From the start of September, children as young as nine months will be eligible for funded childcare in England. This second stage of the roll-out of new childcare entitlements will for the first time see children under age 2 receiving the ‘free entitlement’ to a part-time childcare place, covering up to 15 hours a week 38 weeks of the year.

All 3- and 4-year-olds are already eligible for a part-time childcare place, and those whose parents are in paid work can get up to 30 hours a week of free childcare. Since April this year, the part-time entitlement has been extended to 2-year-olds in working families (in addition to a pre-existing entitlement for the roughly 25% most disadvantaged 2-year-olds, whether their parents work or not). The September 2024 change will extend part-time eligibility to younger children aged 9 months and up, before these ‘working families’ entitlements double to 30 hours a week in September 2025.

What are the aims of the new entitlements?

The main aim of these new entitlements is to reduce childcare costs for working parents, and therefore to encourage more parents to enter (or stay in) paid work. However, the government’s business case argues that around 60% of the financial benefits from the new entitlements will come from better child development and educational outcomes for the children attending these settings.

How will the new entitlements be funded?

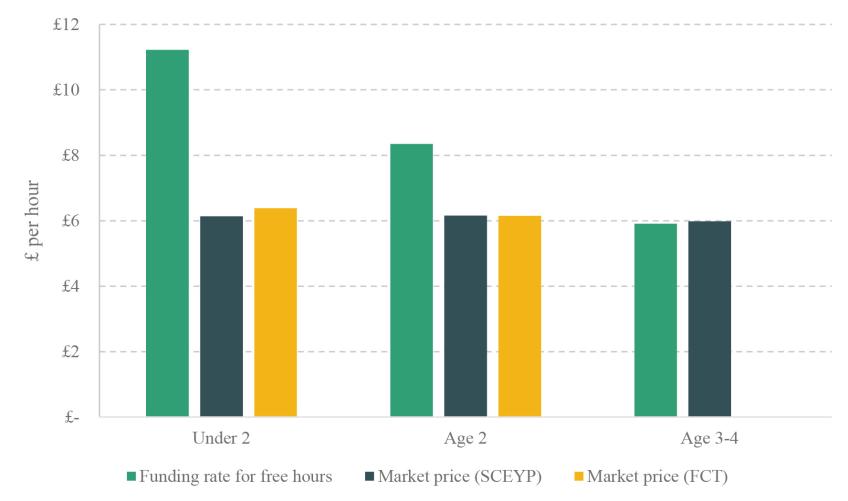

As Figure 1 shows, childcare providers traditionally try to ‘smooth’ the cost of childcare across age groups – charging a relatively similar amount for all pre-school-aged children. But the costs of childcare look very different across age groups; staff-to-child ratios are much tighter for younger children, so the cost of delivering care to the under-2s is much higher than the cost for 3- and 4-year-olds.

By contrast, core funding for the free entitlement aims to more closely reflect underlying costs, so funding rates are much higher for younger children. Even more striking from Figure 1 is how generous these funding rates look compared with market prices. Funding for the under-2 entitlements is set to be £11.22 per hour on average, compared with a market price of childcare of around £6.40 an hour. Funding for 3- and 4-year-olds is much closer to its market price (and has fallen over time in real terms), but even so this funding landscape should mean that – at the national level – the average provider will not lose out from offering these entitlements.

Figure 1. Comparison of childcare funding rates and market prices

Note: SCEYP prices are drawn from 2023 and converted into current prices using CPIH inflation data.

Source: Based on figure 2 of Farquharson (2024). Dedicated schools grant, 2024-25. Survey of Childcare and Early Years Providers (2023). Family and Childcare Trust’s ‘Childcare Survey 2024’.

How will the new entitlements for under-2s affect families?

The first, most obvious effect of the new entitlements will be to change who pays for formal childcare that eligible families were planning to use anyway. This is a straight transfer, with government picking up the tab for childcare hours that parents would otherwise have paid for themselves. Since childcare costs are highest for the youngest children, the value of this new support could be substantial; based on the average price that parents pay for childcare in England, the new entitlements could be worth £3,600 per child a year. (And, at the funding rate paid by the government, the value is closer to £6,400.) Here, the main effect of the new entitlements will be to change families’ financial circumstances, rather than directly altering parents’ employment outcomes or children’s development.

