Downloads

Key findings

- Whether – and if so how and when – the UK leaves the European Union will be perhaps the key determinant of growth over the next few years. Obviously, Brexit will define the terms on which the UK trades with its largest trading partner. But different Brexit outcomes may also be tied to different political outcomes in Westminster, and these come with very different sets of domestic policies that would significantly affect the economy.

- In our base scenario, the UK continues to delay Brexit. In this scenario, we assume a further fiscal loosening of between 1 and 2% of GDP. There would be a chance of small rate cuts. Growth remains below 1% in 2020 and, while it then picks up, it remains very poor, below 1½% in 2021 and 2022.

- Securing a Brexit deal would be better for the economy over the next two to three years than another delay. If this were to come with tax cuts and further spending increases together worth 1 to 1½% of GDP (over and above the loosening at the September 2019 Spending Round), then growth should pick up to (a still poor) 1½% a year in the short term. Some pent-up investment should occur, and consumer confidence would improve, as the risk of a no-deal Brexit recedes.

- A ‘no-deal’ Brexit would be economically considerably worse, even under a relatively benign scenario. We assume this would happen under a Conservative-led government, which would implement further fiscal loosening totalling 2% of GDP. Interest rates are cut to zero alongside £50 billion of quantitative easing. Private consumption and investment growth falls while net trade is also a drag on growth. Overall, the economy does not grow over the next two years, and grows by just 1.1% in 2022, leaving it 2½% smaller in that year than under our base case.

- Revoking Brexit would lead to the best economic outcome. We assume this would require a Labour-led government which, as well as revoking Brexit, would also implement significant tax and spending increases, an overall fiscal loosening and some tightening of labour market regulations. Interest rates would also rise more quickly. This might result in growth of 2% a year. Crucially, this scenario involves a Labour-led coalition rather than a majority Labour government.

- In the short term, implementation of the full 2017 Labour manifesto would offset at least some of the economic benefits of remaining in the EU. Widespread nationalisations, handing 10% of share capital of large companies to employees while redirecting some dividends to the Treasury, or other policies that might reduce private sector investment significantly, would challenge the UK’s traditional ‘business model’ and risk damaging growth by an amount it is not possible to quantify. Unlike Brexit, at least some of these policies will be reversible under future governments.

3.1 Introduction

The global outlook (Chapter 1) and recent trends in the UK economy (Chapter 2) both point to significant headwinds for the economy going forwards. However, arguably the most important determinant of the UK’s economic trajectory will be the continuing process of leaving the European Union. Brexit no longer ‘just’ determines future relations with the UK’s largest trading partner and the transition towards them. It has become intertwined with the political outlook and thus broader economic policies, including monetary policy.

As set out in Chapter 7, Prime Minister Boris Johnson’s government has failed to break the deadlock in negotiations with the EU over the arrangements at the Northern Irish border and the deadlock in parliament over the draft withdrawal agreement specifically and the wider Brexit strategy generally. The government has lost its majority, allowing parliament to pass the EU Withdrawal Act (No.2) in September. According to this Act, the government has to bring a withdrawal agreement through parliament or get a majority of MPs authorise a no-deal Brexit to leave the EU on 31 October. Both seem unlikely and, if they fail, the Act is designed to oblige the government to ask the European Council by 19 October to extend the Article 50 Treaty on European Union (TEU) deadline to 31 January 2020. The EU27 refusing such a request seems unlikely.

Once an extension is secured, it seems unlikely – but not impossible – that another three months will be enough to secure an orderly Brexit with this parliament. To break the deadlock in the UK, voters will probably have to give their verdict in a snap general election or a second EU referendum. In case of the former, polls are inconclusive; it is impossible to say with any confidence what the outcome of an election would be, but the outcome will certainly have implications for the UK’s Brexit policy. Broadly, a Conservative victory with the current leadership could lead to a no-deal Brexit. A defeat for the Conservatives – either by a majority of one opposition party or a coalition of several – could open up a path to reversing Brexit.

Between these two extreme but perhaps most likely scenarios – a no-deal exit or a Brexit reversal – there are others, including an orderly Brexit (‘deal’) or further delays. In this chapter, we describe how we would expect the economy and policy to evolve under each of these four scenarios, starting with our – at least temporary – baseline of repeated delays (Section 3.2) and going on to ‘deal’ (Section 3.3), ‘no-deal’ (Section 3.4) and ‘never Brexit’ (Section 3.5).

