Downloads

Download the report here

PDF | 566.59 KB

The Scottish Government has a range of tax powers at its disposal, which it has used in recent years to forge an increasingly distinct tax policy from the rest of the UK. In its 2025–26 Budget, the Scottish Government made a number of tax policy changes, including to income tax, business rates, and land and buildings transaction tax (LBTT). Alongside the Budget, the Scottish Government also published a Tax Strategy, setting out its approach to tax policymaking and evaluation and a number of priorities for tax policy and administration. Only the income tax changes were clearly linked to the new Tax Strategy.

This chapter of our report assesses the Scottish Government’s Tax Strategy and tax policy in turn; the next chapter looks in depth at one tax particularly ripe for reform – council tax.

Key findings

- The Tax Strategy aims to set out the Scottish Government’s medium-term plans for tax policy, administration and the policymaking process. After setting out some context, it provides a mix of concrete plans and vaguer ambitions under five headings: priorities for the existing system; the economy and tax; tax administration; evidence and evaluation; and future priorities.

- The publication of a Tax Strategy – not something the UK government has done –should be welcomed, and much of what it says is commendable. The aims set out for tax policy are good ones. There is a pleasing emphasis on evidence and engagement as central to future policymaking. The desire to improve administration of the tax system and public understanding of it is laudable.

- But this Tax Strategy is not a strategy for tax policy. It is full of good intentions to engage with others to improve tax policy and delivery, but it says little about the long-term direction of tax policy itself. It does not tell us what kind of tax policy the Scottish Government thinks would best promote its objectives; it does not provide a vision of what individual taxes or the tax system as a whole should look like in 5, 10 or 20 years’ time. It is more of a framework for producing a strategy than a strategy in itself.

- The Tax Strategy recommits the Scottish Government to complete the devolution of taxes already legislated for but not yet implemented – Scottish aggregates tax and air departure tax – but gives no guidance on the future direction of these taxes. No specific priorities for further significant tax devolution are identified, although in a separate submission to a UK parliamentary inquiry, the Scottish Finance Minister says that the current government’s position is that all taxes should be devolved.

- The 2025–26 Budget announced an above-inflation increase in Scotland’s basic and intermediate income tax thresholds, and a two-year freeze in the higher-, advanced- and top-rate thresholds. This continues a pattern of (small) tax cuts for the lower-income half of Scottish income taxpayers and (bigger) tax rises for those on higher incomes. Following these changes, individuals with incomes below about £30,300 will pay up to £28 a year less income tax in Scotland than in the rest of the UK, while those with higher incomes will continue to pay significantly more: £1,528 more for someone with an income of £50,000, and £5,207 more for someone with an income of £125,000. The Tax Strategy commits the Scottish Government to evaluating responses to these tax differences, which could, for example, include people with higher incomes moving to the rest of the UK.

- Business rates will be frozen in 2025–26 for properties with a rateable value of up to £51,000. This will likely benefit occupiers in the short term but landlords in the long term as rents adjust upwards, and will increase the cliff-edge in rates bills at that point (bills for larger properties will increase by 1.7%, in line with inflation). A new discount of up to 40% for small hospitality businesses will be put in place for 2025–26. This will benefit hospitality businesses, but if made permanent would hurt other types of businesses (such as retailers) as property rents would increase, with landlords again the beneficiaries.

- The 2025–26 Budget further increased the top-up to LBTT paid on the purchase of second homes (including rental properties) from 6% to 8% of the purchase price. This means that a landlord buying a £500,000 property, for example, must now pay £63,350, or 12.7%, in LBTT on top of the purchase price (compared with £23,350, or 4.7%, if bought as an owner-occupier’s main home). This makes Scotland’s most ill-conceived tax even bigger and more damaging. The change will encourage owner-occupation, but will make it even more difficult and expensive for those who remain in the rental sector – tenants (who are likely to face higher rents as a result of the policy) as well as landlords.

2.1 Assessing the Scottish Government’s new Tax Strategy

Chapter 1 of the Tax Strategy (Scottish Government, 2024a) says it sets out the Scottish Government’s ‘medium-term ambitions for how the tax system will develop to support the delivery of our four government priorities: eradicating child poverty, growing the economy, tackling the climate emergency, and ensuring high quality and sustainable public services’. Moreover, it aims to ‘support the progression to a tax system which aligns policy aims with outcomes, is informed by robust evidence and engagement with others, and enables us to take a system wide and comprehensive approach to tax policy in Scotland’.

But what exactly does the strategy cover? Does it deliver what it sets out to do? And does it represent a meaningful, coherent strategy for the future of the Scottish tax system – including the Scottish Government’s priorities for further tax devolution?

What does the Tax Strategy cover?

After setting out its high-level vision for the Tax Strategy, the remainder of chapter 1 describes the tax powers devolved to the Scottish Government and the institutional underpinnings for the collection of these taxes (by Revenue Scotland and HMRC) and forecasts of their revenues (by the Scottish Fiscal Commission). It highlights how policies enacted so far have increased the progressivity of the tax system and raised additional revenue to help fund devolved spending. It also recognises the trade-off between raising revenue and potential impacts on taxpayer behaviour and economic competitiveness. In addition, it references the potential role for taxation in ‘encouraging positive behavioural change’ (e.g. by accounting for the potential negative externalities from the use of land for landfill waste disposal and the extraction of sand, gravel and rock).

