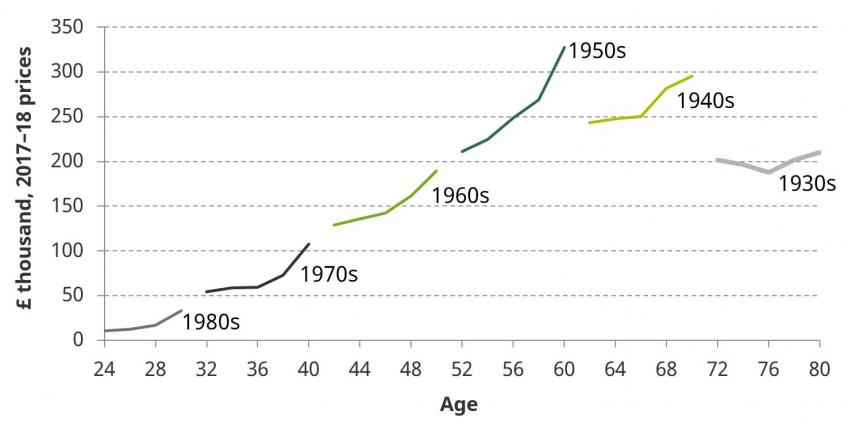

There is increasing attention given to the wealth held by different generations. Various authors have highlighted the fact, illustrated in Figure 1, that those born in the 1950s were the last to experience generation-on-generation increases in wealth and that generations born more recently have not accumulated any more wealth than their predecessors had by the same age. [1] This “stalling” of wealth accumulation has prompted concerns and has been one aspect of the debate around intergenerational fairness that has risen up the political agenda. There is a concern that today’s young people are not building up enough wealth to be able to afford the standard of living in their later life that they might hope for, or expect.

Figure 1: Median net household wealth per adult, by age and generation

Source: Wealth and Assets Survey, various years

What accounts for this “stalling” pattern? Recent IFS research shows that, in terms of the components of wealth, it is lower home ownership rates for more recent cohorts (with consequently lower housing wealth) where today’s young people are falling behind. The 1960s cohort is just behind the 1950s on this measure, but the 1970s and 1980s have seen progressively larger drops in homeownership at comparable ages. While the 1960s and 1970s generations have levels of pension wealth that are comparable or even slightly higher than their predecessors, this is not sufficient to generate increasing wealth overall.

More fundamentally, there is a question about whether stalling wealth accumulation represents a failure by younger generations to save “enough”. One claim is that young people are prioritising the present, spending too much on the much-mocked avocado toast, for example, and not saving enough for their future. The counter-claim is that younger generations do not have a fundamentally different attitude towards saving, but simply face an economic environment much less conducive to the accumulation of wealth.

In research published today, we use an economic model to quantify the importance of different aspects of the changing demographic and economic environment for the levels of saving and wealth accumulation that we would expect to see across different generations. This can help us to consider how important changing circumstances might be in driving the “stalling” of wealth accumulation that we observe. The circumstances that we examine include earnings, rates of return on wealth (including the financial return to housing wealth), the state pension system, the tax system, number and timing of children, life expectancies and retirement timing. If we find that changing circumstances can generate a pattern of “stalling” then there is less need to appeal to changing attitudes towards saving as an explanation for this trend.

We find that a number of aspects of the changing economic environment would be expected to lead to changing levels of wealth across generations and could be expected, when taken together, to overall lead to a “stalling” of wealth accumulation. Of particular importance are earnings and rates of return on wealth. Changing life expectancy, state pension provision and taxes are also relevant, but are less important than earnings or rates of return.

As individuals’ earnings are the main resource they have to fund their spending and saving, it is no surprise that cohort-on-cohort increases in earnings levels seen for earlier generations would be expected to lead to higher wealth. Similarly, the slowing of earnings growth experienced so far by the 1970s and 1980s cohorts would be expected to be a drag on their wealth accumulation, relative to preceding generations. If these cohorts eventually see their earnings rise above those of their predecessors, then their wealth should eventually exceed that of previous generations too.

The rate of return that individuals receive on their wealth is very important for the levels of wealth we would expect them to accumulate. Mechanically, a lower rate of return means that any level of saving translates into a lower level of wealth. Further, a lower return gives less of an incentive to save early in life, as compared to later. Younger generations have not seen, and are not expected to see, as high returns to their wealth as previous generations achieved. Those born in the 1970s and 1980s suffered the financial crisis and its aftermath, while the rapid rises in house prices of the past 30 years, and the stock market performance of the 1980s, are unlikely to be repeated in the coming decades. We find that lower returns of the magnitudes that younger generations are expected to receive over their lifetimes would significantly reduce their wealth accumulation relative to those born earlier.

