Downloads

Download report PDF

PDF | 670.8 KB

Key findings

1. Capital gains tax (CGT) raises around £15 billion per year, less than 2% of total tax revenue. Revenues have risen significantly over time and are forecast to rise further, partly reflecting the increasing role of wealth accumulation in the UK economy.

2. CGT is paid by around 350,000 people (0.65% of the adult population). 3% of CGT taxpayers realised gains of more than £1 million and this group accounted for two-thirds of CGT revenue. The average gain among this group of 12,000 people (0.02% of the adult population) was £4 million. Around half of taxable gains relate to unlisted shares in private businesses.

3. CGT rates vary across assets. They are lower than tax rates on earned income and, in most cases, income from capital. These rate differentials are unfair and create a range of undesirable distortions.

4. The design of the tax base is flawed. Ultimately, by discouraging saving, investment and risk-taking and distorting who holds assets and for how long, it reduces productivity and well-being.

5. Higher rates of CGT would worsen these problems caused by the tax base. But keeping tax rates low cannot solve those problems. There is a strong case for reform.

6. The tax base could be reformed so that CGT does little to discourage saving and investment. This requires giving more generous deductions for purchase costs and losses. There are several ways to do this in practice.

7. Ultimately, we advocate aligning marginal tax rates across all forms of gains and income, while reforming the tax base. Tax rates could be aligned at any level; for example, rates on capital gains (and capital income) could be increased while rates on employment income were reduced. In practice, the ‘big-picture’ solution we set out would include substantially higher CGT rates.

8. Higher CGT rates would increase the incentive for people to leave the UK before realising gains to avoid UK CGT. One option to address this would be to tax people emigrating from the UK on their accrued but unrealised gains, whilst exempting new arrivals from UK CGT on gains they made whilst living abroad. There are challenges with this approach, but it is operated by some other countries.

9. Steps could be taken towards a better-designed system. Low CGT rates on business assets are poorly targeted at entrepreneurship. They lead to more money being held in companies, but do not achieve the commonly stated policy goal of increasing owner-managers’ investment in their own businesses. Business asset disposal relief should be scrapped in favour of more generous deductions for investment costs. Removing CGT uplift (or ‘forgiveness’) at death should also be a priority.

10. The government should seek to make reform credibly lasting. It should set out clear principles and a rationale for reform and commit to the new regime for the length of the parliament. Instability and unpredictability are bad for investment.

7.1 Introduction

There is widespread speculation in the run-up to her first Budget that the new Chancellor, Rachel Reeves, will raise capital gains tax (CGT).

Increasing CGT is one option that was not ruled out in the Labour Party manifesto. And it is easy to explain the inequities that arise from taxing capital gains at substantially lower rates than earned income and, in most cases, capital income. Taxable capital gains are heavily concentrated at the top of the income distribution and those receiving gains pay much lower tax rates than people receiving similar amounts but in the form of employment income.

However, at first glance, CGT might not seem like an obvious choice for a Chancellor looking to raise significant sums. According to official estimates of the revenue effects of different tax changes produced by HM Revenue and Customs (HMRC), a 1 percentage point increase in the higher rates of capital gains tax in April 2025 would raise a measly £100 million in 2027–28 while a 10 percentage point increase would actually reduce revenue by about £2 billion that year.

In the absence of sufficient information as to how these estimates are produced, it is difficult to assess their credibility. Our view is that HMRC’s published estimates are not a good guide to the revenue effect over a longer time horizon and that a rise in CGT rates would, up to a point, raise revenue in the medium run. But increasing headline rates in isolation would involve difficult trade-offs. More revenue would be raised, and with tax rates on capital gains closer to tax rates on income, there would be less distortion to how people chose to work and to take their income. But distortions created by the tax base – the definition of what is subject to tax – would be worsened. Among other things, higher rates would increase unwelcome distortions to commercial decisions about how much to save and invest, which assets to choose and how long to hold them for (see Section 7.3).

Removing the harmful distortions created by the poor design of the UK’s CGT should be a key focus of policy. CGT creates unfairness by arbitrarily favouring one action over another and thereby penalising otherwise-equivalent people who behave in the tax-disadvantaged way.

CGT also creates economic inefficiency. The cost to taxpayers of CGT is not just the money they hand over and the resources they spend complying with their obligations, but the lower well-being that results when CGT leads them to change how they behave. For example, there is a cost to people when they hold on to assets for longer than they would want to absent tax considerations. People also waste time and resources undertaking legal arrangements aimed at saving tax by repackaging income into capital gains. And because it leads to reduced investment and skewed patterns of capital allocation, CGT acts to lower productivity. We are collectively made poorer by a poorly designed CGT.

The good news for Ms Reeves is that the tax base could be reformed to greatly reduce – and in some cases largely remove – the distortions to saving, investment and risk-taking. In short, this would require giving more generous deductions for purchase costs and losses and removing CGT uplift (or ‘forgiveness’) at death. There are several ways that base reforms could be achieved in practice. With a reformed tax base, tax rates could be increased with much less distortion to choices over whether, when or how to invest. We summarise a ‘big-picture solution’ that involves reforming the tax base while aligning overall marginal tax rates across all forms of gains and income (see Section 7.5). This would represent a major change in tax policy, but also offers a significant prize. Importantly, reforming CGT would be worthwhile in its own right: regardless of how much revenue the government would like to raise, it could raise it in a way that was fairer and less damaging to economic growth and well-being. Reform is even more important if the government wishes to raise additional revenue.

The UK currently charges CGT on disposals that an individual makes while they are UK-resident. Higher CGT rates would increase the incentive for those who have accrued large gains to move to a lower-tax country – to retire abroad, for example – before realising them. One option to mitigate this incentive would be to introduce ‘deemed disposal on departure’ for CGT purposes, matched by ‘rebasing on arrival’ for new arrivals (Section 7.5). Effectively, this would move to taxing gains that accrued while a person was living in the UK, rather than those realised here. There are challenges with this approach, but it is already operated by some other countries.

If the government chooses to reform only some rates or elements of CGT, there would be inevitable trade-offs that require careful management (Section 7.6). But there are smaller steps that could be taken in the right direction. For example, we describe a reform that would include removing business asset disposal (BAD) relief – a preferential CGT rate for business owner-managers which is not well targeted at entrepreneurship and leads to a range of undesirable distortions – alongside giving up-front tax relief for investment in shares. The new up-front relief could be thought of as a replacement for BAD relief – a reorienting away from tax relief on large gains to tax relief on investment. Empirical evidence suggests that implementing the two measures together would boost investment and raise revenue. It would be a progressive change: revenue would be raised from the top of the income distribution, while recipients of the new relief are less well off: those investing the most, rather than those making the biggest gains, would benefit most.

Reforming the tax base at the same time as increasing rates would create winners as well as losers (see Section 7.8). Those making relatively low returns (e.g. those making low-risk arm’s-length investments and those taking risks that do not pay off) would pay less tax. Those making very high returns – which could reflect some combination of effort and skill, privileged access to scarce opportunities, and luck – would pay more. But note that raising taxes on high returns could equally be described as removing the tax advantages they receive under the current tax system. We do not take a view on how high tax rates should be, but there is no good reason to tax work less heavily if it generates a capital gain than if it generates employment income.

Whatever changes are made to CGT, a decision would have to be made on the transitional arrangements for existing accrued gains (see Section 7.7). Specifically, to what extent would any benefits of a narrower base and any costs of higher rates be applied to gains that have already been accrued but not yet realised? Giving more generous allowances for past investments would come with a cost but not improve incentives. Applying higher tax rates to past gains would be an efficient way to raise revenue. But it may lead to objections that it is retrospective – though almost all tax increases are retrospective to some degree.