3.2 Base case: uncertainty continues

While it is certainly possible that the Brexit uncertainty will soon be resolved in one of the three directions described in the next three sections, for the time being the UK parliament does not seem to be able to agree on any of them. Even if a general election is called, more time may pass before the new parliament takes a final decision, if it is taken at all. Already, parliament has effectively legislated to request a third extension of the Article 50 TEU deadline. Assuming a deal is not struck and that the government does request an extension, then provided the EU agrees (which we deem likely given the consequences for the economy, expatriate citizens and the situation in Ireland), Brexit will not happen before 2020 at the earliest, and there could be further delays ahead. How would the economy evolve in case of another Brexit delay?

Table 3.1 Growth forecasts for continued Brexit uncertainty, 2019 to 2022

| 2019 | 2020 | 2021 | 2022 | Cumulative, 2019–22 |

GDP | 0.9 | 0.8 | 1.3 | 1.4 | 3.6 |

Private consumption | 1.7 | 1.2 | 1.4 | 1.4 | 4.1 |

Public consumption | 2.5 | 2.2 | 1.2 | 0.9 | 4.3 |

Business investment | –1.2 | 0.3 | 0.8 | 1.3 | 2.4 |

Residential investment | 0.6 | 2.9 | 2.8 | 2.8 | 8.8 |

Exports | –0.4 | 1.1 | 2.6 | 2.7 | 6.5 |

Imports | 2.6 | –1.0 | 2.6 | 2.5 | 4.1 |

Note: Real GDP growth rates.

Source: ONS and Citi Research.

After the last extension of Article 50 TEU in April this year, UK service sector confidence bounced briefly and modestly as no-deal was avoided, while manufacturing sentiment dropped because Brexit stockpiling ended and the global backdrop cooled. As a result of the unwinding of Brexit stockpiling, GDP recorded its first quarterly decline since 2012. We would expect a similar initial response if there is another Brexit delay in October, although the length and purpose of the extension could matter. The longer the extension, the bigger the scope for a sentiment rebound and for at least some pent-up investment projects to be executed. If the extension leads to a general election or a second referendum, sentiment implications would be different compared with an extension for further UK–EU negotiations. On balance, we would expect the economy to grow at a sub-potential rate of 0.5–1% annualised (Table 3.1).

Fiscal policy: easing delayed as well?

Further delays to the Brexit process do not necessarily have to mean that all other policy ceases as well. We would expect a budget with the prime minister’s promised fiscal loosening of 1–2% of GDP. However, it may not come to that if there is a snap election, as we think is likely. Fiscal giveaways would then depend on the outcome of the election, but given that both Labour and the Conservatives have pledged to loosen fiscal reins, we would still factor in a high probability of 1–2% of easing in 2020–21.

Monetary policy: rate cut possible, but depends on details

So far, the Bank of England has treated delays to Brexit as not materially different from a ‘smooth Brexit’. There is merit to this because no-deal is avoided either way. And while a deal would provide some more clarity about the final trading relationship between the UK and the EU than an extension, it would at the same time make the UK’s withdrawal from the EU close to irreversible. However, short ‘awkward’ extensions such as the one the UK secured in April have contributed to lower business confidence. Some Bank of England policymakers have argued that, while revolving Brexit delays are better than no-deal, they are worse than a deal. External Monetary Policy Committee member Gertjan Vlieghe, for example, said that his ‘preferred path of policy in that case is likely to lie somewhere between’ deal and no-deal.1 That opens the door for a rate cut even if no-deal is avoided as soon as a (short) Brexit delay is agreed, i.e. as early as November.

3.3 Economic forecasts: Brexit deal

If the government achieves a deal with the EU and brings it through parliament, it would deliver two notable benefits. First, it would secure a transition phase at least until the end of 2020. Second, the political declaration on future relations would provide some assurance of a future trade deal, even without all the details ironed out. In the somewhat unlikely case where the backstop stays in its current form,2 it would provide additional guarantees of smooth (goods) trade and effectively rule out no-deal after the end of the transition.

On the other hand, a Brexit deal would mean the chance of a Brexit reversal would be substantially reduced. Once out, the UK would have to apply to join the EU like any other third country. And while the UK would likely fulfil the criteria to join with relative ease, it would be very unlikely to receive the special concessions it currently has, such as opt-outs from the euro and judicial cooperation, and a rebate on membership fees. This likely means political support for the UK to rejoin the EU would be less extensive, all else being equal.

