Downloads

Download the report as a PDF

PDF | 7.5 MB

Executive summary

What is the effect of going to university on earnings over graduates’ lifetimes? To what extent do subject choice, institution and the prior academic attainment of those students matter? How much do individuals (and taxpayers) benefit from people going to university, once we account for the costs of financing higher education, and the tax and student loans systems? With around half of young people in England now entering university, evidence on these questions is as important as ever – both for individuals deciding whether, where and what to study, and for policymakers concerned with financing higher education.

This report investigates the lifetime financial returns to starting a full-time undergraduate degree at a UK university before age 21. We use detailed data on a cohort of England-domiciled students who were born in the mid 1980s and took their GCSE exams in 2002. We estimate how much graduates from this cohort can expect to earn over their lifetimes, and also how much they would have earned over their lifetimes had they not gone to university. We use these estimated gross lifetime returns for the 2002 GCSE cohort as an estimate of the gross returns that can be expected by future cohorts; available evidence supports this choice. We apply today’s tuition fee, student loan and tax policies to consider how these returns, net of the costs of a degree, would be shared between graduates themselves (through higher take-home pay) and the government (through student loan write-offs and higher tax revenues) under current policy. We produce estimates of the lifetime return to degrees that are informative for current and prospective students and policymakers.

This is the latest in a series of reports by researchers at the Institute for Fiscal Studies, commissioned by the Department for Education, using the Longitudinal Education Outcomes (LEO) data, which link school records, university records and tax data for English students. The work follows on from Britton et al. (2020), who also estimated the lifetime returns to higher education (HE) for the same 2002 GCSE cohort based on their observed earnings to age 30, which is relatively early in people’s careers. This report updates and extends that evidence base, drawing on seven additional years of tax data (up to 2023/24) that allow us to observe how the earnings of the same set of graduates actually evolved into their mid 30s.

This work focuses on the financial returns to higher education: the earnings benefit for individuals over working life and the tax benefits for government net of the cost of financing higher education. It does not seek to provide a complete picture of the impacts of higher education – for instance, on pension contributions, health, happiness or job satisfaction, or potential spillovers to others. We study the returns to undergraduate degrees for students who actually enrolled in them. Our results should not be interpreted as the returns that would be realised if the higher education sector were significantly expanded or contracted, or if large numbers of students were reallocated across courses and universities.

Key findings

- On average, graduates earn substantially more than non-graduates in their 30s. For a cohort of English school pupils who took their GCSE exams in 2002, we observe their earnings up to age 37. We compare those who started full-time undergraduate degrees by age 21 with those who continued in education after age 16 but did not start university, and find large earnings gaps: at age 37, median earnings among women who attended university are 56% higher than among women who did not, and among men are 28% higher.

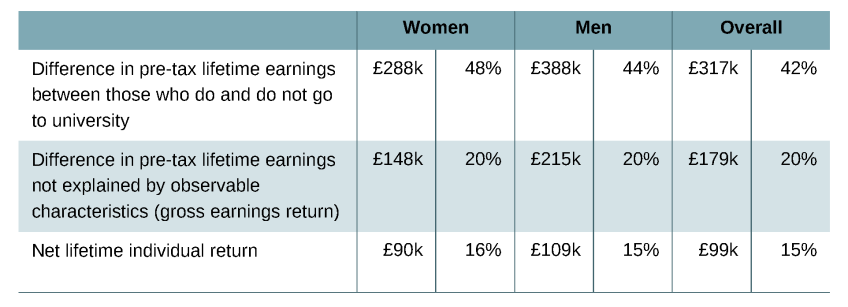

- We project that earnings gaps between graduates and non-graduates will persist throughout their working lives. We simulate the earnings and employment of the 2002 GCSE cohort up to age 67, using administrative and survey data on older cohorts. We project stronger earnings growth for graduates than for non-graduates through their 40s. Over their lifetimes and on average, we estimate that women from the 2002 GCSE cohort who attended university will earn around £290,000 (48%) more than women who did not, and graduate men around £390,000 (44%) more. These figures are in today’s prices and apply Green Book discounting.

- We estimate that differences in the background characteristics and prior attainment of graduates and non-graduates explain around half of these raw lifetime earnings gaps. When we adjust for these differences, we estimate that women who attended university will earn around £150,000 (20%) more over their lifetimes on average and men around £220,000 (20%) more than those same graduates would have earned if they had they not gone to university. We call these adjusted differences the ‘gross lifetime earnings returns’ to an undergraduate degree.

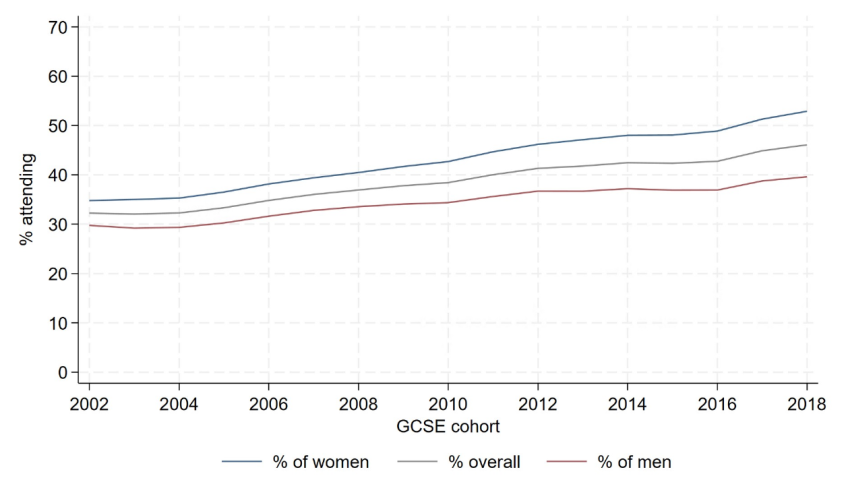

- Available evidence suggests that the earnings of the 2002 GCSE cohort are informative for policymakers and students today. It is not possible to predict with certainty how much current students will earn over the next five decades, or how much they would have earned if they had not gone to university. However, the earnings trajectories of young graduates (and young non-graduates for whom university was a realistic possibility) look strikingly similar across the 11 GCSE cohorts since 2002. We also estimate that at each specific age early in people’s careers, the gross earnings returns to attending university have remained stable across these cohorts: we do not find any evidence that the graduate premium has declined for later cohorts. This is despite a substantial increase in the share of young people who started a degree by age 21, from 32% in the 2002 GCSE cohort to 42% among those who took their GCSEs in 2013. We therefore treat the estimated gross lifetime returns for the 2002 GCSE cohort as a guide to the gross return that can be expected by future cohorts.

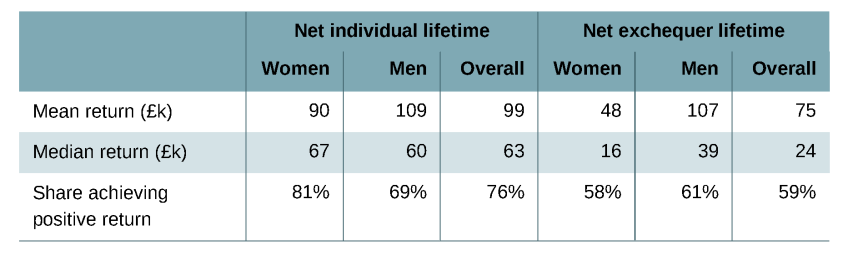

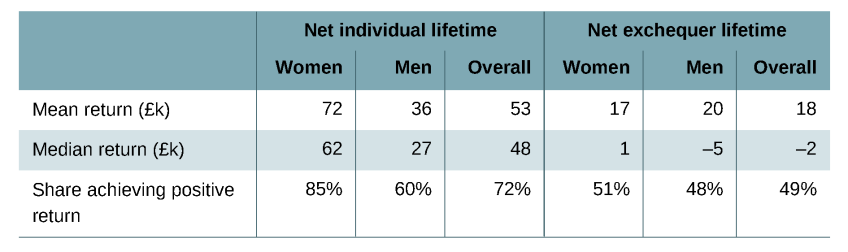

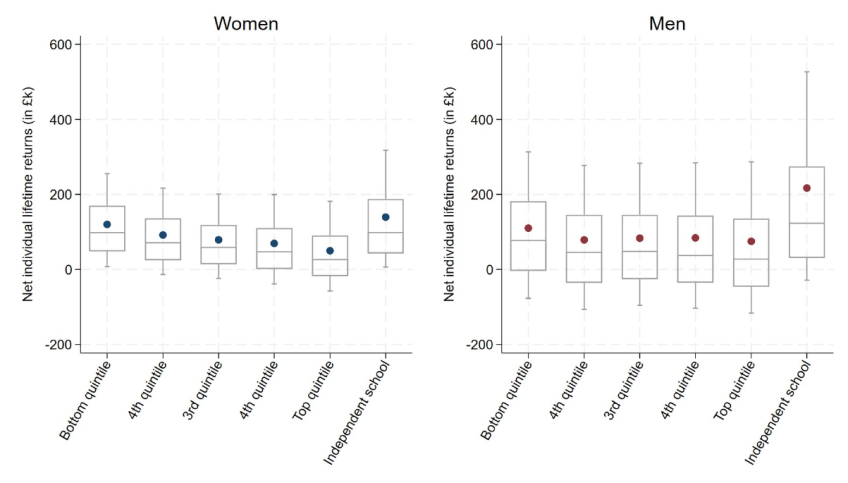

- Expected returns remain large and positive after accounting for taxes and the costs of doing a degree. We apply today’s tuition fee, student loan and tax policies to our estimates of the gross lifetime returns to doing a degree. We estimate large positive average returns from the point of view of the student. To the extent that the past is a guide to the future, the average graduate can expect to be around £100,000 (15%) better off financially than a similar young person who did not go to university, even after accounting for extra income tax, employee National Insurance contributions and student loan repayments. We estimate a slightly higher average gain for men (£109,000) than for women (£90,000). We call these the ‘net individual lifetime returns’ to an undergraduate degree.

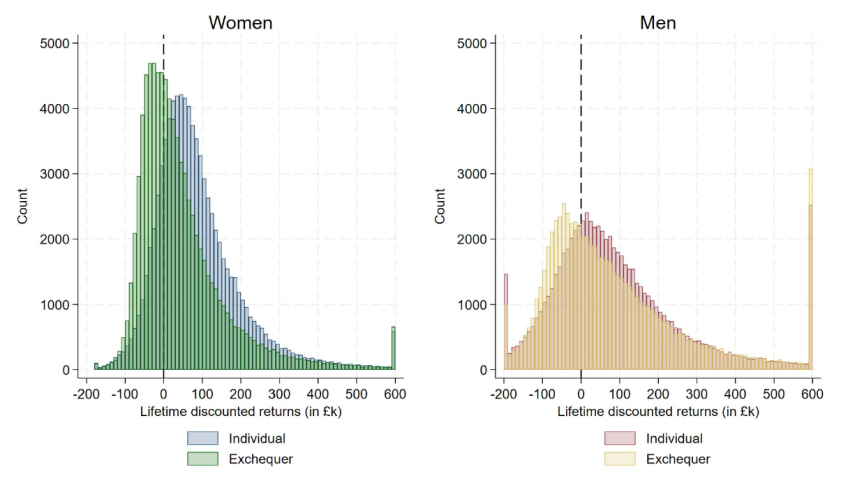

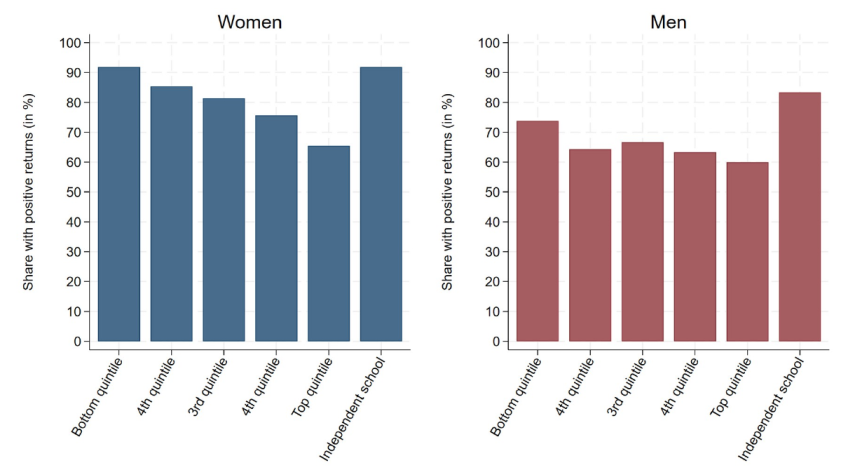

- These averages mask substantial variation in individual returns across people. We estimate that the 10% of women with the highest net lifetime returns can expect to gain more than £230,000; 10% of men can expect to gain more than £330,000. These very high returns for some pull up the mean returns; median net individual lifetime returns are lower, at £67,000 for women and £60,000 for men. We estimate that around 20% of women and 30% of men can expect a negative return, i.e. they would be financially worse off than if they had not gone to university. We estimate that the 10% of women with the lowest net lifetime returns are more than £30,000 worse off, while 10% of men can expect to be more than £90,000 worse off over their lifetime.

