Downloads

BN276-The-impact-of-COVID-19-on-share-prices-in-the-UK%20.pdf

PDF | 966.37 KB

The spread of COVID-19, and international measures to contain it, are having a major impact on economic activity in the UK. In this briefing note we describe how this impact has varied across industries using data on share prices of firms listed on the London Stock Exchange, and how well targeted government support for workers and companies is in light of this.

This follows Ramelli and Wagner (2020) [1] who describe the impact on the US and China by looking at changes in share prices; Gormsen and Koijen (2020) [2] provide further analysis of the US.

Changes in share prices allow us to see how different industries are affected by COVID-19 in real-time. Stock market data does have a few limitations however, when it comes to measuring the impact of the crisis. Notably it does not include small firms, firms which are not publicly listed, the third sector or the public sector, which might be affected quite differently. For example, many public sector services have seen an increase in demand. In addition, many of these firms operate internationally, so changes in their share prices will represent the effects not only on the UK economy but also in other markets that they operate in. Finally, other factors may also have affected share prices over this period.

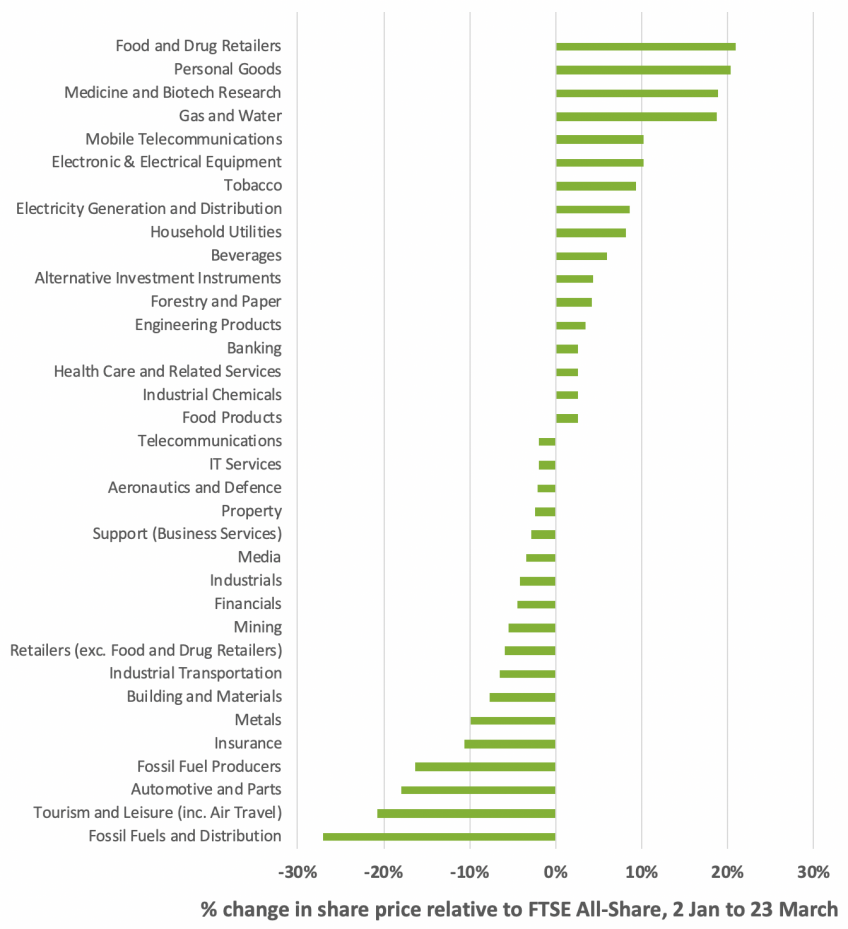

Figure 1 shows the change in the share price of all firms listed on the London Stock Exchange relative to the FTSE All-Share index between 2 January and 23 March 2020 (the FTSE All-share index fell by 35% over this period). The industries that have been hardest hit include tourism and leisure (which includes air travel), fossil fuels production and distribution, insurance, retailers (excluding food and drug retailers) and some large manufacturing industries. At the other end of the spectrum some industries have outperformed the market, including food and drug manufacturers and retailers, utilities, high tech manufacturing and tobacco. Unsurprisingly, firms in medical and biotech research have also outperformed the market (falling by 16% relative to the overall fall of 35%).

Changes in share prices reflect market expectations about a number of effects, including: changes in final demand (people are buying more of some items and less of other items), changes in intermediate demand (the firms that they sell to are changing what they want to buy and how much), and restrictions in supply (it may be difficult for some firms to obtain inputs they need due, for example, to interruptions to their supply chain).

Figure 1: Percentage change in share prices of firms in different sectors listed on the London Stock Exchange relative to the FTSE-All Share Index, 2 January – 23 March 2020

Notes: Authors' calculations based on indices of sector share prices, as reported on shareprices.com (accessed on 25 March 2020), using Industry Classification Benchmark definitions.

