Downloads

Download chapter PDF

PDF | 1023.72 KB

Executive summary

- Spending on cash transfers for those of working age – the focus of this chapter – has generally grown in the UK, both in real terms (from an average of £1,000 per working-age adult per year in the late 1970s to £2,500 just before the pandemic (in today’s prices)) and as a share of national income. But over the period of austerity between 2010 and the pandemic, the working-age benefits bill fell both relative to national income and per person.

- The targeting of support on different demographic groups has changed radically. Over the long term, the UK’s cash transfer system has increasingly oriented itself towards pensioners and those with children. The growing priority given to support for pensioners is an important part of the backdrop behind trends in the working-age system, especially for the tight squeeze on the working-age benefits budget since 2010. In 1990–91 the basic support for a single person with no other source of income was 32% higher for those just over pension age than for those just under, but that figure has now grown to 137%. Within the working-age population, too, there have been big shifts. In 1975–76 an out-of-work lone parent with two children would get just 12% more than a couple without children in otherwise-similar circumstances, but by the eve of the pandemic they would get almost double.

- Major policy reforms over the past 25 years have repeatedly followed a pattern of encouraging people into paid work (using both carrots and sticks) – especially if they do not live with another working adult. Such work is usually part-time, and often associated with very low earnings. The tax credit expansions of the early 2000s, which offered income top-ups for low-earning households, mostly expanded support for working 16 hours per week but often implied strong financial disincentives to go further. Imposing job-search requirements on an increasingly large fraction of lone parents on out-of-work benefits did push many into employment, but essentially all of it was part-time and on weekly earnings less than the 40th percentile. The switch to universal credit – the current flagship reform of means-tested benefits in the UK – especially increases financial incentives to do so-called ‘mini-jobs’ at very low hours, and makes little difference to the incentive to shift from full- to part-time work.

- Much or all of the benefits system is a system of patches applied to problems that we have not found better ways of addressing, such as low pay, ill health and high housing costs. Hence, wider trends in the economy and society can and do radically change what is required of the benefits system. Housing trends are a leading example of factors that leave the transfer system with no easy answers. While rising rents and the shift towards private renting continue, policymakers have to either accept an ever-increasing housing benefits bill or leave a growing fraction of the low-income population highly exposed to high housing costs, or some combination. In reality, both have happened. Housing benefit spending per working-age person has risen by around 40% since the mid 1990s, and yet a growing fraction of the low-income privately renting population are spending large fractions of their income on housing.

- Transfer policy choices should in future factor in the longer-term effects to a greater extent than they have to date. In particular, recent research has shown that part-time work does much less than full-time work for career and wage progression. Hence, a drawback of incentivising some people to work part-time who would otherwise have worked full-time is that their future wages are likely to be lower than they would have been. We understand this better than we did when the UK’s tax credits system was introduced in the late 1990s, for example. The point is relevant for very live policy choices today. New research suggests that changing universal credit to incentivise employment in a way that further encourages part-time work has very different long-term impacts on wages, incomes and the government budget from doing it in a way that reduces the disincentive for full-time work.

- Compared with most developed nations, the UK’s benefit system provides little income protection against job loss. This is especially so for those on middle or high earnings, since those earnings typically buy them no additional support once they fall out of work, due to the UK’s reliance on means-tested, rather than earnings-related, payments. Families without children also have especially low earnings replacement rates, as their out-of-work benefit entitlements have barely changed in real terms for half a century while earnings have doubled. A single childless worker on average earnings in the UK can expect to receive 13% of their in-work income when they lose their job; across the OECD, the average is 55% (if they had been in work for a significant length of time). The growth of a significant in-work transfer system means that the system has shifted towards replacing lost income when a worker’s earnings decline (but they remain in work) and away from when they lose their job altogether.

- If the government wanted to strengthen the insurance it provides against job loss, there would be a number of options it could pursue without a wholesale move towards an earning-related benefits system. These options would include paying higher benefits early on in the jobless spell – perhaps by making them a function of past earnings for a limited period or by more closely linking initial entitlements to actual expenses (e.g. basing housing support on actual rent paid, and child-related support on the actual number of children in the family) – when pre-committed expenditures are especially hard to adjust.

- Imposing job-search conditions on claimants of out-of-work benefits (often known as ‘conditionality’) has become increasingly widespread. But the evidence suggests that the positive impacts of this, especially in the long term, are very arguable. Conditionality needs to be carefully justified with respect to clear goals, and carefully designed with those goals in mind. The extension of conditionality to many more single parents since 2008 has led many to move into paid work, but that work has been almost entirely part-time (fewer than 30 hours per week) and low-earning (in the bottom 40% of the overall earnings distribution). This is precisely the kind of work that tends to bring little or nothing in the way of longer-term benefits for skills, labour market attachment and wages. In combination with the fact that some lone parents have simply begun claims for health-related benefits instead (which come without the same conditions), this has meant that fiscal savings have been very minor. The jury is therefore still out on whether this kind of conditionality is achieving enough to be worth it, at least without effective schemes focused on human capital development running concurrently. Looking to the future, there is the additional issue that job-search requirements are focused on traditional employee work, and this may become increasingly outdated and hard to operationalise with continued increases in self-employment and the gig economy.

- Little is known about the impact of in-work transfers on wage levels – and so we do not know how many of the billions of pounds spent on them actually benefit the intended beneficiaries. It is entirely possible that these benefits, by encouraging people into work, allow employers to pay lower wages than they otherwise would. The available empirical evidence base on this is limited, but suggests that the effect might be significant. More evidence on this – and, crucially, on what other policies (such as the minimum wage) can help limit the unintended consequences for wages – would be extremely valuable. A very similar point applies to the impact of housing-related support on rent levels.

- Well over £10 billion of benefits goes unclaimed each year – but there is scope for changing this. Lack of information about benefits and the hassle or complexity associated with applying for them seem to be key reasons for non-take-up; the evidence on the role of stigma is thinner but what is available suggests that it is less important. Plenty of evidence suggests that simple interventions such as sending reminder letters to those who are likely to be eligible can be effective in boosting take-up, should a government want to do so. Moreover, the advent of ‘Real Time Information’ – where employers provide to HMRC frequent reports of employees’ earnings – could allow a greater role for ‘defaulting’ people into receiving benefits, or at least promptly informing them that they may be eligible. This is an area where experiments are feasible and likely to be fruitful – for example, by providing more information on the crucial issue of whether it is the neediest, or the least needy, that do not claim their entitlements, on which there is currently mixed evidence.

1. Introduction

Cash payments directly to individuals or families are a major component of most modern welfare states, alongside the provision of publicly provided services (throughout this chapter, we use the terms ‘transfers’, ‘benefits’ and ‘welfare payments’ interchangeably). The scale of their importance is easy to under-appreciate. The UK state spends more on cash transfers to those of working age (adults under state pension or retirement age) than on education, or defence and policing combined. At any point in time, more than a quarter of all working-age UK families are in receipt of means-tested benefits (Office for Budget Responsibility, 2018). And even that underplays the true reach of the system: at some point in their lives, most people will be in a household receiving a working-age means-tested benefit (Roantree and Shaw, 2018).

A system of transfers this expansive undoubtedly has large effects on the level of poverty and deprivation, and on the financial incentives that people face. But it does not stop there. For example, as we elucidate in this chapter, it probably affects the earnings and housing costs of people not even receiving the transfers (not to mention the taxes they pay), and it impacts the next generation via the children growing up in families that draw on the state safety net. In short, cash transfers are a very consequential part of our economy and our society.

All of the detailed discussion and analysis in this chapter focuses on the working-age part of the benefit system. As shown in Section 2, an even larger (and growing) portion of the welfare budget supports the living standards of those above the state pension age. Our focus on the working-age system is primarily because these two parts of the system are trying to do very different things. The labour market provides the backdrop, or at least critical context, to the workings of the working-age transfer system. Almost all of it is providing support to people in light of their not being judged to have enough to support themselves through paid work alone – including because they are judged unable to do any paid work at all due to caring responsibilities or health problems. Supporting the living standards of those in retirement is of course crucial, but not within scope of this chapter.

The term ‘cash transfers’ captures money paid to support people who cannot find, or are judged unable to do, paid work, or people who are in paid work and yet have a low income, or who have extra costs arising from children or disability or housing needs. The underlying motivations for these policies can be similarly wide-ranging: for example, preventing or reducing poverty, protecting people from adverse economic shocks (‘insurance’), pursuing ‘horizontal equity’ between people with different costs of living (e.g. due to disability or children), and promoting the life chances of children.

There are many key choices, and trade-offs, that governments face when designing and adjusting these programmes. How much are they willing to spend on them? What will be the balance between support focused on the neediest and support aimed at a broader base? Which demographic groups, or needs, will be prioritised? Will the benefits be in cash or in kind? To what extent will the level of support track people’s fluctuating circumstances in real time, stepping in quickly when needs increase, versus prioritising those in more persistent need? How are the benefits of having a simple system that is easy to understand and navigate to be balanced against the inevitable tendency towards complexity, when policy goals are multiple and the circumstances of the population widely-varying? How will support actually be delivered to people: what is the claiming process like, when does money arrive, how often is it paid, and so on?

Much of the chapter will discuss how policy choices made in the UK have changed over time and how they compare internationally, and the evidence on how these choices can shape the impacts of the system.

There are many ways in which transfer policies can fail to achieve their goals as effectively as might be hoped. For example, incomplete take-up of welfare programmes may inhibit their ability to alleviate poverty. In addition, the perhaps-successful pursuit of one goal can lead to other pitfalls that governments should, and often do, try to avoid (though some of these pitfalls reflect trade-offs that are impossible to get around entirely). For example, trying to maximise the impact of the system on reducing poverty can lead to support heavily targeted on a small group with the lowest resources; but this in turn can lead to negative behavioural effects driven by the steep phasing out of support, and demeaning or stigmatising effects of being a recipient which might themselves inhibit take-up and hence poverty alleviation as well. Of course, as with any public programme, an inadequate level of funding can also lead to a failure to achieve its goals.

One theme that runs through much of the chapter is the intricate relationship between the transfer system and the wider economic and policy environment. Much of the system is effectively applying a patch over social and economic problems that we have not yet found a better way of preventing or addressing (e.g. low pay or poor health). As the problems facing society evolve, the distribution of support provided by the transfer system, and its impacts, will tend to change – both automatically and via deliberate changes to its targeting or design. More progress in other areas of economic and social policy will typically make the transfer system’s job easier.

In broad terms, the chapter is organised in two halves. In the first half (Sections 2 to 4), we describe the UK benefit system and examine recent trends, both in policy and in the economy at large, that impact upon the role that it fulfils. In the second half (Sections 5 to 10), we turn to specific issues in benefit policymaking, summarising existing research, introducing new evidence and discussing lessons for policy.

