Downloads

Download the report as PDF

PDF | 964.88 KB

Preface

This IFS Scottish Budget Report is the first produced as part of a new partnership with Scottish Financial Enterprise (SFE).

SFE is the representative body for Scotland’s financial and professional services industry, with more than 120 members ranging from global organisations headquartered in Scotland, to international companies with substantial operations in Scotland, through to small, locally based fintechs and support companies drawn from all areas of the sector. SFE is funded entirely by its member firms and seeks to connect, convene and champion the sector in Scotland and beyond.

SFE and its member organisations bring additional expertise on issues related to the financial markets and the economy, which complements IFS expertise on public finances and public policy. It has partnered with IFS to support independent and impartial analysis of the tax, spending and public policy challenges and opportunities facing Scotland.

The authors also gratefully acknowledge the support of the ESRC Centre for the Microeconomic Analysis of Public Policy (ES/Z504634/1).

In addition, the authors thank Helen Miller and Ben Zaranko for comments on initial drafts and both Scottish Fiscal Commission and Scottish Government officials for helpful discussions and clarifications.

IFS is an independent Research Institute. As with all our work, IFS researchers have full editorial control over the analysis they undertake and the conclusions they draw. The views expressed are those of the named chapter and section authors only and not of the institute – which has no corporate views – or of the funders of the research. Any errors or omissions are also the responsibility of the authors alone.

Executive summary

The Scottish Budget and Spending Review published on 13 January set detailed spending plans for 2026–27, alongside higher-level plans for the following two years for day-to-day (resource) spending and the following three years for investment (capital) spending. Understandably, the Scottish Government chose to highlight areas where it has chosen to spend more (such as the Scottish child payment) or tax less (such as increases in the basic- and intermediate-rate tax thresholds). But a significant slowdown in funding growth means that these decisions sit alongside tougher choices elsewhere.

This report, building on our initial response to the Scottish Budget, looks in more detail at the spending plans set out. We will consider the funding situation (including funding risks), tax and benefit policy, and public service performance in a series of pre-election briefings to be published over the next two months.

Key findings

Plans for day-to-day public spending

- Most spending portfolios have received top-ups within the current fiscal year (2025–26), funded by a combination of increases in funding from the UK government and money carried forward from last year (2024–25). The Health & Social Care portfolio has been topped up by £722 million, or £587 million (2.9%) after stripping out explicit compensation for higher employer National Insurance contributions (NICs). Such top-ups were always highly likely: as we argued in last year’s IFS Scottish Budget Report, holding budgets flat in real terms, as implied by initial plans, always looked difficult in the face of rising demands and costs. With these top-ups, spending on the Health & Social Care portfolio this fiscal year is set to be 3.3% higher in real terms than last, or 2.6% higher after stripping out explicit compensation for higher employer NICs.

- The 2026–27 Budget sets out initial plans for the Health & Social Care portfolio that once again imply effectively no real-terms growth in spending year-on-year. Indeed, after accounting for increases in pre-planned transfers to councils to help pay for social care services, the remaining elements of the portfolio (such as funding for hospitals and GPs) are set to fall by an average of 0.6% in real terms in the coming year. Top-ups will again likely be needed to avoid deterioration in service provision, but it will be harder to fund such top-ups without making in-year cuts to other portfolios.

- While councils will benefit from these pre-planned transfers (and similar transfers from other portfolios), the funding has already been committed to specific purposes by the Scottish Government (including increasing pay for social care and childcare workers). Even including these transfers, matching the overall real-terms increase in funding that English councils will receive if they increase their tax bills by 5% would require Scottish councils to increase their council tax bills by around 6.5%.

- Looking to 2027–28 and 2028–29, a sizeable boost to funding for the Health & Social Care portfolio (2.4% a year in real terms, on average) is being facilitated by cuts (averaging 1.7% a year in real terms) to spending on most other portfolios. Within the Health & Social Care portfolio, the Scottish Government is also planning a huge relative shift in funding out of hospitals to the community over these years: core funding for the territorial and national health boards (which cover hospitals and the ambulance service, among other things) is set to increase by an average of just 0.4% a year in real terms. The remaining parts of the Health & Social Care portfolio are set to grow much more (averaging nearly 12% a year in real terms), although it is unclear how this will be distributed – for example, between primary care (such as GPs) and social care. And this shift may not be achievable without declines in hospital and ambulance performance as health boards will struggle with their small funding increases unless they can deliver large efficiency gains.

- The trade-offs between spending on different public services in the coming years would have been worse if not for a sizeable reduction in forecasts for net spending on Scotland’s devolved benefit system. This is largely the result of increases in funding from the UK government (largely as a result of the cancellation of planned cuts to disability benefits in England and Wales) as well as reductions in forecast caseloads for Scotland’s adult disability payment, following reductions in successful claim rates.

Plans for capital investment and borrowing

- In-year revisions to the current fiscal year’s (2025–26) budget have seen the Scottish Government reduce planned capital spending, pushing it back to 2026–27 and later. Again, this is in line with last year’s IFS Scottish Budget Report where we highlighted that capital budgets tend to be underspent when they are planned to increase rapidly (as in 2025–26). Pushing back spending may improve value for money if it allows more time for planning investment projects and avoids spikes in construction costs that can arise if spending jumps up rapidly.

- As a result of this, and top-ups to UK government funding, capital spending is now set to increase in 2026–27 rather than decline as initially expected. By far the biggest increase is for the Justice & Home Affairs portfolio (24% in real terms) as spending on new prisons ramps up. Transport is also set to see a notable increase (11%). But Health & Social Care (–10%) and Finance & Local Government (–9%) are set to see cuts in investment spending compared with the current fiscal year.

- Overall capital funding is set to fall over the following three years to 2029–30, but as spending on new prisons starts to wind down, the amount of funding available for other types of investment actually increases slightly in real terms (an average of 0.3% a year). The biggest increases are planned for Housing (+7% a year) and Transport (+1% a year). In contrast, capital funding for the Health & Social Care (–2% a year), Finance & Local Government (–2% a year) and Deputy First Minister, Economy & Gaelic (–5% a year) portfolios is set to fall between 2026–27 and 2029–30. Cuts to Health & Social Care investment may make it harder to deliver efficiency savings, which can be facilitated by investment in better facilities and technology.

- As well as using funding from the UK government and its own borrowing powers to help fund investment, the Scottish Government is considering new public–private partnerships to fund new community health centres and college buildings. With capital funding and borrowing constrained by the UK government, this could speed up the delivery of such facilities. But the official appraisal of this ‘Mutual Investment Model’ suggests such investments could cost up to 60% more over 25 years than investments funded by direct borrowing, and over twice as much as investments made using UK government funding. Funding investment in this way therefore only makes sense in the context of constraints on direct borrowing, and if there are sufficient investment opportunities with high enough impacts to make it worthwhile using this model on top of direct borrowing and UK government funding.

- For its own direct borrowing, the Scottish Government plans to issue bonds for the first time in 2026–27. Its outline business case suggests this will cost a little more than borrowing via the UK government as it has done so far – a central estimate of an extra £100 million for a multi-year £3 billion programme of 15-year bonds, for example. The rationale for borrowing directly is to give more flexibility over repayment terms and to create an opportunity for greater engagement with international investors. The Scottish Government estimates that if this were to lead to an extra 0.1–0.2% of business investment per year, that would cover the extra borrowing costs.

