This comment updates our projections of Scotland’s underlying public finances in light of the latest Office for Budget Responsibility forecasts from the March 2024 Budget. These represented the third consecutive downgrade in oil and gas revenue forecasts following large upward revisions in November 2022.

The Office for Budget Responsibility (OBR) published its latest forecasts for the economy and public finances alongside the Budget on 6 March. These showed a modest improvement in the UK’s public finance position in the current financial year (2023–24), but little change in the medium term.

Delving deeper, the latest forecasts saw the third consecutive downgrade to tax revenues from oil and gas production, shown in Table 1. These downgrades follow big increases in revenue forecasts in 2022, also shown in the table, following Russia’s invasion of Ukraine and the subsequent surge in European gas prices. A fallback in prices and expectations of future prices, particularly for gas, explains much of the downgrade from the very high levels of revenues forecast in November 2022.

Table 1. UK oil and gas revenue out-turns and forecasts (£bn), various forecast vintages

| Forecast | Average out-turn 2015–16 to 2020–21 | 2021–22 | 2022–23 | 2023–24 | 2024–25 | 2025–26 | 2026–27 | 2027–28 | 2028–29 |

|---|---|---|---|---|---|---|---|---|---|

| Oct 21 | 0.6 | 1.4 | 2.5 | 1.7 | 1.4 | 1.5 | 1.4 | ||

| Mar 22 | 3.1 | 7.8 | 4.8 | 2.8 | 2.6 | 2.3 | |||

| Nov 22 | 2.6 | 14.9 | 20.7 | 15.4 | 11.3 | 10.2 | 8.0 | ||

| Mar 23 | 2.6 | 11.0 | 10.4 | 9.5 | 7.6 | 6.9 | 5.4 | ||

| Nov 23 | 2.6 | 9.8 | 6.1 | 7.0 | 5.7 | 4.9 | 4.1 | 2.1 | |

| Mar 24 | 2.6 | 9.8 | 5.2 | 3.8 | 3.5 | 3.0 | 2.9 | 2.2 |

Source: Various Office for Budget Responsibility Economic and Fiscal Outlook publications.

Oil and gas revenues averaged just £0.6 billion per year between 2015–16 and 2020–21. In 2022–23 they amounted to £10 billion, and in 2023–24 they are now forecast to amount to £5 billion. Compared with the £0.6 billion raised per year during the late 2010s, these figures represent increases equivalent to 0.4% and 0.2% of national income, respectively, for the UK as a whole.

With most UK oil and gas production taking place in Scottish waters, the impact on the amount of revenue raised in Scotland is much greater: equivalent to increases of over 4% and 2% of Scottish national income, respectively, compared with the late 2010s position.

However, while substantially higher than in the late 2010s, oil and gas revenues in the current financial year, 2023–24, are now forecast to be around one-quarter of the level expected back in November 2022 (£21 billion). This reduction (£16 billion) is equivalent to around 0.6% of UK national income, but around 7% of Scottish national income.

This illustrates how the concentration of oil and gas production in Scottish waters means that Scotland’s overall tax revenues and in turn its public finances are much more exposed to this volatile and uncertain revenue source than the UK as a whole is.

Under current constitutional arrangements, this underlying, notional public finance position does not matter much: like most revenues, oil and gas revenues are pooled with revenues from the rest of the UK, and borrowing to finance Scotland’s underlying fiscal deficit is undertaken by the UK government as part of its borrowing to finance the UK’s fiscal deficit. (The performance of the oil and gas sector does have an influence on overall Scottish economic performance, particularly in the North East and Highlands & Islands regions.) Scotland’s underlying fiscal position would matter much more under full fiscal autonomy or independence though, as the Scottish Government would then be fully responsible for taxation, public spending, and (new) borrowing and debt.

Projecting Scotland’s underlying public finance position

The best source of information on Scotland’s underlying, notional public finances is the Scottish Government’s official Government Expenditure and Revenue Scotland (GERS) publication. While backwards-looking, and based on existing tax and spending policy (of both the UK and devolved Scottish governments) and economic performance, it provides useful information about the potential starting fiscal position for a fiscally autonomous or independent Scotland.

The future evolution of the fiscal position of both Scotland and the UK as a whole is uncertain and will be affected by both economic factors (including, in the case of Scotland in particular, oil and gas prices and production) and policy decisions. Bearing this in mind, we have projected the latest GERS figures (for 2022–23) forward using the OBR’s March 2024 fiscal forecasts for the UK as a whole. In doing so, we have assumed Scotland’s onshore tax revenues and government spending per capita move in line with the OBR’s forecasts for the UK as a whole, and that Scotland’s share of oil and gas revenues trends back to 100% of the UK total by 2027–28 as the contribution of oil and gas production to these revenues moves back closer to levels prior to Russia’s invasion of Ukraine. We have previously explained why we think these assumptions are a reasonable baseline scenario.

