Downloads

Download the report as a PDF

PDF | 431.83 KB

Executive summary

Persistently low rates of private pension participation among the self-employed have led to increased policy focus on how to boost pension saving among this group. In this report, we use newly linked administrative data to evaluate how private pension saving changes for employees who move into self-employment. Given the structure of the data, we focus on employees who spend at least two years saving in a ‘relief-at-source’ workplace pension, a common form of ‘defined contribution’ pension saving where contributions are made out of post-tax pay and tax relief is then applied by HMRC. We document how pension saving changes for these employees as they then move into self-employment during the period 2009–10 to 2016–17.

Key findings

- Private pension participation falls substantially for employees who move to self-employment. We study workers who move to self-employment after having saved in a workplace pension for at least two consecutive years as an employee. In the first year following the move to self-employment, over 75% of these workers were no longer contributing to a private pension. Although this is a large decline, the share saving in a pension (24%) is slightly higher than the pension participation rate for self-employed workers as a whole, which hovered around 15% during the period we study.

- The mean total pension contribution rate falls from around 8% of earnings in the final year as an employee to just over 2% of earnings in the year after moving to self-employment. This fall is entirely explained by the drop in pension participation. The mean contribution rate among individuals who continue to save in a pension actually rises to around 10% after the transition.

- Younger workers who move into self-employment are less likely to continue saving in a private pension than older workers. In the first year after their move to self-employment, only 13% of workers aged 30 or under are saving in a pension, compared with around 26% for workers aged 31 or over. The mean pension contribution rate for self-employed workers aged 30 or under is also around half that of older self-employed workers in the year after moving to self-employment.

- There are significant differences in pension participation rates after moving into self-employment by whether the worker became a partner or a sole trader and by their previous level of earnings. In the first year after becoming self-employed, almost half of partners are saving in a private pension, compared with less than one-in-five sole traders. Similarly, workers who were in the top third of the earnings distribution as an employee are around twice as likely to continue saving in a pension into self-employment (37%) as workers who were in the bottom two-thirds of the distribution (around 17%).

- The distribution of pension contribution rates narrows after people move to self-employment. The mean pension contribution rate falls by around 9 percentage points for employees in the top third of the distribution of pension contribution rates before becoming self-employed (from 14% to 5%). For the bottom-contributing third of employees, the mean pension contribution rate only declines by around 1 percentage point (from 2% to 1%) when moving to self-employment. One potential explanation for this is that the differences in contribution rates for employees are at least partly driven by differences in employer contributions, which do not exist for self-employed workers.

- The large drop in pension saving for workers moving from an employee job into self-employment highlights the importance of policies that could facilitate pension saving for the self-employed. Employer involvement, payroll-based saving and automatic enrolment mean that saving in a pension is generally easy for employees; however, for the self-employed, saving in a pension involves much more hassle. Policies that make pension saving easier for the self-employed, such as integrating pension saving into either tax returns or business software used by the self-employed, would be a good starting point for reform.

1. Introduction

Self-employed workers make up a significant part of the UK workforce, with over one-in-eight workers in self-employment. However, there are long-standing concerns about low levels of pension saving among this group: only 20% of working-age self-employed workers were saving in a private pension in 2022–23, compared with around 80% of employees (Department for Work and Pensions, 2025a). The trends in pension participation differ markedly between the two groups. In the late 1990s, almost 50% of self-employed workers saved in a private pension; however, this share fell substantially through the 2000s, and has hovered around 20% since the early 2010s. In contrast, pension participation for employees has risen significantly in recent years, from almost 50% in 2012 to around 80% in 2022–23, principally due to the roll-out of automatic enrolment into pension saving between 2012 and 2018. While automatic enrolment has made pension saving much easier for employees, self-employed workers are not covered as they have no employer to automatically enrol them into a pension scheme.

As a result, there is considerable policy focus on the drivers of low levels of pension saving among the self-employed and how to boost saving among this group. Previous research has shown that only around one-third of the fall in pension participation rates for the long-term self-employed between the mid 2000s and the mid 2010s can be explained by the changing composition of the self-employed workforce (such as lower levels of income) (Karjalainen, 2023).

In this report, we instead focus on the pension saving behaviour of workers who are newly self-employed – specifically, those who have moved from being an employee into self-employment. We provide novel evidence of how pension participation and contributions evolve for employees who move into self-employment using newly linked tax data and administrative data from pension providers, and show how these responses differ for different groups of workers. This is important in understanding whether experiences with pension saving for employees translate into higher (or lower) levels of pension saving when they move into self-employment, and in assessing policy suggestions such as facilitating self-employed workers to continue contributing to a previous workplace pension scheme.

2. Data and sample construction

In this section, we describe the linked administrative data we use for our analysis as well as how we construct our sample of workers who transition from an employee job to self-employment.

Data

The data we use for this research are the UK government’s administrative data on pension contributions (known as COM100 data) linked to administrative tax records, specifically Pay-As-You-Earn (PAYE) data for employees and Self-Assessment data for the self-employed. This newly linked dataset contains the highest-quality data on pension contributions and earnings in the UK, and can be used to follow individuals as they move between employee jobs and self-employment. For a more detailed description of this linked dataset, see Appendix B.

Importantly, the COM100 data only contain information on contributions to ‘relief-at-source’ pension schemes. In this pension arrangement, contributions are made out of post-tax income, with HMRC topping up the contributions to apply tax relief. All self-employed pensions and personal pensions, as well as a significant number of pensions for employees, are relief-at-source pensions. However, some employees have another type of pension arrangement, known as net-pay arrangements, whereby tax relief is applied immediately as the pension contribution is made out of pre-tax pay. All defined benefit pensions are net-pay arrangements, as are some defined contribution schemes, and any contributions to these schemes will not be in our data. In other words, while we comprehensively observe pension contributions made by self-employed workers, we only have data on contributions for many – but not all – employees.

Sample construction

We wish to analyse what happens to pension saving for workers who move from an employee job into self-employment. However, not all such transitions will look the same. Some workers will only move into self-employment for a matter of months before moving back into a job as an employee; others may have worked on and off both as an employee and in self-employment for years. Some may have no gap between being an employee and self-employment; others might be out of work for a couple of years.

There is therefore a trade-off in determining the sample we wish to analyse to answer this question. One option is to adopt a broad sample definition, potentially making the observed empirical patterns more reflective of wider, sometimes messy, transitions between employee jobs and self-employment. However, doing so can mean that the results mix up a wide set of different experienced transitions, making it hard to draw obvious conclusions from the data. Instead, we opt for a narrower, cleaner sample definition, focusing on people who were consistently saving in a private pension as employees, before moving into self-employment for at least two tax years (and not remaining in their employee job). This choice makes our results easier to interpret and can imply clearer lessons for policy.

