Downloads

Download report PDF here

PDF | 745.49 KB

Key findings

Average pensioner incomes and pensioner poverty

1. Before, and during, the Great Recession, average pensioner incomes were catching up with working-age incomes. Between 2002–03 and 2011–12, median pensioner incomes grew by 22% (after adjusting for inflation), whereas incomes of working-age adults fell by 3%, due to slow growth prior to 2007 and big falls in incomes during the Great Recession. Poorer pensioners’ incomes were growing at a similar rate to average pensioner incomes prior to 2011, leading to relative pensioner poverty falling from 25% in 2002–03 to 13% in 2011–12.

2. Since 2011, average pensioner incomes have been growing at a similar rate to working-age incomes. Average incomes for pensioners – which are now very similar to average incomes below state pension age – grew by 12% from 2011–12 to 2022–23, driven by higher state and private pension incomes. This growth was almost identical to the growth in average working-age incomes of 13% over the same period – driven up by rising incomes from employment.

3. However, since 2011, income growth for poor pensioners has lagged behind the population as a whole. From 2011–12 to 2022–23, incomes for poor pensioners (at the 10th percentile of the pensioner income distribution) rose by only 5% (after adjusting for inflation). This is in part because poor pensioners have benefited from neither the rises in employment income nor the rises in private pension income that pushed up incomes for people on middle incomes.

4. This slow income growth for poorer pensioners means that relative pensioner poverty rose from 13% in 2011–12 to 16% in 2022–23, equivalent to an increase of 300,000 pensioners. A key reason for low income growth for poor pensioners has been that growth in state pension incomes has been offset in large part by falling levels of other benefits – higher state pensions increase pensioner incomes, making them increasingly ineligible for further means-tested state support. Indeed, for the poorest third of pensioners, state pensions rose by 6% between 2011–12 and 2022–23 but total benefit incomes (including state pensions) only rose by 1%. In other words, the support that poor pensioners get from the state increasingly comes from the state pension, rather than the means-tested benefit system.

5. In the years since the onset of the pandemic (2019–20 to 2022–23), lower-income pensioners experienced higher income growth than higher-income pensioners, as they received more state support during the cost-of-living crisis and have benefited more from falling (real-terms) housing costs. Indeed, relative income poverty among pensioners fell from 18% to 16% between 2019–20 and 2022–23.

6. However, these income poverty statistics understate the financial difficulties faced by poorer pensioners, as they do not account for the fact that poorer households are more exposed to sharp rises in gas, electricity and food prices. Pensioner material deprivation – a measure of the household’s inability to afford key essentials – rose from 6% (700,000 pensioners) in 2019–20 to 8% (1 million pensioners) in 2022–23. For example, the fraction of pensioners who could not afford to keep their home warm rose from 2% to 5% (230,000 to 570,000 pensioners).

Trends in different sources of pensioner incomes

7. Before the pandemic, the average incomes of pensioners were pushed up in part by rising state pension incomes. This was due to a combination of triple-lock indexation of the basic state pension since 2011, the introduction of the new state pension in 2016, successive generations of women having spent more years in paid work, and both men and women having accumulated higher earnings-related pensions. Reforms in 2010 and 2016 also substantially boosted the state pension incomes of many women (notably by comprehensive ‘crediting’ for those who spent long periods out of paid work looking after children). As a result, the gender gap in state pension incomes has all but disappeared for those born after 1950.

8. Despite large increases in state pension incomes for women born since 1950 (and higher average household incomes among pensioners), these changes have not led to large falls in relative income poverty for these women compared with previous generations at the same age (in their late 60s and early 70s). In part this is because the reforms of 2010 and 2016 were designed to boost the incomes of (generally) women with low state pension incomes, rather than boosting the incomes of pensioners with low household incomes. It is also due to higher state pensions leading to falls in eligibility to other benefits for low-income families.

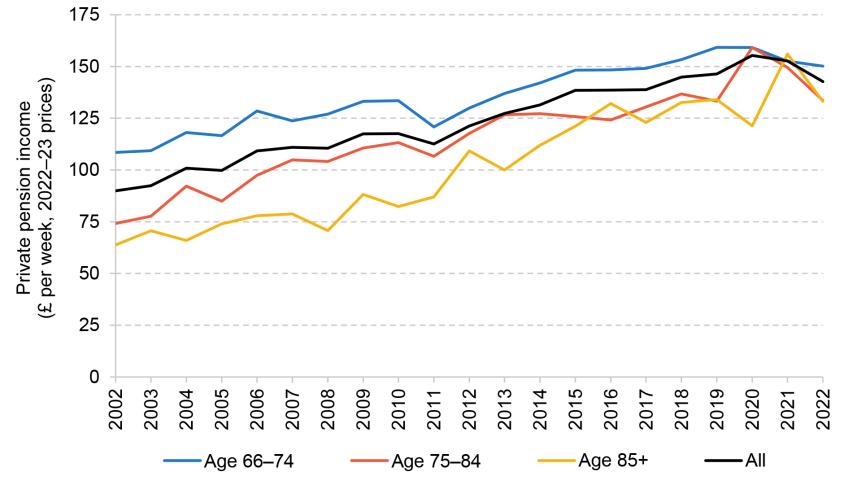

9. Rising incomes from private pensions have been the largest single contributor to growth in average pensioner incomes over the last two decades. This is a result of both gradually increasing coverage (54% of pensioners received income from private pensions in 2019–20 compared with 50% in 2002–03) and increasing amounts received (the average private pension income among those with positive incomes rose from £4,700 to £7,600 a year over this period).

10. Average income from employment (including self-employment) among those aged 66–74 has also been rising gradually over time. This is mainly due to rising employment rates but is also due to rising average earnings among those in paid work. While employment income is not the key income source in older age nor is it the key driver of changes over time, on average it makes up just over half of total household income for working households in their late 60s and early 70s.

4.1 Introduction

Pensioners – the population above the state pension age, currently 66 – make up about a quarter of the adult population in the UK. Given the size of this group, trends in pensioner incomes play an important role in determining trends in the distribution of living standards in the population as a whole. The composition of pensioner incomes, and the factors driving changes to them, are markedly different from those for the rest of the population. Most working-age households receive most of their income from employment, meaning that trends in earned incomes are the key determinant of their incomes. However, only a small minority of pensioners receive significant income from employment.

Pensions – received from either the state or from private sources – make up the majority of income for most pensioners. Pension incomes are driven by a combination of factors such as policy reforms, past employment patterns and the types of pensions offered by employers. State pension entitlements in particular have been subject to substantial reform since the mid 1970s.

Pensioners in low-income households also face a considerably more generous benefit system than working-age households (Cribb and O’Brien, 2022), albeit one where there remain serious challenges around take-up – DWP estimates show that only six out of ten of those entitled to pension credit claimed the benefit in 2021–22 (Department for Work and Pensions, 2024a). Finally, patterns in housing tenure among current generations of pensioners are in stark contrast to the patterns among those under state pension age. Around 74% of pensioner households in 2022–23 owned their home without a mortgage, while 4% owned with a mortgage; 17% of pensioners were social renters and only 5% private renters. By comparison, 23% of working-age households are owner-occupiers without a mortgage and 35% with, while 17% are social renters and 23% private renters. This means that average housing costs among pensioners are generally low, and few pensioners are exposed to changes in either mortgage rates or the private rental market compared with working-age households.

Despite the importance of pensioner incomes in their own right, and the implications for the population as a whole, there has been relatively little work in recent years taking a broad perspective on how pensioner incomes have changed in recent decades. This chapter seeks to remedy that, focusing on three key areas.

First, we provide new evidence on trends in average pensioner incomes, how unequal pensioner incomes are, how that has changed in recent years, and how these trends have fed through to measures of income poverty and material deprivation among pensioners. While the focus of our research is on recent trends, we put these changes in the context of the last 20 years. As incomes measured before and after housing costs are generally similar for pensioners (as housing costs are, on average, low), we mostly illustrate overall incomes after deducting housing costs in order to ease comparability with trends for working-age people, most of whom face significant housing costs.

Second, we dig into more detail on how income from state pensions and benefits has changed over time for pensioners, splitting out changes in state pension incomes from changes in income from other benefits (such as means-tested or disability-related state support). In particular, we show how state pension incomes have changed among recently retired pensioners, and how those changes compare with changes in income from other state benefits.

Finally, we consider the importance of private sources of income for pensioners, both income from private pensions and employment income. These sources of income are more important, on average, for higher-income pensioner households, and the importance of private sources of income has grown in recent decades. This increase is driven by increasing rates of employment among pensioners, as well as higher private pension participation rates meaning that more people are approaching pension age with a private pension.

Before we proceed to the analysis, it is worth noting that our definition of pensioners focuses on people aged 66 (the current state pension age) and over. This means that the changes in average income among our definition of pensioners are not affected by state pension age increases.1 Previous analysis has shown the effects of increasing the state pension age on household incomes (notably, Cribb and Emmerson (2019) and Cribb and O’Brien (2022)), finding that increases in the state pension age substantially reduced average incomes and pushed up income poverty rates.

4.2 Pensioner incomes and living standards over the last 20 years

Trends in pensioner incomes

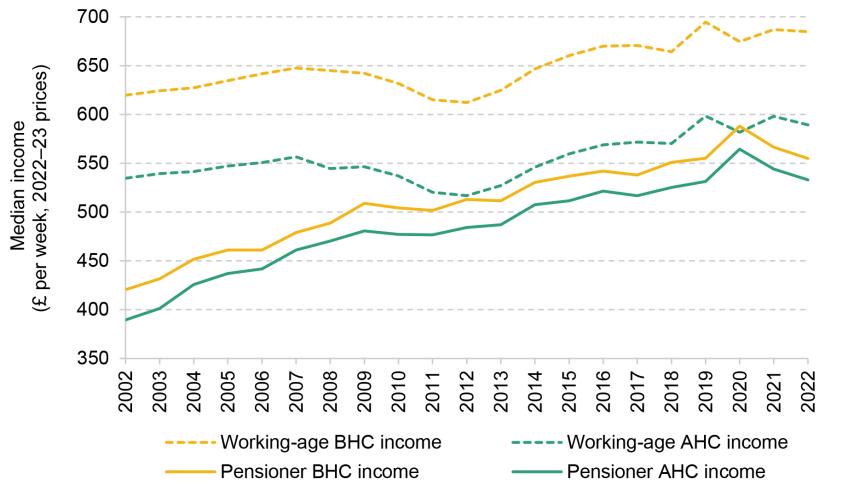

We start this section by analysing median household incomes of pensioners and how they compare with those of working-age households, as shown in Figure 4.1. As in the rest of this report, incomes are equivalised using the modified OECD equivalence scale and expressed in terms of equivalent amounts for a childless couple.2 While equivalisation could affect the long-run trends in incomes if the composition of households changes over time, the overall trends in unequivalised incomes are similar to what we show in this report (see Department for Work and Pensions (2024b) for analysis of unequivalised incomes). The incomes shown are measured as net incomes (after direct taxes and other transfers), in 2022–23 prices. The graph shows incomes both after deducting housing costs (AHC) and before deducting housing costs (BHC).

