Downloads

4-Rewriting-the-fiscal-rules-.pdf

PDF | 740.03 KB

The Chancellor was right to suspend the current set of fiscal targets during the pandemic, and he is also right to take time to consider what a good set of post-pandemic targets will be. With UK Chancellors having announced eleven fiscal targets in the last seven years – most of which were (or would have been) missed, there is no point in rushing to implement another set of poorly designed targets. There appears to be a reasonable amount of consensus across several Chancellors and Shadow Chancellors in many aspects their chosen fiscal targets. Specifically, several – Mr Brown, Mr Osborne prior to 2014, Mr McDonnell, Mr Javid, Mr Sunak and Ms Reeves – have set rules with the desire to raise sufficient revenues to pay for spending that is of benefit now, while being content to borrow to finance spending that delivers future benefits. Such a target is far from perfect, but it does have many desirable features and a version of it has been recommended in successive IFS Green Budgets.

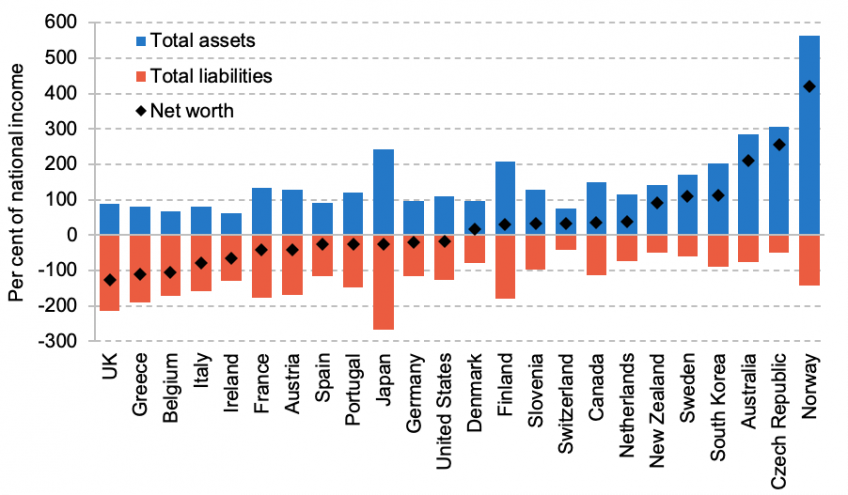

Far harder is setting an appropriate target for debt. While a near-term target for debt risks being too inflexible, there are good reasons to set fiscal policy so that debt will decline as a share of national income over the longer term. Achieving this could help keep future debt interest payments down and could create ‘fiscal space’ so that, if appropriate, debt can be increased again when the next severe adverse shock strikes. However, a narrow focus on debt risks losing sight of the asset side of the public sector balance sheet: when the IMF calculated a measure of net worth – netting total government assets (including both financial and physical assets) and liabilities – the UK was found to have the lowest of twenty-four advanced economies, as shown in the Figure below. It will therefore be important for policymakers not to be tempted to respond to a debt target by selling public sector assets, or not acquiring them even when they would be better managed in the public sector, leading to a further deterioration of net worth.

Figure 1. Government net worth for selected advanced economies

Source: Chart 4.17 of Office for Budget Responsibility (2021) using data from the IMF.

Key findings

- In principle, well-designed fiscal rules could make it easier for governments to borrow for good reasons while making it hard to borrow for bad reasons. Borrowing during periods of temporary weakness or to finance spending that delivers future benefits can be appropriate, but simply borrowing in order to defer announcing or implementing measures that involve difficult trade-offs is not.

- Successive Chancellors have been too quick to announce poorly designed fiscal targets: in total, 11 have been announced in the last seven years, with most of them being missed before being dropped. The Chancellor was right to suspend and review the government’s fiscal targets – and to allow borrowing to rise sharply – when the pandemic hit. The manifesto commitment to reduce debt over this parliament was always badly conceived and Rishi Sunak is right not to attempt to meet it.

- Indications are that both the Conservative Government and the Labour Opposition remain in favour of setting policy so that a current budget balance (or better) is forecast for the medium term. This has much to commend it: it allows borrowing for investment purposes and gives some time for policy to adjust to shocks. But the split between capital and current spending will not always align with what spending does and does not benefit future generations. There is also a judgement to be made about the timescale over which a forecast current budget balance should be aimed for: too short and it could necessitate inappropriately sharp adjustments to policy; too long and governments may have more scope to promise future tax rises or spending cuts that they do not intend – or are perhaps unable – to implement.

- The combined legacy of the COVID-19 pandemic and the global financial crisis (GFC) has been to elevate debt to levels not seen in recent UK history. Debt interest payments are, however, lower than prior to the GFC as interest rates have fallen sharply. Indeed, they are lower as a share of revenue than at any time since 1700. This does not mean additional debt has been costless: the public finances are now much more exposed to increases in interest rates. This has been exacerbated by the fact that the increase in debt since the start of the pandemic has been effectively financed by increased deposits of commercial banks at the Bank of England. There remains a strong case for gilt issuance to be tilted more towards long-dated index-linked gilts in order to lock in the current low real cost of more debt.

- There is a case for setting policy so that over the long term, debt is reduced as a share of national income. This could help reduce future debt interest spending and could create ‘fiscal space’ so that debt could be increased again when the next severe adverse shock strikes. Reducing debt from its newly elevated level will be made harder by known pressures facing the public finances. The Office for Budget Responsibility estimates that the rising costs of healthcare, adult social care and state pensions will total 6.1% of national income by 2050–51, while costs associated with the transition to net zero are estimated to peak much sooner, in 2026–27, at 2.2% of national income.

- The International Monetary Fund estimates that UK general government net worth is the lowest of 24 advanced economies. A clear risk with a narrow focus on debt is that public sector assets are inappropriately sold – or are not acquired – to help keep headline debt down. Whatever its merits, measurement challenges mean that a formal target for public sector net worth may not be sensible. While there are advantages to reducing debt over the longer term, both the Treasury and the Labour Opposition should retain their welcome focus on the broader public sector balance sheet.

- A clear lesson from the last 25 years is that, rather than having firm and fixed fiscal rules, it would be better for these to be considered rough rules of thumb that Chancellors should strive to keep to in most periods. This should be communicated from the outset. We should not pretend that any fiscal target, however carefully designed, will be sacrosanct for evermore.

Authors

Isabel Stockton

Isabel works in the Healthcare sector, and on the public finances. Their research focuses on retaining and developing the NHS workforce.

More from IFS

Understand this issue

Policy analysis

Academic research