From today (1st September), the first 18-year-olds will be able to access Child Trust Funds (CTFs) set up over a decade ago by Tony Blair’s Labour government. When first announcing the policy, the government pointed to the fact that ‘people without assets are much more likely to have lower earnings and higher unemployment, and are less likely to start a business or enter higher education’. But how much difference might these accounts make to the finances of 18-year-olds?

What are Child Trust Funds?

CTFs are accounts given to newborns into which the government made an initial contribution. The key features are as follows:

- The government initially paid £250 into all accounts, with an additional £250 (so £500 in total) paid to the accounts of those newborns whose parents were in receipt of certain means-tested benefits.

- Parents were given a voucher to open an account, but if they did not do so within 12 months HMRC opened an account on the child’s behalf.

- Parents – and others – could contribute to the accounts (up to annual limits).

- The accumulated funds, including any returns, cannot usually be accessed until the child reaches age 18, but at that point the young adult is free to use the funds, tax free, however they wish.

The first accounts went live in April 2005 and were made available to all those born from September 2002. The 2006 Budget announced that an additional government contribution (again of £250 or £500) would be paid on the child’s seventh birthday, so these were first paid in September 2009. The policy was then swiftly abolished by the coalition government in its very first set of cuts: from August 2010 payments at birth were reduced and the top up at age seven was stopped, and from January 2011 all payments from government were stopped, reducing public spending going forwards by an estimated £500 million a year.

In total, 6.3 million CTFs were opened, with 70% opened by parents and 30% opened by HMRC. Overall, 64% of accounts received the standard government contribution and 36% received the enhanced payment, with a total of £2 billion of government contributions going into the accounts. More details on the policy – and its formation and demise – can be found here.

What difference will Child Trust Funds make to the finances of 18-year-olds?

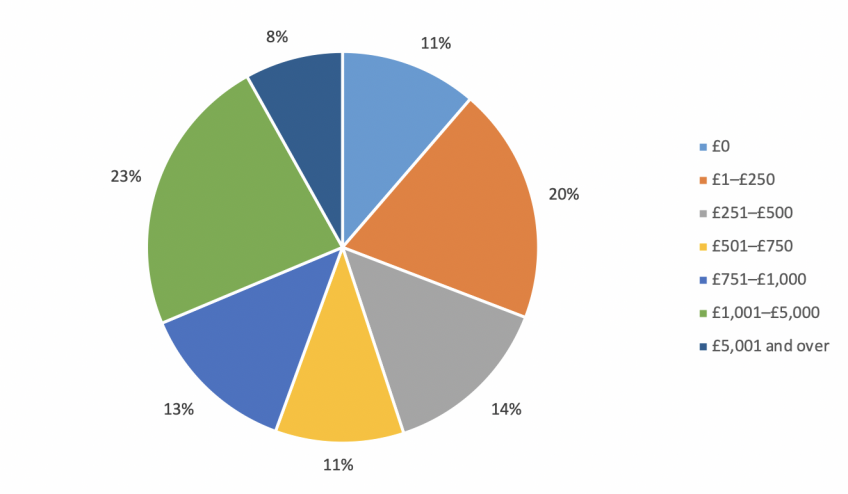

Figure 1 uses data from the most recent wave of the Office for National Statistics (ONS) Wealth and Assets Survey (2016/18) to describe the distribution of CTF balances among those born between September 2002 and August 2003 (as reported by their parent or guardian). At that time, they will have been aged between 12 and 15. There is a considerable range in the amounts held, with 45% reported to hold £500 or less, 23% to hold £1,001–£5,000 and 8% to hold over £5,000. The median amount held is around £650.

For context, the maximum that an account could have received from the government was £1,000 (a payment of £500 at birth and a top-up of £500 at age 7) and the minimum government contribution was £250 (paid at birth, with the child reaching age 7 after these top-up payments had been scrapped). However, the maximum amount that could have been paid into a CTF by family or friends given annual subscription limits is nearly £50,000, which could be worth substantially more by today if it was invested in a stakeholder fund.

Of course, balances will have changed since 2016/18. Most obviously, any funds invested in equities are likely to have fallen in value over the last six months, while additional contributions to the accounts will have boosted them. These figures also almost certainly include a degree of under-reporting: 11% of children were reported not to have a CTF. Of course, these could be some of the 30% of accounts that were opened by HMRC and therefore parents could potentially have always been unaware of their existence.[i]

Figure 1. 2016/18 reported value of Child Trust Funds for those born Sept 2002 to Aug 2003

Source: Authors’ calculations using Wealth and Assets Survey, Round 6 (2016/18).