Efficiency, pay and employment

- The Scottish Government has set its different spending portfolios targets for savings from efficiency improvements and service reform totalling £1.6 billion a year by 2028–29. While the real proof will be in their delivery, the information provided on these plans is, overall, a welcome improvement on that previously available. But less information is provided for the Health & Social Care portfolio than for others, despite this being expected to deliver over two-thirds (£1.1 billion) of the overall savings. And the targets for Scotland’s health boards look highly ambitious – significantly in excess of what has historically been achieved. There is less information than there should be on how each portfolio will contribute to targets of £1 billion of savings in administration costs (contributions to this target are subsumed in each portfolio’s wider efficiency savings target). The same is true for contributions to the target of 0.5% annual reductions in the size of the public sector workforce (no workforce figures are provided alongside projected financial savings).

- Controlling public sector labour costs is likely to be challenging. The Scottish Government is officially sticking to its target of 9% pay rises (in cash terms) over the three years from 2025–26 to 2027–28. With pay awards agreed that average almost 8% over the first two of those years, that would imply an increase of just 1% in 2027–28, which may be difficult to adhere to given that it would almost certainly require real-terms pay cuts. Delivering the targeted overall reductions in the devolved public sector workforce of 0.5% per year is feasible – much bigger cuts were delivered in the early 2010s, for instance – but would require political will to achieve. If, for instance, teacher numbers were protected, and growth in non-administrative NHS staff numbers held down to 1% a year (in line with the last year but less than half the average rate since 2019), employment in other areas would need to be reduced by 1.3% (3,600) per year to achieve targets. There will also likely need to be a reshaping of the workforce as changes in technology and service delivery models mean more people are needed in some areas (e.g. digital technology) and fewer in others (e.g. clerical).

1. Plans for day-to-day public spending

The 2026–27 Scottish Budget and Spending Review (Scottish Government, 2026a and 2026b) set detailed plans for both day-to-day (resource) and investment (capital) spending for the coming financial year, and more aggregated, higher-level plans for the following several years (to 2028–29 for resource spending and 2029–30 for capital spending). In our immediate response to the Budget (Adam et al., 2026), we highlighted the difficult trade-offs between resource spending allocations for the Scottish Government’s different ministerial portfolios. In this chapter, we look in more detail at the resource spending outlook; in the next, we look at the capital spending outlook.

There has been a significant top-up to health spending in 2025–26 …

Before turning to plans for future years, it is first worth looking at how plans for spending in the current financial year, 2025–26, have changed over the course of the year. Table 1 shows the changes in resource spending plans in 2025–26 for the different Scottish Government portfolios at the Autumn Budget Revision (ABR) in September 2025 and Spring Budget Revision (SBR) in January 2026, stripping out the effects of pre-planned transfers between portfolios so as to focus on ‘true’ increases and decreases in budgets.

Table 1. In-year changes to 2025–26 resource budgets, by portfolio

* Finance and Local Government portfolio excludes the £252 million held in the contingency reserve.

**Justice portfolio figures adjusted to remove effect of shift of fire and police pension balancing payments from resource budget to UK-funded annually managed expenditure.

*** Social Justice portfolio figures exclude social security benefits.

**** Reduction in planned spending by the Deputy First Minister portfolio largely reflects use of unspent EU funding in place of Scottish Government funding. We exclude the employability programme, which is included in social security benefits.

Note: We exclude all separately identified National Insurance contributions (NICs) compensation from figures in the final two columns. This will cover most, but not all, NICs compensation.

Source: Authors’ calculations using Scottish Government (2025a and 2026c) and correspondence with the Scottish Government.

The table shows that there have been substantial in-year top-ups to public service spending this year, of which around one-quarter relates explicitly to compensation provided to public sector employers for higher employer National Insurance contributions (£323 million out of £1,158 million). The top-ups have been funded by a combination of additional funding from the UK government and underspends carried forward from 2024–25 via the Scotland Reserve.

The largest top-up has been for the Health & Social Care portfolio – £722 million in total, or £587 million (2.9%) stripping out the funding for employer National Insurance contributions (NICs). Our 2025–26 Scottish Budget Report (Boileau and Phillips, 2025) highlighted the likelihood of this given that the original budget for the Health & Social Care portfolio this year was no higher in real terms than the final budget for 2024–25 – indeed, given that inflation is now expected to be higher, it would have been lower in real terms. Following the top-ups announced in the Autumn and Spring Budget Revisions, the budget for Health & Social Care in 2025–26 is now set to be 3.3% higher in real terms than the final budget for 2024–25, or 2.6% higher after stripping out funding provided for increased employer NICs.

The Finance & Local Government portfolio has seen the second-largest top-up, of £242 million, with around £144 million explicitly labelled as compensation for higher employer NICs compensation. Education & Skills, Transport and Justice & Home Affairs have been topped up significantly too. Notably, the Deputy First Minister, Climate Action & Energy and Parliament & Audit Scotland portfolios have been cut back.

The Spring Budget Revision also confirmed that reductions in forecast social security spending (see below) have freed up funding. In part because of this, around £250 million of resource funding is being held as a contingency reserve in case of unanticipated spending needs between now and the end of the fiscal year. This is similar to last fiscal year (2024–25), when £350 million was held for year-end contingencies. This was ultimately not needed, and the Scottish Government appears to assume that most will not be needed again – with £150 million already assumed to be carried forward via the Scotland Reserve and used as part of the 2026–27 Budget.

… and more top-ups will likely be needed in 2026–27

Carrying forward funding would help with budgetary pressures in the coming fiscal year, albeit only in a one-off way. For example, in our immediate response to the Scottish Budget (Adam et al., 2026), we highlighted that further top-ups to the Health & Social Care portfolio would likely be needed in the coming financial year, 2026–27. This was because the resource budget for that portfolio was due to be just 0.7% higher in real terms than the plans set out in the Autumn Budget Revision for the current financial year – a rate of increase far below Scottish Government estimates of year-on-year increases in health spending needs (Scottish Government, 2025b).

The first bar in Figure 1 updates this analysis to account for changes made to the current fiscal year’s budgets in the Spring Budget Revision, which were confirmed after our immediate response to the Scottish Budget. These amount to a £100 million top-up to the Health & Social Care portfolio this fiscal year, mostly to address increasing demands and costs – i.e. ongoing rather than one-off costs. Taking these top-ups this year into account reduces the scale of the planned increase between this year and next to just 0.2% in real terms.

Figure 1. Change in planned spending on the Health & Social Care and Finance & Local Government portfolios before and after planned in-year transfers in 2026–27

Note: Revenue funding within other portfolios to be transferred in year is added to the Finance & Local Government portfolio and subtracted from the Health & Social Care portfolio.

Source: Authors’ calculations using Scottish Government (2026a) and correspondence with the Scottish Government.

However, the 2026–27 Budget also sets out increases in transfers from the Health & Social Care portfolio to other departments – most notably to the Finance & Local Government portfolio in relation to a commitment to pay social care workers the ‘Real Living Wage’. Stripping out this £160 million, and a further £7 million to be transferred to councils to help pay for free personal nursing care, means that the remaining elements of the Health & Social Care portfolio (including funding for the Scottish NHS) are set to be cut in real terms next year by 0.6%.

