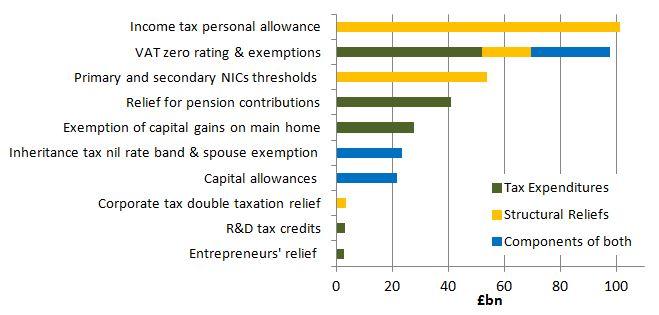

The UK has over 1100 tax reliefs. According to HMRC, we forego over £400bn of revenue each year as a result of reliefs. The top 10 categories (see Figure) cost £375bn. £34bn of the cost is for reliefs from corporation tax and capital gains tax for business assets. These are big numbers well suited to catchy headlines. You can make them particularly striking by comparing them to total government spending – around £800bn – or to corporate tax receipts – around £50bn. But these numbers aren’t particularly meaningful unless you know what tax reliefs are.

Helen Miller, Associate Director at IFS, will be part of a panel at tonight’s CIOT/IFS debate: Business tax reliefs - corporate welfare or essential elements of the tax system? Here she sets out some of the issues.

What’s a tax relief?

Much difficulty arises because there isn’t a clear definition of what counts as a tax relief. Many people will imagine tax reliefs as bungs to special interest groups. And while many reliefs are in place to, in HMRC’s words, ‘help or encourage particular types of taxpayers, activities or products for economic or social objectives, a large number can ‘be regarded as an integral part of the tax structure’. This conceptual distinction between types of reliefs serves to highlight that they can be part of a desirable tax system. But there is room for disagreement about which reliefs should be part of our tax structure and which activities should be encouraged. No matter how we define or classify them, any debate about tax reliefs must ultimately be a debate about tax design – what is it we want to tax and how do reliefs help us achieve that?

Economists want a broad base and low rates, right?

Economists can’t often be accused of clearly conveying their ideas. But one that seems to have been picked up widely is that a good tax system has a broad base and low rates. There’s something to this. Since almost all taxes distort (i.e. change) people’s behaviour in ways that are undesirable, it makes sense not to load all the distortions onto one tax base. A broad base also makes sense because exempting some activities or incomes creates boundaries in the tax system, which in turn create complexity and avoidance opportunities and often lead to unfairness. But, the broad base/low rate rule of thumb doesn’t imply zero reliefs are optimal. In fact, economists often advocate a narrow tax base and high rates. The treatment of North Sea oil, where there are large reliefs for investment costs but profits are taxed at 50% (and until recently at much higher rates), is a good example of this.

A better, admittedly less snappy, rule of thumb is to tax all income and deduct all costs of generating taxable income. The first part of this – tax all income – is related to the desirability of a broad base. The second part is an acknowledgement that a well designed base shouldn’t be too broad. One application of this is that it is desirable to tax companies’ profits rather than revenues. If we tax revenue, we will tax high-revenue, high-cost activities more heavily than low-revenue, low-cost activities. It is inefficient to favour activities that have low costs.

This rule of thumb gives a starting point for rationalising some reliefs as part of a well designed tax system. To continue the example, a well designed corporate tax base will allow firms to deduct costs from turnover to arrive at taxable profits. Wage costs can be immediately deducted. But there are multiple ways to deduct the cost of investment. Using the Annual Investment Allowance, firms can immediately deduct the full cost of the first £200,000 of spending on plant and machinery. For investment above this, they can use capital allowances to deduct a proportion of their investment spending over a number of years. But, there is no deduction for investment in industrial buildings. And while a firm can deduct the interest payments associated with financing an investment through borrowing, there is no equivalent deduction for the cost of using equity finance. The upshot is that our current system does not consistently deduct the cost of investment meaning that some investments are discouraged, some are incentivised and some are unaffected by the tax system. The policy takeaway is that we could do a better job of designing the corporate tax base but this does not mean that we should move to a system with no reliefs for investment expenditure. This is a good example where evaluating a relief requires digging into the policy detail.

When to use the tax system to incentivise?

As a starting point, it is desirable to design taxes in such a way that we minimise the extent to which they lead people or firms to change their behaviour. However, there are exceptions to this. Governments may want to use the tax system to incentivise some behaviours and disincentivise others. The resulting reliefs – such as R&D tax credits, Entrepreneurs’ relief, Patent Box, film tax relief – are those that are most likely to divide opinion. In these cases, we should ensure that there is a clear policy justification, that the policy is well targeted and that the benefits outweigh the costs.

R&D tax credits are a good example of a well justified policy. The market under invests in R&D because some of the benefits from investigating a new technology ‘spill over’ to other firms. R&D tax credits are an attempt to correct this ‘market failure’. They are directly targeted at the activity that we think is under provided – R&D investment – and evaluations show that the policy is cost effective; every £1 of tax credit leads to more than £1 of R&D investment and to an increase in the number of new innovations. This doesn’t imply that the relief has no costs beyond the revenue forgone. It introduces complexity and can lead firms to relabel activities as R&D. Even for a well justified and targeted relief, the benefits must be weighed against the costs.

It is plausible that investment by entrepreneurs also has spillovers and is underprovided. However, Entrepreneurs’ Relief – a large capital gains tax break given to most company owner-managers – is poorly targeted. Unlike R&D tax credits, it is not targeted at investment but at profits. It is available to many businesses that aren’t entrepreneurial but not available to entrepreneurs who cannot take their income in the form of capital gains. It distorts decisions over how income is received and incentivises tax motivated incorporation.

Which of the 1100 can we scrap?

Too many reliefs have weak or poorly articulated policy aims. Reliefs are often hard to rationalise as part of a tax base that reduces distortions or as a policy that is effective at achieving a well defined economic or social goal. To work out which we should scrap or modify, we should get more accustomed to digging into the details and evaluating how each relief stacks up against a clearly stated tax design. The bar for introducing any new relief should be high.

We could scrap some reliefs and increase revenues. But £250 billion of the £400 billion of “reliefs” mentioned above results from the income tax personal allowance, NIC thresholds and VAT zero rating and exemptions. Whether these should count as reliefs at all or as central structures of the tax system is moot. It’s clear that they are not easily and painlessly available as a route to raising more revenue. Lumping all existing reliefs together encourages the idea there are huge sums of money to be raised at little or no economic cost. There aren’t.

Top 10 categories of tax reliefs cost £375bn

Source: https://www.gov.uk/government/statistics/main-tax-expenditures-and-structural-reliefs. Notes: HMRC list 431 reliefs and cost 192. The 2017-18 cost in foregone revenue is £414bn. This should not be seen as the revenue that would be raised if we scrapped all reliefs because it does not account for any behavioural response or any interaction between reliefs. Some of the categories in the Figure are an amalgamation of reliefs (all exemptions and zero rating in VAT is in the second bar).

Other references:

The most recent Office for Tax Simplification (OTS) report list reliefs can be found here.

Data on government revenues and total spending can be accessed from the Office for Budget Responsibility’s public finance databank, available here: http://obr.uk/data/. Figures in the text refer to 2017-18, rounded to nearest £10 bn.

Places are still available at this evening’s CIOT/IFS panel event. To join the debate at the Royal Society of Arts in London, sign up here.

Authors

Helen Miller

Helen is Deputy Director of the IFS and Head of the Tax sector.

More from IFS

Understand this issue

Policy analysis

Academic research