Figure 4.1. Real median household income over time, pensioners and working-age adults, before and after adjusting for housing costs

Note: ‘Pensioners’ refers to those above the age of 66. ‘Working-age adults’ refers to men aged under 65 and women aged under 60. All incomes are equivalised and expressed as equivalent for a childless couple. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

Figure 4.1 shows that the median pensioner income in 2022–23, after deducting housing costs, was £533 per week, compared with £589 per week among working-age individuals – a gap of roughly 10%. Both of these figures are essentially unchanged since 2019. However, that overall effect over three years reflects pensioners first doing better during the pandemic lockdowns than working-age individuals (as they were less affected by labour market disruptions), but then seeing slightly bigger income falls during the subsequent cost-of-living crisis, compared with working-age adults.3

This relatively small gap in incomes reflects a substantial narrowing over time. Pensioner incomes (AHC) grew at a rate of 3.4% per year from 2002–03 through to the Great Recession (2007–08), compared with an annual average growth rate of just 0.8% among the working-age population. Following the financial crisis, working-age individuals fared even worse, with real incomes falling. This means that overall from 2002–03 to 2011–12, median working-age incomes fell by 3% while median pensioner incomes grew by 22%. Since 2011, income growth among working-age adults has picked up once again and followed a relatively similar trend to pensioner incomes,4 with median income growth for both groups at 12–13% between 2011–12 and 2022–23.

It is worth noting that even though the growth in pensioner incomes after the Great Recession was stronger than income growth among working-age households, pensioners still experienced a slowdown relative to the kind of growth seen before the Great Recession. If real incomes had continued to grow at the rate they did between 2002–03 and 2007–08, pensioner AHC income would be 43% higher in 2022–23 than what it actually was.

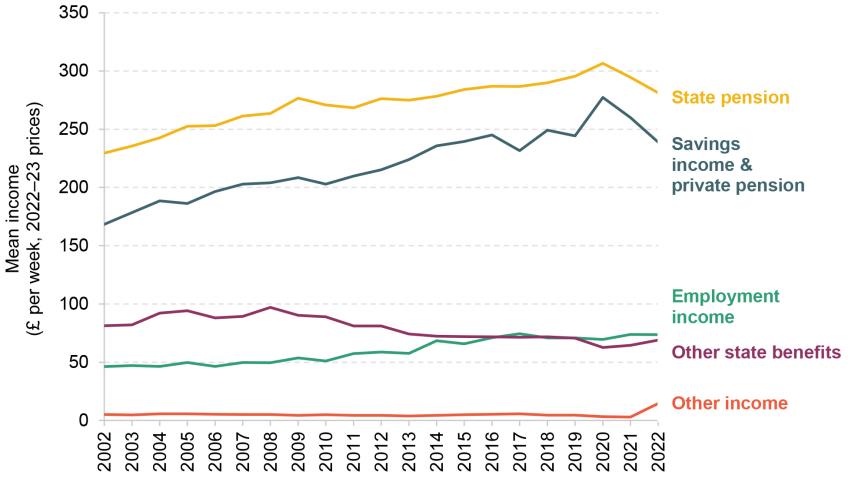

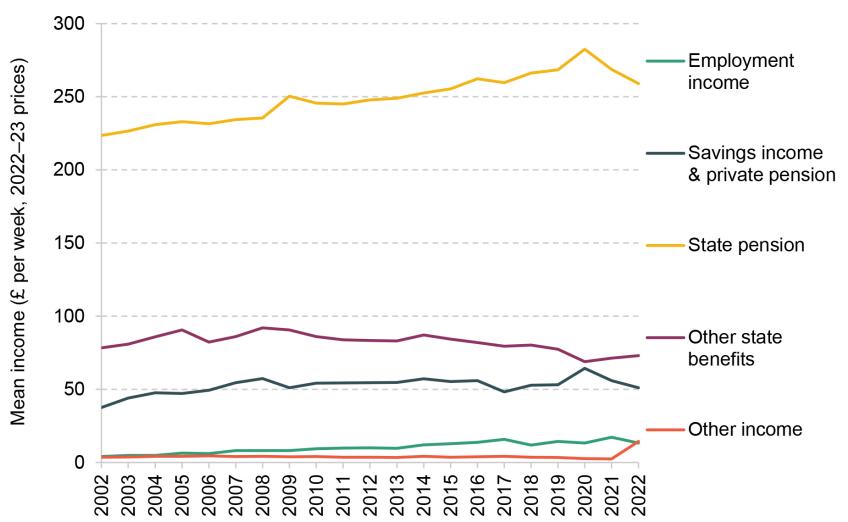

In order to understand the drivers of trends in pensioner incomes over time, we examine the components of pensioner household income and their evolution. Figure 4.2 shows the various components of pensioner income since 2002–03. The state pension is the most important source of income amongst pensioners, followed closely by private pensions and savings. The relative share of these components has been growing over time compared with other components of income.

Figure 4.2. Components of mean household income for pensioners over time, including deductions (housing costs and council tax)

Note: All incomes are equivalised and expressed as the equivalent for a childless couple. ‘Employment income’ includes income from employee jobs and self-employment earnings. ‘Other income’ includes private benefits, child income, the universal energy rebate, the warm home discount scheme and the Welsh fuel support scheme. As total household AHC income also includes council tax and housing costs, these are deducted from the sum of the other components in ‘Other income’. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

Notably, the fall in pensioners’ real median household incomes between 2020–21 and 2022–23 can be attributed to the real-terms falls in state pension and in private pension and savings income. Average state pension income fell in real terms over this period mainly due to the way in which state pensions are indexed each year. In particular, in April 2022, state pensions were increased by 3.1%, which was the inflation measure from the previous September, while CPI inflation in April 2022 had risen to 9.0%. Therefore, the real-terms fall in state pension income was a result of rising inflation and state pensions that only rise with lagged measures of inflation or earnings. The latter also means that this fall will be reversed in coming years – state pensions were increased by 10.1% in April 2023 and by 8.5% in April 2024 in cash terms, both of which are real-terms increases as inflation was falling back towards target.

Pensioners’ average incomes from private pensions and savings have also fallen in real terms since the start of the pandemic. For defined benefit (DB) pension schemes, there is a statutory requirement to increase pension payments each year in line with prices. However, in the private sector, this requirement is generally capped at either 2.5% or 5%.5 With the average rate of inflation around 9% in 2022, these increases were below the rate of inflation, meaning private pension incomes from DB schemes fell over this period.

For those with defined contribution (DC) pensions – who make up an increasingly large share of pensioners – the situation is rather different. These schemes do not provide a guaranteed pension, but rather they provide a pot of money which can be used in retirement. Since 2015, people have been able to decide exactly how to access their DC pension pots from age 55 onwards. Instead of purchasing an annuity (which most people with DC pensions were required to do by age 75 before 2015), an increasing number of people are now taking out money from their DC pension pots flexibly. This means that they can adjust their income drawdowns over time. HMRC statistics on taxable flexible payments show that the rise in average withdrawals (as well as the number of withdrawals) stalled during the pandemic (HM Revenue and Customs, 2021). A number of factors may be driving the fall in the size of flexible payments taken from DC pension pots, such as lower consumption needs or opportunities during the pandemic, or poor returns and high inflation creating uncertainty and potentially eroding the value of a pension pot before it is withdrawn.

Even among those who did purchase an annuity, such as people who accessed their DC pension pots before 2015, the majority purchase annuities that are not adjusted for inflation (Financial Conduct Authority, 2024). This means that private pension income for those individuals will also fall in real terms over time, and particularly so in periods when inflation is high. These changes together are likely to explain some of the fall in the average private pension incomes we see in Figure 4.2.

The graph also shows that income from other state benefits (mostly means-tested benefits and disability benefits, excluding the state pension) fell steadily between 2008–09 and 2020–21. This fall largely reflects younger pensioners being better off than their predecessors were at the same age – a trend we discuss in more detail in Section 4.3. However, this falling trend has been somewhat reversed since the pandemic, as the government introduced various temporary support schemes to help households with the cost-of-living crisis.

In 2022–23, several cost-of-living payments were introduced. These were targeted at households that were deemed to be most vulnerable to the cost-of-living crisis, to offset the impact of lagged uprating – households on the state pension, means-tested benefits and/or disability benefits (Ray-Chaudhuri, Waters and Wernham, 2024). In addition to this more targeted support, measures were introduced to support households more broadly – notably, a £150 council tax rebate for those in properties in Bands A–D and a one-off reduction of £400 in energy bills for all households.

The targeted cost-of-living payments are included in ‘other benefits’ in Figure 4.2, and indeed we can see that the trend of declining state benefits was reversed slightly as the government made these payments to many vulnerable and low-income individuals in 2022–23. The broader cost-of-living support measures (the £150 and £400 sums) are reflected in ‘other incomes’, and again we see an uptick in this category of income in 2022–23. Finally, there have also been gradual increases in employment incomes for pensioners over the last 20 years – a trend discussed in greater detail in Section 4.4.

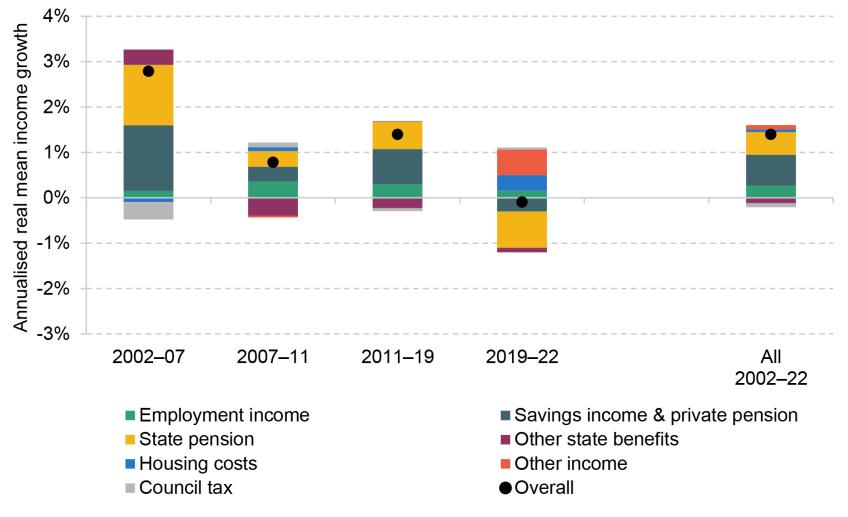

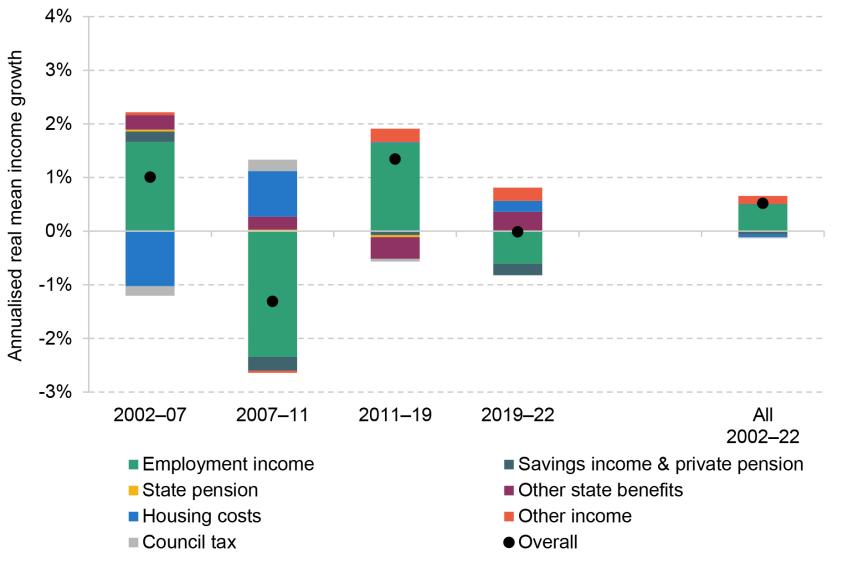

To get a better understanding of how these changes in the various components of income map to total income, we can break down their contribution to income growth. Figure 4.3 shows the contribution of each component of income to overall income growth over the periods 2002–07 (before the Great Recession), 2007–11 (broadly reflecting the period of the Great Recession), 2011–19 (the recovery from the Great Recession) and 2019–22 (the COVID-19 pandemic and the cost-of-living crisis). The black dots show the total growth in mean real incomes over these periods.

