As well as setting spending plans, next month’s Scottish Budget will also set the rates and bands of Scotland’s devolved taxes for 2025–26. Moreover, alongside the Budget, the Scottish Government has said it will publish a tax strategy setting out its high-level approach to tax policymaking.

A key part of its strategy so far has been to increase the income tax paid by those with above-average incomes in order to raise revenue and increase the progressivity of the tax system. In the run-up to the Budget and tax strategy, where the Scottish Government faces a choice about whether to continue with this approach, it is worth asking: ‘What do we know about the impact of these changes?’.

Tax increases on higher earners amount to up to 7% of net income

The Scottish Government’s income tax powers apply to income other than from savings and dividends (to which UK government tax rates still apply). It began to use its powers as soon as it could vary tax bands as well as existing tax rates in 2017–18:

- It increased the higher-rate (40%) threshold by much less than the UK government did between 2017–18 and 2021–22.

- It split the basic-rate (20%) band into starter-rate (19%), basic-rate (20%) and intermediate-rate (21%) bands, and increased the higher rate (from 40% to 41%) and top rate (from 45% to 46%) in 2018–19.

- It further increased the higher rate (to 42%) and the top rate (to 47%) in 2023–24, while following a UK government decision to reduce the top tax threshold from £150,000 to £125,140.

- It introduced a new ‘advanced’ rate of 45% on incomes between £75,000 and £125,140, and again increased the top tax rate (to 48%) in 2024–25.

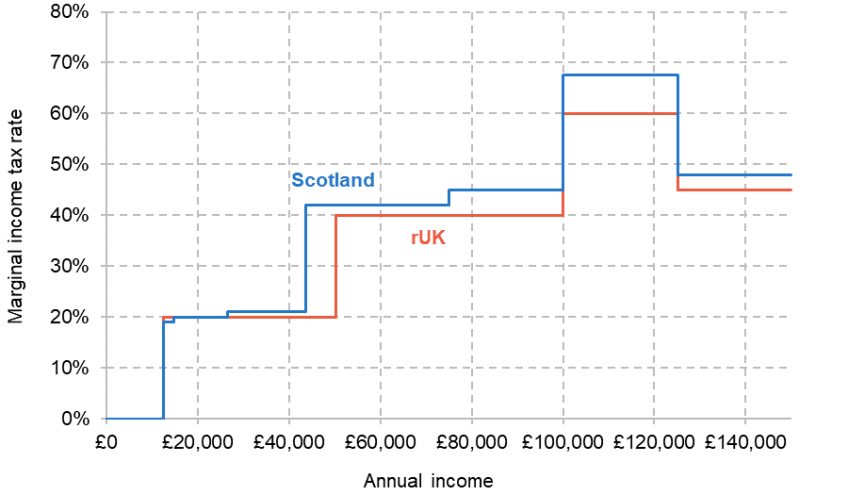

This has led to an increasingly complex income tax schedule in Scotland, with those with an annual income of more than £26,562 facing higher marginal tax rates than in the rest of the UK, as can be seen in Figure 1. The complexity introduced by having 19%, 20% and 21% is particularly unwarranted: for example, a small 0% band followed by a 21% band would be simpler and a little more progressive.

