Downloads

Download the report as a PDF

PDF | 670.6 KB

Key findings

1. Local authorities in England have budgeted £24.5 billion for spending on adult social care services in 2024–25. Around half of this spending goes towards support for working-age adults and around half goes towards support for adults aged 65 and above. Adult social care spending now accounts for more than 40% of all local authority spending on services.

2. Eligibility for government support towards adult social care costs in England is subject to both a financial means test and a needs test. That is, publicly funded adult social care is rationed in two ways: only those with limited financial resources and assessed social care needs above a certain threshold qualify for support from their local council. Both the means test and the needs test have become more stringent in the last 15 years. There is no cap on the costs that an individual can incur. Around one-in-seven 65-year-olds can expect to incur lifetime care costs of more than £100,000, but individuals have limited ability to protect themselves against extremely high care costs. This is the ‘insurance problem’ in social care.

3. The new Labour government has decided not to proceed with the previous government’s adult social care reforms, which would have seen the introduction of a lifetime cap on adult social care costs and a more generous financial means test. As a result, despite decades of handwringing, the insurance problem in social care remains unresolved. This is not an area in need of new technical solutions – the solutions are already known and well understood; it is a question of political priorities.

4. The introduction of a lifetime cap on care costs, while welcome, would not be a comprehensive solution to all of the sector’s ills. Whether or not the charging reforms had gone ahead, there are numerous knotty issues in need of policy attention and political will. In other words, completely aside from whether we have some sort of lifetime cap on care costs, there are outstanding questions around the social care workforce, the stringency of the needs test, rapidly growing demand for care among working-age adults, geographic variation in provision, and much else. Scrapping the charging reforms does not park adult social care as an issue.

5. Demand for care services among working-age adults is growing quickly: the number of new requests for support from individuals aged 18–64 grew by 18% between 2014–15 and 2022–23 (more than three times faster than population growth for that age group), alongside sharp increases in disability benefit claims. These trends signal growing pressure on social care services for younger adults, in addition to the more commonly discussed pressures from an ageing population.

6. In fact, despite significant growth in the older population, the number of older people receiving state-funded care in England has dropped by 10% since 2014–15 due to tightening eligibility criteria, and we estimate that public spending on adult social care failed to keep pace with demographic pressures between 2009–10 and 2022–23. Looking ahead, to meet demand pressures (particularly from an ageing population) and rising costs, the Office for Budget Responsibility projects that UK-wide public spending on adult social care would need to increase by 3.1% per year in real terms over the next decade. After adjusting for savings from the scrapping of charging reforms, that would see spending rise from 1.3% of national income in 2023–24 to around 1.5% in 2033–34 (and then to 1.9% in 2053–54 and 2.2% of national income in 2073–74).

7. Adult social care is the responsibility of 153 local authorities in England, increasingly funded by local council tax revenues since 2010. It therefore matters not just how much is spent at a national level, but where it is spent. In the absence of a well-functioning local government finance system, there is a risk of a severe mismatch between local funding and local needs. This will be of particular importance if the government is serious about introducing a ‘National Care Service’ with consistent service provision across the country. At a minimum, the government should commit to implementing, and keeping up to date, new formulas for assessing councils’ spending needs (existing funding is to a large extent based on formulas last updated in 2013 and in some cases, rather ridiculously, using data from as far back as 2001).

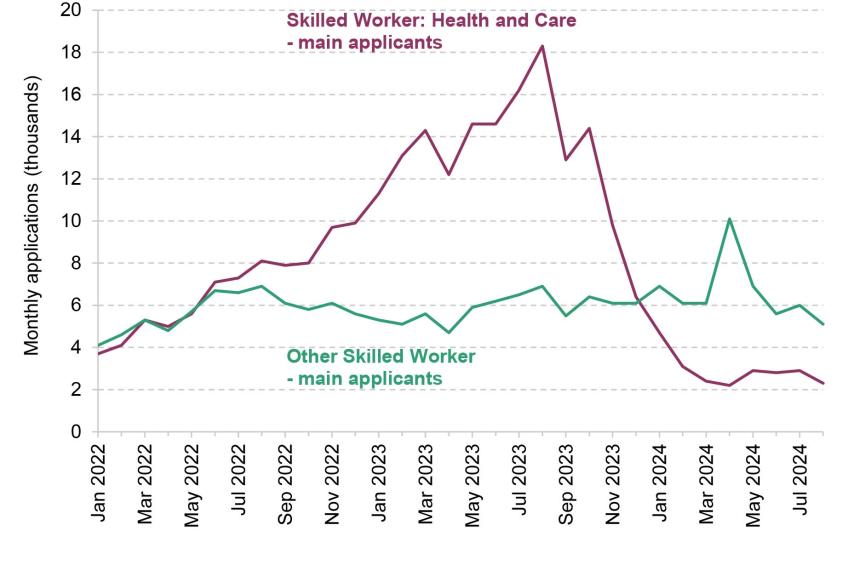

8. Immigration policy significantly affects the adult social care workforce in the UK, with a growing proportion of employees from non-EU countries, now comprising 16% of the workforce, while EU worker representation has decreased. Monthly applications for Health and Care Worker visas have plummeted from an estimated 18,300 in August 2023 to 2,300 in August 2024. The new government has given no indication that it plans to reverse the previous government’s tightening of eligibility for these visas. The trade-off here is a simple one. If the government wants to decrease the number of migrants entering the care sector, it must be prepared either to accept a smaller workforce (i.e. a deterioration in care quality and/or coverage) or to boost the funding allocated to local authorities to raise wages and attract more domestic workers.

9. Successfully implementing various proposed policies and initiatives for the sector – such as the ‘Fair Cost of Care’ reforms and the new ‘Fair Pay Agreement’ aimed at raising fees for providers and wages for care workers, respectively – will likely necessitate additional funding from the government. Without more detail on what these policies (particularly the Fair Pay Agreement) will entail, it is impossible to say how much more funding. The structure of the adult social care market complicates policy in this area. Only one-in-six care workers are employed directly by the public sector. A large majority of care home beds are provided by the private and voluntary sectors, with a significant role for a small number of large providers (the largest 30 care home providers supplied 30% of overall capacity in 2017) and for private equity (which owned approximately 13% of for-profit care home beds as of 2022).

10. Individuals who provide at least 35 hours of care a week may be eligible for carer’s allowance of £81.90 per week. Currently, if the carer earns more than £151 per week after tax, they no longer qualify. This cliff-edge is highly undesirable and can lead to cases where individuals have to repay large amounts to the Department for Work and Pensions if their earnings edge above the threshold. It would be better to have the £81.90 per week automatically adjust to earnings and be subject to a gradual taper (akin to the taper in universal credit).

5.1 Introduction

The adult social care sector is large, important and growing. In England alone, local authorities spend more than £20 billion on care services for more than three-quarters of a million adults each year. Hundreds of thousands more do not receive state support but pay privately towards their care.

The sector is also marked by its complexity. Care is provided formally, by trained professionals (the sector employs more than 1.5 million people), and informally, by family and friends (an estimated 5 million people provided at least some informal care in 2021), and often by some combination of the two. Of those trained professionals, a majority work in the private sector, with only around one-in-six employed directly by the state.

Eligibility for local authority funding towards social care costs in England is governed by both a needs test and a means test. The former means that only those with the most severe care needs qualify for state support. The latter means that council funding is provided only to those with financial assets below £23,250: above that level and people must ‘self-fund’. For some people, the value of their home will count towards that asset test; for others, it will not. Even those with assets below the threshold are expected to contribute from their income. Around one-in-seven people at the age of 65 can expect to incur lifetime care costs of more than £100,000, and individuals have extremely limited ability to protect themselves against those costs. This is a far cry from the relative simplicity of a universal, free-at-the-point-of-use, health service.

This complexity, coupled with a lack of political will, is perhaps why – despite decades of handwringing and promises of reform – the ‘insurance problem’ in social care remains unsolved. The previous government legislated for a set of reforms, set to be rolled out from October 2025, which were to increase substantially the generosity of the financial means test and to introduce a lifetime cap on care costs. During the election campaign, the Labour Party promised to introduce a ‘National Care Service’ and a ‘Fair Pay Agreement’ for adult social care, with close to no details on what those policies might mean in practice. The manifesto did not explicitly commit to go ahead with the previous government’s charging reforms, but some of the party’s statements strongly indicated that it would1. The Conservatives and Liberal Democrats also committed to the reforms during the campaign.

Then, in Rachel Reeves’s spending audit on 29 July, the new Chancellor declared that ‘it will not be possible to take forward these charging reforms’, with the accompanying document stating that ‘the reforms are now impossible to deliver in full to previously announced timeframes’ (HM Treasury, 2024). The new government faces enormous spending pressures, and it is reasonable to decide to prioritise other public services or different groups within society. But the decision to once again kick sorely needed social care reform into the long grass is disappointing and just the latest in a long string of sorry episodes. The insurance problem within social care remains unresolved. It could and should have been addressed a long time ago.

Yet, the introduction of a lifetime cap on care costs is not a comprehensive solution to all of the sector’s ills. Whether or not the charging reforms had gone ahead, there are several knotty issues in need of policy attention and political will. In other words, completely aside from whether we have some sort of lifetime cap on care costs, there are outstanding questions around the social care workforce, the stringency of the needs test, rapidly growing demand for care among working-age adults, geographic variation in provision, and much else besides. Scrapping the charging reforms does not park adult social care as an issue.

