Summary

Six years ago today, Child Benefit was first withdrawn from families containing someone whose annual income is above £50,000 a year. This threshold has since remained frozen in cash terms and there remain no plans to change it. This means that around 36%, or 370,000, more families will lose some Child Benefit in 2019–20 than in 2013–14. Continuing the freeze would mean that, from April 2021, significant numbers of families who do not contain a higher rate income taxpayer will begin to lose some of their Child Benefit for the first time. Moreover, by 2022 more than one in five families with children are set to lose at least some of their Child Benefit - up from one in eight when the policy was introduced. This is one of a growing list of examples of a part of the tax and benefit system being frozen, which never makes sense as an indefinite – and hence potentially permanent – policy.

On January 7 2013 Child Benefit, which is currently worth £1,079 per year for the first child and £714 for each subsequent one, ceased to be a universal payment to families with children. Since then families in which the highest-income parent in the household has an annual income between £50,000 and £60,000 a year have only been entitled to a partial payment. Where one adult has an annual income over £60,000, families have effectively been ineligible for any Child Benefit (technically families can still receive the benefit, before paying it back via an income tax surcharge on the higher-income parent).

- In its first full financial year of operation (2013–14), 13% of families with children (1.0 million) lost at least some Child Benefit as a result of this policy, with 0.7 million losing all of it. This saved the government a total of £1.6 billion in that year (in today’s terms).

- In 2019–20, we estimate that the share of families with children who are affected will be 18% (1.4 million, of whom 1.0 million will have lost all of their entitlement). The annual saving to government will have risen to £1.8 billion (in today’s terms). In other words, the number of families with children who are affected will have risen by about 36%, or 370,000, in just six years.

- This is mostly because the £50,000 threshold has not been indexed. As a result, it will have fallen by 9% in real terms by 2019–20. Had it been price-indexed, then in 2019–20 the threshold would be £55,000. This means 270,000 fewer families would be losing some or all of their Child Benefit, and the public finances would be worse off to the tune of £350 million per year. Had it been earnings-indexed the difference would be bigger still.

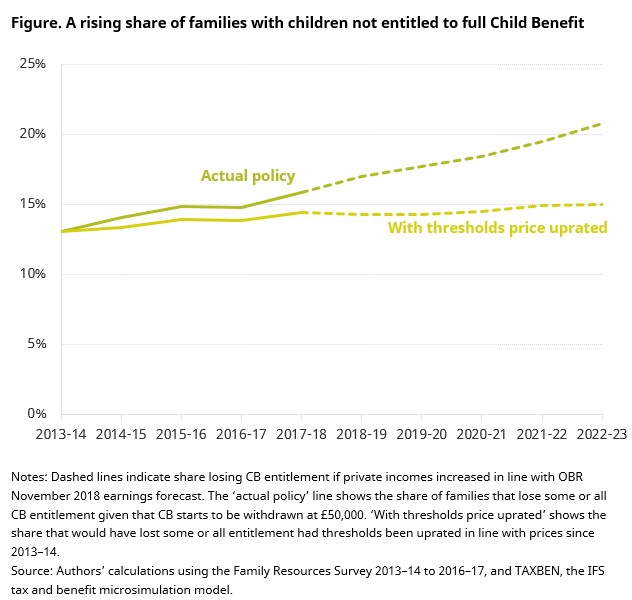

The figure shows the share of families with children not entitled to full Child Benefit over time. Under current policy, which is to continue to freeze both the £50,000 and £60,000 thresholds, the number of families affected by the withdrawal of Child Benefit would continue to increase, reaching 21% (1.6 million) in 2022–23. Very little of that increase would occur if the thresholds were uprated with prices (and virtually none of the increase would occur if they were uprated with earnings).

A further oddity is that when first announced – in the Spending Review of October 2010 – the plan was to withdraw Child Benefit only from families that contained a higher-rate taxpayer. At the time the higher-rate threshold was £43,875. In the March 2012 Budget the then Chancellor, George Osborne, announced that “instead of withdrawing Child Benefit all at once when people earn more than the higher-rate threshold – the benefit will only be withdrawn when someone in the household has an income of more than £50,000. … This means an extra 750,000 families will keep some or all of their Child Benefit.”

Because £50,000 was greater than the higher-rate threshold at the time, this was understandably seen as a more generous policy than the previous plan. But since then the higher-rate threshold has risen, while the £50,000 Child Benefit withdrawal point has remained frozen. As a result of the Autumn 2018 Budget, in both 2019–20 and 2020–21 the higher-rate threshold is set to be £50,000. This means that (broadly) the same number of families will lose some of their Child Benefit in those two years, as would have been the case under the original policy plan for the withdrawal of Child Benefit. Effectively the original policy, disowned by Chancellor Osborne in 2012, is being re-imposed by stealth.

Under current policy there will be a further twist in subsequent years. Because the higher-rate threshold is (sensibly) set to be indexed in line with inflation, but the £50,000 threshold for Child Benefit withdrawal is set to remain frozen, for the first time significant numbers of families without a higher-rate taxpayer will lose some Child Benefit. Given the current outlook for earnings growth, we estimate that this will be true of 60,000 families in 2021–22 and would double to 120,000 families in 2022–23.

This is not to say that the government is wrong to restrict Child Benefit to certain families. But what cannot be justified is to have an ever-increasing proportion of families exposed to the policy over time, with the increase determined by the rise in prices since 2013. If £50,000 was the right number in 2013, then it will not be the right number in 2023, and vice versa.

This lack of indexation has become increasingly prevalent in the tax and benefit system. The point at which the income tax personal allowance starts to be withdrawn (£100,000 a year), the point at which the 45p rate of income tax starts (£150,000 a year), the maximum annual pension contribution limit (£40,000), the personal saving allowances (£500 and £1,000), and the rates of winter fuel allowance are further examples where, by default, inflation erodes the real generosity of the system to an indefinitely greater extent over time. Most of those parameters have been introduced within the past decade, reflecting an increasing and unfortunate fashion for failing to specify a sensible uprating rule.

These are clearly designed to increase taxes, or reduce benefits, in a less visible (though often quite rapid) way. They are making a nonsense of any pretence of sensible design: the government is not even attempting to take a principled view of exactly which families should be keeping all of their Child Benefit, who should be paying higher rates of tax, and so on. Instead, it is simply allowing these choices to be buffeted around arbitrarily each year by inflation. Meanwhile, the cumulative impact it has in raising taxes or reducing benefits by stealth can do nothing for trust in government.

Authors

Carl Emmerson

Carl, a Deputy Director, is an editor of the IFS Green Budget, is expert on the UK pension system and sits on the Social Security Advisory Committee.

Robert Joyce

Robert is a Deputy Director. His work focuses on primarily on the labour market, income and wealth inequality, and the design of the welfare system.

Tom Waters

Tom is an Associate Director at the IFS and Head of the Income, Work and Welfare sector.

More from IFS

Understand this issue

Policy analysis

Academic research