Downloads

Download report PDF

PDF | 480.28 KB

Executive summary

The upcoming Spending Review will involve some very difficult decisions on public service spending, with virtually no headroom against the government’s fiscal rules. The government has set out plans for overall departmental spending to grow by about 1.2% per year in real terms between 2025–26 and 2028–29. However, after accounting for the likely cost of existing commitments on defence, health and childcare, IFS analysis suggests that ‘unprotected’ spending will fall by about 1% per year in real terms between 2025–26 and 2028–29, or by about 3% in total. This currently includes most spending by the Department for Education (DfE), excluding the early years and childcare. This report focuses on the choices and challenges facing policymakers on education in the upcoming Spending Review, with a particular focus on schools and colleges.

Key findings

- If the DfE is treated as an ‘unprotected’ area it could face a 3% real-terms cut to its budget over the next Spending Review period. Delivering such a cut – equivalent to £2.6 billion – would involve difficult trade-offs. Spreading the cut evenly would reduce school, college and adult education funding. Protecting schools and the 16–19 education budget in colleges, as policymakers have often done, would require a more than 20% cut across areas such as adult education, apprenticeships and higher education support. Protecting those areas as well would force cuts of up to 50% to other education spending, such as on universal infant free school meals or the physical education (PE) and sport premium, likely ending some programmes entirely.

- Falling pupil numbers in schools means that protecting the overall schools budget in England in real terms would allow for a 3% increase in per-pupil funding between 2025–26 and 2028–29. Protecting per-pupil funding instead would allow for a £2 billion or 3% cut to school spending, exactly in line with the potential 3% cut in ‘unprotected’ public service spending over the same period.

- Since 2019–20, total school funding has grown by about £9 billion or 16% in real terms. However, about half of this has been taken up by the growing costs of special educational needs provision. Schools have faced rising employer costs, rising energy costs and increasing salary costs. Excluding high-needs funding, mainstream school funding per pupil grew by 37% between 2019–20 and 2025–26. This compares with 38% growth in the costs faced by schools over the same period.

- Schools face a particularly tight set of pressures in 2025–26. Mainstream school funding per pupil is expected to grow by 5.8% in cash terms (including £800 million in compensation for increases in employer national insurance and £615 million to partially cover the costs of 2025 pay settlements). However, school costs are expected to grow by 6.5%, including pay offers of 4% for teachers and 3.2% for support staff. Schools would need to make efficiency savings of £300–400 million to afford these pay rises from existing budgets.

- Spending on pupils with special educational needs is forecast to rise by over £2 billion between 2025–26 and 2027–28, driven by projected growth in entitlements. This will make it harder for schools to deliver any savings over the next few years.

- In contrast to schools, rising student numbers in further education and sixth forms mean that maintaining per-student funding would require an additional £290 million. Protecting the total 16–19 budget would result in a 3% decline in funding per student.

- Colleges have faced significant financial pressures over the last 15 years. Between 2009–10 and 2019–20, funding per student aged 16–19 in colleges fell by 14% in real terms. Although additional funding has been allocated to further education in recent years, spending in 2024–25 remained 13% below 2009–10 levels. The government has set out an additional £540 million of funding in 2025–26, which will keep funding per student flat in real terms relative to 2024–25.

- The government has pledged to recruit 6,500 additional teachers by the end of this Parliament. It is also not yet clear how they would be split across primary schools, secondary schools and colleges. There is evidence that additional teachers are needed in secondary schools, with particular shortages in maths, science and languages. However, the need for additional teachers in further education colleges is even more acute. According to DfE estimates, between 8,400 and 12,400 additional teachers will be needed by 2028–29 relative to 2020–21 levels. Meeting the 6,500-teacher pledge through colleges alone would fall short of the rising need for college teachers. This high projected need is driven both by rising student numbers and by persistent recruitment and retention challenges. A key factor is pay: college teachers earn, on average, £7,000 (or 18%) less than their counterparts in schools.

1. Introduction

On taking office, the new government initially provided a significant boost to public service spending levels in both 2024–25 and 2025–26. However, public service spending plans after 2025–26 remained tight. As a result, the upcoming Spending Review is going to be a delicate fiscal balancing act with many difficult trade-offs. Even after a small reduction in the planned real-terms growth in public spending after 2025–26 from 1.3% to 1.2% per year, the government has virtually no headroom against its fiscal rules and the Chancellor has ruled out further tax rises. While the government could get lucky on growth, there is every chance that global events weigh on the UK’s economic prospects. At the same time, the government has high ambitions and faces strong demands to improve public services, particularly in health and defence. Within this tight fiscal context, government departments may ultimately be asked to deliver savings or absorb pressures within flat or falling budgets.

Behind health, education spending is the second largest element of public spending to be covered by the Spending Review. Decisions on education spending will have consequences for the government’s high ambitions for education, as well as the spending settlements for other areas of public services. The government’s main objective on education is the opportunity mission to improve social mobility. The government also has a high-profile commitment to increase teacher numbers by 6,500 and is rolling out free breakfast clubs across schools.

The government faces some growing challenges and demands on education spending. There has been rapid growth in the number of pupils identified with special educational needs and disabilities (SEND) over the last seven years, which has put huge pressure on funding and spending. There is also a backlog of repairs to school buildings, which came to the forefront of public debate in the re-enforced autoclaved aerated concreate (RAAC) crisis of September 2024. Falling numbers of school pupils may ease the pressures on spending, but falling rolls are also testing the financial sustainability of some schools. Improving economic growth will likely require improvements to skills and training, but colleges and adult education have faced significant spending cuts over the last 15 years. The government’s objectives on higher education are less clear, but many universities are facing financial challenges.

With these constraints and challenges in mind, this report outlines the key trade-offs and likely settlements for education in the upcoming Spending Review. We focus on schools and colleges, as these are the main areas of education spending that will be determined in the Spending Review. Large elements of early years spending are already determined and reflect the government’s commitment to the expanded early years entitlement, although it could still top up other elements of early years and family spending. Much spending on higher education is in the form of student loans, and appears differently in the national accounts compared to the day-to-day departmental spending that is typically set through a spending review process.

We start by setting out the baseline for spending up to 2025–26 and the actions the government has already taken, particularly on schools and colleges. We then explore the pressures likely to shape spending over the next Spending Review period (2026–27 to 2028–29). In the final section, we consider the implications of different spending options in light of the government’s priorities and wider fiscal constraints.

All of our analysis relates to education spending in England only. Decisions in the upcoming Spending Review will only directly affect England in the first instance. The overall level of spending across all public services will then shape the size of the block grants received by the devolved administrations. Decisions on education spending in Wales, Scotland and Northern Ireland will be made by the devolved administrations in light of these block grants.

2. Setting the baseline: education spending to 2025

To understand the trade-offs and choices facing education spending in the upcoming Spending Review, it is important to start with a clear picture of the DfE’s budget and the recent pressures on spending. The Spending Review determines only spending under direct departmental control – known as Departmental Expenditure Limits or DEL. Other areas of departmental spending fall under Annually Managed Expenditure (AME), which covers entitlement-based and demand-driven costs, such as teachers’ pensions in payment.

