Plans to significantly cut Scottish income tax rates are front and centre of Reform UK’s Scottish manifesto. Initial cuts – setting each tax rate 1 percentage point below that in the rest of the UK – would cost around £2.3 billion per year by 2030, with the final goal – rates 3 percentage points below the rest of the UK – costing around £4 billion a year. These are large tax cuts – up to 1.5% of Scottish GDP – in the context of a Scottish budget that is already likely to be under strain due to rising spending pressures and a slowdown in funding growth from the UK government.

The manifesto repeats plans to pay for these tax cuts by ending spending on ‘net zero’ initiatives and by unspecified cuts to spending managed by ‘quangos’. As we highlighted when these plans were first announced in January, the Scottish fiscal framework means that cuts to capital investment – which includes much of the spending on ‘net zero’ initiatives – cannot be used to pay for tax cuts.

Reform UK also claims that the income tax cuts would in fact pay for themselves via higher economic growth. This is not credible. Specifically, the manifesto’s claim that each percentage point of additional economic growth would generate a cumulative £8 billion over 10 years and that this would ‘repay the £2 billion up-front cost four times over’ is wrong in two important ways.

First, the annual costs above already incorporate assumptions about behavioural responses to the tax cuts, including higher labour supply, less tax avoidance and evasion, and higher net immigration. There is room for reasonable disagreement as to the likely size of behavioural responses but there is no evidence to suggest that the tax cuts would pay for themselves. Moreover, because only around one-third of tax revenues are devolved to Scotland, only part of the revenue increase that would result from increased economic growth would accrue to the Scottish Government. Because of this, the Scottish Fiscal Commission estimates that a 1% boost to earnings, for example, would boost devolved income tax revenues by only around £300 million a year (or around £3 billion over 10 years).

Second, the £2 billion (or more) cost of the income tax cuts is not a one-off up-front cost – it is an annual cost. Even if the figure were correct, £8 billion over 10 years does not exceed £2 billion per year, let alone repay it four times over.

The ‘self-funding’ tax cuts are therefore a mirage created by a misunderstanding or misrepresentation of the current devolution settlement and incorrectly comparing cumulative and annual figures.

This is not good enough.

Beyond the headline-grabbing income tax cuts, Reform UK rightly highlights that both UK government and Scottish Government policies lead to some people facing particularly high effective marginal tax rates – whereby most of every additional £1 earned is offset by higher taxes and/or the withdrawal of benefits. Some people face ‘cliff edges’ – whereby earning £1 more can lead to losing thousands of pounds a year in benefits entirely. As we recently argued, the Scottish and UK governments should work together to avoid such situations where possible – for instance, by tapering away the Scottish child payment more smoothly as income rises.

Reform UK’s concrete proposal to taper carers’ benefits is in this vein, and feasible – albeit at a cost. But a broader pledge to use devolved powers, where possible, to ensure no-one faces an effective marginal tax rate of more than 50% could be more complex and more costly. For example, the easiest way to address the high effective tax rates faced by parents with incomes of between £60,000 and £80,000 who are subject to the withdrawal of the UK government’s child benefit – one of the examples cited in the manifesto – would be for HMRC to stop withdrawing child benefit in Scotland. But if agreement could not be reached to do this, the Scottish Government might have to make top-ups to benefits for high-income families to fully or partially offset the child benefit withdrawal by the UK government.

And given that the biggest group facing high effective marginal tax rates is people in families in receipt of universal credit on the earnings taper (who face an effective rate of at least 55%, and often substantially more), addressing this without changes in UK government policy would require top-ups to benefit payments for many low- and middle-income families – pushing up Scottish benefit spending, rather than reducing it as Reform UK says is its intention.

In summary, the combination of big tax cuts and implied benefit increases without any identified source of funding is not fiscally credible. And the analysis of the potential revenue effects of the headline income tax cuts is unserious at best.

Further analysis of tax proposals:

