1 million or more but continue to use 1991 values for everyone else, while England will be operating two property taxes in parallel – the existing council tax based on 1991 values and a separate new supplementary tax on properties currently worth £2 million or more. On council tax policy at least, Wales is in a far better place than the rest of Great Britain.

4. Land transaction tax penalises the rental sector

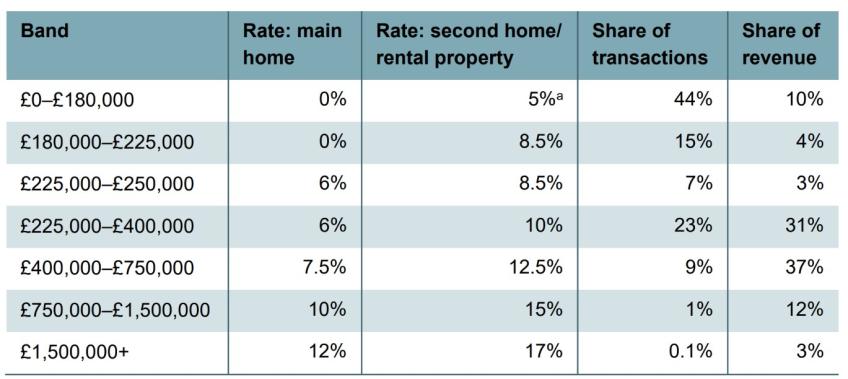

Land transaction tax (LTT) is a tax on property transactions. The rates and thresholds for residential property are shown in Table 4.9

Table 4. Rates and thresholds of LTT for residential property

Note: Rates apply to the part of the value in each band. Rates and thresholds shown have applied since December 2024; shares of transactions and of revenue are for 2024–25.

a Not payable if the purchase price is below £40,000.

Source: Shares of transactions and of revenue calculated by the authors from Welsh Government (2026c).

When the Welsh Government introduced LTT in 2018, like the Scottish Government in 2015, it chose rates that made the new tax more progressive than the non-devolved stamp duty land tax (SDLT) it was replacing. Less tax was payable on low-value property sales, and more tax on high-value property sales, than in England and Northern Ireland.

Greater progressivity

In October 2022, LTT was made even more progressive. The exemption threshold for main homes was increased from £180,000 to £225,000, while the marginal rate between £225,000 and £400,000 was increased from 5% to 6%. This meant a tax cut on purchases between £180,000 and £345,000 (the tax being reduced by a maximum of £1,575, on purchases for £225,000) and a tax rise above that (the tax rise reaching £550 on all purchases above £400,000).

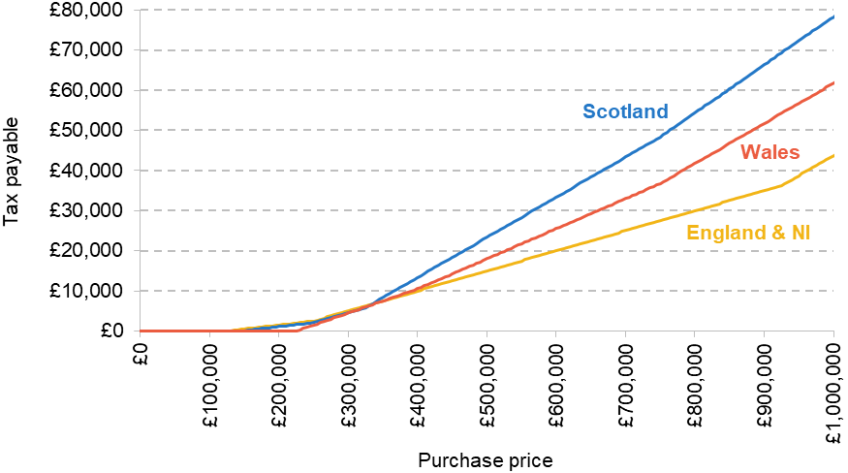

The result is shown in Figure 2. Housing purchases for more than £350,000 are taxed more heavily in Wales than in England, while purchases below that price are taxed less heavily in Wales – unless the buyer is a first-time buyer, as England has a hefty relief for first-time buyers while Wales has no such relief. The tax in Wales is lower than in Scotland for both low-value and high-value purchases.10

Figure 2. Tax on residential property transactions, main home purchases, 2025–26

Note: Rates shown apply where the buyer is not a first-time buyer and does not have another residential property.