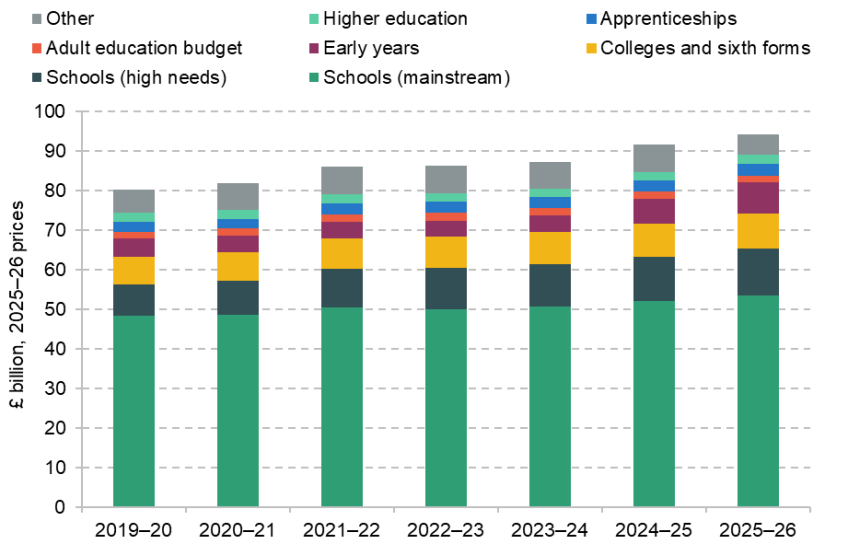

With this in mind, Figure 1 shows day-to-day or resource DEL spending by the DfE from 2019–20 through to 2025–26 (we cover capital spending later in this report). Total day-to-day DEL spending by the DfE has increased from about £80 billion in 2019–20 to around £94 billion in 2025–26 (all in 2025–26 prices). This represents a substantial £14 billion or 17% real-terms increase over the five-year period, with a 3% real-terms rise in the most recent year of 2025–26.

Figure 1. DfE resource spending up to 2025–26 in England

Source: The DfE DEL figures are taken from HM Treasury, Spring Statement 2025 and Public Expenditure Statistical Analyses 2024. School spending, college and sixth form funding, adult education and apprenticeship spending up to 2024–25 taken from Drayton et al. (2025). Adult education in 2025–26 estimated by applying a 6% cash-terms cut to the non-devolved budget in 2024–25 and a 3% cash-terms cut to the devolved budget in 2024–25. Apprenticeship spending in 2024–25 and 2025–26 from Main Supply Estimates 2025 to 2026. Higher education DEL spending taken from DfE Annual Report and Accounts (various years).

The single largest element of spending is the core schools budget, which is due to total about £65 billion in 2025–26 and represents about 70% of the total day-to-day budget for the DfE. This has increased by £9.2 billion or 16% in real terms since 2019–20, with a 3.5% real-terms rise in the latest year of 2025–26. Interestingly, almost half of the overall rise in school funding can be explained by a £4 billion or 50% real-terms growth in funding for high needs. This leaves a rise of about £5 billion in mainstream school funding, and £2.3 billion of this reflects extra funding since 2019–20 to cover the costs of higher employer pension contributions and employer national insurance contributions. The underlying real-terms increase in actual resources in mainstream schools between 2019–20 and 2025–26 is therefore closer to £3 billion or 6%. This picture of seemingly large increases taken up by rising costs of high needs and other school costs will be a familiar picture throughout this report.

The next largest element of the DfE budget relates to funding for 16–19 year olds in colleges and sixth forms. This totalled £8.8 billion in 2025–26 or 9% of the total DfE budget. This is an increase of £1.6 billion or 22% in real terms from 2019–20, with a 3.5% or £300 million rise in 2025–26.

Looking at the other elements of the budget, the next largest element of spending is funding for the early year and childcare entitlement. This represented about £4.5 billion in 2019–20 and initially fell in real terms up to 2021–22. Since then, it has grown significantly as the early years entitlement has been gradually expanded to younger children. Total funding is expected to reach £8 billion for 2025–26. The government is committed to continuing this expansion, with funding expected to reach £9 billion by 2027–28.

The apprenticeship budget then totals about £3.1 billion in 2025–26, which is up by £600 million compared with 2019–20. The adult education budget is about £1.5 billion in 2025–26, which is down from £1.8 billion in 2019–20. This mainly funds statutory entitlements to access education and training for adults with low levels of existing education or limited financial resources to access education.

In addition, there is about £2.2 billion of funding for higher education within the DfE resource DEL. This comprises about £1.5 billion in grants to higher education providers and around £700 million for student support. This upfront funding for higher education is down from about £2.4 billion in 2019–20 (in today’s prices).

However, this is not the full cost of higher education to government. A majority of funding for teaching is in the form of tuition fees, for which most students can access a government-backed student loan, and the vast majority of support for students with their living costs is through maintenance loans. The government expects to issue around £22 billion in student loans in England in 2025–26, of which some portion will be repaid and some eventually written off.1 These write-offs are listed separately in government accounts and not traded off explicitly by the DfE within the spending review process. The funding for higher education within the DfE resource DEL is complementary to this; for example, topping up funding from tuition fees to support the teaching of high-cost subjects, and providing additional support to disabled students or those with childcare responsibilities.

This leaves about £5 billion on other elements. This includes a range of programmes, such as universal infant free school meals, support for PE in schools, support for adoption and fostering, and teacher training bursaries.

Looking at the budget as a whole, we see some very clear implications for the choices facing policymakers in the upcoming Spending Review. The government has already committed to expansion of the early years entitlement. It is also likely that policymakers will strive to avoid cuts to schools and college funding if they can. However, this already accounts for £82 billion or 87% of the DfE budget. Policymakers could choose to cut other elements, such as apprenticeships, adult education or higher education support, but these are smaller areas of spending that have already been subject to cuts in recent years. This leaves £5 billion in other spending. This has also been cut in recent years, and making significant cuts here would probably require cutting entire programmes.

In the rest of this section, we focus on the current pressures facing schools and colleges, which are the largest elements of spending by the DfE.