In this chapter, we set out the current state of the adult social care system and its key features. Section 5.2 describes the adult social care system in England. Section 5.3 considers the nature of the insurance problem within social care and the details of the proposals recently scrapped by Ms Reeves. We then turn in Section 5.4 to some of the looming policy challenges under the status quo, grouping these into five broad and interrelated categories: (i) funding and demographic pressures; (ii) interactions with local government finances; (iii) ‘Fair Cost of Care’ reforms and payments to providers; (iv) the adult social care workforce, including immigration and pay; and (v) support for informal carers. We conclude in Section 5.5 by exploring potential future developments for the sector.

Throughout, the focus is on England and the English system, recognising that this is a devolved issue across the UK, and that any decisions on adult social care in this autumn’s Budget and Spending Review – if there are any – will primarily affect England. While many challenges are shared across the four nations, and we occasionally reference changes introduced by the devolved governments of Scotland, Wales and Northern Ireland, a comprehensive analysis of the specific issues facing each part of the UK would be beyond the scope of a single chapter. Some of these key differences are nonetheless worth noting: Scotland offers free personal care; Wales has a more generous means test and a weekly cap on domiciliary care costs; and Northern Ireland operates with a cap on costs managed by health and social care boards rather than local government. Each of these provides possible directions of future travel in England.

5.2 A beginner’s guide to adult social care in England

Adult social care refers to a broad range of non-medical services provided to support individuals with illnesses or disabilities that cause them to have difficulties with activities of daily living, such as washing, eating, getting dressed and using the toilet, as well as general mobility. This includes older adults – who tend to feature most heavily in the debate – but also a considerable number of younger adults, who tend to have more intensive care needs (e.g. due to a severe learning disability). Most social care is provided informally by family, friends and neighbours. For individuals with more substantial needs, or those for whom informal care is not available, formal care is provided by paid carers and may be funded publicly or privately (self-funding).

The focus of this chapter is the publicly funded adult social care system. Before considering possible reforms (including those recently scrapped by the new government), we set out some of the key features of the current system and consider recent trends in spending and provision.

Key features of the system

A local, not a national, responsibility

Publicly funded adult social care in England is largely the responsibility of local, not national, government. The main exception to this is NHS Continuing Healthcare, discussed in Box 5.1 later. There is no England-wide budget allocated to adult social care, nor any ‘national care service’ akin to the NHS. Instead, it is decentralised and arranged and funded by 153 local authorities with responsibility for social care within their geographic areas. These local authorities are subject to statutory requirements which establish a minimum standard regarding duties and needs assessments, but the interpretation and implementation of these can differ widely depending on local priorities and resources. Local authorities are funded by a combination of grants from central government and local tax revenues, and they retain considerable discretion over the services provided in their area (including the extent to which to prioritise adult social care relative to other services, subject to meeting their statutory requirements).

Since 2010, spending on adult social care has been shielded from cuts relative to other services provided by local authorities (in part because of the statutory duty to provide certain care services). As a result, it has grown to account for a larger share of local authority budgets – from around 35% of all service spending in 2010–11 to around 40% in 2015–16 and around 42% in 2023–24 (Ogden and Phillips, 2024a).

Means-tested and needs-tested

Public funding for adult social care is available only for those with care needs above a certain threshold and limited financial means. In other words, it is subject to both a needs test and a means test. The latter has both an asset and an income component.

Individuals with assets, savings and other capital of £23,250 (the ‘upper capital limit’) or more are ineligible for state support and are expected to meet the full costs of their care until their assets fall below the threshold. There is no limit to the lifetime costs that an individual can face before qualifying for state support. Their main residence is excluded from this asset test if they, their partner or another dependant continues to live in that home.2 Those with assets above £14,250 (the ‘lower capital limit’) but below £23,250 are eligible for partial support: the council pays for a portion of care costs according to a sliding scale, with individuals charged £1 per week for every £250 of assets above the £14,250 threshold (a charge known as ‘tariff income’). Those with assets below £14,250 are not expected to contribute from their assets towards the cost of their care and are not charged any ‘tariff income’.

How mean is the financial means test? Data from the English Longitudinal Study of Ageing (ELSA) suggest that that only 13% of adults aged 65 and above (20% of adults aged 85 and above) had wealth below the upper capital limit (£23,250) in 2018–19. This includes housing wealth, and so is the relevant measure for those entering residential care without a partner or dependant living at home (and so whose main residence would be included in the asset test). When considering those with a partner or dependant living at home (and so whose main residence would be excluded from the test) and individuals in receipt of domiciliary (in-home) care, a more relevant measure would be wealth excluding housing wealth. On this measure, 43% of those aged 65 and above (51% of adults aged 85 and above) have wealth below the upper capital limit. Either way, at a given point in time, most older adults have sufficient assets to be ineligible for local-authority-funded social care.

One reason for this is that the value of the asset thresholds (the lower and upper capital limits) has been frozen in cash terms since 2010–11, at £14,250 and £23,250 respectively. The real-terms value of these thresholds has therefore fallen considerably, during a period when asset prices have risen. Had they been increased in line with the Consumer Prices Index (CPI) since 2010–11, they would have risen to approximately £20,800 and £33,900 in 2023–24, some 46% higher. The means test is becoming more stringent and less generous over time in real terms. Fewer adults are eligible for publicly funded care than would otherwise have been the case (had the thresholds been uprated with inflation).

Even if someone qualifies for local authority funding on the grounds that they have assets below the upper capital limit, they are still required to contribute from their income, including pension3. This is subject to a minimum income floor, an amount that the individual must be left with after making their contribution. For those receiving care in a care home, this is the personal expenses allowance (PEA), set at £30.15 per week for the 2024–25 financial year; for those receiving care in other settings, the floor is the minimum income guarantee (MIG), which varies according to age and circumstances. The MIG rate for a single adult who has attained pension credit age, for example, is £228.70 per week4. This is slightly higher than the minimum level of £218.15 to which a single adult in receipt of pension credit would have their income topped up (UK Government, 2024).

The Care Act 2014 requires local authorities to assess individuals’ care needs against national eligibility criteria, though local authorities set their own assessment procedures and have discretion to provide care to those with needs that do not meet the nationally set criteria. Alongside an increasingly stringent means test, the stringency of the needs test also increased over the first half of the 2010s, as councils responded to funding cuts by restricting support to those with the highest assessed needs (House of Commons, 2017).

There is also evidence to suggest that councils interpret and implement these criteria differently (Ogden and Phillips, 2023). In 2022–23, for example, just under half (48%) of individuals aged 65 and over who requested support received some sort of short-term or long-term care from their council. But in one-in-ten local authorities, fewer than a third of those requesting support ended up receiving some, while another one-in-ten local authorities provided support to more than 70% of those requesting it (NHS England, 2023a). Considerable local discretion remains.

The latest figures for 2022–23 indicate that 72% of individuals aged 65 and above receiving community care services (i.e. care outside of a care home) had that care funded by the state (Office for National Statistics, 2023a). In care homes providing care for those aged 65 and above, 51% were in receipt of state support (Office for National Statistics, 2023b). These figures are in line with government estimates in 2022, which suggested that around half of older adults in care received state support towards their care costs (Prime Minister’s Office, 2022).

Given the stringency of the asset test (discussed above), these high percentages receiving state support may seem surprising. In large part, they reflect the fact that individuals in greater need of social care tend to be less wealthy than the older population at large. Some of the individuals in receipt of state support will have assets above the upper capital limit but have their care provided via NHS Continuing Healthcare (see Box 5.1). Others will have previously had assets above the limit, but have run down their assets over time, eventually becoming eligible for state support. For many care recipients, their main residence will not count towards the asset test and, as mentioned above, a much larger fraction of people have assets below the £23,250 threshold when housing assets are excluded. These (and other) factors explain the seeming discrepancy.

Box 5.1 NHS Continuing Healthcare

If an individual has both health and social care needs but is assessed as having a ‘primary health need’, then the National Health Service has responsibility for arranging and funding all of that person’s care (both healthcare and social care) via NHS Continuing Healthcare. NHS England budgeted £6.5 billion for these services in 2023–24 (UK Parliament, 2023), around 4% of the total NHS budget for the year. The total number of people assessed as eligible for NHS Continuing Healthcare was 28,838 in the first quarter of 2024–25 (NHS England, 2024).

Unlike access to local-authority-funded adult social care, access to NHS Continuing Healthcare is not means tested: an individual’s income or wealth has no bearing on whether or not they qualify for care.

Access is subject to a needs test – the assessment of whether the applicant has a ‘primary health need’. A national framework, introduced in 2007, provides guidance for such assessments. It states that ‘an individual has a primary health need if, having taken account of all their needs … it can be said that the main aspects or majority part of the care they require is focused on addressing and/or preventing health needs. Having a primary health need is not about the reason why an individual requires care or support, nor is it based on their diagnosis; it is about the level and type of their overall actual day-to-day care needs taken in their totality’ (Department of Health and Social Care, 2022b).

Individuals with a rapidly deteriorating condition are eligible for ‘fast-track’ support without the need for a full eligibility assessment. Of those who did undergo a full assessment over the first quarter of 2024–25, one-in-five (20%) were found eligible (NHS England, 2024).