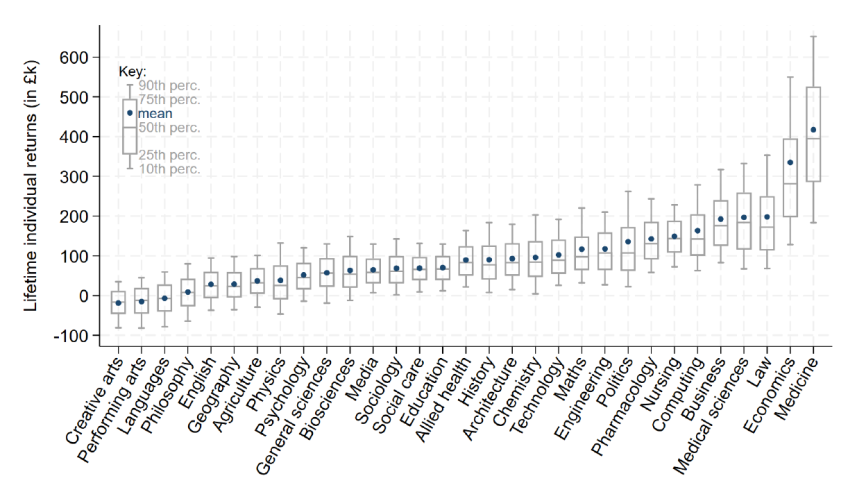

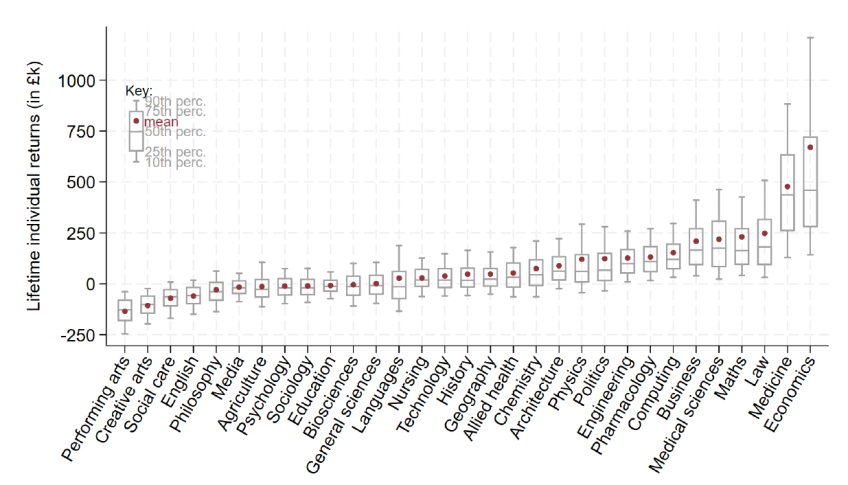

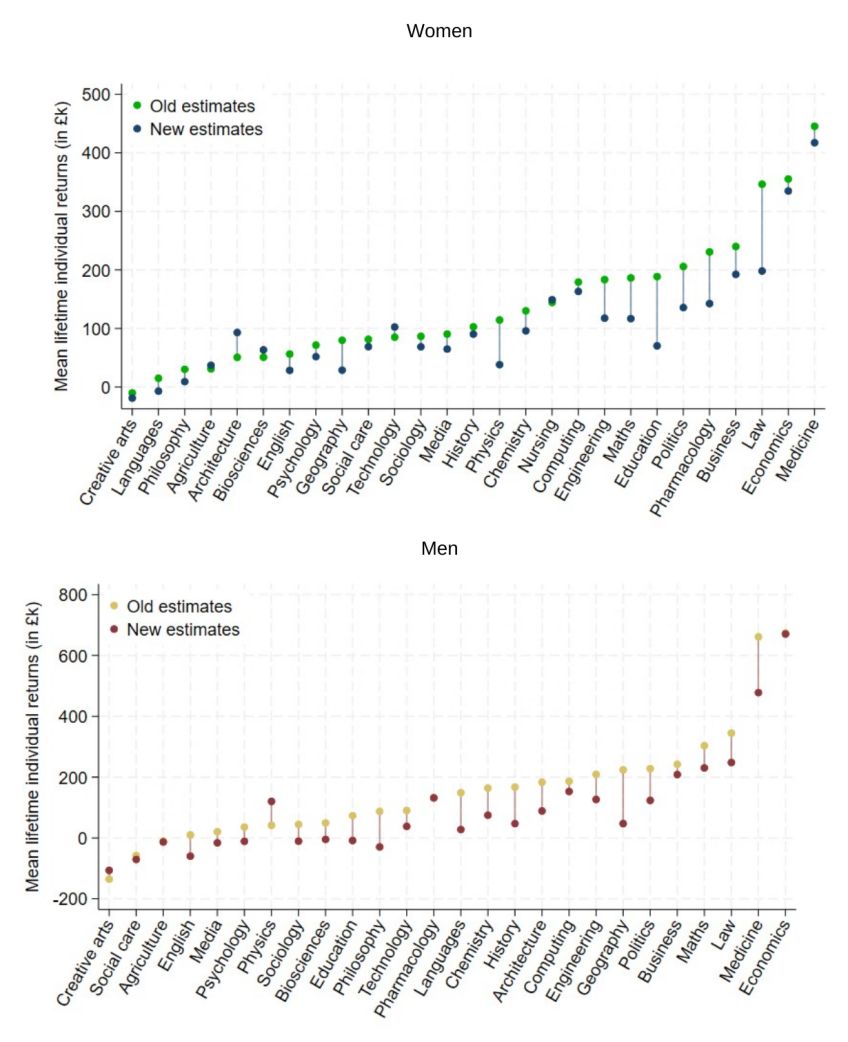

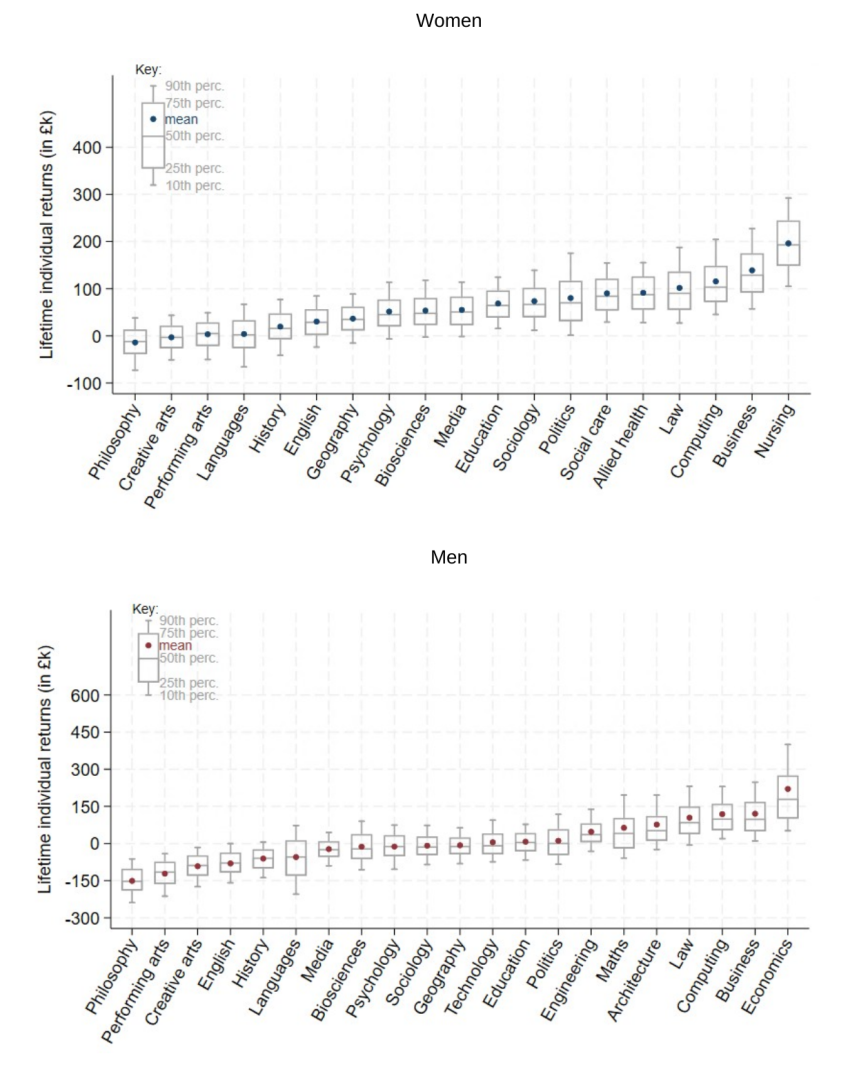

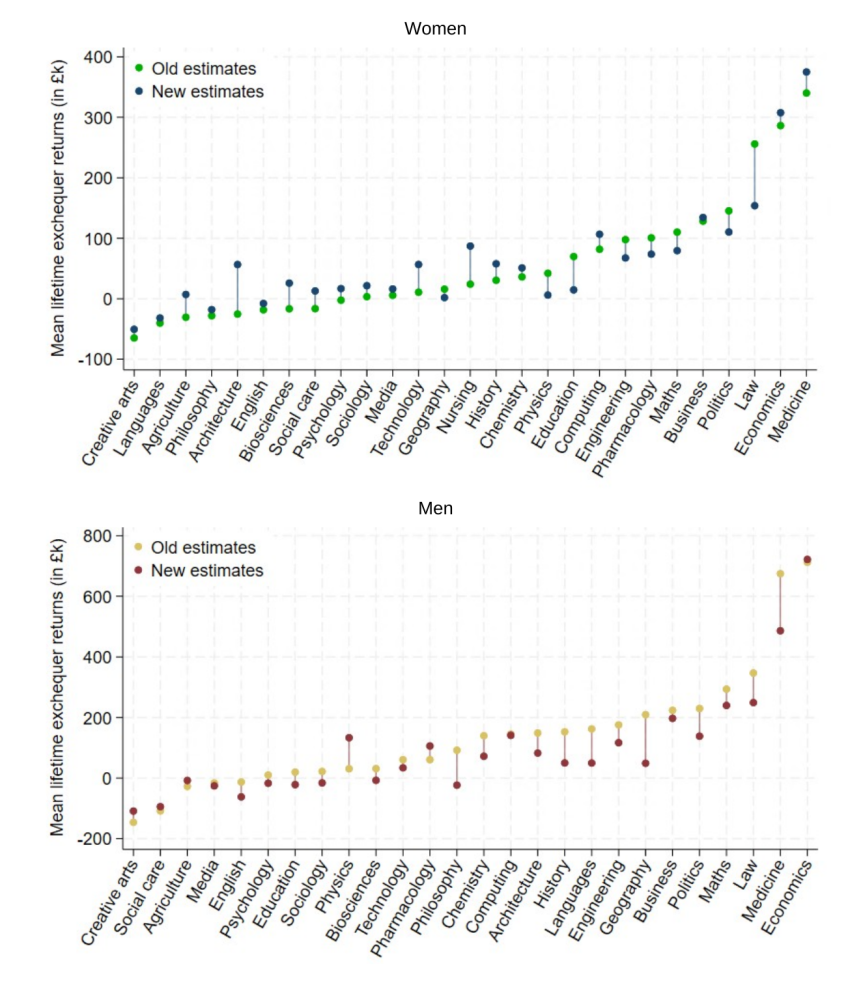

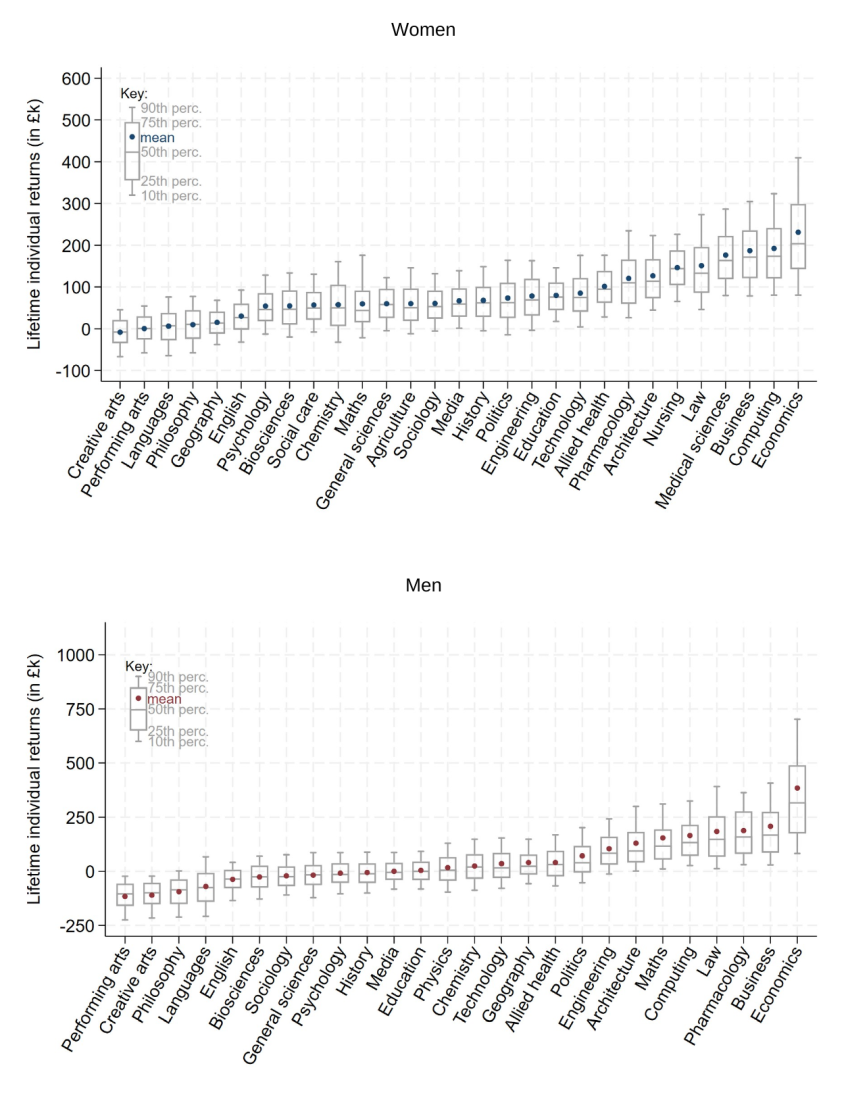

- Variation in estimated net lifetime returns by subject is very large. Medicine and economics offer the highest individual net lifetime returns – over £400,000 on average. We estimate low or negative individual returns on average for several subjects, including creative arts, philosophy and languages (although this does not mean estimated returns are negative for all students who take them).

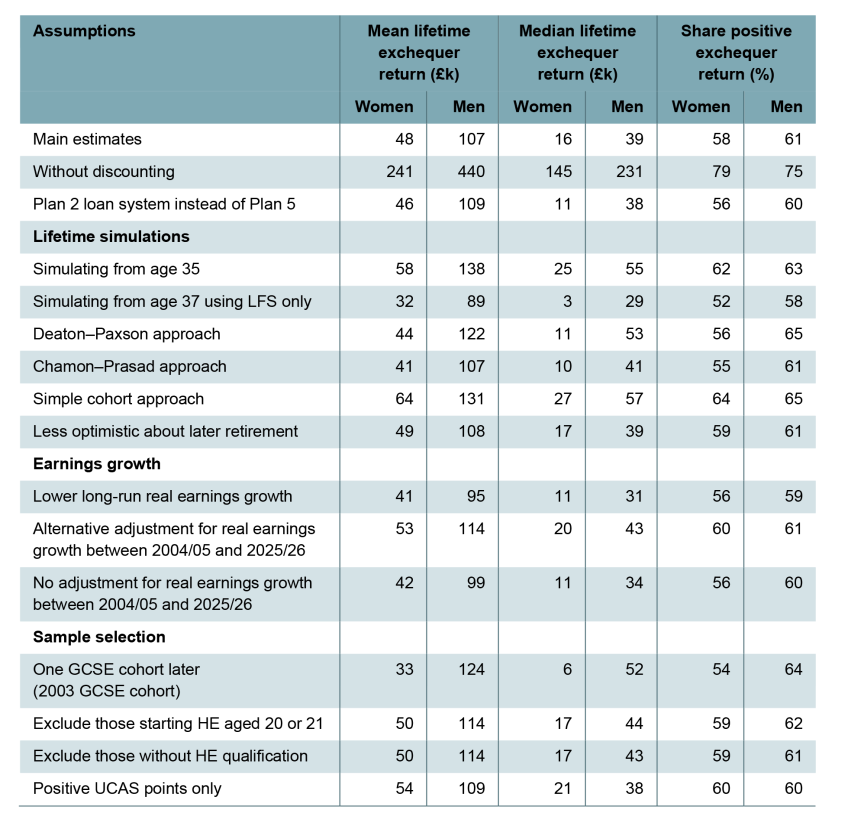

- Financing undergraduate degrees is a substantial investment from the point of view of the taxpayer – but one that pays off in the long run, on average. The exchequer faces up-front outlay on loans for tuition fees and students’ living costs, but when we account for future student loan repayments and revenues from income tax and National Insurance contributions, we estimate that the exchequer can expect average returns of £48,000 for women and £107,000 for men who enrol in university. That said, we estimate that the exchequer can expect to make a loss on around 40% of degrees.

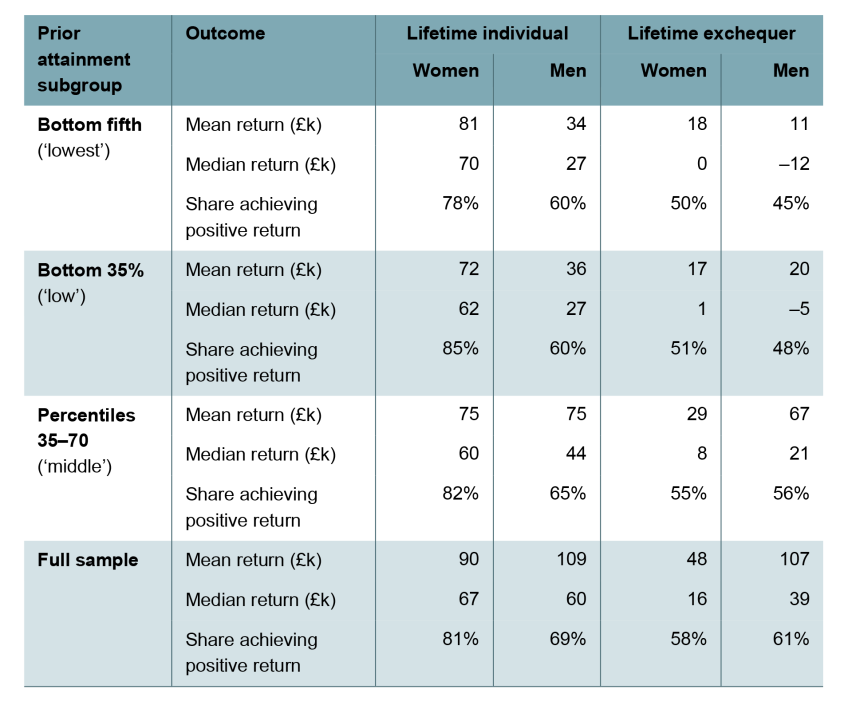

- We estimate that expected individual lifetime returns are lower for students with lower prior attainment, but still positive on average. Among those from the 2002 GCSE cohort who continued in education after age 16, we estimate substantially lower net returns to university for the 35% with the lowest scores in their GCSEs (who had the equivalent of five C grades but no more than four Bs and four Cs in their top eight GCSEs). To the extent that the past is a guide to the future, women with low prior attainment who go to university can expect to be around £72,000 better off financially on average than if they had not gone. The equivalent figure for men is around £36,000. We estimate that individual returns would be negative for around 15% of women and 40% of men in this ‘low prior attainment’ group, with the exchequer expected to make a loss on around half of these degrees. Estimates are similar for the lowest-attaining 20% of students who continued in education after age 16.

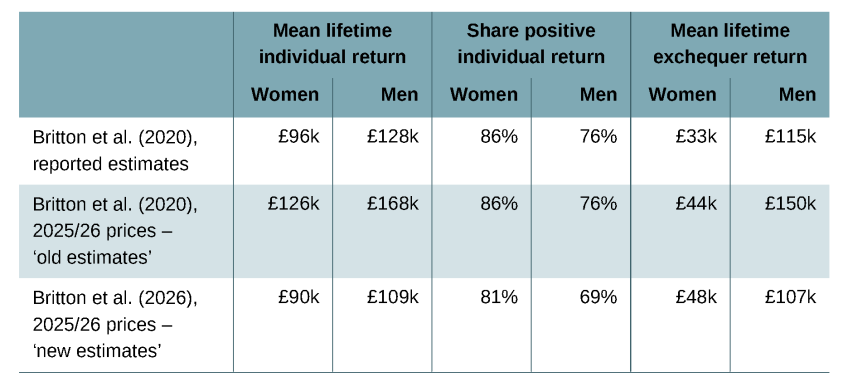

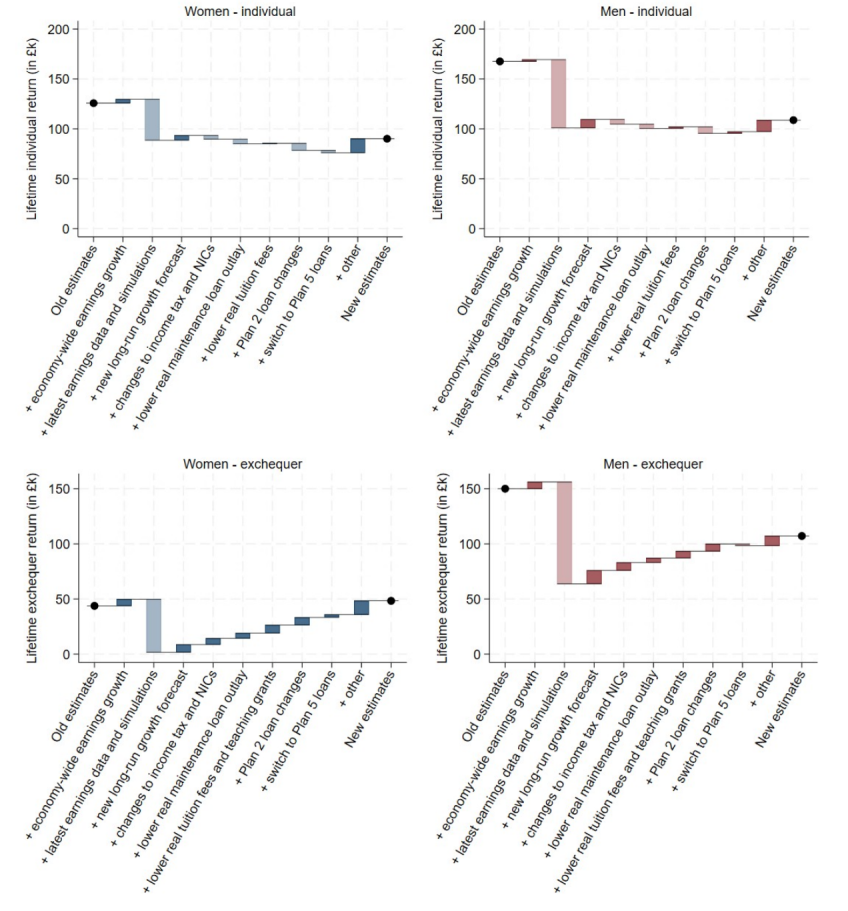

- Our estimates of average net individual lifetime returns are around 30% (£46,000) lower than the headline figures in Britton et al. (2020). The updated estimates are based on the same 2002 GCSE cohort, but draw on seven additional years of tax data that allow us to observe how the earnings of the same set of graduates actually evolved into their mid 30s (up to 2023/24). These actual earnings were lower in real terms than our earlier modelling suggested. This partly reflects the uncertainty inherent in any simulation exercise: we now reflect shifts in the employment patterns of women, and recent shocks including COVID-19 and the cost-of-living crisis were not foreseeable when the last report was published in February 2020.

- Policy changes have also shifted lifetime returns away from the individual and towards the exchequer since Britton et al. (2020) was published. Maintenance loan entitlements have become less generous in real terms, student loan terms have changed and personal tax thresholds have been frozen. The exchequer now faces a lower cost to financing degrees up front, and a larger share of graduates’ earnings gains are expected to accrue to the exchequer through higher tax payments. Taken together, we estimate policy changes have reduced average net individual lifetime returns by around £15,000 (accounting for a third of the overall reduction) and increased average exchequer returns by around £25,000 compared with Britton et al. (2020). Despite the worse picture for underlying earnings, policy changes mean we now estimate higher average exchequer returns for women than in our 2020 report.

