Downloads

Download report PDF

PDF | 958.65 KB

Executive summary

This is our seventh annual report on education spending in England funded by the Nuffield Foundation. It seeks to provide a clear and consistent comparison of the level and changes in spending per student across different stages of education. Our dedicated website (https://ifs.org.uk/education-spending) further provides easy access to our latest analysis, figures and methodology. All figures quoted are in 2024–25 prices and relate to England unless otherwise stated.

Total spending

- In 2023–24, total public spending on education in the UK stood at £116 billion (including the net cost of issuing student loans and in 2024–25 prices). This represents an 11% or nearly £15 billion fall since 2010–11 and represents the level in real terms as in 2006–07. This drop mostly reflects a shift in the cost of higher education from the taxpayer to graduates over time.

- Education spending has also fallen as a share of national income, from about 5.6% of national income in 2010–11 down to about 4.1% in 2023–24. This equals recent historic lows seen in the late 1990s, late 1980s and mid-1960s. There has been no long-run increase in the share of national income devoted to public spending on education spending, despite large rises in education participation over the long run.

Early years

- Total spending on the free entitlement to early years education and childcare nearly quadrupled between 2001–02 and 2023–24, when it reached £4.1 billion in today’s prices. This was largely driven by expansions to the free entitlement. A new expanded entitlement for children aged under 3 is expected to lead to a further doubling of spending to £8.5 billion by 2027–28. This represents a major increase in resources at a time when other stages of education and public services have been squeezed.

- The rollout of the ‘expanded’ entitlement is the biggest ever expansion to the free entitlement. From September 2025, this will provide children in working families with 30 hours of early education and childcare per week between ages 9 months to 36 months.

- Funding rates for new and existing entitlements have seen large increases in 2024–25 to incentivise growth in provision, particularly for younger children: the average hourly rate for under-2s is £11.22, almost twice existing market prices. By comparison, hourly funding for existing entitlements for 3- and 4-year-olds are much closer to market prices. These higher funding rates for younger children better reflect differences in the costs of providing childcare to children of different ages than do current market prices (for instance, younger children require stricter staff:child ratios).

- Between 2016–17 and 2022–23 providers’ costs grew by 25% (mostly due to staffing but also energy, rent and food), which is about twice as quickly as the growth in funding rates for 3- and 4-year-olds (12%). Once we account for rises in providers’ costs, the average funding rate for 3- and 4-year-olds is worth about 15% less in 2024–25 than in 2012–13.

- Local authorities are responsible for distributing funding to providers and take different approaches to targeting spending. Just over a quarter (27%) of local authorities dedicate less than 5% of resources to targeted funding streams, which are intended to support low-income children and children with higher needs and to provide quality and flexibility of provision. Almost another quarter (23%) of areas allocate more than 10% to targeted spending, with these tending to be more urban and more deprived.

- Changes to employers’ national insurance contributions (NICs) and minimum wage rises announced at the Autumn Budget 2024 will particularly affect lower-paid workers. These changes create both winners and losers: a small childcare setting with six or fewer employees on median earnings (£33,000) would benefit from the changes if they are eligible for the more generous employment allowance; providers employing more staff would lose out – and the bigger the employer, the more so.

- The plan to deliver an additional 3,000 school-based nurseries launched in October. Once fully rolled out, this will represent around 30% of the existing number of school-based providers and is intended to drive up the quality of provision. While this may create additional capacity over the longer term, it is unlikely to substantially ease supply constraints by September 2025, the period when demand for new places will be most acute. There may also be a geographical mismatch between spare capacity in primary schools and demand for new early years provision.

Schools

- Between 2019–20 and this financial year (2024–25), total school spending in England grew by about £8 billion. This has led to 11% real-terms growth in school spending per pupil. This reverses past cuts and takes spending per pupil back to 2010 levels.

- In the Autumn Budget 2024, the government allocated a further £2.3 billion to the schools budget in 2025–26, with about £1 billion devoted to high needs. This allows for a further 1.6% real-terms growth in school spending per pupil.

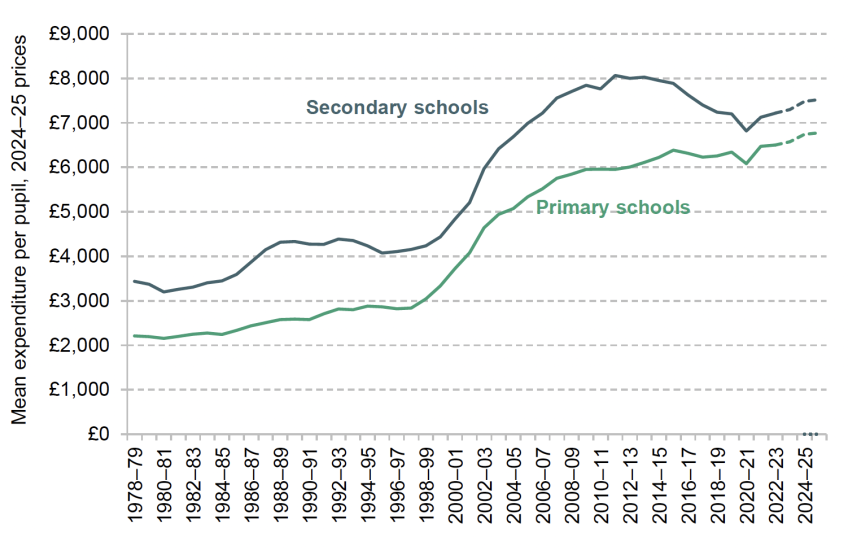

- Secondary school spending per pupil in England in 2024–25 is due to be about £7,400, which is 11% higher than in primary schools (£6,700). This is down from a difference of about 30% in the 2000s and over 50% during the early 1990s.

- Over half of the increase in school funding between 2019 and 2024 can be explained by growth in high needs funding. This reflects the rapid growth in the number of pupils identified as having special educational needs. After accounting for planned spending on high needs, we estimate that mainstream school funding per pupil grew by 5% in real terms between 2019 and 2024, rather than the 11% total increase.

- We estimate that mainstream school funding per pupil will grow by 2.8% in cash terms in 2025–26. We also estimate that school costs will grow by 3.6% in 2025–26 if the pay review body follows the government’s recommendation of a 2.8% pay award for 2025. In this case, schools might struggle to cover their costs without making savings.

- Looking to the 2025 spending review, pupil numbers are expected to fall by 2% between 2025 and 2027. If the government chose to freeze school spending per pupil in real terms, it could make savings of £1.2 billion by 2027. However, the government also projects that high needs spending will grow by £2.3 billion between now and 2027–28. This severely reduces the chances of making savings in the schools budget.

- School capital spending is due to rise from £6.3 billion in 2023–24 to £6.5 billion in 2025–26. This leaves spending within the same range it has been for the last decade and about the same level as in the mid-2000s. From within this spending total, the government will need to cover the costs of the delayed school rebuilding programme, the costs of addressing reinforced autoclaved aerated concrete (RAAC) in schools and other overdue school repair costs.

Further education and skills

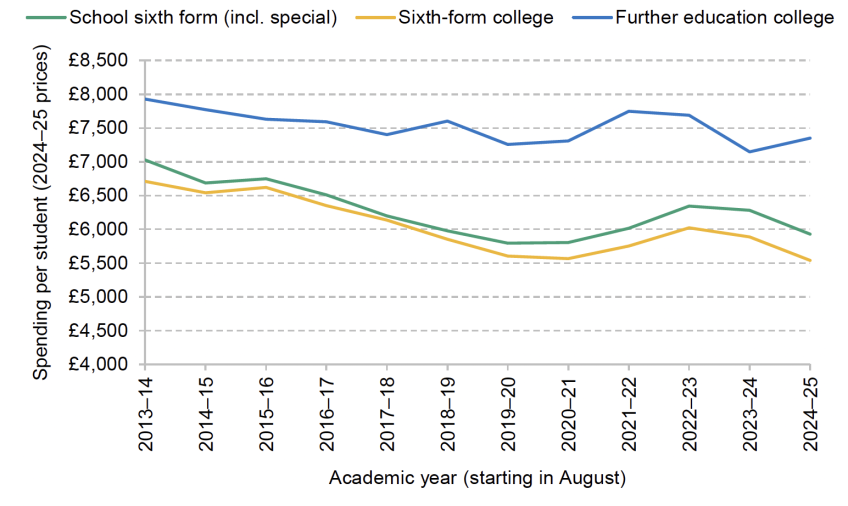

- In the 2024–25 academic year, we estimate that funding per student aged 16–18 in further education colleges will be £7,350, compared to £5,900 in school sixth forms and £5,500 in sixth-form colleges. Higher funding for further education colleges reflects extra funding for costly technical programmes and for students from more-deprived areas.

- Between the 2010–11 and 2019–20 financial years, funding per student aged 16–18 fell in real terms by 14% in colleges and 28% in school sixth forms.

- In the Autumn Budget 2024, the government announced a £300 million cash-terms boost to college and sixth-form funding. Because of rising student numbers and inflation, we calculate that this is only sufficient to deliver a real-terms freeze in funding per student. Combined with increases under the previous government, this leaves college funding per student about 11% lower in real terms than in 2010 and school sixth-form funding per student about 23% lower.

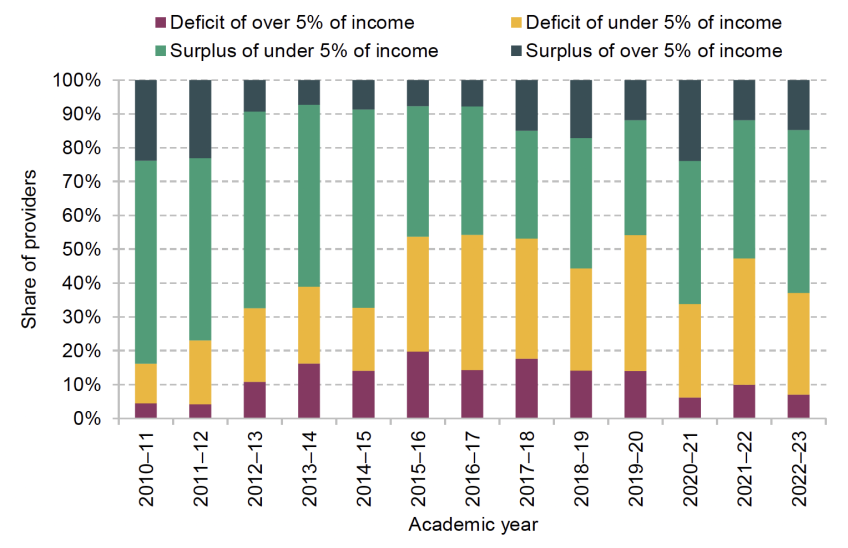

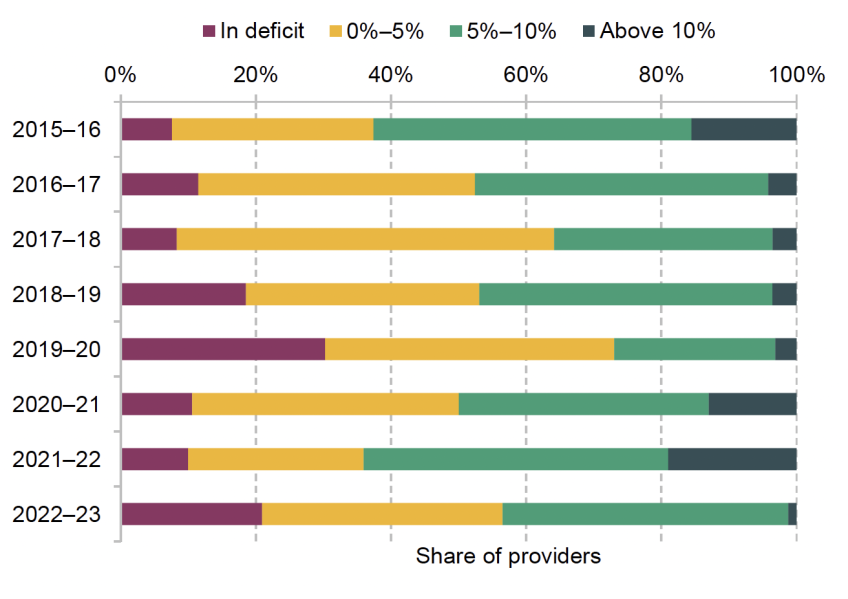

- Colleges and sixth forms face a range of financial uncertainty and challenges. They must accommodate a growing student population, which is expected to grow by 5% or over 60,000 between 2024 and 2028. Average college teacher pay is expected to be about 18% lower than for school teachers in 2025, which is likely connected to the high exit rates amongst college teachers (16% leaving their jobs each year). Meanwhile, whilst underlying college financial positions have improved since 2018, there remained about 37% of colleges operating deficits in 2022–23.