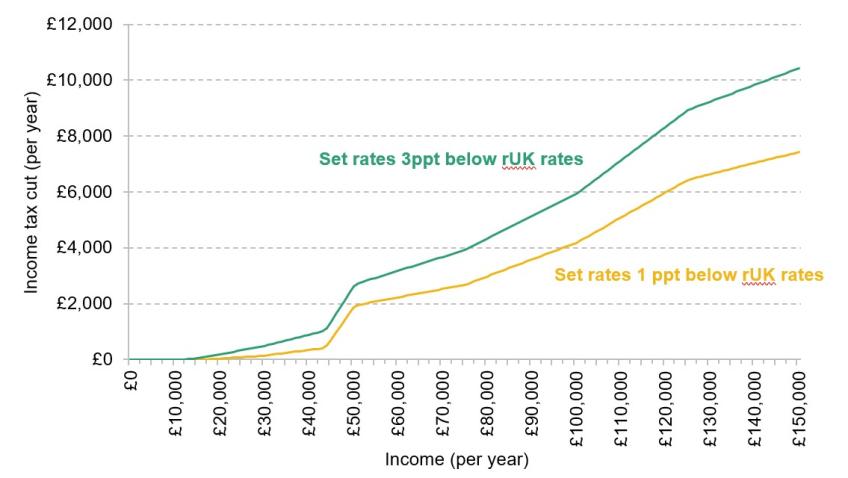

- The initial £2.3 billion of income tax cuts proposed by Reform UK would benefit all income tax payers bar those with the very lowest incomes – i.e. those in the starter-rate band (between £12,571 and £16,537) – where the rate is already 1 percentage point lower than in the rest of the UK. The gains would be much bigger for high-income taxpayers than for low-income taxpayers, as shown in Figure 1 (see below). Someone working full-time on the National Living Wage earning £24,785 would save at most £80 a year compared with current plans (and less if they are in receipt of universal credit). In contrast, someone on £50,000 a year would save around £1,900 a year, and someone on £125,000 a year would save around £6,400 a year. The chart shows that these savings would increase to around £320, £2,600 and £8,900 a year respectively if the ambition of reducing rates to 3 percentage points below those in the rest of the UK were achieved. High-income taxpayers would therefore be by far the largest beneficiaries of these changes.

- Reform UK says it would aim to phase out both land and buildings transaction tax (LBTT) and business rates over 10 years, replacing them with an annual property tax that would raise the same revenue. LBTT is an economically damaging tax that penalises mobility and should be replaced, and business rates in their current form unnecessarily discourage the construction and improvement of business property. Reform UK is right that there is scope for economically beneficial reform here. Unfortunately, while little detail is provided of exactly what Reform UK has in mind, the information that is provided implies the plans have significant shortcomings.

- First, pre-announcing reductions to LBTT would encourage people to hold off buying properties, gumming up the property market: it would be better to enact such a reform without advance warning.

- Second, and more importantly, when describing the proposed annual property tax, the manifesto states that it would ‘end the constant cycle of continual and unpredictable business rates revaluations’. The revaluation of property on a regular basis is a key part of any well-functioning annual property tax – helping to ensure tax liabilities reflect current property values, not values at some arbitrary point in the past. And the rationale for cancelling revaluations – that they discourage businesses from growing their turnover – misunderstands how business rates work: they are based on estimated market rental values of properties, not the turnover of individual businesses.

- In the meantime, Reform UK states that it would reverse the business rates revaluation taking effect in April. This would benefit those businesses occupying properties whose rateable value has increased by more than average and who are therefore set to pay higher bills. But it would hurt those businesses occupying properties whose rateable value has increased by less than average – or even fallen – who are set to pay less from April. As the latter are presumably in areas or sectors where business conditions have deteriorated relative to Scotland as a whole, reversing the revaluation would hit businesses (and landlords) that may already be struggling.

Further analysis of spending proposals:

- Reform UK rightly highlights that the Scottish NHS suffers from a range of issues, as our recent research demonstrated. However, despite putting ‘fixing our NHS and cutting waiting lists’ first in its list of priorities, the manifesto provides no details of either spending or policy initiatives that would help to deliver significant improvements in NHS performance. A planned Scottish Healthcare Reform Commission could help to flesh out the details post-election, but the challenges in improving NHS performance – especially with limited funding – should not be underestimated.

- On schools, Reform UK again rightly highlights evidence of a decline in outcomes relative to England. Reforming the ‘Curriculum for Excellence’ and a greater focus on testing and the collection of comparative data on performance could have benefits. Another proposed focus is changes to provision for children with special educational needs and disabilities (SEND). The issues in Scotland are different from those in England – there has not been the same rise in expenditure or rise in the number with the highest classification of needs as south of the border. But as in England, reforms could be contentious and may require up-front investment to deliver.

- On local government, the manifesto highlights the difficult financial situation facing Scottish councils – which may intensify post-election given planned cuts to funding from the Scottish Government. A proposed review of statutory duties imposed on councils is worthwhile and could identify areas where service requirements could be reformed – such as homelessness prevention duties, specifically highlighted by Reform UK – and/or reporting requirements that could be removed. But the fundamental issue for councils is that spending in areas such as social care services is growing, while funding is being cut. Addressing this would require either cutbacks in service provision or increases in local government funding – the latter being difficult given the tax cuts planned by Reform UK.

Figure 1. Income tax cuts by income level under Reform UK’s proposals

Authors

David Phillips

David is Head of Devolved and Local Government Finance. He also works on tax in developing countries as part of our TaxDev centre.

More from IFS

Understand this issue

Policy analysis

Academic research