Rachel Reeves made a number of big choices in her first Budget.

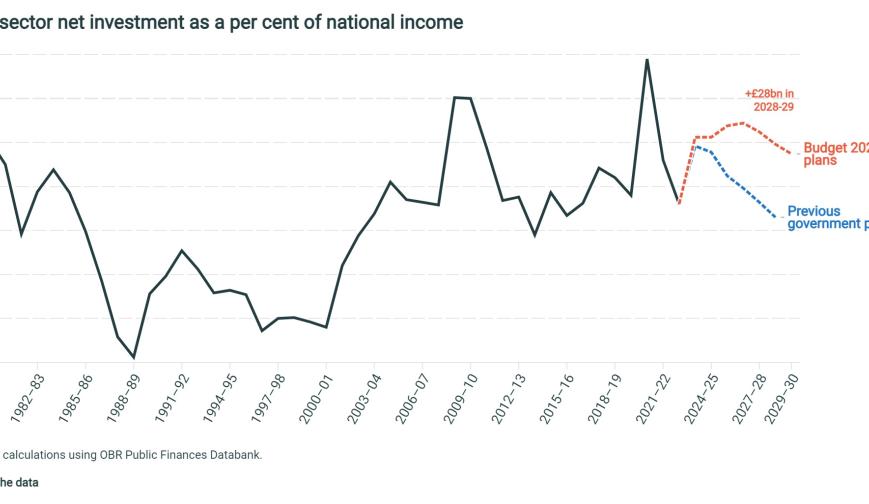

She chose to increase borrowing in order to increase investment spending – or at least to stop it falling as a fraction of national income. Given that the growth benefits of this take some time to arrive, this is a courageous move and a welcome focus on the long term. This was the right thing to do.

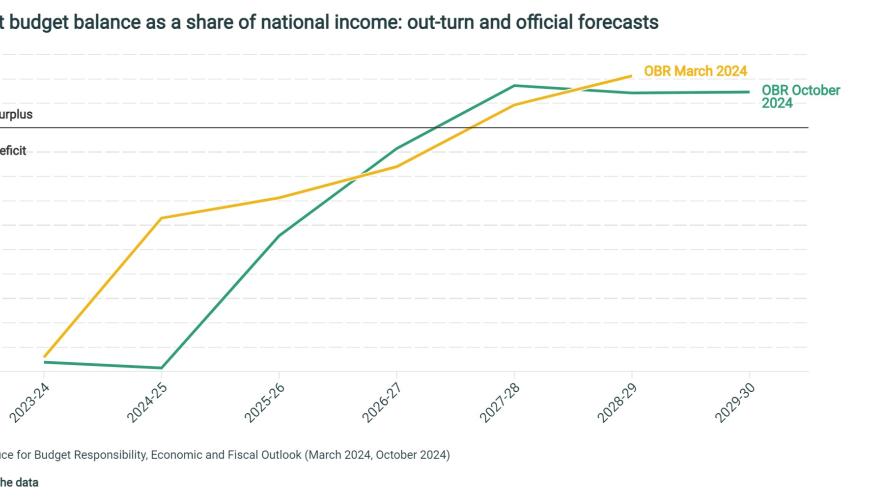

She chose a sensible new primary fiscal rule – that the current budget should be in balance in five years’ time, with that shortening to a three year rolling target after 2026-27. She chose to keep the rather less sensible rule that debt should be falling in the same year of the forecast, but redefined debt to a measure which will treat the National Wealth Fund more favourably, and more generally gives her a bit more headroom to borrow for additional investment.