Chapter 2 of the strategy document sets out the economic and fiscal context in which the Tax Strategy has been made. This includes out-turns and forecasts for revenues, a range of facts and figures for each devolved tax, and demographic projections for an increasingly elderly population which will impact both revenues and public spending requirements. The chapter also highlights some of the key determinants of tax revenue, including employment, earnings and other income growth, property prices and transactions volumes, and the impact of both Scottish and UK government policy decisions (the latter impacting either directly, or indirectly via affecting the size of the block grant adjustments deducted from the Scottish Government’s block grant funding to account for devolved revenues). It also discusses some of the factors underlying recent income tax revenue performance, and the downside risks associated with current income tax revenue forecasts.

All of that is context. The meat of the strategy is set out in chapter 3, and is organised into five main subsections:

- Priorities for the existing system. This includes plans for income tax in 2026–27, information on the Scottish Government’s approach to engaging on and exploring options for local taxation, and a restatement of its commitment to complete the devolution of several taxes already legislated for (we discuss what the strategy says about tax devolution in further detail below).

- The economy and the tax system. A number of actions outside the tax system to support economic and hence tax-base growth are highlighted, including the provision of employability support and the focus of Scotland’s Migration Service on helping employers recruit internationally. This subsection also commits the Scottish Government to review the evidence on how tax policy affects the economy, with an evidence review for income tax to be published this year, and to engage with business on cumulative impact assessments of UK, Scottish and local tax policies.

- Administration of the existing tax system. Priorities identified include improving the public’s understanding of tax, strengthened arrangements for ensuring tax compliance, lower administration and compliance costs, and consideration of making regular changes to devolved taxes via primary (rather than secondary) legislation via the equivalent of the UK’s Finance Bill process.

- Evidence and evaluation. This subsection commits the Scottish Government to a systematic programme of tax policy appraisal and evaluation, with a formal impact evaluation of recent income tax changes and a review of land and buildings transaction tax (LBTT) specifically identified. A set of ‘areas of research interest’ – essentially, questions or issues the Scottish Government is interested in research being undertaken on – is also published as an appendix to the Tax Strategy.

- Future priorities. These include further work to identify which additional tax powers the Scottish Government should prioritise for devolution, explore the potential role of wealth taxation, and consider the role that taxation could play in encouraging positive behavioural change (seemingly with an environmental context in mind).

How useful is it as a strategy?

There is much to welcome in the Tax Strategy. It is to the Scottish Government’s credit that it has published something on this topic at all – not something the UK government has done, despite much urging.1 And much of what it says is commendable. The aims set out for tax policy are good ones. There is a pleasing emphasis on evidence and engagement as central to future policymaking. The desire to improve administration of the tax system and public understanding of it is laudable. The document is full of worthy ambitions.

But it is not a strategy for tax policy.

A strategy for tax policy would set out the Scottish Government’s vision of what a good tax system for Scotland would look like in 5, 10 or 20 years’ time, and how we should expect tax policy to evolve towards that in the coming years. It would trace a path connecting first principles and the Scottish Government’s overarching objectives to concrete policy.

More specifically, it would ideally address the following four groups of questions:

1 What tax powers should be devolved?

Which existing tax policies should be set at the UK level, which at the Scottish level and which by Scottish councils? What new taxes should Scotland be able to introduce unilaterally? If the Scottish Government would like more tax powers to be devolved, what would be its priorities and why? Considerations might include the mobility of different tax bases, the desire for Scotland to diverge from UK policy, and administrative practicality, among other things.

2 What ideal tax system is the Scottish Government aiming for?

Given Scotland’s existing tax powers, how should each tax be designed (and administered) to best meet the Scottish Government’s long-term objectives? How should the different taxes fit together and what is the appropriate balance between them? What is the role of tax (versus non-tax policies) in achieving those objectives? What should, or should not, be taxed at all?

How should devolved Scottish tax policy relate both to equivalent tax policies elsewhere in the UK and to reserved tax policies affecting Scotland, and how should the Scottish Government approach tax policymaking when only parts of the Scottish tax system are within its control? And what might tax policy look like if it had more of the tax powers it wanted? A tax strategy clearly could not describe what tax policy choices would be made under every possible scenario for devolution, but it could give a sense of the principles, priorities and considerations that would drive the Scottish Government’s decisions.

3 How should we get there?

What steps does the Scottish Government plan to take to move towards its ideal, and over what time frame? Should it pursue a ‘big bang’ reform or incremental improvements? How could dauntingly ambitious reforms be broken down into more manageable steps? Do some changes need to precede others, or are some higher priority, or can some be achieved more quickly? What process of evidence-gathering, consultation etc. will it undertake?

4 How might the destination change over time?

How should features of the system – from tax thresholds to property valuations – evolve over time by default in response to inflation and other changes in the economy? And in an uncertain world, where it is not feasible or sensible to say with certainty what every tax rate should be many years into the future, which features of tax policy should be kept stable and which should respond to changing circumstances and priorities? Again, a tax strategy cannot specify exact policy for every possible eventuality, but it can give principles and guidance which help to make its likely response to new developments more predictable.

These are difficult questions. It would be asking a lot for the Scottish Government, in the 18 months it has taken to produce this document, to have produced a tax strategy covering all of this and going from first principles to a fully mapped-out plan for tax policy over the medium-to-long term.

But it is not clear that the document provides much of an answer to any of these questions.

