Now is not the time to raise taxes; the economy is still weak and the recovery only just starting. But that time will likely come. Even before the COVID-19 crisis there were pressures for higher UK taxes to deal with the public finance pressures of an aging society. Now there will likely be demands for a larger state that provides more services (for example, more healthcare or a more comprehensive social safety net) and a role for tax in managing down the elevated public debt and any enduring increase in the budget deficit.

There are lots of options for raising revenues

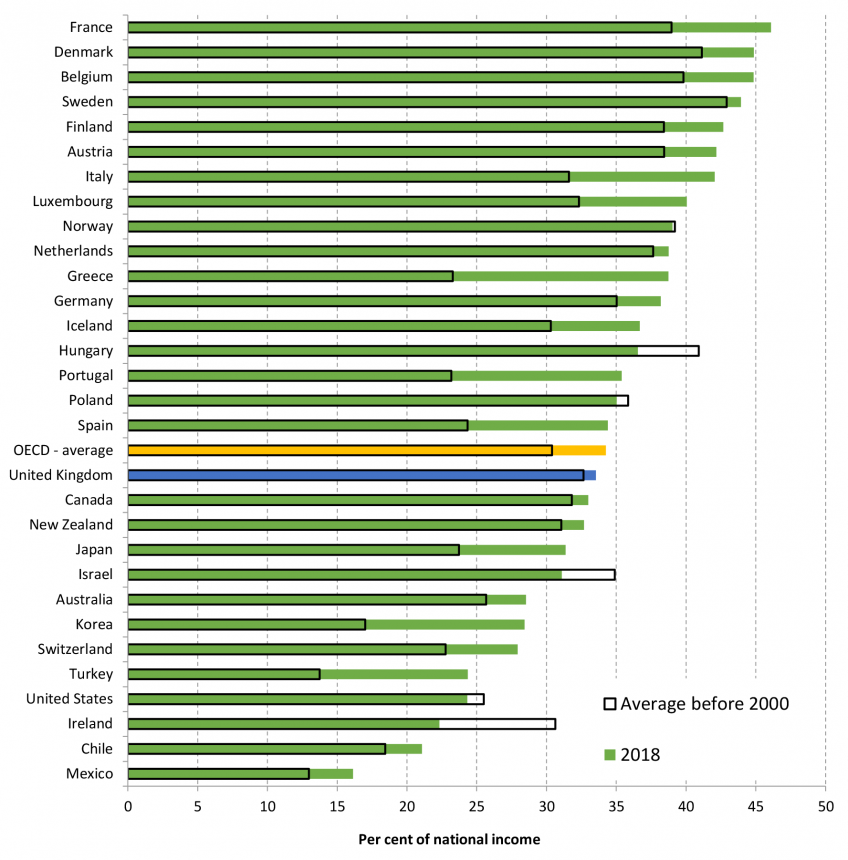

Before COVID-19, the UK was raising 34% of GDP in tax, the highest share since the early 1980s. Many advanced countries have raised their tax takes in recent decades (see Figure 1) and would be entering uncharted territory if they substantially increased the size of their state. But, as evidenced by many countries in Western Europe and Scandinavia, it is possible for most advanced countries to prosper while raising substantially more in tax than they currently do.

Figure 1: Tax revenue as a share of national income, 2018 compared to historic average

Note: Solid bars refer to 2018. For Australia, Greece and Japan, 2017 data shown. Outlined bars provides 1965 to 2000 average, except for the following (brackets give the associated start year): Korea (1971), Mexico (1980), Chile (1990), Poland and Hungary (1991). Source: OECD, Global Revenue Statistics Database, http://www.oecd.org/tax/tax-policy/global-revenue-statistics-database.htm.

A government wishing to raise additional revenues has plenty of options. There are large taxes that can be used to raised significant sums relatively straightforwardly, most obviously by simply increasing tax rates. Tax increases could be targeted at specific groups – for example those with high incomes or high wealth – or at specific activities – for example, the creation of pollution or the consumption of certain goods. We could raise taxes on business – although they will still ultimately be paid by people. With all tax choices come trade-offs. For example, we could raise corporation tax and one advantage of this is that it would only affect companies making a profit – those struggling wouldn’t see an increase in their tax bill. But a higher rate would reduce the incentive to invest in the UK.