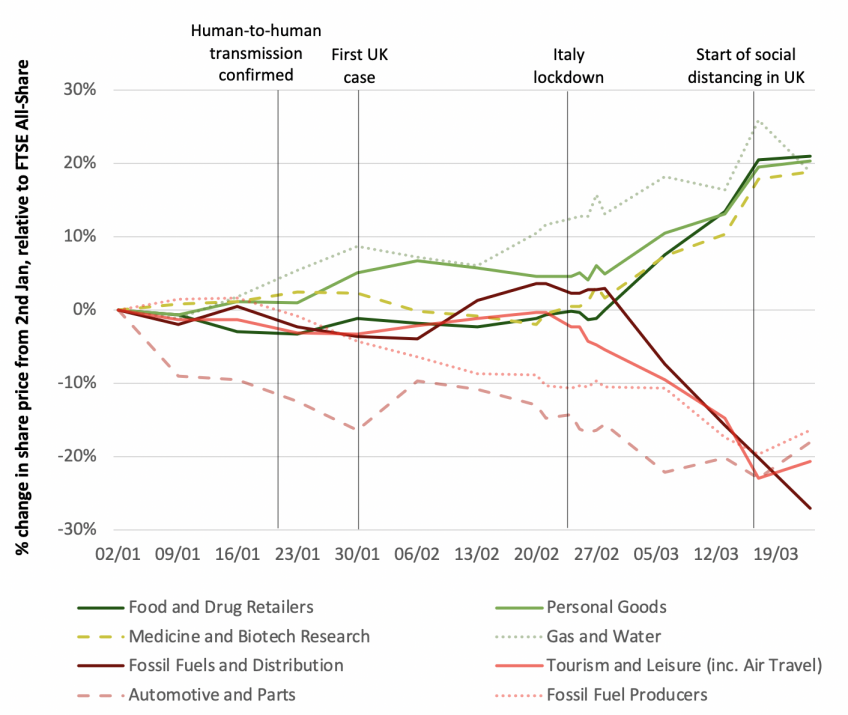

The timing of changes in share prices reflects the timing of changes in market expectations. Figure 2 shows the cumulative change in share price over the period for the four sectors with the largest increase and the largest decrease in their relative share price over the period from 2 January to 23 March 2020. For most of these sectors, changes in share prices did not take place steadily over the period. Instead, big changes in share prices occurred from the end of February, in the days following Italy’s introduction of a lockdown in Lombardy, with very little change in prices in the period before. The exceptions to this are the gas and water, automotive and parts, and fossil fuel production sectors, where changes in share prices took place steadily over the three-month period, possibly driven by other factors.

Figure 2: Percentage change in share prices of firms listed on the London Stock Exchange in sectors with the largest share price movements relative to the FTSE-All Share Index, from 2 January 2020

Notes: Authors' calculations based on indices of sector share prices, as reported on shareprices.com (accessed on 25 March 2020), using Industry Classification Benchmark definitions. Vertical lines indicate: 20 January, the first confirmed human-to-human transmission in China and first WHO report; 30 January, first confirmed case in the UK; 23 February, Italy introduced lockdown in Lombardy; 16 March, the UK Prime Minister first urged social distancing.

On 17 March the government announced a raft of measures aimed at protecting workers and businesses affected by measures taken to contain the spread of COVID-19. These included a 12-month business rates holiday for firms in the retail, leisure and hospitality industries and a Coronavirus Job Retention Scheme (JRS) that would pay 80% of employee wages for furloughed workers up to a maximum of £2,500 per month for each employee. This package was aimed, at least in part, to prevent otherwise viable businesses from shutting down. The value of these measures will vary greatly across sectors. Labour intensive sectors in particular are likely to benefit more from the JRS than other industries. In other sectors, capital costs and purchases of inputs from other industries are more significant; the benefit to firms in these industries will depend crucially on their ability to adjust their costs as they reduce output. For instance, airlines may use less fuel as more planes are grounded and flights cancelled, but they may still face the costs of leasing and maintaining those planes. The extent to which firms can quickly reduce their costs, and then when the recovery starts quickly scale up again, will depend on many factors, such as what these costs are and what sort of supply relationships they have.

