Downloads

R119%20-%20The%20EU%20Single%20market%20-%20Final.pdf

PDF | 560.11 KB

On 23 June 2016, the UK public voted in favour of leaving the European Union. However, important decisions remain about the model for the UK’s relationship with Europe outside of the EU, not least whether the UK seeks to remain a ‘member’ of the Single Market or only seeks (tariff-free) ‘access’.

This report looks at exactly what the Single Market is and distinguishes between ‘membership’ and ‘access’, including the impact on the financial services sector. It also considers the potential for new trade deals beyond the EU and assesses the economic and public finance implications of the various options. This should inform the likely trade-offs between the level of access to the Single Market and other negotiating objectives such as control of immigration and budgetary contributions.

The Single Market

The ‘Single Market’ refers to the EU as one territory without any internal borders or other regulatory obstacles to the free movement of goods and services. The concept was central to the founding Treaty of Rome in 1957, which committed to ‘the abolition, as between Member States, of obstacles to freedom of movement for [goods,] persons, services and capital’.

However, a genuine single market requires a ‘level playing field’ of rules across national boundaries. This means removing ‘unfair’ regulatory restrictions and harmonising, or ensuring mutual recognition of, member-state regulation.

By aiming for free movement of goods and services, a single market goes beyond a ‘free trade area’ or ‘free trade agreement’, which are predominantly concerned with reducing, and in many cases eliminating, trade tariffs on goods between members. A single market tackles other trade costs – especially non-tariff measures such as licensing and other regulatory barriers to trade. As tariffs on global trade have fallen over time, so these non-tariff barriers have become relatively more important, and especially so in services trade. Estimates suggest the costs affecting services trade may be over twice those in goods.

Creating a more level playing field through reducing trade costs leads to higher living standards – it enables more trade to take place: lowering prices and increasing choice for consumers and businesses; and creating a larger market for firms, which enables more specialisation and competition. These benefits appear evenly spread – poorer consumers have benefited more from lower prices since more of their spending is on traded goods. That said more trade with low wage countries can reduce wages for domestic low-skill workers and increase inequality. Much of the analysis of this effect though has focussed on trade with countries such as China rather than relatively high wage EU countries.

Membership versus access

Full ‘membership’ of the EU Single Market substantially reduces the costs of trade within the EU. Whilst some costs such as transport costs and cultural barriers such as language remain, the Single Market eliminates tariffs (border taxes) and customs checks and, importantly, reduces non-tariff barriers, which are particularly important for services trade. Whilst any country has ‘access’ to the EU as an export destination, membership of the Single Market reduces ‘non-tariff’ barriers in a way that no existing trade deal, customs union or free trade area does.

If the UK were able to join the European Economic Area (EEA), we would enjoy near-full membership of the Single Market but likely be obliged to accept EU regulations and free movement of people and make a budgetary contribution. Obtaining membership of the Single Market without meeting these conditions would be unprecedented.

Beyond the EEA, the UK could seek a type of ‘free trade agreement’ (FTA) with the EU. This would likely mean better ‘access’ relative to a situation with no agreement by substantially reducing, and potentially eliminating, tariffs on goods. Some trade agreements, such as the forthcoming EU–Canada deal, also reduce some non-tariff barriers on services, though such deals are rare, harder to agree and stop well short of the kind of service access conferred by membership of the Single Market.

UK service sector and trade role

Service trade does not tend to be affected by tariffs or customs checks – so non-tariff barriers are especially important. Like many developed economies, the UK’s economy is predominantly service-sector based. However, the UK is unusual in that services play a significant role in trade – they have grown significantly in the last 15 years and we export considerably more than we import, creating a service ‘trade surplus’ equivalent to some 5% of national income.

The Single Market has focused increasingly on smoothing trade in services in the last two decades. For UK service exports, the EU is by far the largest market accounting for almost 40%, whereas emerging economies such as Brazil, Russia, India and China together account for less than 5%.

