In her recent speech at the 2024 Labour Party conference, the new Chancellor Rachel Reeves promised that the fiscal event on 30 October will be a ‘Budget for investment’. She said that ‘growth is the challenge and investment is the solution’ and declared that ‘it is time that the Treasury moved on from just counting the costs of investments, to recognising the benefits too’. This has fuelled widespread speculation about how a substantial top-up to investment plans might be reconciled with the new government’s manifesto promise that ‘debt must be falling as a share of the economy by the fifth year of the forecast’.

One suggestion is that the government might adopt a looser debt target than the one adopted by the previous government, to allow for more borrowing for investment while staying within the letter of the fiscal rules.

In all of this, it is important to stress the distinction between the case for more investment and the case for more borrowing for investment. The government could, if it wished, offset any increase in investment through higher taxes, or through lower spending elsewhere (e.g. on public services or social security), and avoid the need for additional borrowing. That is, as Ms Reeves put it herself in her Mais Lecture, the government could ‘prioritise investment within a framework that would get debt falling as a share of GDP over the medium term’. It is perfectly coherent to think that the UK government should invest more, but that this should not be paid for through higher levels of borrowing.

Here, we put that debate to one side, and proceed on the assumption that the government does, for better or worse, wish to relax the fiscal rules to allow for more borrowing for investment. We consider some of the options available to the government, and the key issues and questions at hand in each case.

The key point is that there are advantages and disadvantages of each possible change (some, such as a target for public sector net worth, come with particularly large disadvantages) and no unambiguously ‘right’ answers. It is nonetheless hard to escape the suspicion that the government is attracted not by any theoretical advantages of a change in the debt rule, but by the fact that it would allow for significantly more borrowing for investment without any need for tough choices elsewhere. Rather than hide behind a technical change, if the government believes there is a principled case for more borrowing for investment, it should make it. This could be accompanied by a change in the debt rule to provide new, higher limits on borrowing and an indication of the government’s logic. Yet a large fiscal expansion would not be without risks, and impacts of debt and debt servicing costs cannot be disregarded entirely. Ensuring that the investment funded by that borrowing is – and is widely seen to be – spent well will be crucial.

What might it mean to recognise the benefits of investment?

It was not entirely clear what Ms Reeves meant when she said that ‘it is time that the Treasury moved on from just counting the costs of investments, to recognising the benefits too’.

One option would be to place a greater focus on the potential benefits of public investment in terms of the impact on the economy’s productive potential. A recent Office for Budget Responsibility (OBR) paper set out in detail how the OBR plans to model the supply-side benefits of public investment going forward. Two key points are worth drawing out. First, the OBR’s estimated effects are not huge, and not large enough for investments to be self-financing for many years. Second, many of the supply-side benefits are expected to materialise only in the longer term, beyond the government’s current five-year forecast horizon. A permanent, sustained 1% of GDP increase in government investment is estimated to increase potential output by 0.4% after five years and by 2.4% after fifty years. The return to the exchequer would be smaller, given that the government would recoup less than half of this in additional tax revenues. In light of this, HM Treasury may wish to publish its own analysis on the potential benefits of investment projects, particularly where it considers that the returns are likely to be greater than those set out by the OBR for ‘average’ public investment, or where it is willing to take more of a ‘punt’ on certain kinds of investment.

In addition, the government may wish to consider a forecast horizon of longer than five years when thinking about the profile of debt, in order to allow for more of the benefits to materialise. One risk here is that a promise to have debt falling in (say) ten years’ time is even more susceptible to gaming (e.g. promises to raise taxes or cut spending only after the next election) than a promise to have debt falling in five years’ time. A longer forecast horizon might also make longer-term demographic- and climate-related fiscal pressures more explicit, and harder to ignore, meaning that a longer-term fiscal target is not automatically easier to meet.

Another option would be to consider alternative measures of the government balance sheet that attempt to capture more of the government’s assets as well as its liabilities. This would reflect the ‘benefits’ of investment in that it would capture the assets created through that investment as well as the liabilities (debt) taken on to fund it. The next section considers some of these alternative measures.