Figure 4.3. Contribution of different income sources to mean real income growth for pensioners, by subperiod

Note: The graph shows the contribution to the growth in mean household AHC income over the relevant period that comes from each of the components of income. ‘Pensioners’ are defined as those aged 66 and over. ‘Employment income’ includes income from employee jobs and self-employment earnings. ‘Other income’ includes private benefits, child income, the universal energy rebate, the warm home discount scheme and the Welsh fuel support scheme. Positive growth rates for ‘housing costs’ and ‘council tax’ indicate these costs are falling in real terms. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, various years.

The graph illustrates just how different the drivers of income growth have been in the most recent period compared with the earlier periods. Before the Great Recession, increases in state and private pension incomes, as well as other benefit income (due to the introduction of pension credit), were driving overall income growth among pensioners. During and after the Great Recession, increases in employment income, state pension, and private pensions and savings income were driving overall growth in average pensioner incomes, while the value of other state benefits was falling in real terms.

Since the pandemic, the falls in real income from state and private pensions were offset by the growth in other income (such as the cost-of-living support) and, to some extent, the fall in real housing costs, netting out at an approximately zero overall effect. These trends differ from income trends among working-age households, where the main contribution to both the real-terms increases and decreases in incomes over the same periods comes from employment income (see Figures 4A.2 and 4A.3 in Appendix 4A).

Trends in pensioner income inequality over time

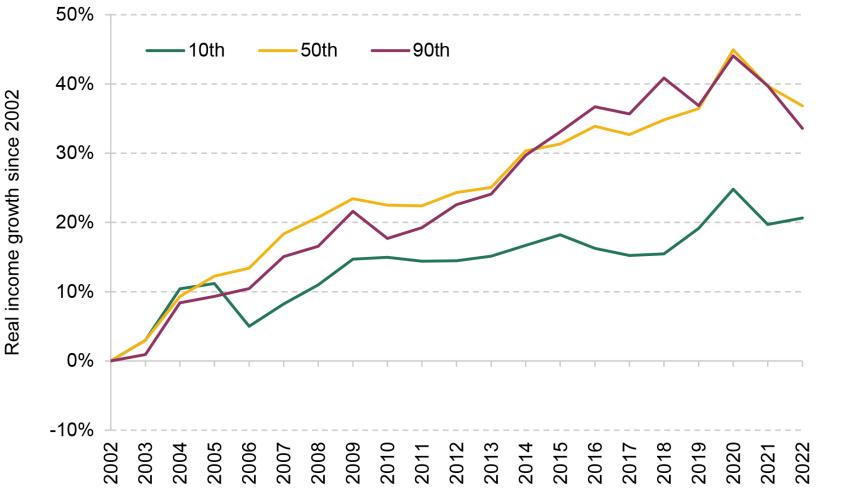

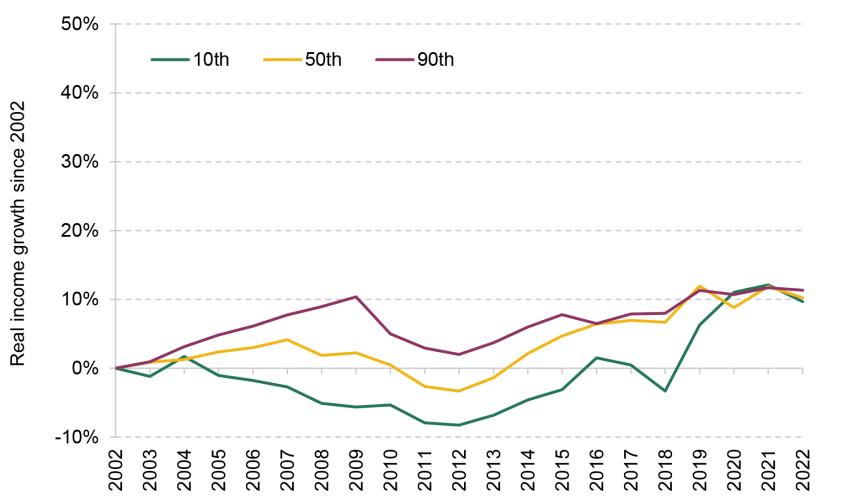

The previous analysis has shown that on average, after two decades of growth, real incomes for pensioners have remained flat since 2019. We now seek to understand how pensioners at different parts of the income distribution have fared. Figure 4.4 shows the growth in real incomes for the 10th, 50th and 90th percentiles of the income distribution, split between pensioners (Panel A) and working-age adults (Panel B).6 The graphs are indexed so that changes in incomes are shown relative to 2002.

Figure 4.4. Growth in real income, by income percentile, for pensioners and working-age adults over time

Panel A. Pensioners

Panel B. Working-age adults

Note: The graph shows real growth in equivalised household income after housing costs since 2002–03 for each year up to 2022–23. Income percentiles are calculated within groups. ‘Pensioners’ refers to those above the age of 66. ‘Working-age adults’ refers to men aged under 65 and women aged under 60. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

First looking at the period from 2002–03 to 2011–12 (after which the recovery from the Great Recession began), we can see that working-age incomes especially at the bottom of the income distribution (10th percentile) were falling, while incomes among the poorest pensioners were more protected, rising by 14% over this period. Incomes in the middle (50th percentile) and top (90th percentile) of the income distribution were also growing faster among pensioners (by 22% and 19% respectively) than among working-age adults over this period.

In the period since the Great Recession (2011–12 to 2019–20), growth in pensioner incomes was faster among middle- and higher-income pensioners than among lower-income pensioners. This is due to the fact that income from private pensions was growing quickly over this period, and these gains are concentrated in the top half of the income distribution. The picture for working-age households was broadly the reverse, with stronger growth in real incomes at the bottom of the income distribution. This was largely due to a rise in employment income for low-income households compared with middle- and high-income households, driven by a fall in worklessness (Cribb et al., 2021), and to the fact that earnings growth was comparatively better for low earners than for high earners over this period (Cribb and Johnson, 2019). Together this means that over the 2010s, income inequality among pensioners was increasing and income inequality among working-age households was decreasing.

These patterns look different for the period from 2019–20 to 2022–23. Average growth in real incomes over this period was negligible or even slightly negative for both pensioners and working-age individuals. However, the profile of growth across the pensioner income distribution is reversed compared with the preceding period. From 2019–20 to 2022–23, it was lower-income pensioners who fared slightly better, as they received greater support from the cost-of-living payments. In contrast, pensioners in the middle and upper parts of the income distribution, who have a much larger proportion of income coming from private pensions compared with low-income pensioners, saw falls in real income over the post-pandemic period, as private pension and savings income fell in real terms. Overall, however, despite the better trends for poorer pensioners since 2019–20, it is still the case that pensioner incomes at the 10th percentile only rose by 5% from 2011–12 to 2022–23.

In conclusion, over the last two decades, pensioner incomes at the middle and top of the income distribution have been growing at similar rates. However, inequality between these middle- and high-income pensioners and low-income pensioners has increased, as growth in incomes for the poorest pensioners has stalled since the early 2010s. In order to shed more light on how low-income pensioners fared over this period, we now turn to understanding trends in the living standards of low-income pensioners.

Incomes of poor pensioners

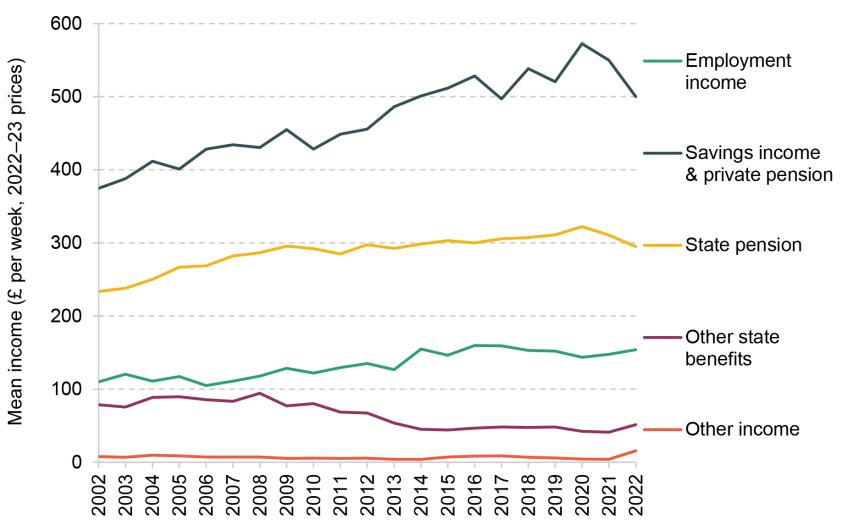

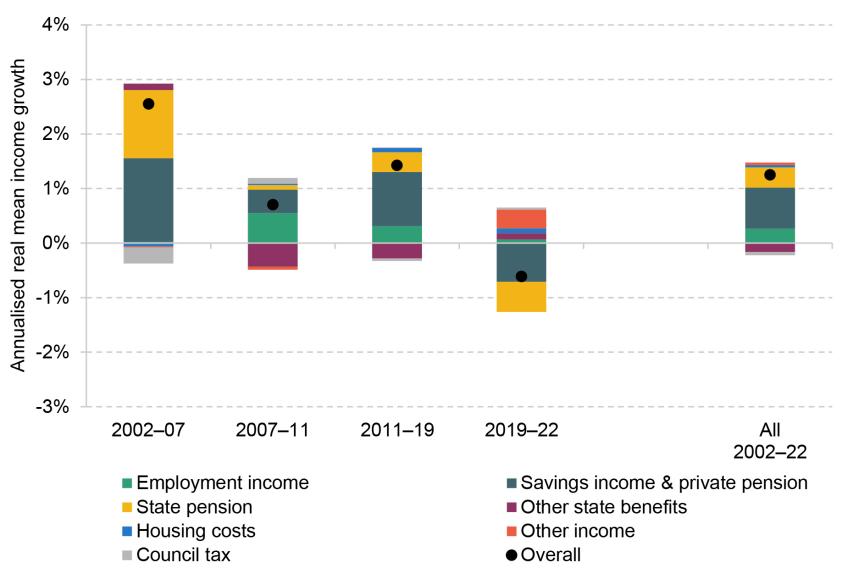

The key sources of income for poorer pensioners are the state pension and other pensioner benefits (see Figure 4A.4 in Appendix 4A), in contrast to high-income pensioners for whom private pensions and savings income (and, to a lesser extent, employment income) are more important (see Figure 4A.5). Figure 4.5 below shows how the components of income have contributed to overall real income growth for the bottom third of the pensioner income distribution (the equivalent graph for high-income pensioners is Figure 4A.6).

Between 2011–12 and 2019–20, real state pension growth boosted the incomes of low-income pensioners by 7.9%. However, as state pensions have risen, the amount of other benefits lower-income pensioners receive has declined. From 2011–12 to 2019–20, for poor pensioners, state pension income rose by £23 (9%), but total income from the state rose by only £17 (5%). Inflation has eroded the value of benefits in recent years, meaning that from 2011–12 to 2022–23 state pension income rose by 6% but total benefit income rose by only 1%. This trend will be discussed in more detail in Section 4.3.

