Downloads

R181-retirement-saving-of-the-self-employed.pdf

PDF | 686.24 KB

The proportion of self-employed workers contributing to a private pension has been steadily declining since the 1990s. This is in contrast to private-sector employees, for whom the rate of pension participation has dramatically increased as a result of automatic enrolment. Furthermore, even before the introduction of automatic enrolment, the rate of decline in pension participation was faster among the self-employed than private-sector employees.

In this report, we seek to explain this decline in pension saving amongst the self-employed. We examine the extent to which the decline has been driven by the changing characteristics of the self-employed population. We then explore changing attitudes towards pension saving, and changes in other forms of saving that might represent alternative ways of saving for retirement (and therefore provide an explanation for the patterns in pension saving).

Key findings

- In 1998, 48% of the self-employed contributed to a private pension, and by 2018 this had declined to just 16%. The proportion of private-sector employees contributing to a pension fell more gradually over this period and, since 2012, has increased sharply due to automatic enrolment. As a result, while, in 1998, pension participation among private-sector employees was on average around the same level as for the self-employed, by 2018 private-sector employees were approximately four times more likely to be contributing.

- This decline in pension participation of the self-employed has taken place at the same time as the population of workers who are self-employed has grown. The number of self-employed workers rose from 3.4 million (12.9% of the workforce) in 1998 to 4.8 million (15.1% of the workforce) in 2017.

- The characteristics of the self-employed have been changing over time. The proportion of self-employed who are female increased from 27% to 32% between 1997–98 and 2018–19, their average age increased from 43.7 to 45.3 years and the proportion working part-time increased from 18% to 24%. Average earnings increased in real terms until the start of the 2000s, but were then flat for some years before falling sharply during the financial crisis. By 2018–19, average earnings among the self-employed were still lagging behind the level they were in 1997–98: a remarkable two decades of lost income growth among this group.

- Self-employed people who are older, have higher earnings, higher levels of education and have been self-employed for longer have historically been more likely to contribute to a private pension. Given such associations between pension membership and individuals’ characteristics, a change in the average characteristics of the self-employed over time may be expected to be an important driver of changed rates of pension coverage.

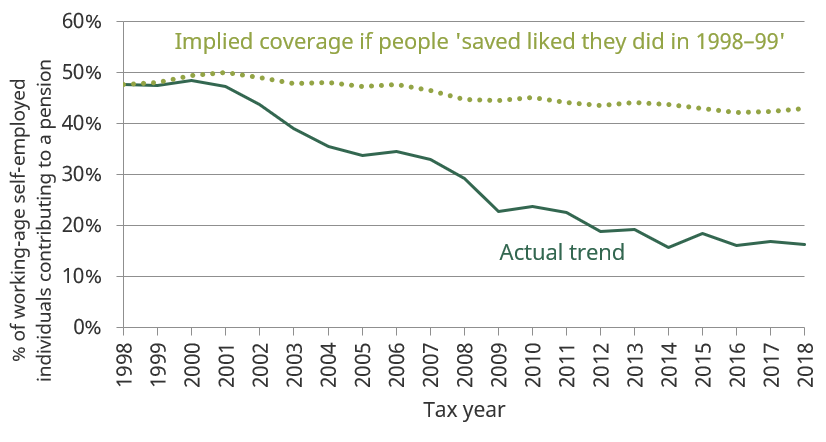

- We find that at most one-seventh of the decline in pension participation among the self-employed could be attributed to these changing characteristics of the self-employed. If the relationship between individual characteristics and pension saving stayed as it was in 1998–99, then the changing characteristics of self-employed workers over the subsequent years would be expected to lead to a fall in pension saving of 5 percentage points – compared with an actual decline of 31 percentage points, as shown in Figure E.1.