7.2 What is CGT and who pays it?

What is capital gains tax?

CGT is a tax on the increase in the value of an asset between its acquisition and its disposal. Broadly speaking, this means its sale price minus its purchase price.2 If an asset is held until death, any capital gain up to that point is subject to uplift (the tax is ‘forgiven’): the deceased’s estate is not liable for tax on any increase in the value of assets prior to death, and those inheriting the assets are deemed to acquire them at their market value at the date of death.

CGT only applies to assets sold by individuals and trustees; gains made by companies are included in profits and subject to corporation tax. The rest of this chapter focuses exclusively on capital gains made by individuals.

Not all assets are subject to capital gains tax. Most notably, increases in the value of owner-occupied homes are exempt from CGT. There is also no CGT charged on assets held within pension funds or Individual Savings Accounts (ISAs) and there are reliefs for various venture capital and employee share schemes.3

Broadly, CGT is based on where people live when they realise capital gains. As such, people who move to the UK can – in principle – be taxed on gains that accrued before they came (though in practice there is a ‘grace period’ during which they are not taxed on gains made on overseas assets), and people who leave the UK can avoid UK tax on gains that accrued while they were here. We return to the specific details below.

As with income tax, there is an annual threshold below which CGT does not have to be paid. In 2024–25, this ‘annual exempt amount’ is £3,000 (having been reduced from £12,300 in 2022–23). This is subtracted from total annual capital gains before calculating the tax due.

From April 2024, there are five CGT rate schedules depending on the source of the capital gain (see Table 7.1).

Table 7.1. Capital gains tax rates, 2024–25

Source of gains | Basic | Higher rate | Additional rate |

Carried interest | 18% | 28% | 28% |

Residential property | 18% | 24% | 24% |

Business asset disposal relief and investors’ relief | 10% | 10% | 10% |

Other assets | 10% | 20% | 20% |

Exempt assets, and all gains unrealised at death | 0% | 0% | 0% |

Source: HMRC.

Carried interest is the share of profits from a private equity fund that is paid (in the form of capital gains) to private equity managers – it is effectively a performance fee. Carried interest faces a higher rate of 28%. Business asset disposal (BAD) relief is a preferential 10% tax rate that applies to capital gains on owner-managers’ shares in their companies, up to a limit of £1 million of lifetime gains from owner-managed businesses. Investors’ relief similarly provides a 10% CGT rate for external investors in unlisted trading companies if they hold the shares for at least three years, up to a lifetime limit of £10 million.

Residential property (except people’s main homes, which are exempt) is subject to higher rates of CGT than other assets (except for carried interest). However, the biggest of those other assets is company shares, which are subject to higher overall effective tax rates as a result of corporation tax levied on the company profits from which shares derive their value. But, even accounting for this, capital gains are taxed at significantly lower rates than labour income (Table 7.2 later shows this).

Both the rates and base of CGT have changed many times since its introduction in 1965. Box 7.1 provides a brief history of the main changes. For further discussion, see Adam (2008) and Seely (2020).

Box 7.1. A potted history of capital gains tax

CGT was introduced in 1965 at a flat rate of 30%. Geoffrey Howe introduced indexation allowances in 1982, ensuring that only gains in excess of inflation were taxed. In 1988, Nigel Lawson aligned CGT rates with individuals’ marginal income tax rates. In 1998, Gordon Brown scrapped indexation allowances for future years and introduced taper relief, which reduced CGT by more the longer an asset was held and was more generous for ‘business’ than ‘non-business’ assets. Taper relief was subsequently made more generous, before then being scrapped by Alistair Darling in 2008. Mr Darling announced a return to a single flat rate, set at 18%, but (following a backlash from business lobby groups) introduced entrepreneurs’ relief (now BAD relief), which applied a 10% rate to the first £1 million (later increased to £10 million then reduced back to £1 million) of lifetime gains for some business assets. George Osborne raised the rate to 28% for higher-rate taxpayers in 2010, but then cut it (for most assets) to 20% for higher-rate taxpayers and 10% for basic-rate taxpayers in 2016. The rate for residential property (other than owner-occupied housing) was reduced from 28% to 24% in 2024.

What capital gains represent

It can be useful to distinguish, conceptually, between returns that reflect ‘normal’ and ‘excess’ returns to capital. Tax has different effects (in terms of both equity and efficiency) depending on whether it is levied on normal and/or excess returns. In short, a tax on the normal return will create a range of distortions, including discouraging saving and investment.

The normal return can be thought of as the return that just compensates savers and investors for the delay in consumption (without any additional compensation for risk-taking). When buying a rental property or shares, for example, a person needs to expect to make at least the risk-adjusted normal return in order to be willing to part with their money.

Returns to capital will often be higher – and sometimes substantially higher – than the normal return. We will refer to all differences from the normal return as ‘excess returns’ (negative if an asset yields a below-normal return). Such returns can reflect:

- Luck in the outcome of risky investments. Since people generally prefer a safe bet, higher-risk investments will generally only be attractive if they offer a correspondingly higher expected return, or risk premium; so those who invest in risky assets can earn above-normal returns on average (not just if they happen to get lucky).

- Economic rents, which are a return greater than that required to make an investment worthwhile. Rents generally arise from a factor being in limited supply, whether that is land or another natural resource, government-induced restrictions such as taxi licences, monopoly power, unique ideas, private information or brands (including those related to innovators, artists, sports stars and firms).

- Effort and skill. Excess returns to capital can directly reflect returns to effort (e.g. where excess returns reflect skill in choosing the best investments or effort that was put into renovating an asset or capturing rents) or indirectly reflect returns to work where labour income is being ‘disguised’ (e.g. where a company owner-manager pays herself in dividends or capital gains rather than through a salary).

In practice, capital returns (whether in the form of gains or incomes) will often reflect a mix of sources. For example, some houses will have amassed large capital gains both as a result of being located in an area that became more attractive and as a result of substantial renovation. Some business assets will be valuable because their owners were highly skilled and put a lot of effort into building a business, and because the business had a monopoly, and because the owners had some good fortune. Also note that some business owners make no meaningful capital investments at all, such that capital gains can entirely reflect ‘disguised’ labour income.

Capital gains will reflect these underlying factors, as well as what share of a return to capital is realised or taken in the form of gains versus income.

Aggregate gains and revenue

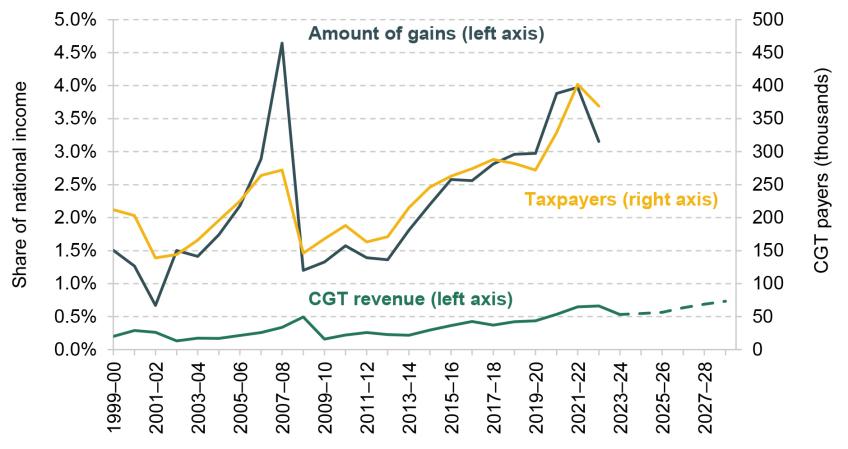

In 2022–23, 370,000 taxpayers realised £81 billion of taxable gains.4 Taxable gains were lower than in 2021–22, but have been rising over time. Taxable gains as a share of national income have risen from around 1% of national income in the early 2000s to over 3% (see Figure 7.1). The large spike in gains in 2007–08 occurred as a result of the government preannouncing the removal of taper relief and (for some) an increase in the CGT rate, which gave asset holders an incentive to sell before the policy change was enacted (Seely, 2010a).