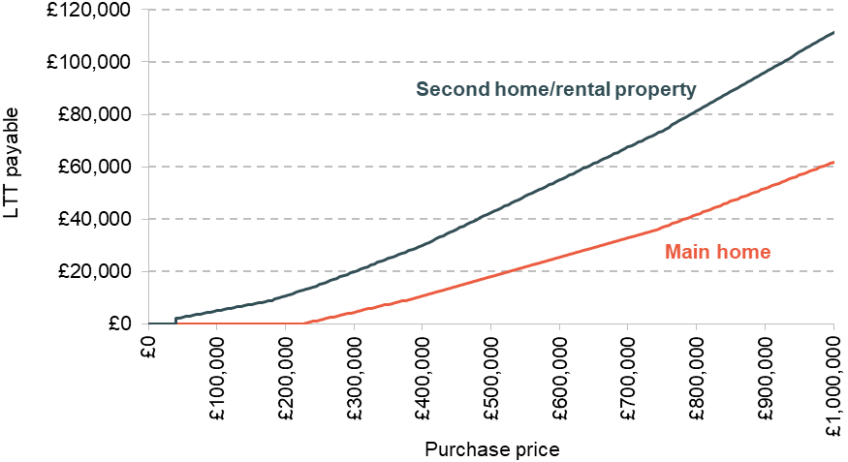

Second homes and rental properties

Figure 2 shows the tax payable when buying a property as one’s main home. As Table 4 and Figure 3 show, substantially higher tax rates apply to purchases of additional homes, as second homes or to rent out. The October 2022 changes to LTT rates and thresholds did not apply to such purchases, but the LTT rates on such purchases were increased by 1 percentage point in December 2024 (mirroring a similar, but bigger, increase in SDLT announced in Rachel Reeves’ first Budget that October). As with the main LTT rates, the surcharge for additional properties is smaller than in Scotland and more progressive than in England and Northern Ireland.

Figure 3. Land transaction tax on residential property transactions, 2025–26

Taxing property transactions is an exceptionally damaging way to raise revenue. It discourages mutually beneficial transactions, so properties are not owned by the people who value them most. This misallocation of property makes everyone worse off.

The difference between the tax payable when buying one’s main home versus an additional home is striking, as Figure 3 illustrates. A £225,000 purchase attracts no LTT if bought as one’s main home, but £12,825 – adding 5.7% to the purchase price – otherwise. Towards the top end of the market, a landlord buying a £500,000 property must pay £42,450, or 8.5%, in LTT on top of the purchase price (compared with £18,000, or 3.6%, if bought as an owner-occupier’s main home). Many will be put off by that.

This is true of rental property as well as owner-occupied property. Increasing the higher rates for additional properties has made a bad tax worse. Penalising the rental sector makes it cheaper and easier for people to move into owner-occupation; but it makes it even more difficult and expensive for those who remain in the rental sector – tenants (who are likely to face higher rents as a result of the policy) as well as landlords. Landlords must already pay income tax on their rental income and capital gains tax on any increase in the property’s value, neither of which applies to owner-occupiers. The case for tilting the playing field even further towards owner-occupation and away from rental is doubtful. But in any case, higher rates of LTT are a bad way to do it. They do not just penalise the rental sector; they penalise transactions within the rental sector. Preventing a landlord who wants to sell their property to another landlord from doing so is bad for both landlords and tenants.

Fundamental reform

Overall, in 2024–25 (the latest data available), the average tax bill across all housing transactions in Wales (purchases of main and additional properties at all prices) was £5,049.11 This is barely half of the £9,889 paid on average in England and Northern Ireland, although average property prices are also much lower in Wales than in England and Northern Ireland as a whole.12 However, the average tax bill in Wales is also significantly lower than the £6,467 seen in Scotland, despite Wales having slightly higher average property prices, because of the lower taxes applied to most transactions in Wales (and especially to the highest-value transactions and second home/rental properties).13 The average tax bill in 2024–25 was a substantially lower percentage of average sale price in Wales (2.2%) than in either England and Northern Ireland (2.7%) or Scotland (2.8%).14

So LTT in Wales is generally a lower tax than its equivalents in the rest of the UK. That is welcome. But given the damage it does, it is still too high – indeed, it would be better if it did not exist at all. As recommended by, among others, the Mirrlees Review of the tax system (Mirrlees et al., 2011) more than a decade ago, the Welsh Government and its counterparts elsewhere in the UK should reduce – or preferably abolish – the tax on property transactions, and make up the revenue by raising more from a reformed council tax and business rates. This would be fairer and more efficient. Making up the revenue through other property taxes would prevent the tax cut bidding up overall property prices and therefore being a giveaway to existing property owners. Another consequence would be to decentralise more of Wales’s revenue-raising to local authorities. The forthcoming reform (discussed in Section 3) to make council tax in Wales fairer by bringing the valuations up to date should be an opportunity to use this improved tax to do more of the work of revenue-raising instead of the damaging LTT.

5. Business rates policy takes the lead from Westminster

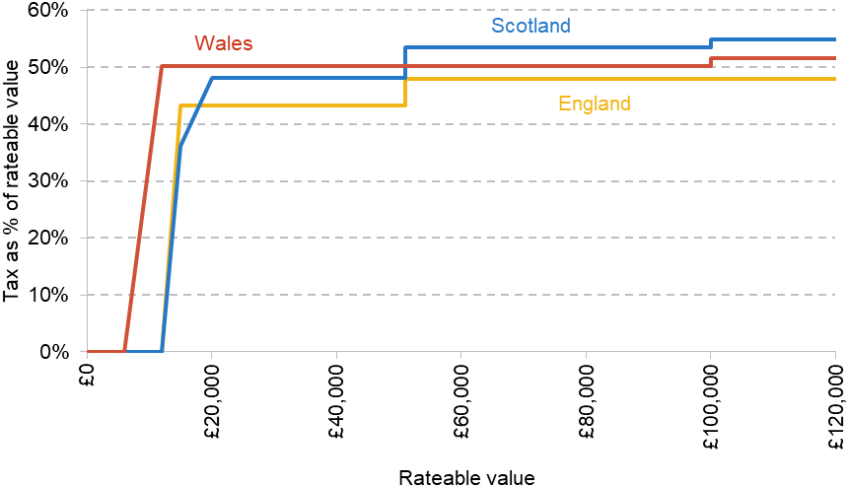

Business rates are a tax paid by firms on the estimated rental value (‘rateable value’) of the property they occupy. Figure 4 shows the standard rates of tax paid as a percentage of rateable value in Wales, Scotland and England.