Schools

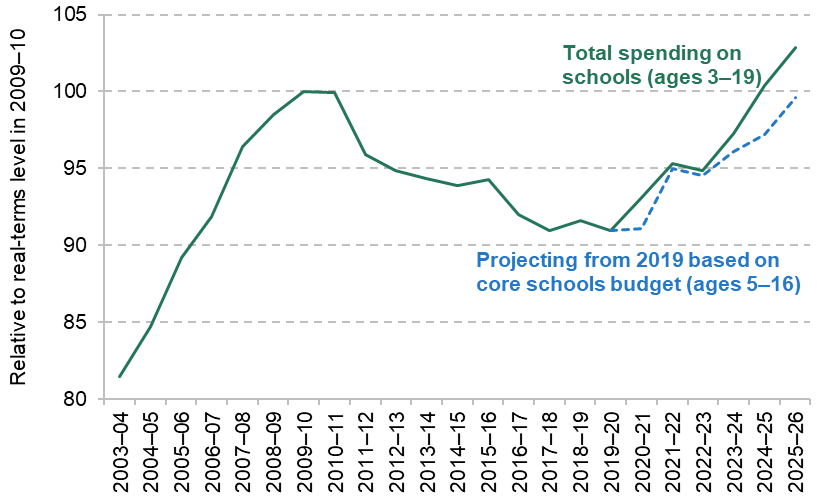

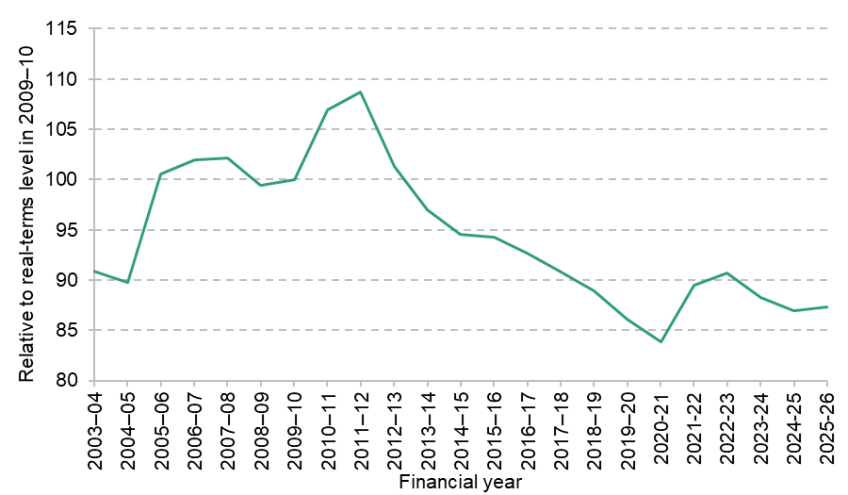

In Figure 2, we show the level of school spending per pupil in England in real terms (relative to its level in 2009–10). This is based on our measure of total school spending by schools and local authorities across pupils ages 3–19, which includes nursery and sixth form spending for consistency as this is treated as school spending in past years. As can be seen, spending per pupil rose significantly in real terms during the 2000s to reach a high point around 2009–10. After that, it fell by 9% in real terms up to 2019–20. Since then, it has risen again in real terms and was back above 2009–10 levels in 2024–25. Further growth is expected in 2025–26, making for total real-terms growth of 13% since 2019–20 and 2.5% growth specifically in 2025–26.

Figure 2. Growth in school spending per pupil in England and costs between 2019–20 and 2025–26 under various definitions

Source: See Methods and data for cash-terms spending per pupil up to 2024–25. Cash-terms spending per pupil for 2025–26 based on the core schools budget (excluding pensions and employer national insurance grants) published in the Autumn Budget 2024 and National pupil projections. HM Treasury, GDP deflators, March 2025.

As shown by the dashed line, we project school spending per pupil based on total national funding in the core schools budget (as detailed in Figure 1). This shows slower growth of 9.5% since 2019–20. This partly reflects the fact that some of the growth spending on 3–19 year olds has been focused on the early years spending and that local authorities have ended up actually spending more on high needs because of legal entitlements.

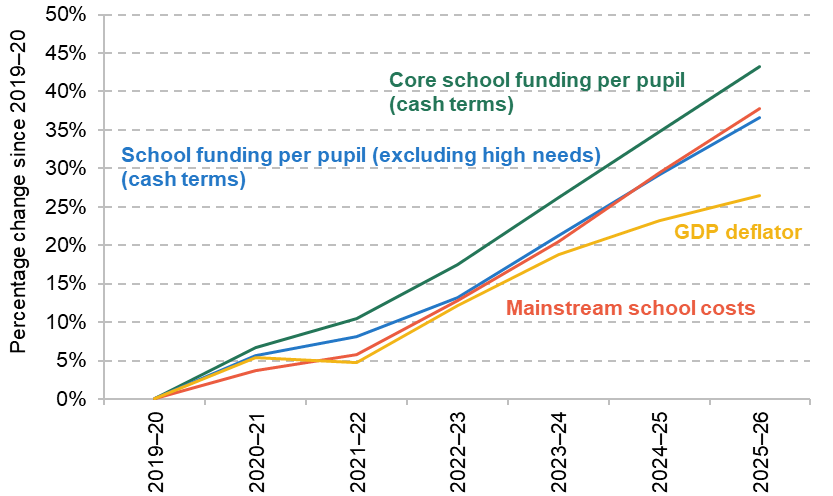

In Figure 3, we consider trends since 2019–20 in further detail. We show the level of cash-terms school funding per pupil relative to its level in 2019–20. This has grown by 43% up to 2025–26. This exceeds the 27% growth in the GDP deflator measure of economy-wide inflation over the same period, meaning that spending per pupil has grown by 13% in real terms over this period.

Figure 3. Growth in school spending per pupil and costs between 2019–20 and 2025–26 under various definitions in England

Note and source: School funding figures are based on the core school budget and high-needs funding detailed in Figure 1. School costs are calculated as the weighted average of teacher pay, other staff pay and non-staff costs, with the methods and approach closely aligned to methods used in the DfE schools’ costs: technical note. ‘Teacher pay’ is based on a weighted average of paybill per head growth of 2.75% in September 2019, 3.1% in September 2020, 0% in September 2021, 5.4% in September 2022, 6.5% in September 2023, 5.5% in September 2024 and 4% for September 2025. Assumed pay drift of 0.2% in 2021–22, −0.2% in 2022–23, 0.4% in 2023–24, 0.3% in 2024–25, 0.3% for 2025–26 and zero for all other years. Increase in teacher costs includes the rise in employer pension contributions from September 2019 and April 2024, and employer National Insurance rises from April 2025. Pay per head figures do not include the temporary Health and Social Care Levy during 2022–23. Increases in costs of other staff pay per head taken from DfE schools’ costs technical notes: 2020 to 2021, 2021 to 2024, 2023 to 2025, and 2024 to 2026. Pay drift and pensions costs for other staff also match the assumptions in the schools’ costs technical notes. Other costs assumed to grow in line with actual CPI inflation up to 2023–24 and Office for Budget Responsibility forecasts after that, as detailed in the Office for Budget Responsibility’s Economic and Fiscal Outlook, March 2025. As assumed in DfE schools’ costs technical notes, 2022 to 2024, 2023 to 2025 and 2024 to 2026, we also add additional amounts for the rising costs of special educational needs provision (0.6% in 2022–23, 0.5% in 2023–24, 0.3% in 2024–25 and 0.6% in 2025–26). HM Treasury, GDP deflators, March 2025.

This, however, is not the full story. As we have seen, a very significant element of the increase in school funding since 2019–20 has been focused on the high-needs budget. Once we exclude high-needs funding, the cash-terms increase in mainstream school funding per pupil since 2019–20 is lower at 37%. On the other side of the ledger, school costs have risen faster than overall inflation due to increases in employer pension contributions in 2020 and 2024, employer national insurance rises from April 2025, rising costs of special educational needs provision, energy costs and rising salary costs. Once we account for these, we estimate that mainstream school costs have risen by 38% since 2019–20. This would indicate no real-terms increase in the resources in mainstream schools since 2019–20.

