The Government is spending around £50 billion more than it raises in revenue

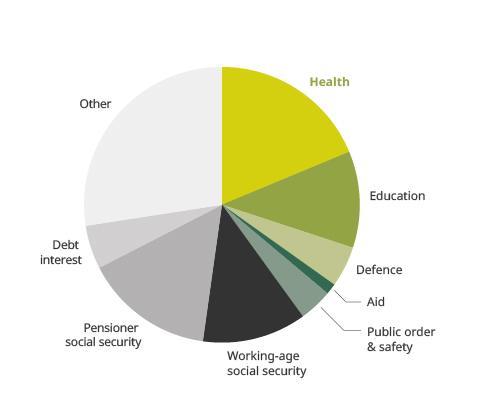

Figure 1a. Government spending, 2016–17 (£771 billion)

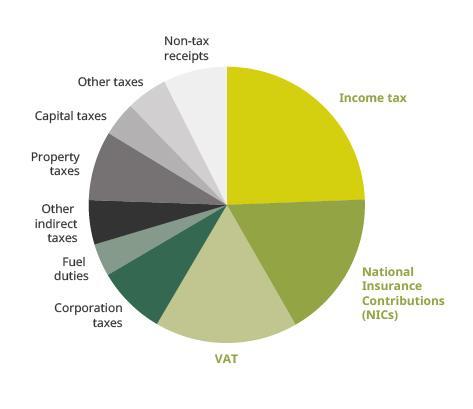

Figure 1b. Government receipts, 2016–17 (£726 billion)

Figures 1a and 1b show how the public sector spent and raised money last year. The largest single areas of spending are Social Security and Health, while three taxes (Income tax, National Insurance Contributions and VAT) account for 60% of government revenues.

Not unusually, the amount that the government spent last year was larger than the revenue generated. The difference between these two numbers is government borrowing, or the deficit.

Borrowing has returned to its pre-crisis share of national income and is set to fall further

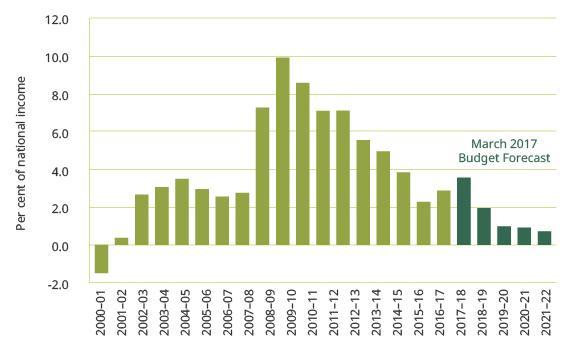

Figure 2. Government borrowing since 2000–01

Figure 2 shows how the deficit has evolved since the year 2000 (the last year in which the budget was in surplus), and how it was expected to evolve at the time of the last budget in March. The deficit increased dramatically between 2007–08 and 2009–10 during the great recession. After 7 years of “austerity” (spending cuts and tax rises), borrowing is now back to its pre-crisis level.

But current plans imply further spending cuts and tax rises over the next few years to reduce the deficit further, and the government aims to eliminate the deficit entirely by the mid-2020s. This is an ambitious target and is unlikely to be easy.

A likely downgrade to the outlook for productivity growth in the budget will push up forecast borrowing and mean the Chancellor has little room for budget giveaways

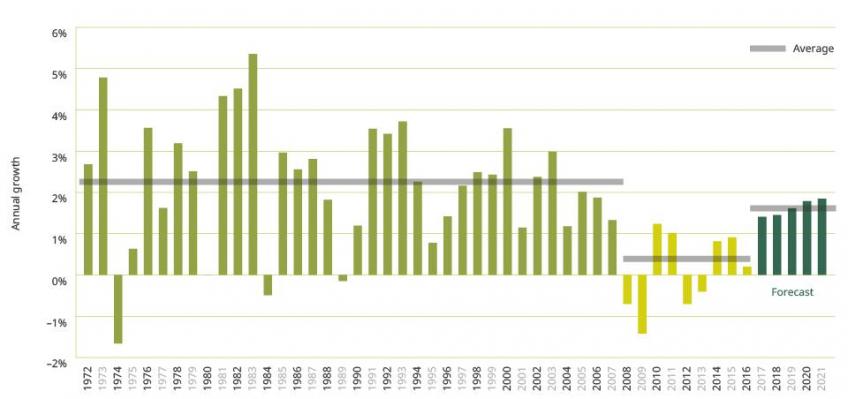

Figure 3. Output per hour annual growth since 1972

Figure 3 shows annual output per hour (productivity growth) since 1972, including the forecast for the next five years from March.