- Looking to the upcoming spending review, the government would need to increase annual funding by £200 million in 2027 in today’s prices to maintain spending per student in real terms, given the growth in the student population. A freeze in total funding in real terms would imply a 4% real-terms fall in funding per student.

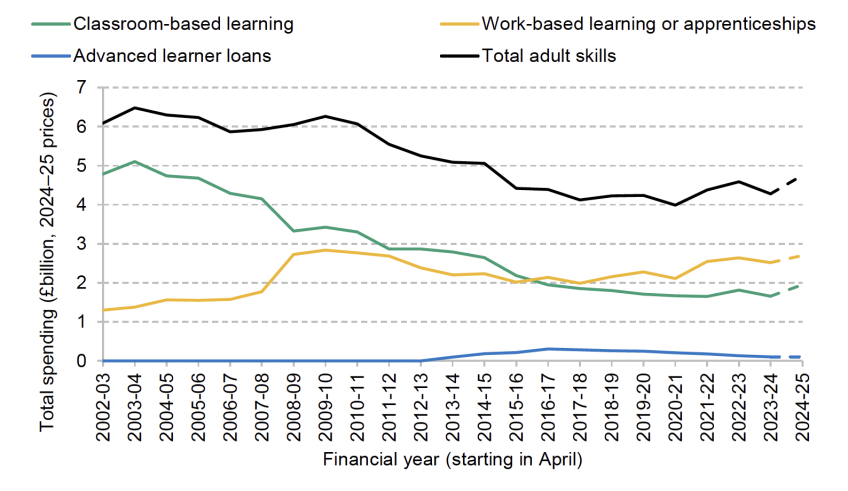

- Total spending on adult skills and apprenticeships is expected to increase by 12% in real terms between 2019–20 and 2024–25. However, this only reverses a fraction of past cuts: total spending in 2024–25 will still be 23% below 2009–10 levels. Spending on classroom-based adult education has fallen especially sharply, driven by falling learner numbers and real-terms cuts in funding rates, and will still be over 40% below 2009–10 levels in 2024–25 even with the additional funding.

Higher education

- Upfront funding for teaching undergraduate students has declined in recent years, standing at £9,750 per year for the 2023–24 university entry cohort (including fees and teaching grants, less bursaries). This is £2,300 or 19% lower in real terms than in 2012–13, driven by cash-terms freezes in the cap on tuition fees for all but one year between 2012 and 2024. This real-terms fall took upfront funding per student back to the same real-terms level as in 2011–12, just before the tripling of the fee caps, and back to the same level as in the early 1990s.

- The new government chose to increase the tuition fee cap for the 2025–26 academic year in line with RPIX inflation, increasing the fee cap from £9,250 to £9,535 (which applies to new and existing students). It is not clear if this policy of indexation will continue. If it does, then upfront resources per student will rise to about £10,000 for students entering courses in September 2025.

- Until recently, there had been some good news for university finances, despite the long-running freeze in domestic fees. Income from international student fees had risen sharply, to £9.4 billion (a fifth of the sector’s income) in 2022–23, and a revaluation of the USS pension scheme had improved sector finances. However, student numbers in 2024 are well below forecasts (23% lower for international students). Together with the rise in employers’ NICs, the Office for Students forecast that a sector-wide surplus of £1.5 billion in 2022–23 could become a sector-wide deficit of around £1.6 billion in 2025–26, unless savings are made.

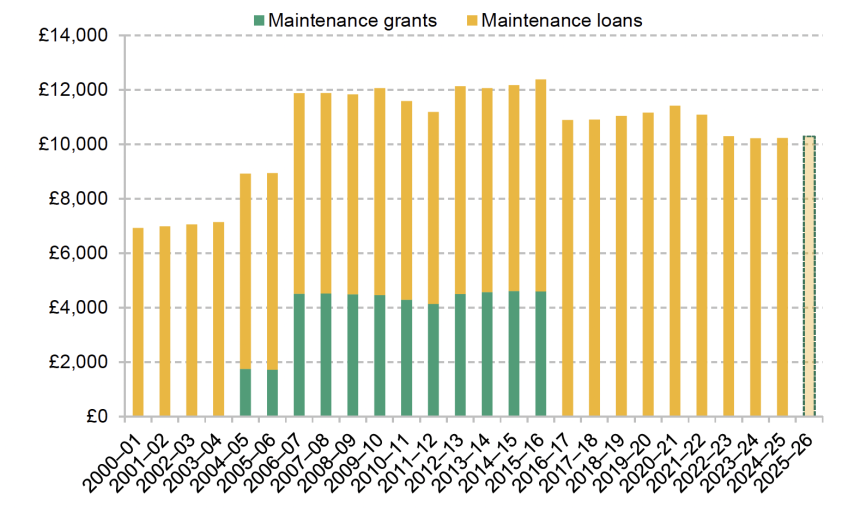

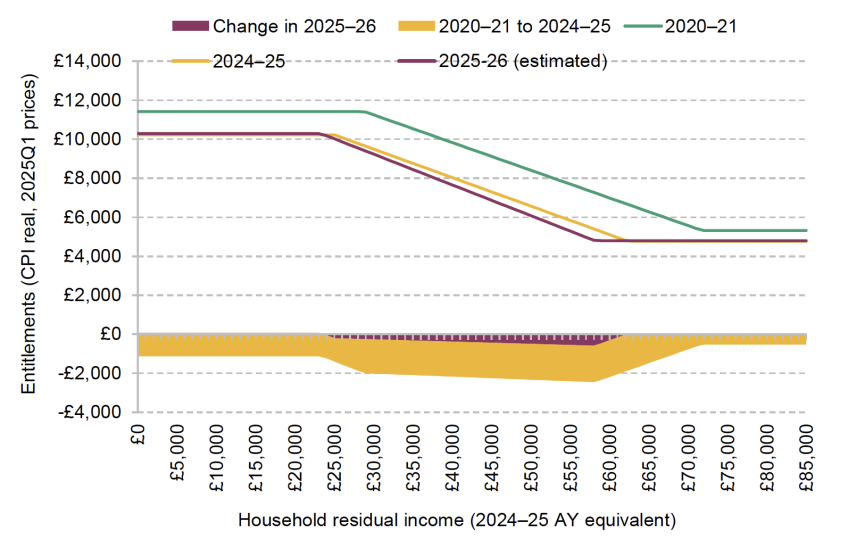

- The new government has chosen not to reverse the significant real-terms cuts in maintenance support for students of recent years. In 2025–26, the poorest students will be entitled to borrow around £1,125 (10%) less in real terms towards their living costs than in 2020. The government is yet to signal any long-run intention for the future of maintenance support, including whether or not they will re-introduce grants.

1. Introduction

Education spending is the second-largest element of public-service spending in the UK behind health, representing £116 billion in 2024–25 in today’s prices or about 4.1% of national income. To make efficient and equitable policy choices, it is crucial to have a clear, consistent picture of how the level of spending at each phase of education has changed over time, the expected future changes and the factors driving these changes. Such issues are a vital component of policy debate, given evidence showing how education investments at different ages combine to drive long-run outcomes (Cunha, Heckman and Schennach, 2010; Johnson and Jackson, 2019).

In a series of annual reports on education spending funded by the Nuffield Foundation, we have sought to cast light on this subject by illustrating how spending per pupil across different stages of education has changed over time. We also publish a range of smaller outputs throughout the year to provide more timely and rapid analysis of the resource challenges facing different phases of education. This analysis is housed on a dedicated website (https://ifs.org.uk/education-spending), providing easy access to the latest figures and the underlying methodology.

The new government has high ambitions to improve education and reduce inequalities. However, like most governments in recent years, it faces a very challenging set of public finances, maybe even more challenging than the situation faced by past governments. In the Autumn Budget 2024, the government chose to top-up departmental spending plans for 2025–26, including a £2.3 billion increase in the schools budget in England. Public-service spending will, over the two years from 2023–24 to 2025–26, grow by an average 3.4% per year in real terms. Departmental spending plans for 2026–27 and 2027–28 will be determined in next year’s spending review. For these two years, the government has pencilled in real-terms increases in overall day-to-day spending on public services of 1.3% per year. However, once likely spending commitments on the NHS, defence and expansions to early years entitlements are accounted for, other areas would very likely face the need to make spending cuts. These would be cuts made from a higher level, following two years of budget increases – but cuts all the same. There is naturally quite a bit of uncertainty around the precise scale of the cuts facing those areas – it matters a lot, for instance, how much cash goes to the NHS, or whether geopolitical developments necessitate a sharp increase in defence spending – but the overall message is clear. On current plans, most areas of education will be asked to find real-terms savings after 2025–26.

At the same time, the cost of special educational needs (SEN) provision is spiralling up by the billions, spending on skills and further education is low by historical standards, and the government faces a delicate balancing act between asking indebted students to pay more for their studies and universities warning of insolvency. It is, of course, possible that these spending plans won’t be implemented. Indeed, historic experience suggests that tight spending plans are likely to get topped up when a spending review comes along and specific choices have to be confronted. But the government has minimal room for manoeuvre against its fiscal rules and the Chancellor has ruled out further tax rises, and while the government could get lucky on growth, there’s every chance that global events weigh on the UK’s economic prospects. This is a delicate fiscal balancing act.

Before we turn to individual areas of education, the rest of this introduction provides overall context on total spending, pupil numbers across each sector over time and the overall methods.

1.1. Total spending on education

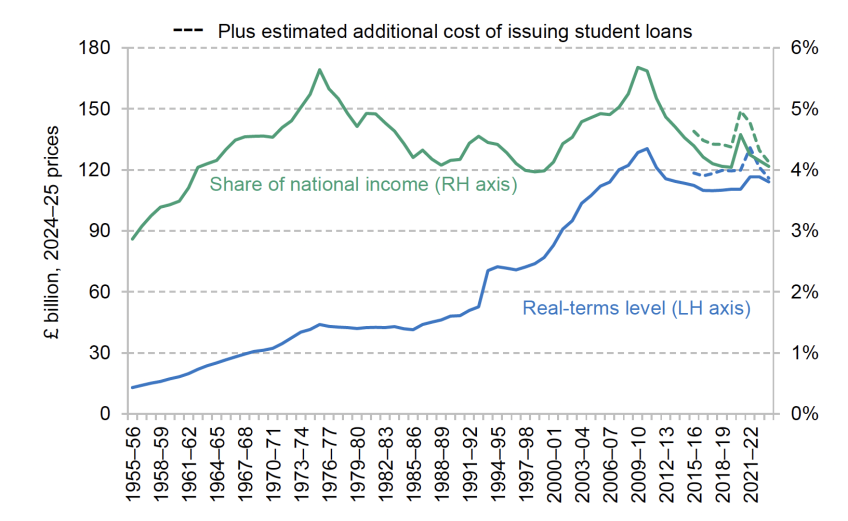

The total level of UK education spending rose significantly up to about 2010. As shown in Figure 1.1, growth was particularly fast from the late 1990s through to the late 2000s, with real-terms growth averaging about 5% per year between 1998–99 and 2010–11. Education spending then fell as public spending cuts began to take effect from 2010 onwards. Between 2010–11 and 2019–20, official education spending fell by 15% in real terms. Since then, it has risen slightly, but remained 12% below its level in 2010–11 by 2023–24.

Some of the decline in education spending during the 2010s reflects initially large declines in capital spending just after 2010 (Sibieta, 2024). These declines also reflect a deliberate increase in effective private funding for higher education through graduate contributions later in life.

