Summary

Next week will see the final – at least for now – rise in the minimum contribution rates that apply under automatic enrolment – the policy which obliges employers to enrol most employees into a workplace pension with the employee then free to opt out if they wish. This observation summarises new evidence on the impact automatic enrolment had as it was extended to affect smaller employers. This is important as over a quarter of private sector employees in the UK work for an employer who has fewer than 50 employees and prior to automatic enrolment (in 2012) just one-in-six of these employees were saving for retirement in a workplace pension.

Automatic enrolment is a key government policy to help employees save privately for their retirement. The policy means that all employers in the UK must enrol most of their employees into a pension scheme. Their employer must then make some contributions to the scheme, and usually the employee will make contributions too. If they want to, the employee can choose to leave the scheme – and therefore not have to make any contributions, but if they do nothing, they will remain in the scheme. Similar policies are gaining traction in other jurisdictions: in the United States California, Connecticut, Illinois, Maryland, and Oregon have all enacted similar policies while Germany, Ireland, and Poland are actively considering them.

Next week sees the final – at least for now – increase in the minimum contribution rates that apply under automatic enrolment: from 5% of eligible earnings (with at least 2% coming from the employer) to 8% of eligible earnings (with at least 3% coming from the employer). This increase will affect about one-in-four of the workforce (it will not affect the self-employed, employees who already contribute more than this amount or employees who have opted out).

In new IFS research released today, funded by the US based Laura and John Arnold Foundation, we have studied what the effect of this policy has been on the employees of small employers. This is important as over a quarter of private sector employees in the UK work for an employer who has fewer than 50 employees and prior to automatic enrolment (in 2012) just one-in-six of these employees were saving for retirement in a workplace pension. Because there is increasing international interest in learning from the UK’s experience of automatic enrolment, a summary of our analysis of automatic enrolment is published today by the Centre for Retirement Research at Boston College.

We have estimated the effect of automatic enrolment by using data from April 2016, at which point some small employers (in this research, those with fewer than 30 employees) had had to introduce automatic enrolment, and others had not, depending on their employer PAYE tax code. This means it was “as good as random” as to whether an employer had introduced it – making it much easier to compare outcomes under the policy to a counterfactual of what would have happened had the policy not applied. (This requires us to assume that employers do not choose to introduce automatic enrolment early, though we look for evidence of this and do not find it to be important.) We focus on those who are “eligible” for the policy (i.e. they earn at least £10,000 per year, are aged 22 to the “state pension age”, and have worked for their employer for at least 3 months).

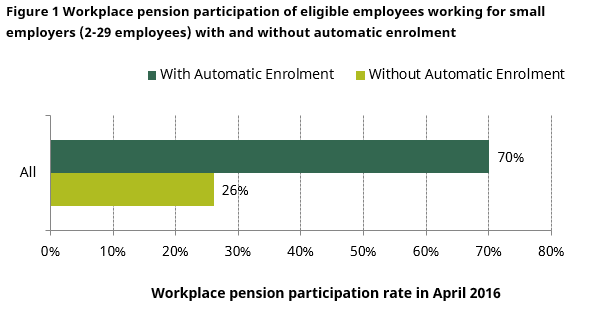

One headline is a huge difference in workplace pension participation for “eligible” employees of small employers with, and without, automatic enrolment, as shown in Figure 1. In absence of the policy, only 26% of employees would have been saving in a workplace pension, whereas once the policy was introduced, 70% of them were – meaning that the participation rate increased by an enormous 44 percentage points. This is even bigger than the increase we found for medium and large employers in its introduction between 2012 and 2015 (an estimated increase of 37 percentage points). As with larger employers, we also find that the largest increase in participation comes from groups that have the lowest participation in the absence of automatic enrolment: younger workers, those with lower earnings and those who have worked for their employer for less long.

Source: Table 2 from Cribb and Emmerson (2019).

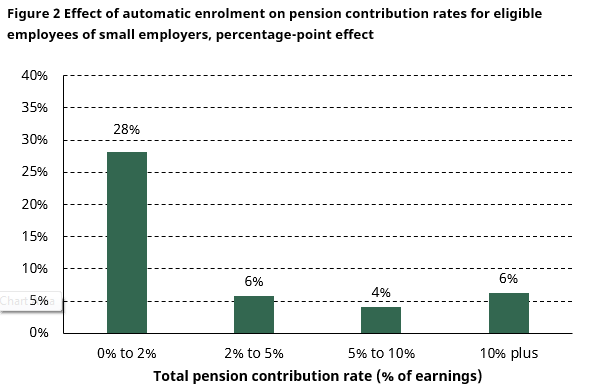

What is important for people’s retirement resources is not whether they are saving, but how much they are saving. In 2016, when the data were collected, the minimum that had to be contributed was 2% of “qualifying” earnings. That has now risen to 5% and next week will rise again to 8%. Figure 2 shows how much of the 44 percentage point increase in pension participation occurred at different contribution rates. Most of the increase – 28 percentage points of it – came from employees having very low minimum contributions. However, similar to the effect on larger employers, there were also significant increases in people having much higher contributions. For example, the policy caused an increase of 6 percentage points in the proportion who had a pension contribution of at least 10% of salary.

Source: Figure 2 from Cribb and Emmerson (2019).

These findings – very large increases in pension participation and even some increases in contributions in excess of the minimum levels – are a very positive story for the pension saving of the employees working for small employers.

Automatic enrolment has also reduced the gap in pension participation among those working for larger employers and those working for smaller employers, as it has had a smaller impact on the former than the latter. However a sizeable gap still remains: under automatic enrolment 88% of those working for medium or large employers are members of a workplace pension scheme compared to 70% of those working for an employer with fewer than 30 employees. Our research tests out different possible reasons for this pension participation gap.

This gap cannot be explained by observed differences in the types of employees working for smaller employers – for example their pay, occupation, gender or age. Nor is much of the gap explained by differences in the generosity of employer contributions.

It therefore remains a puzzle as to why the pension participation rate amongst smaller employers is lower. It could be that people who do not think or worry about their retirement are particularly likely to work for smaller employers, or that smaller employers encourage employees to opt out to save on the cost of providing the pension. Alternatively, it could be that small employers are less effective at communicating the benefits of saving in a pension, particularly if this is the first time that they have provided one.

Understanding this puzzle is important – a key issue for automatic enrolment is the extent to which it gets the right people into a workplace pension and the right people to opt out of being in one. This is the subject of ongoing research at the IFS. But overall the evidence so far on automatic enrolment is positive: large numbers of employees are brought into workplace pensions. While most are enrolled at relatively low contribution rates some are brought in at much higher levels of contributions. There is a case for going further – most obviously in terms extending the band of earnings to which minimum contributions have to apply or, perhaps, increasing the minimum rates of contributions – and for making any improvements sooner than the mid-2020s as the Government current proposes.

Authors

Carl Emmerson

Carl, a Deputy Director, is an editor of the IFS Green Budget, is expert on the UK pension system and sits on the Social Security Advisory Committee.

Jonathan Cribb

Jonathan is an Associate Director and Head of Retirement, Savings and Ageing sector, focusing on pensions, savings and later-life economic activity.

More from IFS

Understand this issue

Policy analysis

Academic research