By lowering the price that parents pay for childcare, the new entitlements will also boost demand for formal care. Some of this will come from families already using formal childcare who want to increase their hours; some will come from families who are already working switching from informal to formal care; and some will come from families newly incentivised to take on paid work. By increasing the amount of formal childcare being provided, the new entitlements will have a more direct impact on children’s development, and potentially on parents’ employment outcomes.

The balance between these two ‘channels’ will be crucial for understanding where the biggest benefits of these new entitlements will be, and how deliverable they will be for the childcare market. In a world where many more families are in the first group (saving money rather than switching behaviour), the burden on the childcare market will be lower, but the overall benefits for child development and employment will be more muted.

It is impossible to know at the outset how many families will be in each of these groups. Our analysis, based on projections from the Office for Budget Responsibility, suggests that by the late 2020s around 85% of childcare hours funded through the new entitlements would have happened anyway, with parents paying out of pocket. But there are huge uncertainties around this number.

Who currently uses formal childcare before age 2?

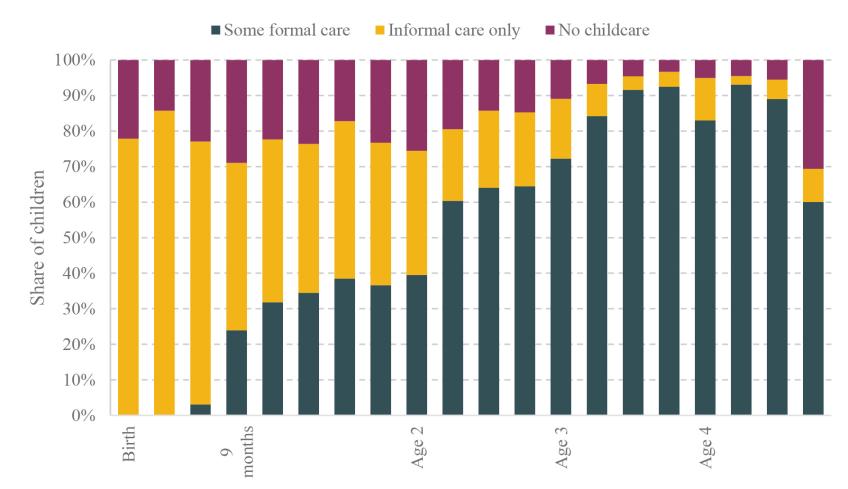

To get a handle on how big the group of potential ‘savers’ might be, we can look at families that are already using and paying for formal childcare. Based on data from 2019 (the latest available information that lets us split out under-2s from slightly older children), around a third of children aged 9 months to 2 years are already using formal care. A further 44% are using informal childcare.

Figure 2 shows that almost no families use formal childcare for children under 9 months (who will not be covered by the new entitlements). By contrast, the share of children in formal care jumps up just after age 2, potentially driven by existing entitlements for disadvantaged 2-year-olds. A few months after turning 3, more than nine in ten children are using formal childcare.

Figure 2. Childcare arrangements, by child’s age in quarters (2019 data)

Note: Child’s age is grouped into quarters (three months). Sample sizes for very young children (0–5 months) and for 4-year-olds (final four quarters of data) are somewhat smaller and so estimates are less reliable.

Source: Authors’ calculations using Childcare and Early Years Survey of Parents (2019).