Figure 7.1. Capital gains, taxpayers and revenue

Note: ‘Amount of gains’ refers to taxable gains measured after the deduction of losses plus attributed gains but before deduction of the annual exempt amount or of taper relief, where relevant. Individuals and trusts are included in all figures. Dashed line is a forecast.

Source: Revenue and GDP measures are from OBR Public Finances Databank, August 2024. ‘Total taxpayers’ is from table 1 of HMRC capital gains tax statistics, August 2024. ‘Amount of gains’ is from Advani and Summers (2020).

CGT raises around £15 billion per year (less than 2% of total tax revenue). As Figure 7.1 shows, CGT revenue – which is affected both by underlying gains and by tax policy choices – has risen over time (as a share of national income) and is forecast by the Office for Budget Responsibility (OBR) to rise further.

Source and distribution of capital gains

Who gets capital gains

Taxable capital gains are very concentrated among a small number of people. In 2022–23, there were 350,000 individuals – 0.65% of the adult population – realising taxable gains.5 This is around 100 times fewer than the number of income tax payers (34.6 million) in that year. Less than 3% of UK adults paid CGT at any point over the 10 years from 2010–11 to 2019–20 (Advani, Lonsdale and Summers, 2024a).

Around 60% of individuals who filed a CGT return in 2022–23 realised gains of less than £50,000, and accounted for just 7% of gains and 4% of the CGT revenue.6 3% of CGT taxpayers realised gains of more than £1 million and this group accounted for 62% of gains and 67% of the CGT revenue. The average gain among this group of 12,000 people – who represent 0.02% of the adult population – was £4 million.

For most of the people receiving taxable capital gains, gains are ‘lumpy’ – they accrue over many years and are realised in a single year. The Office of Tax Simplification (2020, para. 1.18) reports that 72% of taxpayers who reported capital gains in the 11 years from 2007–08 to 2017–18 did so in only one of those years.

Advani, Lonsdale and Summers (2024a) find that half (49.1%) of individuals who paid CGT in 2019–20 did not receive gains at any point over the preceding decade. However, many of the other half received gains regularly: almost one in eight (11.6%) individuals received gains at least five times, while a small minority (0.6%) received gains in all 10 years. Averaging across years when gains were realised, the mean capital gain was over twice (2.3 times) as large for individuals who realised gains every year (£441,000) as for one-off gainers (£194,000).

Taxable capital gains flow disproportionately to people who are already in the top 1% of the income distribution (Advani and Summers, 2020; Delestre et al., 2022). In contrast, untaxed capital gains are more equally distributed. This is unsurprising given that owner-occupied housing and investments held in ISAs are exempt from CGT.

Advani, Lonsdale and Summers (2024a) find that taxable gains are disproportionately concentrated amongst certain demographic groups. Although men receive a disproportionate share of overall income (66%), their share of gains is even larger (74%). Taxable gains are also weighted towards the middle of the age distribution. While around half (49%) of individuals with gains are over 60, most of the value of gains (56%) goes to taxpayers aged 40–59. There are sharp geographical divides, with most gains in London and the South East. The constituency of Kensington has a larger share of total gains (3.1%) than the entirety of Wales (2.0%).

Capital gains by type of asset

Figure 7.2 shows the distribution of capital gains by asset type, based on both the number of disposals of different assets (green) and the value of the gains received (yellow).

Figure 7.2. Capital gains by asset type, 2021–22

Note: Gains are measured before the deduction of the annual exempt amount. ‘Other financial assets’ includes assets such as UK and non-UK listed and unlisted securities, unit trusts and loan notes. ‘Other non-financial assets’ includes intangible assets such as goodwill and tangible assets such as fine works of art.

Source: Tables 7.2 and 7.5 of HMRC capital gains tax statistics August 2024.

Most (85%) disposals were of financial assets. Roughly similar shares (25%) of disposals were of listed shares (those publicly traded on a stock market) and of unlisted shares (in private businesses).

Looking instead by value of gains, a very different picture emerges. Around half of the value of gains related to unlisted shares. The average gain realised on unlisted shares (including those eligible for BAD relief) was more than £120,000. By contrast, on listed shares and residential property, the averages are ‘only’ £18,000 and £61,000 respectively.7

‘Carried interest’, which is received by private equity executives and comprises mostly gains in unlisted shares, is received by only around 2,000 individuals (fewer than 1% of CGT payers) but accounts for just over 4% of the value of gains, with a mean gain of £1,281,000 per individual in 2019–20 (Advani, Lonsdale and Summers, 2024a).

Nature of private business gains

Private businesses span a huge range of industries and scales. They cover everything from chemical manufacturer Ineos, with annual profit in 2023 of £1.4 billion and 26,000 employees, to micro-businesses with a sole employee-shareholder, working, for example, as a consultant. While the former makes substantial investments in new capital annually, a consultant setting up a company likely needs little capital outlay and may have no intention of ever employing anyone else. The tax treatment of capital gains relative to earned income, described further below, encourages the setting-up of such low-capital businesses.

Advani et al. (2024) find that over two-thirds of the gains on unlisted shares go to individuals who are company directors, indicating that they are actively working in the business. Many gains reflect minimal initial capital investment by the individual receiving the gain: half of all disposals of unlisted shares yield gains equating to an average annual return of over 100%.

Combining the carried interest of private equity managers with gains that were eligible for entrepreneurs’ relief in 2019–20,8 a conservative estimate is that around half of all taxable capital gains are closely linked to people’s occupations (Corlett, Advani and Summers, 2020). That is to say that, while taxed as capital gains, these incomes have many of the characteristics of labour earnings.

7.3 Problems with the design of CGT

A good rule of thumb is that the tax system should aim to be neutral: that is, to treat similar activities similarly.9 Our starting point is that taxes should not, without a strong rationale, distort commercial decisions about who holds assets for how long, which assets are chosen and whether remuneration is taken as earnings, dividends or capital gains. Nor should the tax system discourage saving and investment. Yet the current design of capital gains tax distorts all these margins. We briefly summarise the problems that causes below; in Section 7.4, we discuss whether and how the tax system should actively encourage entrepreneurship. We note that the exemption of main homes from CGT (formally principal private residence relief) is a costly relief and creates distortions. Removing the relief would be difficult. The Labour Party has ruled out doing this and we do not discuss the taxation of main homes here.

Ultimately, the fact that the design of CGT discourages some investments and distorts a range of decisions is a source of both economic inefficiency and unfairness.

Economic inefficiency means that, for a given amount of revenue raised, welfare – i.e. how well off people are in a broad sense – is lower than it would otherwise be (if the inefficiencies were smaller). The economic inefficiencies can directly manifest in lower economic output. For example, reduced rates of investment and skewed patterns of capital allocation will mean that, for a given level of revenue, productivity is lower, with this resulting in lower output and incomes.

Unfairness arises because aspects of CGT arbitrarily favour one action over another and thereby penalise otherwise-equivalent people who behave in the tax-disadvantaged way. To give one example among many, consider two people who have made similar investments in their own company and generated similar returns. One takes the return as a flow of dividends (while a higher-rate taxpayer). The other takes the return as capital gains when the company is sold, using another source of income to finance their spending before the point of sale. The first person faces a large and unfair tax penalty relative to the second.