Different debt and balance sheet measures

The previous government’s debt target required that public sector net debt excluding the Bank of England (PSND ex BoE) be falling as a share of national income between years 4 and 5 of the forecast. This measure of debt, sometimes called ‘underlying debt’, strips out the contributions of the Bank of England’s balance sheet – most notably the loans made by the Bank to large companies under the Term Funding Scheme.

The Labour manifesto declared that ‘debt must be falling as a share of the economy by the fifth year of the forecast’, but did not specify which measure of debt. The new government may wish to choose a measure other than PSND ex BoE. Previous governments have targeted ‘headline’ public sector net debt (PSND; see this previous IFS Green Budget piece for a detailed explanation of the difference between PSND and PSND ex BoE). Alternatively, the government could decide to strip out further components from the measure of debt used in its fiscal rule. Examples of debt the government may want to exclude from consideration include any debt taken on by publicly owned or underwritten banks such as the new ‘National Wealth Fund’, or any valuation losses associated with the Bank of England’s quantitative easing programme.

Or, if the government is keen to recognise better the benefits of investment as well as the costs, it could target a broader measure of the government balance sheet. One option would be to target public sector net financial liabilities (PSNFL). Another would be to target public sector net worth (PSNW).

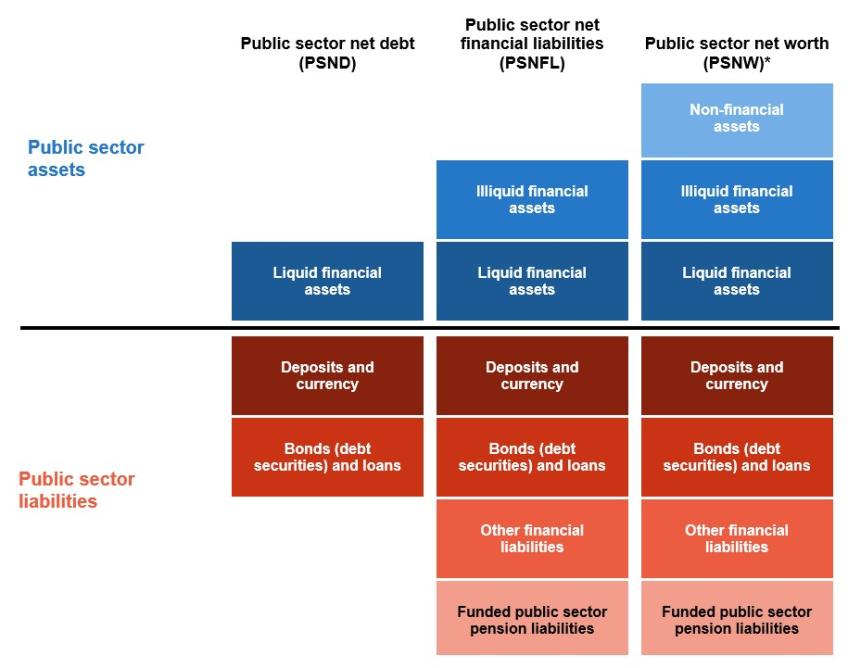

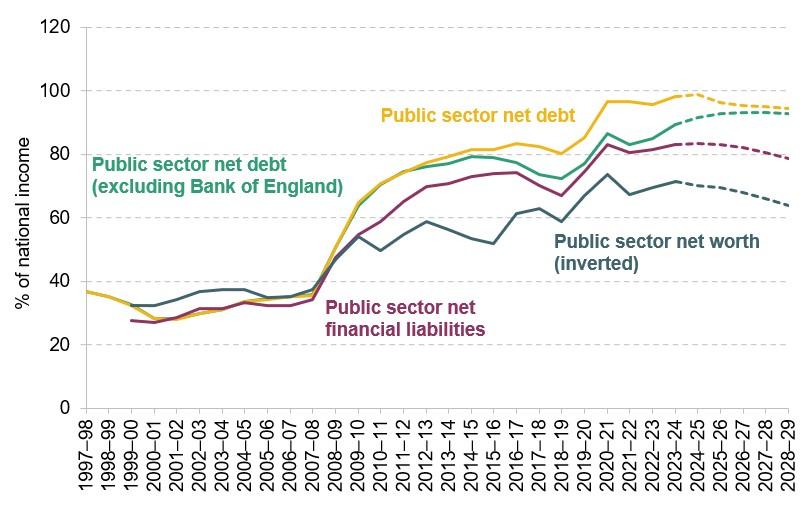

The differences between PSND, PSNFL and PSNW are summarised in Figure 1. PSND nets off the value of liquid financial assets (those that can readily be converted into cash, such as foreign exchange reserves) from the value of the national debt (defined as the public sector’s loan liabilities, debt securities, currency and deposit holdings). PSNFL provides a slightly broader picture, by also including illiquid financial assets (such as the student loan book, and the assets held by funded public sector pension schemes, which are less easy to convert into cash) and a broader range of financial liabilities (such as the liabilities associated with funded pension schemes). PSNW provides a broader picture still, by also including the estimated value of non-financial assets (such as buildings, roads and other transport infrastructure). Some measures of PSNW also include the liabilities associated with unfunded public sector pension schemes – which in the UK is most public sector pension schemes – but these are not shown here for simplicity. Figure 2 shows the evolution of these measures since 1997–98, including the March 2024 forecast.

Figure 1. Assets and liabilities included in different public sector balance sheet measures

* As produced in accordance with the European System of Accounts 2010 (ESA 2010).

Source: Adapted from Office for National Statistics (2021).

Figure 2. Different public sector balance sheet measures in out-turn and March 2024 forecast