The most important driver of the government’s budget position is the economy – it was a reduction in the size of the economy (meaning, for example, lower wages), and a resulting reduction in tax revenues, that led to the deficit increasing dramatically in the late 2000s.

The key driver of economic growth is productivity growth, which has been historically terrible over the last 9 years and shows little sign of improvement. The forecast for productivity this time around is likely to be more pessimistic than in March – that means slower wage growth, slower economic growth and lower tax receipts which will mean higher borrowing.

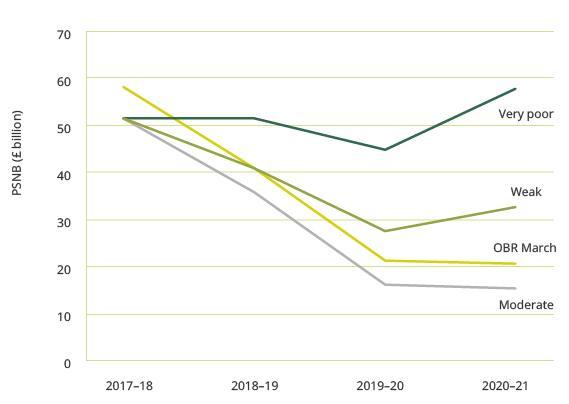

Figure 4. Government borrowing under different growth scenarios

A worse outlook for productivity is bad news for all of us, but it puts the Chancellor in a particularly tricky position. A significant productivity downgrade (represented by the ‘Weak’ and ‘Very Poor’ scenarios in Figure 4) would push up the borrowing forecast substantially. Given this it would be extremely difficult for the Chancellor to offer spending giveaways while still remaining committed to his deficit reduction targets.

On current plans, the spending of government departments will be squeezed further over the next two years

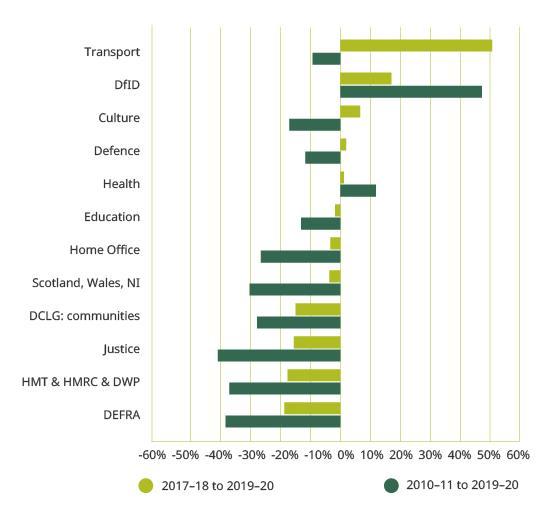

Figure 5. Real-terms departmental budget changes, 2010–11 to 2019–20

Figure 5 shows the real terms (i.e. accounting for inflation) change in the budgets of different government departments over the next two years and for the 2010s as a whole.

The Chancellor is facing calls to loosen spending in a number of areas, and based on this picture its easy to understand why. Almost all departments have faced tight settlements since 2010. Even departments that have been relatively protected from real terms cuts, such as the Department of Health, have experienced much smaller increases than the historical norm. Yet other departments, such as DEFRA or Justice, are set to see cuts of almost 40% over 10 years, with further cuts to be delivered over the next two years.