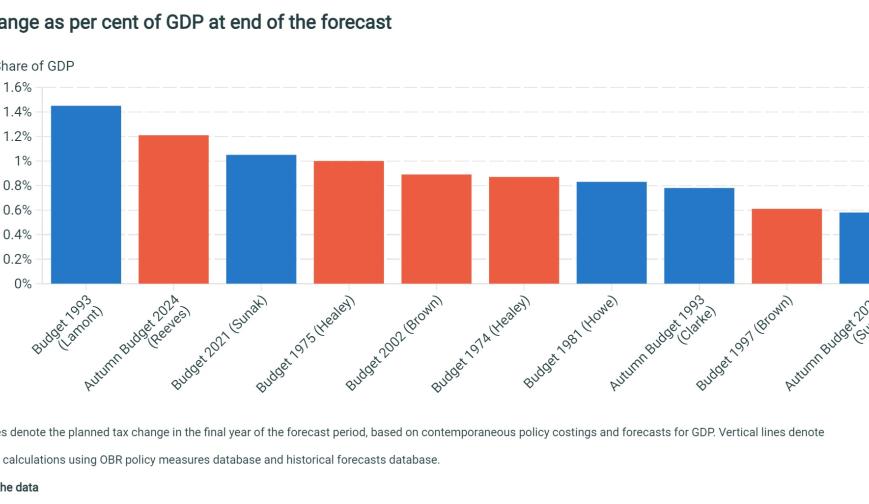

She chose to increase taxes (on the scorecard at least) by an historically big £40 billion or so, with most of that coming from employer NI. That – and an increase in borrowing – allowed her to choose to increase day to day public service spending substantially this year and next, though not thereafter.

The increases in spending look big relative to the previous government’s plans, but that is in large part because their plans were unrealistic. Despite the apparent scale of the increases, this is not going to feel like Christmas has come for the public realm. Ms Reeves may be overegging the £22 billion black hole, but she is not wrong to stress that she got a hospital pass on the public finances.

That’s the big picture. As ever my colleagues will take you through the detail. I want to bring out what I think are the most important aspects of these choices and the risks that Ms Reeves still runs.

Spending

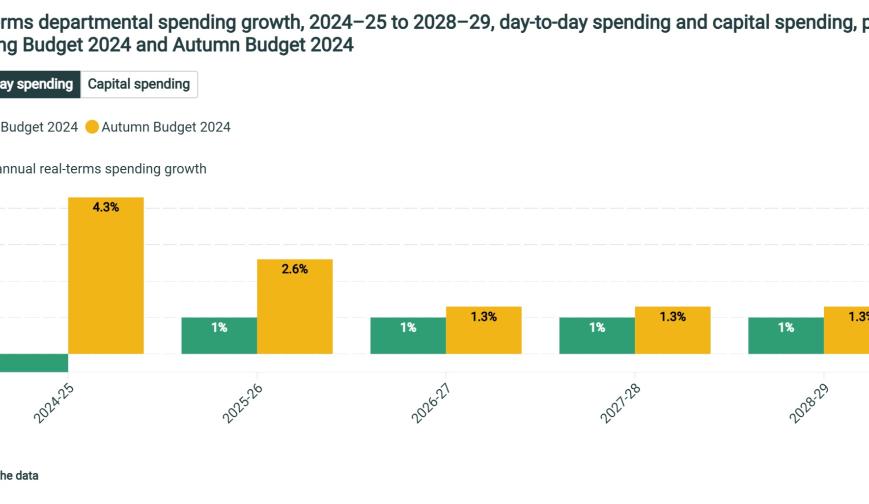

Much the most striking aspect of the spending decisions is how incredibly front loaded the additional spending is. Day-to-day public service spending, after inflation and the additional cost to public sector employers of rising NI, is set to rise by 4.3% this year and 2.6% next year, but then by just 1.3% each year thereafter.