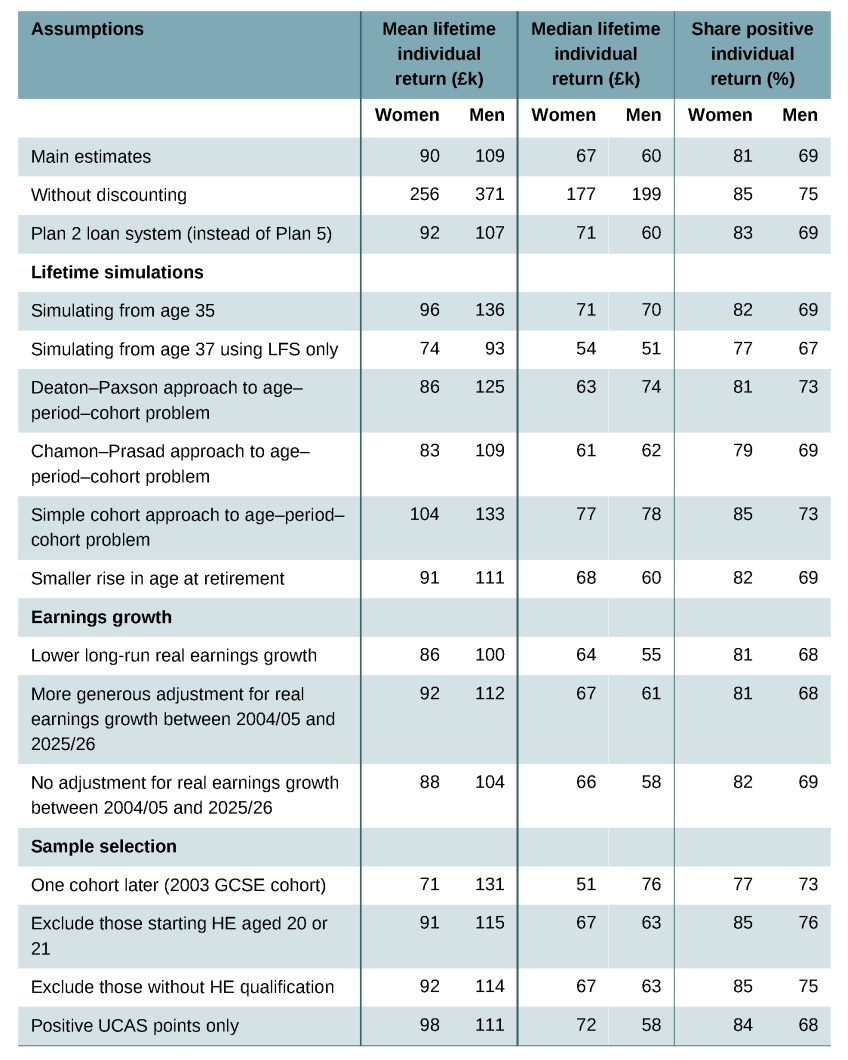

- Any estimate involving assumptions about the future is uncertain – but our conclusion that average net returns for individuals over the lifetime are large and positive is robust. To indicate the sensitivity of these results to the specific assumptions we make, we model alternative approaches to simulating lifetime earnings with the data available, including using earnings data only up to 2021/22 (before the cost-of-living crisis) or assuming long-run real earnings growth is slower than the Office for Budget Responsibility’s projection (1.2% instead of 1.8%). We estimate average lifetime individual returns that are as much as 16% higher or 21% lower for women and 25% higher or 15% lower for men than our main estimates. We do not attempt to model the impact of potential structural changes to the economy (such as might result from AI, for example) or future changes to taxes or student loans policy: these could still mean that the lifetime returns for current students are not well approximated by historical data.

- Our estimates are sensitive to the choice of discount rate, which determines how we compare costs and benefits occurring over different time periods. To express lifetime returns in terms of earnings at age 18, all of the estimates above apply a real discount rate of 3.5% for the first 30 years and 3.0% thereafter, reflecting the government’s Green Book guidance. With a 0% real discount rate (i.e. adjusting only for CPI inflation), our estimates of the lifetime net individual returns to a degree would be much higher: around £260,000 on average for women and £370,000 for men. We would estimate that the exchequer makes a loss on less than a quarter of degrees (compared with 40% with Green Book discounting).

1. Introduction

Higher education has expanded dramatically in England over recent decades, with around half of young people now entering university.1 This expansion has been underpinned by a system for financing higher education that shifts a significant share of the costs of degrees onto graduates themselves in the longer run, while aiming to protect graduates who go on to have low earnings after university from unaffordable student loan repayments. Against this backdrop, understanding the financial returns to higher education – who gains, by how much, and whether those gains justify the cost to both individuals and the taxpayer – is a central question for higher education policy. This report investigates the lifetime financial returns to starting a full-time undergraduate degree at a UK university before age 21.

Previous work at IFS (Britton et al., 2020) has documented large average returns to individuals attending university, but also striking variation: returns differ enormously by subject studied and by institution, and some graduates see little or no financial benefit from their degree. However, those estimates were based on individuals tracked only up to age 30 in the labour market, which is relatively early in people’s careers, and used data up to the 2016/17 tax year. This report updates and extends that evidence base, drawing on seven additional years of tax data (up to 2023/24) that allow us to observe how the earnings of the same set of graduates actually evolved into their mid 30s.

Our approach involves linking individuals’ school, university and tax records so we can observe their background characteristics (gender, ethnicity and socio-economic background), their attainment in Year 6 SATs, GCSEs and A levels, the university they attended and the subject they studied, and their earnings. We focus on a cohort of England-domiciled students who were born in the mid 1980s and took their GCSE exams in 2002. We observe how much they earn in each tax year up to age 37 and, beyond this age, we simulate their employment and earnings over the rest of their working lives. These simulations reflect historical patterns of earnings growth and employment transitions at later ages, and are based on some additional administrative data and the Labour Force Survey. We predict counterfactual employment and earnings profiles for the 2002 GCSE cohort if they had not attended higher education. Comparing this with their actual (and simulated) earnings allows us to estimate the gross lifetime earnings return to a degree.

We then apply today’s tuition fee, student loan and tax policies, to approximate the policies that would apply for someone aged 18 in 2025/26. We do this to make our results as relevant as possible for current students and policymakers. This allows us to estimate how the financial return to higher education – and the cost of a degree – would be split into a net return to the individual (through higher take-home pay) and a net return to the exchequer (through student loan write-offs and higher tax revenues) under current government policy. The results of this accounting exercise can be interpreted as the net returns to undergraduate degrees for the 2002 cohort, had they instead faced today’s policies (and assuming that their earnings would not have themselves been influenced by the policies in place).

We describe the data we use (Chapter 2) and our methodology (Chapter 3) which closely follows that in Britton et al. (2020). We describe the actual earnings of graduates and non-graduates from the 2002 GCSE cohort (Chapter 4). We then estimate individual and exchequer lifetime returns for those who attend higher education under current government policy, and investigate how these vary by gender, subject and institution type (Chapter 5). We discuss the conceptual limitations of our approach, including what these estimates can and cannot tell us about policy, and then assess how sensitive our main estimates are to alternative modelling decisions (Chapter 6). We compare our new headline estimates with those from previous work at IFS and explore why our estimates have changed (Chapter 7). We then investigate the returns for students with relatively low prior attainment (Chapter 8). Finally, we consider how useful our estimates of lifetime returns may be for later cohorts of students, adding new evidence to the important question of how the graduate premium may have been changing over time (Chapter 9).

2. Data

We use the Longitudinal Education Outcomes (LEO) dataset, which links labour market outcomes to school, further education and higher education records. We specifically use:

- school attainment records and demographic characteristics from the National Pupil Database (NPD);

- university records from the Higher Education Statistics Agency (HESA);

- earnings and employment data from HM Revenue & Customs (HMRC).

The NPD records contain rich background characteristics, including a student’s ethnicity, their home region and their eligibility for free school meals. They also contain rich details on a student’s prior attainment, including their scores in standardised tests at age 11 (Year 6 SATs) and their subject choices and scores for both GCSE and A-level exams. The HESA records track students through the university system, detailing the subject and institution for all courses taken by the student. The HMRC records contain data on annual earnings between tax years 2003/04 and 2023/24. From 2013/14 onwards, this includes income from self-employment from self-assessment tax records. Prior to this, we only observe earnings from employment.

The earliest cohort for which we have this fully linked administrative data took their GCSEs in the 2001/02 academic year, and the vast majority of them were born in 1985/86. We focus on this cohort for our main analysis (hereafter referred to as the ‘2002 GCSE cohort’). Among the students for whom we have rich information on background characteristics from school records, this is the cohort for which we can observe earnings at the oldest age. We observe earnings for this cohort between ages 17 and 37.

We also use the Labour Force Survey (LFS), a quarterly survey of approximately 40,000 UK households. Survey questions include demographic details, educational qualifications including subject studied at university, employment and earnings. Households are surveyed for five consecutive quarters and are asked questions on earnings in the first and final waves. We derive two datasets from the LFS: first, a five-quarterly LFS panel, linking individuals’ responses from waves 1 and 5, which we use to examine year-on-year changes in employment and earnings for individuals who respond to both waves; and second, a repeated cross-section of earnings, a snapshot of employment and earnings each quarter for a larger sample of individuals. We use both the year-on-year changes and the repeated cross-section to simulate earnings and employment transitions beyond age 37 for our cohort of interest. We use LFS data from 1997 up to March 2020.2

For graduates, we also complement our simulations using additional administrative data: linked HESA and HMRC records for students from the 1978/79 to 1984/85 birth cohorts. For these students, we observe degree subject and institution attended, but none of the data on demographic characteristics or prior attainment that we take from school records for later cohorts. We observe earnings and employment for these students up to age 44 at the latest and use these data to simulate earnings trajectories for graduates in our cohort of interest between the ages of 38 and 44.

2.1 Sample selection

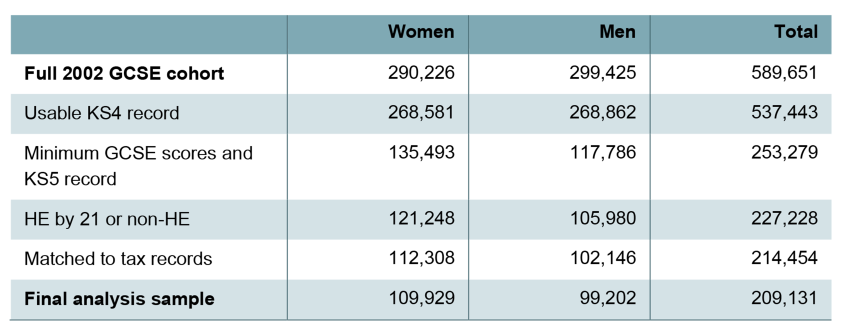

We restrict our main analysis sample to individuals from the 2002 GCSE cohort who achieved at least the points equivalent of five C grades in their top eight GCSE exams. We also require individuals to have a Key Stage 5 record within three years of the year in which they sat their GCSEs. We apply these criteria to ensure that our analysis is limited to people who could have chosen to enter university at, or soon after, age 18.

Following Britton et al. (2020), we focus on the returns to a specific ‘typical’ higher education (HE) trajectory: full-time undergraduate study beginning between the ages of 17 and 21. We exclude those who we observe to start a first undergraduate degree after age 21 or who studied part-time. We also exclude those who have only attended university for an ‘other undergraduate degree’ such as a foundation degree, unless they go on to begin a first undergraduate degree by age 21. We exclude these groups because their returns are likely to differ substantially, and constructing a credible counterfactual is considerably more challenging. Our comparison is therefore between students attending university for a full-time first undergraduate degree and individuals not attending university at all.3 We refer to these as the HE and non-HE groups hereafter for brevity, notwithstanding that in other contexts HE often refers to all study at Level 4 or higher.

Finally, note that we include all those who start a given course in our HE group, regardless of whether they are observed to graduate or to later switch course. This means we are considering the returns to attending university for an undergraduate degree, rather than completing a degree (we use the terms ‘graduates’ and ‘non-graduates’ for our HE and non-HE groups for ease of exposition, even though some individuals in our HE group do not graduate).

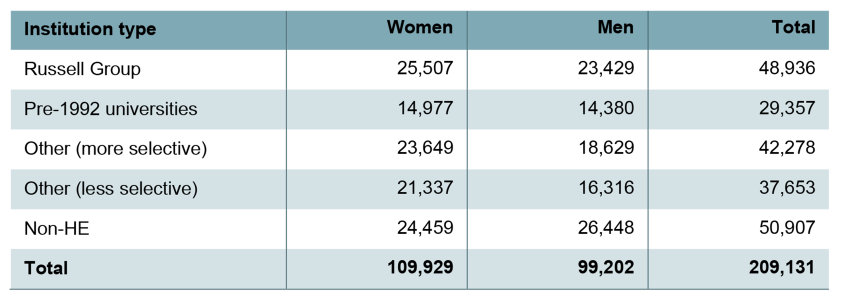

Altogether, our main analysis sample consists of 209,131 individuals, of whom 158,224 (76%) are in our HE group and 50,907 are in our non-HE group. More details on sample selection and sample sizes by sex and institution type are given in Appendix A.

3. Methodology

There are two substantial methodological challenges in estimating the lifetime returns to higher education (HE). First, data limitations mean that we are not able to observe people over the entire life cycle. This limitation is structural: even if we could observe a cohort that had completed their time in the labour market (born in the early 1950s, say), their returns to higher education would not be especially relevant to today’s graduates. Second, people self-select into different HE pathways. This means those who do and do not attend HE may differ in important ways, and they may have different earnings trajectories for reasons other than that some attended university and some did not.

Our approach closely follows Britton et al. (2020). We address these challenges by using data on the 1985/86 birth cohort – the oldest cohort for which we observe detailed background characteristics, which are crucial for addressing the self-selection issue. This cohort is sufficiently recent to still be informative as to the returns to HE today, but is old enough that we observe sufficient years of earnings to estimate lifetime returns. We are now able to observe this cohort’s earnings up to age 37 and then we simulate their employment and earnings up to age 67.

Our method for the simulation combines information on the levels and dynamics of earnings and employment from older graduates and non-graduates in their mid and late careers with long-run official forecasts of economy-wide real earnings growth. For data on older cohorts, we mainly rely on the Labour Force Survey (LFS), but also on some linked administrative records of people who attended university in the mid 1990s. We describe the simulation process in more detail in Section 3.1. The results of these simulations for our HE and non-HE groups are presented in Chapter 4.

Once we have actual (and simulated) earnings paths to retirement for both those who do and those who do not attend HE, we then fit econometric models to estimate the returns to attending HE at each age. This relies on comparing the earnings of individuals who attended HE with those who have similar observable characteristics in the Longitudinal Education Outcomes (LEO) data but who did not attend HE. We use these estimated returns to generate counterfactual earnings profiles for those who attended HE, predicting what they would have otherwise earned if they had not attended HE. The difference between the HE (actual and simulated) and the counterfactual earnings paths provides an estimate of gross earnings returns at each age and for each individual in the 2002 GCSE cohort. We sum these over the lifetime to calculate an individual’s gross lifetime earnings returns.

To make our results as relevant as possible for current students and policymakers, we then apply today’s tuition fee, student loan and tax policies to these gross lifetime earnings returns, approximating the policies that would apply for someone aged 18 in 2025/26. This allows us to estimate how the financial return to higher education – and the cost of a degree – would be split into a net individual lifetime return (through higher take-home pay) and a net return to the exchequer (through student loan write-offs and higher tax revenues) under current government policy. We discuss our approach for estimating returns further in Section 3.2 and we present results in Chapter 5.

Our approach for constructing counterfactual earnings at each age draws upon the rich background information from the National Pupil Database (NPD), which includes information about students’ socio-economic background, demographic characteristics (such as gender and ethnicity) and detailed information on attainment during primary and secondary school. While controlling for these characteristics is a substantial improvement on comparisons of average earnings of graduates and non-graduates, or of those studying different subjects, it is still unlikely to recover the true causal effect of attending HE. In particular, there may be student selection into attending HE based on characteristics that we do not observe in the LEO data and therefore cannot control for, but which have some independent relationship with future earnings: in other words, there may be selection on unobservables. It is typically assumed that a rich selection on observables approach such as ours will somewhat overstate the true causal returns to HE, although this is not certain. We discuss these and other limitations in detail in Chapter 6, as well as describing how robust our main estimates are to different modelling approaches.

We also extend the work of Britton et al. (2020) in two further ways. First, we consider the lifetime returns to HE separately by prior attainment (Chapter 8). Given the dramatic expansion in the number of young people attending university in England over recent decades, the returns for students with lower prior attainment (who are closer to being ‘academically marginal’) are of particular interest. Second, we draw on additional years of tax data to investigate how returns have changed over time for later cohorts of students, and on the latest student entrant data to suggest how changes in the composition of students might have affected average returns (Chapter 9). We describe our approach to the analysis underlying the results in these chapters in Sections 3.3 and 3.4 respectively.

3.1 Modelling life-cycle earnings

We observe earnings and employment for the LEO sample up to age 37 and simulate their labour market outcomes between ages 38 and 67.

Transitions at adjacent ages in the labour market are at the heart of our simulations of life-cycle earnings. We model each individual’s labour market outcomes at a given age as a function of their employment status and income rank within their cohort at the previous age. Our models are estimated on labour market transitions in the LFS and are then applied to the 2002 LEO sample to project forwards from age 37 up to retirement at age 67.

Our focus on transitions captures two important features of life-cycle earnings. First, an individual’s earnings usually do not change smoothly as they age. Instead, they may move between employment and unemployment and experience discrete jumps and falls in their earnings. This is especially important when estimating life-cycle returns net of taxes and student loans, as the tax and loan systems are non-linear. Second, earnings are correlated over time: relatively high earners at a given age are likely to be high earners at the next age. Our model reflects this persistence at adjacent ages, while allowing for potential earnings and employment shocks each year.

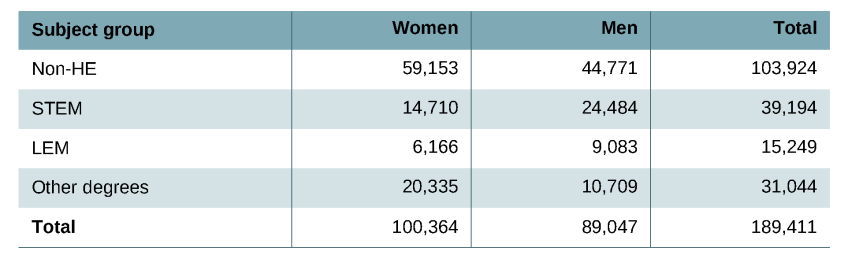

We allow the models to vary by sex and by subject studied at university. Given sample constraints in the LFS, we are unable to estimate separate labour market transitions for each university subject; instead, we split the sample into four groups and estimate separately by sex within each group. Following Walker and Zhu (2013) and Britton et al. (2020), these groups are those studying STEM subjects (science, technology, engineering and maths), those studying LEM subjects (law, economics and management), those studying other degree subjects and non-graduates.