Unfortunately, these official figures do not fully account for the cost to the taxpayer of issuing student loans from 2011–12 onwards. As a result, the series overstates cuts to education spending since 2010–11. Changes to national accounting rules mean that the expected cost of issuing student loans is included in overall measures of government spending and the public finances, such as the deficit. We estimate that if official measures of education spending had followed the new national accounting rules for student loans, education spending would have been around £6 billion higher in 2015–16, £5 billion higher in 2022–23 and £2 billion higher in 2023–24.1 The reason for the decline in spending on student loans reflects the recent changes in repayment terms and increased expected graduate contributions (see Chapter 5 for more details). If we add these numbers to the official measure of education spending, the real-terms cut in education spending between 2010–11 and 2023–24 falls from 12% to 11%. As a result, the real-terms level of education spending in 2023–24 was the same as it was in 2006–07. This decline mostly reflects shifting most of the cost of higher education from the taxpayer to graduates. The actual amount of (gross) upfront support through loans for tuition fees has increased from about £5.0 billion in 2012–13 to £10.1 billion in 2015–16 and about £10.6 billion in 2023–24.

Figure 1.1. UK education spending (2024–25 prices and as a share of national income)

Source: HM Treasury Public Expenditure Statistical Analyses 2024, and previous versions; HM Treasury (2024); Office for Budget Responsibility, Economic and Fiscal Outlook, various editions (https://obr.uk/efo/); Office for National Statistics, ‘Student loans in the public sector finances: a methodological guide’, January 2020 (https://www.ons.gov.uk/economy/governmentpublicsectorand taxes/publicsectorfinance/methodologies/studentloansinthepublicsectorfinancesamethodologicalguide).

Including the adjustments for student loans, education spending represented about 4.1% of national income in 2023–24. This follows a temporary peak of 5% during the height of the COVID-19 pandemic in 2020–21, when spending was boosted and the size of the economy was depressed. The underlying picture, however, is a significant decline in education spending as a share of national income over the last 15 years. Following a significant rise over the 2000s, education spending as a share of national income reached a peak of 5.6% of national income in 2010. Since then, it has declined to its current level of 4.1% of national income. This equals a historic low point, with education spending as a share of national income equal to that seen in the late 1990s, late 1980s and mid-1960s. Indeed, it is clear that education spending as a share of national income has not seen a sustained rise since the early 1970s, when it stood at 4.5–5% of national income. It has instead oscillated between about 4% and 5.5% of national income. This is despite large rises in participation in post-compulsory education over time, both in schools and higher education, as well as the creation of an early years sector.

1.2. Student numbers over time

Total spending figures can obscure the impact of changes in the number of pupils or students, which is often one of the most important factors driving changes in the total and per-student level of spending over time. There have also been some fairly substantial changes to pupil and student numbers in recent times, which are due to continue over the next decade.

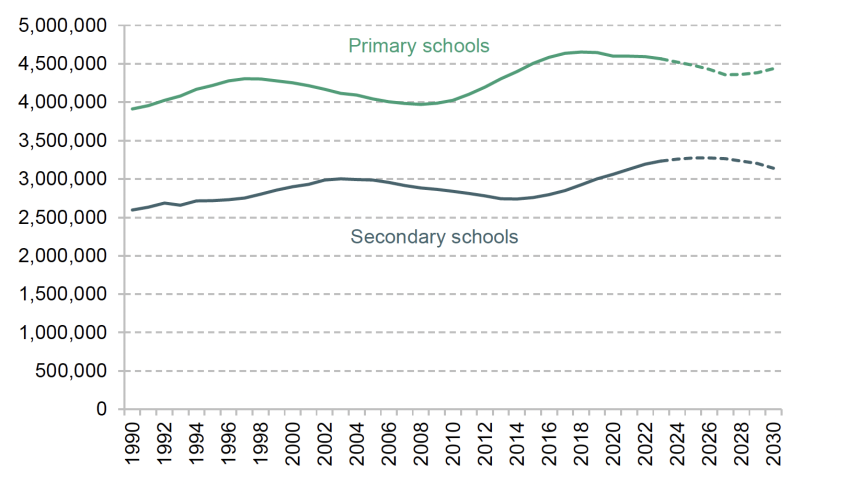

Figure 1.2(a) shows the number of pupils in state-funded primary and secondary schools over time. Numbers in primary schools grew by 17% between 2009–10 and 2019–20, the equivalent of an extra 700,000 pupils – or effectively a full cohort of children. They have since fallen, with a 3% or 100,000 expected drop between 2019–20 and 2024–25. Pupil numbers in secondary schools fell from the early 2000s through to about 2014–15. Between 2014–15 and 2019–20, they then grew by nearly 10% or 300,000, and are expected to have grown by a further 8% or 250,000 between 2019–20 and 2024–25.

Looking beyond 2024–25, the primary pupil population is expected to fall by over 150,000 between 2024–25 and 2027–28, whilst the secondary pupil population is only expected to start falling from 2026–27 onwards and at quite a slow rate initially. This implies a fall in the total pupil population of only about 2% or just over 150,000 between 2024–25 and 2027–28.

Official forecasts for the school-pupil population end in 2027–28, but Office for National Statistics (ONS) forecasts for the total number of children by age groups suggest that the number of primary school age pupils will actually rise by about 2% or 100,000 between 2027–28 and 2030–31, whilst the number of secondary school age children will continue to fall (by over 100,000 or 4% between 2027–28 and 2030–31). This would amount to only a very small net reduction in the total pupil population between 2027–28 and 2030–31. Combined with earlier years, this would imply a 200,000 or 3% fall in the pupil population between 2024–25 and 2030–31. This small fall contrasts sharply with the 600,000 or 8% reduction implied by government forecasts published in 2023.

Figure 1.2. Pupil or student numbers in education in England

(a) Schools

(b) Other stages of education

Source to Figure 1.2: Years refer to academic years starting from September (i.e. 2002 refers to the 2002–03 academic year). Early years numbers represent part-time equivalent places of 3- and 4-year-olds taking up the universal and extended early years entitlement (excluding 4-year-olds in infant classes) and are taken from Department for Education, ‘Education provision: children under 5 years of age’, January 2023, January 2010, January 2006 and January 2002. Primary and secondary school numbers are taken from Department for Education, ‘Schools, pupils and their characteristics’, January 2024 and earlier years, and ‘National pupil projections: July 2024’. Projections for primary and secondary school children for 2028–30 are based on ONS 2021-based forecasts for the growth in the population of 5–9- and 10–14-year-olds. Further education and sixth-form figures refer to 16–18-year-olds in state-funded schools or colleges as measured at the end of each calendar year in Department for Education, ‘Participation in education, training and employment: 2023’. Higher education figures relate to full-time students on first undergraduate degrees and other undergraduate courses from HESA, ‘Who’s studying in HE?’ and also use ‘Historical statistics on the funding and development of the UK university system, 1920–2002’. Forecasts for the early years and 16–18 education are based on ONS 2021-based forecasts for the population of 3–4- and 16–18-year-olds. Forecasts for higher education are based on Department for Education forecasts of entrants up to 2028 (https://explore-education-statistics.service.gov.uk/methodology/student-loan-forecasts-for-england-methodology) and then ONS 2021-based forecasts for the number of 18- and 19-year-olds.

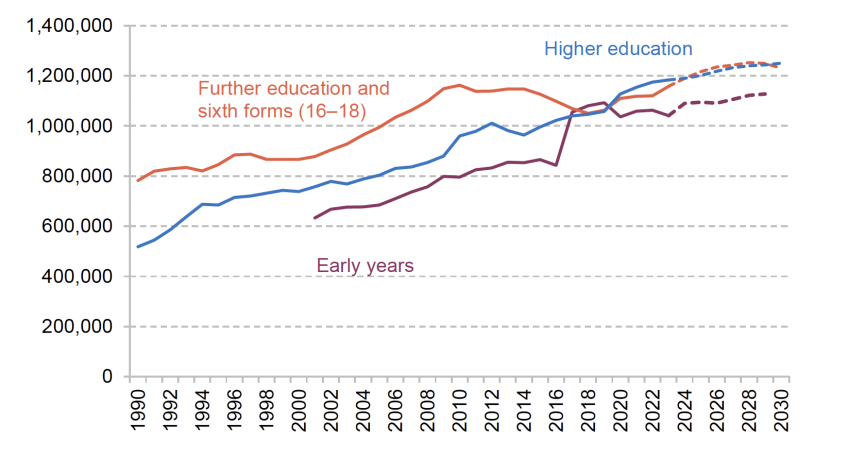

The numbers of pupils in primary and secondary schools are mostly driven by demographic changes, while pupil numbers in other stages of education – early years, further education and higher education – are also affected by changing patterns of participation. Each of these three stages have seen substantial increases in pupil numbers, as shown in Figure 1.2(b). Population growth plays a role, but expansions of the free childcare entitlement (in the early years) and rising participation rates (at later stages) are more important factors driving these changes.

Early years education and childcare in England is increasingly dominated by the ‘free entitlement’ to a government-funded early years education place. The free entitlement is comprised of several distinct offers and has been progressively expanded to cover more children for more hours:

- The universal entitlement offers all 3- and 4-year-olds a part-time (15-hour) place for 38 weeks of the year.

- The extended entitlement, introduced in 2017, offers an additional 15 hours a week of childcare to 3- and 4-year-olds in working families.

- The 2-year-old offer, introduced in its current form in 2014, provides the roughly 40% most-disadvantaged children with a part-time early education place, again for 38 weeks a year.

- The expanded entitlement was announced at the March 2023 budget and is currently being rolled out. From September 2025, this will provide a full-time place (30 hours a week) for children aged 9 months to 36 months in working families.

From 2001–02 to 2016–17, the total number of part-time equivalent places for the universal free entitlement in the early years rose by a third, driven by increases in the population of pre-school aged children and expansions to free entitlement eligibility. With the introduction of the extended entitlement for children in working families in 2017–18, the number of part-time equivalent places jumped. Between then and 2023–24, there were no further expansions of the free entitlement and the number of part-time equivalent places has remained roughly constant. This stability masks two offsetting trends: while the number of places taken up for the extended entitlement has grown by around 63,500, the number of children taking up the universal offer fell by around 9% between 2017–18 and 2023–24, driven by a combination of falls in the population of 3- and 4-year-olds and lower take-up.

Looking ahead, the latest ONS population projections forecast imply that the pre-school age population by 2029–30 will be close to the numbers for 2023–24. Meanwhile, if rising take-up of the extended entitlement continues, we would expect to see around 8% more part-time equivalent places for 3- and 4-year-olds in 2029–30 compared with 2023–24.

Figure 1.2(b) focuses on places for 3- and 4-year-olds, which historically have made up the bulk of children accessing the free entitlement. With the introduction of the expanded entitlements – the largest and fastest expansion to date – this is set to change and will see substantial increases in the number of places for younger children. This is discussed further in Chapter 2.

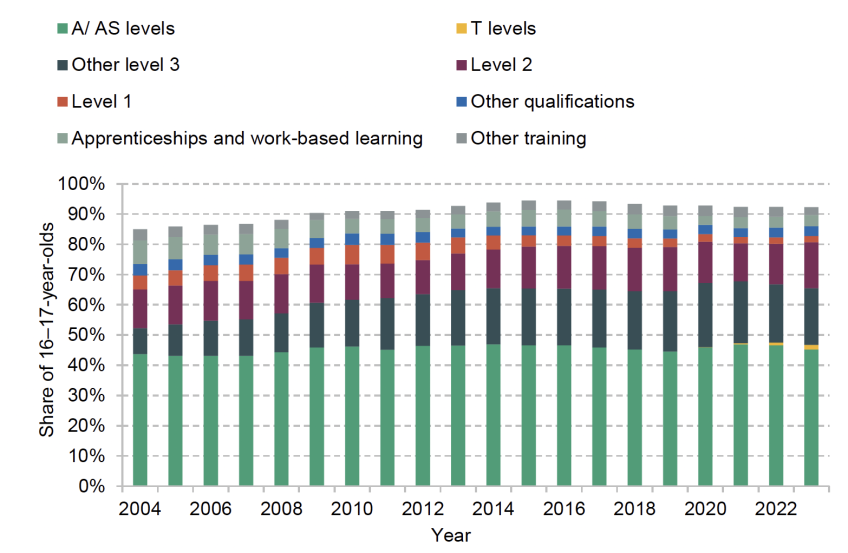

The number of students in 16–18 education grew by almost 50% between 1990–91 and 2010–11, from about 800,000 to 1.2 million full-time equivalent students. After 2010–11, numbers fell by about 10% down to just over a million in 2018–19, reflecting reduced cohort sizes rather than falls in participation.