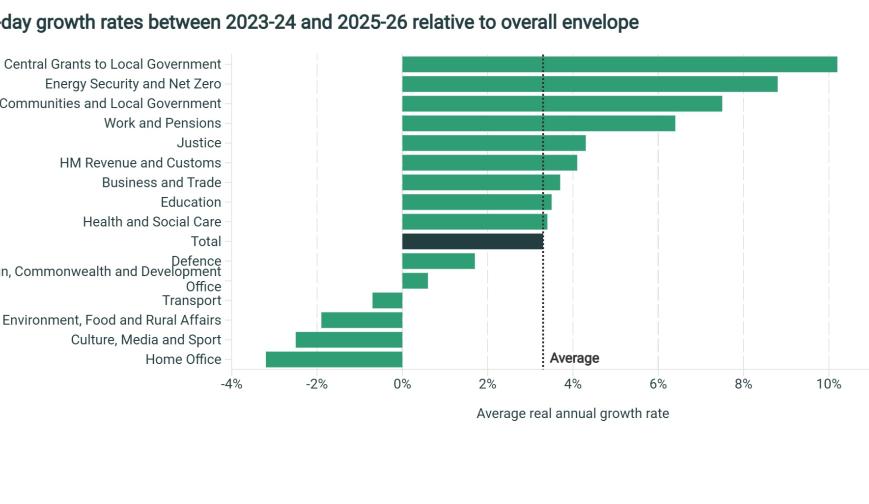

Unusually the NHS is not scooping the pool. It is getting about the average spending increase. Equally unusually local government is doing rather well, as is the justice department, reflecting the severe pressures each is facing.

I am willing to bet a substantial sum that day-to-day public service spending will in fact increase more quickly than supposedly planned after next year. 1.3% a year overall would almost certainly mean real terms cuts for some departments. It would be odd to increase spending rapidly only to start cutting back again in subsequent years.

I’m afraid this looks like the same silly games playing as we got used to with the last lot. Pencil in implausibly low spending increases for the future in order to make the fiscal arithmetic balance. It sounds like it was hard enough to get agreement from departmental ministers to relatively generous settlements in the short term. When it comes to settling with departments for the period after 2025-26 keeping within that 1.3% envelope will be extremely challenging. To put it mildly.

Overall, between 2023-24 and 2029-30 RDEL is due to grow by 2.1% a year. To put that in some perspective Rishi Sunak planned – though did not achieve – RDEL growth of 3.3% a year when, as Boris Johnson’s Chancellor, he set out the 2021 spending review. It grew by 4.4% a year between 1998–99 and 2007–08.

Perhaps even more surprising is the fact that capital spending, at least in the published plans is front loaded. More likely than not there will be underspends, with unspent budgets being pushed into later years.

Note also that some areas where one might expect a lot of additional capital if growth is the focus have not done well. The Department for Transport’s capital budget is being cut over this year and next, for example. The Department for Energy Security and Net Zero is the biggest winner in terms of extra cash. That should help us deliver our climate ambitions, but it is less clear that all green investments will add to the supply-side capacity of the economy – in some cases we’ll producing the same stuff, just more cleanly. That’s valuable. But it isn’t growth enhancing. Increased capital for health and education, of which there is quite a lot, should help improve public services. Again that is valuable but it may not be so different from day to day spending in terms of its growth impact.

To be clear, the focus on investment and on the long term is welcome. But there are some important details to be filled in at the spring Spending Review, and it remains to be seen the extent to which this additional investment will be laser-focused on growth.

