In 2013, the UK government introduced two so-called ‘Help to Buy’ schemes, aimed at boosting the affordability of homeownership: an equity loan scheme for new-build purchases and a mortgage guarantee scheme for lenders. The mortgage guarantee scheme ended in 2016, but was reintroduced (initially on a temporary basis) in 2021 and has since been made permanent. The equity loan scheme ended in 2023, but industry bodies have been calling for its reintroduction (and there are rumours that the government is strongly considering this).

In new IFS research, we estimate how, and for whom, these schemes affected housing affordability among those who did not previously own their home. We define ‘affordability’ as the possibilities individuals have when it comes to buying a home. We measure this in two ways: (i) the highest-value home an individual who did not own their home before the schemes would be able to purchase based on their reported income and an estimate of the largest deposit they could afford and (ii) the share of properties sold in the local authority that an individual lives in that are sold for prices below this maximum value.

We focus on how these criteria were affected for different individuals by the introduction of the schemes in 2013, but they could be used more broadly as a measure of affordability, complementing or replacing classic affordability measures such as house price to income ratios (which do not capture other features of people’s circumstances, such as parental transfers received – increasingly important determinants of homeownership – or changes to borrowing constraints). We find that affordability gains from the schemes were concentrated among higher-income individuals, and that the mortgage guarantee scheme had limited effect on affordability for most non-homeowners.

Help to Buy policies

Demand-side housing policy schemes are one way that governments can boost the affordability of homeownership for those struggling to afford a deposit and/or with insufficient income relative to the size of the loan they would like. The Help to Buy schemes introduced in the UK in 2013 had the dual aims of increasing homeownership and stimulating housebuilding. Similar schemes have since been introduced in other countries.

Under the equity loan scheme, the government provided equity loans for new-build house purchases of up to 20% of a house’s purchase price. This scheme made almost 390,000 loans with a total value of £25 billion in its 10 years of operation. Under the mortgage guarantee scheme, the government offered lenders a guarantee covering some of their losses in the event of mortgage default on loans with loan-to-value (LTV) ratios between 80% and 95%. Around 105,000 mortgages were supported by this scheme between 2013 and 2017, with a total value of £15.8 billion. Both schemes applied to first-time buyers and existing homeowners, with a property price cap of £600,000. In 2014–15, when both schemes were well under way, they supported around a fifth of first-time buyer purchases in England.

The mortgage guarantee scheme relaxed the LTV constraint on mortgage borrowing, under which the deposit must make up a certain fraction of the total house price, loosening the effective deposit requirement from around 10% to 5%. The equity loan scheme also relaxed the LTV constraint (as buyers using the scheme only had to put down a cash deposit of 5%) but also relaxed loan-to-income (LTI) constraints, which typically restrict households from borrowing more than 4.5 times their incomes, since the government-provided 20% loan reduced the maximum required mortgage to 75% of the house price.

Estimating the impacts of Help to Buy on housing affordability among non-homeowners

The effect of the Help to Buy schemes on overall housing affordability will depend on their effect on the supply of houses for sale. By subsidising new-build purchases (and hence raising the prices developers are able to charge for them), the equity loan scheme should in principle have boosted housing supply. Other things equal, this would be expected to lower general house prices and rents, although in practice this effect was limited by restrictions on new building which cover much of England. In addition, by targeting specific groups, the schemes also had an important distributional effect – making homeownership more affordable for some (those currently unable to afford the deposit to buy a house they would like, or with insufficiently high income – often first-time buyers) at the expense of others competing to buy homes in the same market who we would expect to face higher prices.

Past work assessing Help to Buy has looked at the types of individuals who used the schemes to evaluate who benefits. But this is not the same as assessing how the schemes actually affected affordability for different groups. Users of the schemes might not have seen any changes in the houses they could potentially afford, but still used the schemes to avoid having to save as much for a deposit or to rely less on family assistance. Others might have seen big changes in the share of homes they could afford, but still opted not to use the schemes.

We take a novel approach by using the two measures of affordability set out above. We focus on the impact of the Help to Buy schemes on the affordability of homeownershipfor those who did not own homes before the scheme came into effect (potential first-time buyers). We assume no effect of Help to Buy on local house prices. If we included price effects, we would expect them to undermine overall affordability gains, potentially more so in housing markets where supply is more constrained.