Since then, numbers have started to rise again, and the number of students is 10% or 100,000 higher in the latest year of data (2023–24) than in 2018–19. This mostly reflects growth in cohort sizes again. Further rises are expected over the next few years due to population growth, with numbers currently projected to rise by 8% between 2023 and 2028, before then starting to fall slightly. This would make for 100,000 extra students by 2028. If realised, this would clearly place upwards pressure on college and sixth-form spending.

The number of full-time undergraduate students in higher education in England more than doubled between 1990 and 2019, to reach 1.06 million. Participation increased during the pandemic, with student numbers increasing by 6.5% in 2020, but growth has since slowed. In the latest year (2024), acceptances of offers at UK universities increased by 1.3%, far more slowly than the sector forecast (5.8%). As we discuss in Chapter 5, recruitment of international students has also fallen, which creates financial headaches for many UK universities.

Nonetheless, the latest Department for Education forecasts imply a further increase in the number of England-domiciled higher education students of 4% or 44,000 between 2022 and 2026. ONS population forecasts would then imply a total increase of 6.5% or 76,000 by 2030 compared with 2022, taking the number of full-time undergraduate students in higher education to 1.25 million.

Increases in higher education student numbers will clearly place pressure on spending. In the past, such as during the 1990s, spending has not always increased in line with rising student numbers, thereby reducing spending per student. At other times, large increases in higher education student numbers have led governments to make substantial changes to the higher education finance system in order to ensure sufficient levels of resources.

The previous government already made large changes to the student finance system, which will likely reduce the cost of the system to the taxpayer (Waltmann, 2022). However, we have also seen a large real-terms reduction in spending per student as rising inflation eroded the real-terms value of the tuition fee cap, which was frozen in cash terms at £9,250 between 2017 and 2024. This long-running decline in resources is now set to end, with the fee cap due to rise in line with RPIX inflation in 2025.

1.3. Methods and approach

The rest of this report mainly focuses on day-to-day or current spending on different areas of education in England. This is primarily for data availability reasons, though we have also provided analysis comparing school spending per pupil across the four nations of the UK, which indicates higher levels of school spending per pupil in Scotland in particular (Sibieta, 2023a). We also provide some evidence in this report on trends in school capital spending.

For the most part, we focus on public spending on education. This is due to a lack of reliable data on total private spending on each stage of education over time. For schools, we have produced additional analysis comparing state school spending per pupil and private school fees over time (Sibieta, 2023b), including the likely effects removing tax exemptions from private schools. For higher education, we also separately consider the support provided to students with their living costs, and expected graduate contributions to higher education spending through student loan contributions later in working life.

In Chapters 2–5, we examine trends in spending on the early years, schools, further education and skills, and higher education. In Chapter 6, we compare trends in spending per pupil across different stages of education over time. In each case, our methodology for calculating spending per student is detailed in full on the dedicated website (https://ifs.org.uk/education-spending/methods-and-data). In most cases, figures relate to core education spending and exclude temporary support during the pandemic, though it is not always possible to separate this out. Chapter 7 concludes.

In most cases, we calculate real-terms changes by adjusting for economy-wide inflation as captured by the GDP deflator. This is the standard practice used for analysing public spending in the UK. Across long periods of time and in stable economic environments, the GDP deflator is likely to provide a close approximation to the costs faced by education providers. However, the recent spike in inflation was mainly driven by imported food and energy prices, which is not fully captured in the GDP deflator. With this in mind and to provide more context, we often provide analysis of likely costs faced by providers. This also allows us to consider the financial pressures on providers’ budgets, and how the actual funding available to providers compares with their actual cost pressures.

2. Early years

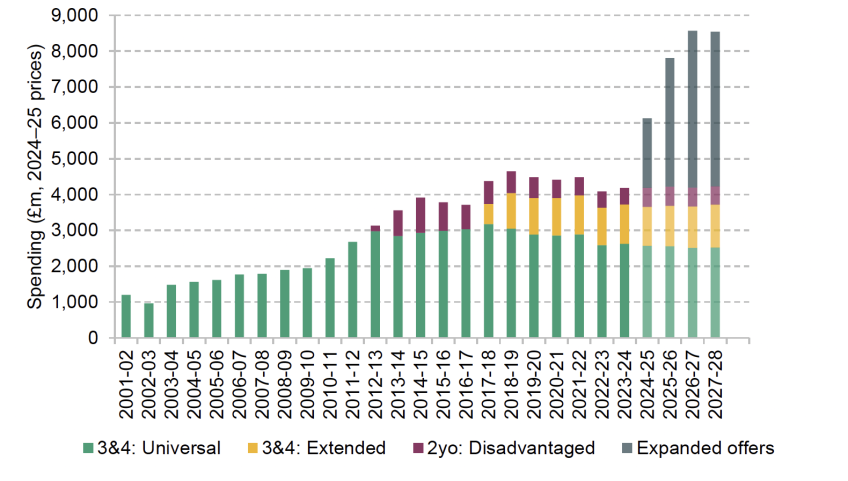

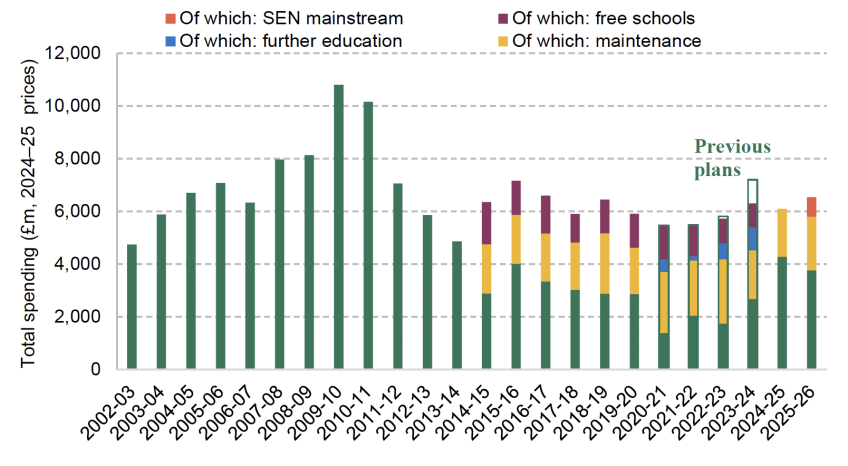

Today, public spending on early years education and childcare is synonymous with the free entitlement programme, the scheme that offers a government-funded place in early education and childcare. The free entitlement has grown to become the largest pre-school education and childcare programme in England – see, for example, Drayton et al. (2023) for a history of how early years support has changed – with spending doubling in real terms over the decade from 2001, and rising further to reach £4.2 billion last year (i.e. 2023–24). On the back of this precipitous rise, it is also set to grow in importance: as shown in Figure 2.1, the free entitlement is forecast to undergo its fastest and largest expansion to date, rising to an estimated £8.5 billion in 2026–27.

The free entitlement is not one single programme; different offers are available to children of different ages, with different eligibility requirements. These include:

- a universal offer of 15 hours a week for all 3- and 4-year-olds;

- an extended entitlement to 30 hours a week for 3- and 4-year-olds in working families;

- a disadvantage offer of 15 hours a week for the most disadvantaged 2-year-olds.

Alongside these schemes is the new ‘expanded’ entitlement announced at the March 2023 budget by the previous government. This new entitlement for working families is currently being expanded under the following timescales:

- from April 2024, 15 hours a week for 2-year-olds in working families;

- from September 2024, 15 hours a week for children aged 9–36 months in working families;

- from September 2025, 30 hours a week for children aged 9–36 months in working families.

Once fully rolled out, the expanded entitlement will provide children in households with all adults in work with access to 30 hours a week of free childcare from the end of maternity leave (nine months) to when children start school.

This chapter is split into three parts. The first (Section 2.1) documents how spending on the existing entitlements has changed over time, including changes to hourly funding rates, before turning to how spending is expected to evolve with the introduction of the expanded entitlements. The second part (Section 2.2) looks at how funding for the free entitlement is distributed by local authorities and the extent to which different types of provision or certain groups of children are supported through the funding system. Finally, in Section 2.3, we consider the implications of the most recent policy changes affecting the early years sector (including the expansion of school-based nursery places and the recent rises in employers’ NICs announced in the Autumn Budget 2024) and look forward to considerations for the upcoming spending review.

2.1. Spending on the free entitlement

Figure 2.1 shows total public spending on the free entitlement over the past 25 years, split by type of programme. For the first decade of this period, the sole programme at the time, the universal entitlement, saw significant real-terms growth of about 120% in total. This saw total spending on a part-time place for 3- and 4-year-olds rise from £1.2 billion in 2001 to £2.7 billion in 2011. Over the 2010s, real-terms total spending on free entitlement programmes continued to rise steadily, a notable departure from the real-terms cuts experienced in other stages of education (see later chapters). Figure 2.2 also highlights, however, how these increases in spending were largely driven by the introduction of additional entitlements rather than increased generosity in the funding of existing entitlements.

Figure 2.1. Total real-terms spending on free entitlement hours in England (£ million, 2024–25 prices)

Note: Entitlements as described at the start of the chapter. The 2-year-old disadvantaged offer was initially piloted in a small number of areas in 2012, before being rolled out nationally in 2013. Because our data on total spending do not split out the universal and extended entitlements, we allocate total spending proportional to their budgets from the Dedicated Schools Grant (DSG). From 2024–25 onwards, we use DSG budget for core funding.

The final years in Figure 2.1 project from 2024–25 (i.e. the first year of the rollout of the expanded entitlements) the expected budget for the free entitlements. This differs from the measures of spending out-turn for previous years but provides a useful indication of how spending may evolve in the coming year. Funding rate rises announced at the March 2023 budget are expected to restore total real-terms funding on existing entitlements (universal, extended and 2-year-old disadvantage) in 2024–25 to the 2018–19 peak of around £4.7 billion in today’s prices. This is even though the number of child-hours delivered for two of these programmes (universal and 2-year-old disadvantage) are lower than they were in 2018–19. In addition, the partial rollout of the expanded entitlements is expected to add a further £1.7 billion to this amount, representing the largest year-on-year increase in our series.

Looking further ahead, spending on the free entitlement is projected to continue to rise substantially in real terms as the new entitlements are rolled out. By 2027–28, total spending will be more than double its 2023–24 level, representing a major increase in the early years budget. This significant injection of funding is notable against the backdrop of a historically challenging position for the public finances (Johnson, 2024).

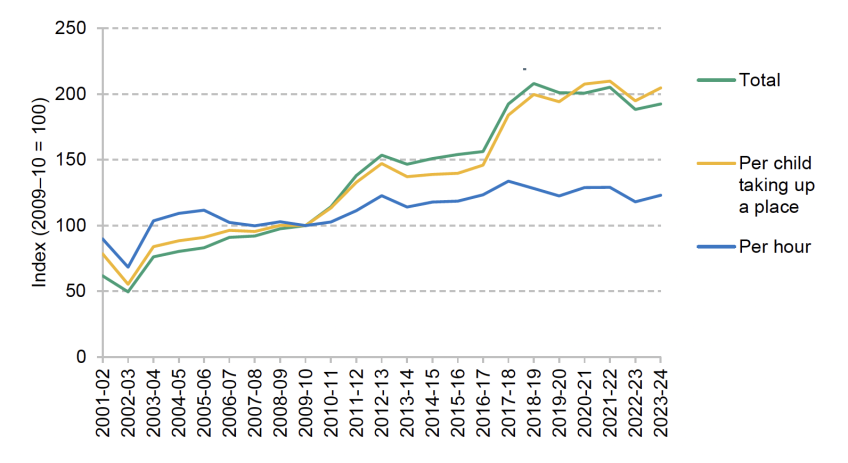

Figure 2.2 paints a picture of a long-term rise in real-terms spending on the free entitlement. However, this period has seen significant growth in the number of children and hours covered by the entitlements, as well as population fluctuations in the number of 2-, 3- and 4-year-olds (see Drayton and Farquharson, 2023 for more detail). It is therefore more instructive to consider how real-terms spending per child and per childcare hour has evolved over time.

Taking 3- and 4-year-olds first (covering the universal and extended 30-hour offer), as shown in Figure 2.2, growth in real-terms spending per child taking up a place has largely tracked changes in total spending and saw substantial real-terms growth, doubling over the decade from 2009–10. Between 2017–18 and 2023–24, where no new entitlements were introduced, spending per place was more volatile as it was exposed to funding rate changes as well as rising costs eroding the real value of resources, particularly during the 2022–23 inflation spike.