Taxes

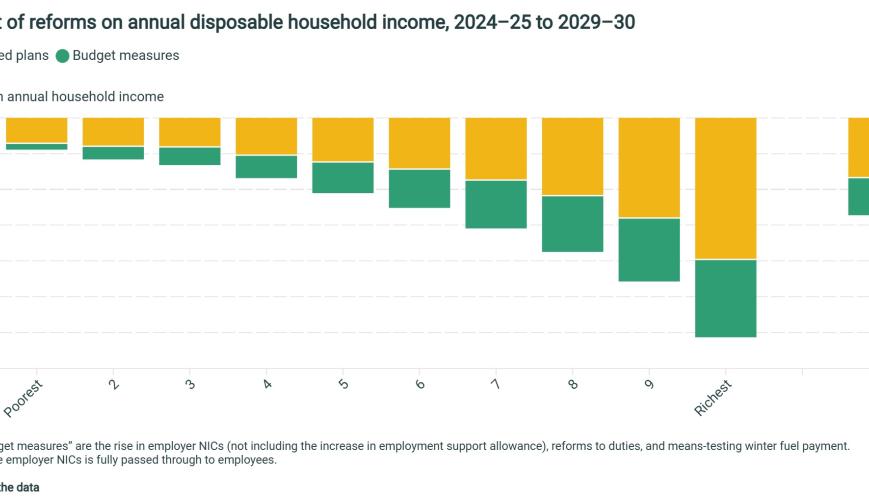

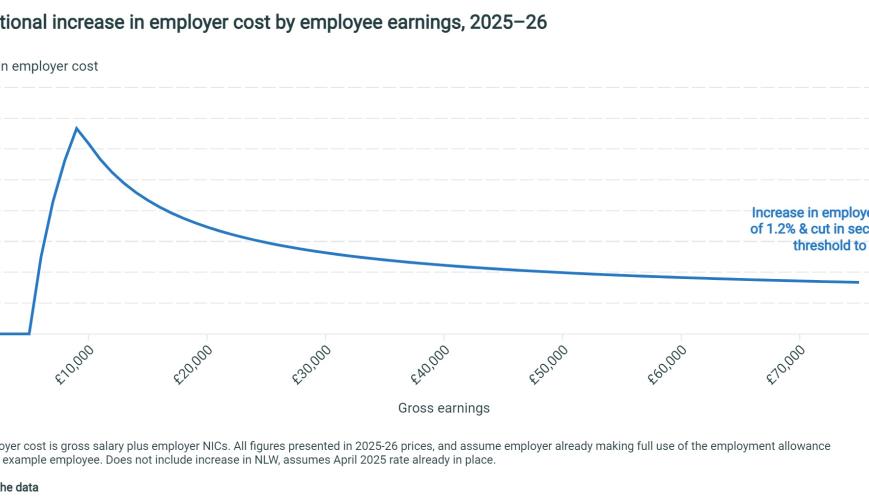

We are all by now aware that employers National Insurance contributions (NICs) are set to rise, and to rise a lot. Given the scale of the tax rise required it was inevitable that one of income tax, VAT or NICs would have to increase in order to pay for higher spending, and so it has transpired. Choosing employer NICs has some downsides. They are of course largely incident on wages. Increasing them increases the wedge between employment and self-employment, and between employment income and other income. But this is a better choice than trying to get big increases from a range of smaller taxes.

It is also worth noting that, net, this increase will not actually get the Treasury anything like the £25 billion stated on the scorecard. As the OBR note, it will result in lower wages, reducing the amount raised from employer NI and reducing employee NI and income tax revenues. That takes the net revenue down to some £16 billion. On top of that there will be an effective £6 billion of compensation for public sector employers.

As for the rest of the tax changes, I will only say that the lack of any apparent strategy or appetite for reform is deeply disappointing. Unlike the coalition’s corporate tax “road map” the one published yesterday is more of a parking space – an ambition not to take a big journey in any direction. That the chancellor decided to increase stamp duty, if only on second properties, is most disappointing of all. It again reduces transactions, increases again the bias in favour of owner occupation, and against renting, and at least part of the consequence will be to reduce the supply of rental housing and so increase rents. The failure to increase rates of fuel duties in line with inflation, and pretend that it will rise in the future, continues the absurd behaviour of Chancellors past. CGT has been increased but not, as is so desperately needed, reformed. More encouragingly the changes to inheritance tax are broadly sensible, though it might take some political courage to see off the inevitable special pleading from those affected.

If this government really wants to focus on growth, then part of the plan needs to be a much more coherent tax strategy than we saw yesterday. Let’s hope for better next year.

Public finances

The remarkable thing is that despite all that extra tax, and despite the tight spending plans pencilled in for the period after 2026, the public finance numbers still look shaky – again a reflection of the desperately difficult inheritance.

Borrowing is up relative to forecasts. The new fiscal rules for borrowing and debt are still met only by small margins.

The new rule that the current budget should balance is met by a margin of just £10 billion. Recent increases in interest rate expectations and likely failure to increase fuel duties – costing £5 billion a year by the end of this parliament – would wipe out much of that headroom. We estimate that you’d need an extra £9 billion or so to avoid cutting unprotected departments after next year. Take those together, and you’ve more than wiped it out.