The effects of these schemes on these definitions of affordability of local homes for different non-homeowners are clearly somewhat nuanced. They depend on the maximum deposit individuals can afford to put down, their incomes (which determine whether loan-to-income constraints or loan-to-value constraints restrict what they can afford), local house prices and the share of local properties that are new-builds.

We use data from Understanding Society, a nationally representative panel household survey covering the United Kingdom. We focus on 22- to 44-year-old non-homeowners living in England between 2009–10 and 2012–13 (just before the Help to Buy policies were introduced). Our approach comprises three steps. In our first step, for each individual, we estimate the maximum deposit that they could plausibly be expected to raise, based on the deposits of similar individuals who had recently moved into homeownership. We model these largest affordable deposits based on a given set of characteristics: age, sex, region, education, household composition, and parents’ occupation and education. We adjust these to account for the fact that those moving into homeownership are likely to be a selected group (e.g. they are likely to have more wealth than observationally similar individuals who do not buy a house), to avoid overstating the deposits that otherwise-similar non-homeowners could plausibly raise. We also account for unobservable differences in deposits individuals can put down by simulating many draws of potential deposits for each individual and averaging impacts across these draws.

In our second step, we translate this deposit into a maximum affordable price given an individual’s income (in addition to the income of their partner, if they have one) and under pre- and post-Help-to-Buy borrowing constraints.

In our third step, we use this maximum affordable price to calculate the share of local properties affordable to them before and after Help to Buy, taking house prices and characteristics as fixed.

The role of income is clearly important in these final two steps. Two constraints limit how much someone can borrow to buy a home: an income limit, under which a mortgage cannot exceed 4.5 times income, and a deposit limit, under which the deposit must cover a minimum share of the house price. For any given individual, one of these will be the binding constraint, which prevents them from being able to afford a more expensive house.

Consider, for example, the decision to buy a £200,000 home. The mortgage guarantee scheme would in theory mean the minimum deposit falls from 10% of the house value, or £20,000, to 5%, or £10,000. But putting down only £10,000 means a £190,000 mortgage must be taken out: if lenders refuse to lend more than 4.5 times income, this house would still be unaffordable to individuals with incomes less than £42,200. An individual with an income of £30,000, for example, would only be able to obtain a maximum loan of £135,000.

Overall findings

We find that most non-homeowners in the early 2010s were constrained by income-related limits on the maximum house price affordable, rather than deposit-related limits. That is, the maximum house price they could afford was determined by their income rather than by their deposit. Reducing the amount that income-constrained individuals must put down as a deposit is not helpful in increasing what they can afford, as it does not allow them to borrow more than they otherwise could. This is the situation of our illustrative individual on a £30,000 income with a £10,000 potential deposit in the section above – the most expensive home they can buy is still £145,000 even with the mortgage guarantee, since they can only borrow up to £135,000 based on income-related lending limits. This is below the £200,000 that the deposit of £10,000 via the mortgage guarantee scheme would have supported.

This finding is in contrast with results from past work on housing affordability, which used observed savings and income to argue that raising a deposit is the main constraint to home purchase. Our exercise is different – rather than using self-reported savings at a point in time, we estimate what deposit an individual could plausibly raise, looking at deposits we see being put down by those similar to them in terms of age, parental characteristics, location etc. We thus account for additional savings households can make in the months before a house purchase, and for parental transfers received at the time of a house purchase (which previous work finds to be both common and substantial). Because our estimated deposits tend to be larger than observed savings at a point in time, we find that the income constraint binds more often than previous work suggests.

