Downloads

Download the report as a PDF

PDF | 479.91 KB

Executive summary

There has been considerable recent debate about the terms of ‘Plan 2’ student loans, which were issued to 11 cohorts of English undergraduate university students: those who started their courses between academic years 2012/13 and 2022/23.1 We have written before about how these student loans work, and how they have changed over time – including as a result of changes announced by the Chancellor at the Autumn Budget 2025.2

To recap, under current government policy, the key repayment terms of these loans are:

- From the April after they graduate, borrowers make loan repayments of 9% of their earnings above a repayment threshold, which is currently £28,470.

- Interest is typically added to an individual’s balance at the rate of inflation measured by the Retail Prices Index plus 3% (‘RPI plus 3%’) while studying. After graduation, interest is added at a rate between RPI inflation and RPI plus 3% depending on their earnings each year.

- The repayment and interest rate thresholds (which determine how much interest is added) have been increased over time, although in different ways from year to year. Before the Autumn Budget 2025, they were set to increase in line with RPI each year. They will now be frozen for three years from April 2027 and will then increase in line with RPI.

Any outstanding loan balance is written off after 30 years with no adverse consequences for graduates.

In this report, we consider the potential impacts of four sets of potential reforms to these Plan 2 loans. We examine the proposals made by the Conservative party and the Liberal Democrats (which focus on changes to the interest rate and repayment threshold respectively), as well as proposals for broader changes (where we specifically model the proposals made by the campaign group Rethink Repayment) and proposals that consider the loan repayment rate and write-off period (where we examine proposals similar to those favoured by some backbench Labour MPs). These distinct sets of reforms each target different features of the current loan system that some people dislike. They would have very different impacts on repayments in the short and longer term, and each would affect different groups of graduates.

Key findings

1. Plan 2 student loans combine above-inflation interest rates (which mean that many graduates see the value of their ‘debt’ increase year on year) with payments that are fixed at 9% of income over a repayment threshold, and a debt that is written off after 30 years. On average, those who started university in 2022/23, and who are in the lowest 10% of the graduate lifetime earnings distribution, will pay back around £9,500 in total, because they will rarely earn above the repayment threshold. The highest-earning half of graduates can expect to repay around £74,000 on average and to pay back much more than they borrowed in real terms because of interest accrued on their loans.

2. Proposals to change the balance of these four features – the interest rate, the repayment threshold, the repayment rate and the write-off period – will affect different groups of graduates, in different ways and at different times. They also imply very different costs to the exchequer. Because of this, decisions over student loan policy are inherently political decisions.

3. The Conservative party has proposed reducing the maximum interest rate on Plan 2 student loans to RPI, removing above-RPI-inflation interest from the loans. Compared with current government policy, this would lead to lower outstanding loan balances for any graduates earning over the lower interest rate threshold (currently £28,470). This reform would not make an immediate difference to most graduates’ monthly repayments. That is because – so long as they have some outstanding loan – the amount borrowers repay each month depends only on how much they earn, rather than on their loan balance.

4. The Conservative proposal would, however, reduce lifetime loan repayments for many middle- and (in particular) higher-earning graduates. Graduates who can expect to repay their loans in full, with interest, would fully repay their loans much more quickly under the Conservatives’ proposal and would repay much less overall. For those who started courses in 2022/23, this proposal would on average reduce lifetime loan repayments by £11,000 in today’s prices on average. The 30% of graduates with the highest lifetime earnings could expect to save upwards of £20,000. Many low-earning graduates would never repay any less as a result of the Conservative proposal – with almost no change in lifetime repayments amongst the fifth of graduates with the lowest lifetime earnings. For these graduates, a lower interest rate would reduce the amount of their loans eventually written off after 30 years, rather than reducing the amount they can actually expect to repay (in any given month or overall).

5. The Liberal Democrats have proposed that the repayment threshold should be increased every year in line with average earnings (instead of being frozen for three years and then increased in line with RPI inflation). From April next year, all those earning above £29,385 would benefit from lower monthly repayments, with most repaying around £210 per year (£17 per month) less by 2029/30. The lower repayments that are made would lead to higher outstanding loan balances for graduates than they would otherwise have.

6. Despite this, the Liberal Democrat proposal would reduce average total repayments from those who started courses in 2022/23 by around £8,000 in today’s prices over their lifetimes. Those in the third and fourth deciles of lifetime earnings would benefit from the largest savings, of around £14,000. The very highest-earning graduates may repay slightly more in total under the Liberal Democrats’ proposal than under current government policy as they would repay more slowly and accrue more interest – although they could avoid this by making voluntary early repayments.

7. Despite having very different distributional consequences amongst graduates, the Conservative and Liberal Democrat proposals might reduce average lifetime repayments by similar amounts: by £11,000 and £8,000 respectively in today’s prices amongst those who started courses in 2022/23. This means the long-run exchequer costs of these policies would also be similar: around £4 billion and £3 billion respectively in relation to this cohort, with somewhat smaller costs associated with each of the earlier 10 cohorts of university graduates who have these Plan 2 loans.

8. The way that student loans are reflected in the public finances is complex and can be counter-intuitive. This means that reforms that generate similar changes in eventual graduate repayments can nonetheless be reflected in the public finances in different ways. Policy decisions about the appropriate level and structure of repayments for graduates ought not to be based on the specific accounting treatment a given reform would receive.