Therefore, in our judgement, it is highly likely that funding for the Health & Social Care portfolio will again have to be topped up substantially in 2026–27 – especially if ambitious targets for efficiency savings discussed in Chapter 3 are not fully delivered. And in contrast to 2024–25, when big in-year top-ups to funding from the UK government were received, and 2025–26, into which some of those top-ups could later be carried forward, the Scottish Government is likely to have less financial wiggle room in 2026–27. Not only do initial 2026–27 Budget plans already assume the use of £150 million of carried-forward funding, but as highlighted by the Fraser of Allander Institute (2026), they also make use of several other one-off sources of funding, and effectively allocate more business rates revenues than are forecast to be collected. Of course, the Scottish Government may be able to carry forward more than £150 million, or the UK government may increase spending and hence funding for the Scottish Government. But it is possible that, like in 2023–24, in-year cuts to some services will be required to make the sums add up. And funding carried forward can only be used once, whereas the spending pressures that need to be covered will mostly be recurring (and indeed growing) in future years too. Repeated reliance on carried-forward and one-off funding sources to fund ongoing spending is a risk to fiscal sustainability.

The third and fourth bars of Figure 1 show that the transfer of the additional social care funding, alongside increases in transfers for various education-related initiatives (from the Education & Skills portfolio), means that whereas resource funding for the Finance & Local Government portfolio is set to increase by 0.1% in real terms prior to these transfers, it is set to increase by 1.3% after the increases in pre-planned transfers are accounted for. But to the extent that this funding is mostly pre-committed to increases in wages, the increase in truly discretionary funding for Scottish councils is still very small. Council tax increases of 3%, which Scottish ministers have suggested would be reasonable, are unlikely to be sufficient to meet rising demands and costs in this context.1 Delivering a 2% real-terms increase in overall funding – in line with the planned increase in English schools and council funding – would require increases in council tax of closer to 6.5% in 2026–27.

The impact of these planned in-year transfers between portfolios on the picture for how funding is changing for two major services (health and local government) highlights the need for greater transparency over spending plans. Reporting increases in funding for the Health & Social Care portfolio before outward planned transfers in the Budget document, but then focusing on increases in local government funding after inward transfers in the Finance Secretary’s speech, risks double-counting planned funding. To avoid this, the Scottish Government could move fully to baselining funding in the portfolio it will eventually be transferred to – avoiding the need for planned in-year transfers of funding. Alternatively, it could publish budgets for all portfolios both before and after pre-planned transfers so that consistent figures can be compared (e.g. all before or all after the transfers).

Plans for 2027–28 and 2028–29 will need fleshing out post-election

Looking further to the future, our immediate response to the Scottish Budget and Spending Review (Adam et al., 2026) highlighted that increases to resource funding for the Health & Social Care portfolio will mean substantial cuts to most other portfolios in 2027–28 and 2028–29.

This is illustrated in Figure 2, which shows that after increasing by 0.6% in real terms in 2026–27, overall resource budgets for public services will increase by an annual average of just 0.2% a year in real terms in 2027–28 and 2028–29. Funding for the Health & Social Care portfolio will increase much faster, by an average of 2.4% a year in real terms. With the exception of the Constitution, External Affairs & Culture portfolio and the Transport portfolio (both increasing by around 3% a year in real terms), all other portfolios will see reductions. These range from 1.5% a year in the case of the Education & Skills portfolio to 4.6% a year in the case of the Social Justice portfolio (excluding social security benefit spending itself). The Finance & Local Government portfolio – the second-largest after Health & Social Care – is set to see reductions averaging 2.1% a year in real terms. The cuts to the Justice & Home Affairs portfolio may be particularly difficult to manage given pressures on the court and prison systems, and the fact that unlike in England, police and fire services cannot raise funding themselves via council tax (accounting for this, equivalent ‘justice and home affairs’ funding is set to increase in real terms in England).

Figure 2. Average annual change in resource spending by portfolio, real terms, in 2027–28 and 2028–29

Note: Finance & Local Government portfolio includes non-domestic rates, Social Justice portfolio strips out social security spending and Deputy First Minister, Economy & Gaelic portfolio excludes employability.

Source: Authors’ calculations using Scottish Government (2026b).

Spending plans are set out at a much less detailed level in the Scottish Spending Review than in the annual Budget, with the breakdown between resource and capital spending plans only provided at the overall portfolio level, for instance. Whoever is in government post-election will need to flesh out the spending plans in significantly more detail if it wants to provide public bodies (including Scottish councils) with multi-year clarity over their budgets. As highlighted in our initial Budget response and as we will explore in more detail in our pre-election briefings, in doing so it might make sense to hold some funding back to allocate later in case devolved tax revenues do not come in as strong as currently forecast.

The Health & Social Care portfolio illustrates the uncertainties inherent in the current high-level allocations set out in the Scottish Spending Review. As discussed above, its overall resource budget is set to increase by an average of 2.4% a year in real terms in 2027–28 and 2028–29. In cash terms, this equates to an average increase of around £940 million in funding each year. However, indicative figures for the territorial and national health boards show their resource funding increases by just £465 million in 2027–28 and £350 million in 2028–29. This equates to 43% of the overall increase in planned spending by the Health & Social Care portfolio, despite these territorial and national boards making up 83% of planned spending in 2026–27.

This has two implications.

First is that the real-terms increases for these territorial and national health boards amount to just 0.4% a year – just one-sixth the rate of the overall increase for the Health & Social Care portfolio. This is a very slow rate of growth by both recent standards and projections of spending needs (Scottish Government, 2025b) and would require big increases in efficiency and productivity to avoid degradation in service quality.2

Second is that if these spending plans were adhered to, the remaining areas of the Health & Social Care portfolio are set to see much larger increases of almost 12% a year in real terms. This would represent a major (relative) transfer of resources out of hospitals. But how would this be allocated between primary care (GPs), other medical services (e.g. dentists, opticians and pharmacists) and social care services? This has big implications both for the different organisations involved in delivering these services, and in understanding the Scottish Government’s vision for health and social care services over the next few years.

It could also have big implications for councils. As highlighted above, the Finance & Local Government portfolio is set to see 2.1% per year real-terms reductions in resource funding before considering any in-year transfers from other portfolios. Suppose, for example, that half of the implied increase for ‘other’ Health & Social Care portfolio spending was allocated to social care transfers to councils. This would reduce the scale of cuts to Scottish Government funding for councils to 0.5% a year in real terms. Increases in council tax of 2% a year would then be sufficient to hold overall council funding flat in real terms. But increases in council tax of around 8% a year in both 2027–28 and 2028–29 would still be needed to deliver the increases in funding that English councils can expect over the same period, where increases in council tax are expected to average around 6%. In the absence of such large increases in transfers from the Health & Social Care portfolio, Scottish councils might need to increase council tax by around 14% a year to match increases in English council funding.

Benefit spending pressures ease

One area of better news from a fiscal sustainability perspective was a significant downwards revision to the expected net cost of Scotland’s devolved benefit system – reflecting both changes to UK government policy and spending forecasts, and changes to forecasts for the impact of Scotland’s disability benefit reforms on expenditure. In the absence of this improvement (and other policy changes), the outlook for public service spending discussed above would have been even trickier, with a small real-terms cut rather than a small real-terms increase in funding over the next three years.