There is considerable geographic variation in this ‘assessment conversion rate’. Just 9% of those assessed in Herefordshire and Worcestershire in the first quarter of 2024–25 were found eligible, versus 34% in Dorset (NHS England, 2024). In other words, just as with eligibility for council-funded care, there remains a great degree of local variation despite there being a national framework – variation that is unlikely to be entirely explained by differences in local need.

For individuals who would not otherwise be eligible for public support, the outcome of the eligibility assessment can have considerable financial consequences. If found to have a ‘primary health need’, the NHS will pay for all costs of their social care; if not, the individual may have to spend many thousands of pounds from their income or savings.

Some individuals who are not eligible for NHS Continuing Healthcare but require care from a registered nurse can receive financial support from the NHS-funded Nursing Care programme which provides a fixed weekly contribution (£235.88 as of April 2024 for most) towards nursing care in a care home.

Among younger adults, most care recipients do receive state support. Of those working-age adults (18–64) receiving community care, 93% are state-funded, and 98% of those in a care home for younger adults are state-funded (Office for National Statistics, 2023a and 2023b). A significant fraction of these individuals will have entered adulthood with a disability, which may have limited their ability to work, earn and accumulate assets. It is older adults – who have had time to build up greater levels of wealth – for whom the stringency of the financial means test is more important.

A mix of public and private providers

Even where adult social care services are publicly funded, this does not mean that they are publicly provided. Councils purchase large volumes of care services from independent providers. An individual may receive care in a private care home but have that care package paid for by the local council.

Around 95% of care home beds are provided by the independent sector (a category that includes private and voluntary sector organisations). The care home sector is fragmented, with around 5,500 different providers in the UK operating 11,300 care homes for the elderly in 2017. The largest 30 care home providers supply 30% of overall capacity. While many providers operate multiple care homes, 80% have just one home, and these single-home providers together supply 29% of all beds (Competition and Markets Authority, 2017). Some of the largest providers are owned by private equity firms, with these firms accounting for around 13% of for-profit care home beds in the UK in 2022 (BBC News, 2021; PHA Group, 2023).

Almost four-in-five care workers in England (79%) are employed by independent providers (Skills for Care, 2023b). A further 5% are directly employed by care recipients and just 16% – around one-in-six – are employed by the public sector (either by local authorities or by the NHS). This means that the government does not (currently) exercise direct control over the pay and conditions of most care workers. It does have an indirect impact, however, through regulation (such as changes to the minimum wage, which is particularly relevant for this sector) and through the fees paid to private providers (discussed in more detail in Section 5.4).

Recent trends in public spending and provision

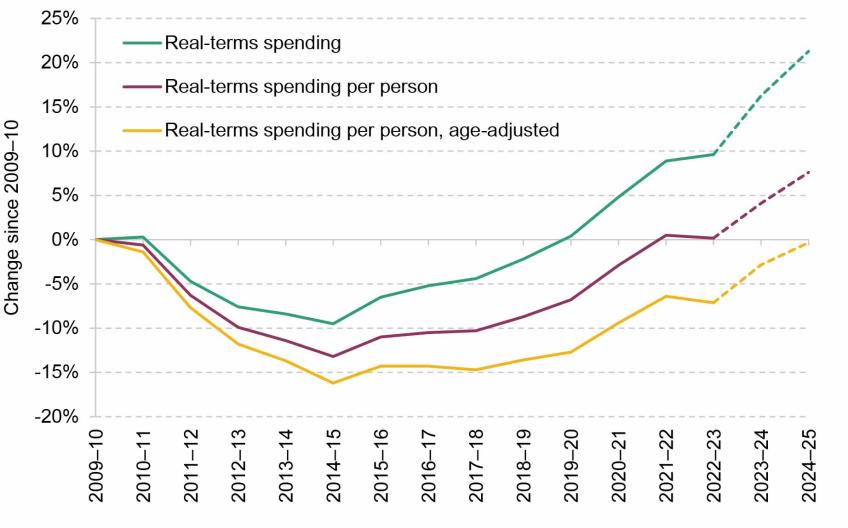

Spending by English local authorities on adult social care services, net of income from fees (e.g. fees from those who are only eligible for partial support and thus pay ‘tariff income’), stood at £22.9 billion in 2022–23 (NHS England, 2023b). Figure 5.1 shows that spending was cut by around 10% between 2009–10 and 2014–15 before recovering steadily, and by 2022–23 spending was around 10% above its 2009–10 level in real terms (i.e. after adjusting for inflation – social-care-specific costs are discussed in Section 5.4)5.

Figure 5.1. Percentage change in net current expenditure on adult social care services (age 18+) in England since 2009–10

Source: Authors’ calculations using: appendix C of Adult Social Care Activity and Finance Report, England, 2022-23 (https://digital.nhs.uk/data-and-information/publications/statistical/adult-social-care-activity-and-finance-report/2022-23/appendix-c); ONS population estimates for England, accessed via Nomis (https://www.nomisweb.co.uk/); ONS population projections (https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationprojections/datasets/z3zippedpopulationprojectionsdatafilesengland); OBR, Fiscal Risks and Sustainability – July 2022 (https://obr.uk/frs/fiscal-risks-and-sustainability-july-2022/); local authority reported out-turns and budgets for 2023–24 and 2024–25 (https://www.gov.uk/government/collections/local-authority-revenue-expenditure-and-financing); Better Care Fund funding for 2022–23 (https://www.gov.uk/government/publications/better-care-fund-policy-framework-2022-to-2023/2022-to-2023-better-care-fund-policy-framework), 2023–24 and 2024–25 (https://www.gov.uk/government/publications/better-care-fund-policy-framework-2023-to-2025/2023-to-2025-better-care-fund-policy-framework); and HM Treasury GDP deflators. Dashed lines show projections.

Spending has then increased further since, as funding for adult social care has been prioritised to a greater extent (e.g. through ringfenced grants and concerted efforts to increase bed capacity to aid discharge from hospitals). Based on local authority spending out-turns and budgets, we estimate that net spending was around 16% higher in 2023–24 than in 2009–10 and 21% higher by 2024–25 (as indicated by the green dashed line)6.

After adjusting for population growth, the reduction in expenditure between 2009–10 and 2014–15 was even more significant, at 13%. Only recently has adult social care spending per person returned to its 2009–10 level. Looking ahead, spending per person is projected to be 4% higher than the 2009–10 level by 2023–24 and 8% higher by 2024–25.

Demand for adult social care services also grew over this period. One, but by no means the only, source of demand growth was demographic change, as the population aged. To account for this, we construct a measure of age-adjusted spending per person, which accounts for changes in the age composition of the population as well as its size. To do this, we attach a weight to each population group based on how much adult social care they use on average (using estimates of social care spending by age published by the OBR, also shown later in Figure 5.3; Office for Budget Responsibility, 2024). This measure suggests that adult social care spending by local authorities has not kept up with demand since 2010. Age-adjusted spending per person declined by 16% between 2009–10 and 2014–15 and, despite subsequent increases, remained 7% below its 2009–10 level in 2022–23 (Figure 5.1). Our estimates suggest that age-adjusted spending per person will return to its real-terms 2009–10 level in 2024–25.

This measure accounts only for changes in demand resulting from population growth and changes in the age composition. It does not account for changes in demand for social care conditional on age. Adjusting for changes in the age structure thus would not capture changes in the prevalence of disabilities, or for changes in physical mobility at a given age, for instance. Accounting for population ageing therefore does not account for all possible changes in the demand for care. Further, this is a measure of all adult social care spending, which includes spending on both working-age and older (65+) adults. A consistent measure of spending by age group is not available for the full period, but the available evidence suggests that spending on the pension-age population was cut to a greater extent over the period and that spending on working-age adults was relatively protected (Harris and Phillips, 2018). This would suggest that age-adjusted spending on older adults has seen a bigger decline. We discuss these issues further in Section 5.4.

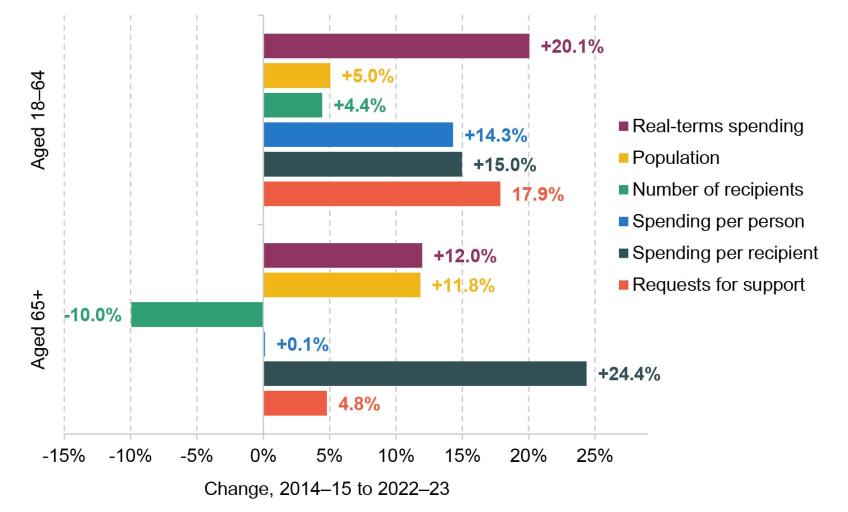

Overall, a little over half (51.7%) of adult social care spending goes towards those aged 65 and above, and a little less than half (48.3%) goes towards those aged between 18 and 64 (this is discussed in more detail in Section 5.4). Figure 5.2 documents how real-terms spending, the population, the number of individuals receiving care, real-terms spending per person and per recipient, and requests for support have changed for the working-age (18–64) and older (65+) populations since 2014–15, when comparable data begin. There are several things to take away.