Figure 4. Business rates schedules, 2026–27

Note: Assumes a business occupying a single property, not engaged in retail, leisure or hospitality, and ignores transitional arrangements associated with the 2026 revaluation. Schedule for England is that which applies outside London. Rateable value is estimated market rental value as of April 2024 in Wales and England and April 2025 in Scotland.

Since the last Welsh elections in 2021, the Welsh Government has steadily reduced average business rate bills in real terms: in most years, it has either frozen tax bills or increased them by less than inflation (on average).

Nevertheless, business rates in Wales remain higher as a share of rateable value than in England, where bills have also fallen in real terms.15 At present, they are also higher than in Scotland; but from 2026–27, as Figure 4 shows, they will be higher for properties with a rateable value below £51,000, but lower for properties worth more than that (only 7% of business properties in Wales, but accounting for the majority of business rates revenue).16, 17 The change is partly because commercial rents have increased more quickly in Wales (and England) than in Scotland, so the tax can be a lower percentage of property value to maintain revenue, even if average bills do not fall in real terms. It may also reflect differences in how expected valuation appeals are accounted for when adjusting the tax rate alongside property revaluations in 2026.

Variation in tax rates by property value

The small jump in the tax rate in Wales at rateable value of £100,000 visible in Figure 4 is new in 2026–27. Until now, the tax rate has been the same for all properties with rateable value above £12,000 (i.e. not eligible for small business rates relief). This was not a matter of choice: the Welsh Government did not have the power to introduce different tax rates. It acquired such powers in 2024, and is quickly making use of them. Mercifully, as Figure 4 shows, Wales still will not have the much bigger jump in tax bills at £51,000 of rateable value seen in England and Scotland, where properties with a £1 higher rateable value attract tax liabilities £2,448 (England) or £2,754 (Scotland) higher.

Whether considering the new, higher tax rate above £100,000 or the long-standing small business rates relief (which takes properties with rateable value below £6,000 – about half of the total – out of tax altogether, and reduces bills for another quarter which are between £6,000 and £12,000), the underlying rationale for varying the tax rate by property value is unclear. It is tempting to think of levying higher tax rates on high-value properties as akin to levying higher tax rates on high-income individuals, but the analogy is flawed. The people who ultimately bear the burden of a tax on business property – a combination of the tax-paying firms’ owners, employees, customers, suppliers and landlords – are not necessarily any better off for high-value properties than for low-value properties. Taxing high-value business properties does not necessarily affect better-off people more than taxing low-value business properties.

In fact, economic theory and the (limited) empirical evidence available suggest that business rates largely get reflected in rental prices in the long run (e.g. Bond et al., 1996; Cambridge Econometrics, 2008). Higher business rates reduce what potential occupiers are willing to pay for a property, and because the total supply of property is quite unresponsive to tax, the reduced demand forces landlords to accept correspondingly lower rents if they wish to find a tenant (though existing long-term rental contracts mean it can take some time for market rents to adjust in this way). Reduced business rates for low-value properties are therefore likely to benefit landlords primarily, rather than the small businesses occupying the premises.

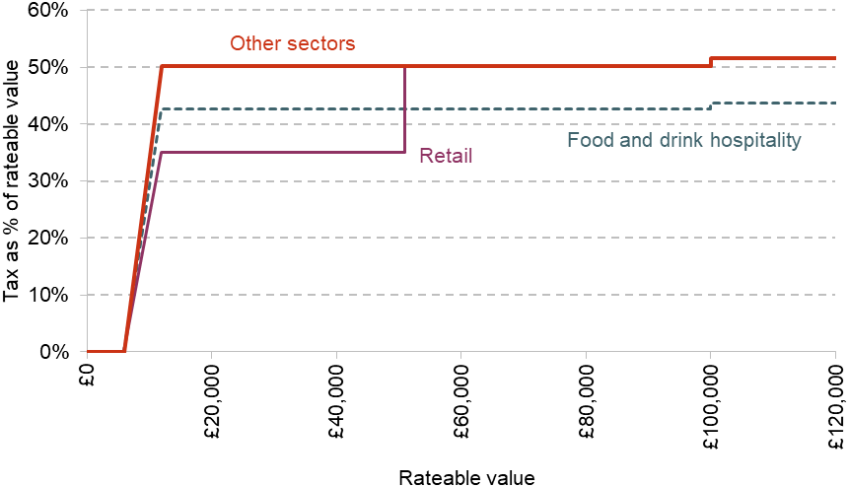

Retail, leisure and hospitality

The introduction of higher business rates above £100,000 is not the only change happening in 2026–27 to the structure of business rates (as opposed to merely bringing property valuations up to date). Figure 5 shows the business rates schedule applying to most businesses, but not the retail sector.

