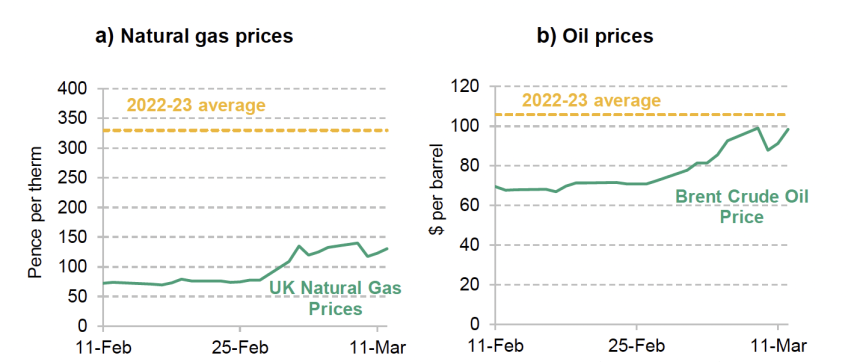

A renewed outbreak of conflict in the Middle East has caused considerable disruption in oil and gas markets. Between 28 February, when the war began, and 12 March, wholesale gas prices have risen by 67% and oil prices have risen by 35%.

These sharp movements have inevitably led to comparisons with the spike in energy prices following the outbreak of the Russia-Ukraine war in 2022, and calls for the government to provide relief for households and businesses. This earlier energy crisis prompted a massive fiscal response, with support for British households and businesses costing around £75bn (almost 3% of GDP) over the two fiscal years 2022-23 and 2023-24. The cost of the UK’s energy support package was bigger than most European countries. Calls have already been made to support those using heating oil, who have already experienced particularly large increases in costs, and to extend the 5p cut to fuel duty that was introduced to deal with the spike in pump prices in 2022 (and set to expire gradually, starting this September). Some other countries have already moved to cap fuel prices following the recent price increases.

How does this current shock compare to the last energy crisis and what might the government be able do about it?

Price increases not yet as large as in 2022 energy crisis

So far, the increase in gas prices is not as large as the shock following the outbreak of the Russia-Ukraine war. Between 2021 and the last quarter of 2022 wholesale gas prices rose three-fold in real terms (deflated using the CPI excluding energy). This led to a roughly proportional increase in domestic energy prices – that is: without government support the real cost of a household energy bill at Ofgem’s price cap would have risen three-fold over this period. The current wholesale price increases would therefore need to worsen substantially, and in a sustained way, to lead to comparable increases in energy bills. Given the volatility of energy prices (that was also seen in 2022), this is of course not something that can be ruled out.

Meanwhile, real-terms oil prices rose by 27% between 2021 and the third quarter of 2022 before coming down in the last quarter of 2022, which is smaller than the short-term increase we have seen from the current conflict. Pump prices also saw a roughly proportional rise to the oil price increase – the real price of diesel rose by 21% and petrol by 17%.

Figure 1. Oil and gas prices since 23 February

Note: 2022-23 average is based on the 2022-23 financial year, stretching from 6 April 2022 to 5 April 2023, uprated using CPI excluding energy. Quarterly futures used for natural gas; front-month futures used for Brent crude oil.

Source: Natural gas prices: ICE Futures Europe UK NBP Natural Gas Futures, accessed via investing.com; oil prices: ICE Brent Crude Futures, accessed via investing.com.

It is important to remember, however, that household energy bills are already 14% higher in real terms than they were before the Russia-Ukraine war. During the last crisis, the government acted to keep average household energy bills below a nominal point of £2,500 (£2,699 in today’s money). The current Ofgem price cap that will come into force from April is set at £1,641 for the average household. In the pessimistic case that the 67% price increases we have seen so far were sustained and passed through in a similar way to household bills, typical household bills would rise slightly above the level at which the government decided to intervene in 2022-23.

Because the gas price increases are so far not nearly as large as they were in 2022-23, the costs of keeping bills below this level would, at current prices, be substantially cheaper. But this is not to say the government should rush into making the same commitments it made three years ago. While support to households and businesses helps to insure them against temporary price movements (and the resulting cash squeeze), it comes at a cost and can blunt the incentive to cut back on energy use when supplies are scarce.

More difficult public finances backdrop

An important consideration is that the public finances are in a more strained position than they were at the start of the Russia-Ukraine war, and a sustained increase in energy prices is likely to worsen them further. As an illustration of scale, modelling by the Office for Budget Responsibility suggests that a (pessimistic) 75% increase in oil and gas prices sustained for a year would raise debt by 3% of GDP after three years. This is because higher inflation would automatically push up welfare spending, while a higher rate on RPI-linked gilts and a higher Bank interest rate would increase debt interest costs. If the government were to keep departmental spending unchanged in real terms, this would increase debt by a further 2% of GDP. The OBR also predicted that impacts would persist as much as five years after the shock, largely due to the supply-side impacts of higher interest rates and energy prices.