Figure 5.2. Percentage change in long-term care spending, long-term care recipients and spending per long-term care recipient by age group, England, 2014–15 to 2022–23

Note: Figures are for long-term care, defined as care provided to recipients on an ongoing, non-time-limited basis. Short-term care is excluded.

Source: Authors’ calculations using NHS Digital, Adult Social Care Activity and Finance Report, England, 2022-23, https://digital.nhs.uk/data-and-information/publications/statistical/adult-social-care-activity-and-finance-report/2022-23.

First, since 2014–15, long-term spending on both age groups grew in real terms, but spending on working-age adults grew faster than that on the 65+ age group (20% versus 12% over the period between 2014–15 and 2022–23).

Second, whereas the number of individuals receiving long-term care aged 18–64 grew roughly in line with the population in that age group (around 5%), the number of long-term care recipients aged 65 and above fell by 10% even while the 65+ population grew by 12% (with faster growth at older ages, as shown later in Figure 5.5). The reduction in the number of long-term care recipients among the elderly reflects the tightening of eligibility criteria (in terms of both the means test and the needs test) discussed above. This reduction has come primarily from the numbers accessing community-based support, rather than those accessing nursing and residential care homes.

Third, the result has been increases in spending per person and per recipient for the working-age group of similar magnitudes (roughly 15%). Yet, among the older population, spending per person has stayed almost constant while spending per care recipient has grown by almost a quarter (24%).

Lastly, the number of requests for support for the 18–64 age group grew by 18% between 2014–15 and 2022–23, versus only 5% for adults aged 65 and above, reflecting growing demand among the under-65 population (discussed in more detail in Section 5.4).

5.3 Charging reform (or not)

The insurance problem

Social care can be expensive. The DHSC estimates that one-in-seven individuals over 65 will face lifetime care costs of more than £100,000 (Department of Health and Social Care, 2022a). But it is difficult to predict exactly who will end up with a substantial care need in old age. Given its uncertainty and costly nature, many people would like to be insured against this risk. The state could pool individual risks and provide protection – bring the ‘magic of averages to the rescue of the millions’, in Winston Churchill’s words – but in this case does not. This lack of ‘social insurance’ stands in contrast to the provision of healthcare, which is free at the point of use for all residents in England. All but the most asset-poor (those with assets below £14,250) are required to contribute towards the cost of their social care, and those with assets of more than £23,250 are ineligible for any council support, as described in Section 5.2. Even individuals who qualify for public support must contribute from their income (subject to a minimum income floor). Moreover, council-funded care packages might not fully meet individuals’ needs, requiring them to top up out of their own income or savings. There is no limit to the social care costs an individual can face in a year or over their lifetime.

The private market for social care insurance is extremely limited, for reasons explored in Box 5.2. There are few financial products available for a healthy working-age adult, or for someone upon retirement, who wishes to insure against the risks of high care costs in old age. The only products available are immediate needs annuities, purchased upon the onset of a care need. So, individuals face a difficult-to-predict financial risk in old age, which threatens to consume a large fraction of their wealth, which the state does not provide insurance against, and which they are unable to insure themselves in the private market.

Box 5.2 Why is the private market for social care insurance so limited?

The private market for social care insurance (known internationally as long-term care insurance, or LTCI) is limited in the UK and elsewhere. Writing in 2011, the Dilnot Commission concluded that ‘there is currently too much uncertainty involved for the private sector to take on the full risk … No country in the world relies solely on private insurance for funding the whole cost of social care’ (Dilnot, 2011). There are numerous reasons for this market failure, on both the supply side and the demand side. These include:

Correlated risks. Would-be LTCI providers face uncertainty about how long individuals will live, their future care needs and the costs of meeting those care needs. The key risk from the insurer’s perspective is that care costs turn out higher than expected. The challenge is that this risk is common to each generation (i.e. likely to manifest as many simultaneous claims) and is likely to be serially correlated across generations (Cutler, 1996). For example, a medical advance that increases life expectancy for care recipients might increase average lifetime costs for everyone within a generation and, because medical advances do not get reversed, will increase average lifetime care costs for all future generations of care recipients also. This adds uncertainty, and makes it difficult to insure against, because the insurer cannot diversify either within or across generations of care recipients. Insurers are unwilling to offer full insurance as a result.

Adverse selection. Providers worry that demand for LTCI will be highest among those with the greatest risk of developing a social care need. Recognising that this will increase expected payouts, insurers respond by raising premiums. At these higher premiums, only the highest-risk individuals are willing to purchase LTCI, and only a small fraction of people end up covered. There is empirical evidence to back up insurer concerns about such ‘adverse selection’: Oster et al. (2010) find that individuals with the genetic mutation for Huntington’s disease, a degenerative disorder, are up to five times more likely to own LTCI.

Low uptake. There are many reasons why we might expect individuals to demand less LTCI than would be socially optimal, even if it was offered by the market at a ‘fair’ price. People struggle to understand and plan for low-probability adverse events, and this is exacerbated in the English setting by the complexity and opacity of the system: many wrongly expect it to function like the NHS (Dilnot, 2011). Further, individuals in their 60s – the age at which LTCI is typically purchased – systematically underestimate their chances of living to old age (O’Dea and Sturrock, 2023), which could reduce their willingness to pay for LTCI as they underestimate their future needs. Individuals may also decide to substitute away from private care and LTCI and to rely more on informal care from family members – possibly to a degree beyond what is appropriate, if it negatively impacts the carer’s well-being or leads to them substantially reducing their hours of paid work.

The Dilnot Commission

The Commission on Funding of Care and Support was established in July 2010 by the newly formed coalition government and was chaired by former IFS Director Andrew Dilnot. In its 2011 report, the Commission concluded that ‘our system of funding of care and support is not fit for purpose, and has desperately needed reform for many years’ (Dilnot, 2011). The report identified the insurance problem described above as the fundamental issue – the fact that individuals face the risk of catastrophic care costs and there is no form of risk pooling to protect them against those costs.

The Dilnot Commission recommended that the government pool risks by introducing a cap on lifetime costs of between £25,000 and £50,000, with a central recommendation of £35,000. It also recommended an increase in the generosity of the means test via an increase in the upper capital limit, above which people must pay the full cost of their care, from £23,250 to £100,000, to provide more protection for many outside the existing means test. It made various other recommendations, such as for a standardised national framework for assessing eligibility for state support and exempting those who enter adulthood with a care need from any form of means test.

The government legislated for Dilnot-style reforms in the Care Act 2014, with a proposed cap of £72,000 and an upper capital limit of £118,000 (and some other differences from the Commission’s proposals). Implementation was delayed in July 2015 and then postponed indefinitely – joining the long list of failed attempts at social care reform (King’s Fund, 2023).

The recently scrapped proposals

In 2019, the Conservatives had a pledge to legislate for long-term reform of social care in their election manifesto. This led to a package of reforms announced by then Prime Minister Boris Johnson in September 2021. These would have increased the generosity of the state’s social care offer – though to a lesser extent than recommended by the Dilnot Commission – in two important ways.

First, an individual’s lifetime care costs would be capped at £86,000, with all spending on personal care after that point to be met by the state regardless of income or wealth7. This was to apply to all individuals regardless of age (with no carve-out for those entering adulthood with a care need, as proposed by Dilnot). The government explicitly argued that this limit would also help to develop the private insurance market by providing ‘greater incentives for the financial services industry to provide relevant products that people see the benefit of purchasing’ (Department of Health and Social Care, 2022a).

Second, the means test would be made considerably less stringent. The lower capital limit – the level of assets below which individuals would not have to contribute to their care costs from their savings – was to be increased from £14,250 to £20,000, and the upper capital limit, above which people must pay the full cost of their care, was to be raised from £23,250 to £100,000. More people would qualify for at least some state support, more people would have all of their costs met by the state, and there would be greater protection against the risk of catastrophic care costs. The government expected around two-thirds of older adults to receive some state support towards their care costs following the reforms, up from around half under the existing system (Prime Minister’s Office, 2022).

The initial impact assessment (Department of Health and Social Care, 2022a) suggested that the costs of the combined package might reach £6.2 billion per year by 2031–32 (£4.7 billion in 2021–22 prices). In October 2021, the Office for Budget Responsibility estimated that the funding reforms would cost around 0.25% of GDP in the medium-to-long term, equivalent to around £7 billion in today’s terms.

These changes were announced alongside the introduction of a new tax, a 1.25% Health and Social Care Levy based on National Insurance contributions (NICs), intended to ‘pay for’ the reforms. First introduced as an increase in the rates of NICs (to be later replaced by the new levy), this came into effect in April 2022. It was then scrapped by then Chancellor Kwasi Kwarteng in the September 2022 ‘mini Budget’. This was one of the few tax cuts not to be swiftly reversed by Jeremy Hunt, Mr Kwarteng’s successor (who in fact went on to cut the rates of employee and self-employed NICs further).