The structure is as follows. In Section 2, as background to what follows, we describe the basic components and workings of the current UK working-age cash transfer system, and we define the scope of our chapter by distinguishing it from broader components of what one might term the ‘welfare state’. In Section 3, we set out how the role of the system has changed over time, through changes both in policy and in the wider economic and social environment. Section 4 examines the effect that the transfer system has on work incentives, both directly through the financial incentives to work, and through conditionality, sanctions and other ‘active labour market policies’. Section 5 discusses take-up of benefits, in particular who claims their entitlement and what the reasons are for non-take-up. Section 6 turns to ‘incidence’: whether, and how much, paying benefits to those in work or those renting homes can reduce their wages or increase their rent. Section 7 briefly discusses a number of implementation issues with transfer policy which are often glossed over but can be of great importance: wait times to receive the first payment, the period over which benefit entitlements are assessed, and who in a couple actually receives the transfer. Section 8 looks at intergenerational effects – how a benefit payment to a parent today might affect the education, labour market and indeed welfare outcomes for their child many years down the road. Section 9 brings together the implications of the evidence discussed for universal credit, the UK’s most important reform to the transfer system in decades, which is still underway. Section 10 discusses a number of broader policy issues and debates with implications across the benefit system. Section 11 concludes.

2. The current cash transfer system in the UK

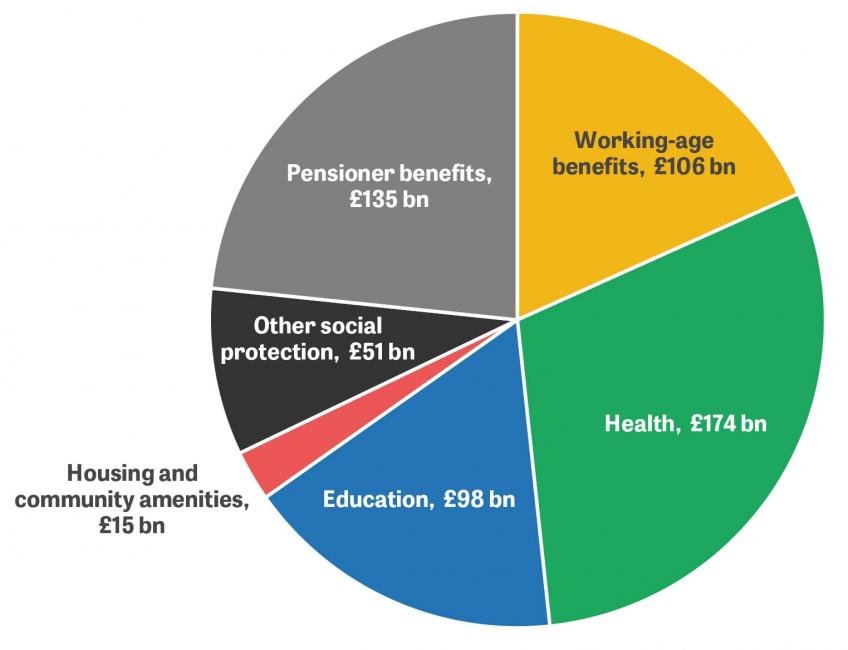

Governments in high-income countries typically provide extensive transfers to households, not only in cash but also in kind, such as in the form of health and education provision. Much or all of that would often be considered a part of the ‘welfare state’ – a term with no hard-and-fast definition. As explained, in this chapter we restrict our focus not only to cash transfers, but also to transfers paid to those below state pension age1. As is made clear by Figure 1, this means we consider only a modest share of the total expenditure on the welfare state defined in much broader ways. Nonetheless, before the COVID-19 crisis, spending on working-age benefits was very significant, standing at around £100 billion per year or 4½% of national income.

Figure 1. ‘Welfare state’ spending, 2019–20 (in 2021–22 prices)

Note: We use 2019–20 expenditure here as the latest public service spending data contain significant COVID-related spending.

Source: Authors’ calculations using HM Treasury’s ‘Public expenditure statistical analyses 2019’ and DWP’s ‘Autumn Budget 2021: expenditure and caseload forecasts’.

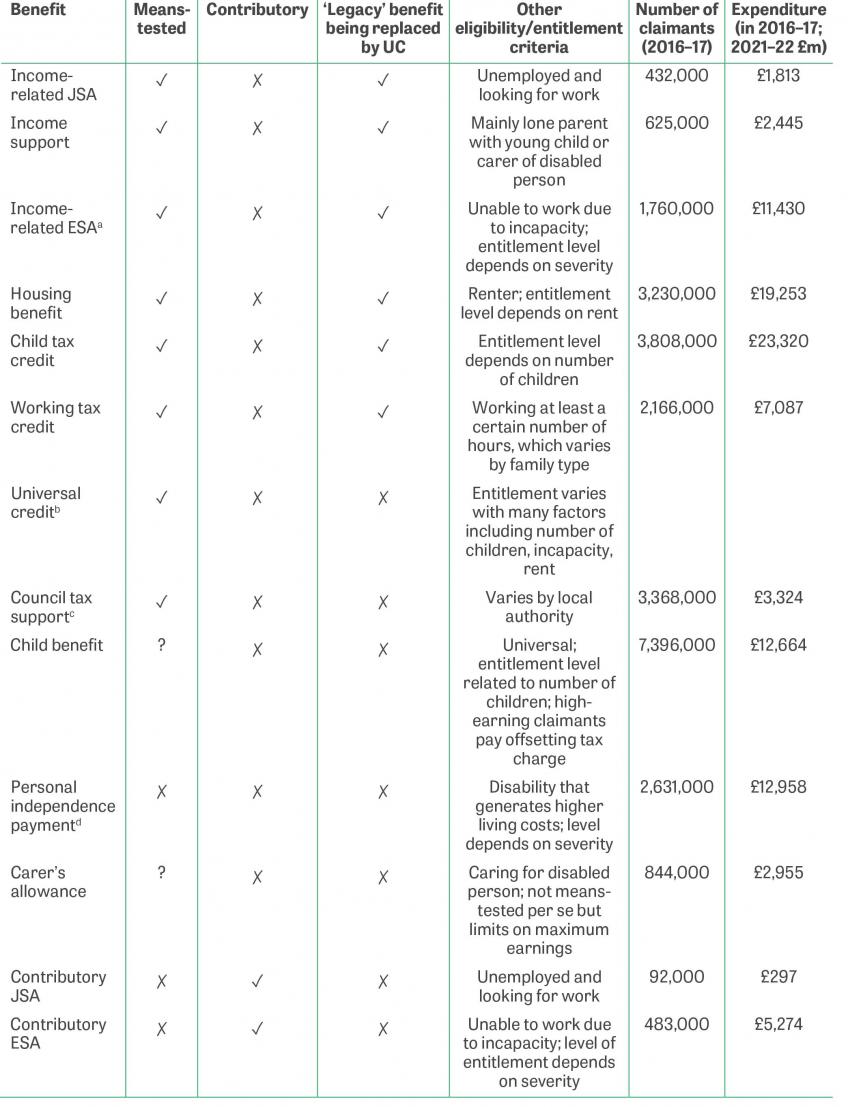

Below we give a broad sketch of the current UK working-age benefit system as it stands in 2022–23. Readers already familiar with the UK system, or wishing to skip the details, can proceed to Section 3. Table 1 provides a short summary of the various benefits2. Figure 2 shows estimates of their mechanical impacts on the rate of relative poverty to help illustrate how they are targeted (i.e. how much poverty would rise by under the thought experiment in which the benefit were abolished and nothing else changed).

All means-tested benefits are assessed at the level of (in the technical UK terminology) ‘benefit units’. These correspond to what are known as ‘tax units’ in the US, consisting of an individual, any partner they have and any dependent children. These units are often referred to using the more accessible term of ‘family’, which we will adopt here to avoid the more cumbersome, less familiar alternative terms, though clearly this does not correspond precisely to the everyday usage of the term ‘family’. For example, a single person without children is considered a ‘family’ for these purposes, and an adult who lives with their parents is not treated as part of the same family.

Table 1. Description of working-age benefits (numbers relate to 2016–17)

Notes to Table 1

a Includes incapacity benefit.

b Number of claimants and amount spent are not shown for UC, which very few people received in 2016–17. When fully rolled out, UC is expected to cost more than £60 billion per year and to be received by 7 million families at any one time.

c Number of claimants and amount spent are for 2012–13, the last year for which council tax support (then council tax benefit) was administered centrally by the Department for Work and Pensions (DWP), and thus the last year for which these data are available.

d Includes disability living allowance, including that spent on children.

Note: We use 2016–17 numbers as UC roll-out began to pick up in 2017–18, distorting the figures. See text for discussion.

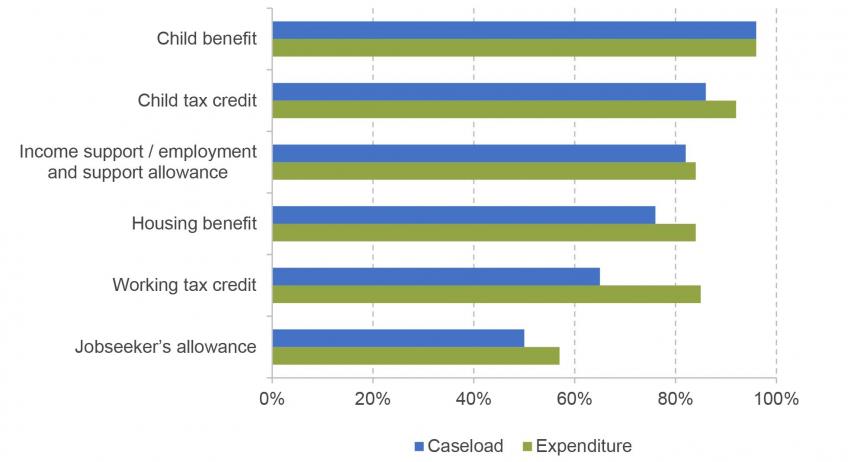

Figure 2. Mechanical effect on working-age poverty rates from abolishing various working-age benefits (2016–17)

Note: The poverty line used is 60% of contemporaneous median after-housing-cost income. See text for definitions. We use 2016–17 data as they largely predate universal credit; the small amount of UC spending in that year is allocated to ‘Out-of-work benefits’. Excludes households comprised entirely of students.

Source: DWP’s ‘Households below average income statistics’, 2016–17.

‘Legacy’ benefits

‘Legacy benefits’ is the term often used to refer to those benefits that formed the bulk of the UK’s means-tested system for those of working age until they were largely replaced by a single integrated benefit, called universal credit (explained shortly) – a process that began in 2013 and is still ongoing. The complex array of support available under this system highlights the many things that the system was – and still is – trying to do. It also reflects the way in which the system has come about, with new priorities or demands from an evolving society sequentially leading to additional strands of support, or to substantial growth in existing strands of support, all layered on top of one another.

While there are still a significant number of existing claimants of these benefits, no new claims for these are generally allowed any more, and eventually these benefits will disappear entirely3. The only exceptions are the two ‘contributory’ out-of-work benefits – entitlement to which is dependent upon having ‘paid in’ to the system through work earlier in one’s life – which will continue to exist alongside universal credit (UC). Describing the legacy system remains a good starting point for understanding the basics of what kind of support the UK offers to low-income households, since the key elements of support – the out-of-work safety net, the extras for housing and children, and so on – all remain in place under the UC system, and largely at the same rates. The legacy benefits are:

- Out-of-work benefits. There are three main benefits that are specifically for individuals who are not working:

o Jobseeker’s allowance (JSA) is paid to individuals who are looking for work. There are two forms of JSA: an income-related version, which is means-tested against family income and assets, and a contributory version, which is not means-tested and is paid for six months to those who meet fairly minimal recent-work requirements. JSA claimants are generally subject to ‘conditionality’: they must prove that they are looking for work and meet regularly with their work coach in order to get the benefit. A single claimant is entitled to £77.00 per week.

o Income support (IS) is very similar to income-related JSA with identical financial entitlements, but there is no conditionality attached and it is only paid to those caring for someone with disabilities or lone parents with a young child.

o Employment and support allowance (ESA) is a benefit paid to those judged to be unable to work because of an incapacity. Like JSA, there is an income-related version which is means-tested against family income, and a contributory version which is not means-tested. Claimants are given differing entitlements based on the severity of their incapacity. Some – those assessed as being able to engage in ‘work-related activity’ – are subject to a form of conditionality, being required to do work-preparation activities such as training and CV writing. Some claimants are entitled to no more than the JSA rate (£77.00 per week for a single person), while single claimants with the most significant incapacities are entitled to £204.75 per week.