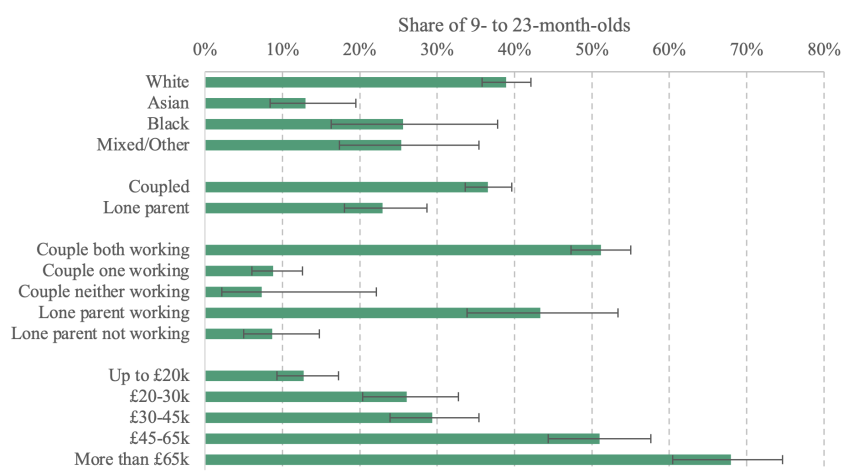

Figure 3 shows that there are big differences in the families with children aged between 9 months and 2 years using and not using formal childcare. While nearly 40% of White families are using formal childcare, fewer than 15% of young children from Asian backgrounds are in formal care. Coupled parents are also significantly more likely to be using formal childcare than lone parents.

But, as the third section of Figure 3 shows, this is driven almost entirely by working patterns: fewer than 10% of families where at least one parent is not in paid work are using formal childcare, compared with 43% of working lone parents and 51% of couples where both adults work. Relatedly, families with a higher (gross) income are much more likely to use formal childcare.

Taken together, this means that the group who will save the most on their existing childcare costs as a result of the new entitlements will be families with relatively higher incomes.

Figure 3. Share of children aged 9–23 months using formal childcare (2019 data)

Note: Capped lines show the 95% confidence intervals. Income figures relate to gross household income and are in 2019 prices.

Source: Author’s calculations using Childcare and Early Years Survey of Parents (2019).

Who might want to start using formal childcare for under-2s?

The new entitlements are intended to change families’ behaviour as well as supporting those already using formal childcare with their costs. But it is not at all clear to what extent this will happen. On the one hand, introducing a childcare entitlement from the end of parental leave might encourage parents – especially mothers – to stay more connected to the labour market, and return to their job rather than taking time out of paid work.

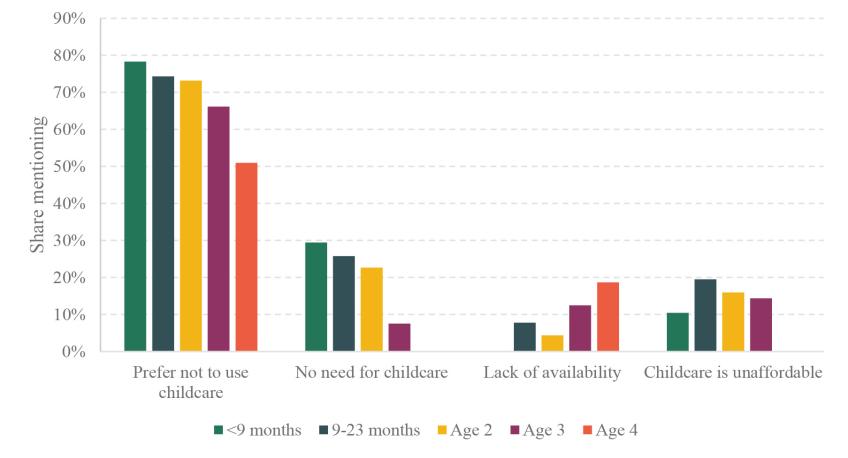

On the other hand, families’ decisions – especially for very young children – are shaped by their preferences for childcare arrangements. Figure 4 shows some of the reasons why families report not using any childcare (formal or informal) for pre-school-aged children. At all ages, the most common reason by far is preference: three-quarters of those with a 9- to 23-month-old report that they prefer not to use childcare. By contrast, a fifth cite issues with affordability, and fewer than one in ten cite lack of access. (Parents could identify as many reasons as they wished.) This suggests that there are real constraints in the childcare market, but attitudes and preferences are potentially more important.

Figure 4. Reasons for not using any childcare (2019 data)

Note: Sample only includes families who did not use any childcare (formal or informal) in the past year. Respondents could select multiple answers. This chart aggregates some similar response categories.

Source: Author’s calculations using Childcare and Early Years Survey of Parents (2019).

Will new childcare places be available for families?