Figure 5. Business rates schedule in Wales, 2026–27

Note: Assumes a business occupying a single property, not affected by transitional arrangements associated with the 2026 revaluation. Rateable value is estimated market rental value as of April 2024.

Like England and Scotland, Wales provided much-needed relief from business rates for retail, hospitality and leisure businesses during the COVID-19 pandemic. Like England (though unlike Scotland), it continued providing relief even after the pandemic receded – but announcing this continued relief one year at a time, stating that it was ‘a temporary relief, which will not continue indefinitely’ (Welsh Government, 2024b). Outside the exceptional conditions of a pandemic, the case for providing relief on a temporary basis was never clear, and doing so repeatedly gave businesses no certainty of what to expect in the medium run.

From 2026–27, Wales – like England – is making the discount for retail properties permanent (though at a less generous level than its temporary predecessors). The discount for retail properties, shown in Figure 5, is more generous than its equivalents in England and Scotland for low-value properties, but it applies only up to a rateable value £51,000 (versus £100,000 in Scotland and £500,000 in England). Once these discounts are taken into account, shops in Wales will face lower business rates than in England or Scotland if they have a rateable value between about £14,750 (England) or £17,000 (Scotland) and £51,000, and higher business rates than in England or Scotland otherwise. The ‘cliff-edge’ withdrawal of support for retail at the £51,000 threshold is exactly the kind of anomaly that, as we noted above, Wales had done well to avoid in its broader business rates schedule. It is simply unfair that a shop worth £1 more than another can attract a business rates liability £7,752 (43%) higher.18 But whether or not the relief is well conceived and well designed, setting policy on a permanent basis rather than one year at a time helps to reduce uncertainty for businesses.

However, the new permanent relief – unlike its temporary predecessors, and unlike the equivalent reliefs in Scotland and Wales – will apply only to the retail sector, not leisure and hospitality. For the food and drink hospitality sector (including pubs, clubs and restaurants) – though not for other leisure and hospitality businesses – there will be yet another ‘temporary’ relief in 2026–27 (also shown in Figure 5), currently due to expire at the end of that year. This was announced only in February 2026, following a (roughly) similar announcement by the UK government for pubs and live music venues in England. In Wales as in England, this is a poor way to make policy. There is no reason to think that support for pubs and restaurants is justified in 2026–27 but not in 2027–28. The Welsh Government should either make the case for why such businesses should be subject to preferential business rates and make the policy permanent, or remove it.

Part of the benefit of preferential tax rates for the retail sector will flow to landlords in the form of higher rents as demand from (potential) retail tenants increases. The policy could nonetheless help to grow or sustain the retail sector, and if more property is used as shops (than would otherwise have been the case) as a result of the lower business rates, then the increased availability of premises could reduce property costs for retailers looking to occupy them – but only to the extent that the reduced availability of non-retail premises symmetrically increased property costs for businesses ineligible for the discount but which compete with the retail sector for properties.

The likely effect of the ‘temporary’ relief for food and drink hospitality is less clear-cut. If landlords and tenants expect the relief to expire as scheduled, then the supply of, and demand for, qualifying premises is unlikely to change much, and nor will market rents – so the relief is likely to be a straightforward giveaway to small pub and restaurant businesses. But the more that landlords and tenants suspect that the relief will be further extended and eventually become a permanent part of the system, the more market rents will be bid up, passing the benefit of the relief on to landlords. And if the relief is then unexpectedly withdrawn, small pub and restaurant businesses would be left with both higher rents and no tax relief: worse off than if the relief had never been introduced in the first place.

While there are concerns about the health of high streets, the principled case for promoting greater use of property for retail (and perhaps hospitality) purposes at the expense of other uses is not clear. Perhaps bricks-and-mortar retail has benefits to wider society beyond what the market will recognise (though no doubt other sectors could make such a claim too), and perhaps reducing the tax on retail property use is the best way to promote the sector (though there are other, more natural candidates); or perhaps, if online shopping and other changes in technology and tastes mean that people are less inclined to spend their money in physical shops than in the past, the sector should be allowed to shrink.

Fundamental reform

The fundamental problem with business rates is not that they increase the cost of premises for the firms occupying them: as we have explained, the burden is mostly passed on to landlords, even if tenants do not realise that their rent would be higher if they did not have to pay business rates. Rather, the problem is that, by reducing property values, business rates reduce the incentive to develop and use property for business at all, making it scarcer and somewhat increasing the cost of premises for all firms.19 The effect of business rates on discouraging the development and use of business property could be removed almost completely by replacing business rates with a land value tax, levied on the value of land excluding any buildings on it.20 In recent years, the Welsh Government has commissioned several pieces of research to examine in detail the feasibility of moving to a land value tax (for both business and residential property) and what would be required to achieve it; see ap Gwilym, Jones and Rogers (2020) and Welsh Government (2025f). That is an encouraging first step.

6. New taxes and the options for further devolution

The current Senedd term has seen no further tax devolution to Welsh Government. However, the Welsh Government has used its existing powers over local taxation to legislate to allow councils to set and retain ‘visitor levies’ on overnight visitor accommodation, discussed in Box 1.