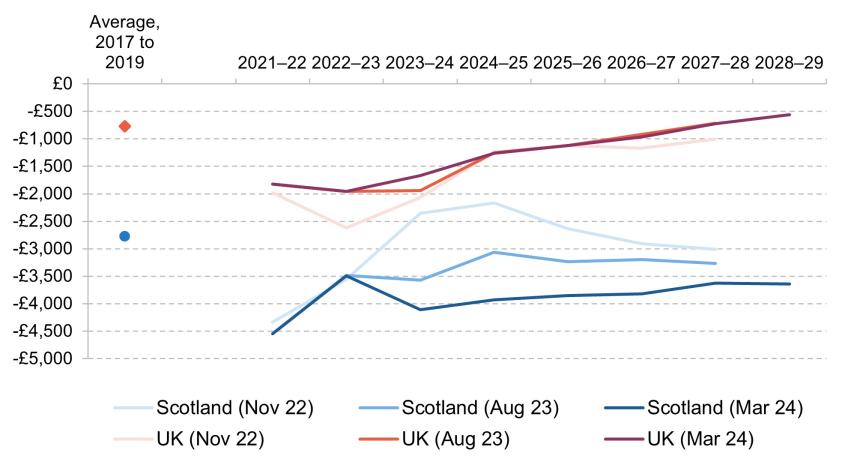

Figure 1 compares the resulting projections for Scotland’s net fiscal balance (in dark blue) with forecasts for the UK as a whole (in dark red). It also shows previous projections, from August 2023 and November 2022, in lighter colours.

Focusing first on the UK, the figure shows that the UK’s net fiscal balance is currently forecast to strengthen (i.e. borrowing reduce) every year, from the equivalent of just under –£2,000 per person in 2022–23 to just under –£560 per person in 2028–29. This reflects a combination of increases in taxation as a share of national income and planned restraint in both day-to-day and investment spending in the next parliament.

If we instead focus on the latest projections for Scotland, the picture is rather different. Based on the OBR’s March oil and gas revenue forecasts, Scotland’s notional net fiscal balance is projected to have deteriorated in the current financial year, and then show little change over the next five fiscal years. This is because while Scotland is also set to see increases in onshore tax revenues and public spending restraint, these are offset by forecast declines in oil and gas revenues.

In the current financial year, 2023–24, Scotland’s net fiscal balance is projected to be around –£4,100 per person (–£23 billion), compared with –£3,500 per person (–£19 billion) in 2022–23. This means an underlying net fiscal deficit in 2023–24 of approximately £2,450 higher per person than the figure for the UK as a whole, up from £1,550 higher per person in 2022–23. This reflects the forecast decline in oil and gas revenues.

Figure 1. Projected Scottish and UK fiscal balances per capita, 2021–22 to 2027–28

Source: Author’s calculations using various Office for Budget Responsibility Economic and Fiscal Outlook publications, GERS 2021–22 and 2022–23, various ONS population estimates and projections, and assumptions discussed in the text.

Comparing the latest projections with our previous projections shows that while forecasts for the UK’s net fiscal position are improved for 2022–23 and 2023–24 compared with previous projections, the opposite is true for Scotland. For example, in November 2022, we projected a net fiscal balance equivalent to approximately –£2,350 per person in Scotland this financial year, just £300 per person more than the figure for the UK as a whole. By August 2023, this had increased to a gap of just over £1,600 per person (–£3,575 versus –£1,940). And, as discussed above, the gap is now projected to be £2,450 per person.

Figures for future years are highly uncertain, particularly for Scotland given the volatility and uncertainty associated with oil and gas revenues. However, based on current OBR forecasts, our baseline projection for Scotland’s net fiscal balance per person in 2028–29 is –£3,640, little changed from 2023–24 levels. In contrast, as highlighted above, the net fiscal balance for the UK as a whole is forecast to strengthen to around –£560 per person. This means Scotland’s underlying fiscal deficit is projected to be around £3,100 per person higher than that of the UK as a whole – which in aggregate terms equates to a difference of around £18 billion.

Concluding remarks

If Scotland’s onshore revenues and spending move in line with the OBR’s forecasts for the UK as a whole, oil and gas revenues would need to amount to around £20 billion per year in 2028–29 for Scotland’s net fiscal balance per person to match the UK’s (assuming 100% of these revenues were from Scottish waters). That would be more than four times more than what they are forecast to raise in the financial year that is about to end. Such an increase is not impossible (in November 2022, revenues were expected to reach this level this year). But it would be the highest real-terms revenues since the mid-1980s, when production of oil, in particular, was substantially higher. A significant and sustained improvement in Scotland’s net fiscal balance relative to that of the UK as a whole is therefore likely to require changes to onshore economic performance and revenues and to public spending.

Authors

David Phillips

David is Head of Devolved and Local Government Finance. He also works on tax in developing countries as part of our TaxDev centre.

More from IFS

Understand this issue

Policy analysis

Academic research