9. The campaign group Rethink Repayment has proposed a much larger package of reforms: a lower interest rate (CPI inflation), a higher repayment threshold, and a reduction in the repayment rate from 9% to 5%. This package would approximately halve monthly repayments from most graduates in the short run and it would also roughly halve expected lifetime loan repayments from the 2022/23 university entry cohort, reducing them by around £28,000 on average. Middle-earning graduates would benefit the most, with the median-earning graduate repaying around £36,000 less over their lifetime. The long-run exchequer cost of this package would be around £12 billion for the 2022/23 cohort alone (three to four times as high as the long-run exchequer cost of the Conservative and Liberal Democrat proposals), and the reduction in lifetime repayments across all Plan 2 borrowers could easily be in the tens of billions.

10. Some combination of policies could reduce graduates’ repayments in the short term but be approximately cost-neutral in the long run. This would require other changes that would lead to some graduates repaying more at some point (most likely later in their working lives). A reduction in the repayment rate from 9% to 5%, combined with an extension of the write-off period for 9 more years, could reprofile payments later in graduates’ working lives while leaving total lifetime repayments from the 2022/23 cohort nearly unchanged. While such a reform would not change the way total costs were shared between taxpayers and affected graduates, it would be likely to redistribute amongst graduates, with higher-earning graduates likely to pay more and lower-earning graduates likely to pay less.

1. What has the Conservative party proposed?

The Conservative party has proposed reducing the maximum interest rate on Plan 2 student loans to RPI,3 removing above-RPI-inflation interest from the loans. This would match the interest rate on new ‘Plan 5’ loans, which have been available to English undergraduate students who started university from the 2023/24 academic year onwards.4 As shown in Figure 1, graduates on Plan 2 loans earning below £28,470 currently face an interest rate of 3.2% and those earning above £51,245 face an interest rate of 6.2%, with a variable rate applied in between. If implemented immediately, this reform would reduce the interest rate applying to the loans of those earning above £28,470, with the highest earners seeing the full benefit of a 3 percentage point reduction going forwards.

Figure 1. Interest rate currently applying to student loans under current policy and under Conservative proposals

Note: Reflects loan repayment terms applying to all borrowers with outstanding Plan 2 student loans between September 2025 and March 2026, i.e. with lower and upper interest rate thresholds of £28,470 and £51,245 and an interest rate between 3.2% and 6.2%. The applicable RPI rate for the period from 1 September 2025 to 31 August 2026 reflects RPI as of March 2025.

Who would benefit and when?

This reform would not make an immediate difference to most graduates’ monthly repayments. This is because – so long as they have some outstanding loan – the amount borrowers repay each month depends entirely on how much they earn, rather than on their loan balance.

No longer applying above-RPI-inflation interest would reduce the outstanding loan balances of any graduates earning over the lower interest rate threshold (currently £28,470). The effect would be greatest for those with high earnings (who face the highest interest rates currently) and those who have relatively large outstanding balances.5

Whether these lower outstanding loan balances change the amount graduates can actually expect to repay is another matter. Those who can expect to repay their loans in full, with interest, would fully repay their loans much more quickly under the Conservatives’ proposal and would repay much less overall. Indeed, this reform would in particular benefit high-earning graduates, who are currently subject to the highest interest rates and, crucially, can currently expect to repay their loans with above-inflation interest.

Many low-earning graduates will never repay any less as a result of the proposed change. For those who never repay the principal on their loans, any above-inflation interest added never increases the amount that they actually repay towards their loans. For these individuals, a lower interest rate would reduce the amount of their loans eventually written off after 30 years, rather than reducing the amount they can actually expect to repay (in any given month or overall).

We estimate this reform may reduce average lifetime repayments amongst those who started courses in 2022/23 by around £11,000 on average (in today’s prices). As shown in Figure 2, the fifth of graduates with the lowest lifetime earnings could expect almost no change in their lifetime repayments. Some in the low- or middle-earning parts of the lifetime earnings distribution would see a reduction in their total lifetime repayments; these will tend to be individuals who are relatively high-earning in some years of working life but are relatively lower-earning in others. The 30% of graduates with the highest lifetime earnings could expect to save upwards of £20,000 in today’s prices on average. We estimate this reform could increase the proportion of graduates from this cohort who repay their loans in full from around half to around two-thirds.

Figure 2. Average expected lifetime student loan repayments of the 2022/23 university entry cohort under current policy and Conservative proposals, by decile of lifetime earnings

Note: Repayments and lifetime earnings are given in undiscounted CPI real terms (2025–26 prices). Lifetime earnings deciles are amongst graduates only. Assumes no borrowers make voluntary early repayments. ‘Conservative proposal’ assumes interest applied at RPI plus 3% during study, and then at RPI in all subsequent years. All other terms of Plan 2 loans are assumed to be unchanged from current policy.

Source: IFS student finance calculator (https://ifs.org.uk/student-finance-calculator); author’s calculations.

The benefits – in terms of lower annual loan repayments – would materialise gradually as increasing proportions reached the point of fully repaying their loans. Very few would see any immediate benefit from this policy, with almost no typical students (who started university around age 18) seeing any reduction in their repayments during their 20s. As shown in Figure 3, the highest-earning third of graduates (based on their lifetime earnings) would see a reduction in annual repayments of £200 on average from around age 32, with the impact peaking in around their mid 40s. The middle-earning third of graduates would be expected to benefit later and by around half as much overall. Their repayments may be around £200 per year lower on average from age 37, and they could repay over £1,000 less per year (in today’s prices) from their late 40s or early 50s. Few of those in the bottom-earning third of graduates would ever repay less as a result of this reform, with the reduction in average annual repayments from this group peaking at £135 per year (£11 per month) in today’s prices, in their late 40s.

Figure 3. Expected change in average annual loan repayments amongst the 2022/23 university entry cohort from Conservative proposals, by age and third of lifetime earnings

Note: Repayments and lifetime earnings are in undiscounted CPI real terms (2025–26 prices). Changes are changes in mean average repayments each year amongst those in the bottom, middle and highest third of graduate earners based on their discounted lifetime earnings. Assumes all borrowers start university at 18. Assumes no borrowers make voluntary early repayments. Assumes interest still applied at RPI plus 3% during study, but then at RPI in all subsequent years. All other terms of Plan 2 loans are assumed to be unchanged from current policy.