In contrast, if we account for the number of hours of childcare children are taking up, we see much more muted growth, with real hourly resources growing by 23% over the 14 years between 2009–10 and 2023–24. That said, this still represents substantially higher growth in real resources compared to spending per pupil on other stages of education over the same period (Drayton et al., 2023).

Figure 2.2. Growth in real-terms spending on the free entitlement for 3- and 4-year-olds (indexed 2009–10 = 100)

Note: Spending on universal and (from 2017–18) extended entitlements for 3- and 4-year-olds. Spending per place is spending per part-time equivalent place (15 hours) across both entitlements, so a child accessing their full universal and extended entitlement would count towards two part-time equivalent places; see https://ifs.org.uk/education-spending/methods-and-data for more details.

Source: See ‘Methods and data’ at https://ifs.org.uk/education-spending/methods-and-data.

Note that 2-year-olds are funded at a different rate, and the picture for spending on the 2-year-old disadvantage offer looks somewhat different: hourly resources have remained roughly stable since its introduction in 2015–16, but total spending on the programme has fallen over time (Drayton and Farquharson, 2023). This is largely driven by a decline in the number of places taken up, which fell by a quarter between 2015–16 and 2022–23. The demographic shifts and tighter eligibility criteria for the programme that are behind this fall are discussed in greater detail in Drayton and Farquharson (2023).

Funding rates

While the total amount of funding for the free entitlement is an important indication of the government’s priorities, what matters more to childcare providers is the hourly funding rate that they receive for children in their care. This provides a proxy2 for the amount of resources providers have to deliver the free entitlement.

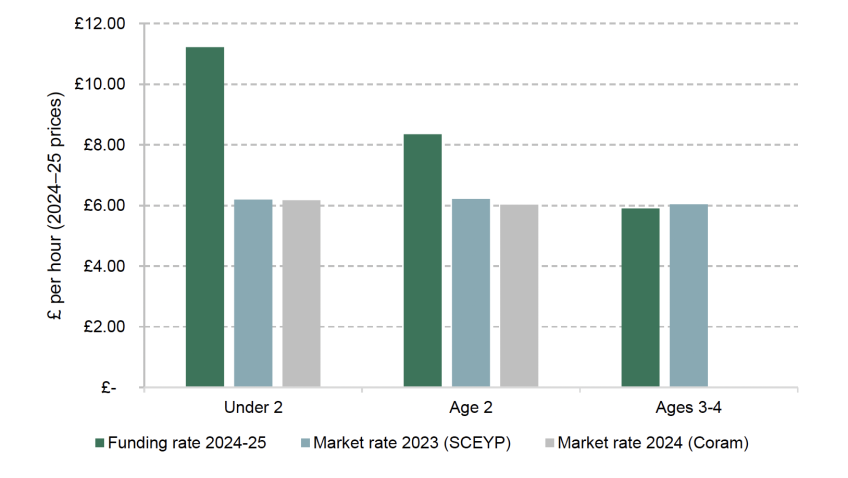

Figure 2.3 shows the average funding rate across England in 2024–25 by age of child, compared to current market prices for childcare. The first pattern that emerges is that providers tend to charge parents similar hourly prices for childcare, irrespective of a child’s age. This smoothing of prices across ages is notable given differences in the costs of providing childcare to children of different ages (for instance, younger children have stricter requirements around the number of staff per child). This gradient in the cost of provision by child age is reflected, however, in the funding rates providers receive for children of different ages in their care, with higher funding rates for younger children.

Figure 2.3. Free entitlement funding rates in comparison to market prices (2024–25 prices)

Note: Market prices are shown from two sources: the Department for Education 2023 Survey of Childcare and Early Years Providers (‘SCEYP’ survey) and the Childcare Survey 2024 from Coram Family and Childcare (‘Coram’ survey). Market rates from the Coram survey are a weighted average of rates across group-based nurseries and childminders, with weights based on number of registered places in the SCEYP survey. Funding rate rates are retrieved from the Dedicated Schools Grant 2024–25.

Source: Department for Education (2023a, 2024a) and Hodges, Shorto and Goddard (2024).

The second takeaway from Figure 2.3 is that funding rates for younger children are much more generous than current market rates. For 2024–25, the government has budgeted for a much higher funding rate for 2-year-olds, while rates for the under-2s will start at £9.45, almost 50% higher than existing prices in the market. This suggests the government is channelling resources towards younger ages to both incentivise expansion in provision for younger children and to better align funding rates with differences in costs of provision for different age groups.

However, hourly funding for the existing entitlements for 3- and 4-year-olds is much closer to market prices on average. While this makes it less likely that this public funding translates into excess profits for providers rather than being put to better use elsewhere in the public sector, it leaves less margin for error: providers who are less financially sustainable, or in areas experiencing challenges with delivery, may be more financially exposed if providers’ costs become misaligned with funding rates.

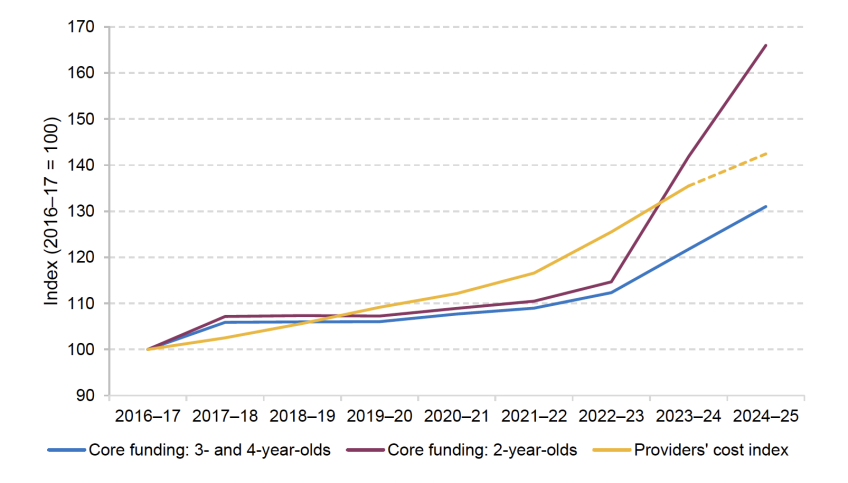

While Figure 2.3 focuses on hourly rates as they stand today, what also matters is how funding rates have evolved over time and the extent to which they have kept up with changes in provider costs. In Figure 2.4, we document how the funding rate has changed over time in cash terms for provision for 3- and 4-year-olds and 2-year-olds, alongside changes in the costs that childcare providers face – the provider cost index. These provider costs account for changes over time in employee wages, including changes in the minimum wage, as well as changes in other components of costs, including energy, rent and food.3

Figure 2.4. Growth in core hourly funding and providers’ costs for 3- and 4-year-olds and 2-year-olds, indexed to 2016–17

Note: Funding rates up to 2022–23 are drawn from the Early Years block of the Dedicated Schools Grant. In 2023–24, funding rates mid-way through the financial year, in September; the chart presents weighted averages of the April–August and September–March rates. The funding rate for 2024–25 has been announced as £8.28 for 2-year-olds and £5.88 for 3- and 4-year-olds in cash terms.

As shown in Figure 2.4, between 2016–17 and 2019–20, funding rates for 3- and 4-year-olds were largely frozen in cash terms, with the exception of an uplift in 2017–18 when the extended entitlement for 3- and 4-year-olds in working families was brought in. Over the same period, the costs that providers incur to deliver childcare slightly outpaced growth in funding: the average provider experienced a 9% rise in costs compared to a 6% increase in funding rate. However, recent years have seen a wedge open up between funding rates for 3- and 4-year-olds and provider costs, as high inflation and rises in minimum wage have generated large cost rises for providers (Drayton and Farquharson, 2022). This has meant that even relatively generous uplifts in funding rates in 2023–24 and again in 2024–25 have not offset the cost pressures. By our estimates, core resources per hour for 3- and 4-year-olds will remain 8% lower in real terms in 2024–25 than in 2016–17 once provider costs are taken into account. This rises to 15% lower relative to 2012–13.

The picture looks somewhat different for childcare for 2-year-olds. As Figure 2.4 shows, while growth in 2-year-old rates tracked changes in funding rates for 3- and 4-year-olds between 2016–17 and 2022–23, the two have diverged in the past couple of years with the largest cash increase in the 2-year-old funding rate in 2023–24 since its introduction (30%4). Funding for 2-year-olds has also been prioritised this year, with a 17% cash-terms rise in 2024–25, well above current market prices.

It is also important to consider how funding rates are set going forward. As explored in Drayton and Farquharson (2024), next year will see a small rise in core funding rates, expected to largely offset the impact of economy-wide inflation (as measured by the GDP deflator). The uplift for 3- and 4-year-olds is slightly higher, meaning that effective funding rates will rise about 1% faster than economy-wide inflation.

However, provider costs are set to rise next year too: rises in employers’ NICs and the minimum wage announced in the Autumn Budget 2024 will leave childcare providers with new expenses (we discuss possible impacts in Section 2.3). For some providers, this will outweigh the modest increases to funding rates, continuing the long-term trend of funding not keeping up with changes in provider costs (Reed and O’Halloran, 2024).

2.2. Distribution of spending across local authorities

Our focus so far has been to study total spending on the early years ‘free entitlement’ at a national level. However, there is no single childcare market for England: different places have different availability of provision and serve different children and families. What matters to childcare providers is not the headline funding rate but what they receive on the ground to deliver the entitlements.

The funding childcare providers receive is governed by a two-step process. First, central government allocates funding between local authorities according to the Early Years National Funding Formula (EYNFF). Under this system, areas receive different hourly funding rates, which vary according to local costs of providing childcare (areas with higher rents for premises and staff wages attract more funding) and the needs of the population (areas with more-deprived or disabled children or children with additional language needs attract additional funding). Drayton and Farquharson (2023) provide more detail on how the EYNFF works and the implications of the funding formula for different areas.

In a second step, each local authority is responsible for distributing funding to the providers in its area based on its own funding formula, known as the Early Years Single Funding Formula (EYSFF). Technically, this results in 153 distinct funding allocation formulas across local authorities; in practice, local authorities are heavily restricted in how they distribute this funding.

The two biggest constraints on local authorities are the requirements to pass through at least 95% of the funding received under the EYNFF to providers5 and to pay the same rate to different types of providers.6 Local authorities are then permitted to offer supplements that can be used to tweak their formula; though again, there are restrictions on the total value of supplements, which must not exceed 12% of total funding. A deprivation supplement is mandatory for 3- and 4-year-olds; other allowable supplements can include:

- quality, to support workforce qualifications or system leadership;

- rurality or sparsity;

- flexibility, to support providers offering more flexible provision to match parents’ working patterns and needs;

- English as an Additional Language (EAL).

Finally, the EYNFF also allocates additional funding streams to areas such as the early years pupil premium (EYPP) and the disability access fund (DAF).7 These supplements operate somewhat differently: instead of raising the base funding rate for a local authority, which is then handed down to providers equally, providers receive extra funding for each eligible child – meaning that funding follows the child.

By design, this standardisation across local authorities in use of the EYSFF imposes some alignment between the rate allocated under the national funding formula and the rates that providers receive. In this section, we study how 153 local authorities use the tools available to them under the EYSFF, focusing on 2023–24, the most recent year of data.

A limitation of this analysis is that this reflects local authority allocations prior to the introduction of the expanded entitlements. These new entitlements represent a major expansion to the previous entitlements (the universal and extended entitlements for 3- and 4-year-olds and the 2-year-old disadvantage offer) and areas may well alter their allocations to support the delivery of the new entitlements for younger children in working families. This will be important to look into as data become available. In our analysis, we exclude the EYPP and the DAF, which allocate additional funding to deprived and high needs children, respectively, as these operate outside of the local authority funding system. We discuss EYPP and DAF funding separately in Section 2.3.

Distribution of spending under the EYSFF

We first study how funding handed down from the national formula is channelled into different types of spending by local authorities. Figure 2.5 divides each local authority’s total funding under the single funding formula (excluding EYPP and DAF) into:

- core – funding for the core hourly funding rate;

- supplements, SEN inclusion fund and Maintained Nursery Supplement – targeted spending to compensate providers with higher cost provision such as through the SEN inclusion fund, supplements for quality and deprivation, and supplementary funding for maintained nurseries;

- centrally retained and contingency – resources held back by local authorities for contingency planning, that is, resources for managing fluctuations in demand, and to support early years related activities performed centrally, including eligibility checking or supporting local authority-wide specialist SEN services.

