Downloads

Download chapter

PDF | 595.64 KB

The falling rate of homeownership among young adults has become an increasingly high-profile political issue. It has also created a clear economic difference between the older and younger generations. There is consensus across the political spectrum that it is too difficult for young adults to get on the property ladder, and both the current and previous governments have introduced a range of policies intended to slow or reverse the decline in young people’s homeownership.

This chapter investigates the key trends in the housing market that young adults face, and the barriers that they create for young prospective homeowners. In particular, using data on the incomes of young adults and the range of property prices in the areas in which they live, we examine the impact of deposit requirements and the cap on mortgage borrowing as a share of income. We show that, since the mid 1990s, it has become harder to save for a deposit and to borrow enough to cover the remaining property price, but the effects differ a lot between regions. We also analyse some of the policy options open to the government, in terms of their potential effects not only on young adults’ homeownership but also on the housing market as a whole.

Key findings

- The last 20 years have seen a substantial fall in homeownership among young adults. In 2017, 35% of 25- to 34-year-olds were homeowners, down from 55% in 1997. The biggest falls have been among middle-income young adults. In terms of housing tenure, they now look much more like the poorest groups than their richer peers.

- Since 1997, the average property price in England has risen by 173% after adjusting for inflation, and by 253% in London. This compares with increases in real incomes of 25- to 34-year-olds of only 19% and in (real) rents of 38%. In most of the country, real house prices have not risen in the last decade; however, they have increased by 30% in London, 8% in the South East and 10% in the East of England since 2007. Rising house prices have benefited older generations at the expense of younger ones and increased intragenerational inequalities.

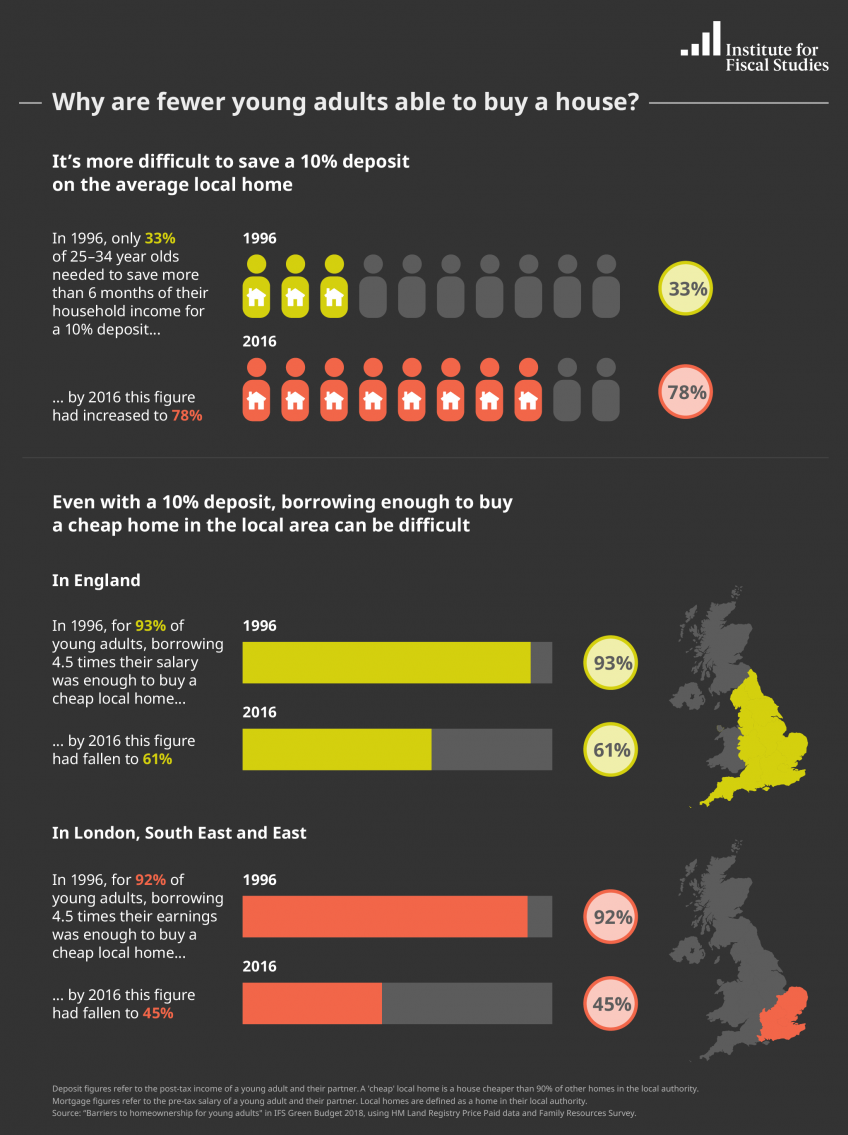

- Increases in property prices relative to incomes have made it increasingly hard for young adults to raise a deposit. The proportion of young adults who would need to spend more than six months’ income on a 10% deposit for the median property in their area has increased from 33% to 78% in the last 20 years. Most of this increase occurred between 1996 and 2006. Over the last decade, stable or falling house prices outside London, the South East and the East of England have meant that raising a deposit has become slightly easier in most of the UK.

- Even with a 10% deposit, many young adults are severely restricted in their ability to purchase a home. Most mortgage lenders will not lend more than 4.5 times salary. In 1996, for almost all (93%) young adults, borrowing 4.5 times their salary would have been enough to cover the cost of one of the cheapest properties in their area assuming they had a 10% deposit. By 2016, this figure had fallen to three-in-five (61%) across England as a whole and around one-in-three (35%) in London.

- Rates of homeownership amongst young adults could potentially be increased by recent policies to advantage young buyers over others (in particular over multiple-property owners) – for example, by reducing stamp duty for the former and increasing it for the latter. But these policies risk increasing house prices or rents or both.

- Increasing the supply of homes and the responsiveness (or elasticity) of supply to prices is crucial. Planning restrictions make it hard for individuals and developers to build houses in response to demand. Easing these restrictions would reduce (or at least moderate) both property prices and rents, boosting homeownership and benefiting renters who may never own. Without greater elasticity of supply, policies to advantage young adults in the housing market will in part push up house prices and will not help (and could even harm) those young adults who will never own a home.

This is a pre-released chapter from the IFS Green Budget that will be published on October 16th. The Green Budget is being produced in association with the ICAEW and Citi and is funded by the Nuffield Foundation.

Authors

Jonathan Cribb

Jonathan joined IFS in 2011. His research areas includes: pensions, ageing and demographic change, public sector pay, housing, and inequalities.

More from IFS

Understand this issue

Policy analysis

Academic research