- Housing benefit (HB). This is a means-tested benefit paid to families in rented accommodation. It is means-tested against income and assets, but can be received irrespective of work status. The highest award a recipient can receive is their actual rent, though claimants renting from a private landlord are generally subject to caps (known as ‘local housing allowance’ rates), with higher caps applied to bigger families and those who live in more expensive areas. Those renting from a social landlord (e.g. councils or housing associations) are not subject to those caps, though if they live in a property deemed too large for their needs their maximum entitlement can be reduced (the so-called ‘bedroom tax’ or ‘under-occupancy charge’) which affects a substantial minority. Entitlements vary significantly with circumstances (income, assets, rent, family size, private or social sector, location), but a couple with two young children and no other income who are renting privately in an average area could be entitled to up to around £150 per week.

- Personal tax credits. Despite their name, these are unrelated to the tax system (except that they are, like most taxes and unlike most other cash transfers, administered by HMRC) and are means-tested transfer payments.

o Child tax credit (CTC) is paid to families with dependent children. Entitlements are higher for larger families (each child generating an additional £56.29 per week entitlement), though children born since April 2017 do not increase entitlements if they are the third or subsequent child in the family (the ‘two-child limit’).

o Working tax credit (WTC) is paid to families who work at least a set number of hours (16 per week for lone parents, 24 for couples with children, 30 for everyone else). A lone parent working 16 hours is entitled to up to £80.45 per week. While in principle those without children are eligible, they are entitled to relatively little and so the take-up rate among such people is quite low.

Other benefits

- Council tax support (CTS) (sometimes called council tax reduction) is a benefit tied to a claimant’s council tax bill, means-tested against family income. The design of CTS is left up to local authorities, but generally a claimant with no other income or assets can get a CTS award equal to most or all of their council tax liability. CTS is usually implemented as a reduction in the claimant’s council tax bill, rather than a separate cash payment. It is means-tested, but was – unlike other means-tested benefits – not replaced by UC. Rather, it will continue to operate as an additional means test in parallel to UC.

- Child benefit (CB) is a payment for families with dependent children. The first child in a family generates a CB entitlement of £21.80 per week; each subsequent child increases entitlements by a further £14.45 per week. For a long time, it was universal (and not taxable) among families with children. However, since 2013, families in which at least one adult has a taxable income of over £50,000 per year are subject to an additional income tax charge. This charge tops out at 100% of the family’s CB entitlement for those families where a partner has an income of over £60,000. It is thus best to think of CB as a means-tested benefit but where means-testing only kicks in from a high threshold, and where, oddly, the phase-out is in operation between £50,000 and £60,000 of the income of the highest-income parent. Note that this also implies that the phase-out rate depends on how much CB the family receives, i.e. how many children are in the family.

- Personal independence payment (PIP) is a non-means-tested, non-contributory disability benefit4. It is designed to compensate individuals for the costs associated with disabilities (such as needing help with mobility, preparing food or getting dressed). Unlike ESA, it is not related to the ability to work – PIP claimants can work without it affecting their entitlement. Entitlements vary from £24.45 to £156.90 per week depending on the assessed level of disability.

- Carer’s allowance (CA) is a benefit paid to those who provide full-time care for a disabled person. It is not means-tested against family income, although claimants are not allowed to work more than a small amount. The benefit is paid at a rate of £69.70 per week.

Universal credit

Universal credit (UC) is the UK’s new ‘integrated’ benefit, combining means-tested support previously separately provided by out-of-work benefits, means-tested benefits for families with children and means-tested benefits to help with rental costs. Eventually, UC will replace the ‘legacy’ benefit system entirely for those of working age (pensioners will still be able to receive housing benefit), though progress has been slow. Roll-out began in 2013 and is not expected to finish until at least 2028. Though there are some important exceptions (principally relating to assets and those with incapacities), families with no other income will normally get the same amount of UC as the total combined transfers they would have received under the legacy system (except for April 2020 to September 2021, when there was a temporary £20 per week increase in UC rates that was only reflected in WTC, and not out-of-work legacy benefit rates). They will also usually be subject to work-search conditionality (similar to JSA). The major difference in entitlements is among families in paid work: UC changes the rate at which benefits are withdrawn against earnings and, unlike WTC, does not have ‘hours rules’ which predicate entitlement on the number of hours worked. We explain how UC changes entitlements for working families in greater detail later in this section.

The government implemented other important changes to the operation and administration of benefits as part of the UC reforms, including the rather infamous ‘five-week wait’ between a claimant making an application and receiving their first UC payment. We discuss these issues, and particularly the five-week wait, in more detail in Section 7.

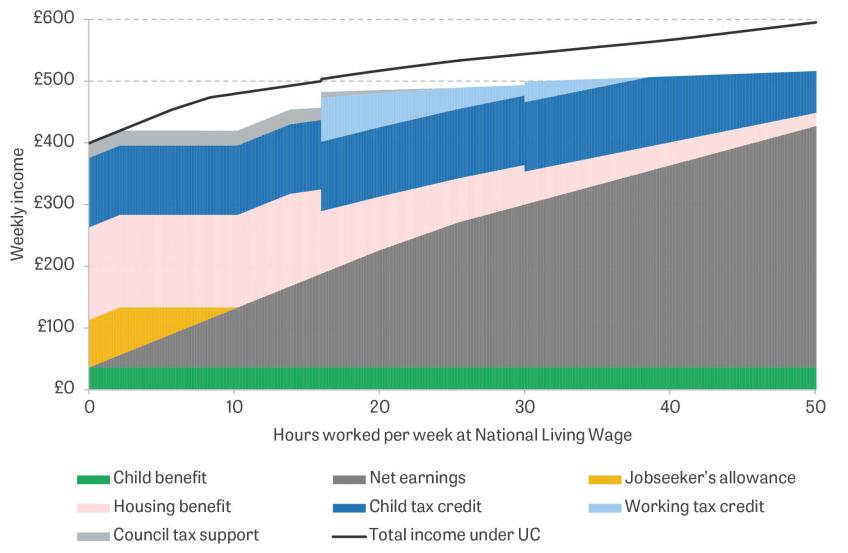

Figure 3. Weekly income for an example lone parent renter with two children earning the National Living Wage

Note: April 2022 tax and benefit system. Example is for a family where both children are under 5 and rent is £150 per week. Family lives in a band C council tax property in a local authority with the national average council tax rate and a council tax support scheme that, for lone parents, rebates 100% of council tax for a family with no income and applies a 20% taper rate for those with income above a certain threshold. Council tax itself is not included (i.e. it would have to be paid out of the weekly income shown). ‘Net earnings’ shows gross earnings minus income tax and National Insurance contributions. ‘Total income under UC’ is universal credit plus net earnings, child benefit and council tax support.

Source: Authors’ calculations using TAXBEN, the IFS tax and benefit microsimulation model.

To give a sense of how UC changes the system, Figure 3 shows benefit entitlements and net earnings for an example lone parent of two children who lives in rented accommodation and is paid the National Living Wage (£9.50 per hour in 2022–23). Legacy benefits, child benefit, council tax support and net earnings (earnings after tax) are shown as stacked areas, meaning that the sum of those areas is the worker’s total net income under the legacy system. Their income under the UC system (net earnings plus UC, child benefit and council tax support) is shown as a line. Under the legacy system, the lone parent has to claim five benefits to get their full entitlement when out of work. As they increase their hours, JSA is quickly withdrawn. When they get to working 16 hours, they become entitled to WTC. This means that the incentives to work at least 16 hours, rather than slightly less, are strong. Increasing hours beyond 16 results in their HB, council tax support and WTC (then CTC) being simultaneously withdrawn, implying a high marginal effective tax rate. In fact, as shown in Figure 4, once income tax and National Insurance contributions are included, it is not uncommon for lone parents to face a marginal effective tax rate of 96% (that is, 96p is lost in higher taxes and lower benefits if an additional £1 is earned).

Under the UC system, things are broadly the same in financial terms when the individual is out of work (although note that, other than child benefit, they now only need to make one benefit claim to receive their full entitlement, with potential implications for take-up, as discussed in Section 5). Above an earnings allowance (the ‘work allowance’), their UC entitlement is steadily withdrawn by 55p for every £1 of net (post-tax) earnings. But, as shown by Figure 4, once we account for tax and the withdrawal of CTS on top, the marginal effective tax rate can still reach 76% – lower than in the legacy system, but high, as discussed in the accompanying commentary by Moffitt (2023). Unlike WTC, UC entitlement is not dependent on working a precise number of hours (though those earning very little sometimes have to fulfil job-search conditionality requirements under UC), so there is no particular incentive to work 16 or more hours, for example. In comparison with the legacy system, UC therefore less strongly disincentivises so-called ‘mini-jobs’ of under 16 hours per week. It also reduces the worker’s effective marginal tax rate – whereas under the legacy system they saw both their HB and WTC (or CTC) withdrawn simultaneously, under UC that benefit alone is being withdrawn at a single rate. For this reason, working renters tend to gain from the switch to UC (Brewer, Joyce et al., 2019). This follows fairly directly from the fact that UC integrates strands of support that separately applied means tests to low-income workers and to renters – collapsing two phase-outs into one for those who are both low-income workers and renters.

Figure 4. Amount lost in increased taxes and withdrawn benefits when earnings increase by £1, for the example lone parent in Figure 3 when working 30 hours per week

Note: See Figure 3.

Source: Authors’ calculations.

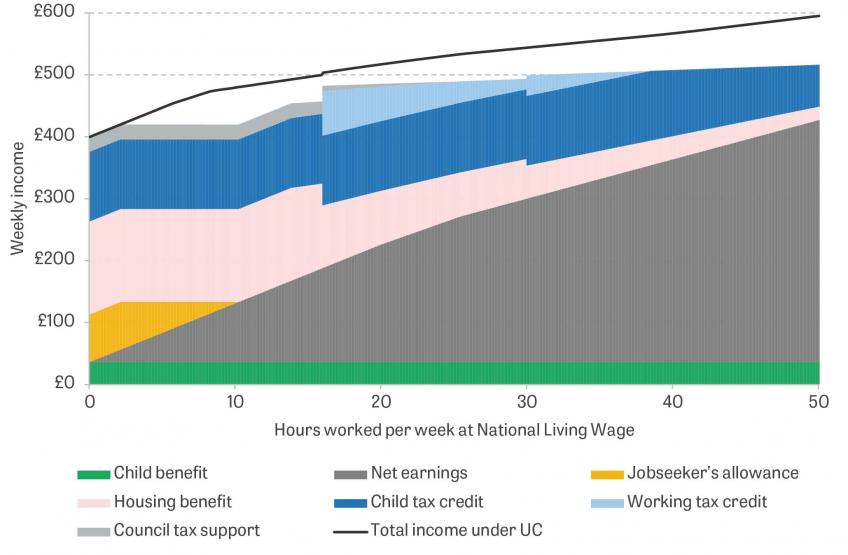

Figure 5 shows incomes for an otherwise-identical lone parent who owns their own home. Because they are not a renter, they are not eligible for HB or the housing element of UC, meaning that their entitlements are quite a bit lower. This also causes a key difference in how they are treated by UC. Under the legacy system, they only see their tax credits (WTC first, then CTC) withdrawn as they increase their hours above 16 – meaning that their effective marginal tax rate is lower than that for the renting lone parent. But under UC, they face the same effective marginal tax rate as the renter because UC has a single withdrawal rate for homeowners and renters alike (though homeowners get a somewhat higher work allowance). Because of this, working homeowners tend to lose from the switch to UC and face higher effective tax rates than under the legacy system (Brewer, Joyce et al., 2019).