Problems caused by the design of the tax base

Many of the problems created by CGT stem from the design of the tax base – the definition of what is subject to tax. In summary, the design of the tax base penalises saving, investment and risk-taking and leads to a misallocation of capital. For example, it can mean that capital is directed away from its most productive use. This creates economic inefficiency and unfairness. The problems are worse at higher rates of CGT. In fact, the efficiency costs created by a distorted tax base rise more than in proportion to tax rates, because low tax rates only change behaviour when the decision is marginal anyway (e.g. when an investment was only just worthwhile); higher tax rates discourage not only more activities, but also more valuable activities. But while lower rates of CGT lessen the problems caused by the base, they cannot fix them. In Section 7.5, we discuss how tax base reforms could directly address the problems described here.

CGT discourages saving and investment

CGT discourages saving and investment in taxed assets. The tax reduces the return the saver can expect to receive on their investment, so some investments that would have been worthwhile in the absence of taxation are made unprofitable by the tax.

Suppose I require a return of 4.5% to persuade me to invest – for example, to put more money into my own company or to buy shares or a property. A 20% tax that reduces the return from 5% to 4% will mean an investment I would otherwise have undertaken will now not go ahead. This is undesirable: too little investment will be undertaken if otherwise profitable investments are made unprofitable by tax. And if an individual would rather save his or her money than spend it now, it is difficult to see why taxes should penalise this choice.

This is not an inescapable feature of CGT. As we discuss in Section 7.5, it would be possible to have a tax system that did not discourage marginal investments (those that generate only a ‘normal’ return and whose viability would be threatened by tax) but continued to raise revenue from investments that earn a high (‘excess’) return – which would continue to be viable even with a tax liability – and from capital gains that represent a return to effort and skill (and luck) rather than capital invested.

With the current tax base, however, CGT does discourage saving and investment. Worse, it discourages different investments to different degrees. The magnitude of the disincentive to save depends on the tax rate (or, more precisely, what the tax rate is expected to be when the gain is realised) – which depends on the type of asset and on how much of the return takes the form of a capital gain rather than some sort of income. It also depends on how long the asset is held and on the risk of making a loss that cannot be offset immediately – factors we discuss below. And it depends on the rate of inflation: the disincentive is greater when inflation is expected to be higher.10 (This was the motivation behind the system of inflation indexation that existed in some form between 1982 and 2008.)

Lock-in effects disincentivise capital reallocation

Capital gains tax creates a ‘lock-in’ effect. If someone has an asset that has risen in value, there is an incentive to hold on to the same asset, rather than selling it (triggering a tax liability) and reinvesting the money in another taxed asset. In effect, if a person sells an asset after one year, buys another one and then sells it after another year, the value of the tax payments would be higher than if they held a single asset for two years. This disincentive to reallocate capital to a different asset locks people into their existing investments.11

In that sense, CGT acts as a tax on transactions (like stamp duties) and leads to misallocation of capital: I will continue to hold on to my existing asset even if someone else could use the asset more productively and I could use my capital more productively elsewhere. The tax system includes reliefs (notably business asset rollover relief and reinvestment relief) specifically intended to mitigate the lock-in effect in some cases, but those are incomplete.12

The lock-in effect is exacerbated by the fact that capital gains unrealised when someone dies are not taxed at all: the deceased’s estate is not liable for CGT on any increase in the asset’s value prior to death, and those inheriting the assets are deemed (for future CGT purposes) to acquire them for their market value at the time of death, not the original purchase price. This creates a big incentive to hold on to assets that have risen in value and bequeath them – even if it would be more profitable to sell them and use the proceeds in some other way before death (at which point other assets, including the proceeds from the sale of the original assets, could be passed on instead) and even if it would be preferable to pass on the assets (or the proceeds from selling them) immediately.

Incomplete loss offsets discourage risk-taking

Much discussion of the effect of tax on risk-taking focuses on the rate of tax on successful projects: higher taxes (on gains or income) reduce the rewards to success. But what matters when considering risky projects – that is, projects where the outcome is uncertain – is the treatment of good outcomes relative to bad ones. Risk-taking is discouraged by the tax system not as a result of the level of tax on income and gains per se, but because of the asymmetric treatment of upside and downside risk. In effect, the government takes a share in the fruits of success but does not take an equal share in the pain of failure.

The current tax system does not treat profits/gains and losses symmetrically. When people make a loss, they are able to ‘offset’ the loss against other gains such that tax is then levied on the net gain. But loss offsets are incomplete. Losses often cannot be relieved immediately; they can be carried forward to offset in future, but the delay reduces the value of the relief; and sometimes the losses can never be offset at all. As a result, the system discourages risk-taking. Other things equal, that is harmful.

Problems caused by differential tax rates

There are large differences in the overall tax rates (i.e. accounting for all levels of tax) levied on capital gains on different types of assets and on gains relative to income (these are shown in Table 7.2 later) – although the lack of indexation for inflation makes comparing effective tax rates on income received now and capital gains realised in the future more difficult.

Gains on different types of assets are taxed at different rates. This skews the allocation of investments (away from what is the commercially best investment towards tax-favoured investments) and penalises people who invest in more heavily taxed assets.

Capital gains are (almost always) taxed at lower rates than capital income, and both capital gains and capital income are (almost always) taxed at lower rates than earnings from employment or self-employment. This creates a bias towards taking any rewards in the form of gains rather than income and towards putting effort into activities that generate gains rather than income.

The incentives created and problems caused by differential rates can be clearly seen for business owner-managers. Tax differentials provide an incentive to work for your own business (through self-employment or as a company owner-manager) rather than as someone else’s employee, even when that is not the most productive choice. They also provide a strong incentive to undertake investments that will result in capital gains rather than income and, where possible, to realise the returns to labour as capital income or gains.

Miller, Pope and Smith (2024) use UK tax records to show that company owner-managers are very responsive to tax incentives. Company owner-managers can choose when and how to take income out of their companies. They can pay themselves a salary, take dividends or take capital gains. Most company owner-managers pay themselves a small salary (equal to the point at which personal taxes become payable) and take any remaining remuneration in the form of dividends or capital gains. Those generating income above the higher-rate threshold retain significant amounts in their company over long periods. Much of this is ultimately withdrawn in the form of capital gains and subject to BAD relief.13 The tax savings can be substantial. For example, among owner-managers claiming (what was then) entrepreneurs’ relief in 2015, average capital gains were £500,000. This delivers a tax saving of £75,000 relative to if the income had been taxed at 25% (the effective higher rate of tax on dividends in 2015) rather than 10%.14

These distortions are inefficient. One implication is that people will not always be making the most productive choices over, for example, what type of work to do or which investments to make. They can also reduce people’s well-being by, for example, leading them to spend their money later than they would absent the tax incentives.

In principle, the distortions created by BAD relief specifically could lead to a misallocation of capital. However, Miller, Pope and Smith (2024) find no evidence that tax-motivated earnings retention affects investment within the company: the retained earnings are kept as cash or other financial assets – for example, shares in other companies – rather than used to buy assets for use in the business. Preferential rates of capital gains tax for business assets therefore lead to more money held in companies but not to any great misallocation of the capital owned by company owner-managers. This also means that preferential rates are not achieving the commonly stated policy goal of increasing owner-managers’ investment in assets for use in their businesses (we return to this in Section 7.4).

Alongside the economic inefficiencies caused by differential tax rates, there is clear unfairness: there is effectively a tax penalty on those people who find it harder to arrange their affairs to take advantage of preferential tax rates.