The visitor levy

In 2025, the Senedd gave powers to local councils to introduce a visitor levy (sometimes called a ‘tourism tax’, though it applies to business trips, etc., as well) on overnight visitor accommodation from April 2027. If, following consultation, a council decides to impose a visitor levy, it will charge a fixed rate of 75 pence per person per night for campsites and shared rooms in hostels and dormitories, and £1.30 per person per night for all other accommodation, including hotels, B&Bs, self-catering accommodation and caravan parks; see Welsh Government (2026d) for more details. So far, Cardiff is the only council to propose introducing a visitor levy (Cardiff Council, 2025). Its consultation finished on 6 March 2026, and it will announce by the end of the month whether it will go ahead with the levy from April 2027.

The visitor levy gives councils an additional revenue-raising option. But that on its own is not a good reason to levy a tax specifically on overnight visitors rather than on anything else.

One argument for a visitor levy is that the tax reflects costs (‘negative externalities’) that visitors impose on an area – whether that is the cost to councils of providing additional services or costs imposed directly on local residents such as via litter and congestion. A subtly different argument is that visitors should make a contribution towards the local service provision they enjoy (a ‘benefit tax’), regardless of whether the cost of service provision is higher as a result of their presence. A visitor levy can also give councils a more direct financial stake in attracting visitors to the area.

Of course, there are counterarguments too. Visitors can bring benefits to an area, not just costs. Taxing overnight stays discourages spending on tourism and business travel relative to spending on other things that may be no more valuable – and discouraging economic activity comes at a cost in revenue from other taxes (such as VAT and income tax), which would be felt by the UK and Welsh governments, not the council making the decision. The administrative and compliance costs of the tax may be significant relative to the modest revenue it could raise. And the policy allows councils to tax people who do not have a vote in the area – potentially politically attractive precisely because it is a form of taxation without representation. The tax burden would not necessarily fall entirely on visitors, however: those who run and work in the visitor economy – many of whom will be local residents – would also be affected, and might lobby and vote accordingly.

There is some logic to this being a local tax, as voters/policymakers in different places may take different views as to the costs and benefits of visitors to the area and whether they want to encourage or discourage visitors. Indeed, if that is the rationale for making the tax local, there is a case for giving councils more flexibility to set the level of the tax and to vary it by (for example) time of year, location and type of accommodation, to allow them fine-tune the tax to local circumstances and preferences. However, greater variation of that kind would add to the complexity of the tax. And there is certainly a case for capping, if not dictating, the tax rates that councils can set, in order to limit the extent to which they can raise revenue at the expense of non-residents and the UK and Welsh governments.

Making the tax a flat cash amount per person per night was an improvement on Scotland’s visitor levy, which requires councils to levy the tax as a percentage of the bill (though legislation is currently passing through the Scottish Parliament which, if passed, will allow Scottish councils to charge a flat cash amount per person per night too). The core reasons given above for taxing visitors – the costs they impose and the public services they benefit from – are not obviously bigger for more expensive accommodation, so charging a flat charge per person per night makes more sense than charging a percentage of the accommodation cost. The most common argument for a proportional tax – that it is more progressive – is weak. It is the progressivity of the tax and benefit system as a whole that matters: not every tax needs to be progressive, and there are much-better-targeted tools available (such as income-related taxes) if the Welsh Government wants to make policy more progressive, rather than taxing well-off travellers more than well-off non-travellers. A flat charge also avoids some complications such as the need to separate out the cost of the accommodation from the cost of any other services that might be bundled in with it.

The current Welsh Government has also recently announced that it is resurrecting a request to the UK government for the power to levy a tax on land with planning permission but where development has failed to commence after several years – the so-called vacant land tax. The Welsh and UK governments have agreed to undertake a joint consultation on this, after the previous UK government rejected the evidence base the Welsh Government previously put forward (Senedd Research, 2024; Welsh Government, 2026e). Such a tax could help to address one concern with the current tax system: the fact that property taxes (council tax or business rates) currently become payable only once a property is ready for occupation can discourage the commencement of development and completion of properties (including encouraging ‘land banking’). However, taxing only land with planning permission rather than all land merely pushes the problem to another place – discouraging the submission of planning applications until development timelines are clearer, and for developments that are made unprofitable by tax. A better approach would be to tax the value of undeveloped land regardless of planning permission, to level the playing field with build-on land (which is subject to council tax or business rates) and therefore reduce the tax disincentive for development. As highlighted in Section 5, the Welsh Government has commissioned research and consulted experts on the feasibility of land value taxation.

In assessing the options for the devolution of existing UK government taxes, it is first worth noting the general pros and cons of tax devolution.21 The possible advantages include:

- tailoring tax policy to preferences and circumstances in Wales, which may differ from those elsewhere in the UK;

- the ability to integrate the newly devolved taxes better with tax and other policies that are already devolved;

- stronger financial incentives for the Welsh Government to boost the economy as a result of the additional revenue retained.

The potential drawbacks include:

- higher administration and compliance costs when tax rates and rules differ in different parts of the UK;

- the potential for taxpayers to respond to differences in tax policy by shifting the actual or reported location of their taxable activities, in turn incentivising tax competition between different parts of the UK;

- risk to Welsh Government finances as a result of greater exposure to relative rises and falls in economic performance when more of the Welsh Government’s funding depends on devolved tax revenues.