Chapters 1 and 3 both begin by setting out laudable aims for a tax strategy or tax policy. These include, for example, taking a system-wide and comprehensive approach, building on underlying principles, robust evidence and engagement with others; a tax system that supports the delivery of government priorities, aligning policy aims with outcomes; going beyond annual budget cycles; and recognising the risk of unintended consequences. These are all worthy ambitions; it is hard to argue with any of them.

But these are ambitions and criteria for how tax policy will be produced in future: the Tax Strategy does not actually undertake the task and reach conclusions. What combination of tax policies would best promote economic growth, or fairness, or simplicity, or environmental sustainability? We are not told.

Of the five subsections of chapter 3 listed above, only the first and last are concerned with what tax policy might actually look like.

The strategy for income tax policy

The only specific policy plans are for income tax rates and thresholds, setting out the following intentions for the remainder of this Parliament (i.e. up to May 2026):

No new bands.

No increase in rates.

Uprate the starter- and basic-rate bands by at least inflation. 2

Freeze the higher-, advanced- and additional-rate thresholds (subject to annual review at the Budget).

Keep over half of Scottish income tax payers paying less income tax than they would in the rest of the UK.

Refraining from adding any more bands to the already overcomplicated Scottish income tax schedule is unambiguously welcome. Adding ever more bands does nothing to the distribution of tax payments that could not be closely approximated by adjusting existing rates and thresholds; it complicates the tax schedule for little-to-no economic benefit.

The rest are reasonable policy choices. But it is hard to see them as part of a broad tax strategy.

There is no indication of why the lower bands should be uprated but the upper thresholds frozen, or why the aim is for more than half of taxpayers to pay less income tax than they would in the rest of the UK (apparently irrespective of how much less, or of how much more the remainder pay, or of how much people pay in other taxes). There is no sense of whether and how this income tax policy is joined up with other tax policies as part of an integrated plan for the Scottish tax system as a whole. If there is any such strategic thinking behind the announcement, the Tax Strategy would surely have been the place to spell it out.

It does differ from a typical Scottish Budget announcement in giving a statement of intent for the whole of the remainder of the Parliament. In practice, at this stage of the electoral cycle, that covers only one extra year. But the principle is worth considering. On the one hand, it helps to give individuals and businesses some forward guidance, reducing their uncertainty about likely future taxes; ‘signalling a period of stability’ is the rationale the Scottish Government gives. On the other hand, it ties the Scottish Government’s hands – or at least reduces its room for manoeuvre – if changing circumstances or policy preferences mean it looks to raise more revenue in future. The Tax Strategy gives no guidance on these pros and cons. When is making commitments a better/worse idea? Which features of tax policy should be kept flexible and used to respond to changing desires to raise revenue or redistribute, and which should be kept stable regardless of these?

The strategy for other devolved tax policies

On other existing taxes, there is little indication of the Scottish Government’s long-term intentions.

For the two next biggest devolved taxes – business rates and council tax – there is an intention to engage with others to consider possible future directions for policy, but no indication of what such directions might be and why. It does not inspire confidence that much-needed reform will actually happen to taxes that are notoriously politically difficult to reform.

Policy on land and building transaction tax is not mentioned at all, except in the context of a review which seems to be focused on detailed technical issues and unusual cases, rather than the underlying rationale for, and design of, the tax. Outside income tax, the biggest tax policy change in the Budget was an increase in the additional LBTT that must be paid on the purchase of second or rental homes, discussed in Section 2.2 below. There is nothing in the Tax Strategy that would help us to assess the merits of this change and how it contributes to – or detracts from – the Scottish Government’s ultimate aims for tax policy, or to judge whether we should expect, in five or ten years’ time, LBTT overall to be higher or lower and the gap between LBTT on first and additional homes to be bigger or smaller.

The relationship with tax policy in the rest of the UK

Some of the tax policy announcements in the Budget mirror changes made by the UK government (on Scottish landfill tax rates, LBTT and business rates); in some places, the Budget refers to the competitiveness of Scottish tax rates vis-à-vis the rest of the UK (non-residential LBTT, business rates for all but the highest-value properties); while in other contexts, the Scottish Government also highlights the greater progressivity of Scottish tax policy than UK tax policy.

Yet there is nothing in the Tax Strategy about the trade-offs between the simplicity benefits of having a system aligned with that elsewhere in the UK, the benefits of diverging to reflect different preferences and circumstances in Scotland, and the benefits of being competitive, or about how those trade-offs might differ across different areas of tax policy. For example, the fact that property is immobile and its supply is relatively unresponsive to taxation means that there is much less economic imperative for the property tax regime to be competitive with that in the rest of the UK (rUK) – or elsewhere – than for other taxes.3 Property taxation is an area where Scottish policy could easily and productively diverge from that in rUK if the Scottish Government wished to forge its own path.

Future priorities

More informative than the discussion of priorities for most existing devolved taxes is the discussion of future priorities. While the desire to seek further devolution of tax powers from the UK government is vague and unsurprising (see below), the other parts – ‘reviewing how tax is balanced across labour, income and wealth, and considering how tax can be used to encourage positive behavioural change’ – signal the direction of travel that interests the Scottish Government: towards more taxation of wealth and more environmental taxation. The Scottish Government did not have to pick out those two particular areas: that it did so provides genuine insight into its thinking. The Tax Strategy gives little by way of rationale or detail – it does not itself provide the promised review or consideration – but promises ‘we will set out our detailed programme of work on future priorities alongside the next MTFS [Medium-Term Financial Strategy] in [May] 2025’. We await that with interest.