Our sample period of interest is from tax years 2009–10 to 2016–17. We do not use earlier data because prior to 2009–10 we do not have access to PAYE tax records for the universe of employees. We do not use later data because employer pension contributions are not reliably captured in COM100 data after 2016–17.

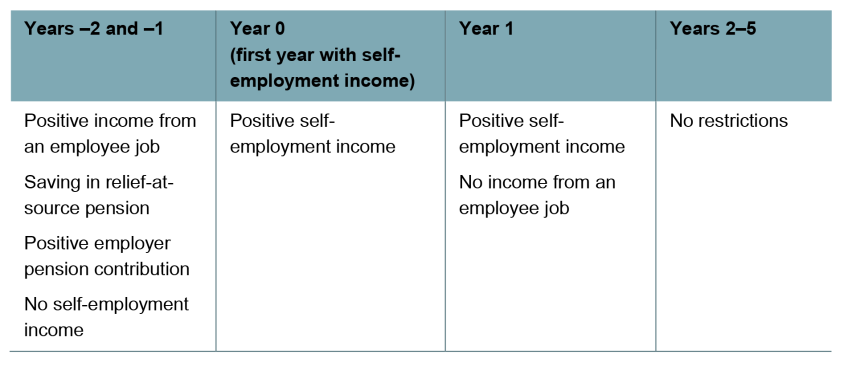

We now set out the steps taken to create the sample of workers we focus on for our analysis, as also summarised in Table 1. First, as COM100 data only cover relief-at-source pensions, we do not know pension contributions for all employees. We therefore focus on employees who are saving in a relief-at-source pension scheme before they move to self-employment, as we know how much they are saving in a pension. We impose some stability before the move by focusing on people who were employees saving in a relief-at-source pension for (at least) two consecutive years (years –2 and –1) and who were not in self-employment in either of those years. This is to focus on employees making a more meaningful transition from an employee job to self-employment. We further restrict the sample to employees who receive a positive employer pension contribution in the two pre-transition years. This is to exclude any employees who may only be saving in a personal, rather than workplace, pension scheme, as these individuals could continue saving into the same scheme after becoming self-employed without any change in saving behaviour.

Table 1. Sample construction

Note: The sample uses data from tax years 2009–10 to 2016–17. Self-employment income contains sole trader and partner income. There are also no restrictions on the sample based on what people were doing three or more years before they move into self-employment.

We also impose ‘stability’ on the move into self-employment, by focusing on people who are in self-employment in both the initial year of transition (year 0) and the following year (year 1). In other words, we exclude people who are self-employed for a very short time. In addition, we exclude people who still receive positive employment income one year after the transition year (year 1), again to focus on a more meaningful transition out of work as an employee into self-employment. We do not make any restrictions on pension saving behaviour from year 0 onwards, as this is precisely the outcome we wish to examine.

Applying these restrictions leaves us with 35,453 transitions from an employee job to self-employment. The sample is small relative to the total self-employed or employee workforce, but it captures a clear, policy-relevant transition and is still large compared with many survey datasets. With automatic enrolment having increased the fraction of employees who are consistently saving in a workplace pension, a larger fraction of people who move from an employee job to self-employment now (in the mid 2020s) would meet our sample criteria compared with when our data are available (mostly during the 2010s, when automatic enrolment had not been fully rolled out).

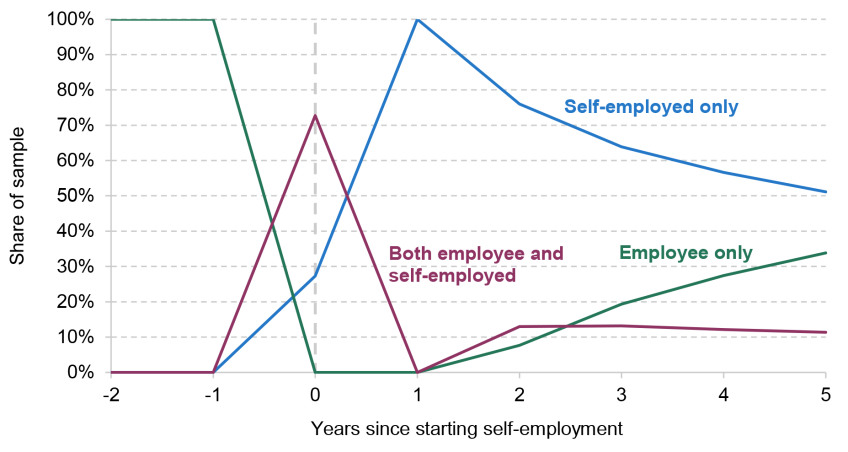

Figure 1 shows the composition of our sample around their moves into self-employment. Prior to the transition (years –2 and –1), 100% of the sample are – by construction – employees. In year 0, we require them to have positive income from self-employment but we make no restriction on whether they receive any income from an employee job. The majority (73%) of the sample are both an employee and self-employed in this year, as many moves into self-employment take place partway through the tax year. In year 1, the whole sample work only in self-employment by construction. Following this, we make no restrictions on the individual’s employment status. As we move further away from the transition, more of the sample move back into an employee job and out of self-employment. By year 5, half the sample work only in self-employment, one-third work only as an employee, and just over 10% work in both modes. We do not make any further restriction to change this, first to avoid shrinking the sample size further and second because we are also interested in what happens to pension saving for people around this transition even if they move back into an employee job.1

Figure 1. Composition of the sample around move from employee job to self-employment (for employees saving consistently prior to move)

Note: ‘Employee only’ refers to workers who have positive income from an employee job and no income from self-employment. ‘Self-employed only’ refers to workers who have positive income from self-employment and no income from an employee job. ‘Both employee and self-employed’ refers to workers who have positive employee and self-employment income.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

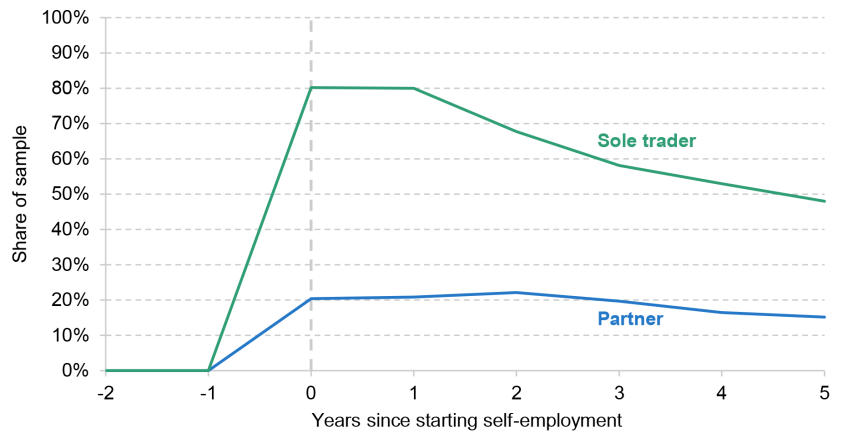

Figure 2 provides more context for the type of self-employment transitions contained in our sample by showing the shares working as sole traders and as partners. Previous work has shown that these two different types of self-employed workers have very different incomes on average and tend to work in different industries (Cribb, Miller and Pope, 2019). In the year of the transition and the following year (years 0 and 1), 80% of the sample work as a self-employed sole trader, compared with 20% as a self-employed partner.2 This is consistent with the finding of Cribb, Miller and Pope (2019) that there were around four times more sole traders than partners in the UK in 2015–16. However, this composition changes slightly in later years following the transition, partly because more workers move back to working as an employee, but also because the share working as a sole trader falls proportionally more than the share working as a partner. By year 5, of those still working in self-employment, 24% work as a partner.