A post-election budget is normally a time for tax rises, which could be used to finance looser spending plans, but this is likely to be difficult for a minority government

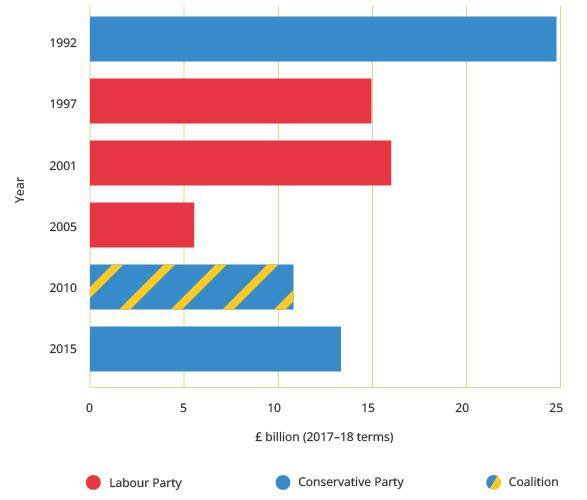

Figure 6. Long-run net tax rise from measures announced in the year following elections, 2017–18 terms

Figure 6 shows the net effect of tax rises announced in the year following every general election since 1992.

If the Chancellor wanted to ease the squeeze on spending while remaining on course to eliminate the deficit by the mid-2020s, one option might be to raise taxes. Indeed, this is what every Chancellor has chosen to do following elections since 1992. However, this may not be a feasible option this time. None of those previous governments were minority governments, and the parliamentary arithmetic this time around is likely to make it difficult to pass substantial tax-raising measures.

Notes

Figures 1a and 1b

Notes: ‘Government spending’ refers to Total Managed Expenditure. ‘Government receipts’ refers to Public Sector Current Receipts.

‘Other indirect taxes’ includes alcohol duties, tobacco duties, betting and gaming duties, air passenger duty, insurance premium tax, landfill tax, climate change levy, vehicle excise duties and soft drinks industry levy. ‘Corporation taxes’ includes corporation tax, petroleum revenue tax, oil royalties, bank surcharge, bank levy and diverted profits tax. ‘Property taxes’ includes council tax and business rates. ‘Capital taxes’ includes stamp duties, capital gains tax and inheritance tax. ‘Other taxes’ is a residual measure, including devolved taxes and environmental levies, which are generally part of government schemes that translate higher revenues directly into higher spending. Non-tax receipts include interest and dividend income and the operating surplus of publicly owned corporations

Sources: Office for Budget Responsibility, Public Finances Databank, October 2017 (http://budgetresponsibility.org.uk/data/); Office for Budget Responsibility, Economic and Fiscal Outlook, March 2017 (http://budgetresponsibility.org.uk/efo/economic-fiscal-outlook-march-2017/); HM Treasury, Public Expenditure Statistical Analyses, July 2017 (https://www.gov.uk/government/collections/public-expenditure-statistical-analyses-pesa)

Figure 2

Note: Figure shows Public Sector Net Borrowing

Source: Office for Budget Responsibility, Public Finances Databank, October 2017 (http://budgetresponsibility.org.uk/data/); Office for Budget Responsibility, Economic and Fiscal Outlook, March 2017 (http://budgetresponsibility.org.uk/efo/economic-fiscal-outlook-march-2017/).

Figure 3

Note: Black lines refer to average growth rates in the relevant periods (1972–2007, 2010–2016, 2017–2021).

Source: Office for National Statistics series LZVB; Office for Budget Responsibility, Economic and Fiscal Outlook, March 2017 (http://budgetresponsibility.org.uk/efo/economic-fiscal-outlook-march-2017/).

Figure 4

Note: ‘Moderate’ scenario assumes OBR downgrades growth in line with the Bank of England’s August Forecast. ‘Very poor’ scenario assumes that productivity growth is only 0.4% per year. ‘Weak’ scenario assumes OBR downgrades halfway towards the ‘very poor’ scenario (productivity growth of 1% per year on average).

Source: C. Emmerson and T. Pope Autumn 2017 Budget: Options for Easing the Squeeze, IFS Report 133 (https://www.ifs.org.uk/publications/10010).

Figure 5

Source: HM Treasury, Public Expenditure Statistical Analyses, July 2017 (https://www.gov.uk/government/collections/public-expenditure-statistical-analyses-pesa).

Figure 6

Note: Colour of bar refers to party or parties in government after the election. All figures based on the cost of the measure in the final year on the scorecard.

Source: Office for Budget Responsibility, Policy Measures Database (http://budgetresponsibility.org.uk/data/).

Authors

Thomas Pope

More from IFS

Understand this issue

Policy analysis

Academic research