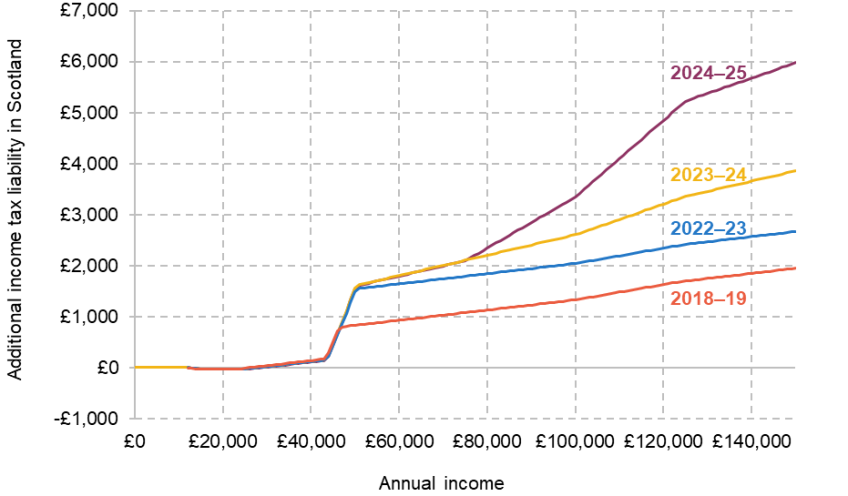

The higher marginal rates on income above £26,562 also mean that middle- and higher-income residents of Scotland pay more income tax than those in the rest of the UK (rUK), as illustrated in Figure 2.

- A taxpayer with an income of £25,000 pays £23 a year less in Scotland than in rUK.

- A taxpayer with an income of £50,000 pays £1,540 a year more in Scotland than in rUK, down from £1,552 last year, but up from £1,489 in 2022–23 and £830 in 2018–19.

- A taxpayer with an income of £100,000 pays £3,346 more in Scotland than in rUK, up from £2,606 last year, £2,043 in 2022–23 and £1,330 in 2018–19.

The biggest proportional difference in income tax liability is for those near the threshold between the advanced and top tax bands. For example, a resident of Scotland pays £5,221 more tax than in rUK if their income is £125,000 – equivalent to a 7% reduction in after-tax income, up from about a 2% reduction in 2018–19, when tax policy first started to diverge notably.

Figure 1. Income tax marginal rate structure in 2024–25, Scotland and rUK

Figure 2. Difference in income tax liability between Scotland and rUK

Note: Assumes all income is non-savings, non-dividends income.

How might these reforms affect taxpayer behaviour?

We would expect these tax policy changes and differences between Scotland and rUK to affect taxpayers’ behaviour, with potential implications for the wider economy.

Higher marginal rates and lower take-home pay may affect residents’ labour supply – by reducing the benefit from working overtime or securing a better-paid job, for example. They may lead to increased (illegal) evasion or (legal) avoidance as taxpayers seek to reduce their tax payments – by doing more cash-in-hand work, paying more into a tax-advantaged pension scheme, or incorporating and taking income in dividends (taxed at UK government rates). They may also affect migration, with those who would be affected being more likely to leave Scotland and less likely to move to Scotland. The fact that there may be other factors attracting high-income people to Scotland (e.g. lower housing costs, a wider range of universal public services) could mean net migration is still positive but does not mean tax policy has no effect – those other factors existed before, and higher taxes have not been used to enhance these factors further (instead being used to offset weak underlying tax base growth and increase benefit payments for lower-income households).

What does the Scottish Fiscal Commission assume about potential impacts?

However, the scale of such effects is highly uncertain, and difficult to investigate – because we need an estimate of how behaviour would have evolved in the absence of the tax changes.

In advance of tax policy changes coming in, the Scottish Fiscal Commission (SFC) needs to make assumptions about the scale of behavioural responses and how this would affect the revenue raised, in order to make revenue forecasts. It separately models responses to changes in tax rates (including labour supply, evasion and avoidance) and to differences in tax rates compared with rUK (intra-UK migration). It assumes very little response for those with an income below the higher-rate threshold, with progressively larger responses among those on higher incomes. For example, the response to a change in marginal tax rates by someone with an income over £500,000 is assumed to be over twice as large as for someone with an income of £150,000 to £300,000, and 7.5 times as large as for someone with an income between the higher-rate threshold and £80,000. These assumptions are based on a review of evidence from the UK and internationally, which finds qualitatively similar patterns: high-income individuals typically have more scope, and more of an incentive, to change their affairs to avoid higher taxes.