Figure 5. Weekly income for an example lone parent homeowner with two children earning the National Living Wage

Note: Example family is as in Figure 3, except they own their own home rather than rent.

Source: Authors’ calculations using TAXBEN, the IFS tax and benefit microsimulation model.

These examples have focused on a lone parent, and things would look similar if we examined couples with children. However, those without children are generally entitled to little in work, especially under the legacy system. In principle, they could get WTC if they worked 30 hours per week. But a worker without children working 30 hours per week at the National Living Wage earns enough that, when the WTC means-test is applied, they are ineligible anyway – so only a low-earning self-employed worker, with an implicit hourly wage below the National Living Wage, would be eligible5. If their rent were, say, £100 per week, they would also have seen their HB tapered to zero. Because UC distributes more to renters and does not have hours rules, it is easier for single people without children to receive some support in work, though the sums remain relatively small.

Application and payment

To claim, benefits claimants typically fill in forms and provide evidence to prove that their circumstances are as they state (e.g. payslips to show their earnings). They are required to provide differing sorts of information depending upon the benefit in question. For example, an application for housing benefit requires the claimant to give their rent level, since their entitlement is related to their rent. For this reason, the means-tested benefits tend to require more information than the non-means-tested ones, since the government needs to collect information on different sources of income and sometimes assets. Under the legacy benefits system, claims were often made on paper forms. Applications for universal credit are generally made online (a feature that became extremely useful during the pandemic, when a huge volume of new claims needed to be processed during a time of social distancing), though those without access to the internet can apply over the phone.

Claimants to disability or incapacity benefits typically need to have their condition assessed before they can receive the benefit. The assessor then makes a determination as to whether the condition prevents the claimant from working (incapacity benefits) or means that they have difficulty with doing everyday tasks (disability benefits). These decisions can be appealed by the claimant, sometimes more than once. Of ‘work capability assessments’ for ESA that do not result in the claimant being awarded the highest level of eligibility, 30% are appealed once (called a ‘mandatory reconsideration’) and 8% are appealed twice6.

Benefit payments are generally made into the bank account of the claimant. One important exception is housing benefit, which is often paid directly to the landlord, especially for tenants in social housing – though this option is generally not available under UC. Payment frequency varies between benefits; under the legacy system, a claimant could receive JSA weekly or fortnightly, while tax credits were usually paid four-weekly. Under UC, there is a single payment frequency of a month. This change can have important consequences, a point we discuss in Section 7.

The fact that so much of the UK’s system is either means-tested (as discussed more fully below) or health-related means that the role of assessment and/or judgement in determining who gets what is relatively large. This is a corollary of having a targeted system that is clearly trying to siphon support to those it deems most in need, though it also opens the door to some of the pitfalls of welfare policymaking when it comes to the well-being of those trying to navigate the system and the reliability with which the intended recipients of support actually get it. This is discussed elsewhere in the chapter, and in much greater depth in the accompanying commentary by Patrick (2023).

Means-testing

One feature that stands out from the short description of the working-age transfers system given above is that it is overwhelmingly a means-tested system: entitlements are focused on those with low current financial resources relative to (proxies for) needs, and are mostly independent of past circumstances. In fact, in 2019–20 62% of benefit expenditure was on means-tested benefits. In Section 3, we describe how the UK got to that point and show that, while this is a common way to design cash transfers, it has not always dominated the UK system as it does now, and nor are other countries’ systems typically so dominated by it. In fact, almost every other country in the OECD has some ‘contributory’ benefit system, where those who have ‘paid in’ more during working life get higher benefit entitlements in the early phase of unemployment. Two associated commentaries (Crafts, 2023; Timmins, 2023) discuss some of those issues in considerably more depth.

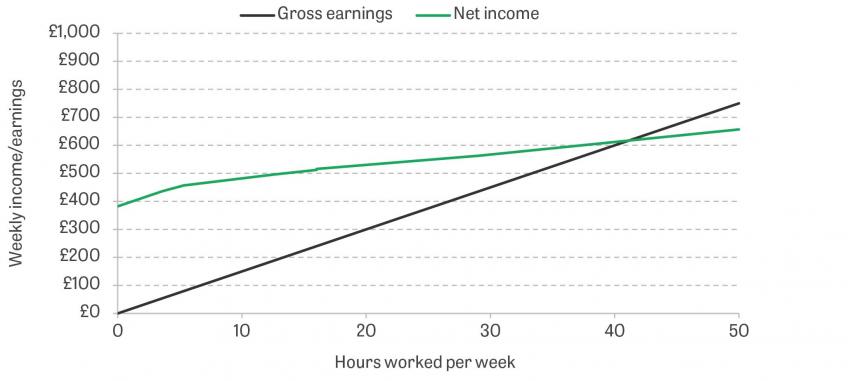

Of course, the switch to universal credit does not (despite the potentially misleading term ‘universal’) get us away from any of the main trade-offs associated with means-tested forms of support. These have been noted, and agonised over, for many decades (see the Beveridge Report (Beveridge, 1942), Dilnot, Kay and Morris (1984), the Mirrlees Review (Mirrlees et al., 2011) and Moffitt (2023)) – but before proceeding to the rest of the chapter, it is worth recapitulating them very briefly. A classic trade-off is achieving redistribution versus not dampening work incentives. This can be seen in Figure 6, which shows gross earnings and net income (after taxes and benefits) for an example household (a single parent renter with two children, who can earn £15 per hour). If they work few hours – and therefore have low earnings – the tax and benefit system attempts to shield them from the very lowest living standards by redistributing to them. If they work and earn more, the extent of redistribution – as measured by the gap between the two lines – falls, and at around the point when they move to full-time work the system takes more away in taxes than it gives back in benefits. In broad terms, then, this sort of structure takes from higher-income families and gives to poorer ones. This inevitably distorts work incentives. In the absence of a tax and benefit system, if they worked one more hour they would receive an extra £15. But with the tax and benefit system, they generally receive less than that – in fact, above about 12 hours of work, an extra hour only increases their net income by roughly £47. If the value they place on an extra hour of time off work is more than £4 but less than £15, then their decisions have been distorted: without the tax and benefit system, they could work another hour and be better off (since they value that time at less than what they would be paid). But the incentives created by the tax and benefit system, and in particular the consumption floor with benefits available at zero hours of work, prevent this from happening.

Figure 6. Gross earnings and net income for an example household

Note: Example household is a lone parent with two children aged under 5, who earns £15 per hour, lives in a band D council tax property in an area with average council tax, is a social renter and has a rent of £150 per week. Net income is calculated using the April 2022 tax and benefit system. Net income is equal to gross earnings minus income tax, employee National Insurance contributions and council tax, plus universal credit, child benefit and council tax support.

Source: Authors’ calculations using TAXBEN, the IFS tax and benefit microsimulation model.

Providing households with insurance against shocks to their income is typically at tension with protecting their financial incentives to work, for very similar reasons to those for why redistribution and work incentives are at tension: if the benefits system reduces the difference in an individual’s income between a situation where they earn little and a situation where they earn a lot, it simultaneously provides them with insurance against low earnings and weakens their financial incentive to earn more.

The trade-off between redistribution or insurance and work incentives is inherent within means-testing – though the extent to which people’s choices are actually affected by those incentives is an empirical question, and one that we cover in Section 4. But there are other features (or, perhaps more aptly, bugs) that have a tendency to come with means-testing too, and hence which are also a key part of the discussion of the UK’s welfare system. These include social stigma, the hassle and informational requirements of claiming, and the ‘relational’ inequality that might result when entitlement to support depends on the judgement of the government or bureaucrats about what someone ‘needs’ or whether someone is doing what is required of them (see Patrick (2023)). In turn these factors may affect how much of the means-tested entitlement is actually claimed and hence its ability to support people as intended.

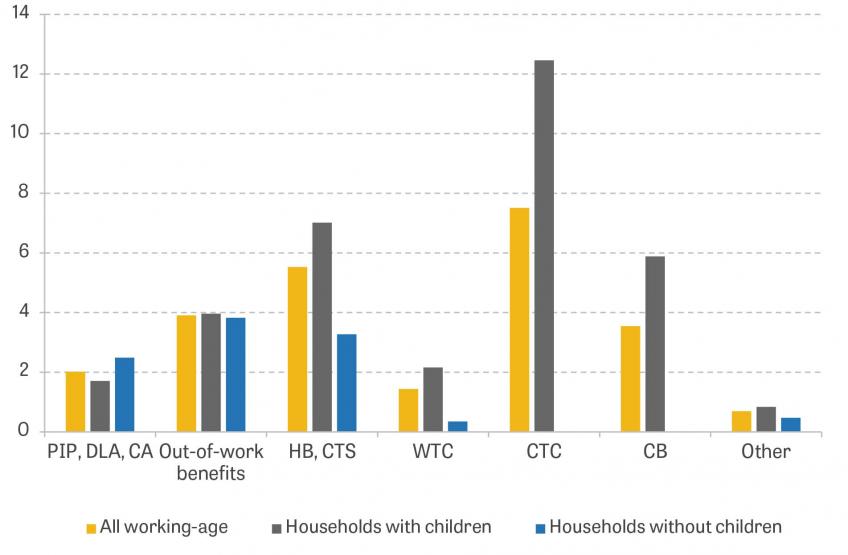

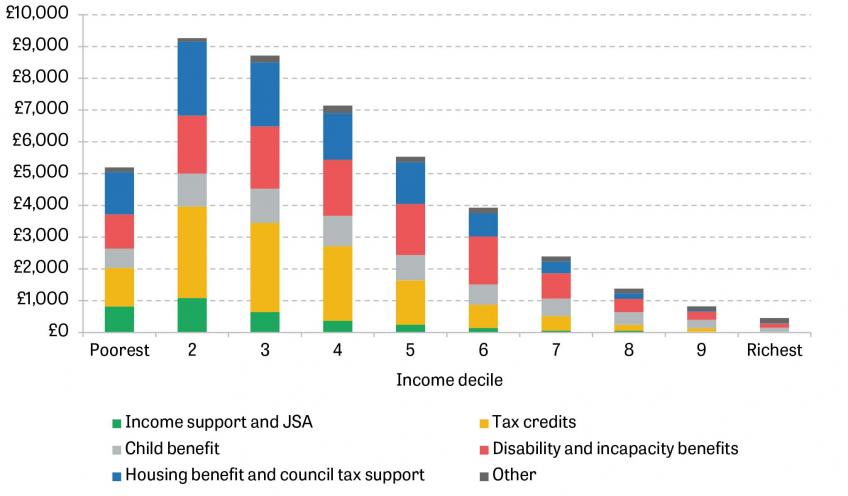

As well as affecting incentives and insurance, the existence of means-testing of course directly determines whether poor or rich households receive transfers. Figure 7 shows the average receipt per household of different transfers across the income distribution. In general, poorer households receive much more than richer ones. This is true overall, and for each individual category of benefit (except for ‘other’). The one nuance to that story is that the lowest-income decile receive less than the second. This is partly because some people are entitled to benefits due to having little or no other income, and yet they do not claim them, and this tends to put precisely such households at the very bottom of the income distribution; in addition, survey respondents under-reporting the benefits they receive will tend to have the same effect. There are also those with a low income who are not entitled to much in terms of benefits, such as those with a significant amount of assets who are out of work.

