In Budget 2016 the Chancellor announced a ‘soft drinks industry levy’ that aims to reduce consumption of sugar sweetened soft drinks. The levy is due to take effect from April 2018 with two rates, one applying to mid-sugar drinks (with 5-8 grams of sugar per 100 millilitres) and a higher rate applying to high-sugar drinks (with more than 8 grams of sugar per 100 millilitres). A recent article in The Lancet: Public Health considers the possible consequences of the levy for a series of health outcomes, such as obesity, type 2 diabetes and dental care. In this Observation we propose a simple change to the soft drinks levy which would increase the likelihood of it having a beneficial effect on these outcomes.

The Lancet study is an important one, but it is also important to interpret the results accurately. The study carefully maps hypothetical changes in manufacturer behaviour through to health outcomes – the outcomes that the policy ultimately targets. However, in order to assess the impact of the levy (or any fiscal policy) there is an important first step, which is that we need to estimate the various ways in which manufacturers and consumers will respond to the policy. The paper is clear that “for each of these responses, the magnitude is uncertain” and it considers three hypothetical scenarios:

1) manufacturers lower the sugar content of mid-sugar drinks by 15% and high-sugar drinks by 30%,

2) manufacturers increase prices by an amount equal to 50% of the tax on the product, with a maximum price increase of 20% and this feeds through to purchases based on estimates of consumer price responsiveness,

3) manufacturers change the marketing of mid-sugar and high-sugar drinks, change portion sizes and introduce new products such that there is a 12% reduction in the market share of high-sugar drinks and a 6% increase in the share of mid- and low-sugar drinks.

The article concludes that hypothetical scenario (1) would result in a larger reduction in sugar consumption from sugar sweetened drinks, and therefore would result in greater improvements in health outcomes, than either hypothetical scenarios (2) or (3).

What the analysis does not speak to is whether the soft drinks industry levy will have the hypothesised effects; will it lead manufacturers to reformulate drinks, as in hypothetical scenario (1), or to any of the effects hypothesised in scenarios (2) and (3)?

How manufacturers and consumers respond to the levy is complicated and uncertain. However, careful economic analysis can help shed light on the possible effects of the levy.

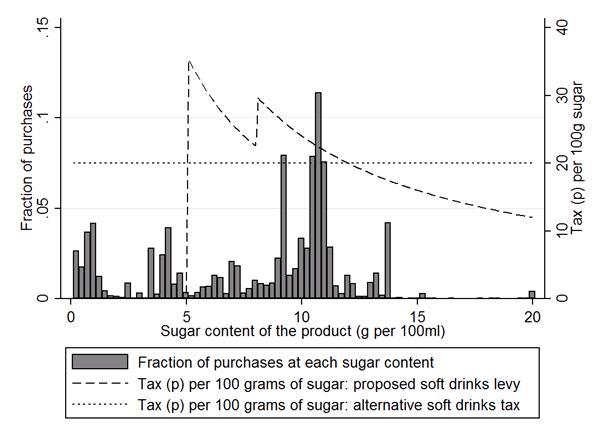

The government have set a revenue target, which the Office of Budget Responsibility has stated implies a rate of 18 pence per litre for mid-sugar drinks, and a higher rate of 24 pence per litre for high-sugar drinks. The dashed line in Figure 1 shows how the proposed tax per gram of sugar (shown on the right hand vertical axis) varies with the sugar intensity of drinks (the amount of sugar per 100 millilitres). The bars show the distribution of the sugar contents across all soft drinks purchased in 2010-11 (with fraction of purchases shown on the left hand vertical axis).

An obvious and important feature of the tax is that there is not a straight line relationship between sugar content and tax charged. There are two ‘kink points’ and between these points the tax per gram of sugar is declining as the amount of sugar increases. This has implications for the strength of incentives that manufacturers will have to reformulate products.

Figure 1

Notes: Fraction of purchases is based on the authors’ calculations using the Kantar Worldpanel for 2010-2011.

Consider, for example, a manufacturer of a 1 litre bottle of drink that contains 11 grams of sugar per 100 millilitres (this is the highest bar in the figure, meaning this was the most commonly bought type of sugary drink). Under the proposed soft drinks levy they face a tax of 24 pence per bottle or 22 pence per 100 gram of sugar in that product. If they reduce the sugar content to 10 gram per 100 millilitre then the tax paid is still 24 pence, and the tax rate increases to 24 pence per 100 gram of sugar, while if they increase the sugar content to 12 gram per 100 millilitre the tax paid remains at 24 pence and the tax rate decreases to 20 pence per 100 gram of sugar. Therefore, the soft drinks industry levy creates no incentives, within each of the mid- and high-sugar product bands, for manufacturers to reduce the sugar in their products. It is only if a manufacturer moves its product from the high- to mid-sugar or mid- to low-sugar band that it will lower the tax it faces. That means that few manufacturers will have any incentive to lower sugar content a little. They will effectively have a choice between a big change in product formulation to lower the tax they face, or no change at all. Big changes may be difficult to implement if consumers have a strong enough taste for sugar.

An alternative, and simpler, tax design would be to tax products at a constant rate per sugar content; an example of such a tax is shown by the dotted line in the figure at a rate of 20 pence per gram of sugar. This would lead to clear incentives for all manufacturers to reduce the sugar content of their products. Consider again a manufacturer of a 1 litre bottle of drink that contains 11 grams of sugar per 100 millilitres. Now the product will face a tax of 22 pence. Lowering the sugar content of the product by 1 gram per 100 millilitres reduces this by 2 pence and increasing the sugar content by 1 gram per 100 millilitres raises tax due by 2 pence. This alternative system could also incorporate bands, like the soft drinks industry levy, to create additional incentives for manufacturers to lower the sugar content of their products sufficiently to move their product into lower tax bands.

A tax per gram of sugar is unlikely to have any higher administrative burden than the proposed levy. It is already necessary to know the sugar content of the product in order to determine into which band it falls. This is the only information that is necessary to levy a tax per gram of sugar. We already operate taxes of this form, both beer and spirits excise taxes are applied per gram of ethanol, rather than per litre of product.

The soft drinks levy may be a reasonable starting point in attempting to reduce excess sugar consumption: there is evidence that households that buy a lot of sugar and households with children purchase a disproportionate amount in the form of soft drinks.However, we believe the effectiveness of the levy could be substantially improved, and the chances of the reformulation hypothesised in the favourable scenario (1) of the recent Lancet paper improved, by a simple and feasible change to its structure.

The new soft drinks industry levy is not scheduled to come into effect until April 2018. The chancellor has time to adjust the structure of the tax to make sure it better targets the sugar content of products and thereby increase the likelihood that it will be effective at encouraging product reformulation.

Note: We gratefully acknowledge financial support from the European Research Council (ERC) under ERC-2009-AdG-249529 and ERC-2015-AdG-694822, from the Economic and Social Research Council (ESRC) under the Centre for the Microeconomic Analysis of Public Policy (CPP), grant number RES-544-28-0001 and under the Open Research Area (ORA) grant number ES/I012222/1

Authors

Rachel Griffith

Rachel is Research Director and Professor at the University of Manchester. She was made a Dame for services to economic policy and education in 2021.

Martin O'Connell

Martin, previously Deputy Research Director, is a Research Fellow at IFS and Professor of Economics at the University of Wisconsin.

Kate Smith

Kate is an IFS Research Fellow and an Assistant Professor at LSE, interested in public finance, industrial organisation and applied microeconomics.

More from IFS

Understand this issue

Policy analysis

Academic research