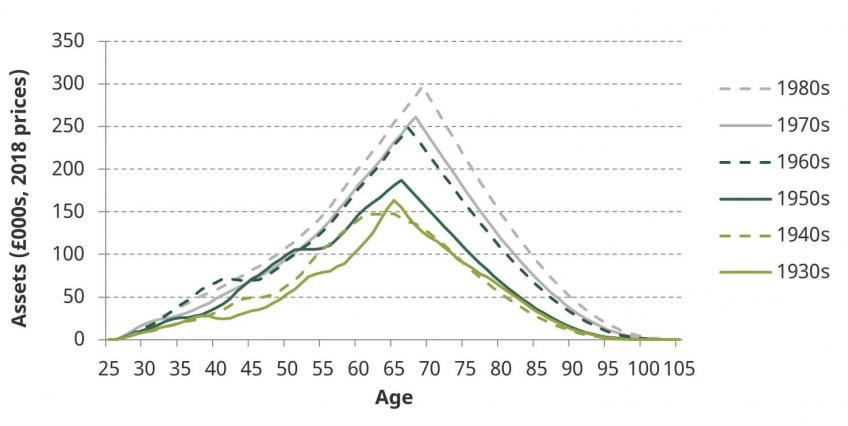

A summary of our overall findings is set out in Figure 2 and Table 1 below. Differences in the circumstances we consider would lead us to expect wealth accumulation to stagnate for those born since the 1960s, at those ages at which we observe this pattern in the data. For example, at age 50, the 1960s generation is simulated to hold 6% less wealth than the 1950s generation held at the same age. At age 30, the 1980s and 1970s generations are simulated to have approximately the same level of wealth. These results suggest that we should perhaps not be surprised by the observed patterns shown in Figure 1. Therefore, we do not necessarily need to point to changing attitudes towards savings between generations to generate a picture of stalling wealth accumulation among those born since the 1960s – the changing economic and demographic circumstances we consider are sufficient to lead to such a picture.

Figure 2: Simulated wealth, by generation

Source: Crawford and Sturrock (2019)

Table 1: Comparison of simulated wealth at selected ages, by generation

Gen. | Wealth compared to the 1950s generation at: | |||

Age 30 | Age 40 | Age 50 | Retirement | |

1930s | 77.4 | 58.3 | 53.7 | 87.3 |

1940s | 72.9 | 83.8 | 63.5 | 78.9 |

1950s | 100.0 (ref.) | 100.0 (ref.) | 100.0 (ref.) | 100.0 (ref.) |

1960s | 125.4 | 164.3 | 94.0 | 132.8 |

1970s | 147.7 | 123.4 | 95.8 | 139.6 |

1980s | 147.3 | 147.2 | 109.0 | 158.9 |

Source: Crawford and Sturrock (2019)

Our model is of course a simplification of reality and does not include all features relevant to savings decisions. One notable omission is that we do not model the impact of the decline in defined benefit pensions. However, the reduction in generosity and availability of these pensions would be expected to further reduce wealth accumulation among more recently born generations, as compared with their predecessors. Another limitation is that while we include a measure of the rate of return to housing in our analysis, changes in deposit requirements and price to earnings ratios have important and complex implications for wealth accumulation that we could not fully model.

Our findings do not mean that the slowing in rates of wealth accumulation is of no concern. To the extent that stalling wealth accumulation is a response to poor earnings growth and low returns, we may be concerned about the implications for equity between generations. However, this does not necessarily mean that policies to increase the private saving rates of younger generations are advisable. It needs to be recognised that individuals in different generations may be responding appropriately to the different circumstances in which they find themselves. Policy-makers could therefore risk doing more harm than good if they seek to increase saving rates without also improving the circumstances – in terms of their financial resources or returns to wealth – that younger people face.

[1] For example, Cribb, Hood and Joyce (2016), Resolution Foundation (2019) and Cribb (2019)

Authors

Rowena Crawford

David Sturrock

David’s research covers household wealth, intergenerational transfers, social mobility, pensions taxation, and health and work at older ages.

More from IFS

Understand this issue

Policy analysis

Academic research