These charging reforms were originally planned to come into operation in October 2023. At the November 2022 Autumn Statement, Mr Hunt announced that the roll-out would be delayed until October 2025, which meant not implementing them until the next parliament (a move welcomed by local government at the time, amidst concerns that funding and capacity were not in place to deliver the reforms successfully (Local Government Association, 2022)).

Then, in her statement on 29 July 2024, Ms Reeves declared that ‘it will not be possible to take forward these charging reforms’, with the accompanying document stating that ‘the reforms are now impossible to deliver in full to previously announced timeframes’ (HM Treasury, 2024). The authors’ understanding is that this amounts to a cancellation, not a(nother) delay, of the reforms. It remains unclear whether other aspects of the reforms, such as the right for self-funders to ask their local authority to commission care for them at the local authority rate, will also be scrapped. The decision not to go ahead with the reforms was scored as saving £1.1 billion in 2025–26 (HM Treasury, 2024), a considerably smaller sum than the eventual long-term savings, which are estimated to amount to £4–£5 billion a year by the end of the parliament (Boileau et al., 2024).

Overall, this leaves the social care system in England roughly where it started: the charging reforms have seemingly been abandoned, and the tax rise introduced to pay for them has been more-than-reversed. The insurance problem remains unsolved.

5.4 Further challenges under the status quo

The adult social care system faces a series of serious challenges in addition to the insurance problem and the charging reforms discussed above. Here, we group these challenges into five broad and interrelated categories: (i) funding and demographic pressures; (ii) interactions with local government finances; (iii) ‘Fair Cost of Care’ reforms and payments to providers; (iv) the adult social care workforce, including immigration and pay; and (v) support for informal carers.

Funding and needs: more money just to stand still

By scrapping the proposals for a lifetime cap on care costs, the new government has decided not to expand the generosity of the state’s offer on adult social care. Relative to a world in which those charging reforms went ahead, the government will save billions. But in the face of growing demand, spending on social care will need to rise just to maintain the system as it is currently configured.

An ageing population

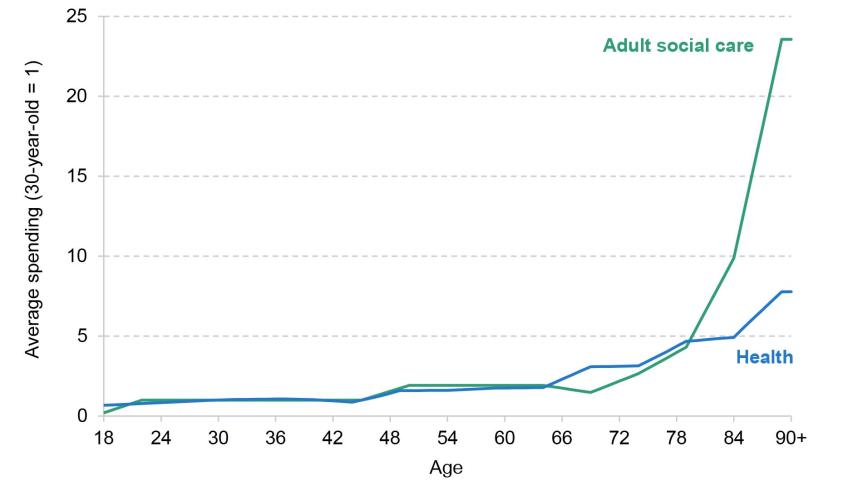

A key source of growing demand for adult social care services is population ageing. Older people are much more likely to have a care need and to use adult social care services. As a result, average public social care spending per person increases significantly with age, particularly after age 70.

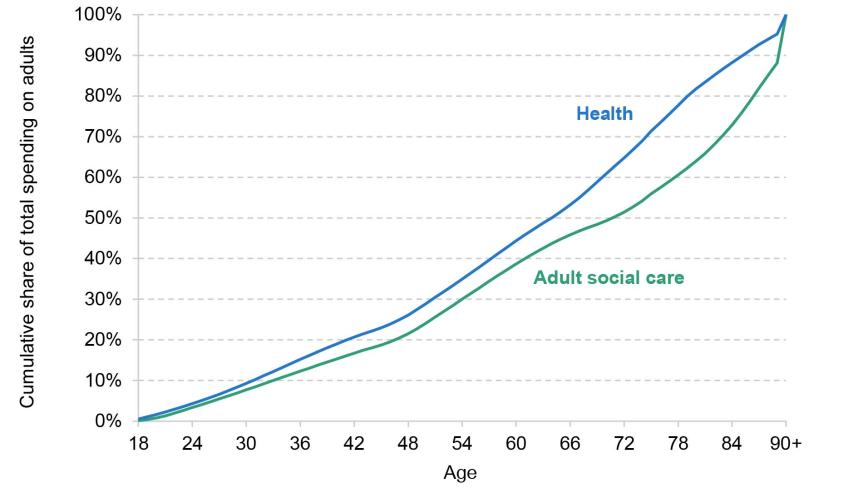

This is illustrated in Figure 5.3, which plots OBR estimates of adult social care spending by age, relative to a representative 30-year-old (Office for Budget Responsibility, 2022). Public spending on adult social care for the average 60-year-old is around twice as high as for the average 30-year-old (an estimated £605 in 2026–27 for an average 60-year-old versus £315 for the average 30-year-old). For the average 75-year-old, it was around three times as high (£941). By age 85, it is more than 12 times as high (around £4,000), and by 90 it is 24 times as high (around £7,400). This is a much sharper increase at older ages than is estimated for healthcare, where spending on a representative 90-year-old is estimated to be around eight times higher than on a 30-year-old.

Figure 5.3. Representative age profile for UK public spending on health and adult social care, relative to a 30-year-old

Source: Authors’ calculations using chart 4.11 of OBR, Fiscal Risks and Sustainability – July 2022, https://obr.uk/frs/fiscal-risks-and-sustainability-july-2022/.

The relative concentration of adult social care spending at older ages can also be seen in Figure 5.4. The OBR estimates imply that around half (52%) of all adult social care spending goes to individuals aged 70 and above, and around a quarter (27%) to those aged 85 and above. The equivalent figures for health spending – which is less concentrated at the very oldest ages – are 41% and 12% respectively. Note, though, that working-age individuals (who are more numerous) still account for close to half of all adult social care spending; this group is discussed below.

Figure 5.4 Implied cumulative distribution of UK public spending on health and adult social care, by age

Source: Authors’ calculations using chart 4.11 of OBR, Fiscal Risks and Sustainability – July 2022 (https://obr.uk/frs/fiscal-risks-and-sustainability-july-2022/) and ONS population estimates for the UK by single year of age in 2022 (accessed via https://www.nomisweb.co.uk/).

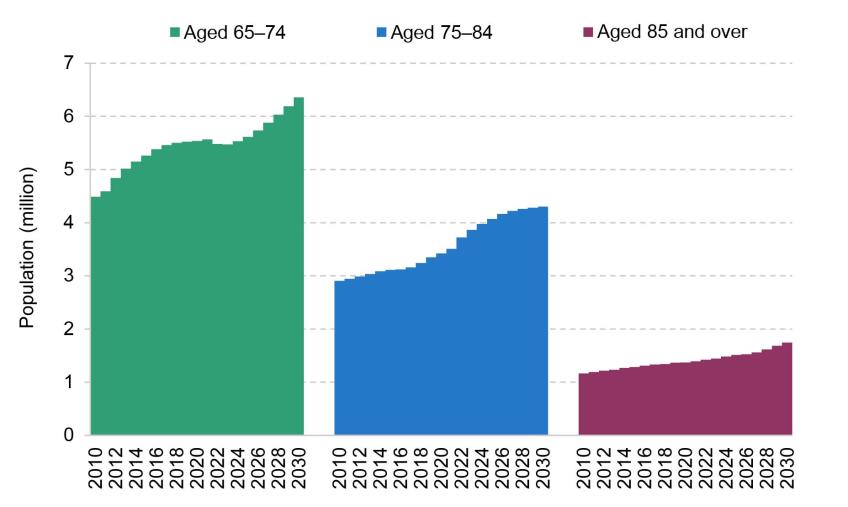

The population at older ages in England has grown substantially since 2010 and is projected to continue to grow between now and 2030. Between 2010 and 2024, the English population aged between 65 and 74 grew by 23.2%, the population aged between 75 and 84 grew by 36.8%, and the population aged 85 and over grew by 27.3% (Figure 5.5). The equivalent figure for the overall population is 10.7%. Between 2024 and 2030, these older groups are again projected to grow more quickly than the population at large, with the greatest proportional increase (17.7%) in the population aged 85 and over – the group that makes heaviest use of adult social care services.

Figure 5.5. Population aged 65–74, 75–84 and 85+ in England

Note: Data for 2010 to 2023 are population estimates. Data for 2024 onwards are (2021-based) population projections.

Source: ONS population estimates – local authority based by five year age band (accessed via https://www.nomisweb.co.uk/); ONS principal projection – England population in age groups (https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationprojections/datasets/tablea24principalprojectionenglandpopulationinagegroups).

As the population continues to age, demand for care will increase. To the extent that the older population grows wealthier, this may not translate into additional demand for publicly funded care, as many will not qualify for state support, especially if the thresholds used in the financial means test continue to be frozen. Pressure on the broader sector will nonetheless continue to grow, and official projections (discussed below) suggest that meeting demographic pressures will necessitate higher public spending on social care in future.