Source: OBR Public Finances Databank (September 2024), https://obr.uk/data.

There is a debate to be had about the merits of targeting each of these measures (we consider some of the most important ones below). Notably, a commitment to have regard for all of them is already legislated – although it tends to garner far less attention than the main fiscal rules. But the government will presumably also have (at least) one eye on the impact adopting each of these measures for the main fiscal rule might have on the government’s ability to borrow to invest. To that end, Table 1 shows how the government would have been performing against a range of fiscal rules in March 2024 (had it replaced PSND ex BoE with an alternative measure without making any other changes to the structure of the rule). A switch to headline PSND would have added around £16 billion of so-called ‘headroom’ in March 2024; a switch to PSNFL would have added £53 billion; and a switch to PSNW would have added £58 billion.

Table 1. Performance against various fiscal rules, as of March 2024 Budget

| Fiscal rule | Margin (‘headroom’) against rule in March 2024 Budget | Difference in ‘headroom’ relative to previous debt target |

|---|---|---|

| PSND ex. BoE falling as a share of GDP in year 5 of the forecast (2028–29) | 0.3% of GDP (£8.9 billion) | - |

| PSND falling as a share of GDP in year 5 of the forecast (2028–29) | 0.8% of GDP (£24.9 billion) | +0.5% of GDP (+£16.0 billion) |

| PSNFL falling as a share of GDP in year 5 of the forecast (2028–29) | 1.9% of GDP (£62.0 billion) | +1.6% of GDP (+£53.0 billion) |

| PSNW rising as a share of GDP in year 5 of the forecast (2028–29) | 2.0% of GDP (£66.8 billion) | +1.8% of GDP (+£57.8 billion) |

| Memo: current budget balance in year 5 of the forecast (2028–29) | 0.4% of GDP (£13.6 billion) | +0.1% of GDP (+£4.7 billion) |

Note: Figures may not sum due to rounding.

Source: OBR Public Finances Databank (September 2024), https://obr.uk/data.

There are three things to note. First, any increase in ‘headroom’ against these targets would not allow for a large increase in borrowing to fund tax cuts or day-to-day spending, because the government would still be bound by its promise to bring the current budget into balance (a target against which the government would have had just £14 billion of ‘headroom’ in March 2024). Second, just as a target that requires PSND ex BoE to be falling between year 4 and year 5 of the forecast suffers from major design flaws (flaws which have been extensively discussed elsewhere), so too would a target for PSNFL or PSNW to be falling between year 4 and year 5. Third, just because a change to targeting PSNFL or PSNW might add as much as £50 billion to the government’s measured ‘headroom’, this does not mean that the government should increase borrowing by anything like that amount. Indeed, always aiming to have a stock measure (such as debt) falling by the finest possible margin (to ‘max out’ any ‘headroom’) breeds an environment where policy flip-flops in response to highly uncertain changes in the forecast.