International issues

There are differences in the taxation of capital gains across countries which can affect people’s location decisions. The UK is currently around the middle of the pack for headline CGT rates compared with other major economies, although there is huge variation in approaches. Like the UK, the US currently taxes long-term gains on most assets at a top rate of 20%. The top rates in France (34%), Ireland (33%), Spain (28%), Germany (26%) and Italy (26%) are somewhat higher than the UK’s, and some countries – such as Australia and Denmark – tax capital gains at full income tax rates. However, several countries do not tax capital gains at all, including Switzerland and New Zealand, as well as more typical tax haven jurisdictions. Additionally, some countries such as Ireland and Italy do not tax capital gains on the foreign assets of new arrivals.

Capital gains are generally taxed on a ‘residence’ basis, meaning that UK residents must pay UK CGT on their worldwide gains, irrespective of where the assets are located.15 Non-residents only pay UK CGT on gains from UK land and property. Consequently, the main impact of the UK’s CGT regime, from an international perspective, concerns the movement of people (into or out of UK residence); investment in UK assets is affected only insofar as that is linked to whether people live in the UK.

Specifically, the UK currently charges CGT on disposals that an individual makes while they are UK-resident. This means that if someone accrues capital gains while living in the UK but then leaves the UK before selling the asset, they pay no UK CGT (unless the gains are from UK land and property or the individual moves back to the UK within six years, in which case they are taxed on the gains they realised while abroad). This creates an incentive for those who have accrued large gains to move to a lower-tax country – to retire abroad, for example – before realising them.

The flip side is that individuals who move to the UK are potentially liable for UK CGT on capital gains that they accrued prior to arrival, if they subsequently dispose of these assets while UK-resident – unless the gains are on foreign assets and they dispose of them within the ‘grace period’ they get after moving to the UK (four years under the new regime being introduced from April 2025, generally much longer under the ‘non-dom’ regime that is replacing). That creates a disincentive to move to the UK from a lower-tax country (and an incentive to move to the UK from a higher-tax country).

7.4 Support for entrepreneurship

We describe in the next section how to reform the tax base so that it is neutral with respect to a range of decisions, including investment. Such a tax base would mean that CGT did not discourage investment. But in policy discussion, arguments for preferential CGT rates are often predicated on the assumption that the government is not seeking neutrality: it is seeking to actively encourage investment and entrepreneurship. For example, at the point of announcing entrepreneurs’ relief, Alistair Darling (then Chancellor) said: ‘I am determined that we do as much as possible to encourage entrepreneurship’.16 In this section, we therefore discuss whether CGT should be used to support entrepreneurship.

It is important to recognise that the difficulty and risk associated with entrepreneurship do not themselves justify favourable tax treatment. If the market rewards for particularly difficult or risky activities are not sufficiently high to compensate for the additional difficulty and risk involved, it suggests that the activities are not worth undertaking: there is no reason for the government to give them special tax breaks. A justification for government intervention arises only if markets fail to provide the appropriate incentives for entrepreneurship.

Markets do sometimes fail, and there is a case in principle for encouraging some types of business activity. For example, some businesses may be particularly innovative but underinvest relative to the efficient level because part of the return to investment flows to other firms which can learn from the new products or processes (i.e. there are ‘externalities’). There may also be barriers to entry or obstacles to growth of small businesses, such that the market generates too little activity in the small business sector.

But preferential rates of CGT are poorly targeted at market failures in two ways.

First, the incentives apply much more widely than where there is a rationale for government to try to increase the level of activity. CGT rates are lower than tax rates on employment for everyone, not only in those cases where there may be market failures. There is no clear reason to want to encourage investment in, for example, artwork or second homes. Even BAD relief, which is somewhat targeted, can be accessed by anyone operating a business, not only by those making significant investment or those doing something entrepreneurial. As a result, even though lower CGT rates may boost some of the activities that have externalities, at the same time they create a series of other unintended side effects. These include, for example, more people keeping income in their companies for much longer than they otherwise would.

Second, for those firms generating externalities, lower tax rates will often have little effect on incentives to invest. The benefit of lower tax rates accrues disproportionately to those who make high private returns on their activities; those are likely to be viable even without support. It is much more effective to target activities that are only borderline-viable and their specific critical features (such as investment and finance costs) where tax can make a difference to whether projects go ahead. In short, it is more effective to use the tax base.

7.5 How to fix CGT

There is a strong case for reforming the structure of CGT. This could be done in a revenue-neutral way or to raise more revenue: however much revenue the government wishes to raise, it could be raised in a fairer and less damaging way.

To recap: the design of the CGT base creates a range of problems, including disincentives to save and invest and incentives to hold on to assets for longer than would otherwise be desirable. These problems would be worse at higher tax rates. But keeping preferential rates of CGT (relative to tax on income) and differential rates across assets also creates various inefficiencies and unfairness. Moreover, low rates of CGT are not well targeted at fixing the problems caused by the tax base. Nor are they well targeted at incentivising entrepreneurship. Any change in CGT rates would, given the current tax base, come with trade-offs – some problems would be made better and some worse.

We propose the following big-picture solution to fixing the design flaws in CGT: the tax base should be changed so that there are full deductions for any amounts of money saved or invested. This is equivalent to saying that the tax base should be reformed so that the normal return to saving and investment (see Section 7.2) is not taxed. In addition, fixing the tax base would require being more generous in the treatment of losses and removing uplift of CGT at death. With a reformed tax base in place, tax rates could be increased with little concern about weakening incentives to invest and take risks. Ultimately, we advocate that overall tax rates – i.e. including all layers of tax – be aligned across all forms of income and gains in order to remove the problems caused by differential rates. This solution was originally set out in Mirrlees et al. (2011).

In this section, we summarise the components of this big-picture reform package. In Section 7.6, we discuss the types of trade-offs that arise if only some parts of the full solution are adopted. In Section 7.7, we lay out the choices that would inevitably have to be made when transitioning to a new system.

Components of reform

More generous deductions for asset purchase costs

Broadly speaking, the way to stop CGT disincentivising saving and investment (in a domestic context) is to give a full deduction for the amount saved – equivalently, to remove the normal return from tax and tax only excess returns (as defined in Section 7.2). There are three ways to achieve this outcome:

- Up-front deductions: allow the purchase cost of an asset to be tax-deductible at the time of purchase, rather than only when the asset is later sold (a ‘cash-flow’ tax treatment);

- A stream of annual deductions: give a stream of annual tax allowances that represent the normal return on the purchase cost (a ‘rate-of-return allowance’);

- Deductions at the point of sale: step up the purchase cost with an interest rate (the normal rate of return) – rather than an inflation rate as used in the past – when deducting it from an asset’s sale price to calculate the taxable gain (‘indexing for an interest rate’).

Here we briefly sketch out these three approaches. The treatment of losses is important for all three approaches and we return to that below. For a detailed discussion, including of caveats and possible reasons to choose one approach over the others, and for worked examples of the different approaches, see Adam and Miller (2021).17

The cash-flow approach. Under this approach, an individual can deduct the purchase cost of an asset from their income at the point of purchase. When they sell the asset, tax is levied on the full proceeds of sale, without deducting the purchase cost (since that was deducted up front). With a tax rate of 20%, say, the government effectively bears 20% of the cost of the investment and takes 20% of the proceeds. If the value of the proceeds exceeds the cost of the investment, then 80% of the proceeds will exceed 80% of the cost, so any investment that is profitable before tax will be profitable after tax: the tax does not discourage investment. But the government gets 20% of any return in excess of what is required to make the investment worthwhile.

The cash-flow approach is akin to the income tax treatment of pensions (but without the restrictions on when money can be accessed or the ability to take 25% of withdrawals from a pension tax-free): contributions attract tax relief at a person’s marginal tax rate, while income received from a pension is taxable. The cash-flow approach is also already in place for the self-employed when they purchase plant and machinery that qualify for the annual investment allowance: the cost of investment is fully deductible up front and any money received from the business – whether from working with the equipment or from selling it – is taxable. Adam and Miller (2021) describe in detail how a new cash-flow vehicle (which they call a Personal Shareholding Account) could be used to allow people to buy new equity (in their own or others’ companies) in a tax-neutral way.