Figure 7. Average annualised receipt per working-age household across the income distribution

Note: Income deciles are calculated using equivalised household income, at the individual level. Universal Credit is categorised as ‘Income support and JSA’. Benefit receipt is usually measured at a weekly, fortnightly, four-weekly or monthly level; the figure shows the annualised equivalent. Households are ranked into deciles using the whole population; averages are taken among working-age households only.

Source: DWP’s ‘Households below average income statistics’ 2016–17 data, in 2021–22 prices.

3. How has the role of the system changed over time?

In this section, we examine how the role and design of the cash transfer system have shifted over time, thanks to both policy reforms and wider changes in the UK’s economy and society. In general when documenting longer-run trends at a high level, we examine the period since the mid 1970s, over which we have comprehensive administrative data on benefits. When looking in more detail at the drivers of trends and how they relate to policy, where we typically need to use the additional information provided by survey data, we focus our attention on the mid 1990s onwards, as the Family Resources Survey – used for much of this analysis – began in 1994–95. We often stop our analysis at 2019–20 to abstract from temporary distortions resulting from the pandemic, though where data sources go up to 2022–23, we include those years.

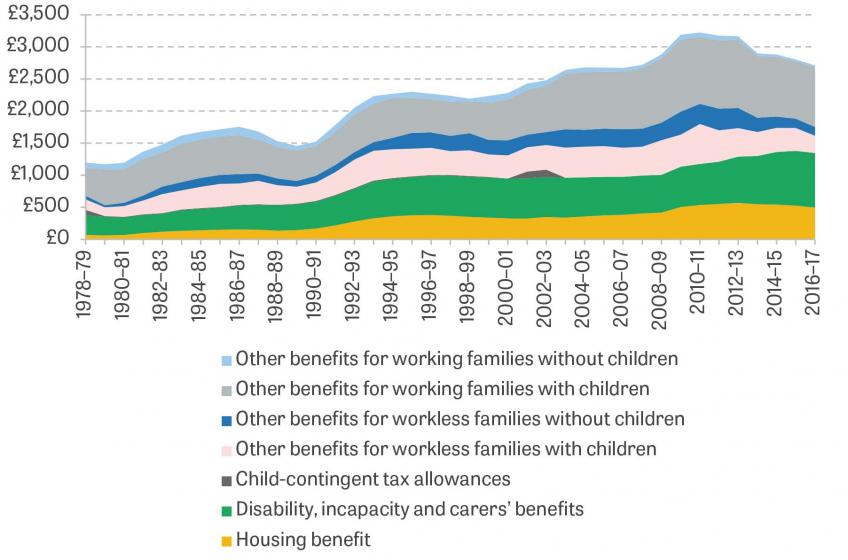

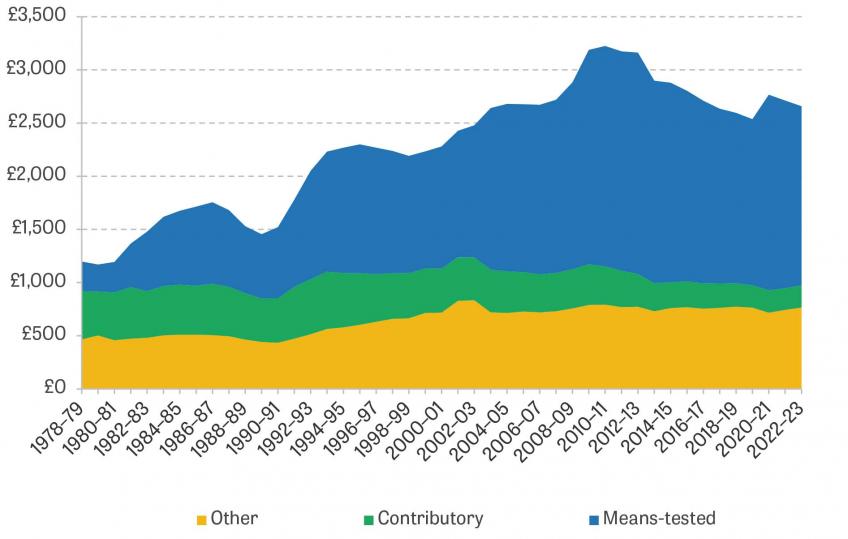

The net effect of the changes in the system and the wider economy is summarised by Figure 8, which decomposes real per-capita working-age benefit spending according to its ‘purpose’8. We plot the cost of housing programmes as well as the cost of programmes to support claimants with disabilities. The remaining benefits bill is divided according to whether the recipient family has children and contains at least one adult in paid work. Between 1978–79 and 2016–17, the vast majority of the growth in spending has come from three broad areas: housing benefits (in yellow on the figure); health-related (disability, incapacity and carers’) benefits (in green); and other benefits for working families with children (principally tax credits and their forebears, and child benefit; in light grey).

As already hinted, these patterns are driven both by changes in the economy and wider society, and by explicit policy reforms – which themselves are often in response to those economic and social changes. Even over just the past 25 years or so, which is the focus of most of our discussion, families’ circumstances have changed quite dramatically – particularly their working patterns and housing.

Figure 8. Working-age benefit spending (2021–22 prices) per capita

Note: Universal credit is treated as an ‘other benefit’, though some of the expenditure is to cover housing costs or to support carers or those with an incapacity. ‘Child-contingent tax allowances’ are any reductions in income tax liability induced by the presence of children, and include child tax allowances, the additional personal allowance, and children’s tax credit. There are no such allowances from 2003–04 onwards. We include data only up to 2016–17, as after that the increasing prevalence of universal credit makes it difficult to examine trends in spending by purpose.

Source: Authors’ calculations using DWP, ‘Benefit expenditure and caseload tables, Autumn Budget 2021’; TAXBEN, the IFS tax and benefit microsimulation model; Family Resources Survey, 1994–95 to 2016–17; and Family Expenditure Survey, 1978 to 1993.

Pensioners and working-age adults

The core focus of this chapter is on the working-age benefit system, but it is worth briefly discussing the way in which its size has changed relative to the system for pensioners.

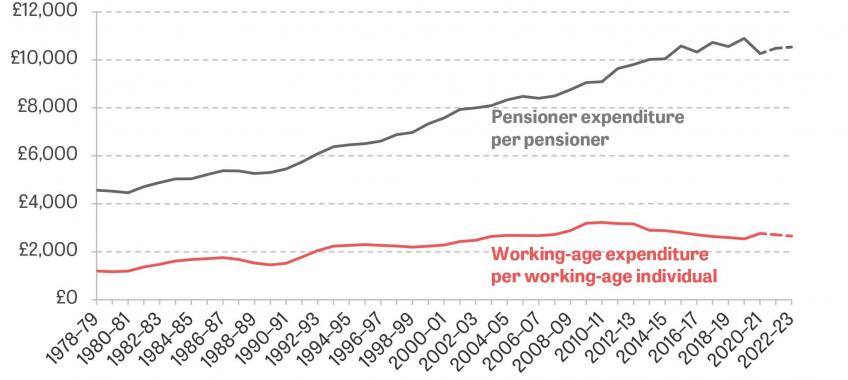

As shown in Figure 9, the total working-age benefit bill has generally grown over time, although not without exception. Real spending per working-age adult rose from around £1,200 per year in the late 1970s to £3,200 in 2010–11, before falling back to £2,500 just before the pandemic. By contrast, pensioner spending has steadily risen, including during the 2010s. On the eve of the pandemic, the working-age benefit bill made up 4.3% of national income, while the pensioner bill accounted for 5.5%. That 1.2 percentage point gap is around the highest since comparable records began in 1978–79, and has steadily grown since the mid 1990s. This partly reflects the ageing population, but also policy change – over the past decade or so there have been significant cuts to the working-age benefit system, while pensioner benefits were largely protected or increased.

Figure 9. Benefit expenditure per capita (2021–22 prices)

Note: For this figure, ‘working-age’ is defined as being under the female state pension age (even for men) and ‘pensioner’ is defined as being above it – this is how the administrative data are presented, as the female state pension age is when historically both men and women have become eligible for means-tested pensioner benefits. Figures for 2021–22 and 2022–23 are projections.

Source: Authors’ calculations using DWP’s ‘Benefit expenditure and caseload tables, Autumn Budget 2021’ and ONS’s ‘Population estimates for the UK and constituent countries by sex and age’.

As a consequence of these changes, the basic support for a single person with no other source of income is now 137% higher for those just over pension age than for those just under it. Back in 1990–91, that figure was 32%. Hence, while this chapter discusses the design of working-age cash transfers, the priority given to transfers made in the working-age portion of life versus those made during retirement is itself an important choice, and has in recent years helped shape the austere context within which working-age transfer policy is made.

Indeed, the current policy of increasing the state pension (the main – now almost universal – state transfer to pensioners; broadly the UK’s equivalent of the US’s Social Security) each year by the highest of inflation, earnings growth and 2.5% (a policy known as the ‘triple lock’) may well also cause a significant intergenerational transfer: in the limit, this policy is not sustainable (it implies pensions becoming an ever-increasing share of national income), and it is possible that the population currently of working age will not all end up benefiting in full from the same generosity.

Working and workless families

There have been significant changes in household employment over recent decades, as well as a shift in how policy treats household employment.

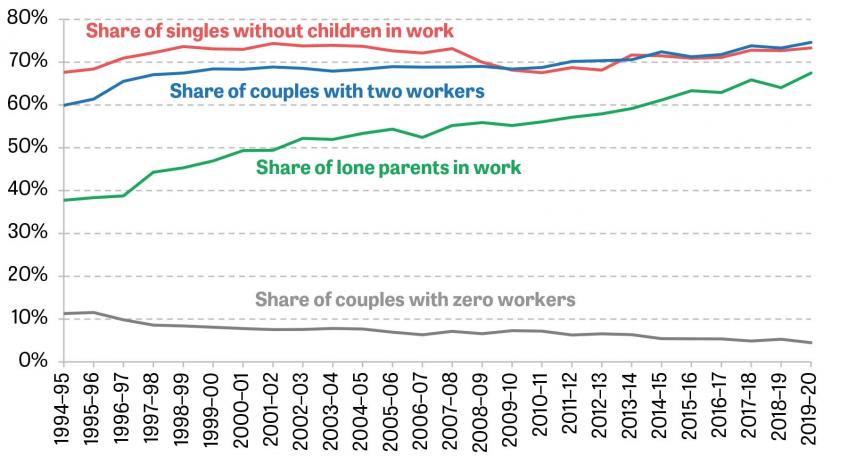

An important factor here is the rising rate of female employment (from 53% in 1971 to 63% in the mid 1990s to 73% on the eve of the pandemic). A particularly pertinent shift from the point of view of the transfer system has been a sharply increasing employment rate among lone parents (the vast majority of whom are mothers), which, as Figure 10 shows, has almost doubled from 38% in 1994–95 to 67% in 2019–20. Among couples, the proportion in which neither partner is in paid work has halved over the same period, from 11% to 5%. Together these changes have led to a declining rate of household worklessness. Moreover, the rising female employment rate – combined with little change in the male employment rate – has also meant that the share of couples in which both partners work has steadily increased.