Figure 2. Shares of sample working as sole traders and as partners around move from employee job to self-employment (for employees saving consistently prior to move)

Note: See Table 1 for the definition of the analysis sample.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

3. Moves into self-employment and pension saving

In this section, we analyse how pension participation and contributions evolve around the move to self-employment. Throughout, it is important to bear in mind the timing of the transition, as described in Section 2. Year 0 is a transition year in which many individuals still have some income as an employee (and therefore may still be saving in a workplace pension), while year 1 is the first year in which everyone in the sample is fully self-employed. From year 2 onwards, we place no restrictions on whether individuals remain self-employed or move back into an employee job, so patterns further away from the transition will partly reflect changes in labour market status as well as changes in pension saving behaviour.

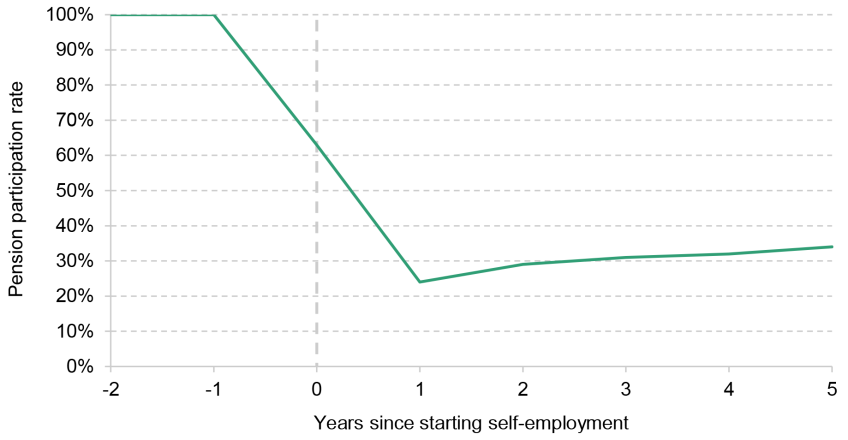

Figure 3 shows pension participation rates around the transition to self-employment. In the two years prior to starting self-employment, 100% of the sample are saving in a private pension. This is by construction since we restrict our sample to employees saving in a relief-at-source pension in the pre-transition periods because our data contain no information about net-pay pension saving. In the year of the transition to self-employment (year 0), 63% of the sample are saving in a private pension. However, a majority of the sample spend at least some of this year working as an employee, as shown in Section 2, so it is likely that many of these are simply continuing to save in a workplace pension when they are employees.

Figure 3. Pension participation rate around move from employee job to self-employment (for employees saving consistently prior to move)

Note: See Table 1 for the definition of the analysis sample.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

In year 1, when all the sample works only in self-employment, 24% are saving in a private pension. This means that the substantial majority of the sample are not saving in a private pension, but it is above the participation rate among the self-employed overall during our sample period in administrative data, which varied between 10% and 20% depending on the year and the definition of self-employment used (Karjalainen, 2023). This suggests that, during our analysis period, individuals who were saving in a pension while an employee were slightly more likely to then continue saving after becoming self-employed, compared with the self-employed as a whole. While this could reflect some small persistence in pension saving behaviour following the transition to self-employment, it may equally be driven by ‘selection’, as individuals who saved in a pension while recently an employee are likely to have a higher underlying propensity to save than other individuals in self-employment. The pension participation rate then increases slightly over time, reaching 34% by year 5 following the transition.3

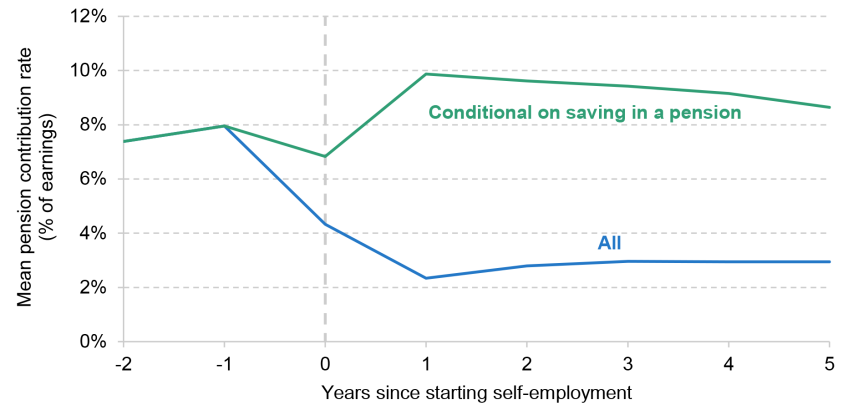

Of course, as well as pension participation, how much people are saving is also important. Figure 4 shows the mean pension contribution rate (i.e. contributions as a percentage of total earnings) among our sample in the years we study. The blue line shows this out of everyone – that is, including ‘zeros’ for workers who are not saving at all in a pension, while the green line restricts the sample just to pension savers. Throughout, we include in this measure both individual and, for employees, employer pension contributions.

Figure 4. Mean pension contribution rate around move from employee job to self-employment (for employees saving consistently prior to move)

Note: Includes both employee and employer pension contributions for employees. The ‘All’ line refers to the mean pension contribution rate among everyone in the sample, including zeros for those not participating in a pension. See Table 1 for the definition of the analysis sample.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

Averaged across the whole sample, the mean pension contribution rate falls following the move to self-employment, from 8% to around 2–3%. This is entirely explained by the drop in pension participation seen in Figure 3: the mean pension contribution rate among savers actually increases after the transition, from 8% to almost 10%. One potential explanation for this is that those who continue to save while in self-employment have a particularly high propensity to save, and so have a high contribution rate.