The rate-of-return allowance. This approach would look a lot like the current capital gains tax, in the sense that there was no full up-front deduction for any amounts saved or invested and tax was levied on the nominal capital gain at the point the gain was realised. The change from the current system would be to introduce a new annual allowance equal to the normal return on the purchase cost of the asset.18 This is referred to as a rate-of-return allowance (RRA).

The logic of an RRA is straightforward. To avoid discouraging investment, the normal rate of return – the return required to persuade someone to undertake extra investment – must not be taxed; an RRA is an explicit allowance, each year, for the normal return, ensuring it is deductible from taxable income or gains. If exactly the normal return is earned, no tax would be levied. Any excess returns would be taxed in full.19 In practice, the normal return (the risk-free interest rate used to calculate the annual allowance) could be measured as the nominal interest rate on medium-term government bonds.

Indexing for an interest rate. Rather than providing an annual RRA, an alternative way the government could ensure that no tax was paid on the normal return would be to adjust the deduction that is given when an asset is sold. Specifically, the taxable capital gain could be calculated as the sale price minus the purchase price indexed (or stepped up) with the (normal) interest rate over the period the asset was held.20 This is the third way to stop CGT from disincentivising saving and investment: levy it on an asset’s sale price minus its purchase-price-plus-interest, not just its nominal purchase price. This would be a tax on excess returns.

This approach is somewhat familiar in the UK because indexation for inflation was part of CGT (in some form) from 1982 until 2008, and continued in corporation tax until 2017. The government could reintroduce indexation of capital gains, but for an interest rate (the normal rate of return) rather than an inflation rate.21

Importantly, the reform to the tax base we are advocating – regardless of which of the three approaches was used to implement it – would bring a range of benefits, including removing the disincentive to invest, removing the lock-in effect and avoiding biases between assets.22

Improve loss relief

In order to minimise the extent to which the tax system discourages risk-taking, taxes on capital gains (above normal returns to investment) should ideally be matched by equally generous relief for those making ‘losses’ (including below-normal returns).23

At present, there are various restrictions on how losses can be offset. Capital losses can usually only be offset against capital gains, even in the same year, and can be carried forward indefinitely but only carried back in very limited circumstances.

There are various ways that loss relief could be made more generous. Broadly speaking, these include: allowing carry-back as well as carry-forward; carrying losses forward (and back) with interest to maintain their present value; and letting people offset their capital losses against income rather than capital gains in a wider range of circumstances (although losses should never be offset at a higher rate than corresponding income/gains would be taxed). There are genuine concerns about the use of artificial losses for tax evasion and avoidance. Care is therefore required in changing the treatment of losses. But we are confident that some improvements are possible.24

Abolish uplift at death

Currently, if someone keeps an asset until they die then no capital gains tax is levied on any rise in its value from when it was acquired until death. This uplift of CGT at death should be abolished.

Uplift at death provides a huge incentive for people to hold on to assets that have risen in value, even if, in the absence of tax considerations, they would prefer to sell them and use the proceeds in some other way, and even if someone else could use the assets more productively. And the ability to escape tax in this way provides a big incentive to set up a business and roll as much money as possible into it, rather than working as an employee. These incentives would be exacerbated if tax rates on capital gains or income were increased. Abolishing uplift at death would therefore reduce some distortions in its own right, but it would also remove one of the downsides of moving towards alignment of tax rates across different forms of gains and income. Removing uplift at death should be prioritised as one of the first steps taken towards the long-run ideal we set out above.25

There are two ways to remove CGT uplift at death. Those inheriting assets could be deemed to acquire them at their original acquisition cost, rather than at market value at the date of death. They would therefore pay CGT on the full gain when the asset was sold. Alternatively, an asset could be treated as if it had been sold at the point of death, such that the deceased’s estate was liable for CGT at the point of death and the individual inheriting the asset would be treated as if they had immediately bought the asset at its market value on the date of inheritance (‘deemed realisation’).

These reforms would mean that CGT would sometimes be payable on top of inheritance tax (and, under the second option, at the same time). That is not a flaw. CGT and inheritance tax are serving different purposes – inheritance tax is not a substitute for CGT. On death, if an asset has accrued gains, it is appropriate to tax these just as much as if the asset were sold the day before death, when it would currently be taxed.

Align rates

Economic inefficiency and unfairness are caused both by different types of assets’ facing different CGT rates and by CGT rates’ (almost always) being lower than tax rates on income, including dividends for those in the higher- or additional-rate tax bands and employment income.

Ultimately, we advocate aligning marginal tax rates across all forms of gains and income, while making changes to the tax base (as outlined above).26 That is, we recommend aligning rates not only within CGT (across assets) but across capital gains, capital incomes and employment income.27

When looking to align rates, or move towards that goal, it is important to consider all layers of tax. It is only by aligning overall rates – including all layers of tax – that a level playing field can be created. Within CGT, this means accounting for corporation tax such that the CGT rates on shares would be lower (to account for corporation tax levied on the underlying profits) than the rates on other assets.28 When considering the rates that apply to employment income, one must account not only for income tax but also for employee and employer National Insurance contributions (NICs). The combined rates of tax on different income sources are shown in Table 7.2 (note that income tax rates differ in Scotland).29 Full alignment would require that within the basic-, higher- and additional-rate bands, all of the rates be the same across sources of income and gains.

Table 7.2. Combined marginal tax rates by income form, 2024–25

Source of gains | Basic rate | Higher rate | Additional rate |

Carried interest | 18% | 28% | 28% |

Residential property | 18% | 24% | 24% |

Non-corporate business assets (BADR) | 10% | 10% | 10% |

Corporate business assets (BADR / IR) |

|

|

|

with 19% corporation tax | 27.1% | 27.1% | 27.1% |

with 25% corporation tax | 32.5% | 32.5% | 32.5% |

Other assets – not shares | 10% | 20% | 20% |

Other assets – shares |

|

|

|

with 19% corporation tax | 27.1% | 35.2% | 35.2% |

with 25% corporation tax | 32.5% | 40.0% | 40.0% |

Exempt assets, and all gains unrealised at death | 0% | 0% | 0% |

Source of income |

|

|

|

Employment | 36.7% | 49.0% | 53.4% |

Self-employment profits | 26% | 42% | 47% |

Rent and interest | 20% | 40% | 45% |

Dividends |

|

|

|

with 19% corporation tax | 26.1% | 46.3% | 50.9% |

with 25% corporation tax | 31.6% | 50.3% | 54.5% |

Note: BADR stands for business asset disposal relief. IR stands for investors’ relief. We show marginal combined rates including (where relevant) corporation tax at the 19% small profits rate and the main 25% rate. Employment income includes employee and employer National Insurance contributions. Self-employed profits include self-employed National Insurance contributions. Income tax rates are different in Scotland; employment and self-employment lines shown here apply in the rest of the UK.

Tax rates could be aligned at any level; rates on employment income could be reduced while rates on capital gains (and capital income) were increased. If CGT rates were aligned with current (overall) tax rates on labour income, it would require very large rate increases. For example, the rate on ‘other assets – not shares’ within the higher-rate band would need to be increased from 20% to 49%. For shares (which fall within ‘other assets’), and if accounting for corporation tax at 19%, the rate would need to be increased from 20% to 37% (such that the overall rate moved from 35.2% to 49%). As part of alignment, BAD relief would need to be removed. We take no stance on the overall level of tax rates. But we note that, in practice and since employment tax rates are not going to be levelled down to capital gains tax rates (it would represent a huge tax cut), aligning rates (as laid out in our ‘big-picture’ solution) would include substantially higher CGT rates.