Figure 10. Work status of working-age families

Note: Excludes families entirely comprised of full-time students.

Source: Authors’ calculations using the Family Resources Survey, 1994–95 to 2019–20.

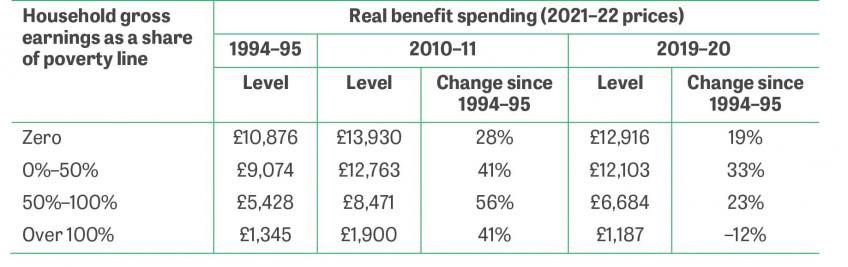

Table 2. Real benefit spending per household per year (2021–22 prices), split by household gross earnings as a share of the relative poverty line

Note: ‘Earnings 0%–50% of poverty line’ only includes those with strictly positive earnings. Excludes households comprised entirely of students.

Source: Authors’ calculations using Households Below Average Income, 1994–95 to 2019–20.

A rising share of families with someone in paid work automatically tends to mean a rising share of transfers supporting families with someone in paid work (from 31% in 1994–95 to 48% in 2019–20). But there have also been deliberate shifts in policy which reinforce that pattern, especially through tax credits. This can be seen in Table 2, which takes broadly representative survey data on the income sources of UK households, groups households according to what fraction of the (relative) poverty line their gross (i.e. pre-tax-and-transfer) earnings make up, and shows mean real benefit receipt for each group – in three selected years. Over the past 25 years, benefits for families in work with low earnings have climbed faster than for other groups – both those out of work and those on higher earnings levels. Benefits in families with gross earnings exceeding the poverty line have declined in real terms by 38% since 2010–11 – a consequence of the more aggressive means-testing of benefits that reach high up the distribution that we describe at the end of this section.

One corollary of shifting support more towards working families on low earnings is that families have greater financial incentives to have someone in work. Indeed, this was always one of the major goals of the expansion of tax credits, and the next subsection elucidates further the work incentive effects. It is worth noting that the goal of encouraging paid work more through the welfare system has also been pursued through non-financial means, with strengthened use of job-search requirements (‘conditionality’). There is good evidence that these policy changes have themselves been partly responsible for changes in employment patterns. In particular, tax credit reforms in the early 2000s increased employment among lone parents (by around 5 percentage points (Brewer et al., 2006))9, as did the expanded use of job-search conditionality from 2008 (Avram, Brewer and Salvatori, 2018; Codreanu and Waters, 2023).

A consequence of focusing more on (means-tested) in-work support is that the transfer system provides a good deal of insurance against a decline in earnings for those who remain in work (since, if the worker is on benefits, the earnings loss is to a significant extent replaced by higher in-work transfers). Conversely, as the out-of-work safety net has not kept pace with growth in earnings, the system now provides less insurance against employment loss than it used to. This is compounded by the lack of earnings-related benefits in the UK, particularly for those not on the lowest earnings – having previously been in a mid- or high-earning job typically does not buy additional support upon job loss, unlike in many other countries. Families without children have especially low earnings replacement rates, as their out-of-work benefit entitlements have barely changed in real terms for half a century while earnings have doubled. Bourquin and Waters (2020) show that a single childless worker on average earnings in the UK can expect to receive 13% of their in-work income when they lose their job; across the OECD, the average is 55% (if they had been in work for the past 21 years).

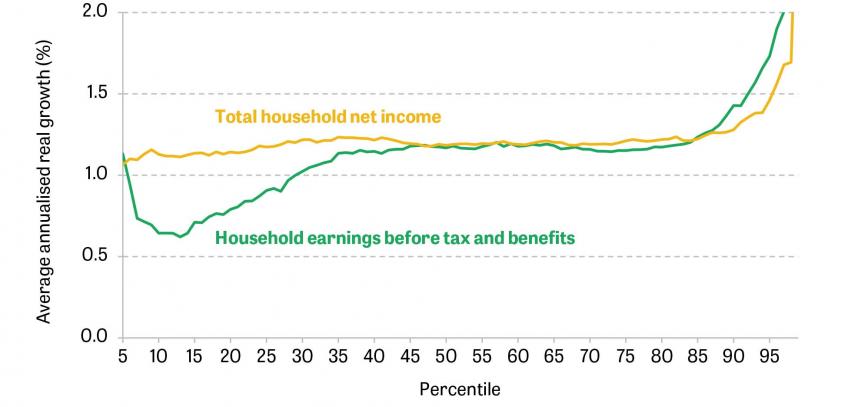

The growth of in-work benefits has had profound consequences for the distribution of income. Figure 11 shows changes in the distribution of household earnings before taxes and benefits, and after tax and benefit net income, between 1994–95 and 2019–20 for working households. (Note that a larger share of households were working in 2019–20 than in 1994–95.10) Inequality in gross earnings before tax and benefits has clearly risen. Earnings at the 10th percentile grew by an average of 0.6% per year over the period, compared with 1.2% at the median and higher still above the 90th percentile. But once we account for taxes and benefits – i.e. move from the green to the yellow line – the change in income among the bottom 90% or so is almost completely flat. In other words, in-work benefits have (outside the top 10%) completely offset the increase in earnings inequality among those households with someone in paid work. As Cribb, Joyce and Wernham (2022) show, the opposite has happened if we focus specifically on the austerity period since 2011, when the transfer system has been cut back (see final subsection of this section).

Figure 11. Annual growth in household gross earnings and net income, by percentile, 1994–95 to 2019–20

Source: Cribb, Joyce and Wernham, 2022.

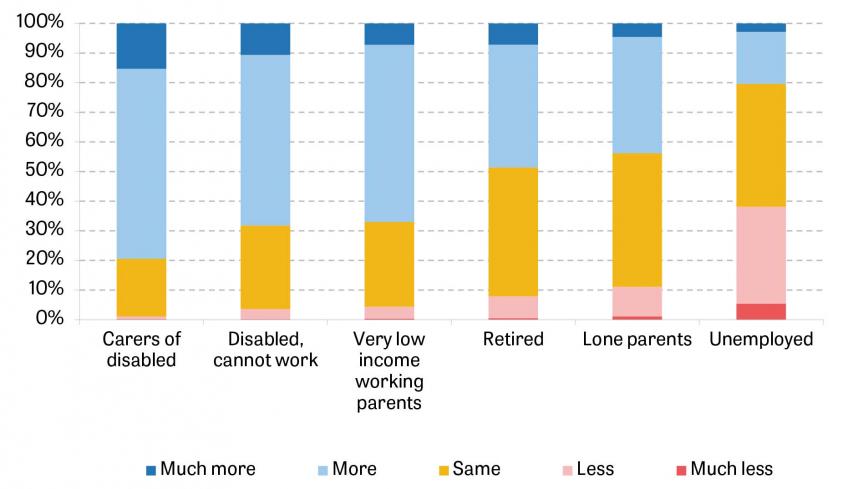

Figure 12. Share of people who support higher or lower benefit spending on different demographic groups

Note: Question asks ‘Would you like to see more or less government spending than now on benefits for …’. Those who refused to answer the question or stated ‘don’t know’ are excluded.

Source: Authors’ calculations using British Social Attitudes Survey 2017.

Perhaps part of the explanation for the little change seen in basic out-of-work benefits, alongside the expansion of in-work support, is the political preferences of voters. Figure 12 shows the shares of the population who support more or less benefit spending on different demographic groups (in 2017 – the latest time these questions were asked). The groups with the greatest support for more spending are the disabled and their carers. But there is also a high degree of support for spending on ‘very low income working parents’ – two-thirds of respondents support spending more, against just 4% who support spending less. The only group where, on average, people support reducing benefits is the unemployed (20% support more versus 38% less). These questions have been asked intermittently since 1998, with not much change in levels of support (with the exception of the retired, for whom support for extra spending has fallen quite significantly). Given these preferences, the shifts in the shape of the system towards those in work are perhaps not surprising.

Part-time work and full-time work

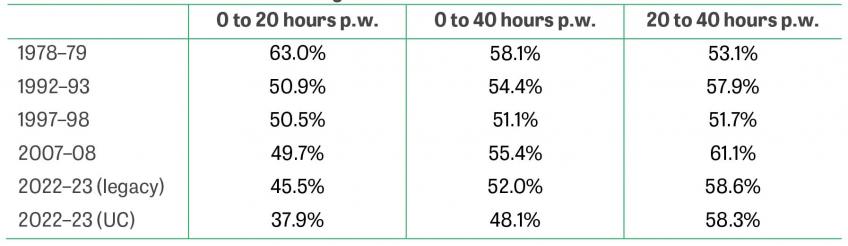

An important aspect of the expansion of in-work benefits is that it has been concentrated more on those who work part-time than on full-timers (for the purposes of this chapter, we define ‘part-time work’ as working fewer than 30 hours per week). For example, under the legacy benefits system, lone parents must work at least 16 hours per week to be eligible for the work-related element of tax credits, but due to the means-testing of tax credits effective marginal tax rates when moving beyond 16 hours of work per week have been very high for many workers.