Whichever taxes we choose, there is substantial scope for improving the structure of taxes in ways that would allow more money to be raised with less pain. Taxes can create a range of undesirable distortions to economic activity. For example, taxes can disincentivise work or investment or distort how effort or assets are allocated across the economy. These distortions can lead to resources being diverted away from their most productive uses, which in turn depresses economic output. While we can’t avoid all such distortions, many of the distortions created by taxes are not inherent features of a particular tax but rather arise as a result of poor tax design. For example, capital gains tax, corporation tax and business rates are all currently designed in a way that makes them more damaging to economic output than they need to be. There is substantial scope to reduce the distortions created by taxes by improving tax design.

Another factor affecting how damaging a tax is to economic output is how progressive it is. One of the reasons that consumption taxes may be more growth-friendly than income taxes is that they are generally less progressive. In general – though not always – reducing the amount of redistribution done in the tax system would increase aggregate income, but at the cost of greater inequality. There is typically a balance to be struck between a focus on progressivity and a focus on growth. However, whatever level of progressivity a government chooses, there are more and less efficient ways to achieve it. Not all taxes need to address all objectives and not all are well suited to being made progressive. What matters ultimately is how progressive the overall tax (and benefit) system is.

Three big taxes provide straightforward ways to raise large sums

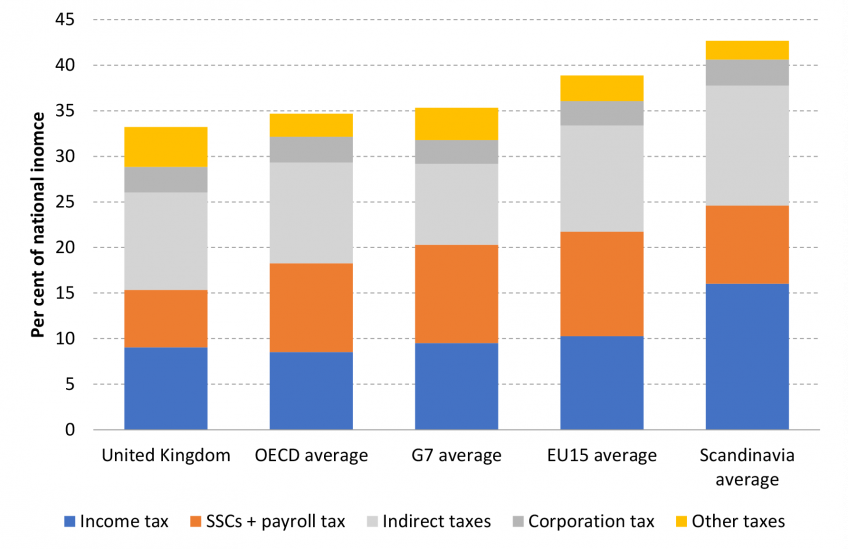

All OECD economies raise the majority of their tax revenues from three taxes: income tax, social security contributions (SSCs) and general sales taxes (VAT in the UK) (see Figure 2). These taxes account for two-thirds of UK tax revenues. Countries that raise a higher share of GDP in tax than the UK almost always raise more from these and in particular from SSCs.

A relatively straightforward way for a government to raise a substantial amount of additional revenue would be to increase the rates of income tax, SSCs or VAT. Small rate changes for these taxes tend to raise relatively large sums because they have a broad base.

For example, in the UK in a normal year, adding 1 percentage point to all income tax rates, all employee and self-employed National Insurance contribution (NICs) rates, or the rates of VAT, would raise £5.7 billion, £6.4 billion and £7.2 billion respectively. Doing all of these would raise over £19 billion, a little under 1% of GDP (£20 billion).

Figure 2: Sources of tax revenue across countries, 2016

Note: SSCs is social security contributions (NICs in the UK). The OECD average excludes Mexico, for which a tax-by-tax breakdown is unavailable. Source: OECD, Global Revenue Statistics Database, http://www.oecd.org/tax/tax-policy/global-revenue-statistics-database.htm.