International issues

Higher CGT would make the UK a less attractive place for people to live at the time they realised a capital gain. It would affect incentives to work and invest in the UK only to the extent that those are linked to where people live when they realise a capital gain – though there are undoubtedly some such links: for example, people running a business tend to work and invest in the country they live in, and may be reluctant to emigrate purely for tax reasons when they want to sell the business. Non-residents (and corporate investors) investing in the UK would be unaffected by reforms to CGT, except insofar as they applied to investments in UK land and property.

Higher effective rates of UK CGT would thus increase both the incentive for individuals with accrued but unrealised capital gains to leave the UK and the disincentive for such individuals to come to the UK. One option to address this would be for the UK to introduce ‘deemed disposal on departure’ for CGT purposes, matched by ‘rebasing on arrival’ for new arrivals.30 This would ensure that all gains accrued by an individual whilst UK-resident are taxed in the UK, even if they subsequently moved abroad, but would correspondingly exempt from CGT any gains accrued prior to arrival.

- Rebasing on arrival (ROA) works by granting new arrivals (or returners) to the UK a ‘rebasing’ of their assets to their value at the date of arrival, so that only rises in value after they arrive are subject to UK CGT.

- Deemed disposal on departure (DDD) works by treating individuals who leave the UK (i.e. become non-resident for tax purposes) as having disposed of their assets at the end of their final year of residence, thereby bringing into CGT all of the gains that they accrued whilst UK-resident even if they have not made an actual disposal.

In combination, ROA–DDD would in effect move CGT from taxing gains realised while living in the UK to taxing gains accrued while living in the UK. There are practical challenges with this approach: for example, it would require valuing assets at the points of arrival and departure; and DDD could create cash-flow difficulties for some of those leaving the UK who face a CGT liability despite not selling their assets (though there are possible ways to mitigate this). There would be a number of other difficult design issues to negotiate, beyond the scope of this chapter. But it would clearly be feasible for the UK to adopt ROA–DDD, since the policy is already in operation in Australia, Canada and elsewhere.31 The UK is unusual internationally in having no CGT charge on emigrants (unless they move back to the UK within six years).

While ROA–DDD would help to address the concern that higher CGT would lead people to realise gains outside the UK (eating into the potential revenue yield of the tax rise), it would not address the concern that higher CGT rates would lead people to accrue gains outside the UK – that is, to live outside the UK while they work and invest to generate capital gains. Indeed, by making it harder for people to live in the UK and accrue gains here without paying CGT, it might make that problem worse. This is similar to the effect that (for example) increasing income tax rates can have on internationally mobile individuals, but for business owners and investors rather than top-earning employees. The likely aggregate impact should not be overstated, though: relatively few of those making large capital gains ever move countries. And people’s decisions over where to live while they work and invest to generate capital gains may be less responsive to taxation than decisions over where to live when they realise those gains.

Potential emigration is therefore a consequence to bear in mind when increasing CGT rates (like international mobility matters for other taxes, to varying degrees) – though note that, on the flip side, more generous deductions for investment would make the UK a more attractive place for investors to live. But concerns about the mobility of a small number of people should not stop the government from moving towards alignment of tax rates across sources of income and capital gains for the wider UK population. Low rates of CGT across the board are not well targeted at attracting internationally mobile individuals. Most CGT revenue does not come from highly mobile groups, and it is not clear that mobility is closely linked to capital gains specifically (rather than high incomes, or particular industries or activities, or the treatment of those arriving or leaving).

Simplification

CGT is complex. It creates a large burden on taxpayers and on HMRC. Some of the components we have laid out – notably, implementing an RRA or moving to a form of indexation – would add a small amount of further complexity. Although it is worth noting that we do not envisage anything like the complexity that arose under the previous system of indexation, not least because modern IT would make implementing the system significantly less costly. But our big-picture solution would be a substantial simplification overall. Moving towards neutrality reduces the need for – or at least takes the pressure off – boundaries in the tax system and therefore the need to have rules to police those boundaries. For example, under the full solution, there would be no tax incentive to shift between income and capital gains such that it would not really matter whether carried interest or share buy-backs were treated as generating income or capital gains. Significant legal simplification would come from obviating the need for whole swathes of existing anti-avoidance legislation.

In practice, the extent of remaining complexity would depend on which specific reforms were pursued – a cash-flow approach would be simpler than an RRA, for example – and on any transitional arrangements (see Section 7.7).

7.6 Trade-offs and options when making partial reforms to CGT

The previous section set out the components of a fully reformed tax regime for capital gains and income. In the big-picture solution, the tax base changes would apply to all investments, regardless of whether they went on to generate capital incomes or gains. And rate alignment would take place not only within CGT but also in relation to income taxes. A fully reformed system represents a significant prize. It would be less distortionary – and therefore more growth-friendly – because tax would no longer be as much of a driver of how people choose to work or realise returns to their efforts or investments, of asset choices or of the timing of transactions. Since there would be no big tax differences between similar activities, there would be little need to police boundaries and the system would be much fairer.

But, even if the government accepted this as the right end goal, it is unlikely that it would make all of the changes in the upcoming Budget. More likely is that the government would choose to reform some rates or elements of CGT, possibly leaving the rest of the tax system (i.e. outside CGT) unchanged. In this case, trade-offs would inevitably arise. Here we briefly highlight some of the main trade-offs.

- Reforms to the CGT tax base that provide more generous deductions for purchase costs or losses would reduce distortions and reduce disincentives to invest. But these reforms would cost money (and be a giveaway to relatively rich people). If the government wishes to raise revenue, it will need to do at least some rate rises alongside these base reforms.

- Increases in rates of CGT without removing uplift at death would increase the incentive to hold on to assets until death. We argue that uplift at death should be removed regardless of what other reforms are planned.

- Increases in rates of CGT without changes to the tax base would lessen some distortions, including the incentive to work through one’s own business rather than be employed and to realise the returns to investment in the form of gains rather than income, but worsen others, including weakening investment incentives and exacerbating the bias against risk-taking and the lock-in effect. And recall that distortions caused by the tax base rise more than in proportion to tax rates, because low tax rates only change behaviour when the decision is marginal anyway whereas higher tax rates discourage not only more activities, but also more valuable activities.

- Different sources of income are taxed at different rates, so if rates of CGT are changed but tax rates on income are not,32 tax rate differentials (and the associated distortions they cause) will inevitably persist across different types of income and gains. If the government wanted to align the tax rates on gains with the rates on income, it would have to choose which source of income to align with. For example, self-employed profits and dividends are taxed at particularly low rates relative to employment income within the basic-rate tax band (see Table 7.2 earlier). In this case, CGT rates could in principle be moved towards alignment with any of the tax rates on income. If they were aligned (within the basic-rate band) with tax rates on employment income, there would be a strong incentive to take investment returns in the form of dividends rather than capital gains. If they were aligned with dividend tax rates, there would continue to be a tax penalty on employment.

- Higher rates of CGT would weaken work incentives – for example, by increasing the tax on owner-managers’ labour supply. (Although note that employees’ labour supply would still be taxed more heavily. And increasing tax on capital gains while reducing tax on employment income could even out the treatment of different forms of remuneration without increasing tax on work overall.)

There are many ways in which partial reforms could be done. Here we discuss just two options that would combine reforms to the tax base and to tax rates, assuming that the government will not change tax rates outside CGT.

Advani, Lonsdale and Summers (2024b) also discuss possible reform options and lay out estimates of the revenue and distributional effects of increasing CGT rates while making various changes to the tax base.