Owing to the requirement to pass through at least 95% of core funding for the 3- and 4-year-old entitlements to providers, and restrictions on how much funding can be allocated to supplements, there is a reasonably high level of conformity in how different local authorities allocate funding. In particular, the pass-through requirement ensures that at least 95% of core funding is split between the base funding rate, supplementary funding rates, the SEN inclusion fund and contingency funding. On average, local authorities distribute 88% of funding to the core hourly funding rate, received equally across providers. Three-quarters of local authorities allocate at least 85% of funding to the core rate.

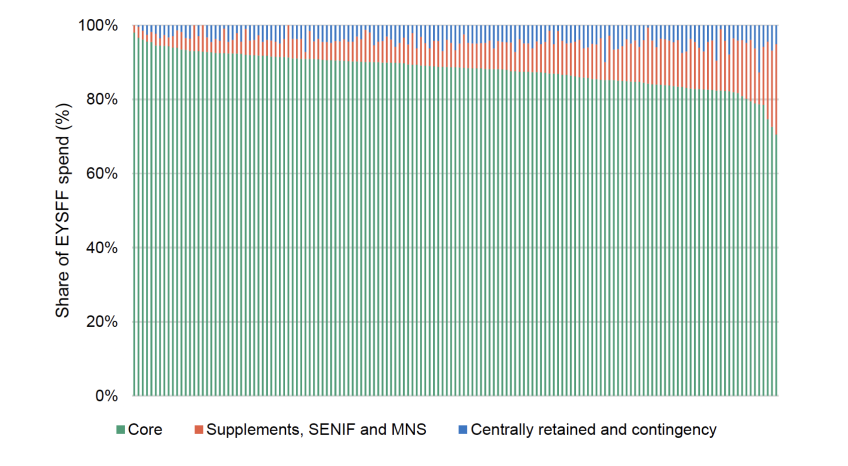

Figure 2.5. Composition of spending under the EYSFF, by local authority

Note: Excludes spending on the EYPP and the DAF. The pass-through requirement requires at least 95% of core funding to be split between Core, Supplements, SENIF and MNS, and contingency funding. Since we conceptually group centrally retained and contingency funding, it cannot be read from this graph whether a local authority meets the pass-through requirement.

There is variation, however, in how local authorities make use of supplements and SEN inclusion funding, the mechanisms through which areas can target more resources to providers serving higher-needs population or delivering higher-quality or more flexible provision. Just over a quarter (27%) of local authorities dedicate fewer than 5% of resources to these more-targeted funding streams, while almost another quarter (23%) of areas allocate more than 10% to this targeted spending. Areas distributing more through supplements and the SEN inclusion fund tend to be more urban (around two in five are in London) and more-deprived. We study the use of supplements in greater detail in the following subsection.

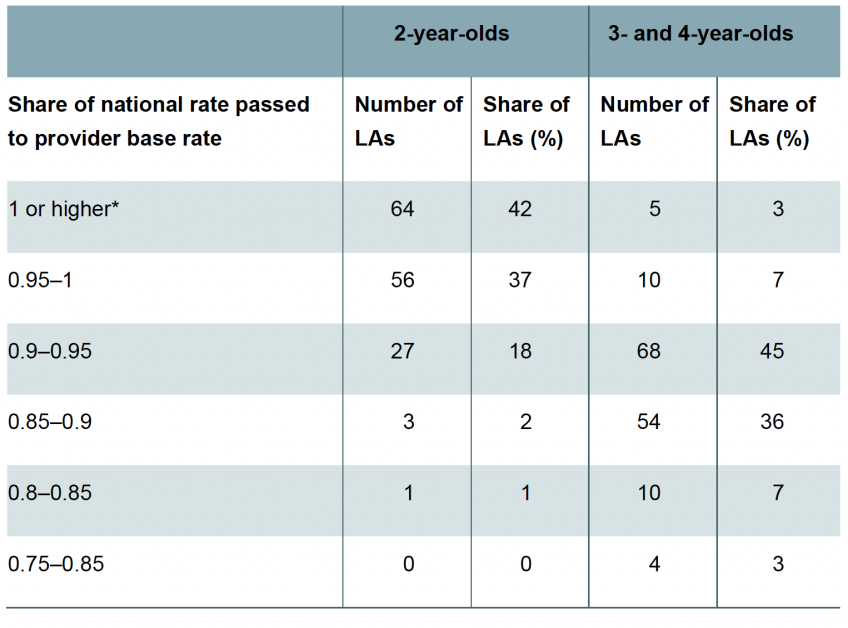

Another way to see how the centrally determined funding rates translate into resources on the ground is to examine how closely provider base rates set by local authorities align with the EYNFF rates. Table 2.1 shows differences across areas in the proportion of the EYNFF funding rate that providers receive in their base rate from local authorities.

Table 2.1. Core rates under EYSFF versus EYNFF for 2023–24

Note: * Only two and one local authorities (LAs) have a pass-through higher than 1 for the 2-year-old rate and 3- and 4-year-old rate, respectively.

For 2-year-old funding rates – which, for 2023–24, relate to the 2-year-old disadvantage offer – many local authorities (41%) pass on exactly the EYNFF rate to providers. A further 37% of areas pass through at least 95% of the EYNFF rate. Since the 2-year-old disadvantage entitlement is eligible only to low-income children, it serves a less variable population, and therefore resources are more easily targeted through the base rate with less need for additional supplements (as we will see, this was also encouraged in Department for Education guidance). As the expanded entitlements draw in 2-year-olds from working families into the free entitlement, however, local authorities may need to change their funding formulas to ensure providers are encouraged to (continue to) offer childcare places for disadvantaged 2-year-olds.

For 3- and 4-year-olds, fewer resources feed into core funding relative to targeted spending (e.g. supplements), resulting in lower pass-through from the EYNFF rate to the universal base rate. Very few areas pass on the EYNFF rate to providers exactly, and only 7% of areas set the base rate to 95% of the EYNFF rate or higher. Still, all local authorities feed at least three-quarters of the EYNFF rate into their base rate for 3- and 4-year-olds, with the majority of areas falling in the 85–95% range.

Local authorities’ use of supplements

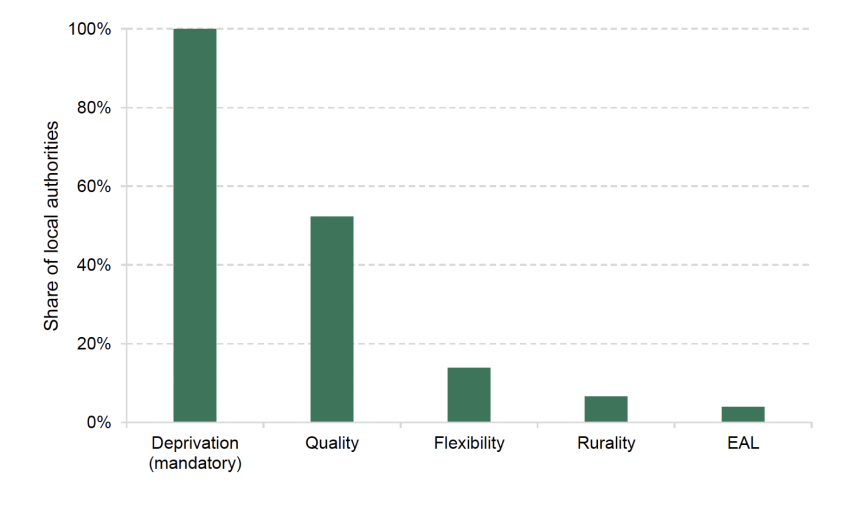

Figure 2.6 shows, for each type of supplement permitted by the Department for Education, the share of local authorities who offer additional funding for that factor for entitlements for 3- and 4-year-olds.8

Figure 2.6. Use of supplements for entitlements for 3- and 4-year-olds by local authorities

All local authorities use deprivation funding for 3- and 4-year-olds, which is a mandatory requirement. This can be measured in different ways: some areas top up funding for children eligible for the EYPP, others may target providers located in deprived neighbourhoods (e.g. based on the Index of Multiple Deprivation, IMD). Around half of local authorities additionally fund higher quality provision, that is, providers with more qualified staff or who support other local providers to deliver quality provision, at higher rates. Only around 1 in 10 areas support flexibility of provision, for instance, providers who offer wraparound care or out-of-hours provision. This suggests incentivising high quality early years education and childcare and supporting provision for parents who require flexibility (such as shift workers) through higher funding rates is not a universal approach taken by local authorities. Variation in use of quality and flexibility supplements may also have implications how different types of provider fare in different areas. For instance, childminders often provide greatest flexibility of provision, while quality supplements are more likely to benefit group-based providers, whose staff tend to hold more early years qualifications, and providers with more resources to support systems leadership amongst local providers.

Figure 2.6 also highlights that very few areas compensate for rurality and for serving children with EAL. Partly, this is because most areas will not serve especially rural or EAL populations. Yet, the relationship between the use of the supplements, rurality and EAL is not entirely straightforward. For instance, it is local authorities with high, but not the highest, shares of children with EAL that make greatest use of the EAL supplement: no local authorities in the top quartile of children with EAL use the supplement, while 14% of local authorities in the third quartile have an EAL supplement. This suggests that in areas with more homogeneous populations (mostly rural or mostly EAL), support flows through the core funding rate, while in more mixed areas it is useful for local authorities to target support via supplements.

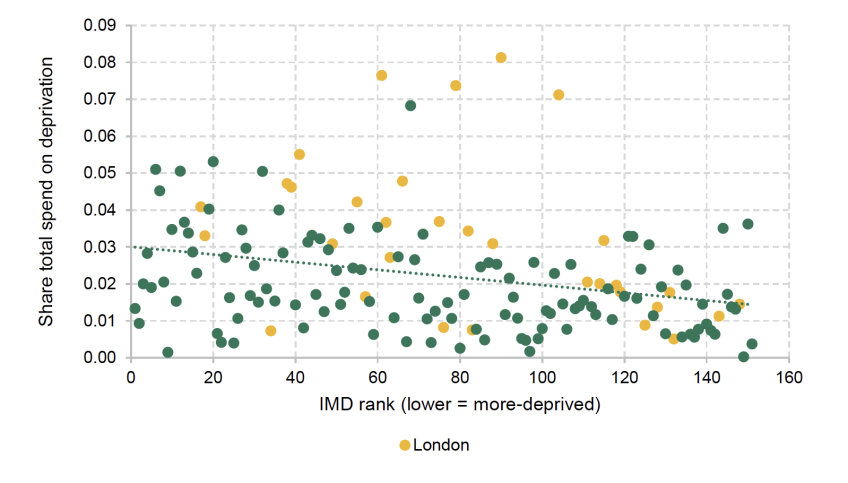

As well as considering how local authorities use the different supplements available to them, it is also important to consider the extent to which they align with the needs of an area. Figure 2.7 plots for each local authority the share of total spending under the EYSFF going to deprivation uplifts against the average level of deprivation in the local authority, measured using the index of multiple deprivation (IMD). The downwards-sloping relationship confirms that more-deprived areas tend to allocate more funding to deprivation supplements: an increase in deprivation equivalent to moving 10 ranks on the IMD is associated with a 5 percentage point increase in the proportion of funding dedicated to deprivation. That said, there is a lot of variation in funding for deprivation amongst local authorities with similar levels of deprivation. It is also notable that some of the local authorities with the most resources dedicated to deprivation are those in the middle of the pack and many are based in London. A number of London boroughs have pockets of deprivation alongside wealthier neighbourhoods, possibly making it more effective to direct resources via supplements compared with more uniformly deprived areas.

Figure 2.7. Value of deprivation supplement by local authority IMD

Note: 2019 index of multiple deprivation. Share of total spend under the EYSFF, excluding the DAF and EYPP.

Overall, the EYSFF is a transparent method of allocating funding to different providers within a local area. The requirements for what local authorities can and can’t do with free entitlement funding are relatively restrictive, generating a fair amount of conformity in how money is spent in different places. There are differences, however, in how much areas spend on targeted funding streams (supplements for deprivation, quality, rurality, EAL and SEN inclusion fund), with more-urban and more-deprived areas making greater use of these funding mechanisms. These areas are likely to have a higher prevalence of disadvantaged and SEN children, indicating that funding is responsive to need. Interestingly, some particularly high-need areas make less use of supplements than those in the middle of the pack, suggesting that the funding system provides areas with the flexibility to tailor resource allocation to the needs of the local area.