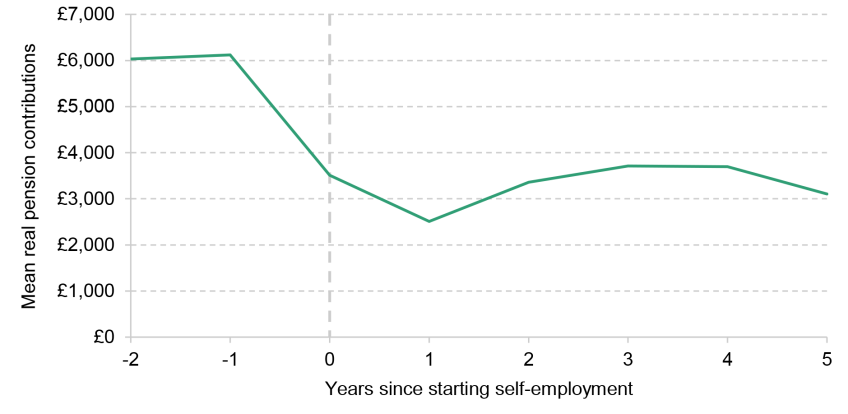

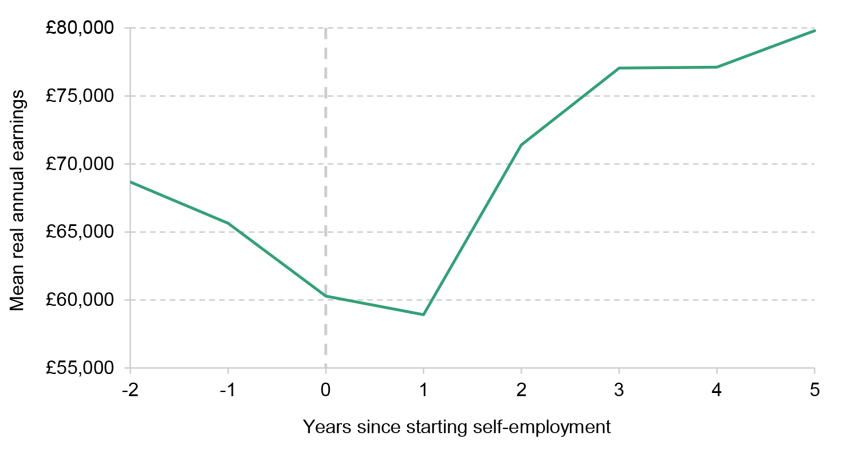

Figure 5 illustrates that mean pension contributions in real cash terms also fall considerably with the transition to self-employment, from £6,100 annually in year –1 to £2,500 in year 1. Pension contributions start to rise after this, reaching £3,700 by year 4, consistent with mean earnings actually increasing for our sample in later years, as shown in Figure A1 in Appendix A.4

Figure 5. Mean real annual pension contributions around move from employee job to self-employment (for employees saving consistently prior to move)

Note: Includes both employee and employer pension contributions for employees. The figure plots mean annual pension contributions for everyone in the sample, including zeros for those not participating in a pension, in 2026–27 prices, deflated using the Consumer Prices Index (CPI). See Table 1 for the definition of the analysis sample.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

Summary

Overall, moving from an employee job to self-employment is associated with a large and immediate drop in pension participation among individuals who were previously saving consistently in a workplace pension. Only around one-quarter continue to save once fully self-employed, although this is above the rate for the self-employed as a whole. Average pension contribution rates also fall substantially, due to the fall in pension participation. These patterns are consistent with employer involvement and workplace defaults playing a large role in the pension saving behaviour of employees, but not persisting once these workers move into self-employment.5

4. How do the results differ for different groups?

The results in Section 3 potentially mask substantial heterogeneity in pension saving behaviour around the point at which employees move into self-employment. In this section, we examine how pension participation and contributions differ across groups in terms of their age, type of self-employment, employee earnings prior to moving to self-employment, and pension saving behaviour as an employee. This helps shed light on whether some groups are more likely than others to maintain engagement with pension saving after leaving their employee jobs.

Differences by age

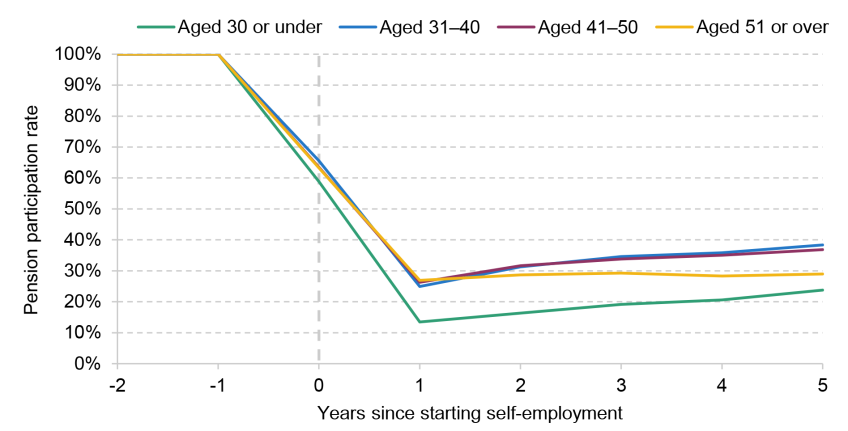

Figure 6 shows pension participation rates around the move to self-employment, split by age in the year before the person starts self-employment. Pension participation falls sharply for all age groups once individuals become fully self-employed, but the fall is particularly large for the youngest group (aged 30 and under). In year 1, only around 13% of those aged 30 or under are saving in a pension, approximately half the rate of those aged 31 or over. Pension participation then rises gradually after year 1 for all age groups, though differences still persist. By year 5, the participation rate among those aged 30 or under (24%) remains well below that of those aged 31–40 and 41–50 (around 37–38%). Pension participation for those aged 51 or above increased only slightly over the period, reaching 29% by year 5, potentially as this group is less likely to move back into an employee job.

Figure 6. Pension participation rate around move from employee job to self-employment (for employees saving consistently prior to move), by age

Note: Ages are defined based on the year before the transition year (year –1). See Table 1 for the definition of the analysis sample.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