Focusing on the latest year in particular, we estimate that school costs will grow by 6.5% in 2025–26. This includes confirmed pay rises from September 2024, increases in employer national insurance (schools were explicitly compensated with a £800 million grant for these costs) and forecast inflation. It also includes recently confirmed pay increases of 4% for teachers from September 2025 and 3.2% for support staff from April 2025.2 In contrast, mainstream school funding per pupil is expected to rise by the lower amount of 5.8% (including compensation for employer national insurance rises and the extra £615 million provided to schools to partially cover the cost of the teacher and support staff pay rises). The faster growth in school costs means that schools will effectively need to make efficiency savings of around £300–400 million, or about 0.7% of their budgets, in order to afford the pay rises.

Making efficiency savings is likely to be more challenging for schools given recent pressures. Between 2009–10 and 2019–20, school spending per pupil fell by 9% in real terms and schools would have had to have sought savings as a result. This is true whether we use the GDP deflators or school costs as a measure of inflation (Britton et al., 2020). Since 2019–20, mainstream school funding has grown relative to the GDP deflator, but only just about kept pace with school costs in most years. This divergence between the GDP deflator and school costs reflects a range of factors, including: the exclusion of the rising cost of imported energy from the GDP deflator; the rising costs of special educational needs provision; and extra employer costs, such as pension contributions and employer National Insurance.

Colleges and sixth forms

Figure 4 illustrates real-terms spending per student aged 16–19 in further education, indexed to its 2009–10 level. The primary source of funding for colleges and sixth forms in England is the 16–19 education budget. This accounted for 59% of college income in 2022–23 (the most recent year for which college accounts data are available3) with the remainder coming through adult education and apprenticeship funding (23%), private income for education (11%) and other sources, such as commercial income, which accounted for 5%.

Figure 4. Growth in 16–19 education spending per pupil in England (actual and projected for 2025–26)

Note and source: See Methods and data for cash-terms spending per pupil up to 2024–25. Cash-terms spending per pupil forecast for 2025–26 based on figures published in the Autumn Budget 2024, the May 2025 government announcement and Office for National Statistics national population projections. HM Treasury, GDP deflators, March 2025.

As with school spending, 16–19 spending per pupil increased in real terms during the 2000s, although it peaked later in 2011–12. In the decade between 2009–10 and 2019–20, spending per student declined by 14% in real terms. The previous government allocated an additional £2.3 billion in cash terms between 2019 and 2024 to increase funding relative to 2019 (Drayton et al., 2025), but rising student numbers and inflation limited any real-terms gains. In the current academic year, 2024–25, spending remains 13% below 2009–10 levels.

The planned changes to employer National Insurance contributions announced in the 2024 Budget will affect colleges as well as schools. To offset the impact, the government has announced £155 million in funding for post-16 schools, academies and colleges,4 which we estimate should be sufficient to cover the additional costs for these providers. In the 2024 Autumn Budget,5 the government also announced an additional £300 million for further education (an 3.5% increase in cash terms). From this total, £250 million will be used to raise the 16–19 funding rate by 3.8% in the 2025–26 academic year.6 A further £50 million was announced as a grant to support pay awards for further education teachers. This appears to be a one-off grant, which colleges may be expected to sustain from their existing budget in future years. With around 55,000 teachers across further education and sixth form colleges in England and a median salary of approximately £35,000 in further education colleges,7 this grant should enable a pay increase of roughly 2–3% this academic year. In May 2025, the government announced a further £190 million to support colleges and other 16–19 providers in the 2025–26 financial year.8 Taken together, the additional funding for 2025–26 means that spending per pupil will remain constant in real terms and about 13% below its level in 2009–10.

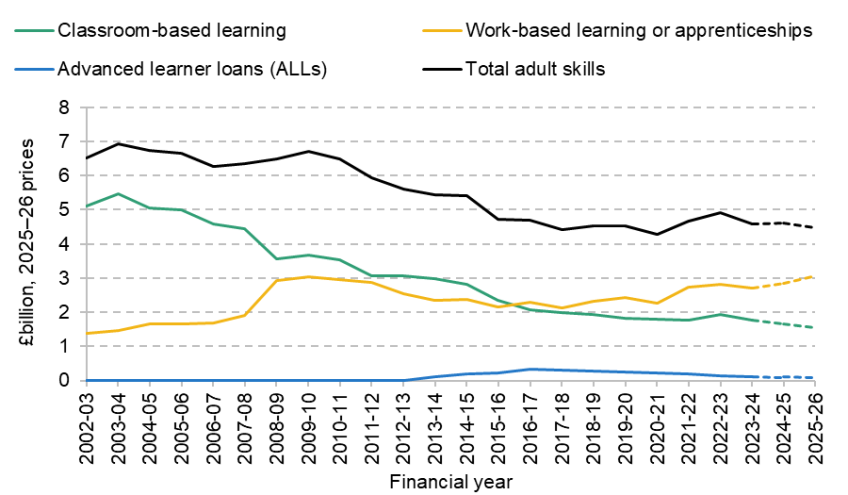

Figure 5 presents public spending on adult education and skills. This funding source accounted for approximately a quarter of total college income in 2022–23 (the latest year for which college accounts data are available9). Unlike schools or 16–19 education, it is not meaningful to present adult education spending on a per-student basis, due to the wide variation in programmes of study and types of learners. Instead, the figure shows total spending broken down into three components: classroom-based learning (primarily statutory entitlements for individuals with low qualifications or limited resources), work-based learning or apprenticeships (this is mainly used for employer subsidies to support the cost of apprentice training) and initial public outlay on further education loans.

Figure 5. Public spending on adult education and skills (actual and projected for 2024–25 and 2025–26)

Note and source: See source for figure 4.6 in Drayton et al. (2025) for figures up to 2023–24. The 2024–25 forecast for classroom-based spending assumes a freeze in cash terms relative to 2023–24. For 2025–26, we model a 6% cash-terms reduction in the non-devolved adult skills fund and a 3% cash-terms reduction in the skills budget for devolved areas. The forecast for spending on work-based learning or apprenticeships in 2024–25 and 2025–26 is from Main Supply Estimates 2025 to 2026. Forecasts for Advanced Learner outlays in both 2024–25 and 2025–26 assume cash-terms spending remains unchanged from 2023–24. HM Treasury, GDP deflators, March 2025.

Public funding for adult skills has declined significantly since its peak in the early 2000s, which has coincided with a steep decline in the number of adult learners. The number of publicly funded classroom-based qualifications taken by adults in England fell from 5.6 million in 2004–05 to just 2.3 million in 2023–24, which is a 58% reduction (Drayton et al., 2025). In part, this reflects deliberate government decisions to withdraw funding for low-level and non-regulated courses, which often have low returns in the labour market. The previous government allocated an additional £900 million in day-to-day funding for adult education in 2024–25 compared with 2019–20 as part of the 2021 Spending Review (Drayton et al., 2025), but overall spending remains well below historical levels in real terms. In the final year of the current Spending Review period, 2024–25, total spending is projected to reach approximately £4.6 billion – around a third lower in real terms than the £6.9 billion peak in 2003–04. The reduction has been particularly severe in classroom-based learning, where expenditure has fallen by 70% from £5.5 billion in the early 2000s to £1.7 billion in 2024–25.