The new measure of debt, PSNFL, is due to fall in the fifth year of the forecast, but by only £16 billion. That is a small amount. PSND (ex BoE), the measure targeted by the last government is due to increase slightly in every year of the forecast, while plain vanilla PSND is broadly constant.

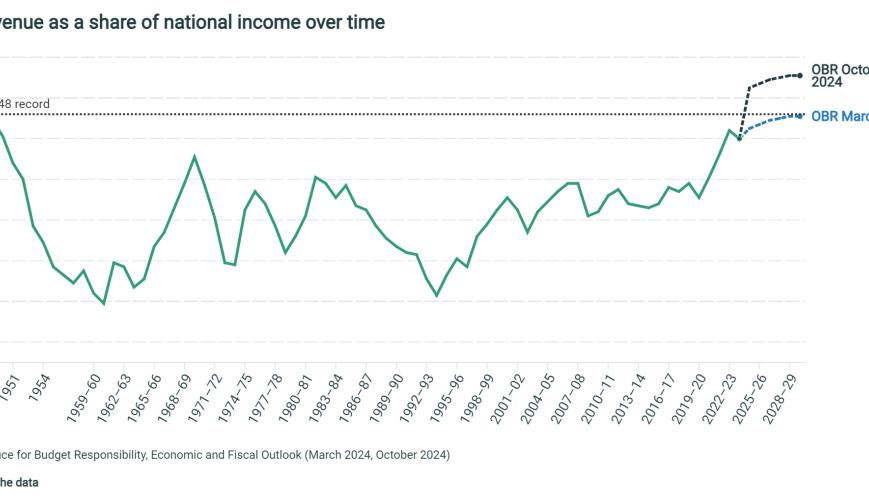

All this despite the fact that taxes are set to rise from 36.4% of national income today to 38.2% by 2029-30 – an all time high for the UK. That is a remarkable 5% of national income higher than pre pandemic. This is the decade of higher taxes. Meanwhile spending in 2029-30 will also be 5% of national income above its pre pandemic level. The state has grown, and it seems unlikely to shrink again anytime soon. As we have said time and again, absent radical surgery to the welfare state for which there is no apparent political or public appetite, this always looked inevitable irrespective of which party was in office.

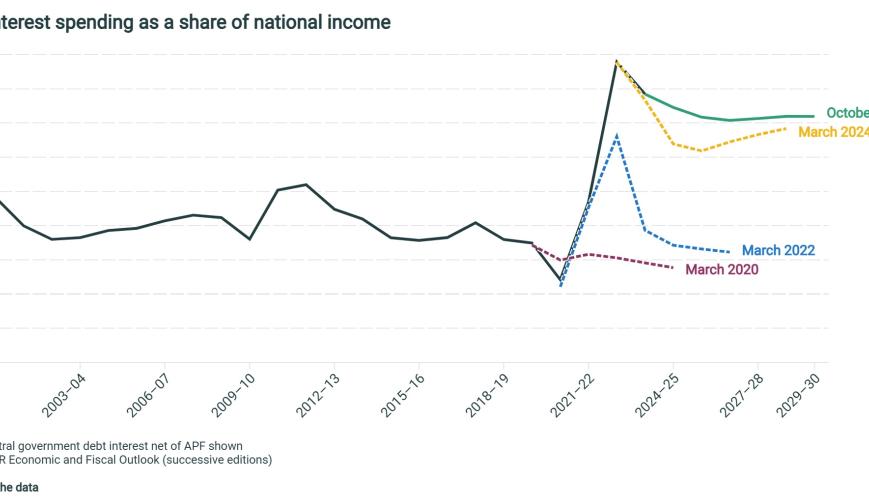

Another big part of the problem is elevated spending on debt interest. It is due to come in at around 3.5% of national income, or more than £100 billion each year – that’s about 1.5% of national income more than it averaged over the two decades to 2020. The OBR has revised up its view of likely debt interest payments by about £12 billion a year compared with its March forecast, largely because of higher borrowing, higher inflation and higher interest rates resulting from decisions taken in this Budget. We need to run substantial primary surpluses to avoid debt running away.