On balance, then, it seems likely that most of the places delivered through the ‘new entitlements’ will not actually be new – they will be childcare places (or hours) that parents would otherwise have paid for themselves. This is especially true for the 2024 stages of the roll-out, since part-time places are expected to have less impact on families’ choices and behaviour than the full-time care that will start from September 2025. For these childcare places, the key question is whether providers will be willing to sign up to the free entitlement system. This will be made substantially easier by the very generous funding rates for under-2s shown in Figure 1.

Nevertheless, there will be some demand for new childcare places. The Labour government promised during the election campaign to deliver 100,000 new places in school-based nurseries, but the timelines and details for this are still unclear. More broadly, the government’s approach is ‘if you fund it, they will come’: the assumption is that setting a generous funding rate will incentivise providers to enter the market or to expand their business.

There is sound logic behind this approach. In a November 2023 survey (the latest representative data available), around 40% of providers said they would likely offer more places to under-3s (a further 14% did not know). In addition, 17% of providers who do not currently look after under-3s said they would likely start offering places for this age group.

But there are also risks. Since childcare operates in many very local markets, a misalignment between funding and costs in one area could have a significant impact on the local childcare market. Providers might also be uncertain of how much funding they will actually get (national rates govern overall funding levels, but local authorities make the final decision on how much individual providers will receive). And even at the national level, providers might be sceptical of how funding rates will evolve in the future; rates for the existing entitlements have often been frozen in cash terms for several years, while their real-terms value is eroded.

What about the childcare workforce?

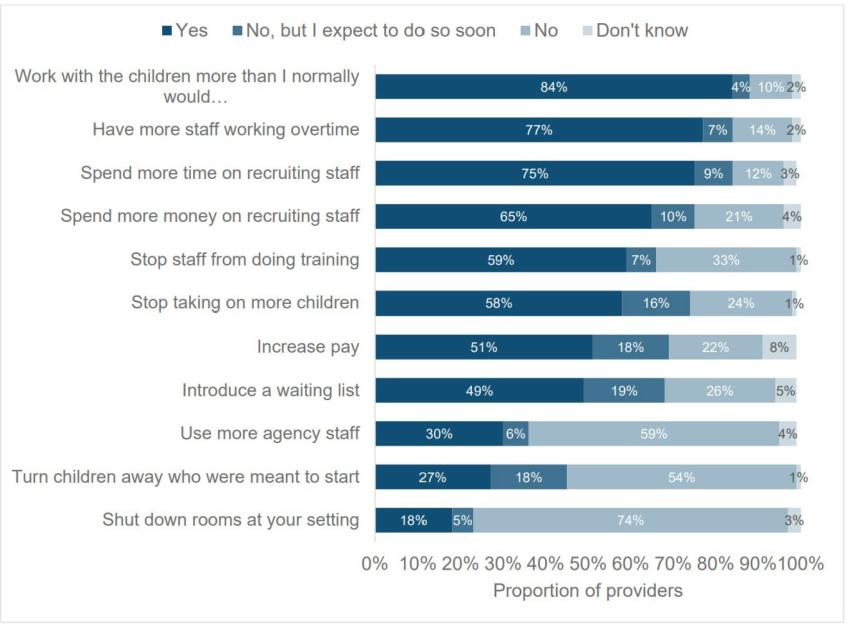

The biggest concern that early years providers raise, though, is workforce. In November 2023, two-thirds of providers said they had experienced staffing issues in the past year. There are problems both with recruitment and retention: around 30% of providers with a vacancy received no applications at all. And around 20% of childcare workers leave their jobs each year, twice the rate for school teachers.

The most common reason for leaving is to look for better pay; half of staff quitting nursery settings cited this. But, as Figure 5 shows, just half of providers experiencing staffing issues had increased pay. These data come from November 2023, before many providers had been informed about the funding their setting would receive for delivering the new entitlements. But with much more clarity since then about the funding rates for younger children, it is difficult to see a route to successful delivery that does not involve providers using some of this uplift in resources to increase wages to attract and retain staff.

Figure 5. Actions that group-based providers have taken as a result of staffing issues

Note: Based on data collected in November 2023.

Source: Figure 5 of Department for Education (2024), ‘Pulse Survey of Childcare and Early Years Providers’.

Authors

Christine Farquharson

Christine's research examines inequalities in children's education and health, especially in the early education and childcare sector.

More from IFS

Understand this issue

Policy analysis

Academic research