The Tax Strategy and future tax policymaking

Beyond the design of tax policy itself, much of the rest of the Tax Strategy sets worthwhile goals that are easy to endorse.

The Tax Strategy is peppered with sensible-sounding promises to engage (or continue engaging) with others: with local government on the future of council tax, with business and other stakeholders on the operation of business rates, with HMRC on improving tax administration, with researchers on the evidence on the effects of taxation, and so on – including ‘reaching out to groups who may not often contribute to the conversation on tax’. This is all welcome.

Likewise, policymaking should of course be informed by robust evidence, so the emphasis on gathering that, including by publishing a review of the evidence on income tax this year and more broadly by developing ‘a systematic and regular programme of appraisal and evaluation across the Scottish tax system’, is welcome. From a researcher’s point of view, the appendix that lists the Scottish Government’s ‘areas of research interest’ (ARIs) – research questions on which it would value external input – is particularly helpful, so that future research can be focused where it will be most valuable to policymakers. The promise of ‘exploratory funding available to support the development of these ARIs’ makes it more likely that such research will actually happen.

The aims to work with others to improve public understanding, tax compliance, tax collection mechanisms and the legislative process are all laudable. The steps mentioned, such as publishing ‘externally commissioned research on international best practice on tax communications and engagement’ and ‘an updated compliance plan for Scottish Income Tax, increased communication with taxpayers to promote good compliance, and risk-based analysis of compliance risk’ all sound useful. But these are still just about how the Scottish Government will engage and produce plans in future – not actual plans now with concrete proposals. It remains to be seen what will be achieved in practice.

So, the Tax Strategy is full of ambitions and promises for tax policymaking in future, but says little about the long-term direction of tax policy itself.

It is more of a framework for producing a strategy than a strategy in itself.

What does the Tax Strategy say about further tax devolution?

In contrast with the sections on tax policy in previously published financial strategies, the Tax Strategy says little directly about the Scottish Government’s priorities for further tax devolution.

It restates its intention to enact taxes already agreed for devolution and legislated for, but yet to be enacted: the Scottish aggregates tax (which will replace the existing UK-wide aggregates levy) by April 2026, and the air departure tax (which will replace the existing UK-wide air passenger duty) once subsidy control rules related to exemptions for flights to the Highlands and Islands are resolved. The increase in the number of taxes managed by Revenue Scotland and the (small) increase in revenues that would be devolved to the Scottish Government are highlighted. However, the opportunity to provide information on the direction of tax policy for these two taxes is missed: even if the plan, at least initially, is to mirror existing UK policy to provide certainty and stability to taxpayers, that is worth stating.4

The strategy highlights a request made to the UK government for powers to create a Scottish building safety levy payable by the developers of residential properties, to replicate a policy legislated for in England and to be enacted this autumn.5 However, it does not reference plans to consult on proposals for councils to be able to charge a levy on cruise ships.6

The unsuitability of the method – based largely on a household survey with a small sample size – initially proposed for assigning half of estimated VAT revenues raised in Scotland to the Scottish Government is recognised. Instead, alternative options are to be explored, although what these may be is left unsaid. Do they, for example, include options that would require additional reporting by businesses (e.g. on the location of their sales and customers within the UK)?

Beyond this, any proposals on wealth taxation or tax policies to influence behaviour towards the environment coming out of the aforementioned exploration of these issues would likely require further devolution (unless implemented via local taxation powers). However, there is no reference to the devolution of VAT, National Insurance contributions or full powers over income tax, which was highlighted in the most recent Medium-Term Financial Strategy as desirable (Scottish Government, 2023). It appears that remains the position of the Scottish Government, though, with a recent submission to a House of Commons Scottish Affairs Committee Inquiry going even further and calling for the devolution of all taxes under ‘full fiscal autonomy’.7

Thus, while it is welcome that the Tax Strategy shifts the focus onto priorities for the use of powers and reform of tax policy processes already under the Scottish Government’s control, there was a missed opportunity to at least bring together what the Scottish Government has said before about further tax devolution and explain how additional powers could help achieve tax policy objectives.

2.2 Assessing the Scottish Government’s tax policy decisions

The 2025–26 Budget itself (Scottish Government, 2024b) made several changes to Scotland’s tax policy, including to income tax thresholds, rates and reliefs in business rates, LBTT rates for the purchase of second and rental homes, and Scottish landfill tax rates. As shown in Table 2.1, this mix of revenue-reducing and revenue-raising measures is forecast by the Scottish Fiscal Commission (SFC) to raise a net £54 million in 2025–26, rising to £207 million in 2026–27 and £241 million in 2029–30. These amounts are small in the context of forecast revenue of £25 billion in 2025–26 and £30 billion in 2029–30.

Table 2.1 Tax policy changes announced in the 2025–26 Scottish Budget (£ million)

Tax policy change | 2025–26 | 2026–27 | 2029–30 |

Income tax |

|

|

|

Increase basic- and intermediate-rate thresholds by 3.5% in 2025–26 | –24 | –25 | –28 |

Freeze higher-, advanced- and top-rate thresholds in 2025–26 and 2026–27 | +76 | +211 | +244 |

Business rates |

|

|

|

Freeze basic poundage rate for 2025–26 | –9 | –11 | –12 |

Continue Islands and Remote Areas Hospitality Relief for 2025–26 | –5 | 0 | 0 |

Introduce partial mainland hospitality relief for 2025–26 | –22 | 0 | 0 |

LBTT |

|

|

|

Increase additional dwelling supplement from 6% to 8% | +32 | +29 | +33 |

Scottish landfill tax |

|

|

|

Increase rates to match UK landfill tax rates | +6 | +4 | +4 |

Total | +54 | +207 | +241 |

Source: Scottish Fiscal Commission, 2024.