Table 2 shows forecasts of the net cost of Scotland’s devolved benefits – i.e. the difference between forecast spending and the funding provided by the UK government via the benefits block grant adjustments (BGAs) – as of June 2025 (the forecasts published alongside the 2025 Medium Term Financial Strategy) and as of January 2026 (the latest forecasts published alongside the Budget). The table also shows the components of change: changes to the block grant adjustments and various changes to Scottish benefit spending forecasts.

Table 2. Forecast net benefit expenditure, and components of changes in forecast (£ million)

Source: Authors’ calculations using Scottish Fiscal Commission (2026).

The table shows that whereas the net cost of Scotland’s devolved benefits was forecast to grow from £1.2 billion this year to £2.0 billion by 2029–30, the latest forecasts are for a net cost this year of just under £1 billion, rising to £1.2 billion by 2029–30.

In the longer term, most of this reduction in the net cost reflects higher funding from the UK government via the benefits block grant adjustments. In turn, this reflects increases in forecast disability benefit expenditure in the rest of the UK, both as a result of higher underlying growth and as a result of the cancellation of planned increases in the severity of disability needed to qualify for personal independence payment (PIP).

But there have also been reductions in forecast benefit spending by the Scottish Government. There are two main components to this. First, as discussed by the Scottish Fiscal Commission (2026), the latest data suggest that success rates for applications for adult disability benefit (the Scottish replacement for PIP) have declined, while the rate of awards reduced or ended at review has increased – both of which reduce forecast expenditure. We will examine this issue in more detail in our pre-election briefing series. Second, with the UK government removing the two-child universal credit limit nationwide, there will be no need for the ‘mitigation payments’ previously planned by the Scottish Government.

2. Plans for capital investment and borrowing

Capital spending plays an important role in sustaining and improving public services and facilitating economic activity and growth. This chapter analyses the Scottish Government’s plans for capital spending and associated borrowing over the next four years.

Capital funding has been pushed from 2025–26 to 2026–27 …

Again before looking to the future, it is first worth examining the Scottish Government’s updated plans for capital spending this financial year, 2025–26.

It has reduced planned capital spending compared with both the initial plans set out in December 2024 (by £201 million or 2.7%). The reduction compared with the overall spending plans set out in the Autumn Budget Revision in September 2025 (£226 million or 3.1%) is a little larger, although note that not all of the spending then planned had been allocated to specific portfolios. Compared with those updated plans though, the Scottish Government now plans to make substantially less use of Crown Estate (ScotWind) proceeds (–£188 million) and to borrow less (–£42 million). Very slightly offsetting this is the fact that there is slightly more capital funding to draw down from the Scotland Reserve than previously expected (+£4 million). This enables the Scottish Government to borrow more and draw down more ScotWind proceeds in future, as we discuss below.

The biggest in-year cutbacks to planned investment have been for the Climate Action & Energy portfolio (–£131 million or 27%), largely due to less investment in offshore wind (–£103 million or 69%), and the Transport portfolio (–£120 million or 6%), driven by slower-than-hoped-for progress on the provision of new ferries and active transport infrastructure. The Health & Social Care portfolio saw a top-up (£100 million or 11%) to its capital budget, largely for research and development.

Capital spending will still have increased in 2025–26 compared with 2024–25, but at a slower pace than the original plans implied – an increase of 13% in real terms, compared with the 16% implied by the original 2025–26 Budget. This slower increase and pushing back of capital spending is in line with what we anticipated and recommended in our 2025–26 Scottish Budget Report (Boileau and Phillips, 2025). The Scottish Fiscal Commission (2026) states that this has been done because the Scottish Government was on track to underspend compared with previous plans. And as we previously highlighted, a slower ramp-up in capital spending could improve value for money by allowing more time to plan and select projects, and by helping to avoid temporary spikes in construction costs due to high demand. It also allows for greater capital investment in later years when projects may be better developed and more deliverable.

… and will now increase rather than fall

In contrast to this year, the Scottish Government now plans to borrow more in 2026–27 (£491 million as opposed to £430 million). When combined with a top-up to UK government capital funding confirmed in the UK Budget in November, this means total capital funding for 2026–27 will grow by £381 million (5.3%), rather than fall by £68 million (0.9%) as expected in June 2025. When accounting for inflation, this amounts to a real-terms increase of 3.0%.

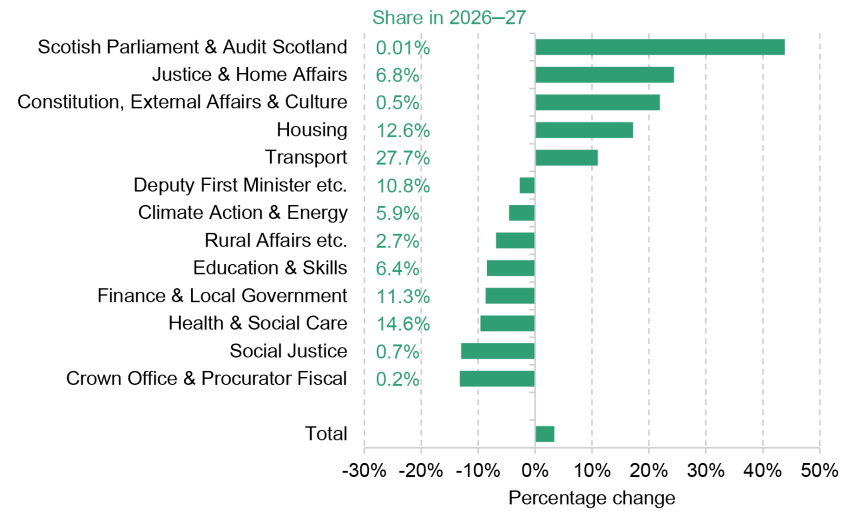

Figure 3 shows the planned rate of growth in capital spending by portfolio. Overall, spending is set to grow by 3.4% in real terms (around 0.4% of funding this year is not allocated to a specific portfolio, so planned spending is set to grow faster than funding). The main positive contributions to spending come from increases to Transport (+11.0%) and Justice & Home Affairs (+24.4%). At the same time, the Budget lays out significant year-on-year cuts to Health & Social Care (–9.6%), Finance & Local Government (–8.7%), Climate Action & Energy (–4.6%) and the Deputy First Minister portfolio (–2.7%). Capital spending can be lumpy though as major construction projects start and end, so one must be wary of reading too much into a single year’s change.

Figure 3. Annual percentage change in capital spending by portfolio, real terms, in 2026–27

Note: Includes financial transactions and standard capital spending. Total change in capital spending is different from change in capital funding as not all funding has been allocated to portfolios in 2025–26.

Source: Authors’ calculations using Scottish Government (2026a) and correspondence with Scottish Government.

Looking beyond the coming year, the Scottish Government plans a steady reduction in capital spending over the Spending Review period, with real-terms cuts of 2.2% in 2027–28, 1.6% in 2028–29 and 1.2% in 2029–30.

