The level of the state pension is increased each April in line with the ‘triple lock’: the highest of CPI inflation, average earnings growth or 2.5%. The September CPI inflation figure, which feeds into this calculation, came out on 22 October at 3.8%. This is below the average earnings growth figure for May to July 2025 of 4.8%, meaning that in April 2026 the full rate of the new state pension is likely to rise by £11 to £241 per week. Although not every pensioner receives exactly this amount, the majority of newly retired pensioners receive the full rate of the new state pension, or an amount very close to this.

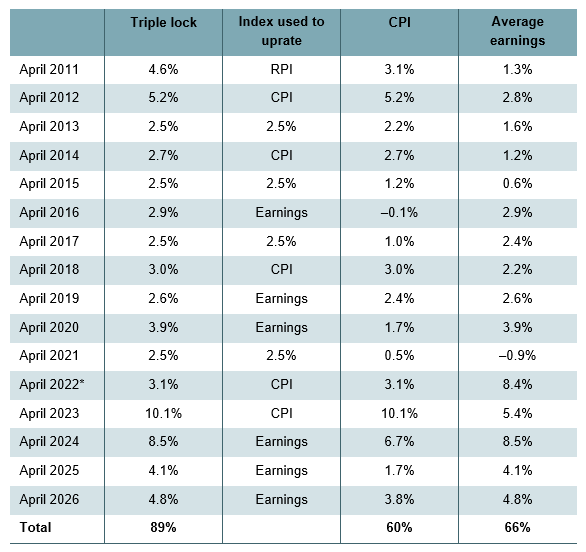

As shown in Table 1, since the introduction of the triple lock in 2011, the value of the state pension has risen much faster than either average earnings or prices. At £241 per week, a full new state pension is expected to be £30 per week (14%) higher than it would have been under average earnings indexation since 2011. According to the Office for Budget Responsibility (OBR), the triple lock has pushed up spending on the state pension so that it now (2025–26) costs the government £12 billion more per year than the cost would have been if the state pension had been uprated in line with average earnings since 2011.

Table 1. Triple lock indexation since its introduction

* The triple lock was suspended in April 2022 because of dramatic growth in earnings in Summer 2021 caused by the unwinding of the effects of the furlough scheme (Coronavirus Job Retention Scheme).

Note: Indexation was in line with the Retail Prices Index (RPI) measure of inflation in 2011, before the government moved to Consumer Prices Index (CPI) indexation of state benefits and public pensions.

Source: Updated from Hobson, Harker and Kirk-Wade (2023) using Office for National Statistics data on earnings and CPI inflation.

Triple lock adds uncertainty to public finances

The generosity of the triple lock has a substantial and growing impact on public finances. Spending on the state pension will continue to increase due to the ageing population, but the triple lock also plays a part. And because the triple lock increases the value of the state pension based on the maximum of three figures, two of which are potentially volatile over time, forecasting state pension spending in the future also becomes more difficult under this indexation policy.

Indeed, the OBR estimates that spending on the state pension will rise by around £80 billion in today’s terms by the 2070s, and over half of this increase is projected to be due to the triple lock. But under a more volatile economic environment the triple lock could cost an extra 1.5% of national income – or £44 billion in 2025–26 terms – on top of this. On the other hand, if future inflation and earnings growth were less volatile in the future, the triple lock could cost £40 billion less in today’s terms than projected in the central estimate.

Distributional impacts of different pension policy choices

In July the government launched the third Independent Review of the State Pension Age, which aims to consider whether the rules around pensionable age are appropriate. While the review will only focus on the state pension age rather than how the state pension is uprated over time, it is important to consider how potential changes to these two policies would affect different people.

Raising the state pension age delays the point at which people can receive their state pension. This delay affects poorer people, who on average have a lower life expectancy, more because the loss of a year of state pension income is more important for those with lower life expectancy as they spend fewer years above the state pension age (see Cribb et al., 2023 for more detail). On the other hand, those with a higher life expectancy benefit relatively more from the triple lock, as they are more likely to be receiving a generously indexed state pension into their 90s. In other words, using further increases to the state pension age as a way to rein in spending on the state pension, while keeping the triple lock, will tend to favour groups that are better off.

A more predictable and transparent alternative

While the triple lock has helped increase pensioner living standards over the last 15 years, a better approach is needed for the future. As recommended in the IFS Pensions Review, a more sustainable and predictable option would be to uprate the state pension in line with a ‘smoothed earnings link’, similar to the approach used in Australia.

This would mean that the government sets a target level for the new state pension, expressed as a share of median full-time earnings. In most years when the state pension is at the target level and earnings are growing in real terms, the state pension would be uprated in line with average earnings growth. But in years when inflation rises above average earnings growth, the state pension would instead rise in line with inflation. This inflation protection would then continue as real earnings recover to allow the state pension to return to its target fraction of average earnings. Together these features of the smoothed earnings link would mean that the state pension both keeps up with growing standards of living in the long run, while providing inflation protection in times of economic turmoil. This would provide greater predictability for both pensioners and policymakers. While the government has committed to keeping the triple lock this parliament, a sensible approach would be to move away from the triple lock after the next election.

Authors

Heidi Karjalainen

Heidi is a Senior Research Economist in the Retirement, Saving & Ageing sector. Her current research is on pensions and saving for retirement.

More from IFS

Understand this issue

Policy analysis

Academic research