Based on these assumptions, the costings published alongside the most recent increases in Scotland’s income taxes imply that behavioural responses will offset approximately half of the revenue that would otherwise be raised by the ‘advanced’ rate of 45% (£73 million out of £147 million in 2024–25, for example), and around 85% of the revenue that would otherwise be raised by the increased top rate of 48% (£45 million out of £53 million in 2024–25). However, the SFC highlights the significant uncertainty around its behavioural assumptions and the resulting revenue impact estimates.

What do we know about actual impacts?

Concrete quantitative evidence on the actual impact of Scotland’s income tax policy changes is limited, but HMRC has published two studies focusing on the initial 2018–19 reforms.

The first looks at how changes in marginal tax rates affected the reported incomes of those working in Scotland pre- and post-reform. It estimates that top-rate taxpayers reduced their declared income by between 0.52% and 0.77% for every 1% reduction in how much of an extra pound of income a taxpayer retains after tax (the marginal retention rate or MRR), depending on the precise methodology used. Estimates for higher-rate taxpayers were instead clustered around 0.3–0.4% for every 1% reduction in the MRR, with little evidence of any effect for those with incomes below the higher-rate threshold.

This pattern is qualitatively as expected and assumed beforehand by the SFC, although the size of the estimated effects is a little larger, especially for higher-rate taxpayers. However, the statistical margins of error around the estimates are wide and overlap with the assumptions made by the SFC, which has therefore chosen not to update its assumptions.

The second HMRC study looks at how changes in average tax rates affected labour market participation and migration. For those remaining in Scotland, it finds no evidence of reduced labour market participation – perhaps unsurprising given the relatively small scale of tax changes in 2018–19 and the big reduction in income that leaving the labour market would entail for most affected taxpayers. It does find a reduction in net migration to Scotland, though, with the largest responses among those with the very highest incomes. For example, the estimated response is equivalent to a 2.56 percentage point increase in the likelihood of a taxpayer with an income of £500,000 or more leaving Scotland for every 1% reduction in how much of their overall income they retain after tax (the average retention rate or ARR). This compares with between 0.19 and 0.44 percentage points for others with incomes over the higher-rate threshold.

These estimates are again somewhat higher than the SFC assumed in its costings (and continues to assume) and equate to a net movement of around 1,000 taxpayers and £61 million of tax receipts from Scotland to rUK – although again HMRC notes wide margins of error. Somewhat surprisingly given that we would expect it to take time for migration responses to play out, this effect all takes place in 2018–19, with no evidence of impacts just one year after the reforms in 2019–20. This raises the possibility that estimates for both years are picking up some other factor as opposed to the tax changes in Scotland, in addition to the usual health warnings about wide statistical margins of error.

Overall, then, the available quantitative evidence suggests important behavioural responses to Scotland’s higher marginal and average income tax rates for those with the highest incomes – potentially a bit larger than assumed in the SFC’s policy costings. Indeed, the central estimates of behavioural response from HMRC’s two studies would suggest that previous increases in Scotland’s top rate of income tax will have slightly reduced revenues rather than slightly increased them as the SFC’s assumptions imply.

But as well as being subject to wide margins of error, this evidence only relates to the first, modest changes in income tax in Scotland. Responses to the bigger differences in policy that have since developed may differ: perhaps many taxpayers had already changed their affairs, so the additional effect of subsequent changes has been smaller; alternatively, perhaps the bigger differences mean it is more worth incurring the costs of adjusting behaviour, so impacts are larger.

Unfortunately, evidence on the more recent effects of Scottish income tax policy decisions is sparse indeed.

HMRC has published another study looking at the overall cross-border migration of taxpayers between Scotland and rUK, and vice versa, which covers the period up to 2021–22 – several years after income tax divergence began, but before the biggest differences emerged. This finds an increase in net migration to Scotland during the period since tax policy started to diverge, including among the higher-income taxpayers whose taxes have increased in Scotland.