Growing demand at younger ages

Adult social care is often perceived as a service primarily for the elderly, but it plays a crucial role in addressing the needs of working-age adults as well. In 2022–23, a little less than half of total adult social care spending by local authorities in England (48.3%) went towards those aged 18–64. A similar share (49.6%) of spending specifically on long-term care packages goes towards 18- to 64-year-olds. These figures are broadly consistent with the estimates presented in Figure 5.4 for the UK as a whole.

Working-age adults in receipt of adult social care tend to have more severe needs and require more intensive care packages. There are more individuals aged 65 and above receiving long-term care than working-age adults receiving it (370,000 versus 259,000 at the end of 2022–23), but long-term care spending per recipient is considerably higher among younger adults (£35,330 at the end of 2022–23) than among adults aged 65 and above (£25,070). Combined, this explains the overall 50:50 split in spending between the two age groups.

Figure 5.2 earlier shows that spending on working-age adults has increased more quickly than spending on older adults since 2014. Changes in how social care spending is broken down mean we cannot say precisely how spending on different groups has evolved over a longer period (e.g. since 2010), but the available evidence suggests that working-age spending was relatively protected and that spending on older adults faced larger cuts over the early 2010s (Harris, Hodge and Phillips, 2019; Crawford, Stoye and Zaranko, 2021).

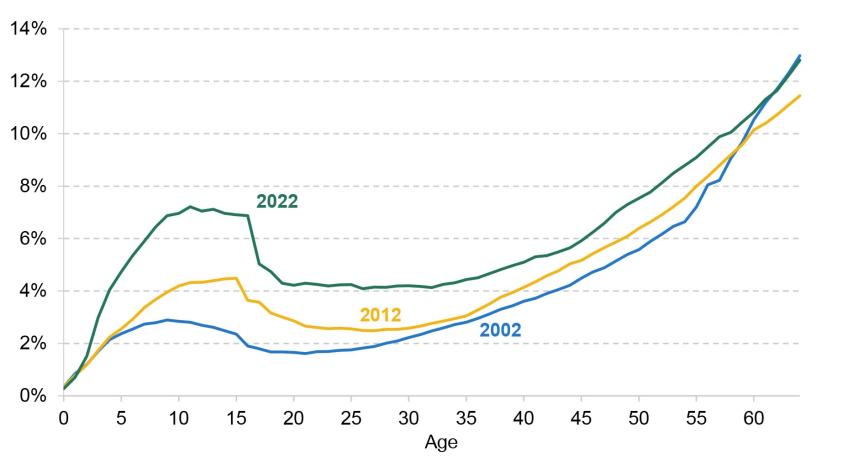

The substantial increase in spending for working-age adults in recent years reflects the growing demand for support. Figure 5.2 also shows that the number of new requests to local authorities for social care support from adults aged 18–64 grew faster than the number from adults aged 65+. This is consistent with other evidence of sharp increases in disability among younger adults. Banks, Karjalainen and Waters (2023) highlight a sharp rise in disability benefit claims among working-age adults between 2002 and 2022, reproduced in Figure 5.6. The proportion of younger adults claiming health-related benefits has continued to grow since (Ray-Chaudhuri and Waters, 2024; Latimer, Pflanz and Waters, 2024), and we would expect this also to be true of claims for severe conditions that are more likely to result in a care need. There is no simple relationship between rates of working-age disability and demand for adult social care, but we certainly would not expect higher rates of disability to be associated with less demand for care services.

Figure 5.6. Share of individuals claiming disability benefits by age (ages 0–64), Great Britain

Note: Values denote the share of individuals, by single year of age, who receive disability living allowance, personal independence payment or attendance allowance. The sharp decline in claim rates around age 16 reflects the fact that the assessment process changes at that age, and child claimants are sometimes ineligible under the adult assessment criteria.

Source: Banks, Karjalainen and Waters, 2023.

We might expect rapid growth in the number of adults diagnosed with learning disabilities to translate into greater demand for long-term care support. In 2022–23, 46% of those aged 18–64 receiving local-authority-funded long-term care did so primarily due to a learning disability, and this accounted for most of the spending on this age group (68%) (NHS England, 2023a). Between 2014–15 and 2022–23, spending on long-term care support rose by 47%, with even greater increases for other types of long-term support, such as memory and cognition support (151%) and mental health support (80%). Meanwhile, the number of monthly claims for personal independence payment (PIP) due to learning disabilities grew by 412% between 2019–20 and 2023–24 (Latimer, Pflanz and Waters, 2024). Recent trends suggest that we might expect demand for social care among working-age adults to grow, and the associated pressures will be in addition to those stemming from the ageing of the population.

Long-term projections

As the population grows and ages, we should expect demand for adult social care services to grow. Meeting that demand, with the system configured as it is, will require additional resources. One estimate, from the Health Foundation, suggests that to meet future demand, adult social care funding in England would need to grow by 3.4% per year in real terms up to 2032–33 (Boccarini et al., 2023). This compares with average real growth of 0.7% per year between 2009–10 and 2022–23, and 2.4% per year between 2014–15 and 2022–23. It is slightly higher than the average real-terms growth rate implied by official OBR projections over the next decade (3.1% per year)8.

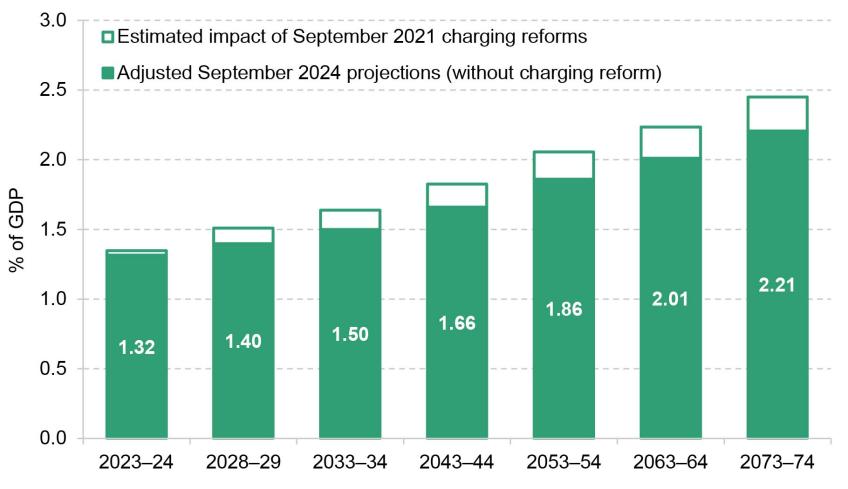

Figure 5.7 shows the OBR’s projections of UK public spending on adult social care as a share of national income, reflecting demand pressures (including from ageing) and growth in costs. After adjusting for the estimated savings from scrapping the charging reforms discussed in Section 5.3, spending is projected to rise from around 1.3% of national income in 2023–24 to around 2.2% of national income in 2073–74.

Figure 5.7. OBR projections of adult social care spending in the UK

Note: Charging reforms refer to the lifetime cap and more generous financial means test announced in September 2021 and discussed in Section 5.3. Estimates for the long-term cost of charging reform come from the July 2022 FRS report, which are combined with long-run projections from the September 2024 FRS report. Figures are for the UK.

Source: Authors’ calculations using OBR fiscal risks and sustainability reports, July 2022 and September 2024.

Importantly, these are projections rather than predictions: they are estimates of how much spending might be needed to meet the growth in demand and maintain the system as it is. It is possible that future governments will decide not to keep pace with demand; they could decide to reduce or increase the generosity of the system. The point is, more money will be required just for adult social care to stand still.

Interactions with local government finance reform

The previous subsection considered the pressures on adult social care funding at a national level. A further set of complications and policy challenges come when we consider how that funding is allocated at a sub-national level, and how this interacts with the local government finance system. Even if funding grows in line with demand at the national level, this does not mean that the same will necessarily be true at every local level.

Different areas have different levels of demand for care services and different local cost pressures. They also have differing abilities to raise revenues themselves through local taxes, such as council tax. To ensure that the same range and quality of services can be provided in different places, the government has historically used measures of assessed spending need and revenue-raising capacity to allocate funding across different parts of the country. There are two problems here. The first is that the main estimates of councils’ spending needs are out of date (they have not been updated since 2013 and are based in part on data that are even older). The second problem is that the allocation of most funding has not accounted for even these out-of-date estimates of need properly for many years, or for the revenues councils can raise for themselves9. In practice, this means councils in poorer areas tend to get less than they are assessed to ‘need’, while the opposite is true for councils in richer areas (Ogden et al., 2022; Ogden and Phillips, 2023).

Failing to account adequately for changing patterns of local need risks a world where the level of funding provided to each area is disconnected from the local demand for services, including publicly funded adult social care services. For example, while the population of England is projected to age over the coming years (as discussed above), the rate of ageing is by no means uniform across the country. Some councils are forecasted to experience much higher growth in their elderly population than others. For example, over the next six years, some local authorities (the Isle of Wight, Dorset, Northumberland) are projected to see the share of the local population aged 65 and over increase by more than 2 percentage points; in others (Bristol, Coventry), it is projected to increase by less than 0.5 percentage points. Some areas are ageing much faster than others and will see much faster growth in demand for care services as a result.