Source: IFS student finance calculator (https://ifs.org.uk/student-finance-calculator); author’s calculations.

How much would this cost the exchequer?

If this change applied only to the last cohort who took out these loans – those who started university in the 2022/23 academic year – we estimate the reform could cost the taxpayer in the region of £4 billion in total in today’s prices. This reflects the change in total expected lifetime repayments on their loans as a result of the lower interest rate applying to their loans after graduation, expressed in today’s prices, and would be spread over roughly the next 30 years.6

The impact on expected repayments from each of 10 earlier cohorts of students – all those who started courses between academic years 2012/13 and 2021/22 – is likely to be smaller, as many of them will already have accrued some above-inflation interest after they graduated. The Conservative proposals do not appear to include any retrospective removal of interest that these graduates have already accrued. Many students in the earliest cohorts will have graduated more than a decade ago, meaning that they are already nearly a third of the way through the 30-year repayment period.

How would this be reflected in the public finances?

As we have discussed in prior work,7 the way that student loans are reflected in the public finances is complex, and can be counter-intuitive. We do not attempt to provide a comprehensive account here (interested readers are advised to consult the section ‘Accounting for the cost of student loans’ in our guide to spending on higher education8 as well as ONS’s methodological guide to student loans in the public finances9).

A reduction in the interest rate applied to Plan 2 student loans (as proposed by the Conservatives) would intuitively represent a hit to the public finances: graduates would accrue less interest on their loans and pay back less over their lifetimes. From an accounting perspective, this would show up as lower current receipts for the government (when interest is added to loan balances, the share that is expected to be repaid is recorded as a current receipt in the year it is added). It is difficult to precisely estimate the size of this effect without access to detailed data on outstanding loan balances, but a reasonable ballpark estimate might be a low-single-digit billions hit to government receipts each year, for the next 30 years.

One complicating factor, though, is that if the interest rate on student loans is lower, the portion of their loans that (some) students will fail to repay will also be smaller. The portion of student loans that is not expected to be repaid counts as capital spending for the government when loans are first issued. If the interest rate on existing loans is lowered, the government’s original expectation for the portion that would not be repaid will have been too high, and the amount of capital spending recognised in the public finances when these loans were issued will have been too large. A correction is therefore required when policy changes; ordinarily, this would give rise to a capital receipt. So, somewhat counter-intuitively, a reduction in the interest rate on Plan 2 loans could be expected to improve the short-term borrowing numbers. That is, a change which unambiguously weakens the government’s long-term fiscal position could show up as an improvement in the short-term fiscal picture.

However, to complicate matters even further, our understanding is that in this case, a change in the interest rate would be treated differently, so as not to have the perverse impacts on the public finance numbers described in the previous paragraph. Specifically, the change in the value of the loan book would show up in the National Accounts in ‘other economic flows’ rather than as lower capital spending and lower borrowing.

The broader point is that the accounting treatment of student loans for public finance purposes is immensely complex. Policy decisions about the appropriate level and structure of repayments for graduates ought not to be based on accounting treatment or on whether (or not) a long-term weakening of the government’s fiscal position can be presented as a short-term improvement for the purposes of shifting the metric used for the fiscal rules.

2. What have the Liberal Democrats proposed?

Under current government policy, the repayment threshold (the earnings level above which graduates make repayments) is set to be frozen for three years. From April 2030, it is then set to increase each year in line with RPI inflation. As we have described before, the freeze will increase graduates’ monthly repayments from April 2027 onwards – the point at which the threshold would otherwise have risen.10 In the 2029–30 tax year – when the threshold would have been expected to reach around £32,265 without the freeze – affected borrowers can expect to repay around £260 more.

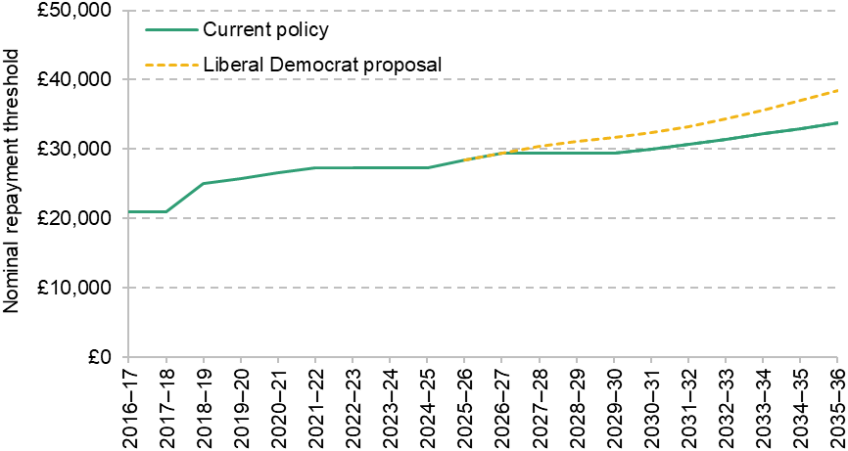

The Liberal Democrats recently published their own plan for changes to Plan 2 student loans, under which the repayment threshold would be increased each year in line with average earnings growth.11 This would return the default indexation rule to what it was before the Johnson government’s student loans reform in 2022.12 As shown in Figure 4, under current forecasts this would see the threshold increase until 2030 (instead of being frozen from April 2027) and then continue to increase more quickly over time (as average earnings are forecast to rise more quickly than RPI). Indexation with average earnings would see the repayment threshold increase in real terms over time.