Figure 4.5 highlights two reasons for rising income inequality between pensioners at the middle and bottom of the income distribution. Low-income pensioners are less likely to have significant private pension wealth, and so have not benefited from the increases in average private pension income since the Great Recession. Low-income pensioners also face higher and rising real housing costs, which suppressed the AHC incomes of poorer pensioners between 2011–12 and 2019–20. The rise in housing costs for low-income pensioners over this period is driven by a real-terms increase in private and social rents.

Figure 4.5. Contribution of different income sources to mean real income growth for low-income pensioners (lowest-income third of pensioners)

Note: The graph shows the contribution of the growth in mean household AHC income over the relevant period that comes from each of the components of income. ‘Employment income’ includes income from employee jobs and self-employment earnings. ‘Other income’ includes private benefits, child income, the universal energy rebate, the warm home discount scheme and the Welsh fuel support scheme. Positive growth rates for ‘housing costs’ and ‘council tax’ indicate these costs are falling in real terms. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, various years.

The trends since 2019–20 have been markedly different for poor pensioners. The reliance on the state pension, and its (temporary) decline in real value in April 2022, pushed down poorer pensioners’ real incomes. Between 2019–20 and 2022–23, the real-terms fall in the state pension reduced real household incomes of low-income households by 3.1%. However, since the pandemic, low-income pensioners have benefited more from the fall in real housing costs (given the higher likelihood of paying private rents which did not keep up with inflation over this period) and the additional cost-of-living support, with the fall in housing costs and the increase in other income each pushing up real incomes by 3.6%. Similarly, low-income pensioners were also less exposed to the falls in earnings from employment and real-terms falls in private pensions and savings income over this period, as these are a smaller proportion of total income for this group. This has led to the positive, albeit fairly modest, growth in incomes for low-income pensioners between 2019–20 and 2022–23, compared with falling incomes for higher-income pensioners.

Changes in pensioner living standards over time

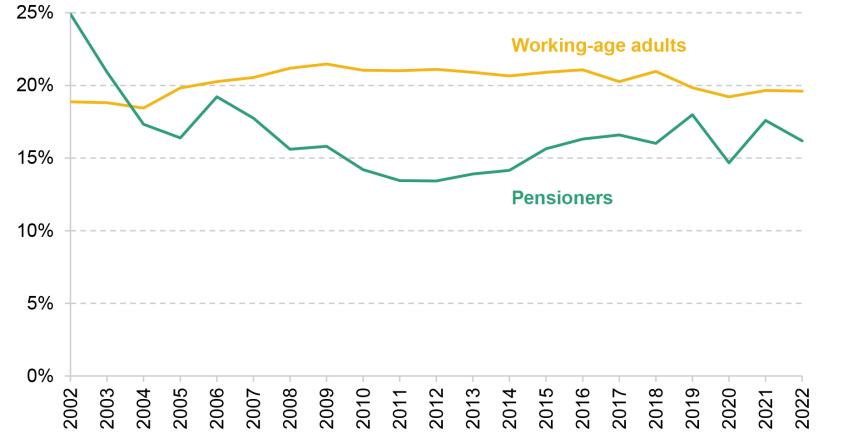

Given the trends in incomes for pensioners at different parts of the income distribution shown above, this subsection discusses the consequence of these trends for pensioner poverty rates and deprivation. Figure 4.6 shows relative poverty rates (AHC) for pensioners and for working-age adults. Relative poverty rates indicate the proportion of individuals with household income below 60% of the contemporaneous median income (among the whole population).

Figure 4.6. Relative poverty rates (AHC) for pensioners and working-age adults

Note: Relative poverty is defined as 60% of contemporaneous median income. ‘Pensioners’ refers to those aged 66 and over. ‘Working-age adults’ refers to men aged under 65 and women aged under 60. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

Relative poverty among pensioners has generally followed a ‘U-shaped’ pattern from 2002–03 to 2022–23, with relative poverty for pensioners falling from 2002–03 to 2008–09, staying relatively flat for a few years, and then rising slightly from 2012–13 up until the onset of the COVID-19 pandemic. The sharp fall in the pensioner poverty rate between 2002–03 and 2004–05 likely reflects the introduction of pension credit in October 2003. Compared with its predecessor (income support for people aged 60 or over), more households were entitled to pension credit and the reform led to higher average awards. 7

This pattern is different from the flatter profile of relative income poverty among the working-age population over this period. For example, after the 2008 financial crisis, relative poverty rates fell for pensioners but rose for working-age individuals. This is because real earnings fell significantly in the aftermath of the Great Recession for working-age individuals, whereas pensioners were largely insulated from these effects.

In contrast, as the economy recovered from the Great Recession and real earnings rose in the mid 2010s, this boosted incomes for working-age people more than for low-income pensioners, leading to small rises in pensioner poverty in the mid 2010s. Despite some fluctuations in relative poverty during the COVID-19 pandemic for the pensioner group, relative poverty rates for pensioners are currently around the same position they were in 2018–19. This implies that the pandemic did not lead to dramatic changes in relative poverty rates among pensioners.

To understand better how living standards have evolved, we look beyond income-based measures of living standards to indicators of material deprivation. Material deprivation measures whether households can afford a range of basic items and activities. A household is classed as materially deprived if it is unable to afford a certain number of these basic items, with more weight being given to items that more families report being able to afford. Looking at a measure of material deprivation is particularly important in recent years, as measures of real household incomes, by construction, assume that all people face the same inflation rates. This has not been true during the cost-of-living crisis as higher gas, electricity and food prices have disproportionately affected lower-income people, as shown in Chapter 3 of this report.

Figure 4.7 shows the share of people who are materially deprived over time. The list of items and the threshold that needs to be crossed for a family to be classed as being in material deprivation are different for pensioners and working-age individuals, so the two series are not directly comparable in magnitude. However, it is informative to compare the trends over time.

Figure 4.7. Share of pensioners (and working-age adults) in material deprivation

Note: The graph shows the shares of pensioners and working-age adults who surpass their respective material deprivation thresholds. A pensioner is said to be in material deprivation if they have a pensioner material deprivation score greater than 20. A working-age adult is said to be in material deprivation if they have an adult material deprivation score greater than 30. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2010–11 to 2022–23.

Figure 4.7 shows that the rates of material deprivation for pensioners and for working-age adults fell steadily after 2013. These falls point to a considerably more positive picture over the 2010s than that shown by measures of relative income poverty. However, these falls in the level of material deprivation among pensioners (and to a lesser extent working-age people) have been undone within the two years following the COVID-19 pandemic, with the proportion of pensioners who are materially deprived now at a similar level to that in 2013–14, and the proportion for working-age people now at 2015–16 levels. It is important to note that these deprivation indices should be treated with care during the pandemic period, as lockdowns and social distancing measures prevented people from living their normal lives. Some of the activities mentioned in the material deprivation questionnaire, such as eating out, were heavily restricted during lockdowns, making it more difficult to interpret people’s responses to whether they can afford these activities. But we see a continued and substantial increase in the share of people in material deprivation in 2022–23 compared with the previous two years, reflecting the impact of the cost-of-living crisis.

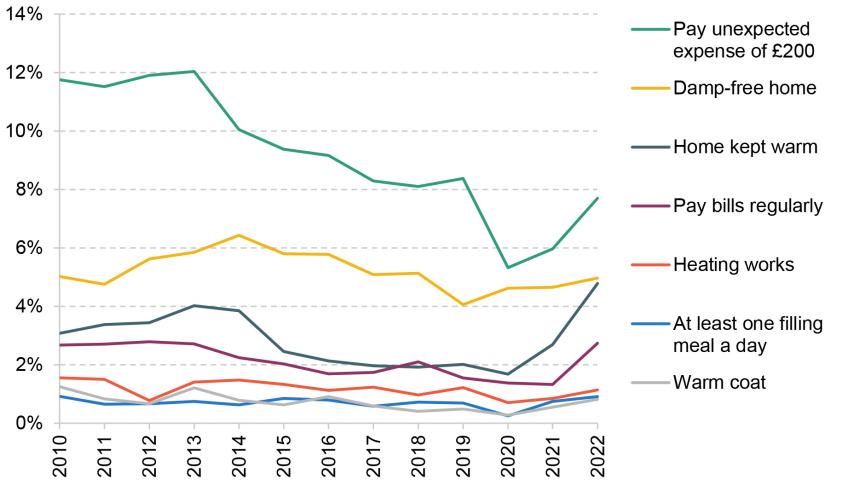

To understand what is driving this rise in material deprivation, we can look at the items that make up the material deprivation score. Figure 4.8 uses a selection of material deprivation items for pensioners, showing the fraction that cannot afford these items. Fifteen items are included in the index, and we show seven of them to aid legibility. We exclude activities that were most affected by social distancing and lockdowns as they would have been heavily restricted for some of the pandemic period: seeing friends and family; getting regular haircuts; going on holiday; going out once a month; having access to a car or taxi. We also do not include three items that have not shown significant change over time: being able to replace your cooker; having access to a telephone; keeping home in a good state of repair.

Figure 4.8. Components of material deprivation: share of pensioners who cannot afford certain items

Note: A selection of pensioner material deprivation items are shown. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2010–11 to 2022–23.

Figure 4.8 shows that the increase in the rate of material deprivation since 2020–21 is not being driven by one component of material deprivation, but rather by a range of factors. In particular, the share of pensioner households being unable to keep their home warm rose sharply from 1.7% to 4.8% during the cost-of-living crisis (between 2020–21 and 2022–23). The share of pensioners saying they are not able to afford to pay bills regularly rose from 1.4% to 2.7% over the same period. The prevalence of being unable to pay an unexpected expense of £200 has risen too, although this appears to be simply returning to around its pre-COVID level.

Ultimately, this means that although average incomes among pensioners have not fallen significantly since the onset of the COVID-19 pandemic, the ability of pensioners to afford basic items – in particular, their ability to keep their home warm – has declined markedly during the cost-of-living crisis. Despite this, it is notable that the overall material deprivation index, and many of the components shown in Figure 4.8, were in 2022–23 at levels similar to or lower than what they were in 2010–11. In other words, while the cost-of-living crisis reversed the recent falls in material deprivation, the rates of material deprivation are still either the same as or lower than they were during the Great Recession.

Summary

Average pensioner incomes have been increasing since the early 2000s, driven by increases in state pension and private pensions (and to lesser extent employment income). Up until around 2011, this growth was much faster than growth in average incomes for working-age adults (due in part to the large falls for working-age adults during the Great Recession). Since 2011, the recovery in employment income for working-age adults means that median pensioner and working-age incomes have grown at similar rates.

The trends for poor pensioners are quite different. Strong income growth throughout the 2000s meant falling relative poverty, down to 13% in 2011 from 25% as recently as 2002. But since 2011, the trends are much less favourable to poorer pensioners, with their incomes rising by only 5% between 2011 and 2022, and relative pensioner poverty rising to 16% by 2022. Poorer pensioners did not benefit from rising employment and private pension incomes that benefited middle-income people (of working-age or pensioners respectively). And increased state pension incomes – for lower-income pensioners – have been significantly offset by reduced eligibility for means-tested benefits.

Looking at the trends since the pandemic in particular, average pensioner incomes in 2022–23 were at the same level in real terms as in 2019–20. This is driven by real falls in state pension incomes, as well as in private pension incomes. These falls were mostly offset by additional cost-of-living support from the government and falls in real housing costs. For state pensions, these recent real falls were purely the effect of uprating using a lagged measure of inflation and therefore will be temporary as large cash increases in 2023 and 2024 have pushed the real value of the state pension back up relative to prices as inflation has fallen back.