Among the working-age population, recent growth in rates of health-related benefit claims has been broadly proportional to the number of claimants in each area in 2019–20 (i.e. growth across areas has been similar in percentage terms), but the rates of absolute growth have been much faster in areas that already have higher claim rates (Latimer, Pflanz and Waters, 2024). For instance, the claim rate in Blackpool has increased from 14.9% in 2019–20 to 19.1% in 2023–24, a 28% increase (4.2 percentage points); in Wokingham, the claim rate has increased from 3.1% to 4.3%, a 36% increase (1.1 percentage points). We would not expect these patterns to map neatly onto growth in demand for adult social care services, but we might expect similar amounts of geographic variation.

The challenge is that the areas seeing the greatest increase in social care pressures may not be the ones that see the biggest increases in funding.

Local authorities are increasingly reliant on local council tax revenues: the share of local authority funding received from council tax increased from just over a third (36%) in 2010–11 to more than half (56%) in 2019–20 (Ogden and Phillips, 2024a). This hides substantial variation across the country, however, with local authorities in more deprived areas typically less able to raise revenues from council tax and more reliant on grants from central government.

The spending plans inherited by the new government imply real-terms cuts to ‘unprotected’ budgets, including grants to local government (see Chapter 3). That could pose significant financial challenges for the areas more reliant on those grants. For instance, under a scenario in which councils with responsibility for social care were allowed to increase council tax bills by 5%, and grants were cut evenly across the board (by 7% in real terms each year), councils in the most deprived tenth of areas could see their funding rise by only 0.6% in real terms per year, compared with 2.6% in the least deprived tenth (Ogden and Phillips, 2024b). Addressing these imbalances across councils would require significant redistribution of grant funding, potentially leading to very large cuts in the grants to less deprived areas, which it may be politically difficult for the government to impose.

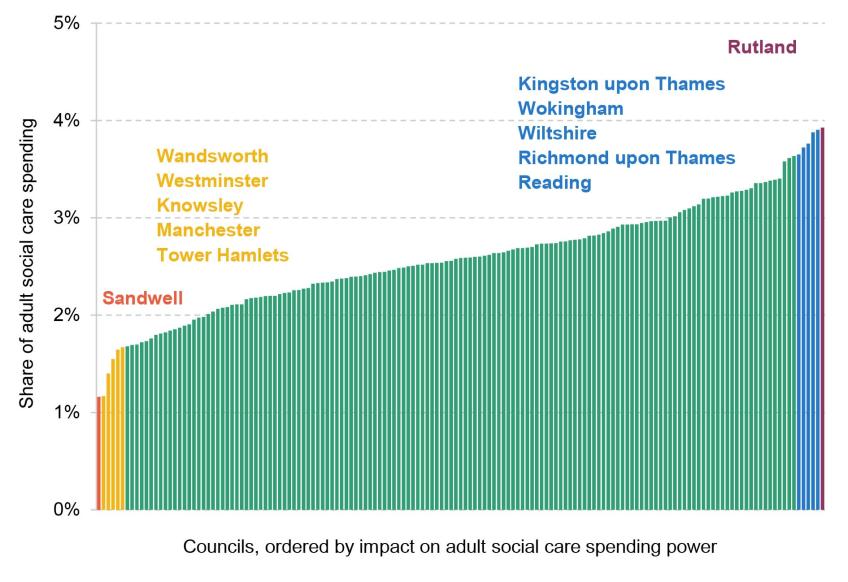

Another way to illustrate this challenge is to consider how much extra adult social care each local authority could purchase for a given percentage increase in its council tax bills. Figure 5.8 shows the percentage increase in adult social care spending that could be afforded from a 2% increase in council tax bills. In some areas – Rutland, Kingston upon Thames, Wokingham – a 2% increase in council tax would allow for nearly a 4% increase in adult social care spending. In 15% of areas, it would pay for less than a 2% increase in adult social care spending (i.e. the adult social care budgets of these councils are already bigger than the total amount that they receive from council tax, so a 2% increase in council tax revenues translates to a less-than-2% increase in adult social care spending). There is no good reason to suppose that the best-placed areas to raise additional funding from local taxes are also those facing the largest growth in demand for adult social care services.

Figure 5.8. Estimated additional spending from 2% council tax rise, as a share of adult social care spending in 2023–24

Note: Estimated revenues from an additional 2% increase in council tax band D rates in 2023–24 as a share of net expenditure on adult social care in 2023–24, for upper-tier local authorities. Net expenditure from spending out-turns, and from budgets for authorities for which out-turns are not available.

Source: Authors’ calculations using council tax levels in 2023–24 and local authority revenue expenditure and financing data for 2023–24.

Relying on local taxation to deliver additional funding for services has the potential to undermine efforts to ensure that all councils are equally able to meet local demand and deliver high-quality public services. It could, in other words, lead to wide disparities in service provision – at least if it is not accompanied by a well-designed local government finance system, which is very much the case at the moment. More generally, there is an inherent tension between a desire for greater devolution of taxes and powers to local areas and a desire for consistency in service provision across the country (Phillips, Simpson and Smith, 2018).

The government faces a fundamental decision on whether adult social care is a local or a national responsibility. The Scottish Government is moving towards a ‘National Care Service’ with the aim of providing more consistent services across Scotland (Phillips, 2022). In England, the Labour Party’s general election manifesto proposed ‘a programme of reform to create a National Care Service, underpinned by national standards, delivering consistency of care across the country’ (Labour Party, 2024).

Any assessment of this (vague) promise will depend on one’s view of the appropriate role of local versus central government, and the merits of devolving versus centralising powers. If the goal is to ensure consistent service provision across England, centralising social care funding, with ring-fenced grants allocated based on an up-to-date spending needs formula, could be attractive. Yet this would inevitably also bring major challenges, especially in the transition.

For one, assessing the relative spending needs of different areas is extremely difficult, and there is no guarantee that such a system would in fact lead to consistent service provision (Harris and Phillips, 2018). Maintaining some degree of local discretion might, perhaps counter-intuitively, help to offset the inevitable flaws in centralised needs assessments, with councils able to reprioritise spending across services to better match local needs.

Second, moving to such a system would mean transferring some of the funding currently provided to councils to the new National Care Service. Determining how much to subtract from each council’s budget is far from simple. Some areas use their local discretion to spend less than national funding formulas suggest they ‘need’. The question then arises: should these councils lose the amount they actually spend? Or the amount central government estimates that they would need to spend to deliver an average quality of service? Or something else? The choices made in this process would have major distributional implications. For a discussion of these and other issues, see Phillips, Simpson and Smith (2018) and Phillips (2022).

Labour’s manifesto also promised that ‘services will be locally delivered’ under its National Care Service, which is either a trivial observation about the nature of in-person services or a commitment to maintaining a role for local authorities. If adult social care is left within councils’ remit, one improvement would be to commit to updating spending needs assessments frequently and regularly and redistributing funding accordingly. In a tight funding environment, even that could be more difficult than it sounds. Whatever form the ‘National Care Service’ takes, interactions with the local government finance system are sure to add complications.

Fees paid to private providers and the ‘Fair Cost of Care’

One consequence of the cuts to local government funding over the 2010s was a reduction in the real value of fees they paid to care providers, as local authorities sought to make large savings from their budgets. One estimate suggested that local authorities reduced their fee rates by an average of 6% in real terms between 2010–11 and 2016–17, though this followed substantial increases over the 2000s (House of Commons, 2018).

To compensate for reduced fees from local authorities for publicly funded care recipients, care homes became increasingly reliant on self-funders, who paid significantly higher fees to cross-subsidise. A 2017 study by the Competition and Markets Authority found that self-funders in ‘larger providers’ were charged 41% more, on average, than those with their places funded by local authorities and that this was threatening the financial sustainability of the sector – particularly in places with fewer self-funders and thus greater reliance on public funding.

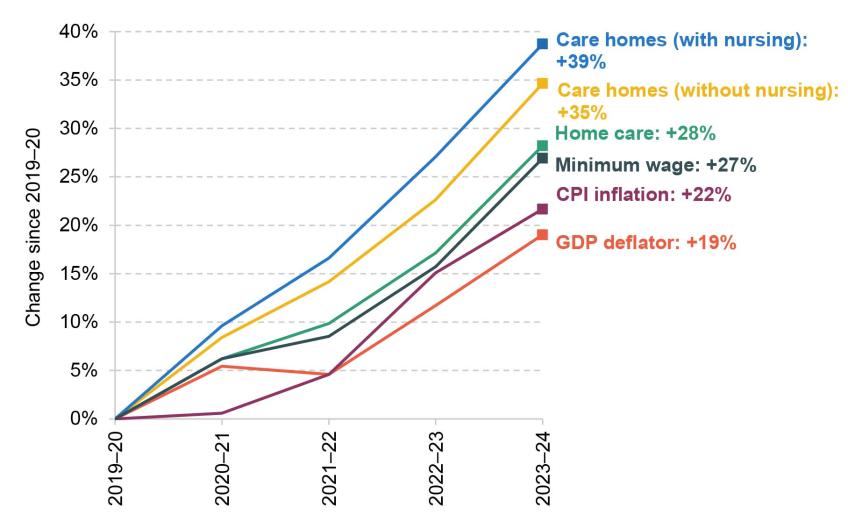

The downwards trend in local authority fees has gone into reverse in recent years. Between 2019–20 and 2023–24, the average fee paid by local authorities for an hour of home care increased by 28% (Figure 5.9). The average fee for a care home place for an adult aged over 65 without nursing increased by 35%, and by 39% for a care home place with nursing. This compares with an increase in the National Living Wage of 27% during the same period (itself a major cost driver) and household inflation of 22% as measured by the CPI.