Income tax

Unlike the last two years, there will be no changes to Scottish income tax rates in 2025–26 (with the Tax Strategy stating an intention to keep them the same in 2026–27 as well, as discussed above). Changes were made to thresholds, though, slightly reducing the income tax paid by low- and middle-income taxpayers and increasing the tax paid by high-income taxpayers relative to indexing tax bands in line with inflation.

- The threshold above which the basic (20%) rate becomes payable will increase by 3.5% from £14,876 to £15,397 in 2025–26, with the threshold at which the intermediate (21%) rate becomes payable also increasing by 3.5% from £26,561 to £27,491. Compared with indexing the starter- and basic-rate bands by inflation (the SFC’s default forecasting assumption),8 which would have seen the thresholds increase to £14,915 and £26,799 respectively, this saves basic-rate taxpayers £5 per year and intermediate-rate taxpayers £12 per year.

- The thresholds at which the higher, advanced and top rates of income tax become payable will be frozen at £43,662, £75,000 and £125,140, respectively, in 2025–26 and 2026–27. Compared with indexing the relevant tax bands in line with inflation (the SFC’s default forecasting assumption), which would have seen these thresholds increase to £44,191, £76,061 and £127,267 respectively, in 2025–26 this will cost higher-rate taxpayers £98 per year, advanced-rate taxpayers £136 per year and top-rate taxpayers £199 per year. The further freeze planned for 2026–27 will increase these losses to approximately £280, £360 and £530 per year respectively.

Taken together, these changes raise income tax revenue in a broadly progressive manner, continuing the long-standing pattern of Scottish income tax policy. With all income tax thresholds frozen in the rest of the UK, these changes increase the extent to which low- and middle-income taxpayers pay less tax in Scotland: they will pay up to £28 per year less in Scotland, as opposed to £23 this year. The changes will slightly reduce the extent to which higher-income taxpayers pay more in Scotland: for example, someone on £50,000 will pay £1,528 more, down from £1,542 more in the current financial year.

Figure 2.1 shows the marginal rate structure for Scotland’s income tax in 2025–26, while Figure 2.2 compares income tax liabilities in Scotland and rUK.

Figure 2.1. Income tax marginal rate structure, Scotland and rUK, 2025–26

Figure 2.2. Difference in income tax liability between Scotland and rUK

Note: Assumes all income is non-savings, non-dividends income.

In 2025–26, the marginal rate of income tax will be higher in Scotland than in rUK on incomes above £27,492 (the intermediate-rate threshold), with particularly large differences of 22 percentage points (42% as opposed to 20%) for incomes between £43,662 and £50,270 as a result of Scotland’s lower higher-rate tax threshold, and of 7.5 percentage points (67.5% as opposed to 60%) for incomes between £100,000 and £125,140 as a result of the interaction of the UK government’s tapering of the tax-free personal allowance and Scotland’s 45% ‘advanced’ rate of income tax.

The marginal rate structure is significantly more complex in Scotland than in rUK, with six official tax rates (in addition to the 0% up to the personal allowance) and a seventh created by the tapering of the personal allowance above £100,000. As discussed in Adam and Phillips (2021), this proliferation of rates, and especially having separate 19%, 20% and 21% rates, is hard to justify economically: a small 0% band on top of the UK government’s tax-free personal allowance followed by a 21% rate would be both simpler and more progressive, taxing the lowest-paid income tax payers less than the system currently in place.

Figure 2.2 shows how the slightly lower bills in Scotland than in rUK for the majority of taxpayers are dwarfed by the much higher bills for those on higher incomes. It also shows how the additional tax paid by higher-income taxpayers in Scotland has built up over time. The amount paid by someone with an income of £125,000 is around £5,200 higher in Scotland than in rUK in both 2024–25 and 2025–26 (the changes in the Scottish Budget are relatively small), up from around £3,360 in 2023–24 and £1,700 in 2018–19. As discussed in Phillips (2024), evidence from both Scotland and other countries suggests that the additional tax due on high incomes will have affected taxpayers’ decisions over work, migration and the avoidance and evasion of taxes, potentially to the extent that the increases in the top rate of tax could have reduced rather than raised revenues (although the overall set of changes made to income tax by the Scottish Government since devolution is still almost certainly revenue-raising).

In its costings of the most recent reforms, the SFC assumes that such behavioural responses will reduce the yield from freezing the higher-rate threshold by 8%, the yield from freezing the advanced-rate threshold by around a quarter, and the yield from freezing the top-rate threshold by almost two-thirds (Scottish Fiscal Commission, 2024). These assumptions are plausible and draw on a wide range of evidence about how responsive taxpayers are to changes in tax policy.

Moreover, the SFC estimates that in the absence of behavioural responses to Scotland’s income tax policy changes, and if the underlying income tax base in Scotland had grown in line with that in rUK, the Scottish Government’s tax policies would mean its net income tax revenue position would be £1.7 billion in 2025–26, approximately 40% more than the actual forecast of £1.2 billion.9 To a large extent, this will reflect other factors depressing Scotland’s income tax base (such as slower private sector earnings growth in the late 2010s and early 2020s, in part linked to the declining high-paid oil and gas industry), but the impact of behavioural responses to Scotland’s higher tax on high incomes is also likely to have played a role.