Financial services a key beneficiary of Single Market membership

Granting substantial access to the EU single market for financial services firms outside of EEA would be unprecedented. However, for the UK, EEA membership would come with the important risk that regulation of the UK’s leading international financial centre would be determined largely by decisions made by the EU with relatively limited UK influence. The benefits of passporting and membership will need to be balanced against this risk.

New trade agreements unlikely to substitute fully for EU trade

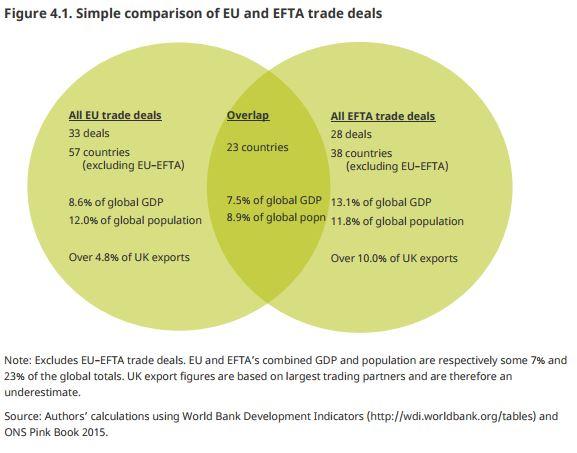

Outside of the EU, the UK would be able to pursue trade deals with other countries. As part of the European Free Trade Association the UK could strike bi-lateral deals and may be able to benefit from EFTA’s existing trade deals which are broadly similar in coverage to the EU’s and actually currently cover countries with a higher proportion of global GDP (13.1% versus 8.6%) and cover more of the UK’s exports (over 10%). Still, it is not clear that these trade deals would automatically apply to the UK as a new EFTA member, and they offer little enhanced access for services.

Even if UK exports to China grow in line with strong Chinese economic growth through to 2030, export levels are unlikely to reach anywhere near current levels with the US or EU. Trade deals might well facilitate export growth, especially in goods. However, trade deals that cover services are still relatively rare and they are time consuming to agree. In any case, trade deals that genuinely enable service trade, such as Single Market membership, tend to involve mutual regulatory recognition and harmonisation.

Macroeconomic and public finance impact of membership and access

In the short-term, indicators on the strength of the economy since the EU referendum are still emerging but the Bank of England has revised down its forecasts for growth throughout the next three years, with the largest revision to its GDP forecasts since the introduction of the Monetary Policy Committee in 1997.

However, in the medium to long-term, the model the UK chooses will matter significantly to the economy and living standards. Maintaining membership of the Single Market as part of the EEA could be worth potentially 4% on GDP – adding almost two years of trend GDP growth – relative to World Trade Organisation (WTO) membership alone. This would, on average, mean higher living standards and likely be distributed across income levels. Both theory and the available modelling suggest EEA membership would be likely to mean stronger UK economic performance than an FTA with the EU.

In terms of the public finance implications, the macroeconomic effects dominate the direct savings from a reduced direct EU contribution. On top of the £24–31 billion weakening of the public finances by 2020 from the short-term impacts of leaving the EU for an EEA or FTA scenario, WTO membership would leave the government needing to find a further £4–8 billion, and more in the long term. Contrasting EEA and an FTA is more difficult, as the assumptions on budget contributions matter and these are uncertain. Still, overall, even the UK’s current net EU budget contribution of £8 billion is small relative to public finance impacts from the economy relating to membership and access, and budget contributions may therefore be an area of potential compromise in negotiations.

Authors

Carl Emmerson

Carl, a Deputy Director, is an editor of the IFS Green Budget, is expert on the UK pension system and sits on the Social Security Advisory Committee.

Paul Johnson

Paul has been the Director of the IFS since 2011. He is also currently visiting professor in the Department of Economics at University College London.

Ian Mitchell

More from IFS

Understand this issue

Policy analysis

Academic research