Figure 4. Nominal Plan 2 student loan repayment threshold, under current policy and under Liberal Democrat proposal

Note: Dashed lines show forecasts.

Source: Author’s calculations using https://www.gov.uk/guidance/previous-annual-repayment-thresholds; OBR’s Economic and Fiscal Outlook, November 2025 (https://obr.uk/efo/economic-and-fiscal-outlook-november-2025/); OBR’s ‘Long-term economic determinants – March 2025’ (https://obr.uk/supplementary-forecast-information-on-long-term-economic-determinants-and-personal-independence-payment-policy-costing/); and Liberal Democrats’ proposal (https://www.libdems.org.uk/news/article/our-plan-to-fix-the-student-finance-system-and-support-graduates).

Who would benefit and when?

Unlike the Conservative proposal, this reform would reduce monthly loan repayments from any graduates required to make them, and would do so in the short term. By April 2029, we estimate that on current forecasts, the repayment threshold would be expected to reach around £31,710, compared with £29,385 under current government policy. As shown in Figure 5, this would not benefit anyone earning under £29,385, who would not be required to make repayments anyway. Those earning between £29,385 and £31,710 would benefit on a sliding scale, with all those earning over £31,710 repaying around £210 (£17 per month) less in 2029–30. The reduction in annual repayments as a result of this policy would then continue to rise each year as the gap between the repayment threshold under the Liberal Democrat and current government policies continued to widen.

Figure 5. Monthly Plan 2 student loan repayments in 2029–30 by annual earnings, under current policy and under Liberal Democrat proposal

Note: Assumes an individual is only making repayments towards a Plan 2 student loan. ‘Liberal Democrat proposal’ assumes the repayment threshold is increased each year from April 2027 in line with the OBR’s latest forecast for growth in average weekly earnings as of the previous quarter 3.

However, lower repayments each year would also mean higher outstanding loan balances in the future. For those primarily worried about high loan balances, the Liberal Democrats’ plan might therefore seem counterproductive, even though higher loan balances due to this reform would never have any effect on repayments for around half of all graduates and for many others would not affect repayments for decades. (This is assuming that the system will not be changed again; given constant tinkering in the past, one might quite reasonably fear that loan balances might end up mattering earlier and for more graduates.)

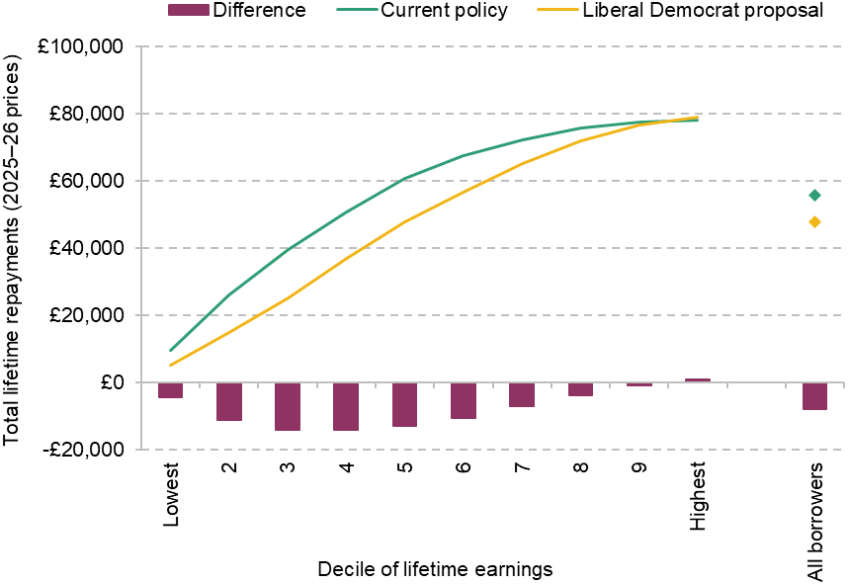

Over graduates’ lifetimes, this reform may reduce average loan repayments by around £8,000 in today’s prices. This is of a similar magnitude to the change in average lifetime repayments under the Conservative proposal (£11,000) but would have different distributional consequences amongst graduates. As shown in Figure 6, the largest lifetime savings from the Liberal Democrats’ proposal would accrue to graduates in the third and fourth deciles of lifetime earnings, who may expect to repay around £14,000 less in total. The lowest-earning third of graduates (by lifetime earnings) could repay around £10,000 less on average under the Liberal Democrat proposal – compared with around £1,000 less under the Conservative proposal.

Figure 6. Average expected lifetime student loan repayments of the 2022/23 university entry cohort under current policy and Liberal Democrat proposals, by decile of lifetime earnings

Note: Repayments and lifetime earnings are given in undiscounted CPI real terms (2025–26 prices). Lifetime earnings deciles are amongst graduates only. Assumes no borrowers make voluntary early repayments. ‘Liberal Democrat proposal’ assumes the repayment threshold is increased each year from April 2027 in line with the OBR’s latest forecast for growth in average weekly earnings as of the previous quarter 3. All other terms of Plan 2 loans – including the freeze in the interest rate thresholds – are assumed to be unchanged from current policy.

Source: IFS student finance calculator (https://ifs.org.uk/student-finance-calculator); author’s calculations.

The very highest-earning graduates – who could expect savings of upwards of £20,000 in total under the Conservative proposal – may repay slightly more in total under the Liberal Democrats’ proposal than under current government policy. With a higher repayment threshold, they would make smaller repayments earlier in life and pay off their loans more slowly, accruing more interest before having fully repaid. However, they would be able to avoid being made worse off in this way by making voluntary early repayments towards their loans.

