Downloads

WP201717.pdf

PDF | 1 MB

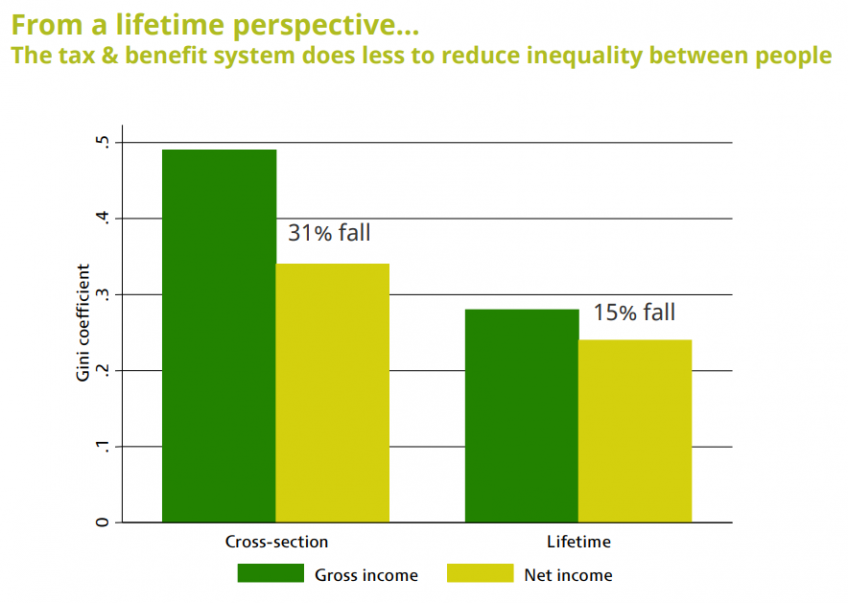

This paper examines the distributional impact of increases to out-of-work transfers, increases to work-contingent transfers, and increases in higher rates of income tax over the whole of life. We find that, in contrast to what is implied by standard snapshot analyses, increases to work-contingent benefits are just as effective at redistributing resources to the lifetime poor as increases to out-of-work benefits. This has important implications for the equity-efficiency trade-off typically thought to apply to work-contingent transfers. However, we find that higher rates of tax on annually assessed income are an effective way of targeting the lifetime rich, as incomes are more persistent towards the top of the distribution. Our results illustrate the importance of moving beyond an exclusively snapshot perspective when analysing tax and transfer reforms.

This working paper is an updated version of W16/17.

Authors

Jonathan Shaw

Jonathan is a Research Fellow at the IFS and a Technical Specialist in the Economics Department at the Financial Conduct Authority.

Peter Levell

Peter joined in 2009. He has published several papers on the microeconomics of household spending and labour supply decisions over the life-cycle.

Barra Roantree

Barra is a Research Fellow at IFS and Assistant Professor of Economics at Trinity College Dublin.

More from IFS

Understand this issue

Policy analysis

Academic research