Business rates

The 2025–26 Budget reduced business rates for two groups: permanently, for the occupiers of properties with a rateable value (i.e. estimated annual market rental value) of up to £51,000; and for 2025–26 only, for hospitality businesses and grass-roots music venues with a capacity of up to 1,500.

The tax rate on properties with a rateable value up to £51,000 (the ‘basic poundage rate’) will be frozen at 49.8% for the second year in a row,10 rather than increasing in line with inflation to 50.6%. This represents a permanent cut in business rate bills.

In the short term, this freeze will likely benefit the occupiers of properties up to £51,000 that pay business rates, although this will include large businesses occupying multiple small properties as well as the small businesses the Scottish Government says it is targeting for support. In the longer term, though, both theoretical and empirical evidence suggest that the main beneficiaries are likely to be commercial landlords, as rents and property prices rise (or fall less) relative to what they would otherwise have done.11 Some businesses could lose out: for example, those benefiting from the ‘small business bonus scheme’ which do not pay business rates could face slightly higher rents as a result of increased competition from those benefiting from lower rates bills. The freeze in the basic rate poundage while the intermediate poundage is increased in line with inflation to 55.4% will also increase the size of the jump in business rates at the £51,000 threshold to just over £2,850 (up from £2,400). This is equivalent to an 11% jump in business rates bill and an approximately 4% jump in combined rent plus rates bill at the £51,000 threshold. Charging £2,850 extra tax for a property that costs £1 more to rent is absurd – unfair and potentially distortionary – and it would be better for the Scottish Government to remove this cliff-edge, as it did elsewhere in the property tax system when it introduced LBTT (which has no such jumps) in place of stamp duty land tax (which did have at the time).

The extension of a relief of up to 100% for hospitality businesses in the Scottish islands and three remote mainland areas (Cape Wrath, Knoydart and Scoraig), and the introduction of a relief of up to 40% for hospitality businesses elsewhere in Scotland, apply in 2025–26 only. Reliefs will be capped at £110,000 per business (matching a cap in place for a broader relief for the retail and leisure sectors, in addition to the hospitality sector, in both England and Wales), and will be available only on properties with a rateable value up to £51,000 under the mainland Scotland scheme.

These schemes likely will help hospitality businesses, especially in the short term. If the reliefs were made a permanent feature of Scotland’s business rates system, we would expect the higher demand for properties suitable for hospitality usage to lead to much of the benefit being passed on to landlords (and hospitality businesses that own their own properties). Hospitality businesses themselves would still likely gain somewhat because increased demand from them for property would likely push up rents by less than they gain from lower rates bills. But other potential users of the properties (such as retail or leisure businesses, or residential renters if the properties are convertible) would likely lose out, as they too would face increased rents due to the higher demand from hospitality businesses but would not benefit from reduced rates bills.

The Scottish Government should make clear as soon as possible whether these new reliefs will be temporary, as announced, or made permanent (or at least long-term) features of the business rates system. It should avoid following policy in England where multiple one-year extensions to a broader relief for the retail, hospitality and leisure sectors increased uncertainty for businesses, landlords and the government’s finances. In contrast, the decisiveness with which the Scottish Government ended reliefs for the retail, hospitality and leisure sectors in place during the COVID-19 pandemic was welcome from a policymaking perspective.

These two new policies continue a Scottish trend – and wider UK trend – of increasing differentiation of business rates tax rates by property value and type of occupier. Figure 2.3 shows the rates bill as a percentage of rateable value for businesses in the hospitality sector (in blue) and other sectors (in red) in mainland Scotland assuming they occupy one property.

Figure 2.3. Scottish business rates as a percentage of rateable value, 2025–26

Note: Assumes a business occupies one property.

No rates are payable on properties with a rateable value up to £12,000 (provided the combined rateable value of all properties a business occupies is no more than £35,000) as a result of the Small Business Bonus Scheme for rates relief. For a business occupying a single property, the reduction in bill as a result of this relief is tapered from 100% for rateable values up to £12,000 to 25% for a rateable value of £15,000, above which the discount is reduced more gradually, finally being removed for properties with a rateable value of £20,000. This means, for sectors other than hospitality, business rates bills increase from 0% of rateable value for properties up to £12,000, to 37.4% for properties with a rateable value of £15,000, to the basic poundage of 49.9% for properties above £20,000. For properties in the hospitality sector on the mainland of Scotland, the 40% relief in 2025–26 means the equivalent tax rates will be 0%, 22.5% and 29.9%, respectively. Tax rates (and bills) jump up at a rateable value of £51,000, particularly for businesses in the hospitality sector as they will no longer be entitled to 40% relief at that point. There is a further small jump at £100,000, where the higher rate of business rates kicks in.

It is tempting to think of levying lower tax rates on low-value properties as akin to levying lower tax rates on low-income individuals, but the analogy is flawed. The people who ultimately bear the burden of a tax on business property – a combination of the taxpaying firms’ owners, employees, customers, suppliers or (most likely) landlords – are not necessarily any worse off for low-value properties than for high-value properties. Taxing lower-value business properties less heavily is not necessarily progressive with respect to household income.