Relatedly, there is no reason to think that the relative magnitude of the fall in these different measures of debt would look similar in future forecasts. Just because it is easier to meet a PSNFL target today does not mean that will always be the case. There is a danger in choosing a fiscal target opportunistically, because it gives the desired answer on ‘headroom’ at a particular moment in time. There are costs to frequently changing the fiscal rules, and the new government should use this opportunity to choose a fiscal target it is willing and able to stick to in the longer term.

Target a slightly different measure of debt?

The merits of a switch to targeting headline PSND were discussed in a previous IFS Green Budget piece. The crux is that the key reason for such a switch (beyond the simple one that it might allow the government to borrow a bit more) would be to reduce the impact of Bank of England operations on performance against the fiscal rule for the next few years. The Bank of England is making losses on its quantitative easing programme, and is therefore making claims on the indemnity provided by the Treasury which underwrites those losses. The recognition of these losses is expected to push up PSND ex BoE over the coming years (including in year 5 of the forecast, the only one relevant for the fiscal rule) but to have a much smaller impact on headline PSND in those years (because a bigger chunk of these losses have already been recognised in PSND in the past – see here for more detail on the specifics).

The principled argument for a switch to PSND (or stripping out the impact of Bank of England operations in some other way) rests on the argument that the interaction between these losses and the current debt rule is leading to overly tight fiscal policy. This is where the poor design of the existing debt rule is important. It targets only the change in debt between two years (years 4 and 5 of the rolling forecast period). Losses from the indemnity are lumpy, and if losses are particularly concentrated in the fifth year of the forecast (due to the timing of Bank of England asset sales under quantitative tightening – or more precisely, and even more ridiculously, what the OBR judges the timing of the Bank of England’s asset sales under quantitative tightening might be), then this would lead to a temporary overstatement of the need for a fiscal tightening. In that case, targeting PSND (or stripping out Bank operations in some other way) might be judged an improvement.

As well as the Bank of England, the government could choose to exclude other parts of the public sector from its fiscal rule. In particular, publicly owned or underwritten banks (including the new National Wealth Fund) are included in the public sector for accounting and statistical purposes, and so their debt counts towards the total. The idea behind the National Wealth Fund is that, with its initial capital injection of £7.3 billion, it will seek to take on more debt (leverage its balance sheet) and undertake speculative investments on government priorities such as the net zero transition – much like any other bank, though with different objectives. But if these public investment banks are constrained by the government’s overall debt target, they may be limited in their ability to take on more debt. Of course, we would not want these banks to become over-leveraged, or to take on too many risks. The question here is whether they are better constrained through other means (such as banking regulation). Other countries – such as Germany – exclude debt taken on by publicly owned or underwritten development banks from their fiscal targets; see here for the argument that the UK should do the same.

Target public sector net worth (PSNW)?

Changing the measure of debt used in the fiscal target might allow the government to do more borrowing for investment, but would not in itself change the degree to which the benefits of that investment are recognised.

One option, therefore, would be to target PSNW rather than PSND. The arguments for and against doing so were discussed in detail in the 2023 IFS Green Budget. The key attraction of a PSNW target is that, by capturing a more comprehensive range of liabilities and assets, it can provide a more complete picture of the impacts of government action (or inaction). So, if the government were to borrow to invest in transport infrastructure, the additional debt taken on would show up in the government’s liabilities, but the value of the assets created (e.g. new roads or railway tunnels) would also be reflected as a non-financial asset within PSNW. It could also give the government greater incentives to invest in higher-quality projects and to better manage and maintain its assets.

There are, however, considerable downsides to a formal, numerical target for PSNW. Interested readers should consult last year’s IFS Green Budget, but the key issue is that changes in PSNW might tell us little about the government’s ability to access capital markets or service its debt. Non-financial public sector assets – such as the UK road network, school buildings, prisons, and army barracks – are either extremely difficult to sell, extremely difficult to value, or both. The problem with them being difficult to sell is that they are little use in a fiscal crisis if they cannot be sold off to meet financing needs. The problem with them being difficult to value is that a Chancellor might be more tempted to cut taxes or increase spending in the face of a favourable revaluation (say, if a change in statistical methodology led to the conclusion that the best estimate of the monetary value of the road network is higher than previously thought) than he or she might be tempted to carry out a fiscal tightening in the light of an unfavourable one.