While pensioner poverty has – if anything – fallen since 2019, there was a significant rise in material deprivation. This was driven particularly by an increase in the share of pensioners saying they cannot heat their home. Taken together, this illustrates that while incomes of poor pensioners were to a large extent protected since the pandemic, this was not enough to protect all pensioners form the effects of rapidly increasing gas, electricity and food prices.

4.3 How has state support for pensioners changed over time?

The previous section highlighted how important income from the state is for pensioners, most notably the state pension, but also other state benefits. This section examines in more detail how pensioner incomes from the state have changed over time.

In this section and in Section 4.4, we split pensioners by age group. We do this because the experiences that shape the economic outcomes of today’s pensioners vary based on when they were born, working and retiring. For example, at any given point in time, pensioners of different ages faced different state pension rules and have had different work histories due to the economic and labour market conditions they faced during their working life.

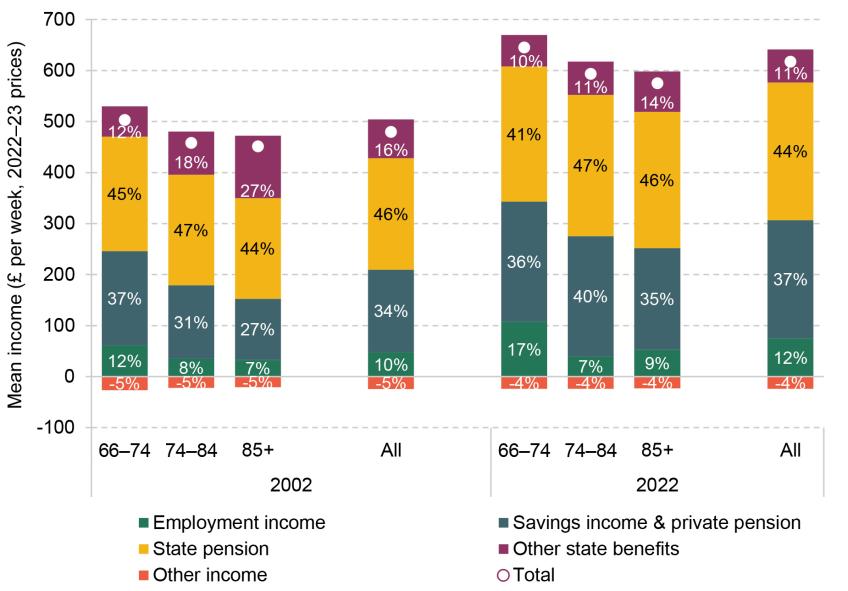

We therefore begin this section by looking at the level and breakdown of the components of household income (before housing costs) by age group, in 2002–03 and 2022–23, as shown in Figure 4.9. This graph shows that younger pensioners have higher real incomes in both years, and that incomes have risen in real terms over the last two decades, by between 27% and 30% among all age groups. It also shows that the higher incomes amongst younger pensioners are largely driven by higher employment income. Income from the state pension makes up over 40% of BHC household income for all age groups in both 2002–03 and 2022–23. It is consistently, over time and across age groups, the largest component of income. Therefore understanding state pension income patterns is vital for explaining overall trends in pensioner incomes – the issue to which we now turn.8

Figure 4.9. Components of household income by age group over time, with percentage figures indicating the share of each component in total income (the white dots)

Note: The graph shows mean household income before housing costs of individuals within the specified age groups. All incomes are in 2022–23 prices and are equivalised and expressed as the equivalent for a childless couple. ‘Employment income’ includes income from employee jobs and self-employment earnings. ‘Other income’ includes deductions from income, most notably council tax. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 and 2022–23.

Impact of state pension reforms on pensioners

Since the introduction of the new state pension in 2016, people have not earned the right to additional earnings-related state pensions. These changes to the earnings-related state pension mean that average state pension income is lower among younger cohorts than among the older groups. However, other state pension reforms that took place in recent decades have benefited groups that previously had a lower state pension entitlement. In particular, the state pension ‘crediting’ arrangements for years not in paid work but doing certain activities – for example, caring for children – have become more comprehensive over time, in particular benefiting married women. In this subsection, we look at how these changes affected female pensioners’ average incomes.

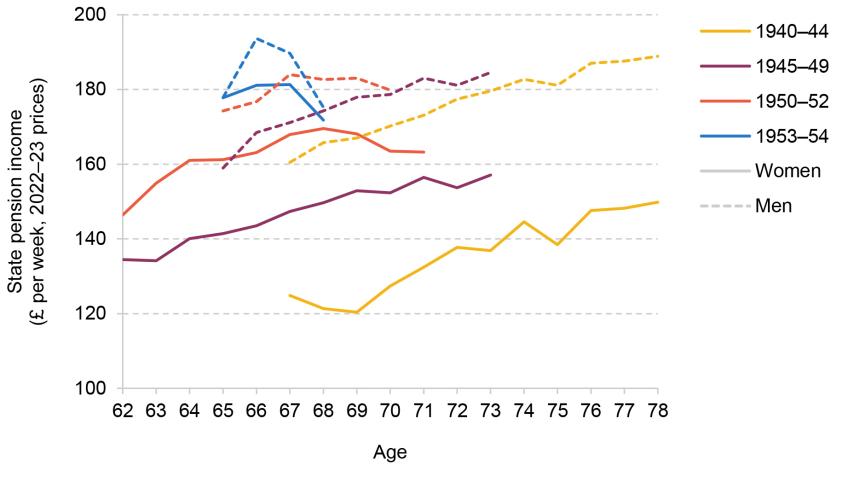

Figure 4.10 shows median state pension income and median household income for men and for women born in different years. Looking at Panel A first, we can see that the gap in individual state pension incomes between men and women is much larger among older generations than among younger generations of pensioners. For example, women born between 1940 and 1944 would expect to receive, on average, less than 80% of the state pension income that men in that cohort were receiving, while women born between 1950 and 1952 can expect to receive around 90% of the state pension income of men born at the same time. By the 1953–54 cohort, women are receiving almost as much as men. Put another way, women born in 1953 and 1954 had state pensions that were 21% higher than for those born in the late 1940s (1945–49). For men, the increase was only 5%.

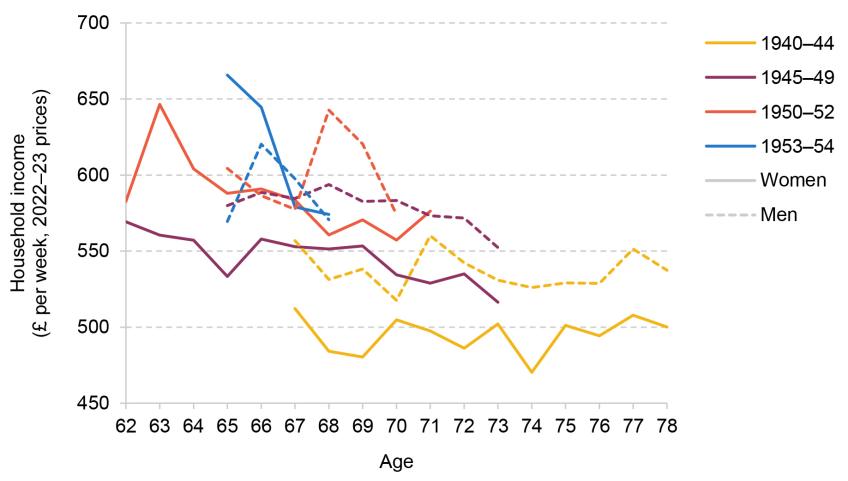

Figure 4.10. Median individual real state pension income and household income by birth cohort, sex and age

Panel A. Median individual state pension income

Panel B. Median equivalised household income

Note: The graph shows the median state pension income received by individuals and the total household income for an individual within the specified birth cohort over different ages. Birth cohorts are defined over financial year of birth. Incomes are presented in 2022–23 prices. Household incomes are equivalised and expressed as the equivalent for a childless couple.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

The gap between men and women has closed for a couple of reasons. First, women born more recently had greater labour market attachment during their working lives, which increases state pension entitlement due to the earnings-related part of the state pension (especially for the older cohorts, who faced the old state pension system) and to a higher number of qualifying years which build state pension entitlement.

Another reason for the gap closing is the reforms that took place over this period. People reaching the state pension age since 2010 (for women, those born since April 1950) were able to qualify for more comprehensive credits for time spent not in paid work but caring for children, increasing the number of qualifying years women with children receive. People reaching the state pension age since 2016 (for women, those born since April 1953) are eligible to the new state pension, which appears to have reduced the gender gap in state pension incomes further.

Given these large reductions in the gender gap in individual state pension incomes, it is also interesting to consider to what extent these state pension reforms feed through to household incomes. Panel B of Figure 4.10 shows the median household income (after housing costs) for men and women from different birth cohorts by age. Focusing on the differences in incomes for women by cohort, similar to the pattern we saw with individual state pension incomes, younger generations of women have higher household incomes than the preceding cohort did at the same age. In fact, generation-on-generation growth in household income is larger than the growth in state pension income. This is due to both women’s private sources of income and (potential) spouses’ incomes being higher for the younger cohorts.

So far, we have focused on median state and household incomes. However, a key feature of some of the state pension reforms in recent decades was increases in state pension incomes for some individuals who would otherwise have very low – or no – state pension income. In particular, women who spent long periods out of the labour market caring for children, who would have previously had a very low state pension, were since 2010 (i.e. for women born in 1950 and later) able to receive a higher state pension entitlement in recognition of the caring activities.

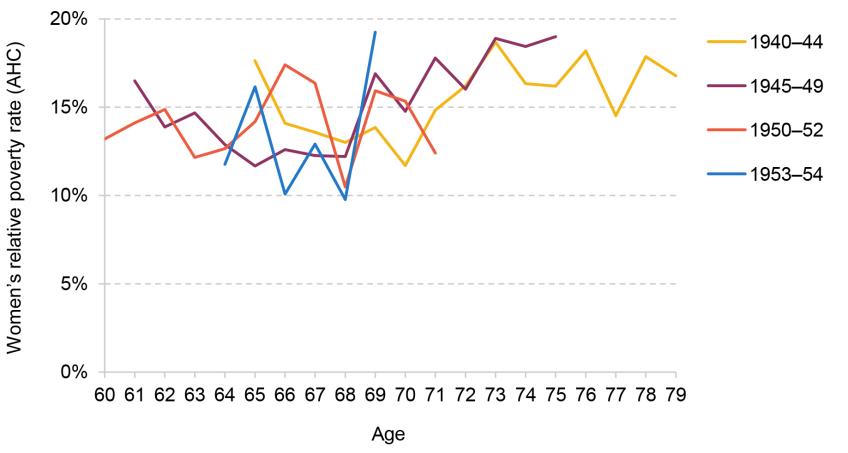

As a result, we want to understand to what extent the increases in the state pension entitlement of women have resulted in changes to poverty rates among female birth cohorts. Figure 4.11 shows, among the same cohorts of women as above, the rate of relative income poverty (after housing costs) by age.