Additional spending on short-term measures would not, in itself, affect the Chancellor’s performance against her fiscal rules (which are assessed based on the forecast fiscal position in 2029-30, when a temporary support package would be expected to have expired). However, the government faces much higher borrowing costs than it did in 2022, and these could grow further if interest rates go up, making it harder to fund an expensive support package. Some of the cost of the package of support in 2022 was covered by new taxes – the energy profits levy and the electricity generator levy – on energy producers who enjoyed ‘windfall’ gains from the surprise increase in prices. These taxes were still in place when prices fell and have raised around £15 billion in the four years since their introduction. But because they are still in place, the government was already banking on getting some proceeds from these taxes before the war started. This means that if it wanted to find additional tax revenues of the same magnitude over and above the pre-crisis revenue forecasts, it would likely have to either raise the rates of these taxes or introduce new measures.

How to design a support package

The conflict has so far been underway for a fortnight. It would be sensible for the government to delay a decision about potential support packages until it is clearer how long the conflict might last. However, given that there are already calls for support, it is sensible to start considering how such support could best be designed.

If the government were to provide support then, given the tight fiscal environment, it is doubly important that it is provided in a way that achieves good ‘bang for the buck’. This means delivering support to those whom the government decides most need it, while not blunting the incentive to reduce consumption of energy for those who are able to cut back.

In the previous energy crisis, most of the government’s support measures for households were not targeted according to income or energy need. While some relief payments were specifically made to households on means-tested or other benefits, the majority of direct household support was delivered in the form of a substantial energy price subsidy, fuel duty tax cuts and a universal £400 rebate off energy bills. In 2022-23, £20bn was spent on energy price subsidies, and a further £13bn on universal energy bill rebates. The 5p cut in fuel duties cost a further £2bn. Collectively, these three measures accounted for 74% of the roughly £48bn support package for households that year. The remainder (roughly £12bn) was spent on more targeted support: cost of living payments to households receiving state benefits and council tax rebates to those in lower council tax bands, although neither of these were directly linked to energy needs. In addition, the government provided £7bn of energy price subsidies for businesses. Some of the support measures also extended through into 2023-24, costing an additional £20bn.

General price subsidies or tax cuts linked to energy consumption ensure that households with high energy needs (due to for example health conditions, or a poor-quality home, or living in a remote location where driving is essential) are not left substantially out of pocket due to causes outside of their control. But they also come with significant costs. Subsidies to gas and electricity prices reduce incentives to cut back on energy use and are expensive – during the last energy crisis, each £1 households spent on energy cost the government 40p (if price subsidies were repeated, their cost would depend on the extent of the subsidy). Delaying the scheduled increases in fuel duties due to take place in September, December and March until next April would cost £600m in 2026-27.

More targeted cash payments, that do not distort energy prices, would help the government deliver support where it is needed in a more cost-effective manner.

Previous IFS research used bank account data to model both the responses of households and the costs to the government of different combinations of subsidies and energy bill rebates. Using the government’s choice over how much to rely on price subsidies and how much to rely on rebates, the authors were able to infer the weight the government put on providing relatively more support to those hit hardest (which could be done by spending more of the budget on subsidies, which naturally protect heavy energy users) compared with the weight put on reducing the impact on the average household (through cash payments, which lead to less overconsumption of energy). This allowed them to find policies that could have potentially achieved similar outcomes – in terms of both supporting those hit hardest and reducing the impact of energy prices on the average household – at lower cost.

One recommendation from the research was to deliver support as cash rather than money off energy bills (which induced some households to spend more on subsidised energy). Another was to make better use of data on either income or historical energy bills to target cash payments better.

A smaller price subsidy alongside cash transfers to those on low income, as well as delivering transfers as cash rather than as money off energy bills, could have achieved similar outcomes at 8% lower cost than was actually spent on these two schemes (a saving of £2.7bn). Basing the cash transfers on the previous year’s energy usage rather than income would have led to a similar-sized cost saving. However, combining information on both household income and past energy usage would have been more than twice as beneficial – reducing the cost of reaching a similar outcome by 18% or £5.8bn. This is money the government could either have used to increase the generosity of the overall relief package or spent on other priorities.

Targeting cash transfers at those with low incomes and/or high energy use would require investment in the government’s ability to link together data on households from different sources. But as these figures show, these are investments worth making. Recent initiatives to link energy consumption data, held by the Department for Energy Security and Net Zero, with household income data, held by HMRC and the Department for Work and Pensions, are therefore welcome.

The fact that this energy price shock has come in the spring, when temperatures are rising and energy demand falling, gives the government some time to prepare for a potentially harsh winter. While we all hope that we will not see a repeat of previous events, it is worth thinking now about whether we are prepared in case we do.

Authors

Peter Levell

Peter joined in 2009. He has published several papers on the microeconomics of household spending and labour supply decisions over the life-cycle.

Nick Ridpath

Nick joined the IFS in 2023 and works in the Education and Skills sector, focusing on the long-run impacts of education policy.

Bobbie Upton

Bobbie is a Research Economist in the Taxation and Environment sectors, looking at air pollution and taxation of capital income.

More from IFS

Understand this issue

Policy analysis

Academic research