Simulating employment

We model employment at each age and for each individual as a function of the individual’s employment status at the previous age and, if they were employed, their earnings rank at the previous age.4

For those employed at the previous age, we predict the likelihood of an individual remaining employed as a function of their earnings rank at the previous age, using a probit model. This is estimated using the five-quarterly LFS panel data, separately by sex and subject group. For those unemployed at the previous age, we do not observe an earnings rank and so instead assume their probability of being employed at an age matches the mean rate of employment amongst people of the same age and in the same sex–subject group in the LFS who were unemployed at the previous age.5

We have different definitions of employment in the administrative and survey data, and these also cover different time periods. To avoid jumps in the estimated employment rate between the ages of 37 and 38, we adjust the parameters estimated in the survey data so that they are consistent with the parameters we would have estimated from applying the same method to the administrative data at an overlapping age. This is done by fitting an identical model to the administrative data at the age 36–37 transition, saving the ratio of the parameters estimated using the administrative and survey data, and adjusting the parameters estimated at each later age in the survey data by this same ratio.

Using the fitted, smoothed and adjusted parameters, we calculate a probability of each individual in the LEO sample being employed at a given age, given their earnings rank in the previous year, and we randomly assign their employment status accordingly. We do this iteratively for all transitions from 37–38 up to 66–67.

Simulating earnings rank

Similarly, we model earnings rank at each age and for each individual as a function of the individual’s earnings rank at the previous age. We use a copula method to capture intertemporal dependence in earnings ranks.6 Given an individual’s position in the earnings distribution at the previous age, a copula function describes the probability distribution of that same individual’s earnings rank at the next age. Intuitively, this method allows us to capture that an individual’s earnings rank strongly but not perfectly predicts their earnings rank the following year, so that there is some re-ranking between ages.

We estimate copulas from the five-quarterly LFS data, separately by age, sex and subject group. As with modelling employment, we adjust the parameters to account for differences between the administrative and survey data. We use the estimated copula parameters to simulate a rank in the earnings distribution for each individual in our sample at each age, given their earnings rank in the previous period, beyond age 37. For those unemployed at the previous age, we cannot use the copulas to simulate a rank. Instead, we retain the earnings ranks of individuals of the same age, sex and subject group who re-enter employment in the LFS and randomly assign one of these ranks to individuals re-entering employment in our sample. We do this iteratively for all transitions from 37–38 up to 66–67.

Assigning earnings levels to ranks

Having assigned individuals at each age a rank in the earnings distribution (amongst people of the same age, sex and subject), we then need to assign actual earnings levels to these individuals, if they are employed in our simulation. To do this, we need to model how earnings will change for a set of individuals at consecutive ages. For this exercise, we do not rely on individual labour market transitions (i.e. repeated observations of earnings for the same individual over time) but instead use cross-sectional data on all individuals observed at a given age. This means we can use individuals reporting their earnings in only one wave of the LFS, increasing our sample size. Using this larger sample, we can estimate profiles of earnings growth over age separately by sex and for each subject, rather than by subject group.

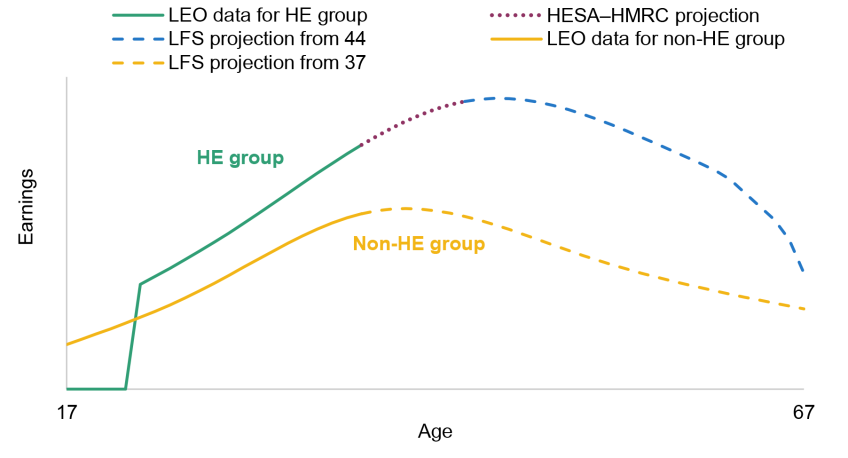

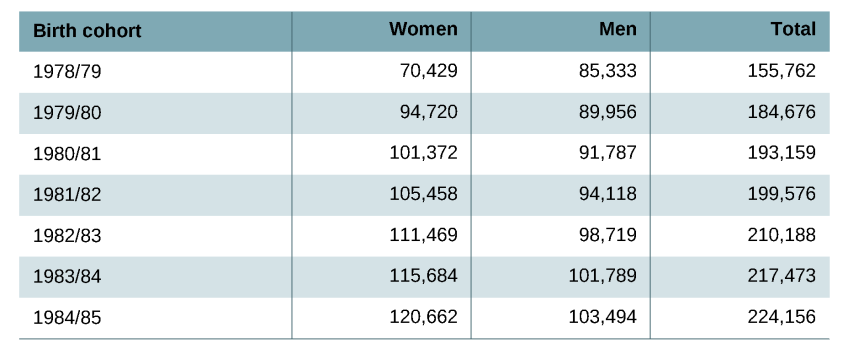

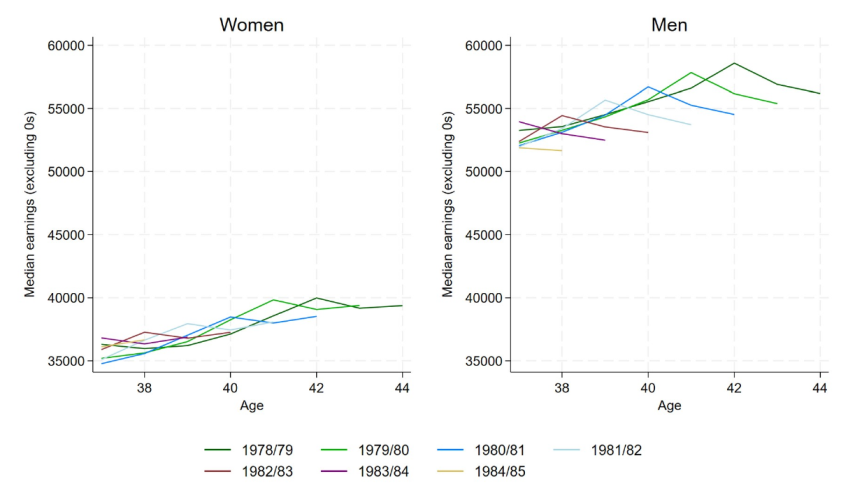

Additionally, we use linked HESA–HMRC data for cohorts of students that are slightly older than our 2002 GCSE cohort. The samples by subject and age are much larger and more recent in these administrative data, so we favour the HESA–HMRC data over the LFS where possible. These data are not available for our non-HE group as only those who attend higher education have a HESA record. For our HE group only, we use HESA–HMRC cohorts born between academic years 1978/79 and 1984/85 to construct earnings profiles up to age 44, then use the LFS to extend these profiles beyond age 44, as shown in Figure 3.1.7 In Chapter 6, we also show the robustness of our results to using the LFS only for ages 38 to 44 instead of the HESA–HMRC data.

Figure 3.1. Schematic representation of our methodology

Note: The figure provides a schematic representation of the actual and simulated earnings for individuals from our HE and non-HE groups.

Extracting measures of earnings growth by age from observational data is challenging because each birth cohort is only observed at a given age in a single period. For instance, if 38-year-olds are observed to earn more than 37-year-olds in a given year, this could be because the 38-year-olds have an extra year of experience (an age effect) or might reflect something about the specific cohorts – for instance, that the 37-year-olds initially joined the labour market during a recession or had different experiences at school (a cohort effect). Equally, if individuals in the same cohort (who were in the same school year) are observed to earn more in 2025 than they did in 2024, this could reflect an age effect, or economy-wide earnings growth between 2024 and 2025 (a period effect). It is in general impossible to disentangle the effect of changes in age from changes in period and cohort without making substantive assumptions. In the economics literature, this difficulty is known as the age–period–cohort problem.

Our preferred approach to this problem is to take a ‘simple period view’: we effectively assume that there are no cohort effects, and attribute earnings differences across cohorts in a given year to age effects rather than to cohort effects.8 More specifically, we de-mean earnings data from the LFS or HESA–HMRC data within tax years, removing variation in average earnings over time that is due to changing macroeconomic conditions. We then compare de-meaned (log) earnings at each pair of adjacent ages, and perform this exercise separately by sex and subject: intuitively, we pool across many years of data and, for example, compare the earnings of women aged 40 who studied law with the earnings of women age 41 who studied law, to estimate how the earnings of women who studied law typically change between these ages.9 This is only one possible way of extracting measures of earnings growth with age from data on previous cohorts. We discuss several alternative methods, and the robustness of our results to these, in Chapter 6 and Appendix G.

For non-graduates, we calculate average (log) earnings growth at each percentile of the earnings distribution, separately by age and sex, and apply these earnings growth rates to each percentile of the distribution of non-graduate earnings observed in the LEO data at age 37. This allows us to simulate a full distribution of non-graduate earnings at each later age. For our HE sample, we also start with the earnings distribution observed in administrative data by sex and subject, but then adjust the mean and standard deviation of the earnings distribution by sex and subject group at each later age based on by-age changes observed in the LFS. We sample systematically from the resulting distribution to map specific earnings levels at each age onto earnings ranks.

We must also account for how economy-wide earnings might change over time in future years, independent of age effects. To do so, we apply forecast long-run real growth in average weekly earnings based on the latest published official forecasts from the Office for Budget Responsibility (OBR), which currently project real growth of 1.8% each year in the long run.10 In Chapter 6, we show the sensitivity of our results to a less optimistic real earnings growth projection. Importantly, the projection used affects the simulated levels of both graduate and non-graduate earnings, but also implicitly changes how important earnings differences are at later ages compared with at earlier ages.

Modelling retirement

Changing retirement patterns over time are a threat to the reliability of our life-cycle simulations. This is especially true for women, where the state pension age for some women we observe in the LFS data was 60. It has since risen to 66 and is soon set to increase to 67. To reflect rising retirement ages in later cohorts relative to those observed at older ages in the LFS data, we fix model parameters for eight years at age 51, with parameters from ages 60 to 67 corresponding to ages 52 to 59 in the data. In practice, our estimated returns will not be dramatically affected by what happens to employment rates of individuals later in life as earnings are discounted; earnings towards the end of people’s working lives will have a smaller impact on their total discounted lifetime earnings than earnings at the start of their careers. We show the impact of an alternative approach to modelling retirement in Chapter 6.

3.2 Estimating returns

As described above, a key challenge is addressing the self-selection problem. Those who attend university tend to have performed better at school and on average come from higher socio-economic status backgrounds. The NPD data allow us to adjust for a very rich set of prior attainment and background characteristics that are likely to be correlated with both an individual’s choice to attend higher education and their labour market outcomes. We do this in a regression model which we use to develop a counterfactual gross earnings profile for each graduate had they not attended HE. We then calculate net (post-tax) earnings by applying the tax and student loan systems. We approximate net individual lifetime returns based on the difference between net graduate earnings (using actual data up to 37 and simulated data thereafter) and net counterfactual earnings.

Assigning counterfactual employment

We assign a counterfactual employment status for every graduate had they not attended HE. This is important because whether someone attends university will also have an effect on the probability of them having positive earnings in any given year.

We estimate a probit model for the probability of being employed at a given age as a function of a set of background characteristics observed in school records – specifically,

- scores in maths, English and science in Year 6 SATs (Key Stage 2 exams taken at age 11);

- scores in maths and English GCSEs and overall points score in GCSEs (Key Stage 4 exams typically taken at age 16);

- UCAS points obtained in Key Stage 5 exams;

- dummies for whether an individual studied maths, sciences, social sciences, arts, humanities, languages, vocational or other subjects at Key Stage 5;

- dummies for the region in which students were living in the year they took GCSE exams;

- dummies for nine different ethnic groups (e.g. White, Black African, Black Caribbean);

- various proxies for a student’s socio-economic status, measured in the year they took GCSE exams – specifically, whether they were eligible for free school meals, the Income Deprivation Affecting Children Index (IDACI) quintile of the small area in which they lived and whether they were attending a private school;

- whether they were recorded as having special educational needs;

- whether or not English was their first language.

We estimate this model on our sample of non-graduates, separately by sex and age, and use the fitted models to estimate a counterfactual employment rate amongst those who studied each subject, by sex and age. Each graduate begins with their actual (or simulated) employment at each age, and we then randomly assign additional graduates to be employed (or unemployed) in their counterfactual scenario to match these counterfactual employment rates by sex, age and subject.11 Intuitively, we reflect that both an individual’s actual employment status in the LEO data and their observable characteristics – which predict employment amongst non-graduates – are informative as to the probability that individuals in our HE group would have been employed had they not attended university.12

Estimating counterfactual earnings and gross earnings returns

To construct counterfactual earnings, we estimate the following regression at each age, separately by sex:

(3.1)

where is the log of individual i’s income at age a, are dummies containing the interaction terms between our 31 subject classifications and 4 institution type categories, and is a set of background characteristics – the same set as in the bulleted list above. We allow the effect of all these background characteristics to vary between graduates and non-graduates by interacting them with a dummy for whether an individual attended higher education (denoted ). Finally, accounts for varying levels of earnings at each age, and is an idiosyncratic error term.

Between ages 38 and 67, we fix the coefficients on our control variables at their age-37 values. The assumption here is that in relative (log) terms, the effect of background characteristics will be roughly constant across the life cycle from age 37. This assumption is necessary because, from age 37 onwards, we are relying on simulated earnings that are unlikely to completely capture dependence on background conditions. For example, this allows us to reflect that among individuals with identical earnings at age 37 who studied the same subject at the same university, those who performed better at school may still have higher future earnings expectations than those who did not perform as well.

The regression coefficients provide a predicted return for each individual graduate at each age, which is the effect of their interaction, combined with the differential effect of their individual background characteristics for graduates:

As above, for ages 38 to 67 we fix the coefficients on the control variables at their age-37 values. We then subtract this predicted return from graduates’ earnings to generate their counterfactual earnings:

This calculation only applies to those with positive actual (or simulated) earnings. For those who do not have positive actual earnings but who are employed in the counterfactual scenario, we assign counterfactual earnings by setting the , and variables to 0 and predicting their earnings based only on their background characteristics, .

This set-up enables us to estimate gross earnings returns separately by subject and institution type, for each gender.

Estimating net individual and exchequer returns

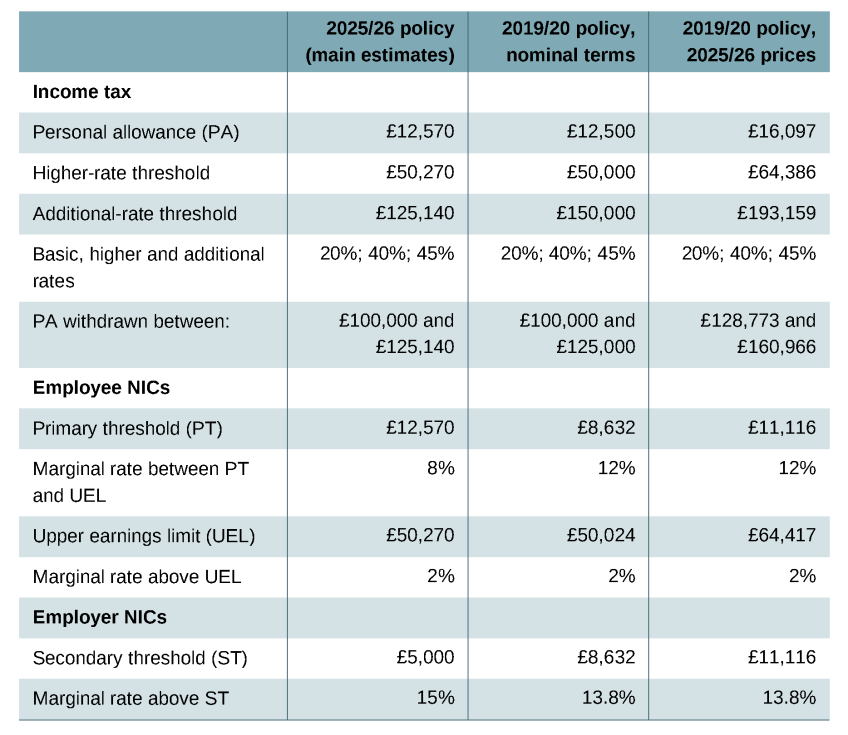

To move from gross earnings returns to estimates of net individual (and exchequer) returns, we apply the tax and student loan systems to the actual (and simulated) and counterfactual earnings of our HE group each tax year. We model these systems as if the cohort we study were 18 years old in the 2025/26 academic year to make our results as relevant as possible for policymakers and for those beginning undergraduate degrees now. In order to capture real earnings growth between the two cohorts, we adjust the earnings of the 2002 GCSE cohort in line with real earnings growth for the whole economy in the period between 2004/05 and 2025/26, when the respective cohorts would be at or entering university. This adds around 5.4% to all graduate and non-graduate earnings at all ages.13

We then apply the income tax, employee National Insurance and employer National Insurance rates and thresholds that applied in the 2025/26 tax year and project thresholds forwards in line with current government policy. For instance, this means we model planned cash-terms freezes in personal income tax thresholds until April 2031, after which point we assume these thresholds will rise each year in line with forecast CPI inflation.14 To make the modelling manageable, we do not differentiate between employment and self-employment earnings even though these are taxed differently.