The £35,000 cap on the total rateable value a business can occupy to receive the small business bonus relief means the relief does reduce the cost of property for small businesses relative to large businesses (which are likely to occupy multiple properties with a total rateable value of more than £35,000, or larger individual properties).12 This will mean more properties occupied by small businesses and fewer properties occupied by large businesses. The hospitality relief will also reduce the cost of property for relatively small hospitality businesses relative to other types of relatively small businesses (such as retailers, or small professional services businesses), affecting the size of these business sectors. These may be the intended effects of the reliefs, but by distorting business size and sector relative to what would otherwise pertain, the reliefs are not economically costless.

Land and buildings transaction tax

Purchases of second or rental properties in Scotland – around a fifth of housing transactions – are subject to an additional dwelling supplement (ADS) payable on top of the main rates of residential LBTT shown in Table 2.2.13 The 2025–26 Scottish Budget increased the ADS from 6% to 8% from 5 December 2024.

Table 2.2. Rates and thresholds of LBTT for residential property, 2025–26

Band | Rate | Proportion of transactions, 2023–24 |

£0–£145,000a | 0% | 36% |

£145,000a–£250,000 | 2% | 33% |

£250,000–£325,000 | 5% | 14% |

£325,000–£750,000 | 10% | 16% |

£750,000+ | 12% | 1.2% |

a£175,000 for first-time buyers.

Note: Rates apply to the part of the value in each band. Additional 8% of the full purchase price payable on transactions above £40,000 if the buyer owns another residential property.

Source: Proportions of transactions calculated by the authors from Revenue Scotland, LBTT monthly statistics, December 2024, https://revenue.scot/news-publications/publications/statistics/monthly-lbtt-statistics.

This increase in the ADS continues a trend. Before April 2016, there was no ADS. It was first brought in at that point at a rate of 3%, and has been gradually increased since then to its current rate of 8%.

Figure 2.4 shows what the new rate of ADS implies for tax bills. A landlord buying a £500,000 property, for example, must now pay an eye-watering £63,350, or 12.7%, in LBTT on top of the purchase price (compared with £23,350, or 4.7%, if bought as an owner-occupier’s main home). Many will be put off by that. (On that scale, the LBTT discount for first-time buyers – worth £600 for any purchase above £175,000 – is barely discernible on the graph.)

Figure 2.4. Land and buildings transaction tax on residential property transactions, 2025–26

Taxing property transactions is an exceptionally damaging way to raise revenue. It discourages mutually beneficial transactions, so properties are not owned by the people who value them most. That misallocation of property makes everyone worse off. The increase in the ADS makes a bad tax bigger and even more harmful.

The rationale given in the Budget was that it would raise revenue and that ‘the increased rate also supports the Scottish Government’s commitment to protect opportunities for first-time buyers in Scotland’. The SFC estimates that it will indeed raise revenue, around £30 million a year, though that is less than half of what it would have raised if people were not put off making such purchases by the tax increase (Scottish Fiscal Commission, 2024). And penalising the rental sector will indeed make it cheaper and easier for people to move into owner-occupation. What the Scottish Government did not mention is that it will also make it even more difficult and expensive for those who remain in the rental sector – tenants (who are likely to face higher rents as a result of the policy) as well as landlords.

The case for tilting the playing field even further towards owner-occupation and away from rental is doubtful: bear in mind that landlords must also pay income tax on their rental income and capital gains tax on any increase in the property’s value, neither of which applies to owner-occupiers. But in any case, an LBTT supplement is a bad way to do it. The ADS does not just penalise the rental sector; it penalises transactions within the rental sector. Preventing a landlord who wants to sell their property to another landlord from doing so is bad for both landlords and tenants.

This is even more pointed as it comes alongside a new power for councils to ask ministers to designate areas for rent controls. The combination of rent controls and high LBTT could lead to a withering of the rental market in some areas, and while some tenants could benefit, others would lose.

Unlike the ADS, the main rates and thresholds of residential LBTT have not changed (apart from a temporary COVID-related relief) since it replaced the UK-wide stamp duty land tax in Scotland in 2015–16. But freezing thresholds for a decade is a big real-terms reduction, again making the tax bigger (and therefore more damaging) over time: the resultant fiscal drag means that 64% of housing purchases were above the £145,000 threshold for paying the tax in 2023–24, up from 47% in 2015–16, and the number subject to the 12% top rate trebled in that time – still to only 1.2% of transactions, but accounting for 23% of revenue from residential LBTT (excluding the ADS).14

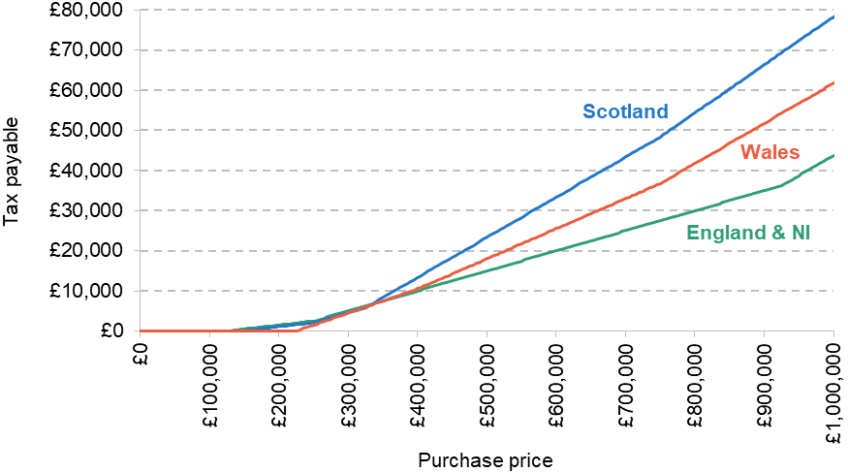

As with other taxes, Scotland’s tax on housing transactions is more progressive than that in England and Northern Ireland.15 Purchases above £333,000 are taxed more heavily in Scotland than in England or Northern Ireland (see Figure 2.5), and purchases below that level are taxed less – unless they are first-time purchases (since Scotland’s discount for first-time buyers is less generous than that in England and Northern Ireland) or second/rental properties (since Scotland’s supplementary tax on such purchases is higher).