One option to lessen some of these concerns (previously proposed by researchers at the Institute for Government) would be to introduce a target defined in terms of the impact of policy on PSNW, rather than the level of PSNW itself. That would limit the degree to which changes in PSNW unrelated to policy (such as methodological changes in how the road network is valued) induce a fiscal policy response. The problem is, the recorded value of many assets created by government investment (the ‘replacement cost’) bears little relevance to the economic or social value of the asset, or to assessments of fiscal sustainability. In other words, in practice, the measured impact of policy on PSNW might bear little relation to its ‘benefits’.

These are very good reasons why more traditional measures of debt, debt interest and borrowing will remain important for fiscal policy, and ought to be considered alongside any target for PSNW.

Target public sector net financial liabilities (PSNFL)?

Another option would be to target PSNFL, a less comprehensive measure of the balance sheet than PSNW (see Figure 1). The key difference between a target for debt (PSND) and a target for PSNFL is that PSNFL also includes illiquid financial assets (such as the student loan book) and a broader range of financial liabilities (such as the liabilities associated with funded pension schemes – but not the much larger liabilities from pay-as-you-go pension schemes or the state pension). Notably, it does not include the kinds of assets that an increase in investment spending is likely to buy – such as energy pylons or hospitals.

Instead, the main theoretical attraction of a PSNFL target is that in capturing a broader range of government assets and liabilities, it provides a more complete picture of the government’s financial position, while removing some of the perverse incentives associated with a narrow focus on PSND (such as the incentive to sell off long-term financial assets for less than their market value, since PSND is reduced by the money raised through the sale but is unaffected by the loss of the asset). In other words, a fiscal rule targeting PSNFL would encourage the government to have greater regard for its financial assets as well as its liabilities.

Table 1 shows that in March 2024, a target for PSNFL to be falling in year 5 would have provided the government with more than £50 billion of additional ‘headroom’ relative to the previous government’s target for PSND ex BoE. The difference is largely driven by the differential treatment of student loans. Where student loans are not expected to be repaid, this now (sensibly) scores immediately against public sector net borrowing. But PSND still increases by the full amount loaned out – i.e. even including the amount that is expected to be repaid subsequently. The difference is that the portion of student loans that are expected to be repaid in future are added to the illiquid financial assets captured by PSNFL. So, the same liability appears in both, but in PSNFL this is partially offset by an asset. So when the size of the student loan book increases (e.g. due to growing student numbers or an increase in the amount that students can borrow), PSND will increase by more than PSNFL (or, equivalently, PSND will fall by less than PSNFL).

There are, inevitably, some notable downsides to a PSNFL target. One issue is that, as with PSNW, performance against a PSNFL target would not necessarily be informative about the government’s ability to access capital markets or service its debts. The financial assets included in PSNFL but not PSND are illiquid (like student loans, assets held by the local government pension scheme, or mortgage books acquired during the financial crisis). In a financing crisis, where the government is seeking to sell off assets, these are likely to be less useful than liquid assets such as foreign currency holdings, but more useful than non-financial assets (such as the prisons estate or aircraft carriers, which cannot realistically be sold). For that reason, the concerns raised above about PSNW are less acute for PSNFL, but remain concerns all the same. A situation where PSND were on a permanently rising path, even if counterbalanced by the accumulation of financial assets in the public sector (so, if PSNFL were stable or falling), may still be risky.

Another issue is that departments may also face new incentives to design policies that create financial assets (e.g. student loans rather than a graduate tax to finance higher education) purely because of differences in how the accounting treatment affects ease of compliance with a PSNFL target. There are also methodological challenges to estimating PSNFL (see OBR discussion of these challenges here and here). Revisions to PSNFL estimates for past years can be large – for example, in September 2023, estimated PSNFL in 2021–22 and 2022–23 fell by £38 billion and £26 billion, respectively, due to methodological improvements and the incorporation of data on public sector funded pensions that become available with a lag. Forecasts for the future may be even more volatile. This means that measured ‘headroom’ against a PSNFL target – especially one for PSNFL to be falling (since it then matters where you start from) – could be even more prone to wild revisions without a material change in the fiscal situation.