Assessment

Rachel Reeves was faced with a genuinely difficult inheritance and the last government must take a lot of the responsibility. Its spending plans for this year and for the future lacked credibility. To cut £20 billion from employee National Insurance last year in the face of known fiscal pressures was not responsible.

Ms Reeves has responded by increasing taxes, spending and borrowing, taking the former to record levels. Changing the fiscal rules to allow more investment is probably sensible, and the extra investment should boost long term growth if it is well spent. It is good to see such a focus on the long run.

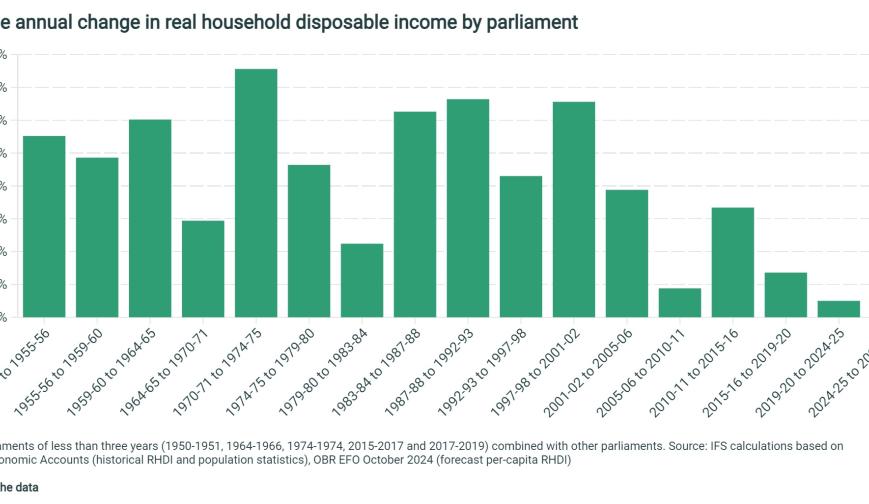

Set against an ambition to achieve the fastest economic growth in the G7 over this parliament though there was little in the Budget itself. Delivery may come later – through planning reform, reform to trade and competition rules, an enhanced industrial strategy, tax reform in the next Budget. All that remains to be seen. Worryingly for the government, and indeed all of us, the OBR has reduced its forecast of household income growth, and expects income growth over this parliament to be lower than over any other parliament in modern times – except the last parliament. Not a recipe for a happy public come the next election.

There will be more to come. There is almost no wiggle room against the two new fiscal targets. Even after changing the definition of debt Ms Reeves has almost as little headroom against her debt target as Jeremy Hunt had against his. She is meeting her borrowing target only by repeating the same silly manoeuvres as her predecessors used to make it look as if the books will balance. Let’s pretend we’ll increase fuel duties next time, but not do it this year. Let’s pretend that we’ll really rein in spending in a couple of years after splurging this year. That’s not going to happen. The spending plans will not survive contact with her cabinet colleagues.

Also disappointing is some of the presentation – even after the “conspiracy of silence” entered into during the election campaign. How the Budget red book can include the sentence “it [the government] is not increasing the basic, higher or additional rates of income tax, National Insurance contributions or VAT” is beyond me. The continued pretence that these changes will not affect working people risks further undermining trust. To produce a distributional analysis which includes the positive effects of higher public service spending whilst excluding the effects of the increase in employer NI just will hardly enhance the credibility of the exercise. And that’s on top of the fuel duty and future spending fictions mentioned above.

Ms Reeves may also want to reflect on the damage done by having allowed various rumours to circulate for so long. If there was never any intention to change the income tax treatment of pensions then my goodness she should have said so, rather than allow so many to cash in lump sums early. If she is done with CGT she should say so. If she has plans then better to be explicit about them than to allow another year’s worth of speculation.

This budget did signal a change of policy direction. But if the government is really wanting change then it’s not just the levels of tax and spending it needs to look at, it’s how it prepares a coherent strategy, how it presents what it is doing, and how it builds confidence through transparent communication.