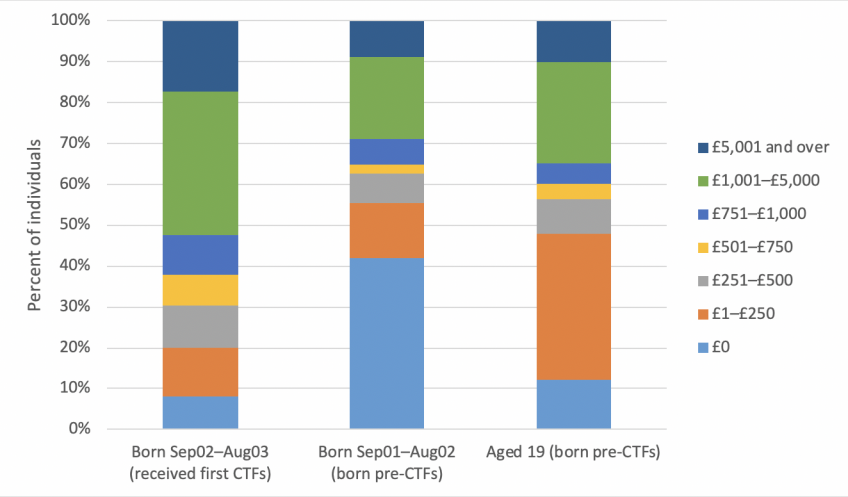

While some of the amounts held in CTFs may sound modest, it is important to set this in the context of the wealth distribution of young adults. To do so, we consider a broader measure of wealth, as those with CTFs could potentially have less wealth in other forms (for example, if parents made contributions to the CTF instead of making them to their child’s savings account). The first column of Figure 2 describes the distribution of total gross financial wealth for those born between September 2002 and August 2003 (i.e. the same group for whom the distribution of CTF values is shown in Figure 1). The second column describes the distribution of the same measure of wealth for those born a year too soon to benefit from a CTF (i.e. between September 2001 and August 2002, who were aged 13–16 when interviewed). It is striking that those eligible for the CTF are much more likely to have wealth than those born just too soon to benefit from the policy. Median total wealth among those eligible for the first CTFs was £1,200, compared with just £100 among those born slightly too early. Indeed, 92% of those with CTFs appear to have positive financial wealth (and the true figure ought to be higher than that), compared with 58% of those born a year earlier.

Figure 2. Distribution of total gross financial wealth

Source: Authors’ calculations using Wealth and Assets Survey, Round 6 (2016/18).

One possible effect of the CTF policy is that it might have changed the way children’s assets are organised, with savings put in children’s own names from a younger age. The final column shows the distribution of wealth among those aged 19 when interviewed in 2016/18. These figures are not directly like-for-like, as this information is collected from individuals themselves rather than their parents and, of course, they are a few years older. However, it is clear that many young adults hold little wealth. While 88% had some gross financial wealth, 50% had £300 or less.

What effects might Child Trust Funds have?

It is clear from Figure 2 that in the absence of CTFs many young people have no, or very low levels of, financial wealth and therefore the policy will have made a substantial difference to the distribution of financial wealth of those aged 18. But – despite the rather grand claims made at the time the scheme was introduced – we should not expect to see large impacts on the proportions who continue in higher education, get onto the property ladder by a certain age or start their own business as a direct result of the CTF. There is only so much difference a CTF with an average balance of around £650 could realistically make and it was always far from clear that these accounts were the best use of public spending, not least because the public policy objective was never especially well articulated.

Of course, we also don’t know the extent to which these funds in the child’s name will simply reduce the amount that parents transfer to their children in other ways. The effect on actual access to resources remains unknown.

It could be, however, that the CTF was remarkably well timed in that a boost to the spending power of one group of young adults could be particularly welcome in the current context. The public heath response to the COVID-19 pandemic has had particularly severe impacts on young adults: their education has been disrupted and many of the jobs that disproportionately employ young people have been severely hit by the shutdown. For those turning 18 with a CTF, the funds could enable them to make an investment that assists them with their learning or be a welcome buffer to help them through some difficult months. The key question that remains open is how well those accessing their funds for the first time will spend their CTFs.

Note:

This work was produced using statistical data from the Office for National Statistics (ONS). The use of the ONS statistical data in this work does not imply the endorsement of the ONS in relation to the interpretation or analysis of the statistical data. This work uses research data sets which may not exactly reproduce National Statistics aggregates. The Wealth and Assets Survey is collected by the Office for National Statistics, and was made available through the Secure Research Services environment. Crown copyright material is reproduced with the permission of the Controller of HMSO and the Queen’s Printer for Scotland.

[i] To find out where a Child Trust Fund is held on your behalf, visit https://findctf.sharefound.org/ or https://www.gov.uk/child-trust-funds/find-a-child-trust-fund

Authors

More from IFS

Understand this issue

Policy analysis

Academic research