Winding down prison construction frees up capital funding for other areas

The slow decline of total capital funding over the Spending Review period masks very different trends for different portfolios. In particular, after 2026–27, capital funding for Justice & Home Affairs is set to fall by a real-terms average of 31% per year, a fall driven by the anticipated end of the HMP Highland and HMP Glasgow prison construction programmes. The Scottish Government can channel these freed-up resources to other infrastructure priorities. Other (non-Justice) capital spending is set to grow by an annual real average of 0.3% after 2026–27, as Figure 4 shows.

Figure 4. Real-terms capital spending plans (2026–27 = 100)

Source: Authors’ calculations using Scottish Government (2026b).

Housing is set to continue to see substantial increases, with capital investment growing by a real-terms average of 7.1% per year until 2029–30. Transport is also prioritised, with real average annual growth of 1.1%. These increases are offset by cuts elsewhere, namely the Health & Social Care (–1.9% on average), Finance & Local Government (–1.8%) and Deputy First Minister, Economy & Gaelic (–5.3%) portfolios.

The cuts to Health & Social Care capital funding will have to be managed particularly carefully, in light of ambitions to make significant efficiency savings in day-to-day spending for this portfolio (see Chapter 3). Digitising and automating services are often key ways in which productivity can be increased, but this often means up-front capital investment is needed to deliver gains down the line. The picture for the UK Department of Health and Social Care – which, similarly to Scotland, is set to deliver the bulk of the productivity improvements planned across UK departments – looks somewhat different, with plans implying average annual real-terms increases in capital spending of 0.8% between 2026–27 and 2029–30 (compared with cuts of 1.9% per year in Scotland).

Investment will be supported by borrowing and resource-financed models

The capital spending discussed above will be largely paid for via funding from the UK government. As we will show in our upcoming election briefing series, this funding is higher in Scotland than in England and Wales. However, as already highlighted, the Scottish Government also makes use of borrowing to boost its capital budget. It has also historically made use of, and plans in future to make use of, public–private partnership arrangements to fund up-front investment costs from future resource budgets. This is in some sense similar to standard borrowing, in that future resource budgets must meet interest and repayment costs, but with important differences.

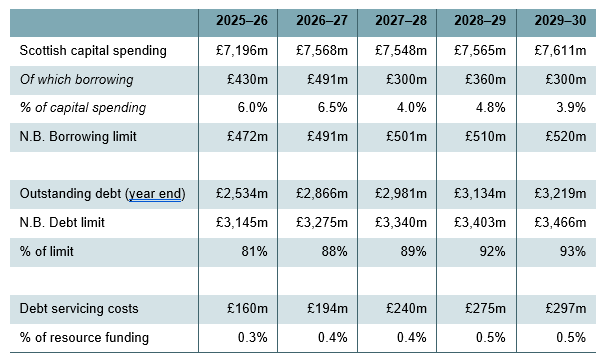

The Scottish Government’s capital (and other) borrowing powers are set out in its fiscal framework agreement with the UK government (HM Government and Scottish Government, 2023) and are subject to both annual limits on borrowing and aggregate caps on total outstanding debt. These restrict how much the Scottish Government can borrow to invest, on top of the capital funding provided by the UK government and from Scotland’s own devolved revenues. Table 3 shows the scale of borrowing planned, how that compares with these limits, and the debt servicing costs incurred.

Table 3. Scottish Government capital spending, borrowing, debt and repayments

Source: Authors’ calculations using Scottish Fiscal Commission (2026).

The table shows that this financial year and next, borrowing is set to fund around 6% of capital spending, but this is set to fall to between 4% and 5% over the following three years as annual Scottish borrowing is reduced. This is so that the Scottish Government can maintain some headroom against its overall debt limits – although debt is still forecast to creep up from 88% of the limit at the end of 2026–27 to 93% by the end of 2029–30. If the Scottish Government wanted to maintain borrowing and investment at higher levels, it could choose to pay down existing debt more quickly – although that would increase annual debt servicing costs, which must be covered from resource funding. Debt servicing costs will remain low as a share of the Scottish Government’s resource funding, but are increasing because of both the increased outstanding stock of debt and the higher interest rates due on more recent and planned borrowing.

To date, the Scottish Government has borrowed via the UK government. But from 2026–27, it will commence issuing its own bonds. Box 1 discusses the practicalities and potential costs and benefits of this – and why we will be able to learn relatively little about the prospects for borrowing for a more fiscally autonomous or independent Scotland from the experience of issuing bonds as part of the UK.

Box 1. Borrowing directly through Scottish bonds

Author: Angus Macpherson

In November 2025, the Scottish Government announced that it intended – subject to the outcome of the next election, the then prevailing market conditions, and its specific needs at the time – to embark on a £1.5 billion bond issue for capital investment ‘over the life of the next parliament’, with the first issuance targeted for 2026–27 (Scottish Government, 2025c). This will be in place of borrowing via the UK government’s National Loans Fund: the borrowing and debt stock limits set out in the Scottish fiscal framework agreement will still apply.

The decision to begin borrowing directly via the sale of Scottish bonds was one of the recommendations of the First Minister’s Investor Panel. Based on extensive discussions and interviews with international and domestic investors, the panel concluded that the issuance of bonds could improve engagement with national and international capital markets (Investor Panel, 2023). In particular, it argued that borrowing directly in this way would provide a motivation and a vehicle for regular engagement with investors, giving the Scottish Government both an opportunity to market Scotland’s investment opportunities and an opportunity to receive intelligence on the impact of investor attitudes – including from the interest rates it could borrow at. This would help overcome several issues identified via engagement with investors: limited research and hence knowledge on the specifics of Scottish policy and investment environment; and a sense that investor views of Scottish policy were not always well understood by ministers and officials. Issuing bonds would also allow the development of relationships with rating agencies and bond market participants, including a track record of repayment.

The Scottish Fiscal Commission (2026) has also highlighted that having its own bond programme would give the Scottish Government more flexibility over repayment terms than borrowing via the National Loans Fund. For example, rather than making regular repayments of both interest and principal (the amount initially borrowed), ‘bullet repayment’ bonds could be issued where only interest is payable regularly and the principal is repayable at the end of the loan (akin to an interest-only mortgage, and in line with how the UK and other governments tend to repay their borrowing). This would free up funding for other purposes in the short term but mean substantially bigger repayments in the years where the principal became due – with existing fiscal framework rules preventing (resource) borrowing from being used to cover these repayments and roll over the debt (which the UK and other national governments can do). The Scottish Government could also choose to borrow over shorter or longer time frames than available from the National Loans Fund (10–25 years).

The Investor Panel and the outline business case produced by the Scottish Government (2025d) recognise that there would be costs associated with direct bond sales. First, there would be operational costs related to bond issuance, reporting and associated consulting and advisory costs. Second, the central expectation is that the interest rate that would need to be paid would be a little higher than borrowing via the National Loans Fund. Rating agencies have given the Scottish Government the same rating as the UK government, and bonds will be priced by investors relative to similar UK bonds (gilts). However, it should be anticipated that investors will seek a premium to reflect the fact that the Scottish Government will be a new bond issuer and that liquidity is likely to be lower (the UK government is one of the most established issuers, with a large liquid market for its debt).