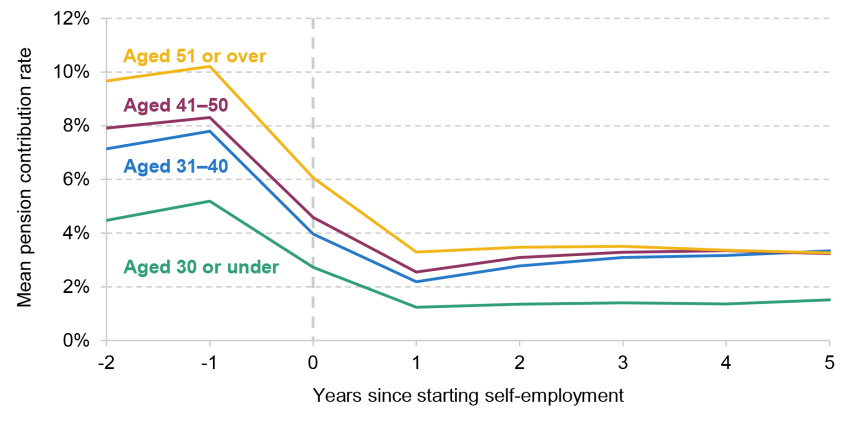

Figure 7 shows mean pension contribution rates by age, averaged across everyone in each group (i.e. including zeros for non-savers). Prior to starting self-employment, mean contribution rates increase with age, ranging from around 5% for the youngest group (30 and under) to around 10% for those aged 51 and over. Mean contribution rates then fall substantially for all age groups after the move into self-employment, with the differences between age groups narrowing somewhat. In year 1, mean contribution rates are around 1.2% for those aged 30 or under, compared with around 2.2–2.6% for those aged 31–50 and around 3.3% for those aged 51 or over. In other words, the difference in mean contribution rates between the youngest and oldest age group fell from 5 to 2 percentage points around the point that people start in self-employment. By year 5, mean contribution rates have risen somewhat for those aged 31–50 (to just over 3%), but they remain low for the youngest (30 and under) group at around 1.5%.

Figure 7. Mean pension contribution rate around move from employee job to self-employment (for employees saving consistently prior to move), by age

Note: Includes both employee and employer pension contributions for employees. The figure plots mean pension contribution rates, as a percentage of earnings, for everyone in the sample, including zeros for those not participating in a pension. Ages are defined based on the year before the transition year (year –1). See Table 1 for the definition of the analysis sample.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

Overall, these results highlight that younger workers are substantially less likely to maintain pension saving after moving into self-employment, even several years after the transition. This is consistent with patterns from the Financial Conduct Authority’s Financial Lives 2024 survey, which showed that younger workers were much less likely to be highly engaged with their pension than older workers (Financial Conduct Authority, 2025).

Differences by type of self-employment

We now compare outcomes for those who enter self-employment as a sole trader and those who enter as a partner, based on the legal form entered at the point they start self-employment (year 0). As shown in Figure 2, partners make up a minority of transitions in our sample, but a sizeable one. Previous research has shown that there are large differences between these groups, with partners having substantially higher average incomes than sole traders, for example (Cribb, Miller and Pope, 2019).

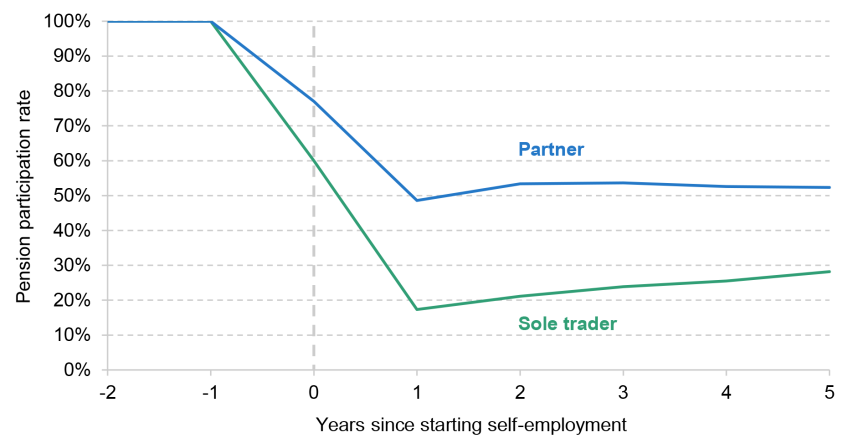

Pension participation is substantially higher after moving to self-employment among those who become partners than among those who become sole traders, as shown in Figure 8. In year 1, around 49% of those who initially become partners are saving in a pension, compared with only around 17% of those who initially become sole traders, a difference of just over 31 percentage points. From year 2 onwards, participation among those entering partnerships remains broadly stable at just over 50%, whereas participation among those becoming sole traders rises gradually, reaching around 28% by year 5. This increase for sole traders may occur because sole traders are more likely to re-start an employee job than are partners.

Figure 8. Pension participation rate around move from employee job to self-employment (for employees saving consistently prior to move), by type of self-employment entered

Note: The groups are defined based on legal status in the transition year (year 0), even if people then change legal status or move out of self-employment in later years. See Table 1 for the definition of the analysis sample.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

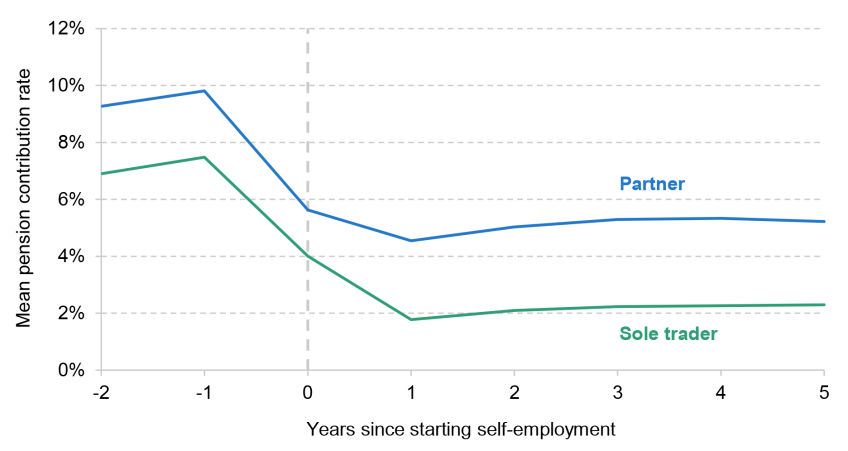

Figure 9 shows corresponding differences in mean pension contribution rates (as a share of earnings), again including zeros for non-savers. Employees who subsequently become partners had higher contribution rates even when they were employees (at around 10% in year –1, compared with around 7.5% for those who subsequently become sole traders). If anything, this difference widens slightly after the move into self-employment. In year 1, the mean contribution rate is 4.5% for partners, compared with 1.8% for sole traders. By year 5, contribution rates are 5.2% for partners and 2.3% for sole traders. Taken together, these figures suggest that low pension saving after entry to self-employment is much more concentrated among those who become sole traders; those who become partners are far more likely to continue saving, and to save at higher contribution rates.

