We develop a new quantile-based panel data framework to study the nature of income persistence and the transmission of income shocks to consumption. Log-earnings are the sum of a general Markovian persistent component and a transitory innovation. The persistence of past shocks to earnings is allowed to vary according to the size and sign of the current shock. Consumption is modeled as an age-dependent nonlinear function of assets, unobservable tastes, and the two earnings components. We establish the nonparametric identification of the nonlinear earnings process and of the consumption policy rule. Exploiting the enhanced consumption and asset data in recent waves of the Panel Study of Income Dynamics, we find that the earnings process features nonlinear persistence and conditional skewness. We confirm these results using population register data from Norway. We then show that the impact of earnings shocks varies substantially across earnings histories, and that this nonlinearity drives heterogeneous consumption responses. The framework provides new empirical measures of partial insurance in which the transmission of income shocks to consumption varies systematically with assets, the level of the shock, and the history of past shocks.

Find the working paper here.

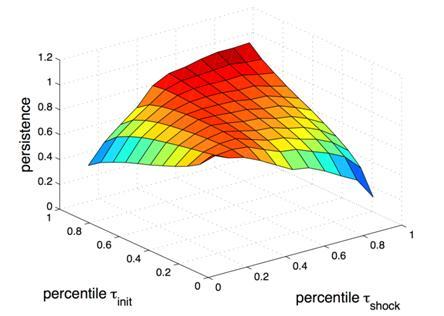

Figure. Quantile autoregression of log-earnings

Authors

Richard Blundell

Richard is Co-Director of the Centre for the Microeconomic Analysis of Public Policy (CPP) and Senior Research Fellow at IFS.

Manuel Arellano

Manuel is a Research Fellow of the IFS and a Professor of Econometrics at CEMFI, Madrid.

More from IFS

Understand this issue

Policy analysis

Academic research