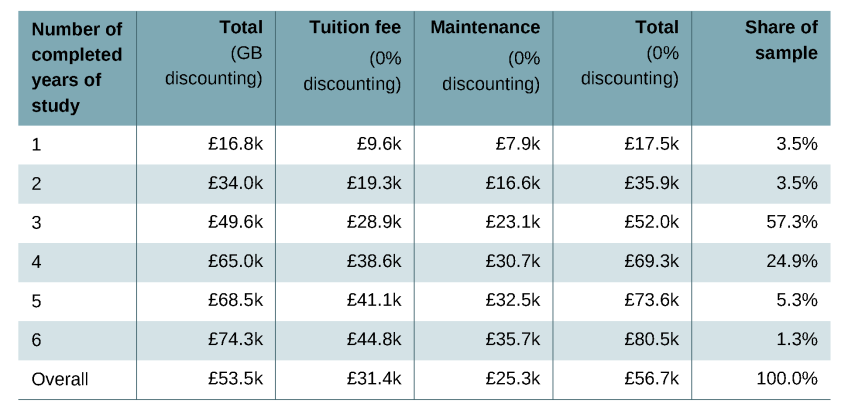

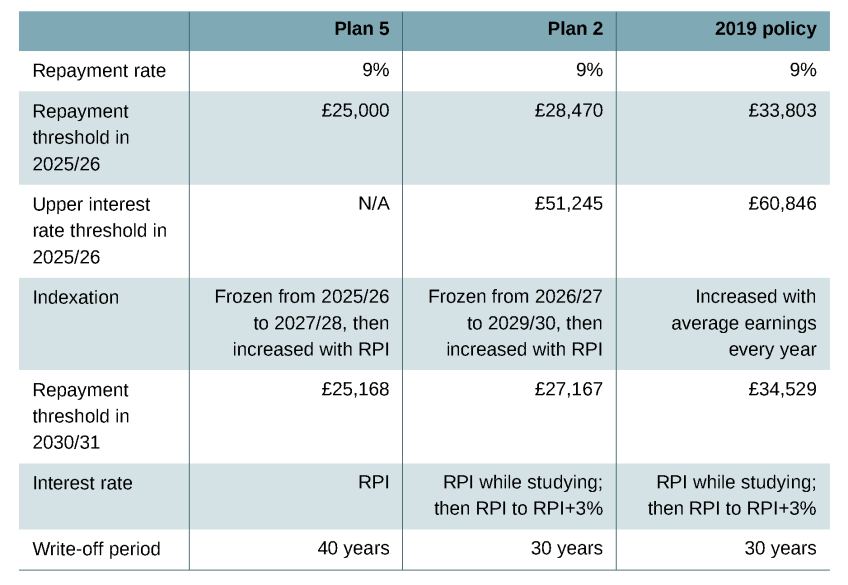

We estimate student loan borrowing, assuming students borrow the maximum they are entitled to for both tuition fees and living costs. The amount we estimate individual students borrow reflects how many years they study for, their socio-economic background and whether they study at a university in London. We estimate average borrowing of £52,000 in today’s prices amongst those who borrow for three years of study. This roughly matches the latest published DfE forecasts for average loan borrowing of £49,300 amongst full-time HE students who started courses in 2025/26 and took out three years of loans (Department for Education, 2025a). We model student loan repayments over the life cycle assuming that students face the ‘Plan 5’ student loan terms available to undergraduate students starting courses in 2025/26. In Chapter 6, we show the sensitivity of our results to instead applying the terms of ‘Plan 2’ student loans, which were available to those who started courses between 2012/13 and 2022/23. Further technical details on how we estimate student loan outlay and repayments are provided in Appendix B.

While the vast majority of up-front spending on HE is now in the form of government-backed loans, we also estimate government spending on grants to universities for teaching particular courses. This high-cost subject funding accounts for around 70% of recurrent funding that the Office for Students distributes.

Converting earnings streams into lifetime estimates

To compare costs and benefits stretching over many years in ‘present value’ terms, we convert earnings streams into ‘lifetime’ values by applying a discount rate. This captures that a given amount of additional income may have more value (to the government, and to many individuals) if it is received today compared with further in the future. This is beyond any impact of changes in the price level over time; we have already adjusted for inflation by expressing estimates in today’s prices (in ‘real terms’).

High discount rates can have a large effect on the expected lifetime returns to higher education, as attending HE is usually associated with costs in people’s early 20s (in the form of forgone earnings, and spending on the part of government) and the benefits of higher earnings may only emerge later in life. In what follows, we mostly use the Green Book’s recommended real discount rate of 3.5% for the first 30 years of earnings beyond age 18 and a real discount rate of 3.0% thereafter, to express lifetime returns in terms of earnings at age 18. This approach reflects the government’s official guidance on comparing social costs and benefits occurring over different periods on a consistent basis (HM Treasury, 2026), and supports comparisons with appraisals of other government policies and with earlier work. We also show the sensitivity of our main estimates to instead applying a 0% real discount rate: this adjusts earnings in future years for inflation but applies no further adjustment to reflect time preferences. We discuss the mathematical details of our discounting in Appendix B.

3.3 Estimating returns by prior attainment

The significant expansion of higher education in England over recent decades has been concentrated amongst students with lower prior attainment, making the returns for this group of particular policy interest (see Chapter 8 for evidence on the changing composition of HE entrants by prior attainment). We extend upon Britton et al. (2020) by estimating lifetime returns separately for students in the 2002 GCSE cohort with low prior attainment, defined as those in approximately the bottom 35% of our analysis sample by GCSE attainment.

We define this group based on GCSE scores, specifically as students who achieve at least the points equivalent of five C grades but no more than four Bs and four Cs (or equivalent) in their top eight GCSEs. Achieving four Bs and four Cs would place someone at roughly the 65th percentile of GCSE scores across the full 2002 GCSE cohort. We recognise that university entry is not determined by GCSE attainment alone. However, there are many routes through Level 3 study into HE, which are difficult to standardise and compare across individuals. Given the strong relationship between GCSE scores, Level 3 outcomes and university selectivity, we use GCSE attainment as our measure of prior attainment for this analysis. Just over half (53%) of those meeting our definition of low prior attainment in the 2002 GCSE cohort attended HE by age 21, indicating that this is a group with substantial overlap across the HE and non-HE choice. We discuss the composition of this group and present results in Section 8.1.

We also explore a narrower definition of low prior attainment, considering only the bottom fifth of our analysis sample, in Appendix I. This would include those at up to around the 55th percentile of GCSE scores across the whole GCSE cohort. Our preference is for the slightly broader definition of low prior attainment, as we believe the larger sample size makes our estimates more reliable while still capturing a group that can be considered ‘academically marginal’.

To estimate returns for these prior attainment groups, we restrict the sample to low-prior-attainment students and rerun the life-cycle simulation, regression equation (1) and the net returns calculation described above. We drop a small number of subject–institution-group cells with insufficient sample sizes within the subgroup.15

It is worth noting that we apply the same simulation parameters as in our main estimates – the copula parameters, employment probit parameters, and subject–age earnings profiles from the Labour Force Survey and HESA–HMRC data – to all prior attainment subgroups. We do not have sufficient information on prior attainment in the LFS to estimate separate earnings dynamics by subgroup. Differences in projected life-cycle earnings across prior attainment groups therefore arise from applying common growth profiles to the age-37 earnings distributions specific to each subgroup, which already differ substantially. This approach means that any genuine differences in earnings dynamics by prior attainment beyond age 37 will not be reflected in our simulations. To the extent that low-prior-attainment graduates and non-graduates experience slower earnings growth in their later careers than the average for their subject and sex, our estimates of their lifetime returns will be modestly upward-biased. In principle, the HESA–HMRC data could be used to estimate prior-attainment-specific earnings profiles up to age 44 for graduates, but sample sizes become too small for many subjects.

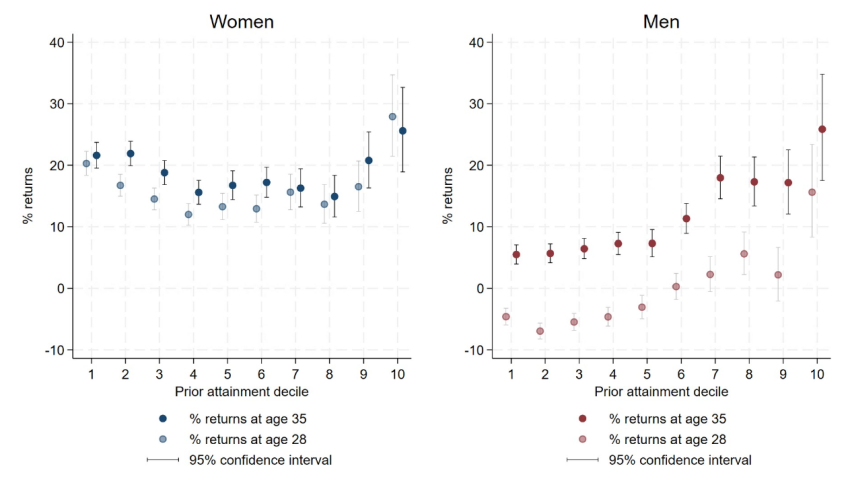

Returns by prior attainment decile

In Section 8.2, we complement our analysis of net individual lifetime returns by estimating gross earnings returns at a given age by prior attainment decile (within the selected sample). This relies only on earnings observed in the LEO data, rather than our simulations. We pool three cohorts – the 2002, 2003 and 2004 GCSE cohorts – to increase our sample size, allowing us to cut the sample by prior attainment more finely. We estimate the following regressions separately by sex and age:

(3.2)

where is the log of individual i’s gross earnings at age a, is a dummy for whether the individual attended HE by age 21, which we interact with a dummy for each decile of prior attainment, defined by scores in a student’s top eight GCSEs as above. These ten dummies () are also included as controls to account for different earnings levels by prior attainment decile amongst those who do not attend HE.

We use the set of background characteristics described in Section 3.2, , and add an additional dummy variable for over-18 entry to HE, since the number of years since graduating is a strong predictor of earnings even among people at the same age, and we may see different patterns of late entry across prior attainment deciles. Since we pool across three cohorts, we also include a cohort fixed effect, , to capture differences in earnings levels across cohorts. We are also able to include a small number of students who were excluded from our main estimation sample as low sample sizes by subject area are not a concern for this exercise.

Our coefficients of interest, , provide an estimate of the gross earnings return at age a, to attending HE, for students in prior attainment group p, controlling for background characteristics.

3.4 Estimating how returns have changed over time

Reweighting lifetime returns to reflect more recent cohorts

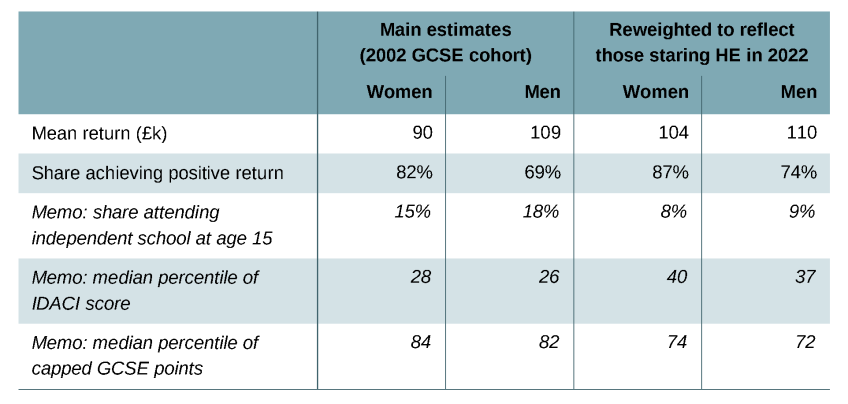

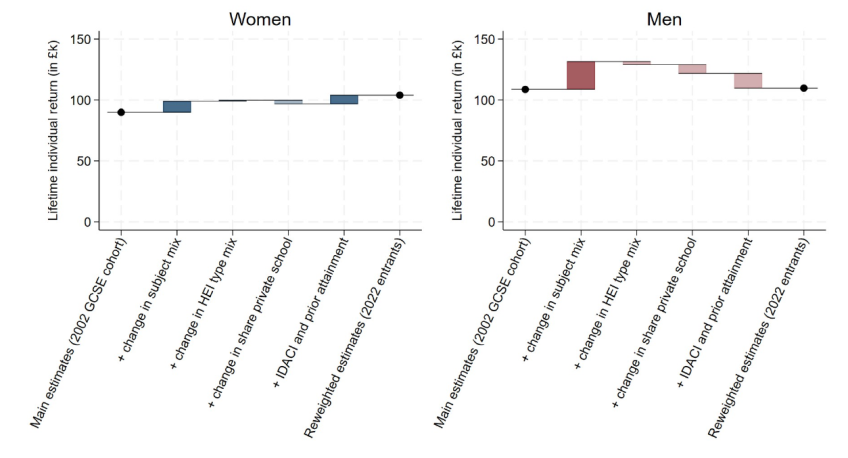

Our central lifetime returns estimates are based on the 2002 GCSE cohort, which attended HE in the mid 2000s. To provide suggestive evidence on what lifetime returns might look like for more recent entrants, in Section 9.2 we reweight our main estimates from Chapter 5 to reflect the characteristics of the 2022/23 HE entry cohort (the most recent for which we have HESA data). This accounts for changes in subject and institution mix and background characteristics, but makes no adjustment to average returns to reflect changes in the overall number of university entrants. We focus on net lifetime individual returns for this exercise.

To do this, we focus on those who started a full-time undergraduate course before age 21 for the first time in 2022/23 and who meet the same sample selection criteria applied to the HE group in our main analysis: a Key Stage 5 record and a minimum level of attainment in their top eight GCSEs.16 We then match each individual in this cohort to up to three individuals in the 2002 HE sample for whom we estimate lifetime returns. The match is exact on sex, subject area studied (using the second level of HESA’s Common Aggregation Hierarchy; hereafter CAH2), HE institution type, and whether the individual was attending a private school at age 15. Within these cells, we match them to their ‘nearest neighbours’ based on their GCSE attainment and a proxy for their socio-economic status. Each individual in the 2022/23 cohort is then assigned an estimated net lifetime return based on the average individual return amongst their three nearest neighbours.17 We aggregate to overall mean average returns and shares with positive returns by sex.

Those who entered HE in 2022/23 at age 18 would have sat their GCSEs in Summer 2020. As a result of disruption to assessments caused by the COVID-19 pandemic, these students were instead awarded centre-assessed grades, which were higher across the board than in a typical year. The increase was substantially larger in independent schools than in state schools: the share of GCSEs awarded grade 7 (formerly A) or above rose by 14.6 percentage points in independent schools between 2019 and 2021, compared with 7.5 percentage points in non-selective state-funded mainstream schools (Plaister, 2022). Standardising GCSE points within cohorts handles the level shift, while standardising separately by school type handles the differential inflation. The 19- and 20-year-old entrants in the 2022/23 cohort took their GCSEs in 2019 and 2018 respectively, before the pandemic: the standardisation within cohort also helps with this.

We emphasise that this is a particularly speculative exercise. It provides some suggestive evidence about how changes in the subject and institution mix and background characteristics of those entering HE over time may have affected average returns for later cohorts. However, by construction, we estimate returns for the 2022/23 cohort under the strong assumption that subject-, institution- and characteristic-specific lifetime returns are constant across the two cohorts. To the extent that labour market conditions, the value of a degree or other features of the graduate experience have changed in ways that affect returns within these cells, the reweighted estimates will not capture those changes. We discuss this and other limitations in Section 9.2, where we present the results.

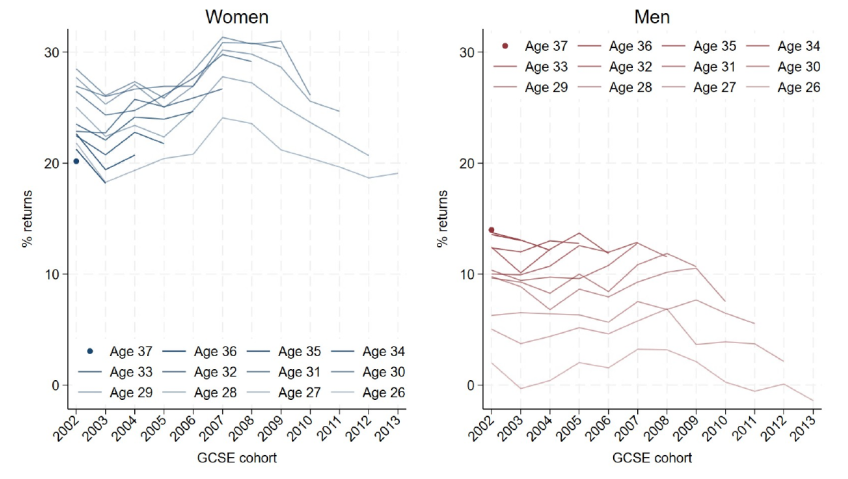

Estimating how returns at a given age have changed across cohorts

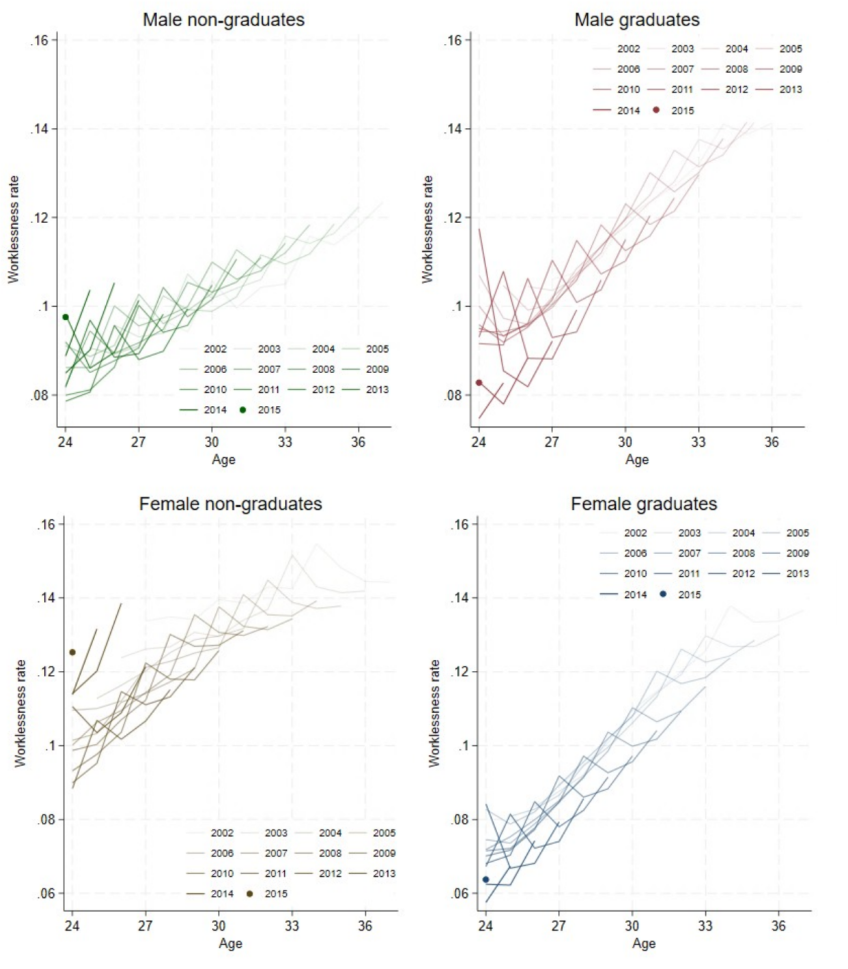

To provide more direct evidence on how returns have evolved across cohorts, we also estimate point-in-time gross earnings returns at a given age separately for a set of GCSE cohorts. Rather than projecting earnings and employment dynamics over the full life cycle, this approach exploits the fact that we are now able to observe earnings up to a specific age for multiple cohorts.

The number of cohorts we can observe at a given age varies. We observe earnings at age 26 for the largest number of cohorts: those from the 2002 to 2013 GCSE cohorts, who would have first entered HE at age 18 between academic years 2004/05 and 2015/16. At the other end, we observe earnings at age 37 only for the 2002 GCSE cohort, our main cohort of analysis. We present results across the full range of ages and cohorts we can observe.

For each age a between 26 and 37, and for each cohort in which we observe earnings at that age, we estimate

(3.3)

where is the log of individual i’s gross earnings at age a, is a dummy for whether the individual attended HE by age 21, and is the set of background characteristics described in Section 3.2 as well as a few additional controls described below. Our coefficient of interest, , is an estimate of the gross earnings return to an undergraduate degree at age a, controlling for background characteristics. We run this regression separately by age and sex. We also run a version where we include a dummy variable for each subject classification, in place of the single HE dummy, allowing us to look at returns by subject at a given age.