The balance between these pros and cons depends both on the specific taxes in question and on the powers already devolved to the Welsh Government. The current Welsh Government has itself commissioned analysis of the options for the further devolution of income tax, but has not indicated a preference to devolve other taxes such as NICs, indirect taxes or corporation tax. Some other parties are more keen on tax devolution though (e.g. Plaid Cymru, 2024).

A full assessment of the options is beyond the scope of this report. Here instead, we provide a summary of the key points.

- The case for devolving the power to set income tax rates for savings and dividends income is perhaps strongest. Doing this would allow future Welsh Governments to apply their tax rates to all taxable income. This would avoid the horizontal inequities that could arise under the current system – with those whose income comes from dividends or savings neither gaining or losing like their compatriots from Welsh Government income tax changes. In turn, this would also help close off one way individuals could respond to potential future changes in Welsh Government tax policy – setting up a company and receiving their income in the form of dividends rather than earnings. However, the ability of company owners to retain income within their companies – potentially for years – rather than pay it out immediately as dividends would expose the Welsh Government to another potential avenue for tax avoidance that it does not currently face (the employees and self-employed individuals currently subject to Welsh income taxes cannot shift income over time in this way).

- Devolving powers over income tax bands would enable the Welsh Government to more finely tune the distributional effects of income tax policy. However, care would need to be taken to avoid overcomplicating the tax rate structure – there are better options than the politically driven splitting of the basic rate band into three bands (starter, basic, intermediate) that the Scottish Government chose to do.

- Devolving a greater share (or all) of income tax revenue to Wales would create stronger financial incentives for the Welsh Government to grow the tax base but would also increase budgetary exposure to income tax revenue risk.22 As it stands the Welsh Government only bears part of the gains and losses from changes in the Welsh income tax base. For example, with the Welsh rate of income tax at 10%, it bears half of the effect of changes in the basic rate tax base (with the UK government’s Welsh basic rate of 10% meaning it bears half too), and a quarter of the effect of changes in the higher rate tax base (with the UK government’s Welsh higher rate of 30% meaning it bears three-quarters). Compared with full devolution of income tax revenues, the current situation therefore entails weaker financial incentives for the Welsh Government to grow the income tax base, but also lower exposure to income tax revenue risks. This partial exposure to changes in the income tax base also affects the incentives the Welsh Government faces when setting income tax rates. In particular, while it bears the full ‘mechanical’ revenues effect of changes in the Welsh rates of income tax, it only bears part of the effects of any behavioural responses to changes in tax rates on the income tax base – part is borne by the UK government as a spillover effect on its share of the income tax base. This could encourage the Welsh Government to set higher rates of tax (especially for the higher and top rates of tax where both behavioural responses are larger and it bears a particularly small part of changes in the income tax base) than it would if income tax revenues were fully devolved.

- Devolving powers over NICs would allow future Welsh Governments to, for example, align NICs thresholds with any changes they make to income tax thresholds (if such powers are also devolved to the Welsh Government). This would allow Wales to avoid the situation Scotland finds itself in, with a combined income tax and employee NICs rate of 50% between the Scottish higher rate threshold (£43,662) and UK higher rate threshold and NICs upper earnings limit (£50,280), which then drops back to a combined rate of 44% above £50,280 (because the NICs rate drops from 8% to 2% at the upper earnings limit). It is possible to avoid such situations without the devolution of NICs, but doing so requires adding extra income tax rates (for example, a 36% rate on incomes between £43,662 and £50,280 so that the combined income tax rate and NICs also equals 44%).

- Depending on the scope of powers devolved on the rates and base of income tax, NICs and capital gains tax, future Welsh Governments might be able to make more fundamental changes to how different forms of income are taxed. For example, it might be possible to equalise overall tax rates across different forms of income (employment, self-employment, dividends, capital gains) while also reducing disincentives to save and invest. This would result in both a more efficient tax system – with less distortion to taxpayer behaviour – and a fairer tax system – by removing many of the arbitrary (and large) differences in tax rates faced by people receiving their income in different forms. However, such reforms would create many losers as well as winners, and this may discourage a future Welsh Government from pursuing reform (as it has perhaps discouraged the UK government). The current Welsh Government has made progress in reforming council tax and shown interest in wider property tax reform, but wholesale reform of the taxation of income would be much more complex, and create more big losers than reform of property taxation (as well as many winners).

- Devolving VAT to the Welsh Government would require major changes to the operation of the tax, raising administration and compliance costs. It is therefore less suitable for devolution than the aforementioned taxes, although if Welsh preferences over VAT rates and policies differ significantly from preferences in the rest of the UK, it could still be considered. Part of the challenge in devolving VAT would be due to the difficulty of apportioning value-added between different activities conducted by a single business (such as their warehouses, shops, headquarters, websites and support operations) that has operations in both Wales and the rest of the UK. But it would also reflect the way VAT works: it is charged on sales, but businesses can deduct the VAT they have paid on their inputs. Devolved VAT could therefore mean businesses not only having to charge different VAT rates in Wales and the rest of the UK, but having to record where their input purchases came from, as different amounts of input VAT would be deductible based on this. Alternatively, borders between Wales and the rest of the UK could be treated like international borders for the purpose of VAT: businesses ‘exporting’ to/from Wales would charge a 0% rate on their ‘exports’ to other businesses. This would avoid the need for businesses elsewhere in the UK to keep track of Welsh rates of VAT (anything ‘imported’ from Wales would be zero-rated), and vice versa. But businesses would have to keep track of whether their customers were VAT-registered businesses and, if so, where they were based, in order to work out whether VAT should be charged or zero-rating applied in the first place, which would also entail costs and potentially be more open to fraud.