Wales has seen a similar trend and internal migration statistics suggest that more rural and more affordable areas of England have also seen an inflow of taxpayers and taxable income. So this is not a Scotland-specific trend. But these data do suggest that any migration response to Scotland’s higher taxes was not big enough to offset fully other factors driving inflow of taxpayers – at least up to around 2½ years ago.

Other published evidence is limited to a number of surveys.

The Fraser of Allander Institute recently found mixed views from businesses, with roughly one-third reporting no impact of Scotland’s higher rates of income tax on their business, one-third reporting a small impact, and one-third reporting a fair amount to a lot of impact. Key issues identified include recruitment and retention, wage pressures, and resulting impacts on competitiveness and investment, although some businesses argued the increases helped support long-standing policies such as free higher education that are attractive to highly skilled workers. The Institute of Directors Scotland found more concern, with just over half expressing serious concern and a quarter slight concern about income tax policy divergence, with less than one in seven expressing no concern. Issues raised were similar to those in the Fraser of Allander survey.

However, such surveys, while useful in highlighting businesses’ views of income tax policy, do not quantify the scale of any impacts on recruitment, retention or investment.

What can we learn from evidence from other countries?

As mentioned, the SFC’s assumed behavioural responses draw on both UK and international evidence on the nature and scale of responses to income tax rates. Given that business concerns focus particularly on the divergence in tax rates with respect to rUK, it is worth considering what lessons can be learned from other countries with intra-country variation in income taxes.

The key finding is that while such differences do appear to affect migration, the scale of effects varies a lot across countries and for different types of taxpayers. Overall migration responses to variations in tax appear to be larger when policy varies over smaller geographical areas such as Swiss cantons (see here and here) than larger areas such as US states (see here, although recent research from California finds bigger effects) – which makes sense as it is typically easier to move smaller distances. We might therefore expect migration to/from areas near the Scotland/England border to be more affected by tax policy than areas in the north of Scotland.

Impacts appear higher than average for certain groups of the population such as inventors and those who were originally from outside the relevant jurisdiction (see here and here). These findings suggest that attracting and retaining people from outside Scotland, as well as researchers, inventors and other groups in which moving for work is more common, is likely to be more affected by income tax policy than retaining groups with more attachment to Scotland.

Perhaps most relevant overall for Scotland is evidence from variation in tax rates across the regions of Spain. This suggests a degree of response roughly in line with the aforementioned estimates by HMRC.

Lessons for the upcoming tax strategy

Overall, evidence from Scotland, the rest of the UK and overseas suggests that behavioural responses to Scotland’s higher taxes will have offset a significant part of the revenue that would otherwise have been raised – and indeed potentially more than offset the revenues for the top rate of tax. But there remains a significant degree of uncertainty about the scale of effects, particularly for the bigger changes in policy seen over the last two years.

With this in mind, reports that the Scottish Government’s tax strategy will commit it to a structured process of policy appraisal and evaluation are welcome – it is important that this work continues for income tax.

The Scottish Government and HMRC should also focus on developing more rapid indicators of the impacts of tax policy, using information from monthly PAYE income tax submissions by employers and changes of address by taxpayers – ideally publishing summaries and making (suitably anonymised) data available to external researchers. Information from recruitment firms, payroll providers and financial services providers could also be explored.

The tax strategy is also an opportunity to consider the tax system in the round – it is not only income tax that the Scottish Government could use to raise revenues in a progressive manner. We will return to this issue in our analysis of the published tax strategy. And given tax increases in the last two Scottish Budgets, it may make sense to await evidence of their impact on taxpayers and tax revenue, rather than further increase income tax rates on higher incomes. The Scottish Government should also be open to reversing course if new evidence again suggests bigger-than-expected behavioural impacts – a strategy should always be open to revision, not set in stone.

Authors

David Phillips

David is Head of Devolved and Local Government Finance. He also works on tax in developing countries as part of our TaxDev centre.

More from IFS

Understand this issue

Policy analysis

Academic research