Figure 9. Mean pension contribution rate around move from employee job to self-employment (for employees saving consistently prior to move), by type of self-employment entered

Note: Includes both employee and employer pension contributions for employees. The figure plots mean pension contribution rates, as a percentage of earnings, for everyone in the sample, including zeros for those not participating in a pension. The groups are defined based on legal status in the transition year (year 0), even if people then change legal status or move out of self-employment in later years. See Table 1 for the definition of the analysis sample.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

Differences by earnings level before starting self-employment

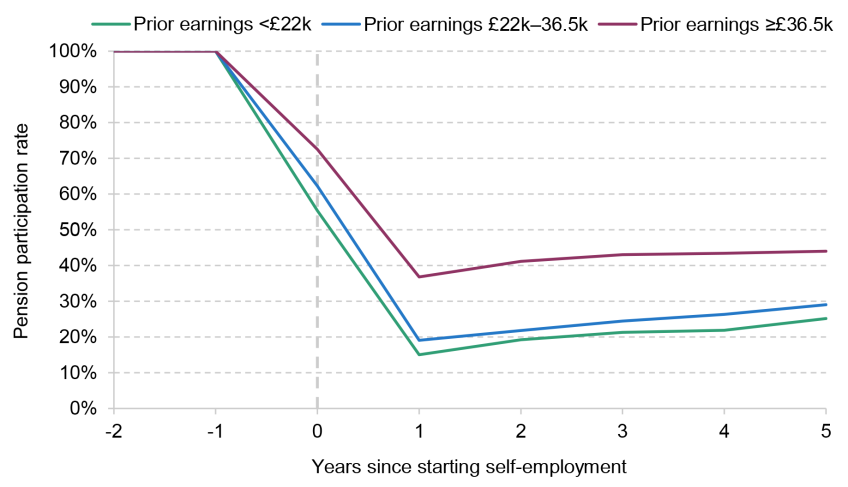

Figure 10 compares pension participation after the move to self-employment for three different groups, defined based on their average level of earnings in the two years prior to the transition (i.e. years –2 and –1). For employees earning less than £36,500 (in 2023 prices – approximately the bottom two-thirds of the earnings distribution for this group before starting self-employment), pension participation falls to below 20%, compared with a rate of 37% for those earning at least £36,500 initially. Interestingly, we do not see large differences in pension participation rates after moving to self-employment between workers who had low and those who had medium levels of earnings when an employee.

Figure 10. Pension participation rate around move from employee job to self-employment (for employees saving consistently prior to move), by level of earnings as an employee

Note: The groups are defined based on real average annual earnings in years –2 and –1. See Table 1 for the definition of the analysis sample.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

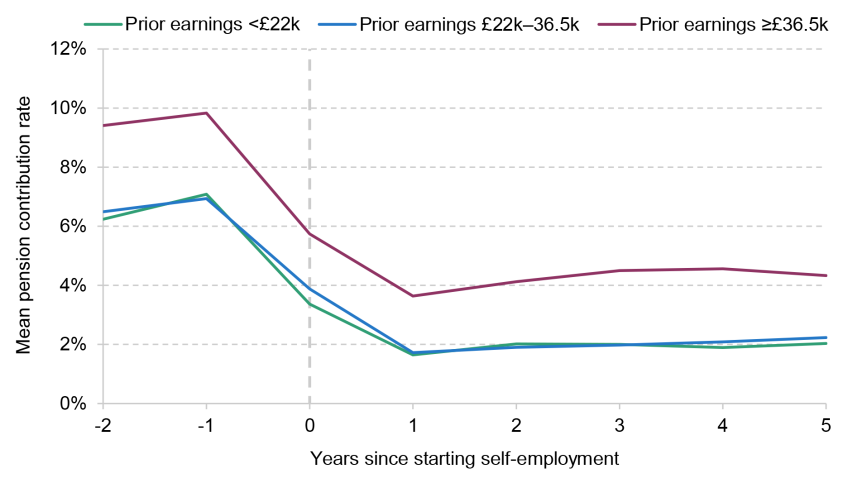

Average pension contribution rates are also very similar for the bottom and middle earnings groups both before and after moving from an employee job to self-employment, as shown in Figure 11. For these groups, earning less than £36,500 when an employee, mean pension contribution rates fall by around 5 percentage points from around 7% before the transition to just 2% of earnings after becoming self-employed (including zeros for those not saving). Mean pension contribution rates are unsurprisingly higher for the top earnings group both before and after the transition, although we see a fall of 6 percentage points, from 10% to around 4%, for this group. These patterns again chime with results from the Financial Conduct Authority (2025), which finds higher levels of engagement with pensions among respondents with higher household income.

Figure 11. Mean pension contribution rate around move from employee job to self-employment (for employees saving consistently prior to move), by level of earnings as an employee

Note: Includes both employee and employer pension contributions for employees. The figure plots mean pension contribution rates, as a percentage of earnings, for everyone in the sample, including zeros for those not participating in a pension. The groups are defined based on real average annual earnings in years –2 and –1. See Table 1 for the definition of the analysis sample.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

Differences by pension contribution rate before moving to self-employment

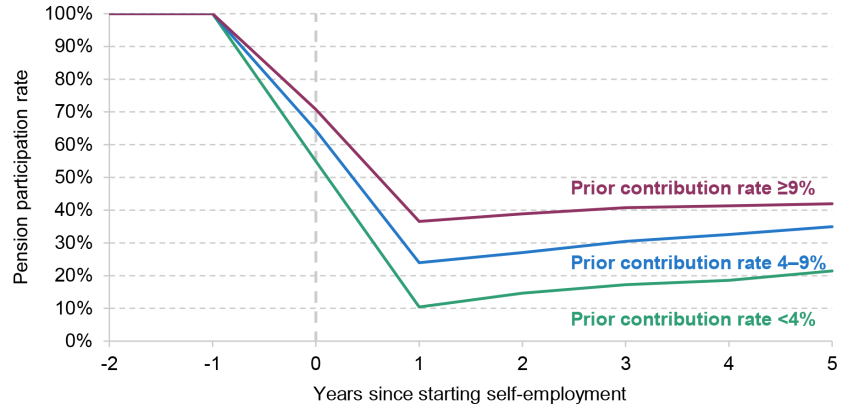

The final dimension of heterogeneity we analyse is by level of pension contribution rate before moving into self-employment. We again split the sample into three groups of approximately equal size, this time based on their average pension contribution rate in the two years prior to starting self-employment, including both employee and employer pension contributions. We then plot how pension participation rates evolve for these three groups in Figure 12. Those with lower pension contribution rates while an employee are less likely to continue saving in a private pension in self-employment: in year 1, pension participation is 37% among those contributing 9% or more pre-transition, compared with only 10% for those contributing less than 4%.