The funding allocations for the Adult Skills Fund in 2025–26 have not been confirmed yet, but DfE guidance appears to suggest there will be a 6% cash-terms cut to the non-devolved adult skills fund10 and reports suggest a 3% cash-terms cut to the devolved adult skills fund.11 This would mean the overall budget for classroom-based learning would decline by around 7% in real terms between 2024–25 and 2025–26. While classroom-based provision is expected to face further reductions, the apprenticeship budget is set to rise by 8.5% in real terms, increasing from £2.8 billion to £3.1 billion in 2025–26. The overall effect is to keep total adult skills funding relatively flat between 2024–25 and 2025–26, but with a clear shift toward funding apprenticeships.

3. Pressures on the education budget

The Spending Review comes at a time of constrained public finances and mounting pressures across the education system. Schools and colleges face a shared set of pressures that will shape the demands placed on the education budget over the coming years. Demographic change, workforce challenges, rising special educational needs, and the condition of the education estate all raise difficult trade-offs for policymakers. This section sets out the main challenges likely to drive cost pressures over the next Spending Review period and the scope for making savings in light of these challenges.

Demographic change

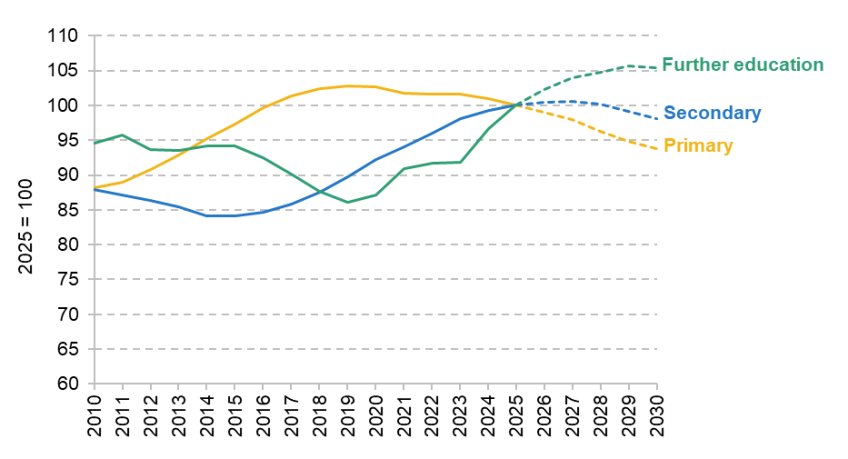

In state-funded primary and secondary schools, pupil numbers are projected to fall by 3% between January 2025 to January 2029 (Figure 6). This decline is concentrated in primary schools, where enrolment is expected to drop by 5% while numbers in secondary schools remain broadly stable, although these projections are subject to significant uncertainty. This demographic shift could create some fiscal headroom; for example, if per-pupil spending were held constant in real terms, it could deliver annual savings of around £2 billion by 2028–29.

Figure 6. Indexed actual and projected pupil numbers in England, 2010–30, 2025 = 100

Source: Actual and projected primary/secondary pupil numbers from 2010 to 2028 from National pupil projections, reporting year 2024. Further education numbers from 2010 to 2025 from Drayton et al. (2025). Projections are extended to 2035 using projected percentage changes in the relevant age group derived from Office for National Statistics 2022-based population projections by year of age.

In contrast, pupil numbers in further education are projected to rise by 6% over the same period. This increase will place upward pressure on spending in the sector, potentially offsetting savings from schools and requiring significant additional investment just to maintain current per-student funding levels.

Looking first at schools, there are of course practical difficulties associated with cutting total school spending by freezing it in per-pupil terms. Many elements of spending may not be particularly variable in the very short run. For instance, if classes cannot be amalgamated or cut, then it may not be possible to reduce staff numbers by as much as the total change in pupil numbers would imply. School closures could allow for sharper reductions in spending, but they can be highly disruptive for both pupils and staff. Nonetheless, with current Office for National Statistics projections indicating that primary school enrolment will continue to decline until 2034, closures may become unavoidable in areas where schools are no longer financially viable. This is more true of some places than others: inner London is projected to see a 10% fall in primary school rolls from 2025 to 2029 whereas the East Midlands is projected to see a rise in numbers.12 School closures may also be more difficult in a system where many schools are Academies or part of Multi-Academy Trusts, and thus mostly outside of local and central government control.

For further education, it may difficult to scale provision quickly enough to meet rising demand. Colleges often face constraints on physical capacity, staffing and course provision, which can make it difficult to expand enrolment efficiently. Recruiting qualified teachers – already a major challenge in the sector – will become even more pressing as student numbers grow.

Workforce recruitment and renumeration

The government has pledged to recruit 6,500 additional teachers in key subjects across schools and colleges by the end of this Parliament. While the precise benchmark for ‘additional’ is unclear, it is likely to refer to a net increase in the full-time equivalent workforce relative to 2024 levels. It is also not yet clear how these teachers will be split across primary schools, secondary schools and colleges.

There is evidence that additional teachers are needed in secondary schools, where pupil numbers are close to their peak. Vacancies have risen from a rate of around 0.1% to 0.8% from 2010 to 2024, translating into 1,850 vacant teaching positions in secondary schools for the 2023–24 academic year (DfE, 2024). Vacancy numbers are highest for core subjects such as maths and English, and vacancy rates are highest for modern foreign languages and design and technology. Teacher numbers have also not kept pace with student numbers: pupil–teacher ratios in secondary schools have risen from 14.8 to 16.8 over this period (DfE, 2024). According to the National Audit Office (2025), the DfE estimates that 1,600 more secondary teachers will be needed between 2024 and 2028.

Recruiting secondary school teachers – particularly in shortage subjects – has proven challenging. Initial teacher training targets, particularly for secondary schools, have been repeatedly missed over the past four years; 2024–25 saw 62% of the target for postgraduate initial teacher trainees actually recruited, translating into nearly 9,000 fewer teachers starting training than aimed for. A wide range of subjects, from physics to music, saw less than half of targeted numbers recruited in 2024. Forecasts for 2025–26 suggest that under-recruitment is likely to continue (McLean and Worth, 2025). Simply raising initial training targets is therefore unlikely to aid progress to the 6,500 target.

The need for additional teachers in further education colleges is even more acute. In 2022–23, around 5% of teaching posts in the sector were vacant – equivalent to approximately 3,400 unfilled positions.12 According to DfE estimates, between 8,400 and 12,400 additional teachers will be needed by 2028–29 relative to 2020–21 levels (National Audit Office, 2025). Meeting the government’s 6,500-teacher pledge through colleges alone would therefore fall short of addressing the rising need for college teachers. This high projected need is driven both by demographic pressures and by persistent recruitment and retention challenges. A key factor is pay: college teachers earn, on average, £7,000 (or 18%) less than their counterparts in schools (Drayton et al., 2025), making the sector less attractive to qualified teaching staff.

Financial incentives – most notably higher teacher pay – remain a central tool for improving recruitment and retention (National Audit Office, 2025). However, raising base salaries to meet the target of 6,500 additional school teachers would likely be expensive and subject to considerable uncertainty. Above-inflation pay rises could also reduce the scope for savings elsewhere in the schools budget. Furthermore, the government does not set college teacher pay and so pay increases for school teachers could risk widening the pay gap between sectors. Alternative approaches, such as targeted incentives for specific subjects or regions, have strong evidence of effectiveness, but could still carry significant costs: the National Foundation for Educational Research estimates that such measures would amount to around £800 million per year (Worth and Tang, 2024). Other potential changes – such as reducing workload – could be valuable if implemented, but may be harder for government to directly influence.