Understanding how this funding system and differences in approaches across local areas map on to measures of performance in the early years, such as availability and quality of provision, is an important next step for future research (Reed and O’Halloran, 2024).

2.3. Future changes and challenges in the early years

In this section, we return to looking at the early years system from a national perspective to assess what we know so far about the rollout of the new entitlements, to study the impact of more recent policy changes and to look ahead to considerations for the spending review.

Delivery of the new entitlements

Local authorities are responsible for ensuring there is sufficient childcare provision for eligible children to access the free entitlements. Since April 2024, this expanded to 15 hours of childcare per week for 2-year-olds from working families and, from September 2024, for children aged 9 months in working families. From September 2025, these children will be entitled to 30 hours per week.

A widely discussed issue (e.g. Drayton and Farquharson, 2023) is around the deliverability of these entitlements. A key determinant of this is the hourly funding rate the providers receive. As discussed in Section 2.1, for 2024–25 this is relatively generous for younger children (2-year-olds and under), which is expected to incentivise providers to offer the new entitlements.

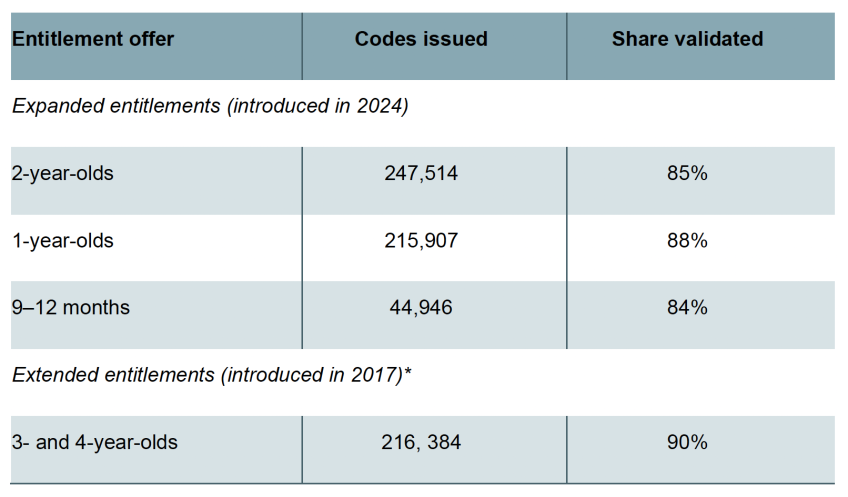

An early indication of how well the rollout is going comes from Department for Education statistics on the number of childcare codes issued and validated for the new entitlements. Codes are issued by local authorities to children who apply and are eligible for the entitlements; they are validated when children take up a place with a provider. The former offers insight into demand for the new entitlements, while the latter is a proxy for the availability of childcare provision.9 The latest release of statistics covers the full summer term 2024 for 2-year-olds, and data for the autumn term 2024 until 13 October for 2-year-olds and for children aged 9–36 months.

Table 2.2 shows, for England, the number of codes issued (representing the number of children) and the share that have been validated (demonstrating that a child has taken up a place) in the first term of eligibility for the new entitlements. The final row provides a comparison with the 30-hour expansion for 3- and 4-year-olds in September 2017. At the same point in the rollout, the share of interested and eligible children taking up childcare across the age groups looks very similar (at around 85%) and, if anything, it is slightly higher for 1-year-olds (88%). This is encouraging as the market for 1-year-olds is less established than for 2-year-olds, likely requiring more new provision rather than changes in who is paying for existing childcare (Farquharson, 2024). This is also broadly in line with take-up during the rollout of the previous 30-hour offer for 3- and 4-year-olds at 90%. Validation rates have since risen to 96% for 2-year-olds by the end of summer term 2024.

Table 2.2. Codes issued and validated by entitlement and age of child for first term of eligibility in England

Note: Using the first release of code data for the first term of eligibility to account for validation rates rising over time. For 2-year-olds, this is for summer term 2024 for codes applied for by 31 March and issued and validated by 2 May. For children aged 9–12 months and 1-year-olds, this is for the autumn term 2024 using codes applied for by 31 August and issued and validated by 13 October. * The final row provides code statistics from the previous extension of the free entitlement of 30 hours for 3- and 4-year-olds for comparison. This covers codes issued by 31 August 2017 and validated by 9 October 2017.

Source: Department for Education (2017, 2024c, 2024f).

Taken together, this suggests that the rollout, at least at a national level, is in line with previous expansions. However, as emphasised throughout this piece, childcare provision operates locally, and at this geography there is more scope for demand and supply to become misaligned.

Department for Education (2024f) analysis suggests substantial variation across the country in the percentage of codes validated for the autumn term 2024 for children aged 9–36 months. Overall, local authorities in the north of England exhibit higher validation rates (i.e. higher proportions of approved children taking up a childcare place) compared with the south. Urban areas also tend to have lower rates. Some areas in London as well as local authorities surrounding London have particularly low validation rates compared with elsewhere; for instance, in Haringey, only 74% of childcare codes have been validated, while in Birmingham the figure is 88%. This suggests that eligible and interested parents in more urban areas, particularly in the South East of England, are possibly unable to access free entitlement places or are not well matched to the places on offer.

Upcoming policy changes

The expansion of the free entitlements represents a large change to early years education and childcare in England but is also a continuation of previous government policy. Finally, we consider policies announced since the new government took office that are likely to affect the early years sector, and we look at challenges ahead for the government’s first spending review.

The first policy is capital funding for primary schools to facilitate the conversion of classrooms into nurseries. This scheme comes with a total funding pot of £15 million and can be used by schools to make adjustments to the school estate, such as changing the layout of rooms, providing additional toilets or creating outdoor play areas, in order to meet regulations for nursery provision. The first phase of the programme, which launched in October 2024, aims to support 300 new or expanded nurseries (Department for Education, 2024g), with the aim of ultimately generating 3,000 additional school-based nurseries. Once fully rolled out, this will represent around 30% of the existing number of school-based providers, although these providers currently make up only 20% of places (Department for Education, 2023a).

Additional support for expanding childcare provision will certainly be welcome, especially if the places generated are higher quality, which is an explicit aim of the policy (Labour, 2024). However, there are two key risks that could undermine the scheme’s ability to meet additional demand for childcare places as the new entitlements are expanded.

The first is around when these additional places will become available. Under current timescales, the first tranche of nursery conversions (which represent one-tenth of the target) are expected to come online for the final stage of the expanded entitlements rollout in September 2025 (Department for Education, 2024g). While this policy may generate additional capacity over the longer term, under existing plans it is unlikely to substantially ease supply constraints when they are most acute. As well as the timeliness of the policy, another consideration is where in the country the additional school-based places will become available. The policy is largely targeted at repurposing primary classrooms where pupil rolls are falling, but if there is a geographical mismatch between falls in primary school population and rises in demand for new early years provision, this could prove a challenge to delivering these nursery school targets.

Another set of policies that is likely to affect childcare providers comes from the Autumn Budget 2024. These policies include increases in the rate of employers’ NICs, albeit alongside more generous offsets for small businesses, and rises in the national minimum wage, which will take effect in April 2025.

Early years staff are essential to delivering early years education and childcare, reflected in the high share of providers’ costs that go to staffing (around three-quarters). Changes that raise the cost of employing workers can therefore have significant impacts on providers’ financial position. Moreover, the Autumn Budget 2024 changes will particularly affect younger and lower-paid workers. A full-time early years worker earning £25,000 a year would see the employers’ NICs bill rise by more than a third, while a minimum-wage worker aged 18–20 would see a 16% jump in hourly wage.

Higher wages would be welcome for many early years professionals earning at or near the minimum and could support the drive to recruit around 35,000 additional early years staff by September 2025 (Department for Education, 2024h). But together with changes to NICs, it also adds cost pressures to providers.

The impact of these changes will really depend on the type of early years provider. Most obviously, childminders, who tend to be self-employed or, if they employ an assistant, often fall within the tax-free allowance, would be much less affected. For most providers, however, what matters is the number of employees and how much they are paid. The majority of the tax increase comes through the reduction in the NIC threshold, which affects employers with lower-paid workers most in proportional terms. These are the same providers who will be most likely to be hit by increases in the minimum wage.

These impacts are somewhat offset by a more generous NIC employment allowance, which could particularly help providers with small numbers of employees, as they are unlikely to pay NICs. However, providers are not currently eligible for employment allowance if more than 50% of their business is done in the public sector, which may apply to more early years providers as the free entitlement expands over time. Two illustrative examples of providers who – if eligible for the employment allowance – would stand to benefit under the Autumn Budget 2024 changes are:

- a small provider with six employees (or fewer), each on median earnings of £33k;

- a small provider with seven employees (or fewer) on the current minimum wage.

Providers employing more staff than in these examples would lose out from the changes announced in the Autumn Budget; the bigger the employer, the more so. Although data availability makes it difficult to assess the impact on the early years sector as a whole, these illustrative scenarios highlight which sections of the market are more exposed to these financial pressures. Over the longer term, providers may be able to ‘pass on’ higher costs to workers: on average, around 60% of the impact of the NICs tax rise will eventually be felt by workers, in the form of smaller pay rises and lower wages. This adjustment will be more challenging, however, for providers with many employees at or near the minimum wage.

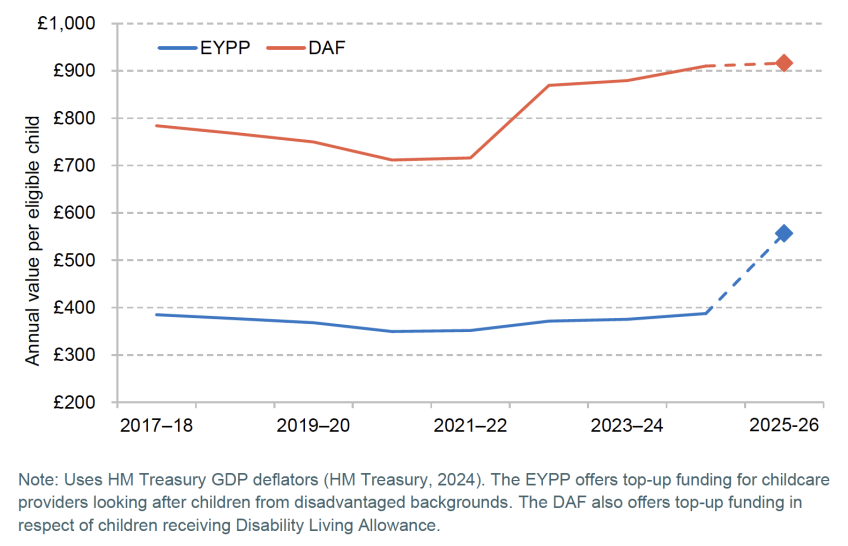

Targeted funding in the early years

Another important area of early years funding is provisions for children with additional needs, such as low-income children through the EYPP and support for SEN via the DAF. These operate differently from the funding formulas discussed earlier and provide additional payments to providers per eligible child. As shown in Figure 2.8, historically, the low frequency of updating rates has eroded the real value of these funds over time, leaving childcare providers with fewer resources to support higher-needs children. For example, the EYPP rate fell by 9% between 2017–18 and 2021–22. A funding system that is responsive to need is more important in the context of rising demand: although smaller in absolute numbers than rises for primary school age children (Sibieta and Snape, 2024), the proportion of children identified as having SEN and taking up the 15-hour entitlement rose from around 6% to 9% between 2018 and 2024, representing a 30% increase in numbers of pre-school age children with SEN (Department for Education, 2024e).

Figure 2.8. Real-terms funding for the early years pupil premium and disability access fund

Note: Uses HM Treasury GDP deflators (HM Treasury, 2024). The EYPP offers top-up funding for childcare providers looking after children from disadvantaged backgrounds. The DAF also offers top-up funding in respect of children receiving Disability Living Allowance.

In 2024–25, there has been a 9% cash-terms increase in the EYPP and DAF, as well as an extension of eligibility to younger children, and the introduction of deprivation supplements for the new entitlements (Department for Education, 2024d). Next year will see bigger changes, with EYPP rising to £570 a year, which is a 44% increase in real terms. This is a major uplift, meaning that, for the first time, the value per hour will be comparable to the pupil premium funding that schools receive for disadvantaged pupils (though because EYPP only applies to part-time childcare entitlements, the total funding will still be half as much as for schools).