Figure 2.5. Tax on residential property transactions, 2025–26

Note: Rates shown apply where the buyer is not a first-time buyer and does not have another residential property.

2.3 Conclusion

The Scottish Government’s Tax Strategy makes the right noises on a range of issues – notably on policy appraisal and evaluation, and the consideration of tax policy in the round – and should be welcomed in the context of the lack of such a document covering taxation as a whole at the UK level. It goes beyond the usual refrain of ‘more devolution, please’ to say something at least about policymaking for taxes already devolved to the Scottish Government.

However, as explained in this chapter, the published Tax Strategy is more of a framework and plan for the tax policymaking process, building in worthy commitments to engagement and evidence-gathering, rather than a strategy for tax policy or administration. With little over a year until the next Scottish election, the current Scottish Government may feel unable to set out more concrete medium-term plans. Whoever is in government in Scotland following the 2026 election should publish a strategy early in its term of office that does set a clear direction for policy for the rest of the next Parliament.

It is also notable that, with the exception of changes to income tax bands, the policies officially announced in the 2025–26 Budget seem somewhat divorced from the Tax Strategy. There is nothing in the Tax Strategy that helps us to understand and evaluate the increase in LBTT, for example. Indeed, it is not clear that that policy is consistent with any economically rational tax strategy.

Tax policy in the 2025–26 Budget did, though, largely follow the patterns of recent years, with increases in income tax for high-income taxpayers, further differentiation of business rates bills for different types of ratepayers and another rise in LBTT on purchases of second and rental homes. The Tax Strategy unfortunately does not provide much clarity on the extent to which this will continue to be this Scottish Government’s approach in 2026–27 and – if it wins the 2026 Scottish election – beyond.

References

Adam, S. and Phillips, D., 2021. The Scottish Government’s record on tax and benefit policy. IFS Briefing Note 324, https://ifs.org.uk/publications/scottish-governments-record-tax-and-benefit-policy.

Bond, S., Denny, K., Hall, J. and McCluskey, W., 1996. Who pays business rates? Fiscal Studies, 17(1), 19–35, https://doi.org/10.1111/j.1475-5890.1996.tb00236.x.

Cambridge Econometrics, 2008. The relationship between national non-domestic rates and rents on commercial property: empirical evidence from Enterprise Zones. HM Treasury / HMRC report, https://webarchive.nationalarchives.gov.uk/20080727055859/http://www.hmrc.gov.uk/research/report42.pdf.

HM Treasury, 2010. The corporate tax road map. https://www.gov.uk/government/publications/the-corporation-tax-road-map.

HM Treasury, 2024. Corporate tax roadmap 2024. https://www.gov.uk/government/publications/corporate-tax-roadmap-2024.

HM Treasury and HMRC, 2011. Tax consultation framework. https://www.gov.uk/government/publications/tax-consultation-framework.

Johnson, P., 2011. Defining a tax strategy. In M. Brewer, C. Emmerson and H. Miller (eds), IFS Green Budget: February 2011. https://ifs.org.uk/sites/default/files/2022-08/11chap9.pdf.

Phillips, D., 2024. The increases in Scotland’s top rate of income tax may have reduced revenues – although significant uncertainty remains. IFS Comment, https://ifs.org.uk/articles/increases-scotlands-top-rate-income-tax-may-have-reduced-revenues-although-significant.

Rutter, J., Dodwell, B., Johnson, P., Crozier, G., Cullinane, J., Lilly, A. and McCarthy, E., 2017. Better Budgets: making tax policy better. Institute for Government, https://www.instituteforgovernment.org.uk/publication/better-budgets-making-tax-policy-better.

Scottish Fiscal Commission, 2024. Scotland’s economic and fiscal forecasts – December 2024. https://fiscalcommission.scot/publications/scotlands-economic-and-fiscal-forecasts-december-2024/.

Scottish Government, 2023. The Scottish Government’s Medium-Term Financial Strategy. 6th edition, https://www.gov.scot/publications/scottish-governments-medium-term-financial-strategy-2/.

Scottish Government, 2024a. Scotland’s Tax Strategy: building on our tax principles. https://www.gov.scot/publications/scotlands-tax-strategy-building-tax-principles/.

Scottish Government, 2024b. Scottish Budget 2025 to 2026. https://www.gov.scot/publications/scottish-budget-2025-2026/.

Endnotes

Authors

Stuart Adam

Stuart is a Senior Economist working in the Tax sector, and focuses on analysing the design of the tax and benefit system.

David Phillips

David is Head of Devolved and Local Government Finance. He also works on tax in developing countries as part of our TaxDev centre.

More from IFS

Understand this issue

Policy analysis

Academic research