The actual premium will be determined by a range of economic and political factors, as well as the size and structure of the bond issuance. It is worth noting that borrowing via the National Loans Fund is currently set at a 0.11% (11 basis points) premium above the rate the UK government borrows at (with the premium being much higher at points during the 2010s). The Scottish Government’s business case therefore shows there is significant uncertainty about how much extra borrowing directly via Scottish bonds would cost – and that it could be cheaper than borrowing via the National Loans Fund. However, the central estimate is that a programme of borrowing £300 million a year over 10 years (£3 billion in total) via 15-year bonds would cost around £100 million more in present-value terms, accounting for administration costs and interest rate differentials. The business case says that an increase in business investment of 0.1–0.2% a year would be sufficient to cover these costs and yield net positive benefits for Scotland. It concludes that ‘there is high confidence that bond issuance would deliver value for money, if it attracts additional investment to Scotland’.

Finally, it is worth noting that the Investor Panel’s recommendation was for the Scottish Government to use its existing powers to issue bonds. The standalone credit rating provided to the Scottish Government is the same as the UK government’s, reflecting the strengths of the Scottish economy and its institutions under current constitutional arrangements. Any changes to these could lead to stronger or weaker ratings (and lower or higher interest rates). The read-across to the rates at which a fully fiscally autonomous or independent Scotland could borrow at is likely to be limited, as they will depend on the specific circumstances prevailing at that time. Moody’s rating, for example, states that ‘Scottish independence could exert downward pressure on the [credit] rating by introducing heightened uncertainty about the institutional framework and potentially raising financial stability risks’. Even if such changes occur, they are unlikely to be imminent. In the meantime, the strong rating already provided, and the greater opportunity for investor engagement that bond issuance would offer, are hoped to increase the quantum and reduce the cost of inward business investment to Scotland.

Note: Angus Macpherson was co-chair of the First Minister’s Investor Panel. All views expressed here are his alone unless directly attributed to the panel or other individuals or organisations.

The box highlights how issuing its own bonds will give the Scottish Government more flexibility over repayment durations and terms, which would need to be offset against the fact that such borrowing would likely be a little more expensive. It could, like the UK government typically does, issue bonds where only interest is due until the principal becomes payable at maturity. That would free up funding in the short term but would be a bigger drain on the budget in the later years when bonds mature and repayments are due. Given rules preventing the Scottish Government from borrowing again to roll over debts (borrowing is only possible for new capital investment), and limits on how much can be held in the Scotland Reserve (which could otherwise be used to build up a ‘repayment fund’ over time), such ‘bullet repayment’ bonds may increase long-term fiscal risks. The Scottish Government could instead issue bonds where repayments of principal are made alongside interest (like a repayment mortgage and like how it currently borrows via the UK government’s National Loans Fund), but this would free up less funding in the short term.

Off-budget borrowing via public–private partnerships

Historically, programmes such as the Private Finance Initiative (PFI) and the non-profit distributing (NPD) model allowed the Scottish Government and councils to utilise private sector borrowing to pay for new infrastructure and facilities, with the government covering the cost of this investment and annual service charges through resource budgets. But changes in public accountancy guidance in the mid 2010s (Audit Scotland, 2015) have made it harder to shift the up-front costs of capital investment off-budget and off balance sheets using these mechanisms – if a project is deemed to be under public sector control, capital investment must be accounted for up front.3 The more recent shift to IFRS16 accounting standards also means that leasing arrangements must be accounted for as up-front capital spending too.

Significant amounts of investment were undertaken under the PFI, NPD and associated models between 1990 and 2020 though: £5.7 billion via the PFI programme up to 2005 and £3.3 billion via the NPD and ‘hub’ programme since 2005 (Audit Scotland, 2020). This year, so-called ‘unitary charges’, which cover both the up-front construction costs and annual service charges (for maintenance, facilities support, etc.), are estimated to amount to £1.2 billion for PFI projects4 and around £0.4 billion for NPD projects.5 Taken together, this amounts to £1.6 billion in the coming year, 2026–27, with the figure for 2029–30 amounting to £1.5 billion. Together with capital borrowing debt servicing costs, these equate to 3.3% and 3.0% of resource funding, respectively.

While it has not made use of such models for new projects since 2020, the Scottish Government’s Infrastructure Strategy consultation (Scottish Government, 2026d) and Infrastructure Delivery Pipeline (Scottish Government, 2026e) state that it is exploring the use of a ‘Mutual Investment Model’ to construct and operate new community health centres. This model, which involves the public sector taking a small equity stake in the private companies delivering and maintaining the facilities, has been utilised previously in Wales and is designed to avoid falling foul of rules on whether projects are controlled by the public sector – and so remain outside capital spending and borrowing limits.

It is estimated that the 12 health centres initially planned would entail capital investment of over £500 million that would otherwise have to be funded up front from capital budgets and borrowing but will instead be funded over time via resource budgets. Similar resource-funded models of investment are also being considered for new facilities for further education colleges and for storage facilities for Scotland’s national cultural collections.

Given constraints on funding and borrowing via the Scottish fiscal framework, use of the Mutual Investment Model could help deliver new infrastructure and facilities more quickly. It is hard to avoid the conclusion though that this is just the latest in a long line of models developed by the UK and devolved governments to borrow ‘off balance sheet’ – effectively gaming fiscal and public accountancy rules. And use of this model is likely to entail higher costs than investments funded via either capital grant funding (1.7–2.2 times higher for an example educational building) or direct Scottish Government borrowing (1.0–1.6 times higher). These higher costs would need to be covered using future resource budgets, squeezing the amount of funding available for other purposes. The Mutual Investment Model is therefore suitable for use if there are a sufficiently large number of investments with high enough returns to justify the additional cost, and/or where significant financial risk is transferred to the private sector. Its use should be carefully controlled and monitored (e.g. through reporting to the Scottish Parliament) – and could be put at risk if there are further accounting changes.

3. Efficiency, pay and workforce

Constrained funding, and a desire to deliver the best services possible in this context, mean the Scottish Government has placed significant emphasis on service reform and on improvements in efficiency and productivity. It laid out its high-level approach to these issues in the summer in its Fiscal Sustainability Delivery Plan (Scottish Government, 2025e) and Public Service Reform Strategy (Scottish Government, 2025f). The Spending Review was an opportunity to say more about what these plans will entail in practice for different service areas. We heard more about the expected scale of efficiencies across spending portfolios, and the actions that will be undertaken to deliver the savings expected – including workforce reductions, and a range of measures to reduce operational costs. But the scale of the challenge in delivering these planned savings in practice should not be underestimated, especially with regards to health and social care, and workforce costs.

Published efficiency plans are welcome …

Table 4 summarises the planned annual savings from efficiency and service reform by 2028–29 set out in the Scottish Spending Review (Scottish Government, 2026b).

Table 4. Planned savings from efficiency and service reform, 2028–29, by portfolio

Note: Savings for the Social Justice portfolio are expressed as a percentage of the budget excluding benefit payments.

Source: Scottish Government, 2026b.

The Health & Social Care portfolio is expected to be by far the largest contributor to the efficiency savings set out: it is planned to deliver £1.1 billion of the £1.6 billion total. This is equivalent to 4.7% of planned day-to-day (resource) spending and 4.4% of overall spending on that portfolio in 2028–29. Measured as a share of day-to-day spending, planned savings are largest for the Climate Action & Energy portfolio, at just under 13%. In contrast, planned savings for the Transport portfolio represent just 0.6% of planned resource spending and 0.3% of overall planned spending. Planned savings for the Finance & Local Government portfolio are also relatively low at just 1.1% of spending – reflecting the fact that the plans exclude any specific targets for efficiency improvements and savings by Scottish councils. If councils were expected to deliver the same efficiency savings as the average for other areas of Scottish Government spending, they would be expected to amount to around £0.5–0.6 billion a year by 2028–29.