This regression differs from regression (3.1) in few ways. First, we include dummies for whether GCSE maths or English point scores are missing, which allows us to retain students with missing scores in our sample. We do not observe these scores for a substantial share of private school students in later cohorts and dropping private school students differentially across cohorts could introduce bias in estimates for later GCSE cohorts. Second, we include a dummy variable for over-18 entry, as in equation (3.2). Finally, we continue to drop students from our sample who attended HE later than age 21 but now retain those who attended HE for the first time after age 26. This is the latest age at which we can observe HE entry (or non-entry) for the 2013 GCSE cohort, and so allows us to apply a consistent sample definition across all of our cohorts. This effectively treats late entry into HE as a possible trajectory for students who did not enter HE before age 21.

4. Lifetime earnings

In order to contextualise our results, this chapter describes the actual gross earnings of our HE and non-HE groups in the 2002 GCSE cohort, up to age 37, and our simulated lifetime earnings profiles, separately by gender. We convert earnings data to 2025/26 CPI-real prices and report all our estimates in these terms (unless otherwise specified). It is important to keep in mind that none of the data presented in this section reflect the returns to higher education. The earnings shown are raw earnings, i.e. there is no attempt to adjust for differences in the background characteristics between those who do and do not go to higher education; we turn to this in Chapter 5. However, we do restrict our attention to individuals who could plausibly have attended HE at or soon after age 18 based on their prior attainment.

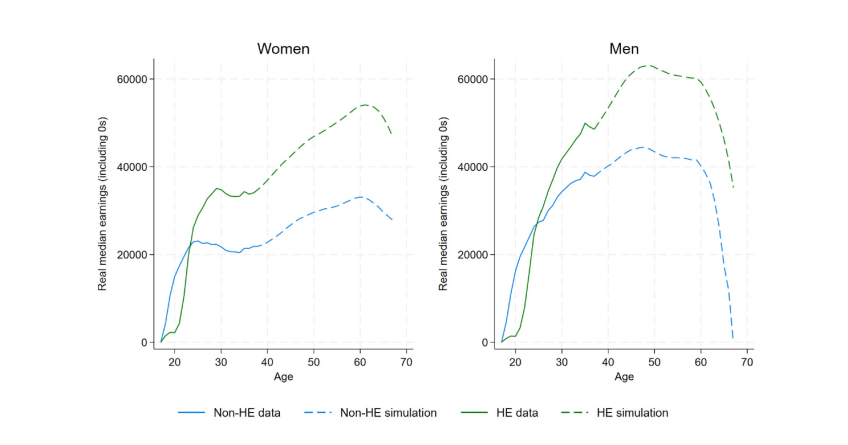

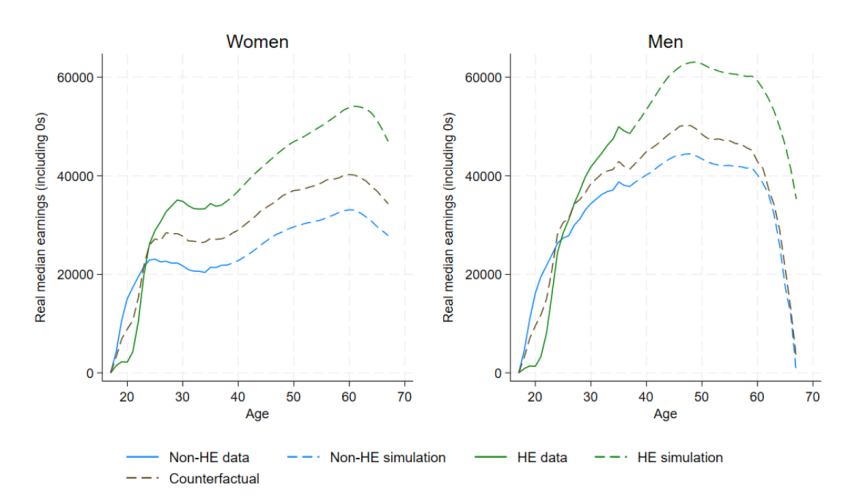

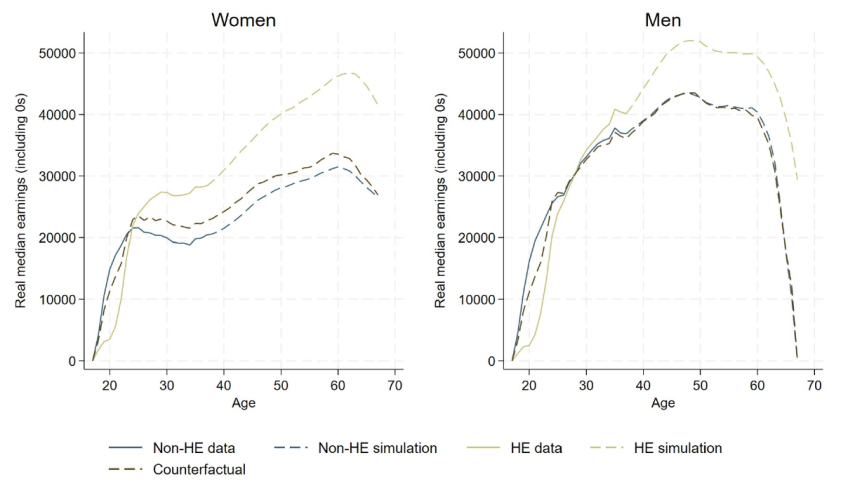

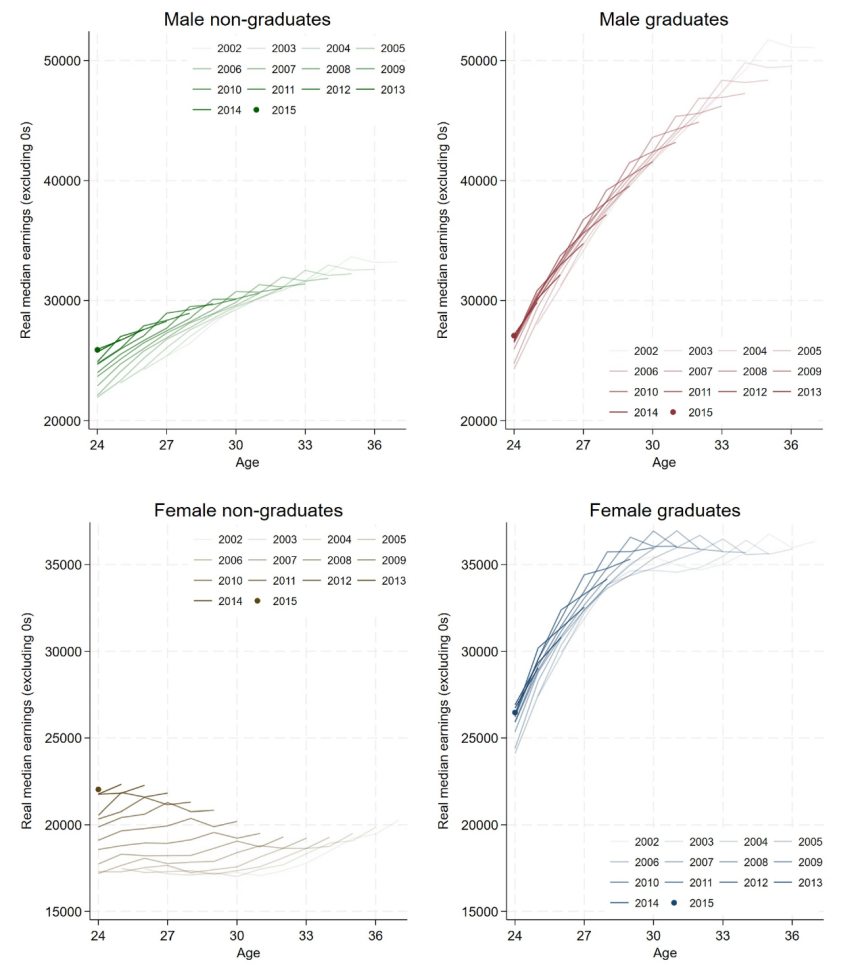

We start by looking at simple plots of median earnings by age. Figure 4.1 shows median pre-tax earnings among graduates and non-graduates, separately by gender. Up to age 37, the earnings are the actual observed earnings for the 2002 GCSE cohort. Beyond age 37, we use the simulated earnings profiles for this cohort, shown as dashed lines.

Figure 4.1. Median actual and simulated gross earnings by age (2002 GCSE cohort)

Note: Gross annual earnings in 2025/26 CPI prices. Includes zero earnings. Sample selected as discussed in Section 2.1, including minimum GCSE attainment and a Key Stage 5 record. Data before age 27 exclude self-employment earnings. Earnings are uprated to reflect economy-wide real earnings growth between 2004/05 and 2023/24, and by 1.8% per year for every age after 37.

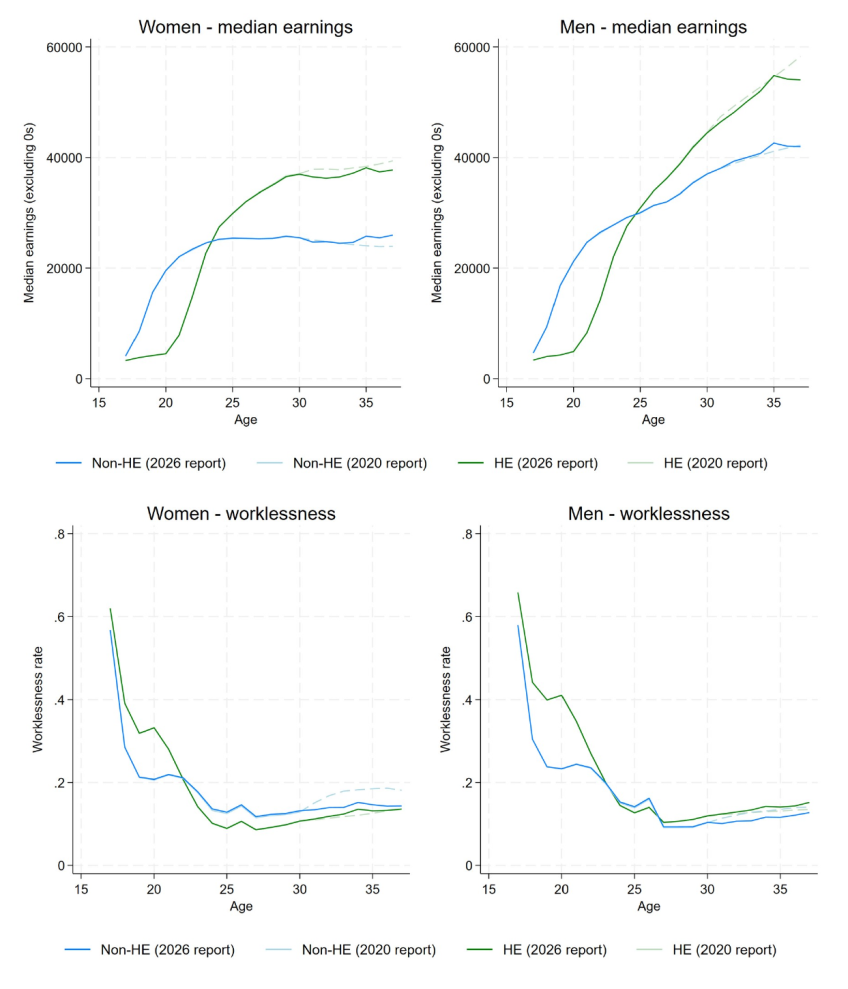

For both women and men, the median earnings of those who attend HE start below the earnings of those without HE, reflecting that people typically forgo earnings while they study, working fewer hours during their early 20s. The earnings of our HE group saw much stronger growth than those of their non-HE counterparts in their late 20s. This is particularly true for women, as median real earnings amongst female non-graduates in this cohort actually declined slightly after the age of 29. At age 30, median earnings of women HE graduates were around £35,000 (in today’s prices), around 60% higher than the median amongst non-graduate women (£22,000). Median earnings amongst male graduates at age 30 (£42,000 in today’s prices) were over 20% higher than those amongst male non-graduates (£34,000). These patterns match those in Britton et al. (2020), as would be expected given that this report uses the same data up to age 30.

With additional years of tax data, we are now able to describe how the earnings of the same set of graduates actually evolved over the subsequent seven years. Median earnings of male graduates continued to grow strongly between the ages of 30 and 35, by around 20% in real terms, and this growth outstripped the growth for non-HE men (13%). This was in stark contrast to women, who saw very little growth in median real earnings over the same period: median earnings amongst both graduate and non-graduate women were around 1% lower in real terms at age 35 than at age 30. These estimates include individuals with zero earnings in a given year so that year-on-year changes combine changes in real-terms hourly pay, in the number of hours worked and in employment rates. The real-terms decline in annual earnings for women between ages 30 and 35 is more likely to reflect reductions in hours worked over this period, rather than a reduction in hourly pay, although we cannot directly test this using tax data as we do not observe hours worked.

Also of note from Figure 4.1 is the year-on-year decline in real earnings at age 36 which was seen across all groups. This corresponds to the 2022/23 tax year and the ‘cost-of-living’ crisis, a period in which nominal earnings growth across the economy did not keep pace with high CPI inflation.18 There was some bounce-back for female earnings at age 37 (in the 2023/24 tax year) but a further slight real-terms decline in median male earnings in the same year.

Earnings gaps between graduate and non-graduate women were similar at age 37 to what they had been at age 30, and we expect this gap to remain fairly stable at between 50% and 60% for most of their later careers. For men, we expect slightly faster real growth in HE than non-HE earnings up to their late 40s, and then slightly slower declines through the next decade. This means that our predicted HE/non-HE raw earnings gap for men increases steadily from 28% at age 37 to around 45% by age 50, after which it stabilises.

Towards the end of working life, median earnings decline for all groups as people start to reduce their working hours, and more individuals drop out of the labour market altogether as they approach retirement.