Figure 5.9. Change in average fees paid by local authorities to external care providers, 2019–20 to 2023–24

Note: Care home figures refer to average fees paid for recipients aged 65 and over. ‘Minimum wage’ refers to the National Living Wage for those aged 25 and over in 2019–20 and 2020–21, and for those aged 23 and over from 2021–22.

Source: Authors’ calculations based on Department of Health and Social Care, ‘Market Sustainability and Improvement Fund 2023 to 2024: care provider fees’ (https://www.gov.uk/government/publications/market-sustainability-and-improvement-fund-2023-to-2024-care-provider-fees) and ‘Improved Better Care Fund: provider fee reporting’, 2021 to 2022 (https://www.gov.uk/government/publications/improved-better-care-fund-provider-fee-reporting-2021-to-2022) and 2020 to 2021 (https://www.gov.uk/government/publications/improved-better-care-fund-provider-fee-reporting-2020-to-2021); Office for Budget Responsibility, economic and fiscal outlook – March 2024 (https://obr.uk/efo/economic-and-fiscal-outlook-march-2024/); HM Government, National Minimum Wage and National Living Wage rates (https://www.gov.uk/national-minimum-wage-rates).

The increases in local authority fees have, in part, been the result of policy action. The Department of Health and Social Care (2021), acknowledging that ‘a significant number of local authorities are paying residential and domiciliary care providers less than it costs to deliver the care received’, announced a ‘Fair Cost of Care Fund’ to provide local authorities with additional funding to increase the fees paid to providers.

Looking ahead, policy changes may act to increase fees further. The 2014 Care Act included a provision, Section 18(3), allowing individuals who self-fund their care to request their council to commission care on their behalf at the local authority rate. This would limit – or in some cases eliminate – the ability of care homes to ‘cross-subsidise’ by charging higher fees to self-funders, who would gain access to the lower, council-negotiated fees. Setting council fees too low and at the same time closing off the ‘cross-subsidisation’ channel could threaten the financial sustainability and viability of care providers, and quality of care could suffer.

This change has not yet been implemented. One policy decision for the new government is whether to continue down this path. It is unclear, at the time of writing, whether Section 18(3) has been scrapped along with the lifetime cap by the new government. Fees are likely to need to increase in any case, but this is particularly the case if Section 18(3) is triggered. Paying higher fees will require additional funding for councils. This is therefore a decision for the upcoming Spending Review – though additional funding for councils could come from local tax rises (e.g. council tax) rather than additional funding from central government.

As mentioned in Section 5.2, the care home sector is relatively concentrated (Competition and Markets Authority, 2017), with a notable degree of private equity involvement. A review of the (mostly US-based) evidence found that private equity ownership in healthcare (including nursing homes) is associated with increases in costs for patients and/or funders (Borsa et al., 2023). To the authors’ knowledge, there is no good evidence on the impact of private equity ownership on care home prices in the UK.It is possible that changes in ownership and market structure have contributed to recently observed increases in fees10. There is evidence from both the UK (Patwardhan, Sutton and Morciano, 2022) and the US (Gupta et al., 2021) that private equity ownership is associated with lower-quality care, which points to a need for careful regulation and monitoring, aside from any debate about fee levels.

Whatever the driving factors behind recent increases in fees, these changes have placed significant pressure on council budgets (Ogden and Phillips, 2024a).

Workforce and pay

The social care workforce: large, growing and low-paid

The adult social care sector is large and growing. Approximately 1.52 million people were employed in the adult social care sector in England in 2022–23, with a total wage bill of around £26.6 billion (Skills for Care, 2023a). A recent workforce strategy produced by the sector estimates that the workforce will need to increase by almost a third by 2040 if it is to grow in line with the number of people aged 65 and over – equivalent to more than 500,000 new posts (Skills for Care, 2024a).

That degree of expansion will require the sector to improve its ability to attract and retain staff. That will depend partly upon how pay and conditions in social care compare with those of other occupations. Adult social care is officially defined as a low-paying industry by the UK government (Low Pay Commission, 2023). The median hourly rate for care workers in March 2023 was £10.11. This was slightly above the National Living Wage (£9.50), similar to the median hourly pay for sales and retail assistants (£10.12) and slightly above the median for cleaners and domestic workers (£9.96) (Skills for Care, 2023a). Pay for care workers has fallen in recent years relative to other sectors (Migration Advisory Committee, 2022 and 2023). Pay differentials within the sector have also fallen: in March 2016, compared with a care worker with less than a year’s experience, a care worker with at least five years’ experience received an average hourly pay premium of 4.4% (33 pence per hour), but by 2023 this had fallen to 0.6% (6 pence) (Skills for Care, 2023a).

The NHS is an important outside option for social care workers. Between 2011–12 and 2021–22, 28% of those who left the care sector went on to nursing auxiliary or nursing roles (Figure 5.10, reproduced from Kelly et al. (2022)). One reason for this is that time working in the social care sector is often used to demonstrate the care experience necessary to apply for many NHS roles. Furthermore, comparable NHS roles tend to pay better: in 2022–23, average care worker pay was £1.33 less per hour than pay for healthcare assistants in the NHS who were new to their roles (NHS Pay Review Body, 2024). NHS workers also benefit from significantly higher employer pension contributions. While social care workers often receive a defined contribution (DC) pension with employer contributions at or near the auto-enrolment minimum of 3% of band earnings (the portion of earnings in respect of which contributions are made), NHS workers receive employer contributions of 23.7% of pensionable earnings as part of the (defined benefit) NHS Pension Scheme.

Figure 5.10. Occupations of lower-paid social care staff in England prior to taking up and after leaving care roles, 2011–12 to 2021–22

Note: The authors are grateful to the Health Foundation for sharing the data behind the graph. ‘Other’ includes all occupations outside of the top 11 shown here.

Source: Kelly et al., 2022.

As pay in the NHS increases – a recent recommendation for a 5.5% pay award for NHS ‘Agenda for Change’ staff was accepted by the new government (see Chapter 4) – one risk is that this exacerbates staffing shortages within social care, unless pay in the social care sector keeps pace.

A ‘Fair Pay Agreement’ for adult social care

The Labour Party’s general election manifesto promised a ‘New Deal for Working People’ with a ‘Fair Pay Agreement’ in adult social care to help empower workers and trade unions in the sector to negotiate better pay and conditions (Labour Party, 2024). The manifesto is clear that this is intended as a first step towards a greater role for sectoral collective bargaining across the broader economy, and that this will be introduced only after wide consultation.

Without knowing more about what form this agreement will take, it is hard to say much about its likely impact, However, it is anticipated that the agreement will lead to increased wages in the sector. Higher pay is expected to bring benefits in the form of lower turnover, lower recruitment costs and improved quality of care. The beneficial impacts on recruitment and retention might be particularly large if a Fair Pay Agreement leads to improved pay and conditions in adult social care but not in other sectors.

Any benefits from higher pay must be traded off against the costs. Social care is a labour-intensive industry, and an increase in pay rates will increase the cost of providing social care services, which will be borne not only by local authorities, but also by self-funders who will face more expensive care costs. In addition, as noted above, the majority of care providers are independent (whether for-profit or voluntary). The ways in which these providers might respond to any sector-wide pay increase are key considerations.

The experience following the introduction of the National Living Wage (NLW) in 2016 – which also represented a big increase in staffing costs – is informative. Giupponi and Machin (2018) found that the introduction of the NLW led to higher wages in care homes without large-scale job losses or care home closures. Instead, firms offset the increase in wage costs by reducing care quality (as measured by Care Quality Commission inspection ratings).

Importantly, the introduction of the NLW was not accompanied by an increase in local authority funding or local authority fees for care services, which limited firms’ ability to raise prices in response to an increase in staffing costs and pushed them to instead respond by reducing the quality of care. In contrast, a comparable study in the US found that increases in the minimum wage led to increases in the quality of nursing home care, because firms were able to charge consumers higher prices (Ruffini, 2022). If this channel is shut down, providers will need to find other ways to adjust.

It may be possible, up to a point, for higher pay to be absorbed by firms via a reduction in profit margins. But, in light of previous warnings about the financial sustainability of the sector, it seems more likely that if the government wishes to avoid the introduction of a Fair Pay Agreement leading to reductions in care quality or care provision, additional funding for local authorities will be required. This would be over and above any funding for the ‘Fair Cost of Care’ reforms discussed above, which do not allow for any new sectoral pay deal. Additional funding would be particularly necessary if self-funders are allowed to ask local authorities to commission care on their behalf (as discussed above), as this will limit care providers’ ability to cover costs by raising the prices they charge to self-funders.

Precisely how much extra funding would be required depends on the outcome of any new sectoral pay agreement – i.e. the scale of any pay rise, and for whom. Recent modelling for the sector estimated that raising pay to the Real Living Wage (currently £12.00 per hour outside of London and £13.15 within London11) and maintaining pay differentials for more senior staff would result in additional public spending of £1.4 billion per year in today’s prices (Skills for Care, 2024a). (The total cost – i.e. including the costs borne by individuals or firms – was estimated at £2.2 billion per year.) This would be in line with recent changes made by the devolved governments of Scotland and Wales (Scottish Government, 2023; Welsh Government, 2024).