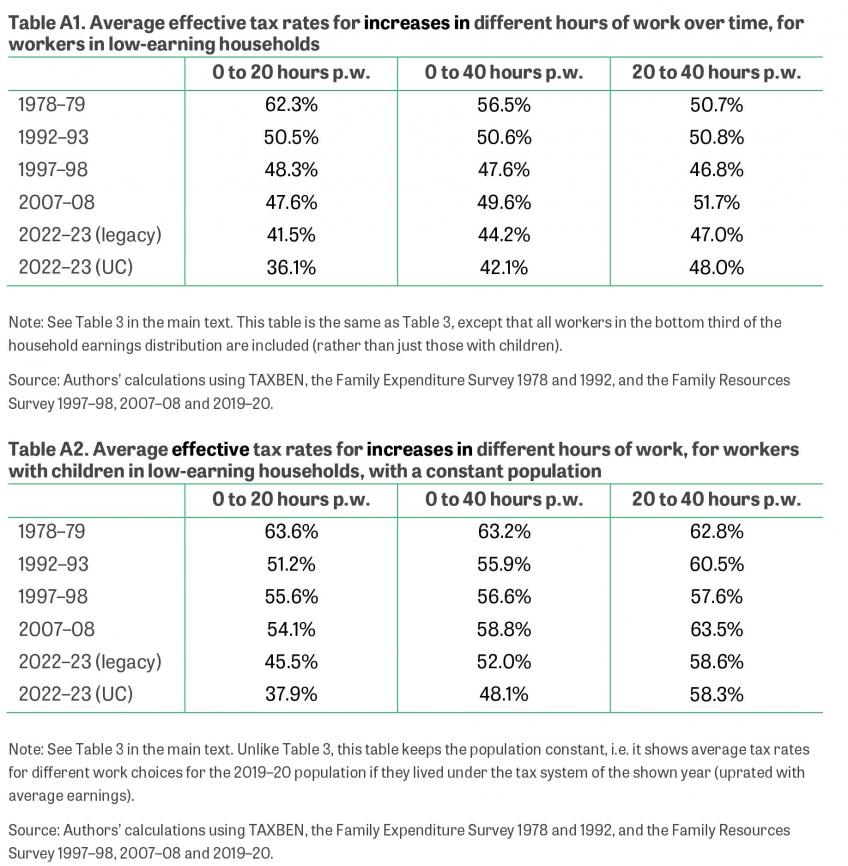

This can be seen in Table 3. Here we focus on workers with children who are in the bottom third of the household earnings distribution (among households in work) – loosely speaking, those whom in-work benefits are largely distributed to (the equivalent table for all workers in households in the bottom third of the earnings distribution is Table A1 in the appendix). We take a representative sample of this group in each year from household survey data, and compute the average effective tax rates they would face when changing their hours of work, due not only to taxes on earnings but also to the withdrawal of means-tested benefits (Table A2 in the appendix is an equivalent of this where the population is kept constant and so only incorporates the effects of policy reforms). The ‘0 to 20 hours’ column, for example, shows the average share of gross earnings that is clawed back in the form of higher taxes or lower benefits when an individual moves from working 0 to working 20 hours per week. Higher tax rates represent a weaker incentive to change hours in the way described. The first two columns show tax rates at the extensive margin – the move from out of work to in work. The third shows tax rates at the intensive margin – in this case, moving from part-time to full-time work.

Table 3. Average effective tax rates on different increases in hours of work over time, for workers with children in low-earning households

Note: The ‘legacy’ and ‘UC’ rows show tax rates under the assumption that the UC roll-out has not yet begun or has been completed, respectively. Sample is workers with children living in households in the bottom third of the household gross earnings distribution (among households in work). For the 2022–23 rows, we use the tax-benefit system in that year deflated to 2019–20 terms using average earnings, and simulate tax rates using the 2019–20 Family Resources Survey data. We account for the threshold change in National Insurance contributions implemented in July 2022 by using the average threshold across the fiscal year.

Source: Authors’ calculations using TAXBEN, the Family Expenditure Survey 1978 and 1992, and the Family Resources Survey 1997–98, 2007–08 and 2019–20.

Since the late 1970s, there has been a very significant decline in extensive margin tax rates for workers with children in low-earning households (and, as we show in Table A2, this is largely driven by reforms rather than changes in the population) – consistent with the evidence in the previous subsection that the system has shifted towards in-work rather than workless families, and driven primarily by a large expansion of work-contingent support through tax credits and their forebears. Since the Great Recession, extensive margin effective tax rates have fallen further due to reductions in income tax rates and benefit cuts. By contrast, intensive margin tax rates have changed much less – today they are around where they were in the early 1990s, and in fact above their level in the late 1970s. In other words, the system has indeed shifted towards more strongly incentivising part-time jobs over not working, while generally weakening the incentives to move from part-time to full-time work. Table 3 also shows that the introduction of universal credit reinforces this, considerably strengthening incentives to work part-time on average, but with little change in the incentive to move from part- to full-time work11. The evidence suggests that people have responded accordingly – a majority of the increase in employment that the tax credit reforms precipitated was in part-time work (Blundell et al., 2016).

The increased use of job-search conditionality is also again worth mentioning as something that has reinforced a wider trend in the direction of welfare policy. The expansion of conditionality for lone parents did result in more doing paid work, as we discuss in Section 4, but it was essentially entirely part-time work and on low earnings.

Families with and without children

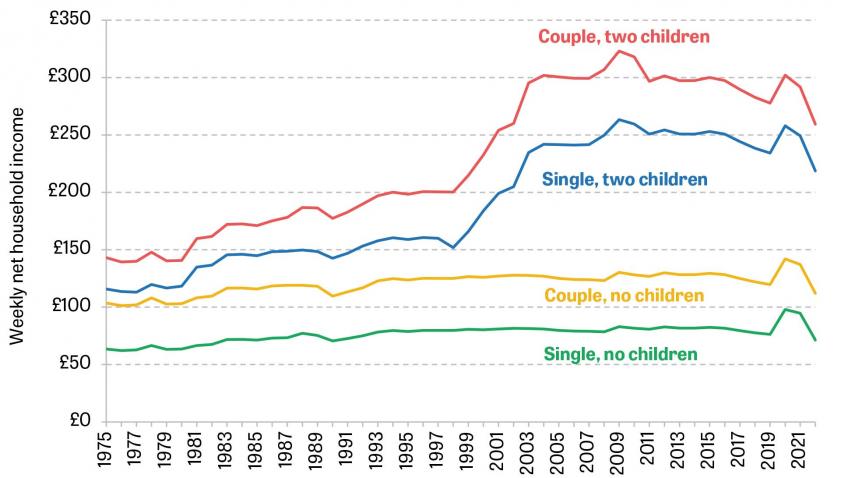

Much of the expansion of means-tested benefits has occurred via increased spending on families with children. This can be seen in Figure 13, which shows real out-of-work income for hypothetical families with no earnings, disabilities or housing costs, under different tax and benefit systems. Until the temporary increase to UC rates implemented during the pandemic (discussed in Section 2), there had, remarkably, been virtually no real-terms change in out-of-work benefit entitlements for families without children over the past half-century. Conversely, benefits for families with children had been considerably expanded. The increases in the out-of-work safety net are, over the period as a whole, roughly equivalent on average to having indexed their benefits to earnings (rather than the actual default of price indexation). Whereas in 1975–76 a couple with two children would get just 38% more than an otherwise-similar couple without children when out of work, by the eve of the pandemic that gap had increased to 132%.

One way of putting these differentials into some context is to compare them with the assumed differences in the needs of different family types implied by official measures of incomes, and income poverty. Income statistics (including the official ones produced by the government) use ‘equivalence scales’ to try to account for the different needs of different-sized families. These scales imply that the couple with two children would need 40% more income than the couple without any in order to have the same current living standard, all else equal – about the gap seen in the mid 1970s, but much smaller than the one present today. Of course, there are plausible justifications for distributing more to families with children than to those without (discussed in more detail in Section 10) that go beyond the economies of scale with respect to current living standards – in particular, impacts on the future life chances of the children. In addition, the equivalence scales themselves should not be taken as an infallible benchmark for relative need: it is notoriously difficult to identify the ‘correct’ equivalence scales.

Figure 13. Net household income over time for out-of-work families, by family type (2021–22 prices)

Note: Figure shows net incomes out of work under the April tax and benefit system of the corresponding year. There were temporary increases to universal credit in April 2020 and 2021 because of the COVID-19 pandemic. To put 2022 into 2021–22 prices, the Office for Budget Responsibility’s March 2022 forecast for CPI is used. The figure assumes that the households are owner-occupiers with no other source of income, two children, one of whom was born before April 2017, and no disabled members and have all their council tax covered by council tax support.

Source: Updated from Bourquin and Waters (2020).

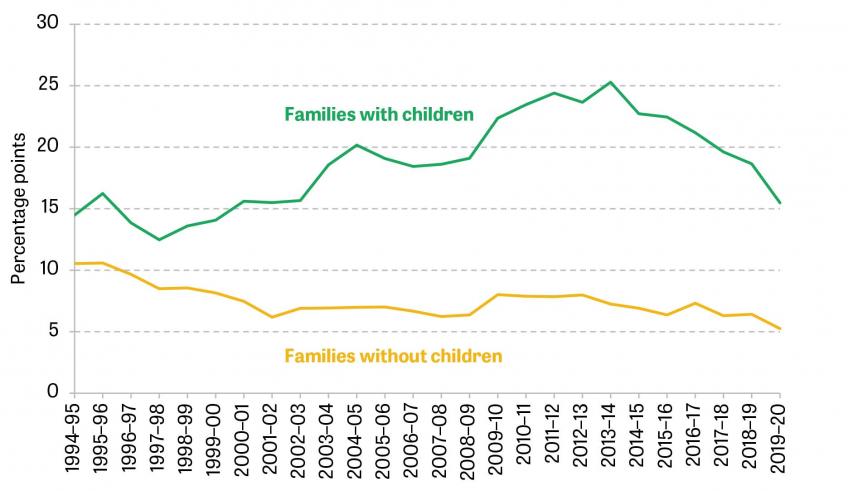

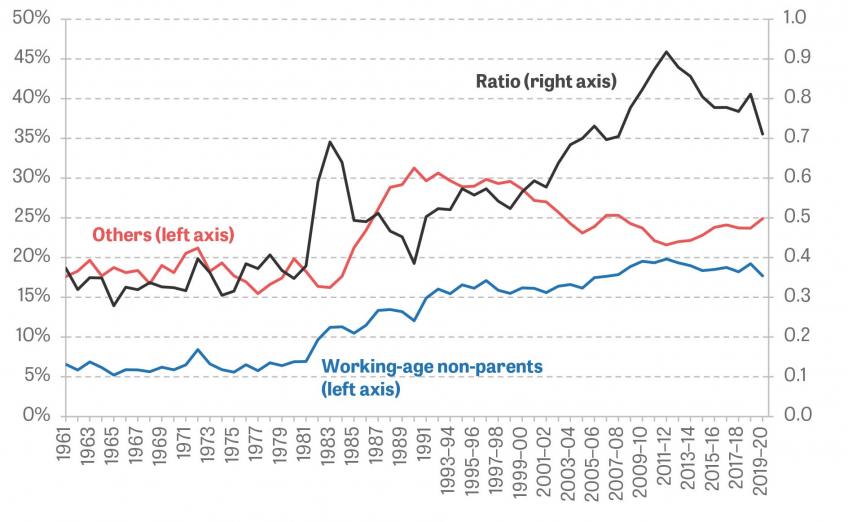

Figure 14 provides another way to see the increased emphasis of the benefit system on those with children. It shows the mechanical contribution of benefits to reducing poverty – that is, if all benefits were abolished and nothing else changed, how much would poverty go up by? In 1994–95 the mechanical effect of the benefit system on relative income poverty (where the poverty line is 60% of median income) was 14 percentage points (ppts) for families with children and 11ppts for those without12. But as the benefit system increasingly shifted towards those with children, the mechanical effect on their poverty rate increased, while it fell for those without children. More recent benefit cuts have lessened the impact of benefits on poverty for those with children, but the differential remains large, at 15ppts and 5ppts respectively. Given these trends, it is perhaps not surprising that poverty has become increasingly concentrated among those without children (see Figure A1 in the appendix): in the 1960s and 1970s, the working-age non-parent poverty rate was only about a third of that for others, but from 1980 the ratio started to steadily increase, and by 2011–12 the rates were almost the same. Again, retrenchments to benefits since then have slightly pushed the rates apart, and larger families in particular have seen a sharp rise in poverty (Cribb et al., 2022). This is at least in part a consequence of two policies: the benefit cap, which places a limit on the amount of benefits that some families can receive (and so tends to affect renters with several children, who typically receive more than other family types), and the so-called ‘two-child limit’, which means that third and subsequent children do not generate extra tax credit or universal credit entitlement. A detailed discussion of the impact of these policies on child poverty is available in Stewart, Patrick and Reeves (2021). In addition, Reeves et al. (2020) show that the benefit cap had a sizeable effect on mental illness.