Conclusion

This is far from an exhaustive discussion. No single measure is a perfect indicator of the health of the public finances, and there is no unambiguously ‘right’ answer. There are principled arguments for and against each of these changes. If the Chancellor really wants her fiscal target to reflect the benefits of investment, that might suggest a target for PSNW. But a formal target for PSNW would come with considerable problems, and we would strongly advise against. Switching to a target for PSNFL would come with fewer problems, and would allow much more space for borrowing for investment (perhaps as much as £50 billion more), but would not meaningfully reflect the benefits of that investment. Readers can make their own minds up as to whether a shift to a measure such as PSNFL would represent a breach of a manifesto promise (though the authors begrudgingly and regretfully acknowledge that this is not a mainstream political issue). Either way, even if a shift to PSNFL allowed for more investment within the fiscal rules, it would not do much to capture the benefits of that investment.

It is hard to avoid the suspicion that the government is attracted not by any theoretical advantages of a change in the debt rule, but by the fact that it would allow for significantly more borrowing for investment. Here, it is worth pausing to comment on scale. On existing plans, public sector net investment is currently forecast to be £53 billion in 2028–29. Net gilt issuance in 2028–29 is forecast to be £87 billion. Against that, any change that allowed for an extra £50 billion of borrowing for investment would be an enormous shift, even if not all of this extra space were used at once. If even half that figure were spent on additional investment, debt (on the previous target’s measure) could be more than 3% of national income higher by the end of the parliament and would almost certainly still be rising at the end of the forecast period, even accounting for typical feedback effects via a larger economy.

Such a large change would also raise questions about the government’s capacity to spend this money well, and about the possible impact on government borrowing costs and interest rates more generally. Previous Treasury modelling suggested that an increase in borrowing of 1% of GDP might increase interest rates by between 50 and 125 basis points, depending on economic conditions. An extra £50 billion of borrowing in 2028–29 (roughly the amount of extra ‘headroom’ provided by a switch to PSNFL) would amount to around 1.6% of GDP. To the extent that the additional investment produced material benefits for the productive potential of the economy, we would expect the impact on interest rates to be smaller. But the point is, additional borrowing on this scale could have a material impact on interest rates.

Importantly, if the government wants to relax its debt rule to allow for more borrowing for investment, it is not enough to justify this on the grounds that ‘investment is good’. It also needs to explain why we should be borrowing to pay for it. If the government believes more borrowing is the best – or perhaps even the only – way to get to net zero emissions and that failure to do so would be more costly than a rising debt path, it should make the case for this explicitly, rather than hiding behind a ‘technical’ change. If the government is confident that extra borrowing for investment would be sufficiently growth-enhancing to improve long-term fiscal sustainability, it should make that case (to citizens, as well as to gilt market participants). This could be accompanied by a change in the debt rule to signal the logic behind this fiscal strategy, but the crucial thing would be to ensure that the investment funded by that borrowing is – and is widely seen to be – spent well. There are undoubtedly opportunities for productivity-enhancing public investment projects in the UK. Given the UK’s history as a low-investment economy, there may even be some low-hanging fruit. But not all investment is growth-enhancing, and not all of what counts towards measured public investment is in tangible assets (more than 10% of the total is student loans, for example). Making the right choices, and having an institutional framework to make that more likely, is key. And regardless of the precise fiscal rules, debt and debt servicing costs cannot be disregarded entirely.

Finally, the government may rightly be concerned that the current debt rule’s conclusions about fiscal ‘headroom’ can swing wildly from one fiscal event to the next even in the absence of significant revisions to economic and fiscal fundamentals. We very much share this concern. But it should then consider the root of this issue: not the measure of debt chosen, but the narrow targeting of the change in debt relative to the change in nominal national income over a 12-month period several years in the future. Put differently, many of the problems identified with the current fiscal framework are downstream of the original mistake – aiming to have debt forecast to fall over the course of one year in five years’ time, and by an ultra-fine margin relative to the inherent uncertainty.

Authors

Isabel Stockton

Isabel works in the Healthcare sector, and on the public finances. Their research focuses on retaining and developing the NHS workforce.

More from IFS

Understand this issue

Policy analysis

Academic research