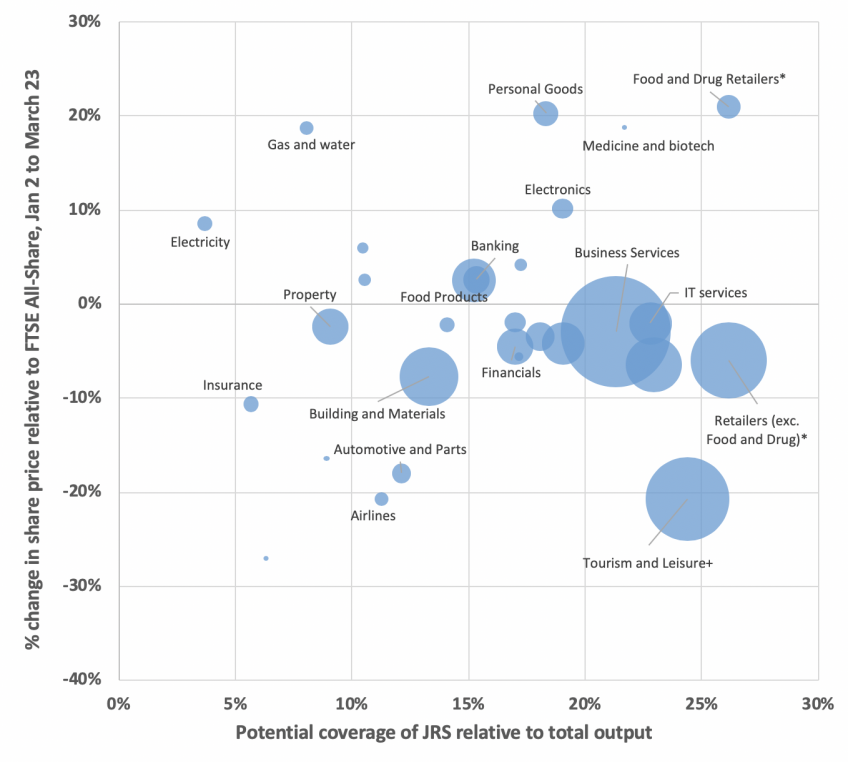

To get an idea of the potential benefit of the JRS scheme for different industries relative to how badly those industries are likely to be affected, Figure 3 plots the potential coverage rates of the JRS scheme against the cumulative relative share price declines for some of the key industries. The horizontal axis shows the maximum extent of support the government has made available via JRS, i.e. if every private sector employee working in that industry (not only those in firms listed on the stock market) was furloughed and all firms claimed the full 80% of labour costs up to the £2,500 monthly limit; we scale this by total output of firms in each industry. The support will vary depending on how important labour is as a share of production, compared to machines and intermediate inputs (such as parts, electricity, etc.), and depending on the distribution of wages in each industry. The vertical axis shows the size of the relative change in share prices from 2 January to 23 March 2020, as shown in Figure 1. The size of each dot represents the number of people employed in that industry.

Figure 3 shows that the support is more effectively targeted at some industries than others. For example, retail, for which labour is a relatively high share of output, has a comparatively high share of output covered by the JRS. Insurance, airlines, automotive and parts, and building and materials on the other hand have relatively small shares covered by JRS. Tourism and leisure (excluding air travel) stands out in being one of the hardest hit industries (in terms of seeing a large reduction in relative share price) and having a relatively high share of protection through JRS.

As the shutdown continues, more capital-intensive firms that are not able to substantially reduce their costs may start to struggle more; this may lead to pressure for further government support. There are likely to be long-run costs to the economy if these firms were forced to shut down and the skills and experience of their workers were lost.

Figure 3: Potential coverage of Coronavirus Job Retention Scheme relative to output for different industries versus their share price changes relative to the FTSE-All Share Index, 2 January – 23 March 2020

Notes: The vertical axis shows the size of the relative change in share prices from Figure 1. The horizontal axis shows the potential coverage of the JRS scheme as a share of total industry output. The size of each dot represents the number of people employed in each industry. Potential coverage of JRS is 80% wage costs in each industry up to a maximum of £2,500 per worker per month. To obtain the potential coverage of the scheme relative to output, we multiply the potential coverage of each industry's wage bill by each industry's share of labour costs relative to total output. Labour shares are taken from the 2015 ONS Input-output tables. The potential coverage of the JRS scheme is calculated using the 2018 Quarterly Labour Force Survey. Employment data are taken from the 2018 Business Resister of Employment Statistics. JRS coverage for medical and biotech research and banking are taken from industries with SIC codes beginning 64 and 72 respectively (which are also included in the coverage rates for business services and financials respectively. Figure does not include data for alternative investment instruments, engineering products, household utilities, metals, mobile telecommunications, or tobacco either because these sectors could not be mapped to industries in the input-output tables or because they had negligible employment shares. We exclude healthcare and related services because the majority of employment in this industry is public sector.

* Potential coverage of JRS for food and drug retailers is assumed to be the same as for retailers (exc. food and drug retailers).

+ We have separated tourism and leisure (excluding air travel) and airlines for the purposes of the horizontal axis, but the share price information is for these two activities combined.

[1] Ramelli, Stefano, and Alexander Wagner. ‘What the stock market tells us about the consequences of COVID-19’. VoxEU, https://voxeu.org/article/what-stock-market-tells-us-about-consequences-covid-19, 12 March 2020.

[2] Gormsen, Niels Joachim, and Ralph Koijen. ‘Coronavirus: Impact on Stock Prices and Growth Expectations’. Becker Friedman Institute for Economics WP 2020-22, 24 March 2020.

Authors

Rachel Griffith

Rachel is Research Director and Professor at the University of Manchester. She was made a Dame for services to economic policy and education in 2021.

Peter Levell

Peter joined in 2009. He has published several papers on the microeconomics of household spending and labour supply decisions over the life-cycle.

Rebekah Stroud

More from IFS

Understand this issue

Policy analysis

Academic research