Figure 14. Mechanical effect of benefits on working-age relative poverty rates

Note: Excludes households comprised entirely of students.

Source: Authors’ calculations using Households Below Average Income, 1994–95 to 2019–20.

The trends in relative spending on those with and without children are dominated by deliberate policy changes, rather than underlying changes in the population: the fractions of low-earning families (bottom 40% of the equivalised family earnings distribution) made up by lone parents and couples with children have consistently hovered around 12% and 31% respectively for the past 25 years.

Support for housing costs

Since the inception of the welfare state, the issue of housing costs, including their wide variability across the country and the relatively large share of income that poorer people typically spend on housing, has challenged policy. As we shall see, in modern times the challenge has been accentuated by key changes in the wider housing landscape, including rapid growth in private renting.

Today, the UK benefit system’s support for housing costs is mainly targeted at low-income renters13. Some homeowners are entitled to Support for Mortgage Interest (SMI), but eligibility criteria are tight (limited to those out of work who have been claiming some means-tested benefits for at least nine months), support covers only interest repayments rather than principal repayments, and as of 2018 SMI is a loan rather than a grant. For this reason, we focus on renters in this subsection14. Importantly, in addition to being eligible for cash support for their rental costs, renters in social housing (those who rent from a housing association or local council) generally also receive support in the form of below-market rents (for more on this, see Adam et al. (2015)). Here we focus only on the direct cash subsidy – housing benefit.

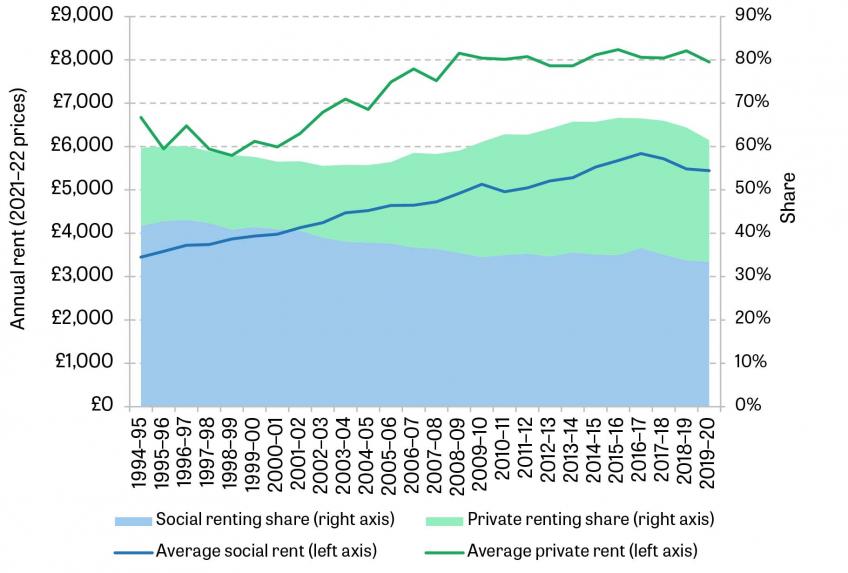

Figure 15 shows housing trends for working-age households in the bottom 40% of the (post-tax/transfer) household income distribution in each year. We choose the bottom 40% simply as an approximation for the part of the population that are often eligible for benefits, though some households inside that group will be ineligible and some outside will be eligible. The sum of the areas in the figure shows that there has been an overall shift towards renting (and hence away from owner-occupation) among low-income households, as there has been for society at large. This comprises a rapid increase in the size of the private rented sector, more than offsetting the long-term decline of social housing. Both private and social rents have increased in real terms over the period, but the growth has been significantly larger among social renters (58% versus 19% since 1994–95).

Figure 15. Housing tenure composition and average rent of working-age households in the bottom 40% of the income distribution

Note: Social and private rents are deflated using the Households Below Average Income before-housing-costs deflator. The figure shows average rent and tenure composition among the poorest 40% of households in each year, as measured by gross income excluding housing benefits.

Source: Authors’ calculations using Households Below Average Income, 1994–95 to 2019–20.

The combination of these trends means that over the past 25 years the amount spent on rent has increased by 53% in real terms on average among all lower-income households (including owner-occupiers, who of course pay zero rent). The most important factor contributing to this change is the increase in social rents (contributing 31ppts), followed by the increase in relative prevalence of private renting (14ppts), followed by the increase in private rent levels (9ppts).

This steady rise in real rents over the past 25 years has added around £5 billion to the annual working-age housing benefit bill (out of a total of around £20 billion15), and has pushed receipt of housing-related benefits further up the income distribution. By 2019–20, one in every three working-age renting families was in receipt of housing benefit or the housing element in UC.

In summary, this is a leading example of where wider trends in the economy and society can radically change what is required of the benefits system. While rising rents and the shift towards private renting continue, policymakers have to either accept an ever-increasing housing benefits bill or leave a growing fraction of the low-income population highly exposed to high housing costs, or some combination. In reality, both have happened. Among low-income private renters, just 8% now have all their rent covered by housing benefits, compared with almost half in the mid 1990s. For 32% of them, the amount of rent not covered by housing benefits eats up at least one-third of their (non-housing-benefits) income – a situation faced by just 14% of the group in the mid 1990s (Bourquin and Waters, 2020). Despite this, working-age housing benefit spending per capita increased by 38% between 1994–95 and 2016–17 (Figure 8). While these housing trends continue, there can be no easy answer for transfer policy. The very latest response from the government has been to nominally freeze the maximum support that private renters can get for housing costs (after raising these caps in the pandemic). As rents rise, this means that the real support provided to renters will steadily dwindle, especially in areas where rent growth is fastest.

Support for those in ill health

Although the universal, free-to-use National Health Service means that the UK benefits system does not need to cover health insurance, health-related benefits exist for income maintenance (in the face of constraints on ability to earn through paid work) and to cover extra health-related costs. We use the terms ‘incapacity’ and ‘disability’ benefits, respectively, to cover these distinct (though overlapping) functions. The modern incarnations of these benefits for those of working age are employment and support allowance (ESA) and personal independence payment (PIP), though many other names have applied in the past.

In addition, health and the benefits system interact in more subtle yet also important ways, since those in poor health are more likely to be out of work or on low earnings and thus eligible for other benefits. In this subsection, we briefly discuss long-term health trends and how they relate to benefit claiming; elsewhere in the Deaton Review, a whole chapter is devoted to health (Case and Kraftman, 2022) and a forthcoming paper will focus specifically on inequalities in disability (Banks, Karjalainen and Waters, forthcoming).

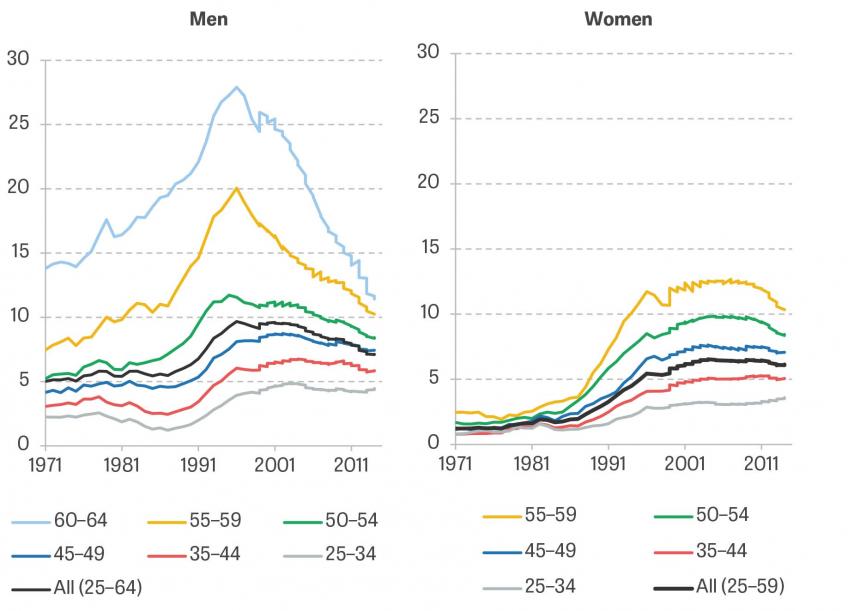

The incapacity benefit caseload has changed substantially over the past half-century. Figure 16 reproduces analysis from Banks, Blundell and Emmerson (2015), showing the share of the population claiming incapacity benefits in different age groups for men and women between 1971 and 2014. The figure shows that the rate of claiming among all groups steadily rose from the early 1980s to the mid 1990s, especially for older individuals. This was a period of rapid economic change in the UK – specifically, deindustrialisation including the decline of manufacturing and near-disappearance of mining – when labour market opportunities for some significantly weakened (Beatty and Fothergill, 2020). This highlights the likely role of labour market conditions in determining health-related benefit claims: health is clearly a crucial factor, but it cannot be decoupled from the wider economic environment. There is a significant amount of US evidence which attests to the same point: health-related benefit claims increase when economic opportunities deteriorate (Black, Daniel and Sanders, 2002; Autor and Duggan, 2003; Autor, Dorn and Hanson, 2013; Charles, Li and Stephens, 2018). For women specifically, the increasing rate of female employment may have also contributed to the rising incapacity benefit caseload. Over this period, eligibility to incapacity benefits was partly contribution-related (even when means-tested routes to eligibility were also available). Rising female employment therefore means more women with the contribution record required for incapacity benefit receipt.

Following a reform to tighten eligibility in the mid 1990s16, claim rates among men have fallen steadily. That decline is particularly sharp among older age groups – prior to reform, more than a quarter of men approaching state pension age were receiving incapacity benefits. Women did not seem to be as strongly affected by the mid 1990s reform as men, and the overall rate of incapacity benefit claiming among women has changed fairly little since 2000. Men and women of the same age are now similarly likely to be on incapacity benefits.

The figure also shows that gaps in the claim rates between different age groups have narrowed considerably for both men and women since the mid 1990s. Instead, the key predictor has increasingly become education. Emmerson, Joyce and Sturrock (2017) show that in 2000, older high-educated individuals were two to three times as likely to claim incapacity benefits as younger low-educated individuals; by 2016, the reverse was true. This suggests that receipt of incapacity benefits may increasingly be a longer-lasting state of affairs, for a group who face persistent challenges in the labour market beyond only their health.

Figure 16. Percentage of individuals claiming incapacity benefits, by age and sex

Note: The figure is restricted to men aged under 65 and women aged under 60, since for most of the period those older were above state pension age and hence generally ineligible for incapacity benefits.

Source: Reproduced from Banks, Blundell and Emmerson (2015).

Banks, Blundell and Emmerson (2015) show that there has also been a steady increase, for both men and women and across all age groups, in the share of incapacity benefit claims for mental or behavioural health problems. By 2014, roughly four in every ten claims was for one of these reasons.

These changes present big challenges. Previously, the caseload was to a sizeable extent made up of older claimants, with largely physical health problems. It was very often acting as a stopgap between wages and state pension entitlement, for those unlucky enough to experience a hit to their economic prospects and/or their health towards the end of their careers. The kind of support that those claimants need is likely to be quite different from that for today’s caseload, who are younger, probably claiming for longer, and more likely to be claiming in light of (often fluctuating) mental and behavioural health problems.