Figure 12. Pension participation rate around move from employee job to self-employment (for employees saving consistently prior to move), by pension contribution rate as an employee

Note: The groups are defined based on average pension contribution rate (as a percentage of earnings) in years –2 and –1. See Table 1 for the definition of the analysis sample.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

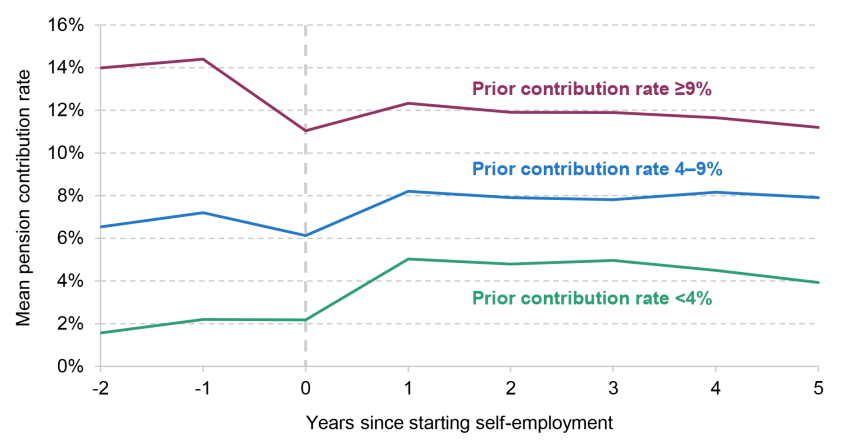

Figure 13 shows that the gaps in contribution rates that, by construction, exist prior to the move into self-employment, persist into self-employment. However, the gaps narrow somewhat. For the top-contributing third of employees, the mean pension contribution rate drops from 14% to around 5% when they move into self-employment; for the bottom-contributing third of employees, the mean contribution rate falls from 2% to 1%.

Figure 13. Mean pension contribution rate around move from employee job to self-employment (for employees saving consistently prior to move), by pension contribution rate as an employee

Note: Includes both employee and employer pension contributions for employees. The figure plots mean pension contribution rates, as a percentage of earnings, for everyone in the sample, including zeros for those not participating in a pension. The groups are defined based on average pension contribution rate (as a percentage of earnings) in years –2 and –1. See Table 1 for the definition of the analysis sample.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

Interestingly, the gaps in average pension contributions conditional on pension saving also narrow, as shown in Figure A2 in Appendix A. One potential reason for this is that employer pension contributions play an important role in the differences in contribution rates among employees, but are non-existent for self-employed workers. Another possible explanation is that those who saved more as employees might not need to save as much when they become self-employed because they have already accumulated a sufficient pension pot.

Summary

In summary, there are notable differences in pension saving behaviour around the move to self-employment for different groups. Younger workers, lower earners and workers who become a sole trader are much less likely to continue saving in a pension after becoming self-employed than older workers, higher earners and those who become a partner, respectively. In addition, the distribution of pension contribution rates narrows after workers move to self-employment. However, despite these differences, it is important to note that we consistently observe a large drop in pension saving alongside the move to self-employment for all groups we analyse.

5. Conclusion

Low rates of pension participation among the self-employed are of significant concern to policymakers,6 and have generated a wide range of suggested policy proposals in response. Of course, key to evaluating any suggested reform is a thorough understanding of which groups have low levels of saving and the drivers behind this. This report has provided novel evidence on pension saving behaviour for workers who transition from an employee job into self-employment using administrative data on pension saving newly matched with HMRC tax data.

Our analysis focuses on workers who are consistently saving in a workplace pension as an employee and then move into self-employment. After the move to self-employment, over three-quarters of these workers no longer save in a private pension. However, the pension participation rate among the workers we analyse (24%) is higher than the pension participation rate among the self-employed workforce as a whole.

This suggests that experiences of saving in a pension as an employee do not have extensive persistent effects on pension saving behaviour when self-employed. This is consistent with the roll-out of automatic enrolment – which dramatically increased pension participation for employees – having little discernible effect on aggregate pension participation among the self-employed during the 2010s. In other words, although many more employees gained experience of saving in a pension due to automatic enrolment, this did not transfer across into markedly higher pension participation rates when these employees moved into self-employment.

Instead, the large drop in pension saving alongside starting self-employment highlights the importance of institutional features in driving pension participation. Employer involvement, payroll-based saving and automatic enrolment mean that saving in a pension is generally easy for employees. Indeed, the path of least resistance for most employees is to save in a pension. For the self-employed, saving in a private pension requires much more active effort. This likely explains why we see a large fall in pension saving rates among all subgroups we analyse, even if the magnitude of the drop differs somewhat by group.

Policies that make pension saving easier for the self-employed would therefore be a good starting point for reform. For example, there is a good case for integrating pension saving into self-assessment tax returns (as suggested by Almond, Phillips and Sandbrook (2022), Cribb and Karjalainen (2023) and Cribb et al. (2025)). At a minimum, this would require self-employed workers to make an active choice about their level of pension contributions when filling out their tax return. This could be taken further by making pension saving the default, with an easy option to opt out within the form. An alternative is greater integration of pension saving into the banking platforms and business software used by many self-employed workers for managing their finances. Research from Nest Insight (Blakstad, Stockdale and Rodohan, 2025) indicates that this approach could be effective in increasing pension saving rates among the self-employed, particularly if pension saving is offered on an ‘opt out’ basis.

In addition, it would be worth considering policies that make it easier for newly self-employed workers to continue saving in the workplace pension pot they had with their previous employer. For example, when an employee leaves a job, their employer could be required to provide details to the employee on how to continue contributing to their current workplace pension (in cases where this is possible). This information would be provided to employers by the pension provider, meaning this requirement should be fairly low cost for employers. This approach could be taken further by having the pension provider contact people who cease saving in their scheme with information on how to set up a direct debit to continue contributing. If either of these options were taken forward by policymakers, it would be worth trialling them before implementation to assess the most effective timing and framing of communication to encourage pension saving, as well as to understand potential costs or downsides from such changes.

Finally, this report also highlights the usefulness of the newly matched data for understanding pension saving. The dataset we use links high-quality, third-party-reported data on pension contributions for the universe of savers in relief-at-source schemes with administrative data on individuals’ incomes and economic activity held by HMRC. This new dataset opens up several avenues for future work. For example, it could be used to study how tax incentives affect private pension saving for the self-employed and high-income people, who are potentially less well represented in survey data and have more complicated financial affairs. Furthermore, the analysis in this report could be extended to better understand heterogeneities in pension saving for different types of self-employed workers, such as by industry.

Appendix A. Additional figures

Figure A1. Mean real annual earnings in the years around move from employee job to self-employment (for employees saving consistently prior to move)

Note: Includes earnings from both employment and self-employment, in 2026–27 prices, deflated using the Consumer Prices Index (CPI). See Table 1 for the definition of the analysis sample.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

Figure A2. Mean pension contribution rate around move from employee job to self-employment conditional on saving in a pension, by pension contribution rate as an employee

Note: Includes both employee and employer pension contributions for employees. The figure plots mean pension contribution rates, as a percentage of earnings, for workers contributing to a private pension. The groups are defined based on average pension contribution rate (as a percentage of earnings) in years –2 and –1. See Table 1 for the definition of the analysis sample.

Source: Authors’ calculations using linked HMRC administrative data on pension contributions (COM100) to PAYE and Self Assessment data, 2009–10 to 2016–17.