The revenue raised from increasing the main rates of any of the big three taxes would come disproportionately from better-off households. If desired, income tax or NICs increases could be targeted more narrowly at higher earners, although this would bring in substantially less revenue. For example, raising only the higher rate of UK income tax (currently 40% for incomes over £50,000) by one percentage point would raise around £1 billion. Raising the additional rate of income tax (currently 45% for incomes over £150,000) by one percentage point is estimated to raise very little, though it might raise more or might lead to lower revenues, depending on how those affected respond. In general, the smaller the group that tax increases are targeted at, the harder it is to raise large amounts of additional revenue.

Raising any of the three main taxes would weaken work incentives. Of these three taxes, increasing NICs weakens work incentives most because all of the revenue comes from taxing earnings. In contrast, some of the revenue from income tax comes from taxing pension, savings and dividend income. Because part of the revenue comes from taxing existing wealth it does less (per pound of revenue raised) to reduce the incentive to work in future. Similarly, VAT will be levied on wealth that is yet to be spent as well as spending from future earnings, such that there is a weaker effect on work incentives.

Cutting reliefs is sometimes a good way to raise revenue

As well as changing tax rates, governments could raise revenue by broadening the tax base: that is, increasing the range of things that are subject to tax. A broader base is not always better – there are very good reasons that some things aren’t taxed and some tax reliefs should be seen as key parts of a well-designed tax system. However, more money could be raised by weeding out poorly designed reliefs.

In the UK, VAT is a prime candidate for base broadening. The UK applies zero VAT to a wider range of goods and services than almost any other developed country. The biggest area of zero-rating is (most) food, from which the government forgoes about £19 billion a year; other big-ticket items include house-building, passenger transport, prescription drugs, water bills, children’s clothes, and books, newspapers and magazines. Relative to a world in which VAT were charged at a standard 20%, the government forgoes around £50 billion a year from VAT zero-rating, and a further £4.8 billion from the reduced rate on domestic fuel.

Removing zero and reduced rates would, on its own, be regressive as poorer households spend a larger share of their budgets on these items. But better-off households spend more, and therefore save more in VAT, in absolute (cash) terms. This means that the additional revenue raised from removing a zero rate would be enough to more than compensate poorer households on average. For example, if the government put VAT on children’s clothes, it could use part of the revenue to increase child benefit so that the poorer half of households were no worse off on average, and still have revenue left over from the richer half of households.

Revenue could be raised while fixing taxes

Fixing the inequitable and inefficient parts of any tax system would be a valuable thing to do in its own right. More often than not, reforms that reduce distortions to economic activity would also increase economic output and mean that more revenue could be raised at less cost to households.

Capital incomes taxes are prime candidates for reform. In many countries capital incomes, including income earned by business owners, are taxed at lower rates than earned income. This is an acute issue in the UK where business owners have been the fastest growing part of the labour market for over a decade and where running a business is taxed at substantially lower rates than employment. The UK government forgoes about £15 billion a year by setting lower tax rates on the incomes of the self-employed and company owner-managers than the incomes of employees.

There is a strong case for aligning overall marginal tax rates across different forms of income regardless of how it is earned. Aligning rates would bring lots of benefits. It would be fairer and would improve the allocation of resources by, for example, reducing tax-motivated incorporation and reducing the resources devoted to tax compliance and avoidance.

If desired, such reforms could be done in a way that directly raised additional revenue. Revenue would come predominately from the top of the income distribution. Increasing tax rates on capital gains, dividends and self-employment income could also reduce the distortions associated with increasing taxes on labour incomes: raising labour income taxes increases the incentive to shift the form in which income is taken away from earnings and towards capital income (one reason raising the additional rate of income tax is estimated to raise little additional revenue), but the incentive to do this would be smaller if capital income tax rates were higher. But moving in this direction in isolation would discourage some savings and investments, creating a trade-off that has plagued capital taxes for decades. These distortions could, however, be avoided if we also made careful adjustments to the tax base, including to how investment costs are deducted in calculating taxable income. If we choose the path of reform we could raise revenues, increase fairness and improve investment incentives.

Structural tax reform isn’t often the easiest way to get revenue or the most exciting sell to voters. But with the economy in such bad shape, options that allow us to raise taxes in less damaging ways should be front runners.

Authors

Helen Miller

Helen is Deputy Director of the IFS and Head of the Tax sector.

More from IFS

Understand this issue

Policy analysis

Academic research