As well as setting out the overall contribution of each portfolio, the Spending Review document provides some detail on the contribution of different types of actions to these plans. Estimates of the contribution of workforce reductions are provided for all portfolios other than Health & Social Care, and amount to £82 million in 2026–27, rising to £237 million by 2028–29. This compares with an overall target set out in the Fiscal Sustainability Delivery Plan of £280 million in 2026–27, rising to approximately £560 million by 2028–29.6 This therefore implies annual workforce savings of around £320 million will need to be found between the NHS and councils in 2028–29 if the overall target is to be met. Other operational efficiencies – such as sharing more facilities and services, and digitising processes – are planned to yield £72 million per year by 2028–29, while reforms to service provision (including a shift to prevention) are costed as yielding £65 million per year by that date. It is important to note though that a key aim of many of the reforms to service provision is better outcomes rather than financial savings.

It is beyond the scope of this report – and, indeed, the expertise of the authors – to assess the various activities set out, their likelihood of success and whether they would generate the efficiency savings estimated. But we do have several high-level observations.

First, the level of detail provided is, in general, a significant improvement on what was previously available. For most portfolios, savings are broken down into several categories (such as workforce reductions, increased use of digital services, and more sharing of support services and facilities), and narrative information on related past and planned initiatives is provided. This is a similar degree of detail to the efficiency plans published alongside the UK Spending Review (HM Treasury, 2025a), and much more substantial than the information published at the UK Budget in November 2025 (HM Treasury, 2025b), when efficiency targets were increased.

Second, despite being the area where the largest efficiency savings are expected, the detail provided for the Health & Social Care portfolio is more limited compared with other portfolios. This may reflect the fact that the plan envisages Scottish health boards agreeing their more detailed plans on an annual basis. But given the importance of savings in this portfolio to overall fiscal sustainability, and the 10-year time horizons in Scotland’s various health system reform plans (Scottish Government, 2025g and 2025h), some further breakdown in expected savings – e.g. frontline versus administrative expenses, elective versus emergency care – would have been helpful.

The lack of detail is all the more striking given the overall level of ambition for efficiency improvements in Health & Social Care. The Scottish Government is targeting 3% annual ‘NHS Board Recurring Savings’, and these make up the majority of anticipated savings for this portfolio. Health boards report delivering recurring savings averaging 1.3% in 2023–24 and 2.2% in 2024–25 (Audit Scotland, 2025), although publicly available information on the nature of these and whether they are indeed efficiency savings (as opposed to cuts in provision) is limited.

IFS researchers estimate that funding efficiency (the output delivered per inflation-adjusted pound spent) for health services increased by an average of just 0.3% a year between 1997 and 2019 across the UK as a whole (Warner and Zaranko, 2024). While this estimate excludes potential efficiency savings from reductions in unnecessary appointments, tests and treatments (which would result in lower output and so not improve this measure of ‘funding efficiency’), it still illustrates how stretching a 3% efficiency target is likely to be. And while a decline in health service productivity during the pandemic means there may be scope for a bounceback in productivity over the next few years, there is a significant risk that health boards and the wider health service will struggle to deliver the expected improvements in efficiency. This would increase the pressure for top-ups to funding discussed in Chapter 1 and would make it harder to maintain or improve service quality.

Third, important information on two key targets – planned savings to administrative expenses (or ‘corporate costs’), and reductions in workforces – is omitted. The Public Service Reform Strategy (Scottish Government, 2025f) set a target of reducing corporate costs by £1 billion, or around 20%, over five years – which on a straight-line basis would imply an annual saving of around £800 million by 2028–29 (the fourth year of the plan). The Scottish Spending Review was an opportunity to provide more information on how progress towards this target would be made, and how these savings would be distributed across portfolios – and, in particular, whether the Scottish Government was avoiding the ‘salami-slicing’ approach to different departments’ contributions to administrative savings found in the UK Spending Review (see Harvey-Rich and Warner (2025)). The omission of this information makes it harder to assess the reasonableness of this target and to monitor progress. Moreover, while the Scottish Spending Review does include targets for financial savings from workforce reductions outside the NHS and councils, there is no information on the associated reductions in workforce numbers or on contributions to the overall target of a 0.5% reduction in workforce per year set out in the Fiscal Sustainability Delivery Plan.

Overall, though perhaps lacking in some areas, the information set out in the Spending Review is highly welcome and does provide greater clarity on the range of measures different parts of the Scottish Government will be taking to help improve efficiency. The challenge of delivering these plans and savings will fall largely to whoever is in government after the devolved elections in May.

… but controlling pay and employment will likely be a challenge

A key challenge the next government will face relates to the control of employment costs.

The Scottish Government restated its plans for 9% cumulative increases in pay, in cash terms, over the three years between 2025–26 and 2027–28 alongside the Budget. However, as highlighted by the Scottish Fiscal Commission (2026), two-year pay deals for 2025–26 and 2026–27 amount to an average of almost 8%, allowing for an average pay award of just 1.1% for 2027–28 (which, given expected rates of inflation, would represent a real-terms pay cut). For most NHS staff (other than doctors), an increase of less than 0.8% would be needed to remain within the 9% three-year target. Past experience and Scottish Fiscal Commission (SFC) forecasts for increases in average earnings of 2.7–2.8% a year from 2027–28 onwards suggest it will be difficult to keep public sector pay awards within these limits. Indeed, the SFC assumes pay awards will average 2.0% from 2027–28 onwards.7 Pay deals averaging 2.0% rather than 1.1% in 2027–28 would cost an additional £250 million per year, increasing the squeeze on either other areas of spending or the size of the workforce. Every additional % beyond that could cost a further £290 million per year.

Turning to employment, delivering 0.5% annual reductions in the Scottish and local government workforce could also be challenging, especially if some areas are protected from staffing cuts. Figure 5 shows the annual change in the full-time-equivalent (FTE) workforce of the Scottish Government and local government workforce by sector, averaged over the last six years since quarter 3 of 2019 (in blue) and over the last year (in red). It shows that over the last six years, the FTE workforce has grown by an average of 1.6% a year, driven by increases in the civil service (+6.2% per year, on average) and the NHS (+2.3% a year, on average). Growth has been much slower over the last year, averaging 0.2% overall, 0.7% for the NHS and 1.5% for the civil service.

Figure 5. Annual percentage change in public sector employment, by sector

Note: Total includes the listed sub-categories as well as other public bodies and public corporations that are not enumerated separately due to changing classifications. The civil service category includes the Scottish Government’s core policy staff, as well as the Crown Office & Procurator Fiscal Service (which is responsible for criminal prosecutions) and delivery agencies such as Revenue Scotland and Social Security Scotland.

Source: Public sector employment in Scotland web tables, available at https://www.gov.scot/publications/public-sector-employment-statistics-web-tables/.

