Downloads

Download chapter summary

PDF | 102.47 KB

While there is no doubt that the UK’s vote to leave the European Union (‘Brexit’) in June 2016 will have far-reaching consequences, there is much we do not know about what these consequences are likely to be. We do not know what form of trade agreement the UK will strike with the EU, what new trade barriers may be imposed on UK–EU trade or what effects these will have on UK industries.

In the face of all this uncertainty, various studies – conducted both inside and outside government – have attempted to predict Brexit’s possible impacts on growth in the economy as a whole. These studies tend to find negative economic impacts of Brexit in both the short and long run, regardless of what kind of agreement the UK strikes with the EU.

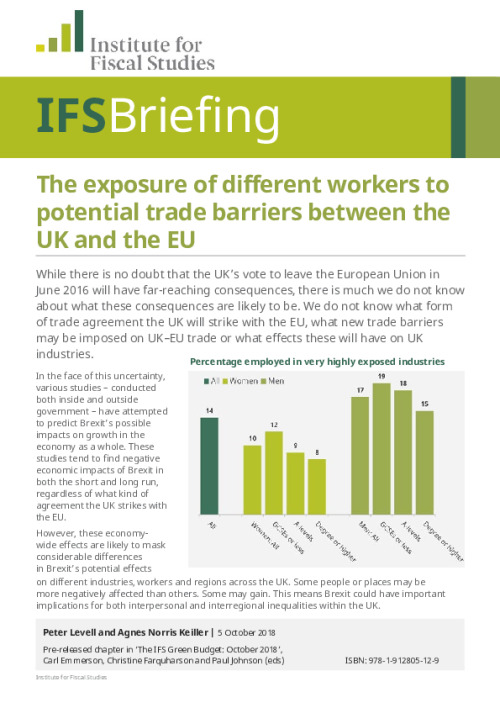

However, these economy-wide effects are likely to mask considerable differences in Brexit’s potential effects on different industries, workers and regions across the UK. Some people or places may be more negatively affected than others. Some may gain. This means Brexit could have important implications for both interpersonal and interregional inequalities within the UK.

In this chapter, we focus on one particular aspect of Brexit – changes in trade barriers with the EU – and examine the consequences these might have for different industries, workers and regions. Throughout, our aim is to shed light on relative impacts across different groups in the population rather than their overall scale. To conduct our analysis, we calculate measures of the impact of new barriers to trade on demand for goods and services produced in the UK, and how these are likely to affect different industries and, by extension, the workers that they employ.

- The EU accounts for 44% of UK exports (equal to 13% of GDP) and more than half of UK imports (17% of GDP). Leaving the Single Market and Customs Union will increase trade barriers and make both importing and exporting more costly.

- Some industries, such as clothing and transport equipment (including car manufacturing), are likely to be especially badly affected by these changes because they sell a large fraction of their output to EU countries. The transport equipment sector will also be hard hit because it imports 25% of its inputs from the EU. The same is true for the chemicals and pharmaceuticals sector. Finance is the most exposed services industry, as it currently exports a relatively large share of its output (12%) to the EU.

- Industries such as agriculture may benefit from trade barriers(though at the expense of consumers) because consumers will substitute away from more expensive imports towards products made by UK industries. However, the industries that could benefit make up a small share of the overall economy.

- Men, in particular those with fewer formal qualifications, are more likely to be employed in the most exposed industries than women and more highly educated men. Workers in process, plant and machinery operative occupations are particularly exposed. These tend to be older men with skills specific to their occupation who, history suggests, may struggle to find equally well-paid work if their current employment were to disappear.

- On average, exposure to new trade barriers is set to weigh somewhat more heavily on the top half of the earnings distribution. While earnings inequality may fall, it will come at the cost of making most UK workers poorer. The likely impacts on inequality between regions are both smaller and much more uncertain than the effects on earnings inequality.

- Low-educated workers are more exposed in some regional labour markets than others. While 19% of low-educated men work in industries we class as highly exposed in the UK as a whole, the fractions in Northern Ireland and the West Midlands are 25% and 24% respectively. Low-educated workers in these regions might find it particularly hard to adjust to the negative consequences of trade barriers.

Figure: Percentage employed in very highly exposed industries, by sex and education

Source: Table 10.1

Note: Very highly exposed industries are those that are estimated to experience a reduction in value added of more than 5%.

This is a pre-released chapter from the IFS Green Budget that will be published on October 16th. The Green Budget is being produced in association with the ICAEW and Citi and is funded by the Nuffield Foundation.

Authors

Peter Levell

Peter joined in 2009. He has published several papers on the microeconomics of household spending and labour supply decisions over the life-cycle.

Agnes Norris Keiller

More from IFS

Understand this issue

Policy analysis

Academic research