Example: index for inflation and align CGT rates with income tax

As part of the big-picture solution, we recommend giving more generous deductions for asset purchase costs. This could be done in several ways, including by introducing an RRA or (equivalently) indexing for an interest rate.

The UK has previously operated a CGT with indexation for inflation. Reintroducing indexing for inflation would eliminate the sensitivity of investment decisions to inflation and would alleviate (but not remove) the disincentives to save/invest, and the lock-in effect. While it would not remove all problems, inflation indexation could be seen as a step towards indexing for an interest rate, and therefore a step in the right direction.

Alongside this partial base reform, the government could increase CGT rates, but not go as far as full alignment with overall tax rates on employment income.

Assuming that only CGT rates are changed, one option would be to align CGT rates with income tax rates. Specifically, that would mean having two sets of CGT rates (illustrated in Table 7.3). The basic, higher and additional rates of CGT would be 20%, 40% and 45% respectively (matching ordinary income tax rates) for all assets except shares, for which they would be 8.75%, 33.75% and 39.35% (matching the special rates of income tax on dividends). This would be a reduction in the CGT rate on shares for basic-rate taxpayers, and an increase in the rate for other assets and other taxpayers.

Table 7.3. An illustration of a potential reform to CGT rates

Source of gains | Basic rate | Higher rate | Additional rate |

All assets except shares | 20% | 40% | 45% |

Shares | 8.75% | 33.75% | 39.35% |

Effective rate on shares |

|

|

|

With corporation tax at 19% | 26.1% | 46.3% | 50.9% |

With corporation tax at 25% | 31.6% | 50.3% | 54.5% |

Note: Headline corporation tax rate is 25%. The small profits rate is 19%.

Source: Authors’ calculations.

CGT rates would be lower for shares than for other assets – just like income tax rates are lower for dividends than for other income – to reflect corporation tax. This is more logical and defensible than the current system where CGT rates depend on the ownership of the business rather than on whether the business profits are subject to corporation tax (and are arbitrarily higher for second and rental homes). Aligning CGT rates with income tax rates is also relatively easy to explain.

This reform would not produce full alignment of tax rates on capital gains across all assets: the effective tax rate (after accounting for corporation tax) would be higher on shares than on other assets. But the alignment across assets would be much closer than it is now, and for the most part this reform would act to align the tax rates on capital gains with those on capital incomes from the same assets.33

This would rationalise the system and move closer towards overall alignment. Within the current system it is hard to understand why capital gains on shares should be taxed more than dividends at the basic rate but less than dividends at the higher rate; or why ordinary income and dividends are subject to basic, higher and additional rates of tax while capital gains are subject only to basic and higher (no additional) rates.

Taken as a package, introducing indexation for inflation and aligning CGT rates with income tax rates would be more efficient and fairer than the current system. Employment income would still be taxed at higher rates than capital incomes or gains – largely as a result of employer National Insurance contributions – but the disparity would be smaller.

Example: scrap BAD relief and introduce up-front relief for investment

We showed in Section 7.2 that around half of taxable capital gains (by value) come from unlisted shares. Many of these will benefit from business asset disposal relief, the existence of which creates very strong incentives to operate via a business and to take returns (including returns to labour) in the form of capital gains rather than income, where possible.

BAD relief (and preferential rates of CGT more generally) is not well targeted at entrepreneurship (see Section 7.4) and leads to a range of undesirable distortions (Section7.3). Simply removing BAD relief in isolation would come with trade-offs: distortions caused by rate differentials would be lessened (e.g. there would be a reduced incentive to take returns in the form of capital gains) but distortions related to the base would be worse (a higher rate would weaken investment incentives and exacerbate the bias against risk-taking and the lock-in effect). Removing BAD relief would also weaken work incentives by increasing the tax on owner-managers’ labour supply (although note it would still be taxed less heavily than for employees).

The downsides of that trade-off could be greatly reduced if BAD relief were scrapped while deductions for asset purchase costs were made more generous.

Adam and Miller (2021) set out one specific option for providing more generous tax treatment of investment in shares. They describe a new vehicle – which they call a ‘Personal Shareholding Account’ (PSA) – that would provide a cash-flow tax treatment (as described in Section 7.5) when people bought newly issued shares. Individuals would receive up-front income tax relief on any money they put into a PSA. Money in the PSA could be used to buy new equity issued by companies, and any dividends or capital gains received within the PSA would not be taxed. But any money the individual withdrew from the PSA would be subject to tax at that point. (Note there would be a single tax rate schedule with no distinction between dividends and capital gains.) That is identical to the current income tax treatment of pensions, except that there would be no 25% tax-free lump sum. The PSA could also be likened to an ISA or to one of the current venture capital schemes (EIS/SEIS/VCTs).34 Unlike any current vehicles, however, it would be available – indeed, intended – for people to invest in their own company (or that of a connected person), not just for arm’s-length shareholders. In that respect, it could also be thought of as a replacement for BAD relief – a reorienting away from tax relief on large gains to tax relief on investment. Importantly, the PSA would be better targeted: it would be available to business owners making new investments at the point they invest and in proportion to the amount they invest, rather than available to all business owners regardless of investment, only many years in the future, and worth more to those who make the most money.

In principle, there would be no need for restrictions on when a PSA could be used: the PSA would be well suited to portfolio investment in the stock market and, since it offers neutral rather than subsidised treatment, there seems little reason to limit the investments. Keeping the availability of the scheme as wide as possible would maximise the economic benefits and help to make the scheme better known. But if the government wanted to ‘test the water’, or were concerned about the potential size of up-front tax relief (although it would get correspondingly more revenue later from taxing withdrawals), then it could impose additional restrictions on PSAs, such as limiting eligible investments to shares in unlisted companies or imposing a cap on the amount that could be invested.

Miller and Smith (2023) empirically estimate the impact on business owners of removing BAD relief (taxing eligible gains at the main 20% rate rather than 10%) while moving to a cash-flow treatment of investment in their own business (i.e. giving individuals up-front income tax relief on any money they put in).35 They find that:

- Removing BAD relief brings benefits (most notably, there is a substantial reduction in people keeping income in their companies for long periods) but leads to a small fall in investment – this is exactly the trade-off we discuss above. It is debatable whether this move, in isolation, would be an improvement.

- Introducing a new up-front relief boosts investment. Moreover, with the new relief in place, the higher rate of CGT has no disincentive effect on investment. (This assumes that there is no effect on people moving their capital into or out of the UK.)

The two measures implemented together work to boost investment and to raise a modest amount of revenue. It is a progressive change: revenue is raised from the top of the income distribution. More specifically, it is raised from people that have made very large gains relative to their investments. Those making large investments and making modest (‘normal’) returns see a tax cut.

7.7 Transition and retrospection

Whatever changes were made to CGT, a decision would have to be made over how to treat existing assets.

The simplest way to introduce reforms to CGT would be to apply them in full to any capital gains realised after the date the reforms were announced. One consequence of this approach would be that higher rates – and any changes to the tax base (such as indexation) – would apply to gains that accrued when the previous system was in place but were realised afterwards, as well as to future investments and accruals. In this scenario, part of the net revenue raised would therefore derive from taxpayers’ past activities rather than their future ones. This is the way that most (although not all) reforms to CGT have been applied in the UK in the past, and is a natural consequence of CGT being a realisation-based, rather than accrual-based, tax.

In economic terms, this is an efficient way to raise revenue: since there is nothing taxpayers can do to change the past, this part of the revenue is raised without distorting people’s behaviour. Taxing the returns to past investment and effort cannot discourage them as they have already happened.

However, the flip side of this is that taxpayers may object that the tax is, in a sense, retrospective. They may have expected the existing CGT regime to persist when they invested and worked to generate the capital gain: the higher tax rate would be applied to gains that had already accrued.