Appendix B. Description of datasets

The data used for this research are the HMRC’s administrative data on pension contributions (known as COM100 data) linked to administrative tax records, specifically Pay-As-You-Earn (PAYE) data for employees and Self Assessment (SA) data for the self-employed. At the time of writing, these linked datasets are expected to be made more widely available for use by researchers in the short to medium term. In this appendix, we provide more information on these datasets, including their construction and what they contain.

The COM100 data are administrative data on the universe of pension contributions made to ‘relief-at-source’ pension schemes. The underlying data are provided from pension providers to HMRC in the COM100 Annual Return of Information form.7 The data currently exist from the 2001–02 tax year through to the 2020–21 tax year.

Importantly, one of the key variables (contributions from the employer) no longer has to be reported from the 2017–18 tax year onwards. This limits the utility of the COM100 data for employees after this point, as we only observe employer contributions for a selected subsample of employees saving in relief-at-source schemes initially, and then for no employees at all from 2019–20 onwards. However, for self-employed workers, the lack of information on employer pension contributions is immaterial, as they have no employer. For this reason, we have only linked the COM100 data to PAYE up to and including the 2016–17 tax year, whereas we undertake the link through to 2020–21 for the SA data (which are data from tax returns for self-employed workers).

The key variables we make use of in the COM100 dataset are the total individual and employer contributions made to the pension pot in the tax year. As noted above, pension providers no longer have to report the employer contribution from 2017–18 onwards and there are no data at all on employer pension contributions from 2019–20 onwards. Importantly, the data also contain two variables indicating the individual who made the contributions that can be used to link COM100 to other datasets – pseudonymised National Insurance number and unique taxpayer reference number.

The first dataset that we link COM100 to is PAYE data held by HMRC. Tax records held within this system provide information on the salaries and pension incomes of all employees and pension recipients whose incomes are sufficiently high to incur an income tax or National Insurance liability. We link COM100 to P14 data, which contain a limited number of variables for the universe of PAYE tax records, between 2008–09 and 2013–14. From 2014–15 to 2016–17, we link to Real Time Information (RTI) data, which contain a larger number of variables for the universe of PAYE tax records.

Individuals with incomes from sources other than employment and pension withdrawals (which fall outside of the scope of PAYE) are required to submit an annual Self Assessment tax return. The COM100 data are linked to these SA records through the use of the HMRC valid view version B datasets supplemented with HMRC SA302 datasets. This linkage gives us information on income from unincorporated self-employment (as well as information on other types of non-employment income and tax liabilities).

These linked datasets contain the data on relief-at-source pension contributions and earnings in the UK for the universe of both employees and the self-employed, and can be used to follow individuals over time. The data on pension contributions are third-party-reported by pension providers, increasing their reliability relative to self-reported pension saving information. In addition, the large sample sizes in these datasets can allow researchers to analyse more specific groups with a much higher level of precision than in typical survey datasets. The research in this report could only be reasonably performed using these datasets, as it necessitates high-quality information on pension saving for both employees and the self-employed, as well as a large sample size to observe a sufficient number of moves into self-employment.

The data used in these datasets are currently available to approved projects and researchers through the HMRC Datalab. Processing code to link them can be provided by the authors upon request. At the time of publication, we are working with the Office for National Statistics (ONS), ADR UK and HMRC to facilitate linkage and access to these linked data in the ONS’s Secure Research Service.

References

Almond, R., Phillips, J. and Sandbrook, W., 2022. Exploring practical ways to support self-employed people to save for retirement. Nest Insight, https://www.nestinsight.org.uk/wp-content/uploads/2022/11/Exploring-practical-ways-to-support-self-employed-people-to-save-for-retirement.pdf.

Blakstad, M., Stockdale, E. and Rodohan, J., 2025. Simplifying retirement saving for self-employed people. Nest Insight, https://www.nestinsight.org.uk/wp-content/uploads/2025/06/Simplifying-retirement-savings-for-self-employed-people.pdf.

Cribb, J., Emmerson, C., Johnson, P., Karjalainen, H. and O’Brien, L., 2025. The Pensions Review: final recommendations. IFS Report, https://ifs.org.uk/publications/pensions-review-final-recommendations.

Cribb, J. and Karjalainen, H., 2023. Understanding pension saving among the self-employed. IFS Report, https://ifs.org.uk/publications/understanding-pension-saving-among-self-employed.

Cribb, J., Miller, H. and Pope, T., 2019. Who are business owners and what are they doing? IFS Report, https://ifs.org.uk/publications/who-are-business-owners-and-what-are-they-doing.

Cribb, J. and Xu, X., 2020. Going solo: how starting solo self-employment affects incomes and well-being. IFS Working Paper 20/23, https://ifs.org.uk/publications/going-solo-how-starting-solo-self-employment-affects-incomes-and-well-being.

Department for Work and Pensions, 2025a. Family Resources Survey: financial year 2022 to 2023. https://www.gov.uk/government/statistics/family-resources-survey-financial-year-2022-to-2023.

Department for Work and Pensions, 2025b. Finishing the job: launching the Pensions Commission. https://www.gov.uk/government/publications/finishing-the-job-launching-the-pensions-commission/finishing-the-job-launching-the-pensions-commission.

Financial Conduct Authority, 2025. Financial Lives 2024 survey: pensions – selected findings. https://www.fca.org.uk/publication/financial-lives/fls-2024-pensions.pdf.

House of Commons Work and Pensions Committee, 2022. Protecting pension savers – five years on from the pension freedoms: saving for later life. Third Report of Session 2022–22, https://committees.parliament.uk/publications/30122/documents/174267/default/.

Karjalainen, H., 2023. Trends in pension saving among the long-term self-employed. IFS Report, https://ifs.org.uk/publications/trends-pension-saving-among-long-term-self-employed.

Acknowledgements

The authors would like to thank Isaac Delestre for assistance with the analysis and Helen Miller for assistance throughout this grant. This work was supported by ADR UK (Administrative Data Research UK), an Economic and Social Research Council (ESRC) investment (part of UK Research and Innovation) (grant number ES/X000362/1). The authors gratefully acknowledge the support of the ESRC Centre for the Microeconomic Analysis of Public Policy (ES/Z504634/1). This work contains statistical data from HM Revenue and Customs (HMRC) which are Crown Copyright. The research datasets used may not exactly reproduce HMRC aggregates. The use of HMRC statistical data in this work does not imply the endorsement of HMRC in relation to the interpretation or analysis of the information.

Endnotes

Authors

Jonathan Cribb

Jonathan joined IFS in 2011. His research areas includes: pensions, ageing and demographic change, public sector pay, housing, and inequalities.

Laurence O'Brien

Laurence is in the Retirement, Savings and Ageing sector. His work focuses on people’s savings decisions and on economic activity in later life.

More from IFS

Understand this issue

Policy analysis

Academic research