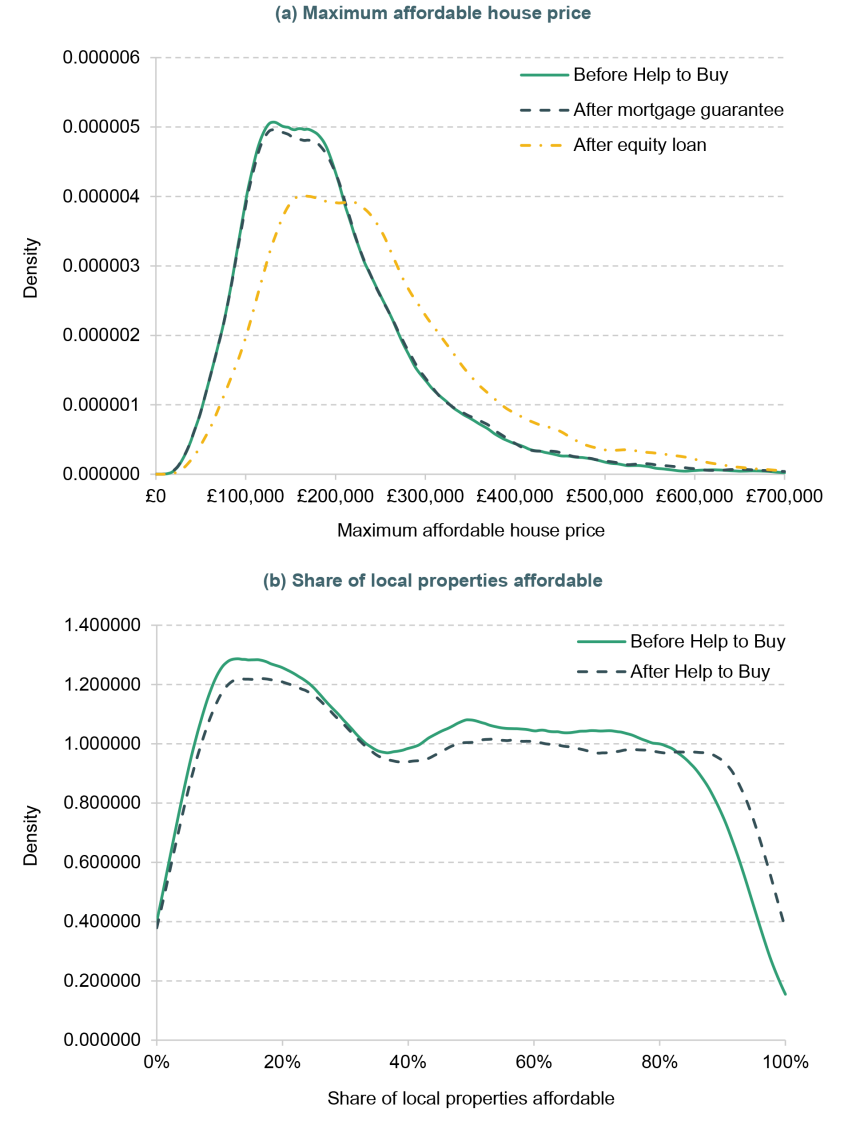

Because income constraints mattered more than deposit constraints in the early 2010s, we find that the mortgage guarantee scheme – which only relaxed the deposit constraint – had limited effects on affordability. We see this in panel a of Figure 1, which shows that the maximum affordable house price hardly changed in response to the mortgage guarantee scheme changes. The equity loan scheme was more important for almost all households. However, since this scheme was limited to new-build properties, it was muted in effect by a low share of available properties. Panel b of Figure 1 shows that the schemes increased the share of local properties affordable, shifting the distribution to the right, but that these effects were not very large.

Figure 1. Distribution of (a) maximum affordable house price and (b) share of local properties affordable, before and after Help to Buy, 2011–12

Note: See Boileau, Conwell and Levell (2026) for more details.

Source: Authors’ calculations using Understanding Society.

Inequality in affordability gains

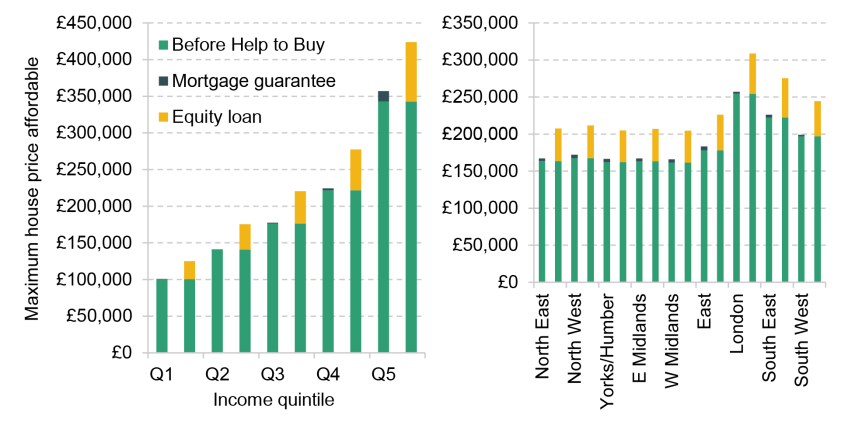

Our use of detailed survey data allows us to break down our estimated affordability levels and gains by non-homeowners’ characteristics. Figure 2 shows that the mortgage guarantee scheme only really made a difference to the maximum house price affordable among those with the highest incomes. This is a function of more of this group being deposit, rather than income, constrained.