- Devolving excise taxes (such as for alcohol, tobacco or fuel) would, in principle, be more straightforward than for VAT (as these taxes are not subject to the same output taxation and input tax deduction mechanism). Devolved taxes on alcohol and tobacco could be aligned with the Welsh Government’s approach to public health – with, for instance, higher alcohol duty for off-licence (as opposed to pub and other hospitality venue) sales being used in place of the minimum unit price. But devolution would still increase administration and compliance costs given excise duties are currently collected at production and import stage, rather than at the retail stage. And substantial difference in excise duty rates could lead to distortions to the location of sales – with cross-border shopping (e.g. such as between Northern Ireland and Ireland).

- Devolving corporation tax to Wales would, as with VAT, entail significant additional compliance and administration costs, with businesses having to allocate profits between Wales and the rest of the UK, and tax authorities having to assess the validity of these allocations (especially if tax rates varied between Wales and the rest of the UK). Profits could be allocated between Wales and the rest of the UK either on the basis of detailed accounts of revenues and costs in each jurisdiction, or on the basis of a simplified formula based on, for example, the location of fixed assets, employment and/or sales. The former (separate accounting) approach would be most prone to profit-shifting, whereas the latter (formula apportionment) approach would most prone to distorting the location of real economic activity, if rates differed between Wales and the rest of the UK. More detailed assessments of these options can be found in the final report of Fiscal Commission NI (2022) – which, while written from the perspective of Northern Ireland, includes a discussion of the pros and cons of devolving each tax from a first principles basis.23

7. Limited powers and minor changes to Welsh benefits

Unlike Scotland, where tax devolution has been accompanied by devolution of significant powers over parts of the benefit system, the Welsh Government has direct powers over only a few, relatively small benefits. Social security is broadly reserved to the UK government. In this section, we discuss the limited range of benefits over which the Welsh Government does have control, which it refers to as the ‘Welsh benefit system’. We then evaluate the broad direction of policy in Wales so far, and how the devolution settlement, in its current form, could facilitate further changes to benefits policy.

The Welsh benefit system

The largest Welsh benefit is the Council Tax Reduction Scheme (CTRS). This is a means-tested benefit that reduces low-income households’ council tax bills by up to 100%. Those with no income other than benefits (and no savings) will typically receive a full reduction, and the reduction is then gradually withdrawn as income and/or savings rise.

The CTRS in England has been controlled by councils rather than central government since 2013–14, at which time central government funding in England for council tax support was reduced. In Wales, the generosity and targeting of the CTRS is almost entirely determined by Welsh Government rather than councils. The Welsh CTRS is estimated to cost £314 million in 2025–26 (Welsh Government, 2025a), and on average provides larger reductions than English local schemes would (Oulton and Wernham, 2026).

The Welsh Government also has broad powers to fund and direct smaller council grants to poorer households. These include schemes such as discretionary housing payments (DHPs),24 which can be made by councils to contribute to housing costs on top of means-tested benefits, and the discretionary assistance fund. The discretionary assistance fund provides one-off payments for those who, due to an emergency, may be unable to pay for essentials. It also provides payments to help with purchases of furniture and appliances, for households in receipt of benefits and lacking savings or credit.25

The Welsh Government also considers other devolved payments and grants as part of its benefit system. For example, it controls:

- the education maintenance allowance – a grant supporting 16–18 year olds from low-income families to remain in education (with no English equivalent since it was abolished in England in 2011);

- the school essentials grant – nationally standardised means-tested grants aimed at helping pay for uniforms, stationery and equipment (which in England instead depend on the policies of individual councils);

- free school meals – which are available to all primary school children, and are means-tested for secondary school children (whereas, in England, coverage is only universal for children in reception to year 2 of primary school, and means-tested for years 3 and above).

Direction of Welsh policy

A clear objective of Welsh Government policy so far has been to increase the generosity of the benefits over which it has control. The largest cash benefit – CTRS – is more generous than most of its counterparts in England; the education maintenance allowance has been retained, while in England it was scrapped; and free school meals are more widely available than in England – though no plans have been announced so far to extend eligibility among secondary students, as has been announced in England from September 2026.26

The Welsh Government has also sought to standardise locally delivered support between councils, and to increase take-up of both Welsh and UK-wide benefits. They have adopted a ‘Welsh Benefits Charter’ focused on integrating application processes for these benefits and improving take-up (Welsh Government, 2024c), and have established the Streamlining Welsh Benefits Steering Group to coordinate the implementation of this charter (Welsh Government, 2024d). This group has commissioned work exploring options to streamline administration and identify residents potentially missing out on benefits (Welsh Government, 2025c). Proposals include single application points and common communications for Welsh benefits, and improved data sharing between councils.