Figure E.1. Role of changing composition

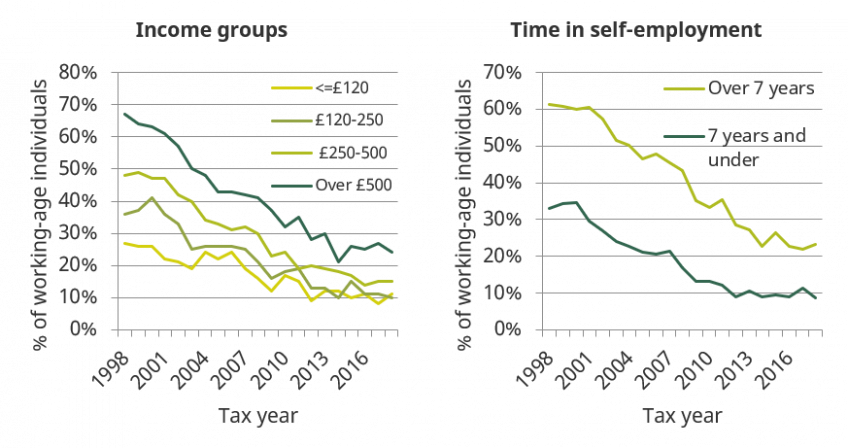

- Pension participation has fallen more dramatically among those groups who had higher proportions saving in 1998–99, such as those who had been in self-employment for a long time or those with higher levels of income. Nearly 70% of the self-employed who were earning over £500 per week were saving in a pension in 1998–99; by 2018–19, this was just 24%. Over 60% of those who had been self-employed for more than seven years were saving in a pension in 1998–99; by 2018–19, this was 23%. (Both are illustrated in Figure E.2.)

- As a result, the individual characteristics (that we can observe) have a much less strong association with pension saving by 2018–19 than in 1998–99. For example, in 1998–99, self-employed men were 21 percentage points more likely to save in a pension compared with women, but by 2018–19 they were only 4 percentage points more likely. In 1998–99, those earning over £500 per week were 40 percentage points more likely to be saving than someone earning £120 per week or less, but by 2018–19 they were only 13 percentage points more likely. In 1998–99, those who had been self-employed for more than seven years were 28 percentage points more likely to save in a pension than those who had been self-employed for seven years or fewer, but by 2018–19 they were only 14 percentage points more likely.

- In fact, the decline in the association between individuals’ observable characteristics and their probability of saving in a pension is such that changes in the composition of the self-employed population would no longer be expected to result in noticeable changes in pension membership rates. One could therefore attribute all of the decline in pension saving over the last two decades to the decline in pension saving conditional on individuals’ characteristics, and none to the changing composition of the self-employed population.

Figure E.2. Pension participation among different groups of the self-employed

- Attitudes towards pensions among the self-employed do not appear to have changed over the past decade in a way that could explain the decline in pension saving. Affordability remains the main reason most give for not saving in a pension. Most self-employed believe that saving in property is safer and gives a higher return than pension saving, but this has been the case throughout the period.

- A declining proportion of the self-employed expect to get private pension income in retirement. This is in some sense reassuring, in that on average the self-employed are at least aware of the consequences of not saving in a pension during working life for their sources of income in retirement.

- The proportion of the self-employed saving in other forms, such as savings accounts, individual savings accounts (ISAs) and shares, has also been declining over the past two decades. The likelihood of saving, and changes in this over time, are similar between employees and the self-employed.

- It therefore does not appear that these financial assets are acting as a substitute for pension saving among the self-employed. Overall, the proportion of individuals saving in either a pension, savings account, ISA or shares has been declining over the past 20 years, and more rapidly for the self-employed than for employees (shown in Figure E.3).

Figure E.3. Prevalence of non-housing saving

- The average wealth held in primary housing has increased dramatically over the last two decades as a result of rising house prices (while rates of owner occupation have fallen). Primary housing is therefore taking up an increasing proportion of the resources of the self-employed, which for some may crowd out pension saving. However, the trends over time in owner occupation and average housing wealth are similar for employees and the self-employed, so it is not obvious that this would explain the faster decline in pension saving among the self-employed.

- Without fully understanding the drivers of the decline in pension saving among the self-employed, it is difficult to be precise about the extent to which policymakers should be concerned by these trends. However, given that pension coverage has declined most rapidly among high-income and long-tenure self-employed, and that other saving outside of primary housing has not increased over this period, this does appear to be an issue that deserves policy attention.

Authors

Heidi Karjalainen

Heidi is a Senior Research Economist in the Retirement, Saving & Ageing sector. Her current research is on pensions and saving for retirement.

More from IFS

Understand this issue

Policy analysis

Academic research