Figure 4.11. Women’s relative income poverty rates (AHC) by birth cohorts and age

Note: The graph shows the relative poverty rate by birth cohort over different ages for women only. Relative poverty is defined as 60% of contemporaneous median income. Birth cohorts are defined over financial year of birth.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

Interestingly, we do not see differences in women’s relative income poverty rates between different generations. Recall that relative poverty rates indicate the proportion of people who have an income of less than 60% of the contemporaneous median. The fact that we see relative poverty remaining stable indicates that cohort-on-cohort growth in average incomes, driven by a range of factors including the previously discussed state pension reforms, improved the incomes of lower-income pensioners, but only at a similar rate as median incomes were rising (therefore not leading to cohort-on-cohort falls in relative poverty). In other words, the incomes of low-income new pensioners have improved against a fixed benchmark, but their incomes relative to other parts of the income distribution have not changed.

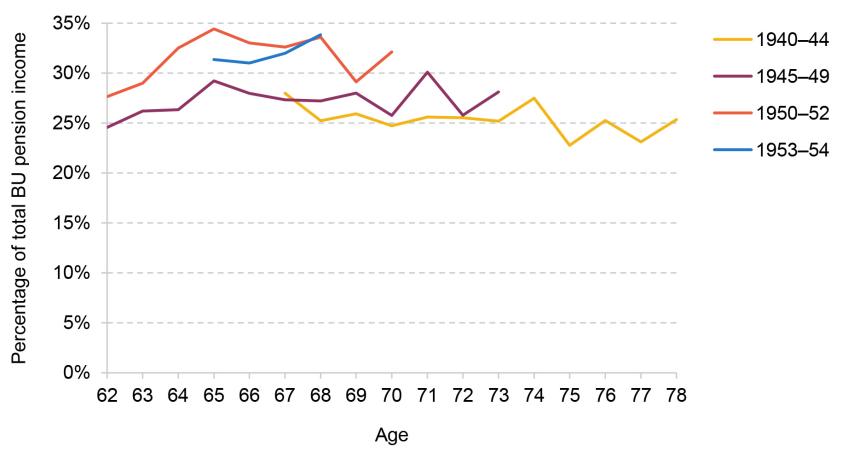

It is worth noting that poverty rates are a household measure to capture the prevalence of low-income households. Other important changes may be happening within households. The women who were more likely to benefit from the improved crediting for years not in paid work are married women, as they are more likely to have spent time out of the labour market caring for young children. Indeed, as shown in Figure 4.12, the split of pension income between men and women in couples has changed in line with the reforms – the fraction of household pension income coming from women (as opposed to men) has been rising for recent generations of new pensioners.

Figure 4.12. Share of total pension income in a benefit unit (BU) contributed by women in couples by birth cohorts and age

Note: The graph shows the share of total benefit unit state and private pension income in couples that is contributed by women by particular birth cohorts over different ages. Birth cohorts are defined over financial year of birth.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

For the 1953–54 generation in their late 60s, on average 32% of household pension income comes from women; this is up from 27% for those born in 1945–49. Together these findings suggest that most of the reforms that increased women’s state pension incomes benefited women who already had higher household incomes, as these reforms were aimed at those who had cared for children earlier on in life, rather than at low-income households. It is likely that many of the women whose incomes are below the poverty line are living in single-person households and may never have had children, and thus would not have benefited from the changes to crediting rules. This can help explain why the 2010 and 2016 reforms do not seem to have had an effect on relative poverty rates among the affected generations of women.

In addition to the changes in how looking after children was credited for building up state pension, there were other ways in which the reforms affected entitlement. The 2010 reform also reduced the required number of ‘qualifying years’ for individuals to receive the full basic state pension; these are the years during working-age with activities that build up entitlement to the state pension. The 2010 reform reduced the number of qualifying years required for a full pension from 44 for men and 39 for women, to 30 years for both men and women. This was then increased back to 35 in the 2016 reforms. Another key change was that while, previously, self-employed workers could not build up entitlement to the earnings-related state pension, since 2016 self-employment does build entitlement to the new state pension.

These changes are likely to benefit other groups who historically may have had lower entitlement to the state pension, such as immigrants who had not spent their whole working life in the UK, and the long-term self-employed (who are disproportionately likely to be from ethnic minorities, specifically people from Pakistani and Bangladeshi backgrounds (Office for National Statistics, 2023)).

Indeed, Cribb et al. (2023) have looked at how immigration and ethnicity gaps in state pension incomes have changed over time as a result of these reforms. Their analysis shows that before the 2016 reforms, there was an ethnicity gap in state pension incomes that could not be explained by immigration status alone, but after 2016 – once we control for immigration status – the ethnicity gap for pensioners is no longer statistically significant. In other words, among those born in the UK, there is no longer evidence of a gap in state pension incomes between those in the white majority and those in other ethnic groups. Cribb et al. also show that after 2010, gaps in state pension entitlements between immigrants and natives were driven by those who arrived in the UK after age 30, meaning that they will not have had enough time to build full entitlement to the state pension in the UK (although they will have had more time to build entitlements elsewhere).

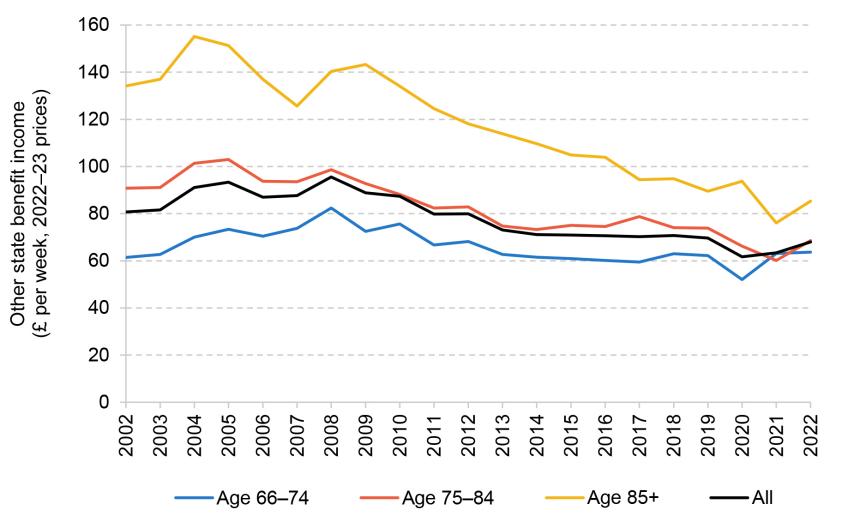

Trends in other pensioner benefits over time

As shown earlier, other benefits (excluding state pensions) have in general become a smaller proportion of pensioner household incomes over time. Figure 4.13 shows that this trend holds across the various age groups, although income from other benefits has fallen most among the oldest age group, particularly since the financial crisis.9

Figure 4.13. Mean state benefit income (excluding the state pension), by age group over time

Note: The graph shows mean household state benefit income (excluding state pension) of individuals within the specified age group. All incomes are presented in 2022–23 prices and are equivalised and expressed as the equivalent for a childless couple. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

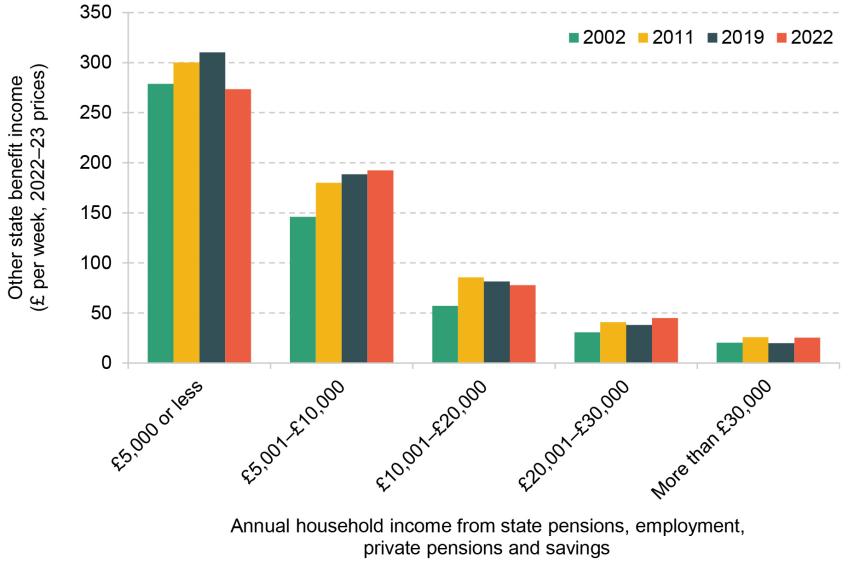

In order to understand the trend of falling pensioner benefits and how it interacts with changes in other incomes, Figure 4.14 shows the mean income that a household receives from state benefits (other than the state pension), where the sample is split into five groups based on their annual (after housing costs) income, excluding the other benefit income. We show the average amounts in 2002–03, 2011–12, 2019–20 and 2022–23.

Figure 4.14. Household income from state benefits (excluding the state pension), split by total household income (excluding other state benefits), over time

Note: The graph shows mean state benefits (excluding state pension) for those in various income groups. Income groups are defined over the real income from state pensions, employment, private pensions and savings summed. All incomes are presented in 2022–23 prices and are equivalised and expressed as the equivalent for a childless couple. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03, 2011–12, 2019–20 and 2022–23.

The graph shows that, conditional on the level of income, the average income received from other benefits by pensioner households in 2022¬–23 was very similar to, if not higher than, the level they received in 2002–03.10 However, the proportions of pensioners in each of these income brackets have changed more dramatically. In 2002–03, 13% of pensioners were in the first income bracket (with an annual income of £5,000 or less) and 18% in the top income bracket (with an annual income of more than £30,000). In 2019–20, before the pandemic, the equivalent numbers were 10% in the lowest bracket and 35% in the highest.

The implication of this analysis is that the fall in mean pensioner benefits (excluding the state pension) among pensioners over time is driven by pensioners being better off now than two decades ago. In fact, if shares of people in each of these income brackets had remained constant at the 2002–03 levels, instead of the £10 per week (2022–23 prices) fall in average income from other benefits between 2002–03 and 2019–20, we would have seen a £21 increase. Looking at a different period, if shares of people in each of these income brackets had remained constant at the 2011–12 levels, instead of the £12 per week (2022–23 prices) fall in average income from other benefits between 2011–12 and 2022–23, we would have only seen a £3 decrease.

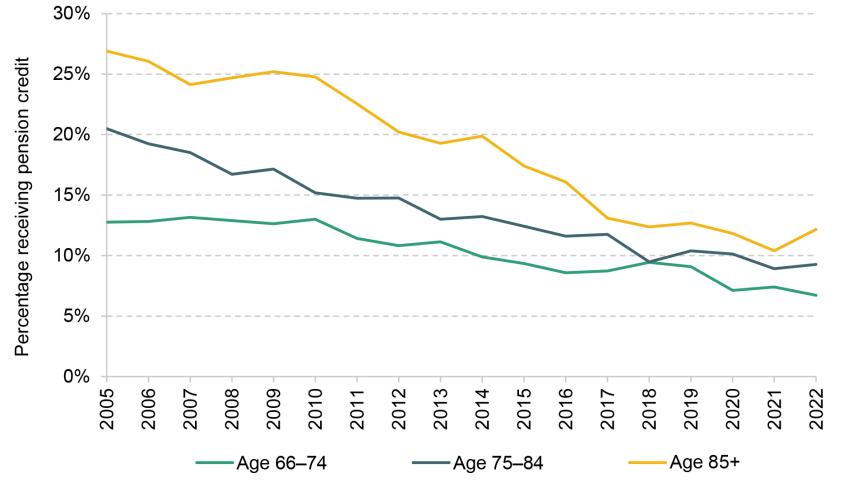

The fact that pensioners are on average better off now than in the past also explains why the prevalence of pension credit, the main means-tested benefit for pensioners, has fallen over time (as shown in Figure 4A.7 in Appendix 4A). This trend is predicted to continue in the future as the full new state pension – which is available to those with at least 35 qualifying years – is now worth more than the standard rate of pension credit. In other words, among those receiving a full new state pension, only those eligible for a higher award of pension credit – due to having a dependent child or eligibility for a disability premium – would be able to receive pension credit.