The Welsh Government has also commissioned work exploring the feasibility of further devolution of administration of UK-wide benefits (Sell 2 Wales, 2025). This could permit more reforms to smooth application processes and increase take-up, including by increasing access to data on benefit recipients. But it is unclear whether the UK government would be willing to devolve responsibility for administration, without also devolving some responsibility over funding and spending as well.

This would affect the risks and financial incentives faced by the Welsh Government. For example, if changes to application processes led to higher take-up (something the Welsh Government explicitly wants) and/or increased rates of fraudulent applications (which could be an unintended consequence of making application processes easier for applicants; e.g. with fewer documentation requirements or verification checks), this cost would be borne by the Welsh Government. Similarly, if changes in households’ demographic or socio-economic characteristics relevant to benefit eligibility evolved differently in Wales compared with England, the Welsh Government would bear the risk of this. In contrast, exposure to increases or decreases in benefit expenditure would mean the Welsh Government gained more financially if its other policies (such as on health or skills) reduced demand for certain benefits. Significant devolution of benefit administration therefore likely only makes sense as part of a broader package of powers over benefits policy and responsibility for benefit spending.

Powers for further changes

Looking forward, the next Welsh Government could also expand devolved benefit provision further under current powers, although the current devolution settlement limits the form such policies could take. It does not have flexibility to offer broad and centrally administered top-ups to UK benefits such as universal credit in the way the Scottish Government can – the Wales Act 2017 explicitly forbids the Welsh Government from providing ‘social security’.

The Wales Act 2017 does, however, make an exception in allowing the Welsh Government to direct councils to provide financial assistance to households, to meet needs for support that the councils might otherwise wish to provide. It also does not preclude the provision of financial assistance for reasons beyond ‘social security’, for example in devolved areas such as education or childcare, or in relation to local taxes. Moreover, the Government of Wales Act 2006 also allows ministers to act broadly to improve the ‘economic well-being’ or ‘social well-being’ of the people of Wales.

This means the devolution settlement gives the Welsh Government significant scope to extend financial support to households, if it so wishes. This power has been exercised through policies described in the previous subsection, and also previous temporary and ad hoc policies. These include the fuel support scheme in 2022–23, which provided one-off means-tested grants through councils to help with high energy costs (on top of support provided by the UK government), and a trial of a ‘basic income’ for care leavers.

Further options to provide ongoing support may be available, for example by the use of DHPs, which may be used to support households with their housing needs. In Scotland, these are used to mitigate two UK benefits policies that cut the universal credit entitlements of some households receiving support for housing costs: the under-occupancy charge (sometimes known as the ‘bedroom tax’) and the benefit cap.

But the Welsh Government must overcome many administrative and legal obstacles to provide such additional support. These include ensuring payments are deemed equivalent to ‘local welfare provision’ by the UK government, so they do not result in additional tax liabilities or withdrawal of UK benefits. This is crucial, because universal credit is tapered away at 100% as unearned income rises – so if the UK government considered a Welsh payment to be ‘unearned income’, recipients who were also receiving universal credit would in fact gain nothing, as universal credit would be reduced pound-for-pound.

Any Welsh payments must also comply with other legal limitations of the Welsh devolution settlement. In particular, regular weekly or monthly payments that might be considered top-ups to ‘social security’ are not permissible, unless these are considered equivalent to local welfare provision, such as CTRS, DHPs or the household support fund. It is unclear whether regular payments analogous to the Scottish child payment, such as the Cynnal (or Welsh child payment) which Plaid Cymru (2025) has proposed, would be allowed under the current framework. Whether or not there is appetite for further devolution of power over benefits, there is clearly scope for further clarity on how far the Welsh Government’s powers over benefits extend.

8. Concluding remarks

In different areas of tax policy, the Welsh Government has been both a follower and leader within the UK. On LTT and business rates, recent Welsh policy has often followed England: on LTT, increasing the higher rates for additional properties in late 2024; and perhaps most strikingly on business rates discounts for retail, hospitality and leisure – extending the relief year-by-year after the pandemic, then making it permanent from 2026–27 (albeit only for retail, in Wales), with an additional one-year relief for pubs added after the UK government did so in early 2026. Council tax has been a different matter. Giving local councils the power to charge a council tax premium on second homes is a Welsh policy recently adopted in England and Scotland too. The Welsh Government has proved more willing to tackle council tax reform than either the UK government or Scottish Government. The system in Wales is already somewhat less antiquated, and the reforms legislated for during this Senedd term will make further improvements – especially with respect to regular revaluations. We can only hope that the UK and Scottish governments follow suit on that. Their ‘mansion taxes’ are a poor substitute for genuine revaluation and reform.

Overall, there has been much less divergence from the English tax and benefit system in Wales than there has been in Scotland. However, the Welsh Government’s tax and benefit powers are much more limited than those of the Scottish Government. The Welsh Government has suggested it would like to raise more revenue through income tax, but has chosen not to do so, because the devolution settlement means that raising substantial revenue would require either increasing the bills of even the lowest-income taxpayers (by increasing the basic rate), or by large increases in the higher and additional rates of tax. On benefits, the Welsh Government has increased the generosity of several of the small parts of the system it has control over. It could go further in some areas – for example, through more targeted use of discretionary housing payments, as in Scotland – but the current devolution settlement does reserve the general power to create and vary ‘social security’ benefits to the UK government.