Importantly, at Autumn Budget 2025, the government also froze the interest rate thresholds (the earnings levels that determine how much interest is added to loans) for three years. As we have described before, the planned freezes in the interest rate thresholds are expected to increase repayments for higher earners in particular.13 Since the Liberal Democrat proposals have not committed to reversing that freeze in the immediate term, we assume that the interest rate thresholds remain frozen for three years, and subsequently increase with RPI.

How much would this cost the exchequer?

In total, we estimate the total exchequer cost of this reform – were it applied only to those who started university in 2022/23 – would be around £3 billion in today’s prices (compared with around £4 billion for the Conservative proposal). This reflects the change in total expected lifetime repayments on their loans as a result of the higher repayment threshold and would be spread over roughly the next 30 years. The impact on expected repayments from each earlier cohort of students is likely to be slightly smaller, as they would be subject to the higher repayment threshold for fewer years of their 30-year repayment period.

How would this be reflected in the public finances?

As discussed in Section 1, the way that student loans are reflected in the public finances is complex. The main fiscal impact of the three-year threshold freezes announced at Autumn Budget 2025 was a one-off reduction of £5.6 billion in capital spending in 2026–27, reflecting an increase in the value to the taxpayer of the stock of existing loans. The main fiscal impact of undoing the freeze – having the thresholds increase each year in line with RPI, as was government policy before November 2025 – would be a roughly equivalent one-off increase in capital spending in the year the policy was introduced.

However, this is not a reliable guide to how the Liberal Democrat proposal might be reflected in the public finances. In addition to reversing these repayment threshold freezes, the Liberal Democrats’ proposals also commit to changing the future indexation of the loans after 2030 (from RPI to average earnings) – which would substantially increase the impact of their proposed reform on expected repayments in the long run.14 In the opposite direction, retaining the government’s planned interest rate threshold freezes would reduce the impact of their proposed reform.

On balance, we might expect the Liberal Democrats’ reform to have roughly double the impact on the public finances of reversing the Budget 2025 freezes. It would be likely to give rise to a one-off capital transfer (from government to borrowers) of somewhere in the region of £10 billion in total. There would also be some reduction in current receipts in future years – as less of the interest added to loans would be expected to be eventually paid with a higher repayment threshold – although this element would be fairly small.

The broader point made in Section 1 bears repeating: policy decisions about the appropriate level and structure of repayments for graduates ought not to be based on the specific accounting treatment a given reform would receive. Any proposals for loan reform should be considered on its own merits, including considering their likely impact on the long-run fiscal sustainability of the public finances.

3. What have graduate campaigners proposed?

Other groups have called for proposals that go even further in both these dimensions, by changing the repayment rate in combination with lowering the interest rate and raising the repayment threshold. For example, the campaign group Rethink Repayment has proposed three changes to Plan 2 student loan terms:15

The repayment threshold would be increased to £31,200, approximately the level it would have reached had it been increased since 2016 in line with average earnings growth, and would be indexed in line with average earnings growth in future years.

The interest rate on the loans would be set to inflation (removing above-inflation interest rates) and the measure of inflation used would be changed to the Consumer Prices Index (CPI), rather than RPI.

The repayment rate – the rate at which graduates make repayments from their earnings above the repayment threshold – would be reduced from 9% to 5%.

Each of these changes would reduce student loan repayments. In combination, they would have a substantial impact in both the short and longer term, and a far larger effect than the proposals from either the Conservative or Liberal Democrat parties. For instance, the immediate impact of implementing reforms such as these would be to reduce repayments from all graduates making Plan 2 loan repayments, approximately halving them for most, as shown in Figure 7.

Figure 7. Monthly Plan 2 student loan repayments in 2029–30 by annual earnings, under current policy and under Rethink Repayment proposal

Note: Assumes an individual is only making repayments towards a Plan 2 student loan. ‘Rethink Repayment proposal’ assumes that the repayment threshold is increased to £31,200 in April 2026 and then increased with average earnings, and that the repayment rate is reduced from 9% to 5%.

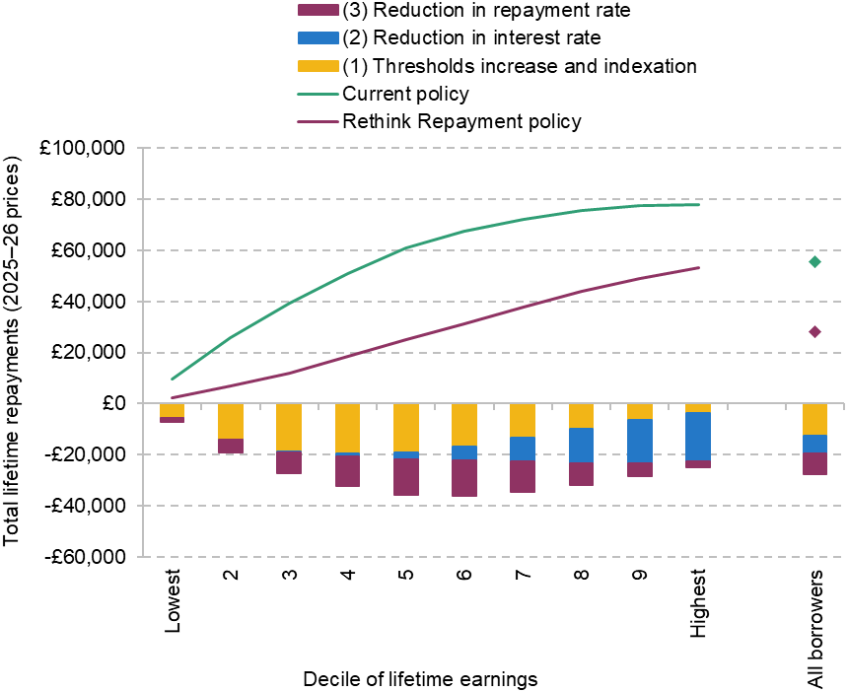

Over the longer term, this package of changes would substantially reduce expected lifetime loan repayments across the earnings distribution. As shown in Figure 8, we estimate that these reforms would roughly halve expected lifetime loan repayments from the 2022/23 university entry cohort, reducing them by around £28,000 on average.16 Middle-earning graduates would benefit the most, with the median-earning graduate repaying around £36,000 less over their lifetime. The lowest-earning tenth of graduates could expect to repay around £2,300 in total over their lifetimes, compared with around £9,500 under current policy, and the highest earners would repay much less overall as they no longer face an above-inflation interest rate after graduation and so would no longer repay more than they borrowed in real terms.