4.1 Earnings by subject

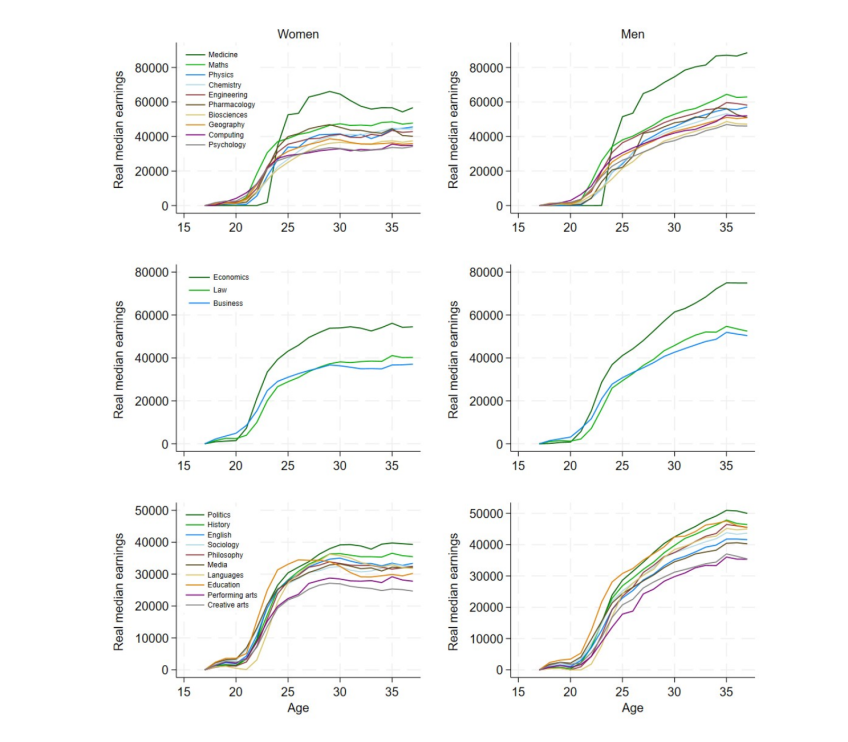

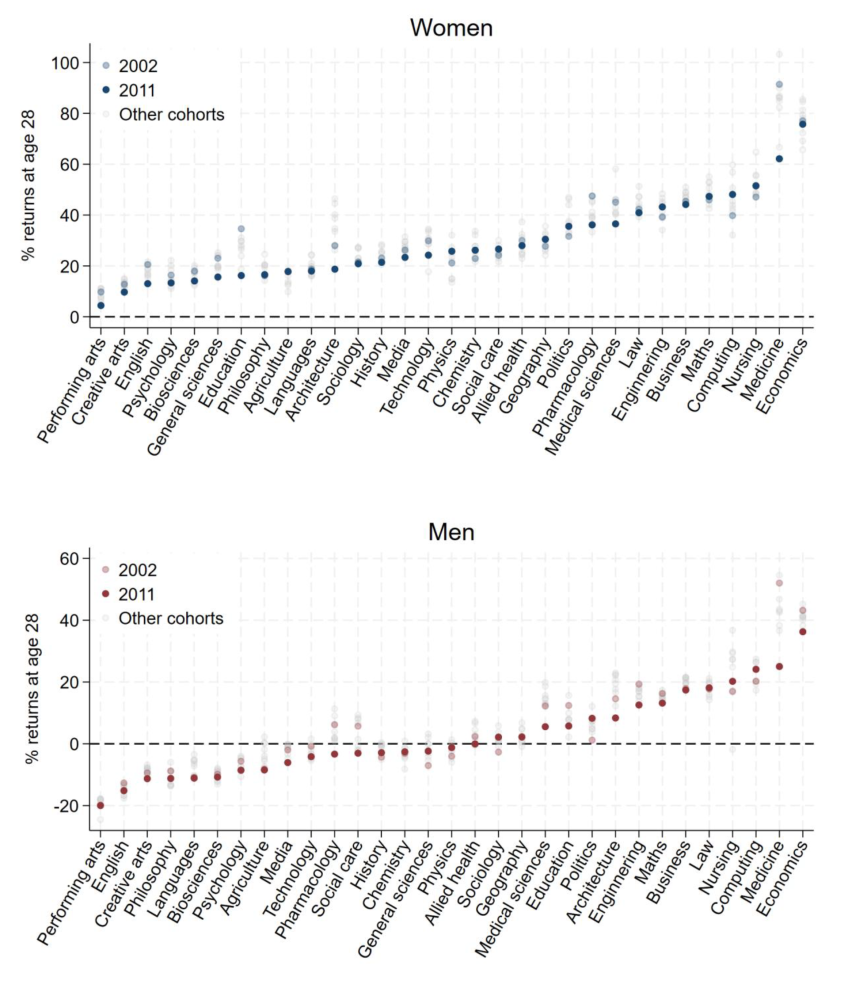

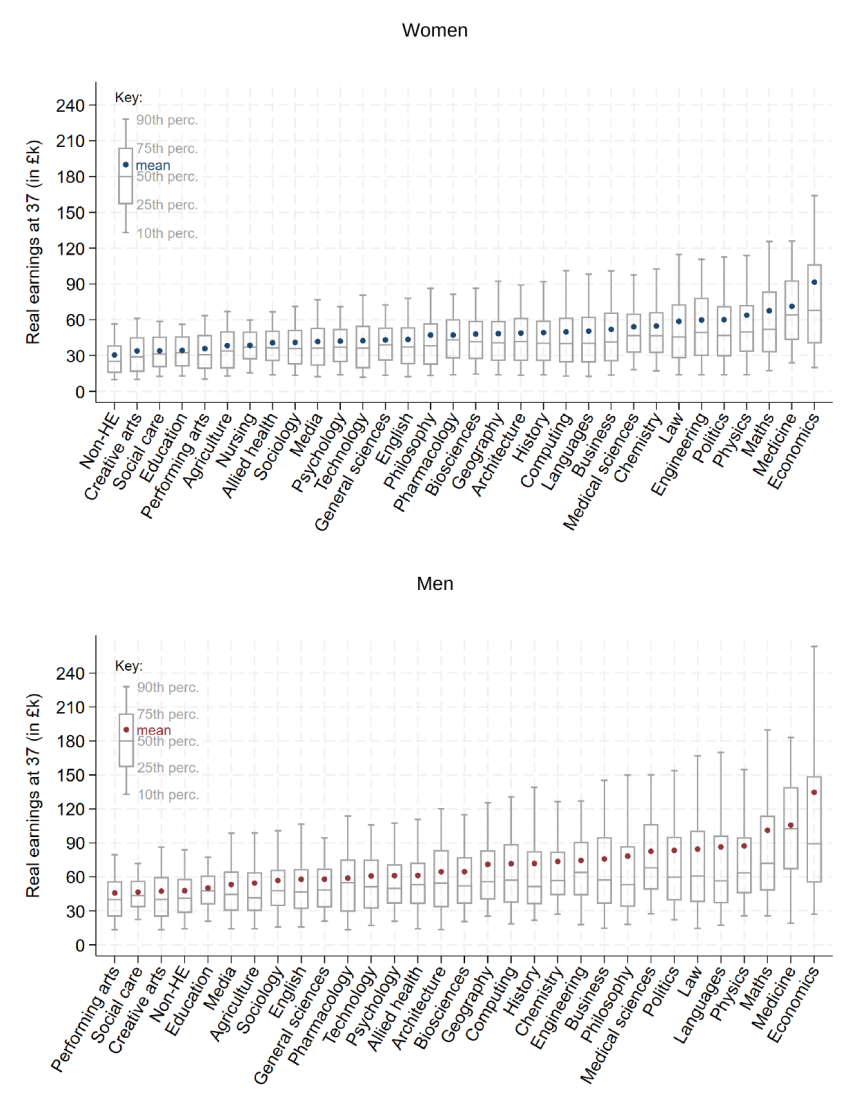

Figure 4.2 shows the trajectory of median earnings up to age 37 for the HE group, split by subject, for women and for men. In general, median earnings of female and male graduates in each subject were very similar at age 25, although across all subjects male graduates saw faster real-terms growth in median earnings after that age. After age 25, medicine and economics were the highest-earning subjects, while creative and performing arts were the lowest-earning.

Figure 4.2. Median actual gross earnings by age (2002 GCSE cohort) including zeros: selected subjects

Note: Subjects are grouped into STEM subjects (science, technology, engineering and maths), LEM subjects (law, economics and management) and other subjects. Includes zero earnings. Sample selected as discussed in Section 2.1. Data before age 27 excludes self-employment earnings (although we expect this to make little difference to the plot as self-employment earnings for later cohorts are low before age 27).

Those who studied medicine had near-zero median earnings up to age 23 (reflecting longer courses), but by age 25 they had the highest median earnings of graduates of any subject amongst both men and women. Medicine remained the subject with the highest median earnings for both male and female graduates, although it was almost overtaken by economics for women at ages 35 and 36. This was in part due to a decline in real median earnings of female medicine graduates after age 29, likely due to declines in working hours (male medics continued to see strong growth in median earnings through their 30s).

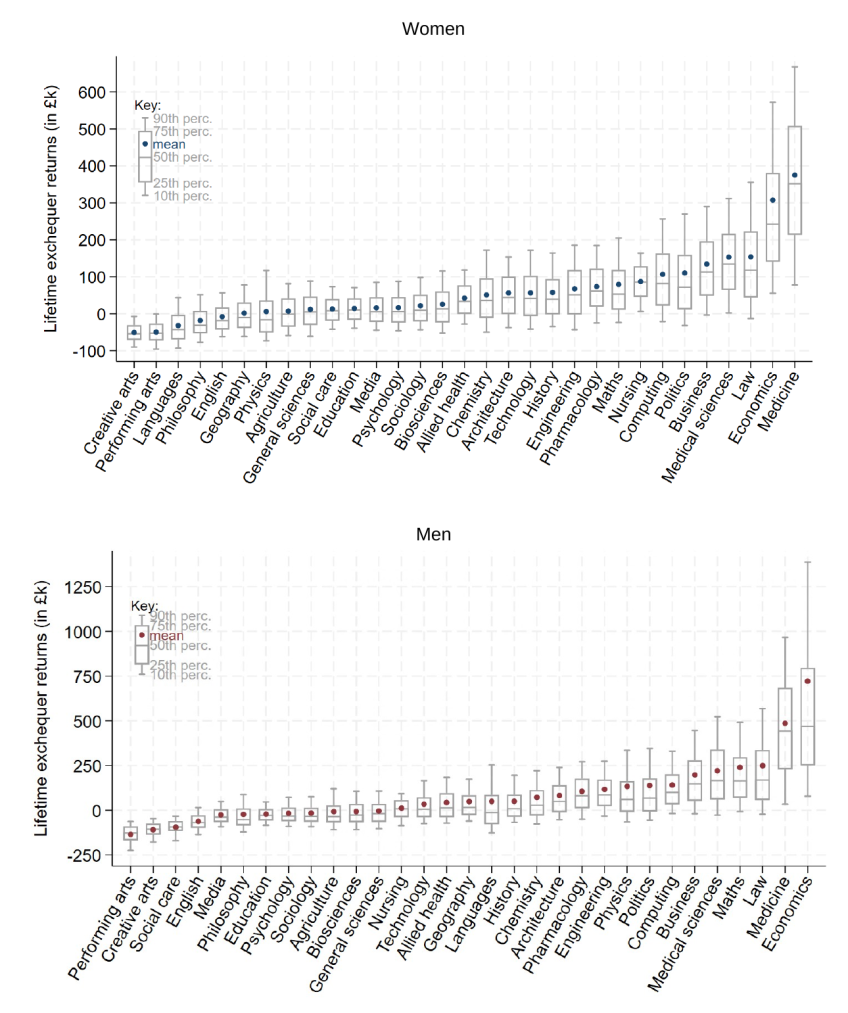

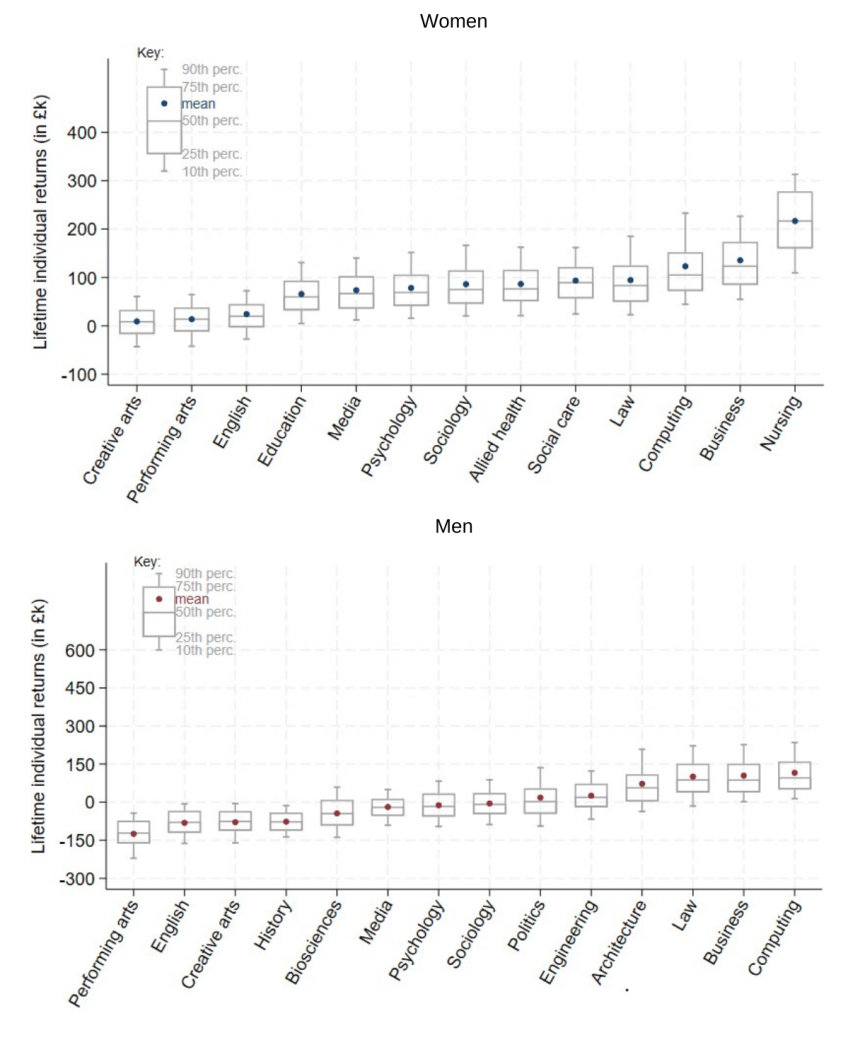

At age 37, there were large differences in median gross annual earnings between graduates of different subjects. However, there was also substantial variation in earnings amongst graduates of the same subject, which we show in Appendix C. Most notably, the distribution of gross earnings for economics graduates is extremely wide: conditional on having positive earnings, 10% of female economists earn at least £164,000 by age 37 (compared with a median of £68,000), while 10% of male economists with positive earnings earn at least £263,000 (compared with a male economist median of £90,000). This variation is not restricted to the higher-earnings subjects, however; 10% of female creative arts graduates earned at least £61,000, while 10% of male creative artists earned at least £86,000.19

5. Earnings returns

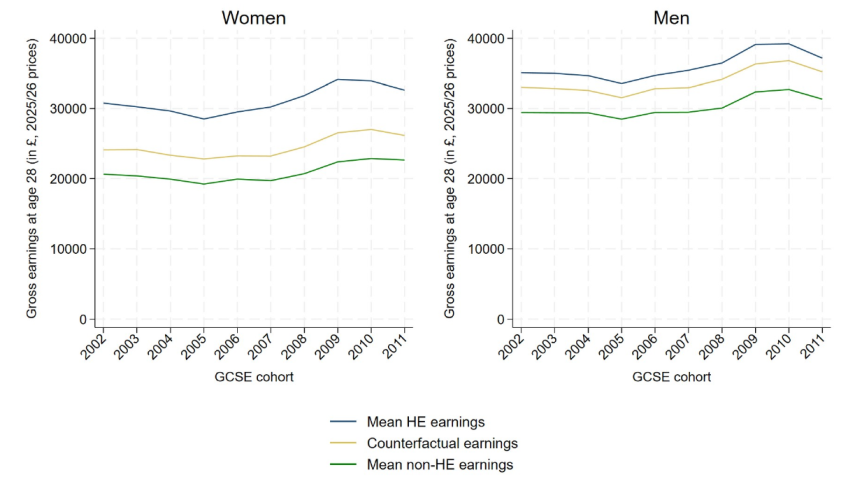

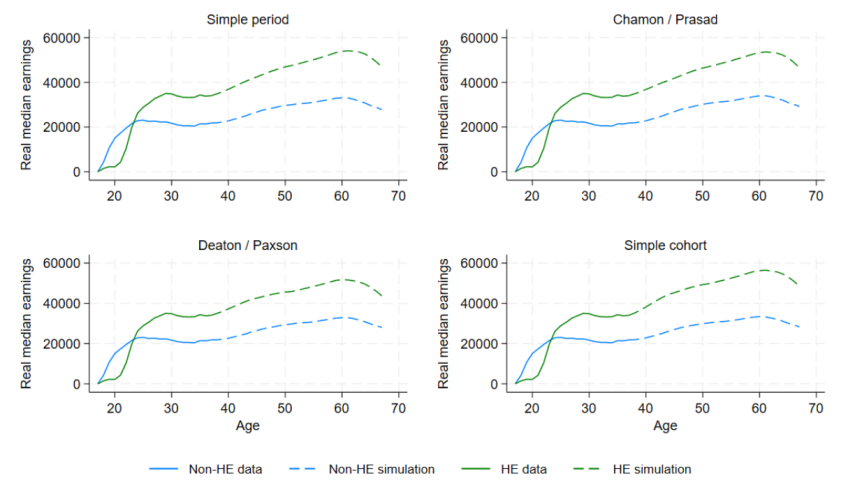

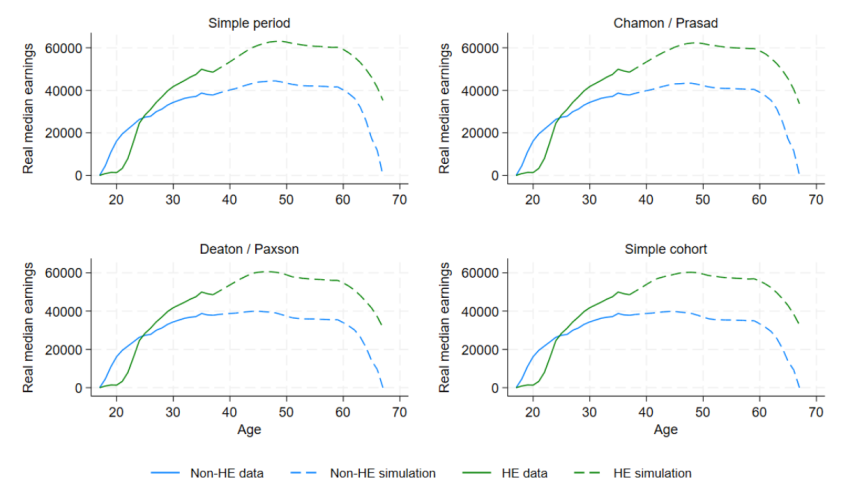

We now consider the returns to higher education. To do this, we estimate the difference between the gross earnings of those who attended HE and the counterfactual earnings those same individuals may have had if they had not started an undergraduate degree by age 21. As the latter cannot be observed, we predict these based on the regression model discussed in Section 3.2, drawing upon the rich background and prior attainment information from school records. As shown in Figure 5.1, we estimate that our HE group would have had higher counterfactual earnings than our non-HE group, even if they had not in fact attended university: the difference between the non-HE and counterfactual lines reflects the earnings difference attributable to selection into attending university, and the difference between the counterfactual and HE lines represents our estimated gross earnings return at each age.

Figure 5.1. Median actual, simulated and counterfactual gross earnings for our HE and non-HE groups (2002 GCSE cohort) by age

Note: ‘HE’ includes those who started a full-time undergraduate degree before the age of 21. Gross annual earnings in 2025/26 CPI prices. Counterfactual earnings estimated as described in Section 3.2. Includes zero earnings. Sample selected as discussed in Section 2.1, including minimum GCSE attainment and a Key Stage 5 record. Data before age 27 exclude self-employment earnings. Earnings are uprated to reflect economy-wide real earnings growth between 2004/05 and 2023/24, and by 1.8% per year for every age after 37.

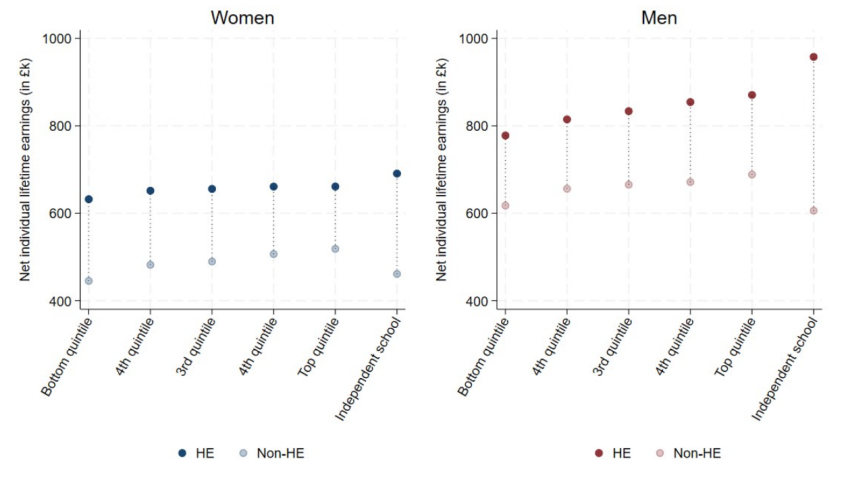

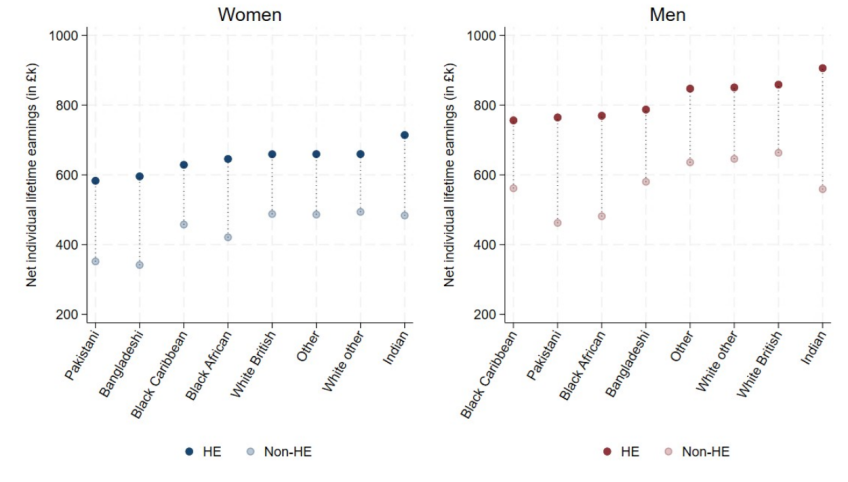

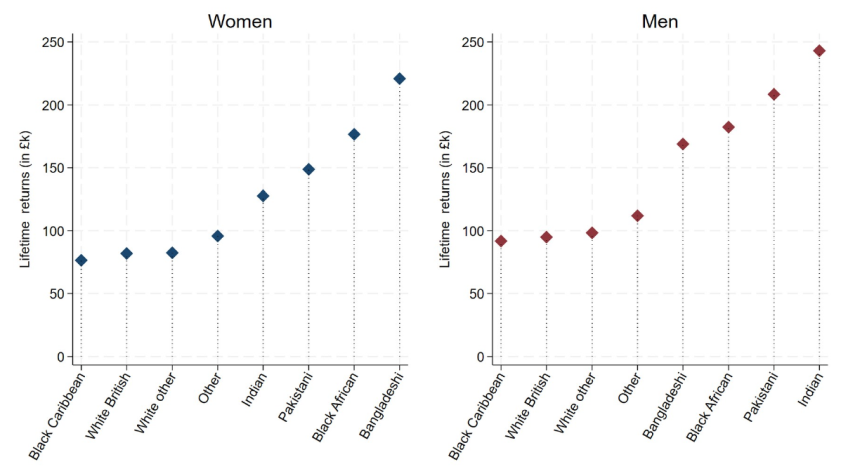

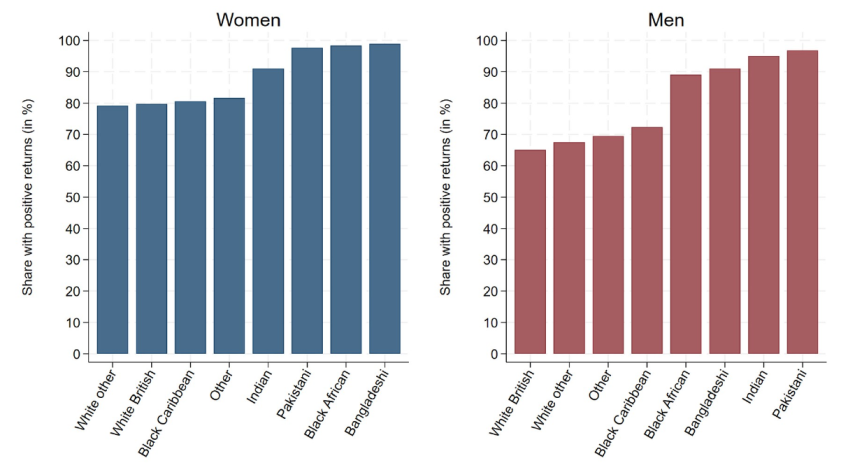

These estimates of gross earnings returns reflect earnings simulations for the 2002 GCSE cohort. We then apply today’s tuition fee, student loan and tax policies to these returns, to approximate how the financial return to higher education – and the cost of a degree – would be split between individuals and the exchequer under current government policy. We first look at average returns to attending HE – from the perspective of individuals and the exchequer – before disaggregating these by subject and institution group. We also disaggregate returns by socio-economic status and ethnic group in Appendix J.

