Downloads

wp201605.pdf

PDF | 2.02 MB

The Smith Commission Agreement, published on 27 November 2014, set out proposals for substantial fiscal devolution to the Scottish Parliament. The Scotland Bill – due to receive Royal Assent shortly – will enshrine these powers in law.

Both the Smith Commission Agreement and the UK Government’s subsequent Command Paper, ‘An Enduring Settlement’ recognised that the devolution of fiscal powers has to be accompanied by the development of a new Fiscal Framework for Scotland.

Without such a framework there could be no fiscal devolution. It is essential in order to set out rules such as: how the Scottish Government’s block grant will be calculated in light of its new fiscal powers; what level of borrowing powers Scotland will have to enable it to deal with the additional economic risks and revenue volatility that it will face; the extent and scope of fiscal rules governing Scottish Government deficits and debt; arrangements for independent fiscal scrutiny, including fiscal forecasting; and arrangements for governing the increasingly complex interactions between Scottish and UK fiscal policy, including dispute resolution.

The Fiscal Framework is not part of the Scotland Bill: it is instead an agreement between the UK and Scottish governments (and therefore does not have the same legal standing as the Bill). It was finally published on 25 February 2016 after many months of negotiations between the two governments. The process of reaching agreement was protracted, and there were a number of contentious areas. But it seems the most significant area of disagreement was how the Scottish Government’s block grant should be adjusted to reflect its new powers.

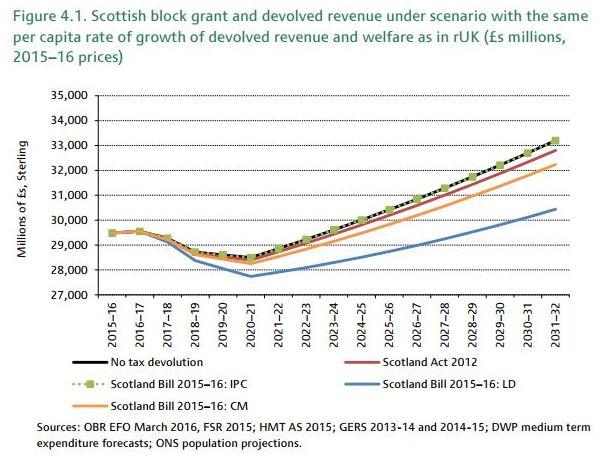

The Smith Commission Agreement established that Scotland’s underlying block grant funding would continue to be determined by the Barnett Formula. But the Barnett-determined block grant would then have to be adjusted to reflect the new powers. On the one hand, the grant would have to be reduced to reflect the transfer of tax revenues from the UK to the Scottish Government, while on the other, an addition would need to be made to reflect the transfer of new welfare spending responsibilities to the Scottish Government.

The Smith Commission Agreement also established a number of high-level principles which it felt the Fiscal Framework should adhere to, and which were expected to govern the development of a proposal to adjust Scotland’s block grant. But, as we showed in our previous report, it is not possible to design a method for adjusting Scotland’s block grant that meets all of the Smith Commission principles simultaneously.

This inconsistency between the Smith principles was the main cause of the protracted negotiations between the two governments, and for several months it seemed likely to undermine the progress of the Scotland Bill. Each government interpreted the principles somewhat differently and chose to prioritise them differently, with the result that each favoured an alternative approach to adjusting Scotland’s block grant. Compromise was finally reached in February 2016, with an agreement on how to adjust the block grant for the next five years. While the mechanism chosen is complex and seems to blend elements of the UK and Scottish governments’ preferred approaches, ultimately it is the Scottish government’s approach that will determine the block grant available to Scotland during this period. After five years, an independent assessment will be carried out and negotiations will take place on how to adjust the block grant in the years beyond 2022.

This report reviews and appraises the Fiscal Framework Agreement, with a particular focus on this issue of block grant adjustment.

The work was carried out jointly with authors at the ESRC Centre on Constitutional Change is the hub for research of the UK’s changing constitutional relationships. Its fellows examine how the evolving relationships between governments and parliaments in London, Edinburgh, Cardiff, Belfast and Brussels impact on the polity, economy and society of the UK and its component nations.

Authors

David Phillips

David is Head of Devolved and Local Government Finance. He also works on tax in developing countries as part of our TaxDev centre.

David Bell

David Eiser

More from IFS

Understand this issue

Policy analysis

Academic research