Figure 8. Average expected lifetime student loan repayments of the 2022/23 university entry cohort under different policies, by decile of lifetime earnings

Note: Bars show changes in repayments due to different components of Rethink Repayment proposal, introducing them in turn. Repayments and lifetime earnings are given in undiscounted CPI real terms (2025–26 prices). Lifetime earnings deciles are amongst graduates only. Assumes no borrowers make voluntary early repayments. The interest rate is reduced to RPI minus 0.4%, rather than CPI. Interest is still assumed to have applied to these loans at RPI plus 3% during study.

Source: IFS student finance calculator (https://ifs.org.uk/student-finance-calculator); author’s calculations.

The share of borrowers expected to fully repay their loans would fall from around half to around 30% under this reform. Despite this, almost all borrowers would be better off under these reforms than under current policy, in that they would be required to make lower loan repayments both each month and in total over their lifetimes. However, the cost of this policy to the exchequer would be substantial. Some graduates may be made worse off if meeting this cost meant higher taxes or lower government spending elsewhere.

How much would this cost the exchequer?

The Rethink Repayment proposal would reduce average lifetime loan repayments by the most of all the proposals considered here and, as a result, would be by far the most costly for taxpayers.

For the last cohort who took out Plan 2 loans – those who started university in the 2022/23 academic year – we estimate that these reforms might reduce total expected lifetime loan repayments by around £12 billion in today’s prices. To give a sense of scale, this compares with total loan outlay for the same cohort of around £22 billion, and estimated lifetime repayments of around £23 billion in today’s prices under current government policy. This £12 billion reduction in expected lifetime repayments from one cohort of borrowers compares with the estimates of around £4 billion and £3 billion for the Conservative and Liberal Democrat policies, respectively.

The impact on repayments from earlier cohorts of students would be somewhat smaller, as the changes would affect them for fewer years: any above-inflation interest these graduates have already accrued would remain on their loan balances, and the earliest cohort with these loans are now around 10 years into their 30-year repayment period.

One way to get a rough sense of the potential total cost of this reform to the exchequer is to start with the Department for Education (DfE) estimate of the ‘fair value’ of Plan 2 student loans, which was £129 billion at the end of March 2025.17 If a package of reforms halved future loan repayments for those with existing Plan 2 loans – as the Rethink Repayment proposal might – then we might expect the fair value of the student loan book to be reduced by something in the region of £60–70 billion.18

How would this be reflected in the public finances?

The largest impact of the proposed changes would be recorded as a one-off increase in capital spending and government borrowing in the year the policy was enacted. The scale of this increase is difficult to quantify, but given the scale of the expected reduction in lifetime repayments, it could easily be in the tens of billions.19 There would also be a longer-running impact of lower current receipts each year for the next 30 years as less interest (which the government eventually expects to be repaid) would be added to the loans.

4. What other options might the government have?

There are many other changes that the government could consider making to Plan 2 loans. Under the current system, the only ways to reduce monthly repayments from graduates in the short term are to increase the repayment threshold (as proposed by the Liberal Democrats) or to reduce the repayment rate (as has been discussed by campaign groups). In this section, we consider changes to the repayment rate alongside potential changes to a final key parameter in the system: the write-off period (currently 30 years after graduation). Similar packages of reforms to this have been proposed by some Labour MPs.

Cost-neutral changes to repayment rate and write-off period

By itself, reducing the repayment rate from 9% to (say) 5% would reduce average expected lifetime repayments by around £12,500 in today’s prices on average for those who started university in 2022/23. The total cost to taxpayers in the form of lower expected loan repayments from this one cohort would be in the region of £5 billion in today’s prices.

If, as some MPs have proposed, the government wanted to do that in a cost-neutral way by spreading repayments over a longer period, it could achieve this by extending the loan duration to around 39 years (close to the current write-off period for Plan 5 loans, which is 40 years).20 This would reduce the repayment burden of the loans in the first 30 years by reducing graduates’ monthly repayments, with the taxpayer cost of this offset by some graduates continuing to make payments for longer.

As shown in Figure 9, such a reform would reprofile payments through the life cycle – shifting more of the payments later in graduates’ working lives. Amongst those who started courses in 2022/23 at around the age of 18, the largest cash reduction in annual repayments would emerge in their early 30s – although many would already have seen substantial reductions before this point. However, the highest-earning third of such graduates might see this reverse – and their annual repayments increase on average – from around age 42. For low- and middle-earning graduates, the benefit in terms of lower annual repayments would be likely to persist until the end of their original write-off period of 30 years, at roughly age 52. After that point, both middle- and high-earning graduates could expect to repay around £2,000 per year more through their early 50s as a result of this reform.

