Last week, alongside the local government finance settlement for 2019–20, the government published a consultation on its plans for a national 75% business rates retention from the following year, 2020–21. This observation highlights two welcome proposals in the consultation that will make the system fairer and more effective. But it also shows that the funding from local taxes available in the new system is unlikely to keep pace with rising spending pressures in coming years. Indeed, without additional funding sources, many services could see cuts into the 2020s and beyond.

Welcome changes to business rates proposed

Last week’s local government finance settlement set out funding plans for 2019–20. Our analysis showed that this continued a trend of finding additional revenues to top up previous plans – especially for richer councils. But the plans still meant funding per person will be 4% lower per person in real terms in 2019–20 than in 2015–16, and more like a quarter lower than in 2010–11.

Looking to 2020–21 and beyond, the government plans significant changes to the funding system. The remaining revenue support grant and a number of other grants, such as the public health grant, are due to be abolished, and instead councils will retain 75% of business rates, as opposed to the 50% retained under the standard scheme presently. The aim is for these changes to be revenue-neutral overall at the point of implementation, although individual councils could see their funding increase or decrease.

Alongside the settlement the government also published a consultation on its plans for 75% business rates retention. Two proposed reforms stand out.

First, the government had previously planned to redistribute revenue growth in one go every 5 or so years to stop struggling councils falling ever further behind in terms of funding. However, this would have meant that in the run-up to a reset, councils would have faced weaker incentives to grow their business rates tax base: they may have retained the revenues for just a few months. Indeed, they may have had an incentive to try to delay the completion of new business property until the start of the next 5 year period so as to keep the growth for a full 5 years, slowing down rather than speeding up the planning system, for instance. Recognising this, the consultation proposes a so-called rolling reset, where councils will be able to retain growth in business rates for a fixed number of years, whenever that growth takes place. This is a welcome change that the IFS has recommended since the introduction of business rates retention.

Second, the government also plans changes that will significantly reduce the financial risk to councils of appeals against business rates valuations. The details are complex and we will analyse them in detail in our response to the consultation. But the principle is again welcome – the valuations are made by the Valuation Office Agency not councils, so risk associated with appeals is a risk outside of councils’ control. And our analysis has shown that these risks can be substantial.

But council tax and business rates unlikely to provide enough funding to councils

However, while councils will welcome at least some of the proposed changes, they will also be concerned about the outlook for funding in the 2020s and beyond under this new system.

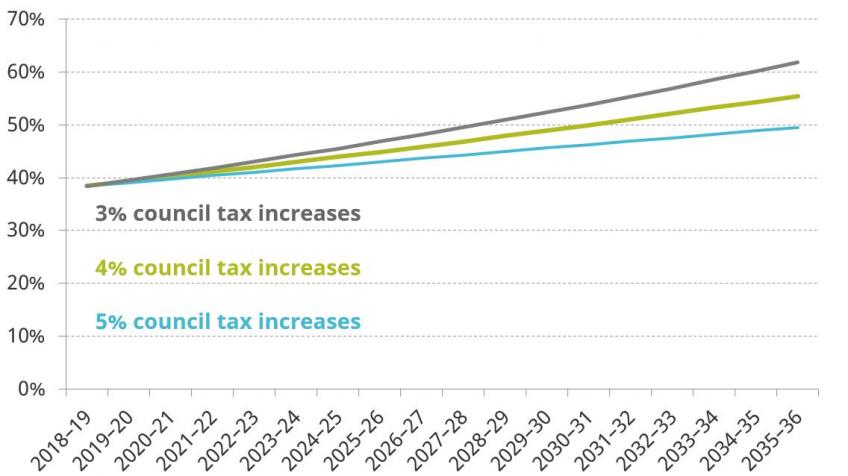

It’s too early to say exactly how much funding councils will have – important decisions need to be taken in the forthcoming Spending Review, and in the so-called Fair Funding Review. What does seem clear though is that revenues from business rates and council tax will not keep pace with rising costs and demands for services. Figure 1 shows projections of the percentage of councils’ revenues from council tax and 75% of business rates that would have to be spent on adult social care services to meet future cost pressures, under various scenarios for council tax increases.

Figure 1. Projections of the percentage of council tax and business rates revenues needed to meet rising demands and costs

For example, even if council tax bills are increased by 4% a year, every year, adult social care spending could increase from 38% to 45% of these revenues by the mid 2020s and 55% by the mid 2030s. This would imply that the real-terms local tax revenues available to other services – such as public health, children’s social services, libraries, housing and refuse collection – would not increase at all during the 2020s and would be falling in the 2030s. And these scenarios are based on the existing adult social care system: any increase in generosity (such as introducing a cap on care costs, or increasing income and asset limits) would see an even bigger squeeze on other services, without additional funding.

It therefore seems highly likely that either grant funding paid for by national taxation would have to be re-introduced at some stage, or additional tax revenues devolved to councils – especially if the social care green paper (now due in the new year) recommends a more generous system. Our next report will consider the scope for devolving more taxes to English councils, in this context.

Authors

David Phillips

David is Head of Devolved and Local Government Finance. He also works on tax in developing countries as part of our TaxDev centre.

Polly Simpson

Neil Amin Smith

More from IFS

Understand this issue

Policy analysis

Academic research