Rising special educational needs numbers

The rapidly increasing number of pupils recognised as having SEND will be a significant spending pressure on the schools budget as long as the high-needs system is not reformed. We summarise the main issues below; further details can be found in our recent briefing (Sibieta and Snape, 2024) and in the overview from the National Audit Office (2024).

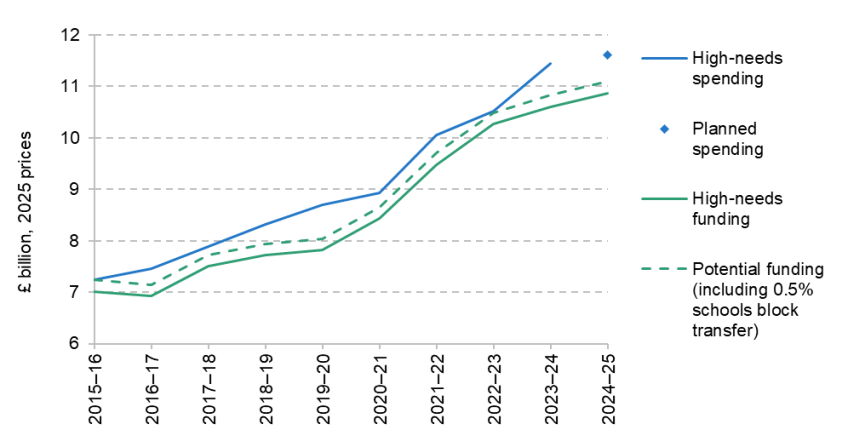

High-needs spending has risen in real terms by an average of £520 million each year since 2015–16, and is now about £4.2 billion or 58% higher in real terms than a decade ago (Figure 7). As we saw earlier, the cost of high-needs funding can account for about half of the total growth in school funding since 2018. Furthermore, the rise in actual spending has outpaced the rise in funding, resulting in large council deficits (National Audit Office, 2024).

Figure 7. High-needs spending and estimated funding, 2015–16 to 2024–25

Note and source: Taken from figure 7 in Sibieta and Snape (2024), updated to reflect actual spending for 2023–24 and using 2024–25 prices from HM Treasury, GDP deflators, March 2025. 2023–24 spending for Cumberland and Westmorland and Furness is not yet reported and so imputed using Cumbria’s 2022–23 spending.

This is mainly due to the growing identification of high-needs pupils with legally binding support set out in Education, Health and Care Plans (EHCPs), which are intended for pupils with the most severe needs. The number of pupils with these plans has risen from 237,000 in 2016 to 434,000 in 2024 and shows no sign of slowing. As such, costs should be expected to continue rising unless the system is dramatically reformed.

Government forecasts quoted by the National Audit Office show that high-needs spending is expected to grow by over £2 billion between 2025–26 and 2027–28 in today’s prices, which is purely as a result of projected growth in entitlements. The government provided an additional £1 billion in high-needs funding for 2025–26. Even with this extra funding, if high-needs funding were frozen at current levels, the funding gaps for high needs would likely rise to about £2.3 billion in 2027–28, and to probably even more up to 2028–29. This is on top of significant deficits that have already been amassed. These have been kept off councils’ books by a ‘statutory override’, an accounting fudge due to end in March 2026 when cumulative deficits are estimated to total around £5 billion (County Councils Network, 2025).14 Many councils would not be able to pay these debts if the override did come to an end in 2026 – it may therefore prove necessary for central government to bail them out or extend the override once again.

Given the scale of the financial pressures, it is clear that the high-needs system needs reform – either to give councils the resources to meet rising costs or to bring down demand for high-needs spending. This would likely come with significant challenges and additional short-run costs; see Sibieta and Snape (2024) for further discussion. Nonetheless, without meaningful change, there is a serious risk that costs and deficits will continue to escalate over the long run. This is particularly because, under the current system, spending on EHCPs (for instance, to employ teaching assistants) is protected by legal entitlement; such legal protections make it particularly difficult for schools to find savings.

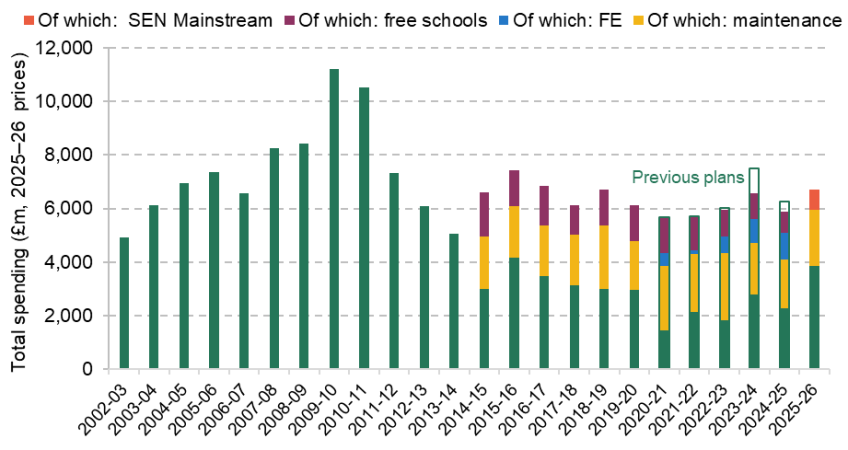

Capital spending

Lastly, we examine capital spending on buildings and maintenance across schools and colleges. Figure 8 presents historical trends in education capital spending in England from 2002–03 through to planned allocations for 2025–26. For recent years, the figure also breaks down capital spending by key components, including school maintenance and repair, free schools, and further education colleges (where data are available). Prior to 2020, the vast majority of capital spending was concentrated on schools.

Figure 8. Education capital spending in England over time, actual and plans in 2025–26 prices

Note and source: Public Expenditure Statistical Analyses 2024, 2023, 2020, 2019, 2014, 2013, 2010 and 2008. Capital spending on further education (FE) capital and free schools taken from DfE supplementary and main estimates (various years). School maintenance and repair spending taken from school capital funding. 2025–26 plans taken from HM Treasury, Autumn Budget 2024. HM Treasury, GDP deflators, March 2025.

Total capital spending on education in England was about £5.9 billion in 2024–25. About £1.8 billion was devoted to school maintenance and repair, £800 million was spent on free schools, £1 billion was spent on rebuilding further education colleges, with about £2.3 billion on new schools and other aspects of capital spending. Interestingly, the actual level of capital spending has been lower than the planned level for the past three years, particularly in 2023–24. This is likely to reflect the significant delays in the school rebuilding programme.15 Money for these delayed projects will either need to come out of allocations from 2025–26 onwards, or the plans will need to be scaled back.

For 2025–26, government plans imply spending of about £6.7 billion. From this amount, the government has already committed to about £2.1 billion for school maintenance (about equal to the average real-terms spending over the past decade). It has also committed £740 million to help mainstream schools adapt infrastructure to expand core provision for SEND. This leaves about £3.9 billion, which will need to cover school and college rebuilding projects, as well as any other capital plans.