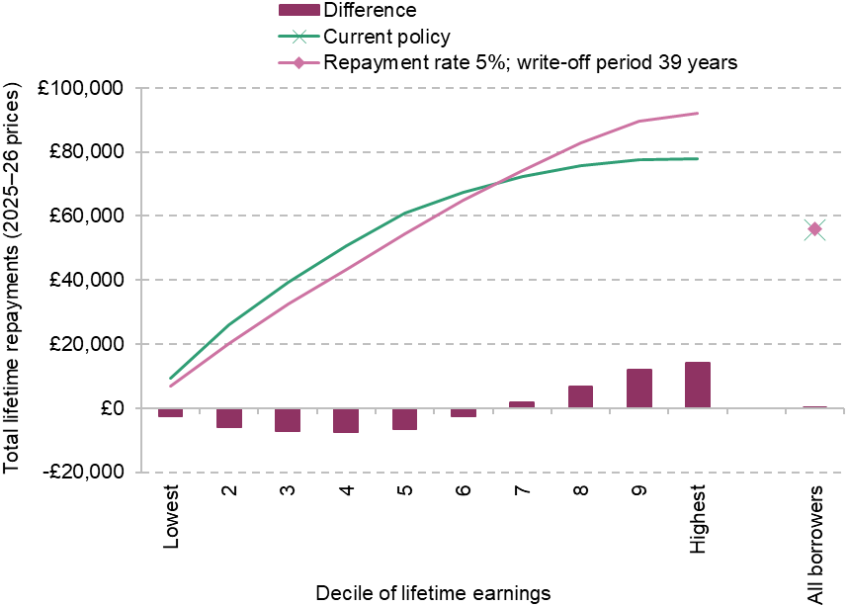

Figure 9. Expected change in average annual loan repayments amongst the 2022/23 university entry cohort from lower repayment rate and longer write-off period, by age and third of lifetime earnings

Note: Repayments and lifetime earnings are in undiscounted CPI real terms (2025–26 prices). Changes are changes in mean average repayments each year amongst those in the bottom, middle and highest third of graduate earners based on their discounted lifetime earnings. Assumes all borrowers start university at 18. Assumes no borrowers make voluntary early repayments. Assumes repayment rate reduced to 5% and write-off period increased from 30 to 39 years. All other terms of Plan 2 loans are assumed to be unchanged from current policy.

Source: IFS student finance calculator (https://ifs.org.uk/student-finance-calculator); author’s calculations.

While this reform would predominantly move repayments between different years for each graduate, it would still have redistributive consequences across graduates, as shown in Figure 10. Such a combination of changes would tend to reduce lifetime repayments from low earners and could increase them substantially for some high earners, particularly those with relatively large outstanding loans.21

Figure 10. Average expected lifetime student loan repayments of the 2022/23 university entry cohort under (near) cost-neutral reform to repayment rate and write-off period

Note: Repayments and lifetime earnings are given in undiscounted CPI real terms (2025–26 prices). Lifetime earnings deciles are amongst graduates only. Assumes no borrowers make voluntary early repayments.

Source: IFS student finance calculator (https://ifs.org.uk/student-finance-calculator); author’s calculations.

We estimate that this particular combination – a repayment rate of 5% and write-off period of 39 years – would slightly reduce total expected repayments from this cohort, by around £0.3 billion in today’s prices. This would make it roughly cost-neutral for the exchequer in the long run, especially in comparison with the other proposed reforms discussed above.22

A similar reform to this was discussed by Labour MP Luke Charters in a recent interview, although he suggested that individual borrowers could be offered a choice between existing Plan 2 terms and a new set of terms, with a lower repayment rate and a longer repayment period.23 Offering graduates a choice between their current loan terms and these terms would allow them to choose the repayment terms they preferred, although we might expect those who anticipate having high earnings in their 50s and 60s to prefer to stick with their current terms. Offering such a choice – and graduates the benefit of lower expected repayments – would therefore tend to increase the exchequer cost of any such reform. It would also add complexity to a loan system – or rather a set of systems – which are already complicated for many graduates (and prospective students) to understand.

Of course, the government could also choose to stick with its current policy. Given the fiscal constraints facing the Chancellor – and the ambition that next week’s Spring Forecast will not contain major policy announcements – this seems perhaps the most likely scenario for now.

In the longer term, there are a range of ways in which current and future governments could look to change how higher education is financed – which would affect either existing student loan borrowers or future students. As described in Box 1, the IFS student finance calculator can be used to model the potential costs and distributional consequences of many of these options.24

Box 1. I have an idea for a policy change. Who would gain or lose? How much might it cost?

The online IFS student finance calculatora produces rough estimates of the cost and distributional consequences of the system for financing higher education in England, and can be used to estimate the impacts of policy changes had they been in place for a single cohort of students. For instance, it can be used to look at the impact of changing the tuition fee cap or the repayment threshold, or restoring maintenance loan entitlements. The calculator can also be used to look at more substantial changes to higher education financing, such as reintroducing maintenance grants, varying the repayment rate with earnings or years since graduation, or implementing a graduate tax.

The model is based on the simulated lifetime earnings profiles of 20,000 representative graduates, which are used to estimate loan repayments under different systems. There is enormous uncertainty in these estimates: they depend on policy remaining constant for many decades into the future and on forecasts for economic growth and inflation into the 2060s. We also assume that the student loans system does not affect students’ choice of subject or graduates’ gross earnings. The more radical the changes to the system, the less plausible this assumption becomes.

As we have discussed before,b figures produced by the calculator do not match official forecasts. This is for three main reasons: we do not have access to the same confidential student loans data as the government so we must make various simplifying assumptions; methodological differences mean we are more optimistic about graduates’ mid-career earnings; and, by default, the model discounts repayments by RPI rather than the HM Treasury financial instruments discount rate (currently RPI minus 0.85% up to 2030, and then RPI plus 0.05%).