2.4. Summary

The discussion throughout has raised a number of considerations ahead of the 2025 spending review. In contrast to other areas of public spending, the spending envelope has already been set for spending on early years education, including funding allocated to the new entitlements. Within this allocation, notwithstanding modest rises next year, money has been directed more towards provision for younger children (via higher funding rates) compared with 3- and 4-year-olds, leaving resources for 3- and 4-year-olds at greater risk of losing value. Tax and minimum-wage changes announced at the Autumn Budget 2024 are expected to add cost pressures to providers and exacerbate this risk. The process for setting rates has historically generated uncertainty for providers, with rates frozen for multiple years and inflation eroding their real value, followed by a big adjustment at a spending review or fiscal event (Drayton and Farquharson, 2023). The spending review would be an opportunity to consider a process for setting funding rates that is more responsive to changing financial pressures.

In terms of targeted early years funding, the rise in EYPP next year represents a major increase in real resources for children from disadvantaged backgrounds, children who are less likely to achieve a ‘good level of development’ by the end of Reception. This is particularly welcome as the new entitlements are by and large geared towards reducing the costs of childcare and helping parents into work rather than addressing inequalities in children’s development. It does, however, come on the back of multi-year freezes to EYPP, which reduced the progressivity of the early years funding system.

3. Schools

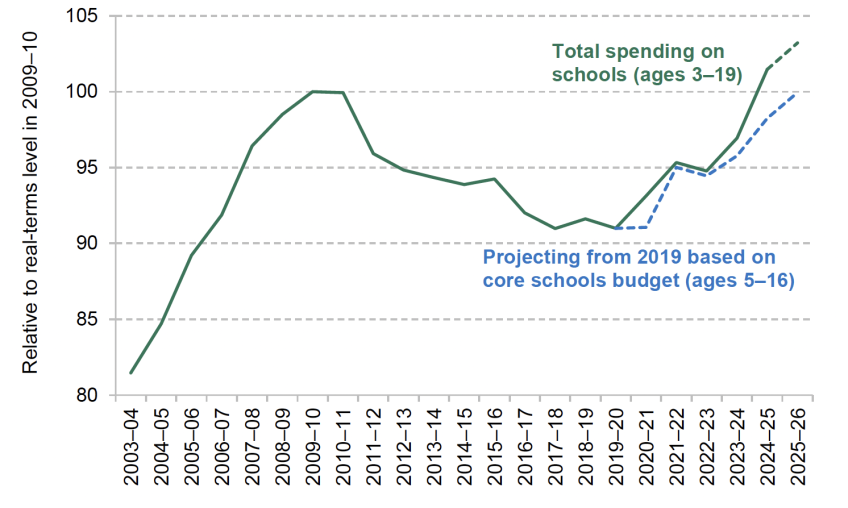

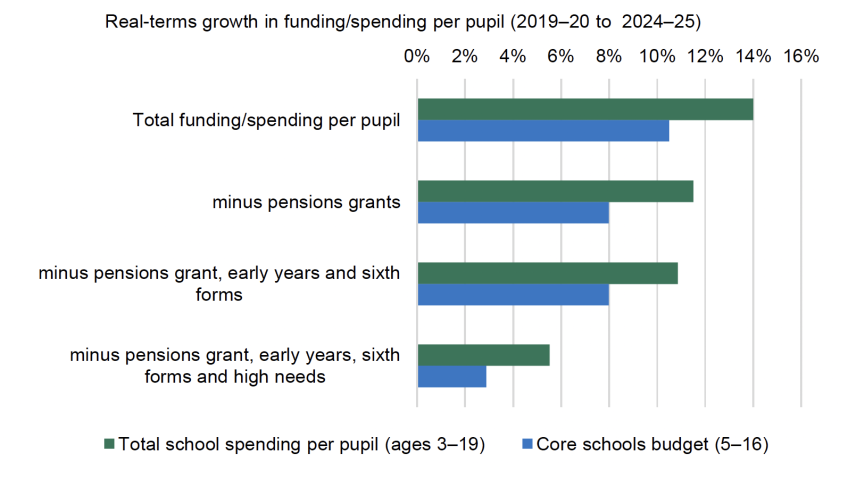

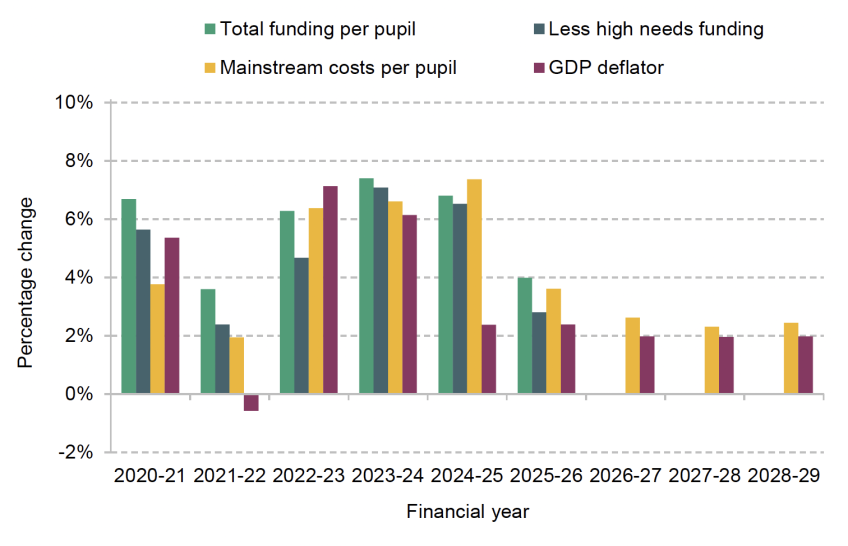

In the Autumn Budget 2024, the new government chose to increase school spending by £2.3 billion, with the core schools budget increasing in cash terms from £61.6 billion in 2024–25 to £63.9 billion in 2025–26. This allows for a 1.6% real-terms increase in spending per pupil. Coming on the back of an 11% real-terms increase in spending per pupil between 2019–20 and 2024–25, this allows spending per pupil to return to, and exceed, its previous high point in 2010. This is not the full story, however.

Out of the £2.3 billion cash-terms rise in the core schools budget in 2025–26, about £1 billion is focused on the high needs budget, which covers pupils with the highest levels of SEN and disabilities. After accounting for this, the £1.3 billion rise in the rest of the schools budget is likely to amount to a 2.8% rise in cash terms in funding per pupil in mainstream schools in 2025–26, which is a very small real-terms rise relative to economy-wide inflation of 2.4%. In contrast, we estimate that school costs are likely to rise by about 3.6%, which includes the effect of government proposals for a 2.8% pay rise. If these projections are accurate, then core school budgets will feel very tight in 2025–26.

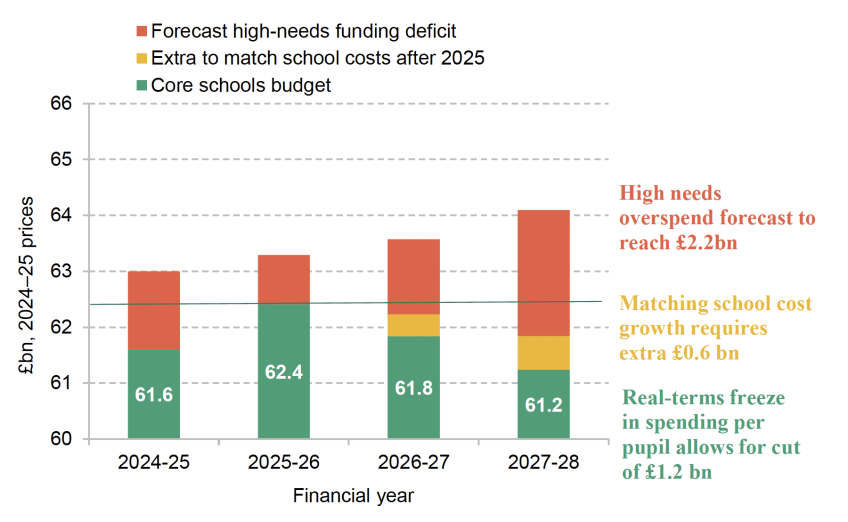

This pattern of seemingly large rises in total school spending per pupil being swallowed up by large increases in high needs funding is a familiar one. About half of the increase in total school spending per pupil between 2015–16 and 2024–25 can be accounted for by rises in high needs funding. As we document in our recent briefing note (Sibieta and Snape, 2024), this reflects rapid increases in the number of pupils with identified needs, particularly those with Education, Health and Care Plans (EHCPs). These plans create statutory obligations to provide specific support to individual children. This has pushed up spending even faster than funding, leading to large deficits across local authorities. These deficits have effectively been moved off balance sheet to prevent local authority bankruptcies. This ‘Statutory Override’ is due to run out in March 2026.

In the rest of this chapter, we present trends in spending per pupil to date and examine the potential pressures on spending in the period covered by the next spending review, particularly 2026–27 and 2027–28. For further details, on the methods used to analyse school spending, please see the accompanying ‘Methods and data’ section at https://ifs.org.uk/education-spending/methods-and-data.

3.1. Total school spending per pupil

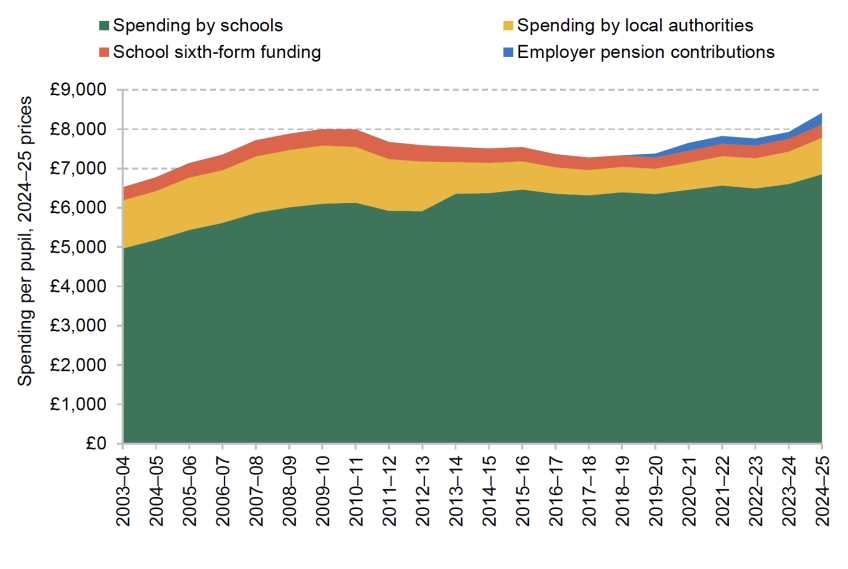

Figure 3.1 shows total school spending per pupil aged 3–19 between 2003–04 and 2024–25 broken down into four different components:

- Funding allocated to schools. This includes funding directly allocated to schools and early years providers. Early year funding for children aged 3–4 is included in primary school budgets for past years. We cannot exclude this for all years, so we include early years funding for children aged 3–4 in all years to maintain consistency. This includes funding for special schools and alternative provision. It also includes high needs top-ups and place-funding provided to state-funded mainstream and special schools.

- Local authority spending. This includes central spending on a range of services for pupils with SEN, admissions, transport and other services.

- Sixth-form funding. This is funding provided to schools for pupils aged 16–19. We include this given that it is often included within total secondary school expenditure figures.

- Extra funding for employer pension contributions. From September 2019, schools received about £1.5 billion in extra funding to meet the cost of higher employer pension contributions. From April 2024, they were provided with a further £1.1 billion to cover another increase in employer pension contributions. We often present figures with and without this extra funding for comparisons over time as the funding was directly intended to compensate schools for higher costs.

Combining all these factors, we calculate total school spending as nearly £70 billion in 2024–25, or nearly £73 billion if we include all recent employer pension contribution grants. This is higher than the core schools budget for England presented by the government, which was £61.6 billion in 2024–25 (this covers school funding for pupils aged 5–16). This can be mostly explained by the fact that we include £3 billion in post-16 funding and over £4 billion in early years funding, as well as additional services provided by local authorities that are funded through the wider local government settlement. However, as we shall show directly below, our measure appears to show faster growth in total school spending per pupil in 2024–25 than the core schools budget on what should be an equivalent basis.