As can be seen, capital spending tends to be lumpy over time. There was a large increase in spending in the late 2000s, with spending increasing from nearly £7 billion in the mid-2000s to over £10 billion in 2009–10 and 2010–11 (all in today’s prices). The large increase reflects the last Labour government’s Building Schools for the Future programme, with delays in this programme leading to the big upticks in spending in 2009–10 and 2010–11. There was then a large decline up to 2013–14. Since then, overall capital spending has oscillated around £6–7 billion per year in today’s prices. Plans for 2025–26 remain well within this range and thus are not significantly different from experience over the last decade.

The big question is whether spending is meeting current needs and how it is likely to evolve going forwards. The National Audit Office (2023) reported that the DfE calculated it needed about £5 billion per year from 2021 to 2025 in order to maintain school buildings and mitigate the most serious risks. This was based on a survey of the condition of school buildings. The DfE instead requested about £4 billion per year based on the rate at which it could increase spending. HM Treasury ultimately allocated only £3 billion per year, leaving actual funding more than 40% below the government’s own assessed level of need (as cited by the National Audit Office).

In September 2024, many schools had to close some or all of their buildings due to safety concerns about RAAC. As a result, the government had to make funding available for remedial action. For 2024–25, this totalled about £164 million and would have been an additional urgent addition as compared with the National Audit Office analysis.

For 2025–26, school maintenance spending is due to be about £2.1 billion, which is about 13% higher than in 2024–25, but still about the same level in real terms as the average over the past decade. This strongly suggests that school maintenance spending remains well below government-assessed levels of need.

Upon taking office, the new government announced a substantial increase in planned capital spending across all departments – amounting to around £100 billion more over five years, compared with the plans inherited from the previous government. These increases were front-loaded, with a particularly sharp increase in funding for 2025–26. Over the period covered by the Spending Review, capital DEL is set to grow by 1.3% per year, broadly in line with projected growth in resource spending. Within that, however, we might expect a significant portion of any increase to be allocated towards defence, as the UK builds up towards its new 2.5% of GDP spending target. This suggests that the outlook for other departments, including education, may remain tight. That said, the expected decline in pupil numbers over the coming years could create scope to shift funding away from new school construction and towards repairs and maintenance, where current spending appears to fall short of assessed need.

4. Options for the 2025 Spending Review

Looking to the upcoming Spending Review, the government has set out plans for overall departmental spending to grow by about 1.2% per year in real terms between 2025–26 and 2028–29. However, existing commitments in areas such as defence, health and childcare will require extra spending. After accounting for the likely cost of these commitments, IFS analysis suggests that ‘unprotected’ spending will fall by about 1% per year in real terms between 2025–26 and 2028–29, or by about 3% in total.16 This currently includes most spending by the DfE, excluding the early years and childcare.

The government could top up its overall spending plans. However, doing so while remaining within its fiscal rules would require a positive shock to economic growth and the public finances, additional tax rises or additional borrowing.

Within its overall public services envelope, the government could choose to protect all (or some parts) of the education budget. But this would necessitate making deeper cuts elsewhere in public services.

In this section, we assess the realistic options for education spending within this constrained fiscal environment, focusing on day-to-day (resource) spending for schools and colleges. We set out the implications of each scenario, including the trade-offs involved and the likely impact on per-pupil funding levels.

Options for schools and colleges

Given the overall constraints on the public finances, the realistic options for school funding seem relatively straightforward – even if not necessarily simple to choose between and deliver. As shown in Table 1, one option is to protect the overall schools budget in real terms. This was the choice made by governments in the 2010 and 2015 Spending Reviews, with increases in the schools budget set out in the 2019 and 2021 Spending Reviews. With pupil numbers projected to fall, this approach would allow for around 3% real-terms growth in per-pupil funding between 2025–26 and 2028–29.

Table 1. Options for school spending in the 2025 Spending Review

Option | Change in school spending between 2025–26 and 2028–29 (2025–26 prices) | Real-terms change in spending per pupil, 2025–26 to 2028–29 |

Freeze total spending in real terms | 0 | +3% |

Freeze spending per pupil in real terms | −£2.0 billion | 0% |

Another natural option would be to protect spending per pupil in real terms. Given the expected decline in pupil numbers, this would deliver a £2.0 billion or 3% cut in total school spending between 2025–26 and 2028–29. This would be exactly in line with the potential cut to ‘unprotected’ public service spending.

Such a cut in school spending might ease the difficult trade-offs facing policymakers across other areas of education and public services. However, there are a number of reasons to believe that it would be difficult to make such cuts in practice.

First, the government is projecting a more than £2 billion rise in spending on special educational needs provision over the next few years, purely as a result of projected growth in legal entitlements. If this materialises, then it would clearly wipe out any opportunities for savings. Spending on EHCPs is also protected in law, which makes it very hard for schools to deliver savings in this area. The government has committed to reforming the system, with more provision in mainstream schools. This could conceivably improve provision and reduce costs in the long run. It would, however, likely involve extra costs in the short run. The government will also need to find a way to address the deficits that councils have accumulated off-balance-sheet over time, which are now estimated to total over £5 billion.

Second, the government has committed to recruiting 6,500 additional teachers, though it remains unclear what baseline this target is measured against or how the new roles will be distributed between schools and colleges. It is reasonable to assume the figure refers to an increase relative to 2024 staffing levels. If teacher numbers are maintained rather than allowed to fall in line with declining pupil numbers, then it would significantly constrain opportunities to make savings within the schools budget.

In Table 2, we consider the same scenarios for college and sixth forms. However, given the projected rise in student numbers in further education, the implications differ significantly from those for schools. The first option is for the government to protect the overall 16–19 education budget in real terms. With student numbers expected to grow, this would result in a 3% real-terms decline in spending per pupil between 2025–26 and 2028–29. Alternatively, the government could protect spending per pupil in real terms, which would require an increase of around £290 million in the 16–19 education budget by 2028–29. In contrast to schools – where falling numbers allow for potential savings – to maintain existing resource levels in further education would require additional funding.