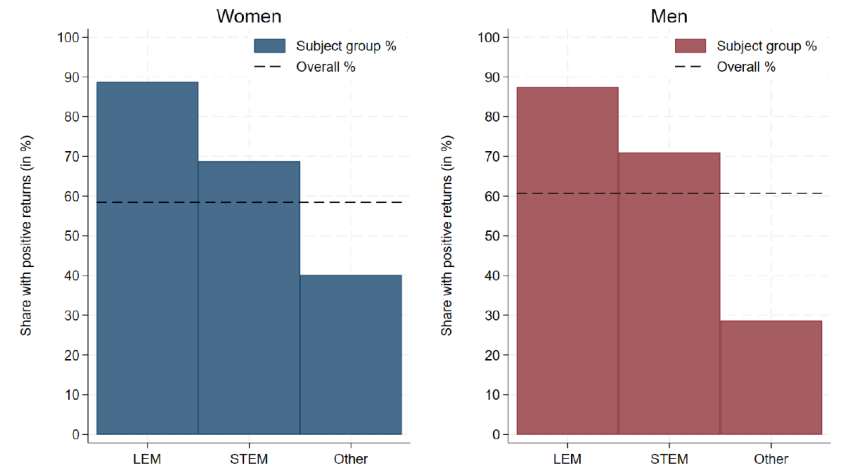

5.1 Average net lifetime returns

From the point of view of the student, we estimate that the overall average discounted present value of enrolling in an undergraduate degree is around £90,000 for women and £109,000 for men. In percentage terms, this represents a gain in average net lifetime earnings of around 16% for women and 15% for men.20 As discussed in Section 7, these returns are around a third lower in real terms than those estimated in earlier work.

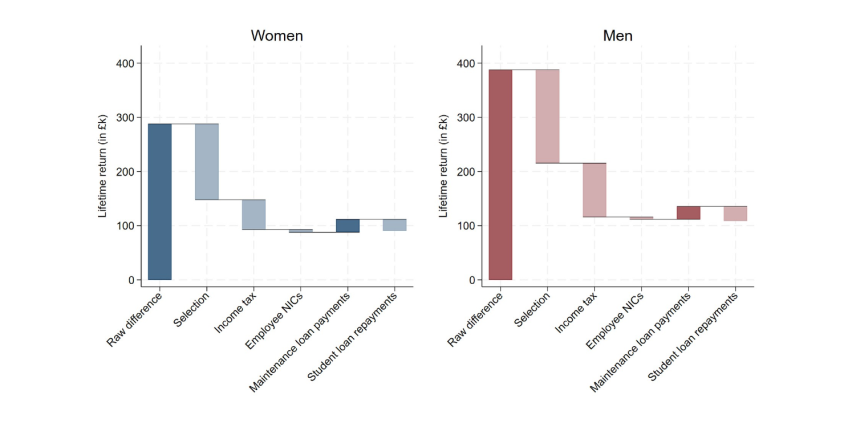

Figure 5.2 shows how we arrive at these estimates of net individual lifetime returns and Table 5.1 summarises the key numbers. The net individual financial return to HE is the sum of the increase (or decrease) in earnings associated with attending university at each age, minus the increase (or decrease) in taxes paid at each age, plus the value of maintenance loans received and minus the value of any student loan repayments made.21

Figure 5.2. Decomposition of lifetime individual returns to higher education

Note: All figures are shown in 2025/26 CPI prices, are discounted using Green Book discounting and are mean averages across our HE sample. The first bar shows the raw difference in gross earnings between those who did and did not attend HE. The second bar shows how much of this difference in earnings can be explained by differences in prior attainment and background characteristics. We then account for differences in income tax and employee National Insurance contributions (NICs) as a result of remaining differences in pre-tax earnings. The penultimate bar adds the maintenance loan payments received by students while studying and the last bar takes into account estimated lifetime student loan repayments. Darker bars indicate additions and lighter bars reductions.

Table 5.1. Average net lifetime earnings differences between graduates and non-graduates and net individual returns

Note: All figures are mean averages, shown in 2025/26 CPI prices and discounted using Green Book discounting. Percentages reflect proportional increase relative to non-HE estimates in each case.

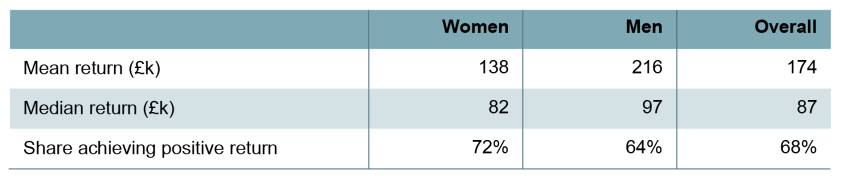

For women, the predicted difference in discounted pre-tax lifetime earnings between those who go to university and those who do not is around £288,000. We estimate that approximately half of that difference can be explained by the different observable characteristics of women who attended HE (we refer to this as ‘selection’ in the figure). That is, we estimate that women who go to university earn around £148,000 more pre-tax than if they had not gone to university; this is the gross lifetime earnings return. Accounting for additional income tax and payments of employee National Insurance on these higher earnings reduces the net individual returns by roughly another £60,000. Including the student loan system slightly increases the return by around £2,000, as we estimate women repay slightly less, on average, in overall student loan repayments (£22,000) than they receive in maintenance loans (£24,000). This results in a final estimated net lifetime return of £90,000 for women.

For men, the predicted difference in raw pre-tax earnings for those who do and do not attend university is greater than for women, at around £388,000. However, the difference that can be explained by observable characteristics is also somewhat bigger, taking the gross return to around £215,000 on average for men. Since much of the additional income later in life will be subject to the higher rate of income tax, the difference in income tax reduces the net return by £99,000 for men; the difference in employee National Insurance payments is much smaller (£4,000). We estimate that men will make student loan repayments of around £27,000 on average, exceeding in present-value terms the average maintenance loans they receive (£24,000), leaving a total average net lifetime return of £109,000 for men.22

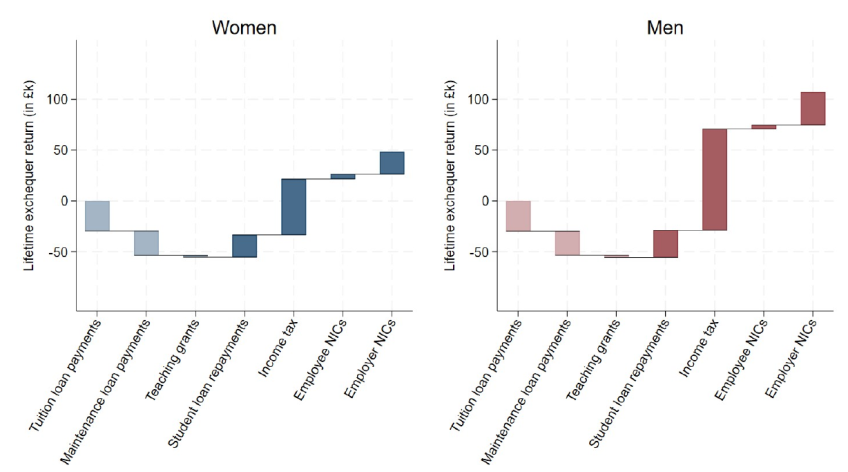

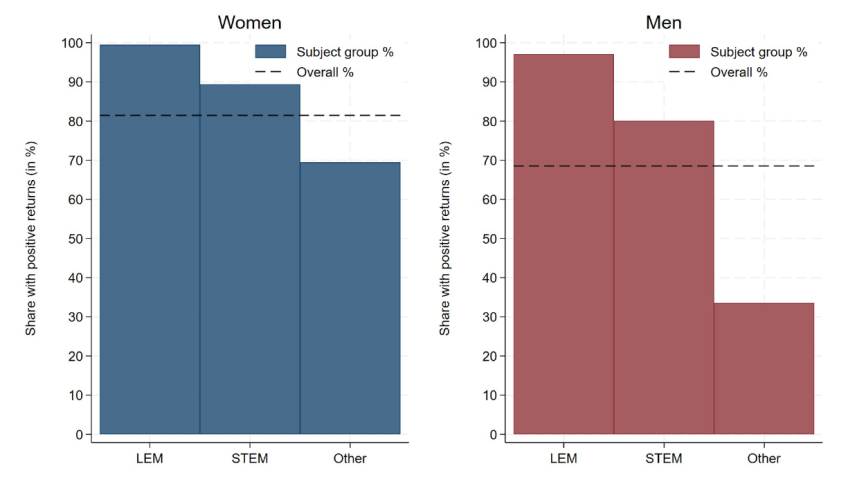

We now turn to estimating the equivalent average returns to the exchequer, i.e. from the point of view of the taxpayer. These consist of the increase in lifetime tax and National Insurance receipts (including both employee and employer NICs), minus any up-front spending on teaching grants and initial outlay on tuition fee and maintenance loans that is not offset by future student loan repayments.23 We estimate there are average lifetime exchequer returns of £48,000 for women and £107,000 for men – which should be interpreted as the average gain to the exchequer from people enrolling in the courses that they did in fact enrol in, compared with not going to university at all.

Figure 5.3 shows the different components of exchequer outlays and returns for women and men. Financing an undergraduate degree costs the exchequer around £55,000 for both women and men in tuition and maintenance loan payments and teaching grants.24 Women will only pay back around 40% of that total up-front cost in student loan repayments, but the higher income tax payments of graduate women more than offset the remaining cost to the exchequer represented by the 60% of initial outlay which is not recovered through loan repayments.25 Adding the additional employee and employer NICs – around £5,000 and £22,000 respectively – leads to the overall figure for the average net exchequer return to HE for women of £48,000 per student.

Figure 5.3. Decomposition of lifetime exchequer returns to higher education

Note: All figures are shown in 2025/26 CPI prices, are discounted using Green Book discounting and are mean averages across our HE sample. The first two bars show the net present value of tuition fee and maintenance loan outlay. The next bar shows the net present value of teaching grants for high-cost subjects. Subsequent bars then show the net present value of government receipts in terms of student loan repayments and higher income tax and National Insurance payments as a result of differences in pre-tax earnings that cannot be explained by differences in prior attainment and background characteristics. Darker bars indicate additions and lighter bars reductions.

Financing a degree costs essentially the same for men as for women but, due to their higher average earnings, men are expected to pay back a larger fraction (around 48%) of that cost in present-value terms through student loan repayments. The increase in income tax payments is the most important part of the exchequer return for men; along with additional receipts of employee and particularly employer NICs, tax receipts increase by around £136,000 per student, resulting in an overall average net exchequer return to HE for men of £107,000 per student.

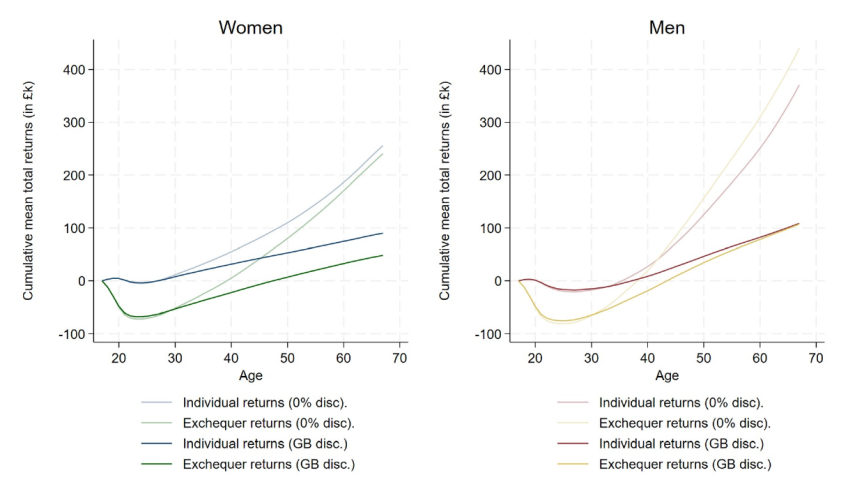

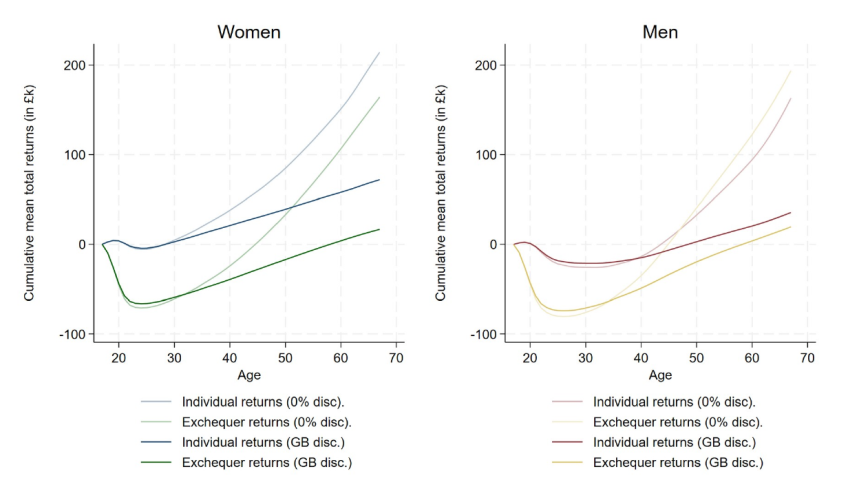

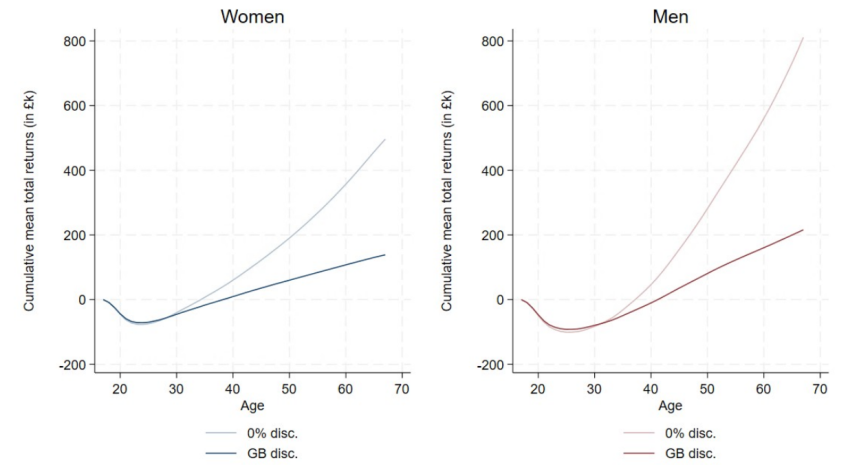

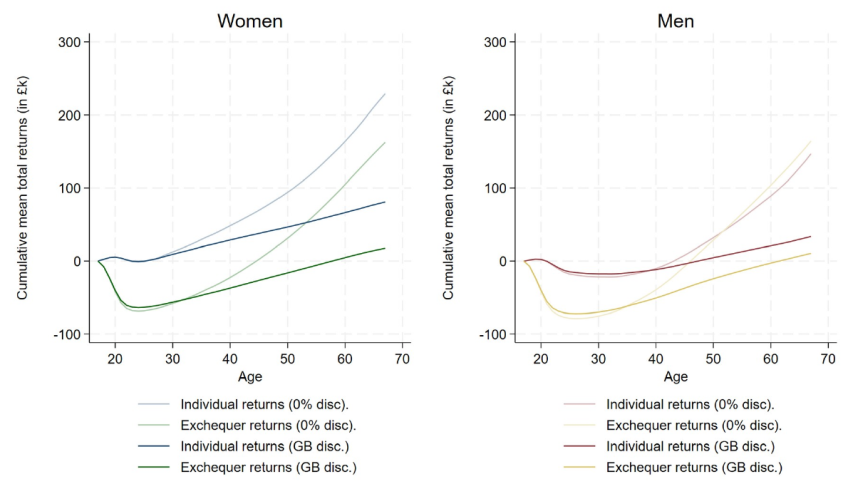

Figure 5.4 shows cumulative average returns by age – both for individuals and for the exchequer. The figures at age 67, with Green Book discounting applied (the darker lines), correspond to the average lifetime estimates discussed in the text above.

Figure 5.4. Mean cumulative individual and exchequer returns to higher education by age

Note: All figures are shown in 2025/26 CPI prices and are discounted using either Green Book (GB) discounting, as in our main estimates, or with a 0% real discount rate. Returns at a given age are discounted cumulative returns to that age.

Several aspects of the graphs are notable. First, while the cumulative discounted returns to women from attending university are positive on average from age 27, for men this is only true from age 38. This mainly reflects that men experience lower earnings returns in their 20s than women (who have worse counterfactual, non-HE earnings). Both individual and exchequer returns for men grow more strongly than for women later in life and exceed returns for women by age 55.

Second, the size of the estimated cumulative returns figures is dramatically affected by the choice of discount rate. With 0% real discounting, net individual lifetime returns would be £256,000 for women and £371,000 for men (compared with £90,000 and £109,000 with Green Book discounting).26 Men’s projected lifetime returns in cash terms exceed those of women, but the difference is much larger with a lower discount rate.