While the prevalence of pension credit is falling, it is still an important benefit to the lowest-income pensioners. A policy issue for the government – as it was for the previous government – is to increase take-up of pension credit, as DWP estimates show that only six out of ten of those entitled to pension credit claimed the benefit in 2021–22 (Department for Work and Pensions, 2024a). Pension credit is well targeted towards the poorest pensioners in the country, and increasing take-up would help boost their incomes.

Summary

Younger pensioners have higher total incomes, reflecting the fact that they are, on average, better off than previous generations of pensioners. State pension is the most important source of income for all pensioners, but even more so for older pensioners, who tend to have less income from private sources (private pensions and employment). There have been a number of reforms to the state pension, many of which have led to increases in the state pension entitlements of groups who previously had low state pension incomes. Indeed, we can see that women reaching their state pension age later have state pension incomes much closer to those of men, compared with previous generations. Along with other trends, those reforms seem to have pushed up the incomes of more recent generations of female pensioners compared with older cohorts.

However, as these reforms have benefited individuals with lower state pension incomes, some of whom would already have been part of higher-income households, we do not see consequent generation-on-generation decreases in relative income poverty rates for women, despite higher state pension incomes on average. Although these reforms have benefited low-income pensioners, they have not led to their incomes growing faster than those of the population as a whole.

In addition, many households that previously would have been receiving means-tested benefits to protect them from poverty, now receive more of their state support in the form of the state pension instead. This is one reason why rising state pension incomes have not fed through as dramatically to lower pensioner poverty.

4.4 Trends in private pensions and employment income for pensioners

In this section, we examine private sources of income among pensioners and how these have evolved over time. In particular, we focus on private pension incomes, as well as income from employment. As shown in Section 4.2, these sources of income are important in driving aggregate incomes for pensioners, particularly for middle- and high-income households, and therefore will also have consequences for income inequality among pensioners.

Private pension income over time

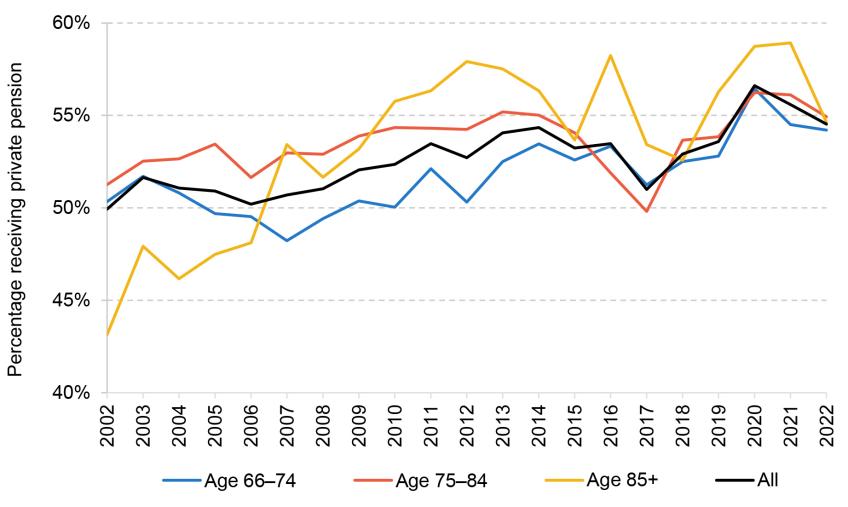

After the state pension, income from private pensions and savings is the second-largest component of pensioner incomes on average, and it is growing in importance over time. Panel A of Figure 4.15 shows the proportion of individuals in different age groups with any private pension income, and Panel B shows the median weekly income over time from private pensions among those with any private pension income.

Figure 4.15. Prevalence and amounts of private pension income for individuals, by age group over time

Panel A. Share with positive private pension income

Panel B. Median amount of private pension income among those with positive private pension income

Note: All incomes are presented in 2022–23 prices and are equivalised and expressed as the equivalent for a childless couple. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

Panel A shows that the proportion of pensioners receiving a private pension has been slowly increasing since the early 2000s. Over the last decade, this is particularly true for the youngest age group, which is consistent with the introduction of automatic enrolment – the statutory requirement of employers to enrol most employees into a workplace pension – having pushed many more people into private pension saving since it started to be rolled out nationwide from 2012.

While private pension coverage is generally fairly high, Figure 4.15 also shows that about two-fifths of individuals do not receive any income from a private pension (in contrast to the state pension, which is received by nearly the whole pensioner population, especially at older ages).

Looking at Panel B, we can see that throughout the period from the early 2000s to 2022–23, younger pensioners’ private pension incomes are higher than those of older groups. This to a large extent reflects differences in labour market experiences of these age groups – the younger groups on average had higher incomes during their working lives, which translate into higher private pension incomes in retirement.

Interestingly, the gaps in the average amount of private pension received by pensioners of different ages have narrowed over time. The larger gap in earlier years is likely due to the fact that in the past, most pensioners were receiving private pension income through defined benefit (DB) schemes (so-called final salary schemes, which typically received higher employer contributions and therefore tend to provide higher incomes in retirement than defined contribution (DC) pensions). Younger cohorts then tended to have stronger labour market histories, leading to higher entitlement. In more recent years, younger generations of pensioners are less likely to have a DB pension and more likely to have a less generous DC pension, which simply provides individuals with a savings pot.

Private pension incomes among all of the age groups have fallen since the pandemic. As described in the first subsection of Section 4.2, this is likely to reflect DB pension incomes growing at a rate lower than inflation and people putting off drawing an income from their DC pension during economic turmoil.

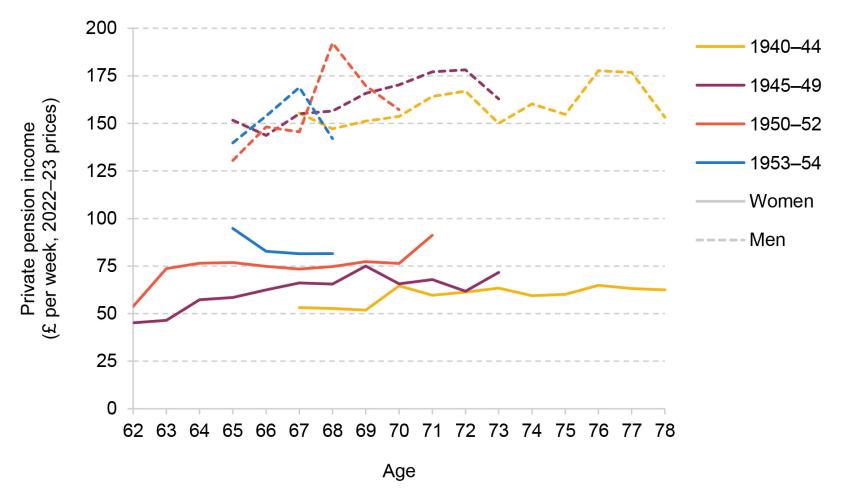

In the previous section, we saw that reforms to the state pension have reduced the gender gap in state pension income over time. We can now see how the private pension gender gap has been changing over time. Figure 4.16 shows the mean private pension income for different birth cohorts of men and women, by age.

Figure 4.16. Mean private pension income by birth cohort, sex and age

Note: The graph shows mean private pension income received by particular birth cohorts at different ages. Birth cohorts are defined over financial year of birth. Private pension income is winsorised at the 99th percentile, presented in 2022–23 prices, and equivalised and expressed as the equivalent for a childless couple.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

It is immediately clear that while there are small generation-on-generation increases in the private pension incomes of women, there is still a large gender gap in private pension incomes even for the youngest cohort. The gap is narrowing – for example, women born between 1940 and 1944 can expect to receive, on average, 38% of the private pension income that men born at the same time received; for the cohort born between 1950 and 1952, women can expect to earn, on average, 48% of men’s private pension income; and by the 1953–54 birth cohort, this number is 56%. But this narrowing is happening at a much slower rate than for the state pension.

It is not surprising that the gender gap in private pension incomes is more persistent. The current gaps in private pensions reflect decades of past differences in labour market experiences between men and women, both in terms of number of years in work and in terms of earnings. Even if recent years had no gender gaps in hourly wages and labour market participation rates, it would be many decades before this filtered through into no gender gap in private pension incomes. Unlike with the state pension reforms, these cumulative differences are not easy to address once these individuals are already in retirement.

Employment around the state pension age

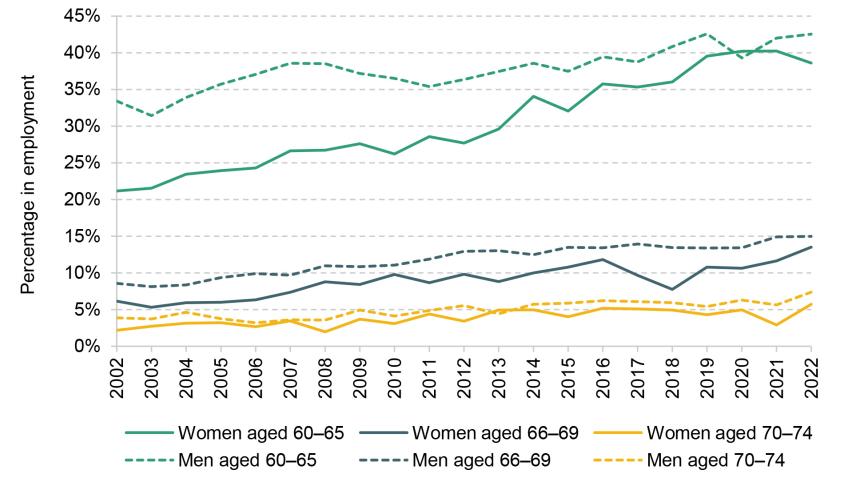

Another source of income for pensioners is income from employment. Employment above the state pension age is not possible for all, especially due to ill health and caring responsibilities but also due to availability of paid work. But for those pensioners who are able and willing to work, employment can act as a flexible source of income. In this subsection, we look at the changing importance of work for pensioners over time.

Figure 4.17 shows the rate of employment among different age groups for men and women separately. As expected, younger age groups – both men and women – generally have higher rates of employment, with 43% of men and 39% of women in their early 60s in paid work in the most recent year of data, compared with 15% of men and 14% of women in their late 60s, and 7% of men and 6% of women in their early 70s. Over this period, women were affected by the rise in the female state pension age from 60 to 65 (between 2010 and 2019), and both men and women were affected by the rise of the universal state pension age from 65 to 66 (between 2019 and 2020). Evidence shows that increases in the state pension age lead to increases in employment rates (Cribb, Emmerson and O’Brien, 2022), but we also see increases in employment rates among these groups in periods when the state pension age was not rising.