Figure 5 shows that reductions in the public sector workforce are possible: further education colleges have reduced their full-time-equivalent workforce by an average of 1.9% a year over the last six years, and police and fire services by an average of 0.4% a year; and local government has reduced its FTE workforce by 0.5% over the last year. But there is still some way to go to meet the overall target of a 0.5% annual reduction: rather than increasing by 1,000 as it has over the last year, the FTE workforce would need to be reduced by 2,300. Cuts far in excess of 0.5% a year were delivered during the early 2010s – peaking at 3.8% in the year to Q3 2011 – but this was associated with significant cutbacks in service provision (especially by local government).

Protecting ‘frontline workers’ could also mean deeper cuts to other parts of the public sector workforce. No definition of ‘frontline workers’ has been provided. Suppose (conservatively) that it included school teachers (53,475 full-time equivalents) and NHS staff other than administrative staff (132,355 FTE) but no other staff.8 Together these groups of workers account for 40% of the entire Scottish Government and local government FTE workforce. Holding the workforce for these two groups constant would mean a cut to the rest of the FTE workforce averaging 0.8% – or around 2,350 – per year. Holding the teaching workforce constant and increasing the non-administrative NHS workforce in line with last year (1.0%) would increase the cut to the rest of the FTE workforce to 1.3% a year – or just over 3,600 per year. And increases in the non-administrative NHS workforce in line with the average over the last six years (2.2%) would increase the cuts to the rest of the Scottish Government and local government FTE workforce to 1.9% a year – or around 5,300 per year.

In addition to reducing the overall size of the Scottish Government and local government workforce, changes in demand for different services, and the efficiency and reform plans discussed above, will require a reshaping of the workforce. There will likely need to be increases in certain parts of the workforce (e.g. those with specialised digital skills) and larger reductions in others (e.g. those in roles where technology allows more work to be automated or undertaken by fewer people).

Thus, while the target of reducing public sector employment by 0.5% a year overall is certainly achievable, it will require political will to deliver, and will see much larger cuts in parts of the workforce – to create space within the overall total for continued increases in other parts where needs are increasing.

References

Adam, S., Boileau, B., Brogaard, M., Michael, J., Oulton, M. and Phillips, D., 2026. Immediate response to the Scottish Budget and Spending Review. IFS comment, https://ifs.org.uk/articles/immediate-response-scottish-budget-and-spending-review.

Audit Scotland, 2015. ESA 10: classification of privately funded capital projects – briefing paper. https://audit.scot/uploads/docs/report/2015/s22_151001_scottish_gov_esa10briefing.pdf.

Audit Scotland, 2020. Privately financed infrastructure investment: the Non-Profit Distributing (NPD) and hub models. https://audit.scot/publications/privately-financed-infrastructure-investment-the-non-profit-distributing-npd-and-hub.

Audit Scotland, 2025. NHS in Scotland 2025: finance and performance. https://audit.scot/publications/nhs-in-scotland-2025-finance-and-performance.

Boileau, B. and Phillips, D., 2025. The overall funding and spending outlook. In D. Phillips (ed.), The IFS Scottish Budget Report 2025–26, https://ifs.org.uk/publications/ifs-scottish-budget-report-2025-26.

Fraser of Allander Institute, 2026. More on the 2026–27 Scottish Budget. https://fraserofallander.org/more-on-the-2026-27-scottish-budget/.

Harvey-Rich, O. and Warner, M., 2025. The outlook for public sector productivity. In C. Emmerson, K. Ogden and B. Zaranko (eds), The IFS Green Budget October 2025. https://ifs.org.uk/publications/outlook-public-sector-productivity.

HM Government and Scottish Government, 2023. Fiscal framework: agreement between the Scottish and UK Governments. https://www.gov.scot/publications/fiscal-framework-agreement-between-scottish-uk-governments/.

HM Treasury, 2025a. Spending Review 2025. https://www.gov.uk/government/publications/spending-review-2025-document/spending-review-2025-html.

HM Treasury, 2025b. Budget 2025. https://www.gov.uk/government/publications/budget-2025-document/budget-2025-html.

Investor Panel, 2023. Mobilising international capital to finance the transition to Net Zero. https://www.gov.scot/publications/investor-panel-mobilising-international-capital-finance-transition-net-zero/.

Scottish Fiscal Commission, 2026. Scotland’s economic and fiscal forecasts – January 2026. https://fiscalcommission.scot/publications/scotlands-economic-and-fiscal-forecasts-january-2026/.

Scottish Government, 2025a. Autumn Budget Revision 2025-2026: supporting document. https://www.gov.scot/publications/2025-26-autumn-budget-revision-supporting-document/.

Scottish Government, 2025b. Scotland’s fiscal outlook: medium-term financial strategy. https://www.gov.scot/publications/scotlands-fiscal-outlook-scottish-governments-medium-term-financial-strategy-3/.

Scottish Government, 2025c. Scottish Government bonds launch planned. https://www.gov.scot/news/scottish-government-bonds-launch-planned/.

Scottish Government, 2025d. Scottish Government bonds programme: outline business case summary. https://www.gov.scot/publications/scottish-government-bonds-programme-summary-outline-business-case/.

Scottish Government, 2025e. Fiscal Sustainability Delivery Plan. https://www.gov.scot/publications/scottish-governments-fiscal-sustainability-delivery-plan/.

Scottish Government, 2025f. Scotland’s Public Service Reform Strategy: delivering for Scotland. https://www.gov.scot/publications/scotlands-public-service-reform-strategy-delivering-scotland/.

Scottish Government, 2025g. Health & Social Care Service Renewal Framework 2025-2035. https://www.gov.scot/publications/health-social-care-service-renewal-framework/.

Scottish Government, 2025h. Scotland’s Population Health Framework. https://www.gov.scot/publications/scotlands-population-health-framework/.

Scottish Government, 2025i. Pupil and teacher characteristics 2025. https://www.gov.scot/publications/pupil-and-teacher-characteristics-2025/.

Scottish Government, 2026a. Scottish Budget 2026 to 2027. https://www.gov.scot/publications/scottish-budget-2026-2027/.

Scottish Government, 2026b. Scottish Spending Review 2026. https://www.gov.scot/publications/scottish-spending-review-2026/.

Scottish Government, 2026c. Spring Budget Revision 2025-26 – supporting document. https://www.gov.scot/publications/spring-budget-revision-2025-26-supporting-document/.

Scottish Government, 2026d. Infrastructure Strategy 2027-2037: consultation. https://www.gov.scot/publications/consultation-infrastructure-strategy-2027-2037/.

Scottish Government, 2026e. Infrastructure Delivery Pipeline 2026. https://www.gov.scot/publications/infrastructure-delivery-pipeline-2026/.

Warner, M. and Zaranko, B., 2024. The fiscal implications of public service productivity. IFS report, https://ifs.org.uk/publications/fiscal-implications-public-service-productivity.

Endnotes

Authors

Bee Boileau

Bee joined the IFS in 2021 as a Research Economist and works in the Retirement, Saving and Ageing sector.

Martin Brogaard

Martin joined the IFS in 2025 and works in the IOD sector, researching consumer behaviour and nutrition. He also works on devolved government policy.

David Phillips

David is Head of Devolved and Local Government Finance. He also works on tax in developing countries as part of our TaxDev centre.

More from IFS

Understand this issue

Policy analysis

Academic research