Figure 2. Maximum house price affordable before and after Help to Buy, by income quintile and region, 2011–12

Note: See Boileau, Conwell and Levell (2026) for more details.

Source: Authors’ calculations using Understanding Society.

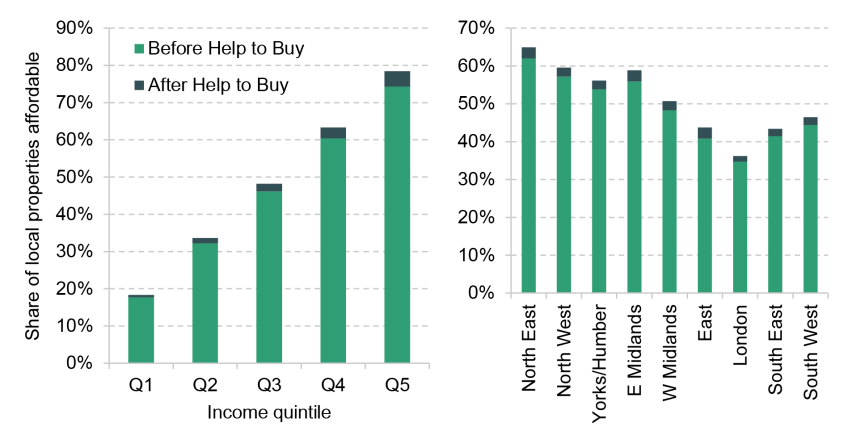

The figure also shows that the equity loan scheme increased maximum affordable prices most among those who could already afford higher prices – those living in London and the South East, and those with the highest incomes. Figure 3 shows how the share of local properties affordable to different groups changed under the schemes. Higher-income individuals saw the largest increases in the share of properties affordable under Help to Buy schemes, as well as the largest increases in the maximum prices affordable. But the patterns are reversed for regional splits: those living in London and the South East saw smaller changes in the share of properties they can afford, even though they saw larger increases in the maximum price affordable, a pattern driven by much higher prices in these areas.

Figure 3. Share of local properties affordable before and after Help to Buy, by income quintile and region, 2011–12

Note: See Boileau, Conwell and Levell (2026) for more details.

Source: Authors’ calculations using Understanding Society.

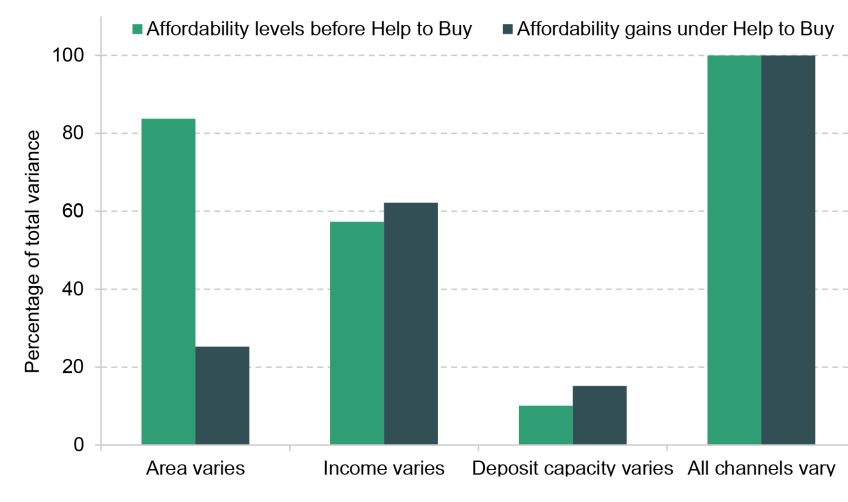

More broadly, our analysis suggests that differences in income and local housing markets matter more for housing affordability than differences in deposit capacity. We can decompose the variation in housing affordability across non-homeowners into three channels: income, local housing characteristics (local prices and the share of new-builds in local areas), and maximum deposit capacity. Figure 4 shows how these three channels each contributed to affordability. The exercise involves, for example, holding income and deposit capacity fixed across people, and allowing only the local housing characteristics they face to change (the first set of bars in the figure) or holding deposit capacity and local housing characteristics fixed and allowing only income to change (the second set of bars). As in the above exercise, we take pre-policy housing and individual characteristics as fixed, not allowing them to change in response to the policy.