Figure 4.17. Employment rates of people aged 60–74, by age group and sex, over time

Note: The graph shows the percentage of people who report being in either full-time or part-time employment or self-employment in each year by age group and sex. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

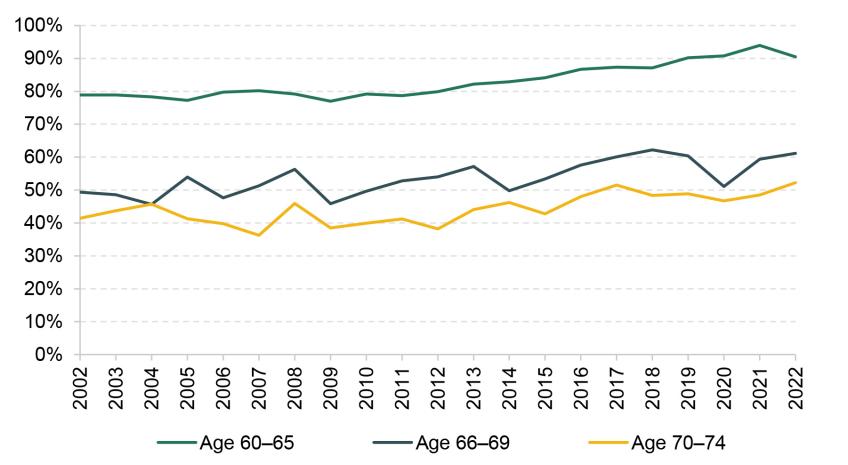

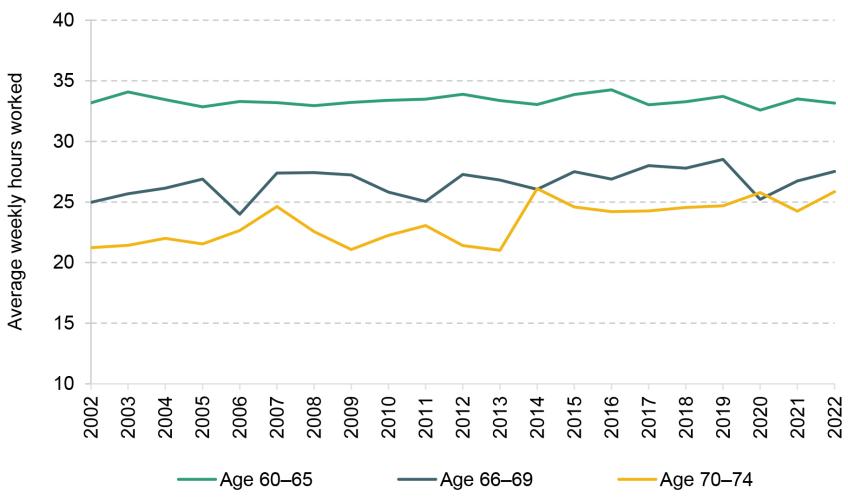

In addition to the younger age groups being more likely to work, they are also more likely to work more hours, as shown in Figure 4A.8 in Appendix 4A. This then translates to higher earnings, as shown in Figure 4.18. While the earnings of workers are increasing over time among all of these age groups, the fastest growth has been among those in the 66–69 age group. Figure 4.19 shows that the proportion of total income coming from employment income among working households is increasing over time. Together these trends illustrate that employment among pensioners is becoming increasingly prevalent over time and that, among those who are in employment at older ages, employment income is becoming a more important source of income.

Figure 4.18. Median employment income for working individuals over time

Note: The graph shows the median earnings from employment and self-employment amongst those with strictly positive earnings each year by age group. All incomes are presented in 2022–23 prices and are equivalised and expressed as the equivalent for a childless couple. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

Figure 4.19. Net household income from employment as a percentage of total household net income amongst working households, by age, over time

Note: The graph shows the ratio of household earnings from employment and self-employment summed over all employed individuals within the specified age groups to total household income summed over all employed individuals within the specified age groups in a given year. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

It should be noted that while higher employment rates boost the incomes of older groups, it is not always clear that they are ‘better off’ in a broader sense. If people are staying in work because of increasing ability to work at older ages – for example, due to the nation’s health being better or there being less age discrimination over time – the higher rates of employment among pensioners could be seen as a positive trend. However, if people feel forced to work because they do not have enough resources otherwise, this may have negative consequences.

Summary

Income from private pensions and savings is on average the second most important source of income for pensioners (after the state pension), although about two-fifths of individual pensioners receive no private pension income. Given that private pension incomes today reflect decades of differences in labour market experiences of different groups, the gaps in private pension incomes between men and women are much wider than the gender gaps in state pension income and they will take much longer to close as there are still large differences in the labour market experiences of men and women on average.

Employment rates among pensioners are low, but rising, and employment income is increasing in importance particularly among younger pensioners. And while only a minority of pensioners are in paid work, employment income makes up an increasing share of total income for those who are.

4.5 Conclusion

As pensioners constitute about a quarter of the adult population, trends in pensioner incomes significantly influence the overall distribution of living standards in the UK. Unlike the working-age population, whose incomes are primarily made up of employment income, pensioner incomes largely depend on pensions, from both state and private sources. Policy reforms and historical employment patterns greatly impact these pension incomes. The benefit system is more generous for pensioners in low-income households than for low-income working-age households, although benefit take-up remains a challenge. Housing tenure patterns also differ, with the majority of pensioners owning their homes outright, leading to generally lower housing costs compared with the working-age population.

Recent decades have seen an increase in average pensioner incomes, primarily driven by state and private pensions and, to a lesser extent, employment income. Prior to 2011, average pensioner incomes were catching up with working-age incomes – due to strong growth before the financial crisis and pensioners not experiencing the large falls in incomes that working-age adults experienced during the Great Recession. This good income growth extended to poor pensioners too – with relative pensioner poverty falling from 25% in 2002–03 to 13% in 2011–12.

Since 2011, the trends have been quite different. Growth in employment income boosted average working-age incomes and growth in private pension incomes and state pensions boosted average pensioner incomes. But this did not extend to poor pensioners – who benefited from neither increases in employment income nor increases in private pension incomes. And growth in state pension incomes for poor pensioners has been largely cancelled out by lower eligibility for means-tested benefits. All this means very poor income growth for pensioners since 2011, with relative pensioner poverty, at 16% in 2022–23, markedly higher than in 2011–12.

As average pensioner incomes were rising in the decade before the onset of the COVID-19 pandemic, income inequality among pensioners was also rising, with the gap between lower- and middle-income pensioners particularly widening as the latter saw larger increases in average incomes from private sources. At the same time, reforms to the state pension have particularly benefited groups with historically lower pension incomes, such as married women, resulting in higher average individual state pension incomes for more recent cohorts of female pensioners. However, these reforms have not significantly reduced relative poverty rates, as they were not particularly aimed at low-income households but rather at women who had been caring for young children during working life. In addition to this, increased state pension incomes may not change the overall state support available to households as rising state pension income may also coincide with reduced eligibility for means-tested benefits.

Appendix 4A. Supplementary figures

Figure 4A.1. Real median household income over time: those above state pension age (SPA) and pensioners, before and after housing costs

Note: This graph shows real median household income of pensioners, referring to those aged 66 and over, and individuals above their state pension age. All incomes are expressed in 2022–23 prices and are equivalised and expressed as equivalent for a childless couple. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

Figure 4A.2. Components of mean household income for working-age individuals

Note: All incomes are presented in 2022–23 prices and are equivalised and expressed as the equivalent for a childless couple. ‘Employment income’ includes income from employee jobs and self-employment earnings. ‘Other income’ includes private benefits, child income, the universal energy rebate, the warm home discount scheme and the Welsh fuel support scheme. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

Figure 4A.3. Contribution of different income sources to mean real income growth for working-age individuals

Note: The graph shows the contribution to the growth in mean household AHC income over the relevant period that comes from each of the components of income. ‘Employment income’ includes income from employee jobs and self-employment earnings. ‘Other income’ includes private benefits, child income, the universal energy rebate, the warm home discount scheme and the Welsh fuel support scheme. Housing costs and council tax are deductions from income. Positive growth rates for ‘housing costs’ and ‘council tax’ indicate these costs are falling in real terms. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, various years.

Figure 4A.4. Components of mean household income for low-income pensioners (lowest-income third of pensioners)

Note: All incomes are presented in 2022–23 prices and are equivalised and expressed as the equivalent for a childless couple. ‘Pensioners’ are defined as those aged 66 and over. ‘Low-income’ is defined as having equivalised household AHC income in the bottom third of pensioners in a given year. ‘Employment income’ includes income from employee jobs and self-employment earnings. ‘Other income’ includes private benefits, child income, the universal energy rebate, the warm home discount scheme and the Welsh fuel support scheme. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

Figure 4A.5. Components of mean household income for high-income pensioners (highest-income third of pensioners)

Note: All incomes are presented in 2022–23 prices and are equivalised and expressed as the equivalent for a childless couple. ‘Pensioners’ are defined as those aged 66 and over. ‘High-income’ is defined as having equivalised household AHC income in the top third of pensioners in a given year. ‘Employment income’ includes income from employee jobs and self-employment earnings. ‘Other income’ includes private benefits, child income, the universal energy rebate, the warm home discount scheme and the Welsh fuel support scheme. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

Figure 4A.6. Contribution to mean real income growth for high-income pensioners (highest-income third of pensioners)

Note: The graph shows the contribution to the growth in mean household AHC income over the relevant period that comes from each of the components of income. ‘Pensioners’ are defined as those aged 66 and over. ‘High-income’ is defined as having equivalised household AHC income in the top third of pensioners in a given year. ‘Employment income’ includes income from employment and self-employment earnings. ‘Other income’ includes private benefits, child income, the universal energy rebate, the warm home discount scheme and the Welsh fuel support scheme. Housing costs and council tax are deductions from income. Positive growth rates for ‘housing costs’ and ‘council tax’ indicate these costs are falling in real terms. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, various years.

Figure 4A.7. Share of people receiving pension credit by age group

Note: The graph shows the share of people receiving pension credit each year within the specified age groups. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2005–06 to 2022–23.

Figure 4A.8. Mean hours worked (for workers), by age

Note: The graph shows the mean hours worked amongst those who report strictly positive hours worked in each year by age group. Years refer to financial years.

Source: Authors’ calculations using the Family Resources Survey, 2002–03 to 2022–23.

References

Bozio, A., Crawford, R. and Tetlow, G., 2010. The history of state pensions in the UK: 1948 to 2010. IFS Report BN105, https://ifs.org.uk/publications/history-state-pensions-uk-1948-2010.

Cribb, J. and Emmerson, C., 2019. Can’t wait to get my pension: the effect of raising the female early retirement age on income, poverty and deprivation. Journal of Pension Economics and Finance, 18, 450–72, https://doi.org/10.1017/S1474747218000057.

Cribb, J., Emmerson, C., Johnson, P. and Karjalainen, H., 2023. The future of the state pension. IFS Report 291, https://ifs.org.uk/publications/future-state-pension.

Cribb, J., Emmerson, C. and O’Brien, L., 2022. The effect of increasing the state pension age to 66 on labour market activity. IFS Working Paper 22/07, https://ifs.org.uk/publications/effect-increasing-state-pension-age-66-labour-market-activity.

Cribb, J. and Johnson, P., 2019. Employees’ earnings since the Great Recession: the latest picture. IFS Report BN256, https://ifs.org.uk/publications/employees-earnings-great-recession-latest-picture

Cribb, J., Karjalainen, H. and O’Brien, L., 2024. Pensions: five key decisions for the next government. IFS Report R319, https://ifs.org.uk/publications/pensions-five-key-decisions-next-government.

Cribb, J. and O’Brien, L., 2022. How did increasing the state pension age from 65 to 66 affect household incomes? IFS Report R211, https://ifs.org.uk/publications/how-did-increasing-state-pension-age-65-66-affect-household-incomes.