Table 2. Options for 16–19 further education spending in the 2025 Spending Review

Option | Change in 16–19 further education spending between 2025–26 and 2028–29 (2025–26 prices) | Real-terms change in spending per student, 2025–26 to 2028–29 |

Freeze total spending in real terms | 0 | −3% |

Freeze spending per pupil in real terms | +£290 million | 0% |

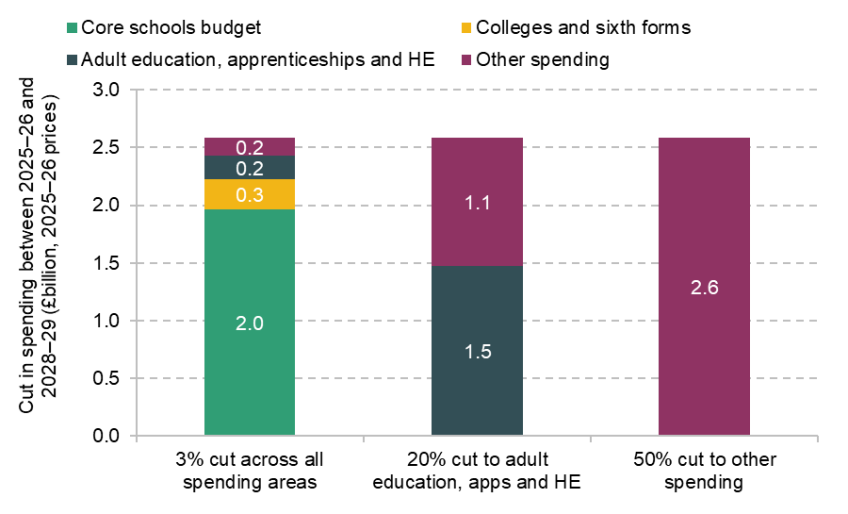

Options across the education budget

Figure 9 summarises a potential set of choices that policymakers could make in allocating resource DEL spending across the DfE to deliver a £2.6 billion real-terms cut over the spending review period – equivalent to a 3% reduction in total DfE resource spending by 2028–29, in line with the average for ‘unprotected’ spending areas. As noted earlier, the government has already committed to expanding the early years entitlement, so it is reasonable to focus on DfE spending excluding the early years entitlement, which is projected to total around £86 billion in 2025–26.

Figure 9. Options for making 3% or £2.6 billion cuts to the DfE resource DEL budget between 2025–26 and 2028–29

If this £86 billion budget were treated as ‘unprotected’, applying a uniform 3% real-terms cut across all areas would imply a £2.0 billion reduction in core school spending, a £260 million cut to colleges and sixth forms, a £200 million cut across adult education, apprenticeships and higher education, and a further £150 million reduction to other smaller programmes. For schools, this would be roughly equivalent to a real-terms freeze in per-pupil funding.

If policymakers instead choose to protect funding for schools and the 16–19 education budget for colleges and other further education providers, this would avoid some of the pressures discussed earlier in this report. However, protecting these areas would require concentrating the full £2.6 billion cut in the remaining parts of the DfE budget – resulting in a more than 20% real-terms reduction for adult education, apprenticeships, higher education, and other smaller programmes.

An alternative option would be to also protect adult education, apprenticeships and higher education. In this scenario, the £2.6 billion cut would need to fall on the smallest remaining parts of the DfE budget, requiring reductions of up to 50% in real terms on other areas of education spending. Such deep cuts would likely necessitate the discontinuation of specific programmes, such as universal infant free school meals or the PE and sport premium.

All of these scenarios assume a fixed £2.6 billion real-terms reduction in the DfE’s resource DEL. Reducing the size of this cut would require deeper savings from other unprotected departments, higher taxes or additional borrowing – none of which is likely to be straightforward or a politically attractive option.

Tough choices ahead for education

The education budget faces intense pressure in the upcoming Spending Review, with rising demands set against a tightly constrained fiscal backdrop. With overall departmental spending set to grow modestly and significant commitments already made in areas such as health, defence and early years, the scope to increase funding for schools, colleges and wider education services is severely limited. At the same time, schools face rising special educational needs costs and need to meet teacher recruitment pledges, while colleges face rising students numbers – pressures that will be difficult to manage within flat or falling budgets.

These decisions are not just about how much to spend but where to spend it. For schools, falling pupil numbers could create some fiscal flexibility: protecting the overall budget in real terms would allow for modest growth in per-pupil funding, while protecting per-pupil funding would enable a reduction in the total schools budget. In contrast, rising student numbers in further education mean that maintaining per-student funding would require additional investment, and protecting the overall 16–19 budget would result in a real-terms cut in funding per student. Meanwhile, adult education, apprenticeships and other smaller programmes risk being squeezed out entirely if other areas are protected.

None of the available options is straightforward. Each involves trade-offs between different areas of the education system, with consequences for the level and quality of provision. In the absence of additional funding, difficult choices will be required about which pressures to prioritise and where savings can be realistically made.

Acknowledgements

The authors gratefully acknowledge the support of the Nuffield Foundation (grant number EDO/ FR-000024394) and the Economic and Social Research Council for support via the ESRC Centre for the Microeconomic Analysis of Public Policy (grant number ES/T014334/1). The Nuffield Foundation is an independent charitable trust with a mission to advance social wellbeing. It funds research that informs social policy, primarily in Education, Welfare and Justice. The Nuffield Foundation is the founder and co-funder of the Nuffield Council on Bioethics, the Ada Lovelace Institute and the Nuffield Family Justice Observatory. The Foundation has funded this project, but the views expressed are those of the authors and not necessarily of the Foundation. Visit www.nuffieldfoundation.org.

References

Britton, J., Farquharson, C., Sibieta, L., Tahir, I. and Waltmann, B., 2020. 2020 annual report on education spending in England. IFS Report R183, https://ifs.org.uk/publications/2020-annual-report-education-spending-england

County Councils Network, 2025. Councils warn of financial catastrophe in 12 months time, with ‘unmanageable’ SEND deficits risking bankruptcy. https://www.countycouncilsnetwork.org.uk/councils-warn-of-financial-catastrophe-in-12-months-time-with-unmanageable-send-deficits-risking-bankruptcy/

Department for Education, 2024. School workforce in England: reporting year 2023. https://explore-education-statistics.service.gov.uk/find-statistics/school-workforce-in-england/2023.

Drayton, E., Farquharson, C., Ogden, K., Sibieta, L., Snape, D. and Tahir, I., 2025. Annual report on education spending in England: 2024–25. IFS report. https://ifs.org.uk/publications/annual-report-education-spending-england-2024-25

McLean, D. and Worth, J., 2025. Teacher labour market in England: annual report 2025. NFER report. https://www.nfer.ac.uk/publications/teacher-labour-market-in-england-annual-report-2025/

National Audit Office, 2023. Condition of school buildings. https://www.nao.org.uk/wp-content/uploads/2023/06/condition-of-school-buildings.pdf

National Audit Office, 2024. Support for children and young people with special educational needs. https://www.nao.org.uk/wp-content/uploads/2024/10/support-for-children-and-young-people-with-special-educational-needs.pdf

National Audit Office, 2025. Teacher workforce: secondary and further education. https://www.nao.org.uk/wp-content/uploads/2025/04/teacher-workforce-secondary-and-further-education.pdf

Sibieta, L. and Snape, D., 2024. Spending on special educational needs in England: something has to change. IFS Report R341. https://ifs.org.uk/publications/spending-special-educational-needs-england-something-has-change

Worth, J. and Tang, S., 2024. How to recruit 6,500 teachers? Modelling the potential routes to delivering Labour’s teacher supply pledger. NFER report. https://www.nfer.ac.uk/publications/how-to-recruit-6-500-teachers-modelling-the-potential-routes-to-delivering-labour-s-teacher-supply-pledge/

Endnotes

Authors

Luke Sibieta

Luke is a Research Fellow at the IFS and his general research interests include education policy, political economy and poverty and inequality.

Darcey Snape

Darcey joined the IFS in 2024 as a research economist in the Education and Skills sector.

Imran Tahir

Imran joined the IFS in 2019 and works in the Education and Skills sector.

More from IFS

Understand this issue

Policy analysis

Academic research