Figure 4. Variance decomposition of affordability levels before Help to Buy and affordability gains under Help to Buy, 2011–12

Note: See Boileau, Conwell and Levell (2026) for more details.

Source: Authors’ calculations using Understanding Society.

Figure 4 shows that the distribution of local housing characteristics accounts for most of the variation between individuals in our estimates of pre-policy affordability. This reflects the fact that local price distributions differ substantially across the country, so non-homeowners in higher-price areas had lower shares of local properties affordable even if they had higher deposit capacity. Geography also determined the share of new-builds available, an important factor in translating the equity loan increase in maximum price affordable into genuine shifts in affordability.

Income was the most important factor driving differences in affordability gains from Help to Buy. Higher-income individuals gained most under the relaxation of borrowing constraints. The importance of income in particular comes from our result that most non-homeowners were limited by the loan-to-income, rather than loan-to-value, constraint on borrowing. This is also consistent with evidence showing that those using the Help to Buy schemes tended to have higher-than-average incomes.

Notably, differences in deposit capacity based on individual characteristics accounted for much less of the variation both in pre-policy affordability and in affordability gains from Help to Buy, with geography and own income much more important. These individual characteristics include parental education and occupation, implying that Help to Buy does not seem either to have entrenched inequalities by parental background in housing affordability or to have boosted social mobility.

Conclusion

Policies to help households into homeownership are much discussed – particularly in a context of high house prices relative to incomes, and of relatively low homeownership rates for young people – but their effects are often difficult to predict. Our new research allows the distributional effects of policies relaxing borrowing constraints for home purchase to be better understood. One key caveat is that our analysis takes house characteristics in different markets as given, and so does not account for any effects of the schemes on local house prices or supply.

Our findings suggest that income constraints can be more important than often assumed in the context of housing affordability. Schemes that only reduce the deposit that individuals must put down, without affecting income-based borrowing constraints, may therefore be unlikely to have significant effects on homeownership rates. Equity-loan-type schemes are more likely to have a meaningful effect on affordability for first-time buyers. The benefits of these schemes to first-time buyers must also be set against their potential downsides, however. To the extent that these schemes do not increase the overall supply of homes for sale, their main effect – as set out above – is distributional: they will improve affordability for some people, while potentially increasing prices for others. Both types of scheme also involve the government taking some of the risk on loans that the private sector is unwilling to make.

The gains in terms of housing affordability vary quite significantly across different groups. We find that individual characteristics seem to have been less important than income and geography in determining affordability gains from Help to Buy. The schemes seem neither to have entrenched inequalities in housing affordability based on parental background nor to have boosted social mobility. The affordability gains from the equity loan schemes were concentrated among higher-income individuals. Since these individuals would normally be expected to be able to save for a minimum deposit quite quickly even without Help to Buy, it is likely that these schemes accelerated their first home purchase by a few years rather than making the difference between becoming a homeowner or not in the longer term.

Schemes that offered more generous subsidies to those with lower incomes could help extend the benefits of Help to Buy to the less well-off – but this would involve a difficult trade-off. It could reduce inequalities when getting on the housing ladder, but would also increase the exposure of both the government and potential new borrowers to housing market downturns. This trade-off would clearly need to be navigated with considerable care.

Authors

Bee Boileau

Bee joined the IFS in 2021 as a Research Economist and works in the Retirement, Saving and Ageing sector.

Lucas Conwell

Lucas is a lecturer for the Department of Economics at University College London and a Research Associate at IFS.

Peter Levell

Peter joined in 2009. He has published several papers on the microeconomics of household spending and labour supply decisions over the life-cycle.

More from IFS

Understand this issue

Policy analysis

Academic research