To note, the options on the calculator default to current policy as it applies for England-domiciled students who started university in the 2025/26 academic year, including reflecting Plan 5 student loan terms. The calculator can also be used to roughly model repayments for those who started courses in 2022/23 – most of whom will not start repaying their loans until April 2026.

a. https://ifs.org.uk/student-finance-calculator.

b. https://ifs.org.uk/articles/student-loans-england-explained-and-options-reform.

5. Conclusions

Different commentators or politicians have very different features of the current Plan 2 loan system in mind when they describe this system as ‘unfair’ or broken. This leads them to very different proposed solutions.

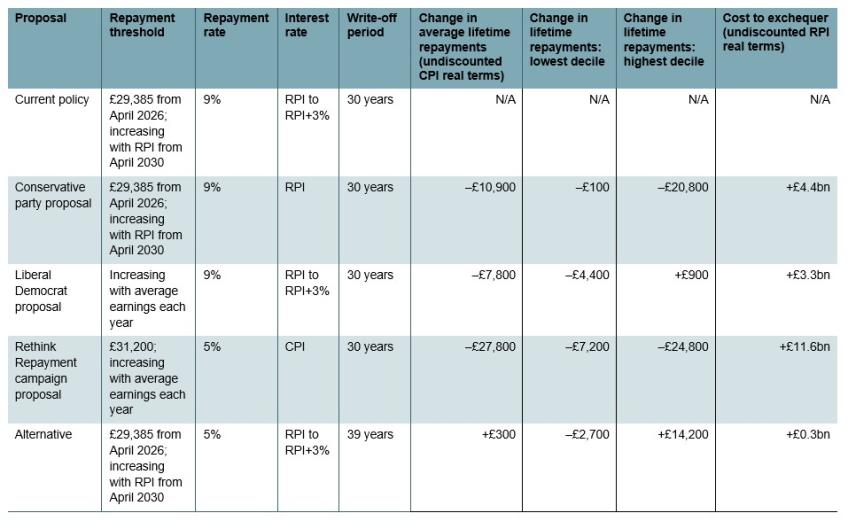

The four proposals discussed in this report would affect graduates’ repayments at different points in time and would have very different distributional implications amongst graduates, as well as very different costs. These are summarised in Table 1 at the end of this report.

The Conservative party proposal (to set the interest rate for Plan 2 loans to RPI inflation) would have benefits for many middle- and (to a greater degree) high-earning graduates, who would repay more quickly and repay less in total. It would prevent graduates from seeing their outstanding loan balances rise at a rate faster than RPI inflation, and would mean more graduates seeing their balances fall year on year. But many of those benefiting – in particular, middle earners – would only benefit from lower repayments many years in the future. The Conservative proposal would not change the actual repayments of the vast majority of lower-earning graduates.

The Liberal Democrat proposal (to increase the repayment threshold) would have roughly similar impacts on average lifetime repayments – and would cost taxpayers a broadly similar amount – but it would have an immediate impact on the monthly repayments of all those required to make monthly repayments. This impact would be fairly small initially but would increase over time. The lifetime gains from this reform would be much larger for lower-earning graduates than under the Conservative proposal – although the reverse is true for higher earners, some of whom may even repay slightly more under this proposal than under current government policy.

The changes proposed by the campaign group Rethink Repayment are far larger, and would produce the greatest reduction in graduate repayments both in the short and longer term. As a result, a package of changes such as this would be considerably more expensive for taxpayers.

The only ways to reduce monthly repayments in the short term by tweaking the current system would be to reduce the repayment rate or to increase the repayment threshold. Either of these changes could be designed to be approximately cost-neutral in the long run only if they were combined with other changes that led to some graduates repaying more at some point – for instance, by extending the write-off period on the loans. Even if these reforms did not change the way total costs were shared between taxpayers and affected graduates, they would be likely to redistribute amongst graduates, with some graduates repaying more and some repaying less than under current government policy.

There are inherently political choices involved in decisions about how higher education should be financed, and how these costs should be shared between individuals – both amongst graduates in the same cohort, and between graduates and the wider taxpaying public. The outstanding Plan 2 student loan book represents a substantial asset on the government books – and repaying these loans will have a meaningful impact on the living standards of several million recent graduates over the next few decades. Most major changes would have important consequences for the public finances, although there are tweaks that government could make that could change who pays, or when they pay, without substantial costs for the taxpayer.

Table 1. Proposed reforms and potential impact if reforms were implemented immediately only for those who started university in 2022/23

Note: Changes compared with estimated repayments and exchequer cost of current government policy. Expected total lifetime repayments are expressed in undiscounted CPI real terms (2025–26 prices) and are for all borrowers and for those in the bottom and top deciles of lifetime earnings. Total exchequer costs of these reforms reflect the change in real-terms repayments expressed in undiscounted RPI real terms (2025–26 prices). Both of these reflect the impact if these reforms were introduced immediately and only for those who started university in the 2022/23 academic year. These figures are likely to overstate the impact on average lifetime repayments and to substantially understate the estimated exchequer cost if the changes were applied to earlier cohorts.

Source: IFS student finance calculator (https://ifs.org.uk/student-finance-calculator); author’s calculations.

Acknowledgements

Funding from the ESRC Centre for the Microeconomic Analysis of Public Policy (ES/Z504634/1) and the Nuffield Foundation (‘Spending across different stages of education 2024-2026’, EDO /FR-000024394) is gratefully acknowledged. The author thanks Jonathan Cribb, Christine Farquharson, Nick Ridpath, Ben Waltmann and Ben Zaranko for their feedback and assistance, and many others at IFS and elsewhere for helpful discussions.

Endnotes

Authors

Kate Ogden

Kate joined the IFS in 2020 and works on local government finance and higher education.

More from IFS

Understand this issue

Policy analysis

Academic research