Fiscal policy: significant easing expected

If the government could command a functioning majority in parliament after passing a deal with the EU, we would expect the government to follow through with most of its fiscal announcements so far, including large-scale tax cuts (discussed in Chapter 8) and spending increases together worth 1–1.5% of national income over and above the £13.4 billion in spending increases already announced in the September 2019 Spending Round (and analysed in Chapter 6). The proposals discussed during the Conservative leadership election but not yet delivered include a cut to the higher rate of income tax (costing up to £9 billion a year), an increase in the threshold at which workers start to pay National Insurance contributions (between £3 billion and £17 billion depending on how it is implemented) and an increase in the threshold at which stamp duty is paid (around £4 billion). Combined, these would constitute a fiscal stimulus of around 1.4% of national income if not associated with commensurate spending cuts or tax rises. Spending increases might be even higher if public investment were further expanded to include additional plans – for example, for high-speed broadband.

Any of these giveaways would come on top of the giveaway reflected in the 2019 Spending Round, which the Bank of England already estimates would boost GDP by 0.4% over its three-year forecasting horizon. This stimulus would hit an economy that is already at or close to full employment. All else being equal, providing stimulus to an economy operating at capacity would put upwards pressure on inflation.

Monetary policy: wait, then hike interest rates

It is safe to say that, even if the UK were to leave the EU with a deal on Hallowe’en, the Bank of England’s Monetary Policy Committee (MPC) would not immediately hike Bank Rate at its November meeting. External MPC member Silvana Tenreyro likely spoke for a majority of MPC members when she said that with inflation falling below target, sterling likely appreciating upon a deal, weaker global growth and consequently a dovish shift at the Fed and the ECB, ‘recent developments likely lengthen the period until there is a sufficient pickup in inflationary pressures for me to vote to raise Bank Rate’.3 Her colleague Gertjan Vlieghe said he would see Bank Rate rising by 25 basis points (0.25 percentage points, ppt) per year on a smooth Brexit assumption. And even that may depend on the UK and the EU agreeing on a much longer transition phase than the 14 months (extendable by one or two years) remaining under the current Withdrawal Agreement.

Forecast impact: GDP above potential in the short term

A deal is not as good as staying in the EU over our forecasting horizon. Even with a deal, UK firms could expect worse access to their biggest export market and face major uncertainty about future trade relations with the eurozone and the rest of the world.

However, we would expect GDP growth to rise above the potential rate of 1.4% to 1.6% in 2021 (as shown in Table 3.2). As immediate uncertainty associated with the plausible risk of a highly disruptive Brexit recedes, in the short term some pent-up investment projects will likely move ahead.

Table 3.2 Growth forecasts in a Brexit deal scenario, 2019 to 2022

| 2019 | 2020 | 2021 | 2022 | Cumulative, 2019–22 |

GDP | 0.9 | 1.3 | 1.6 | 1.4 | 4.4 |

Private consumption | 1.7 | 1.2 | 1.4 | 1.4 | 4.1 |

Public consumption | 2.5 | 3.2 | 2.2 | 0.9 | 6.3 |

Business investment | –1.2 | 5.3 | 0.8 | 1.3 | 7.5 |

Residential investment | 0.6 | 3.9 | 2.8 | 2.8 | 9.8 |

Exports | –0.4 | 2.1 | 2.6 | 2.7 | 7.6 |

Imports | 2.6 | 1.0 | 2.6 | 2.5 | 6.2 |

Note: Real GDP growth rates.

Source: ONS and Citi Research.

Given uncertainty would not fall away completely, this relief would be relatively short-lived, pushing business investment back towards its subdued current growth rates in 2021 ahead of the next deadlines. But in 2020, business investment growth would at least temporarily revert to levels around 5–7% annually, which are typical at the current stage of the economic cycle in the UK. Given business investment accounts for 8–9% of GDP, it alone could add around 0.3–0.6ppt to GDP growth next year in the event of a deal.

In addition, with more certainty about future trade arrangements and additional public spending, potential growth could rise back up a little towards 1.7% per year. A 5–10% rebound in sterling would reduce imported inflation by 0.5–1ppt and boost households’ real purchasing power. House prices would rise, generating supportive wealth effects. A deal would also boost confidence on the EU side and thus boost export growth. In theory, above-trend growth rates close to 2% would be possible in the short term, in particular if the government goes ahead with tax cuts and increased public investment plans, alongside already announced increases in day-to-day spending.

However, despite a deal, the UK would not yet be out of the Brexit woods. Concluding a deal would leave the country swiftly heading for the next deadline or ‘cliff edge’, at the end of the transition period. The current political declaration on future relations guarantees smooth goods trade, if necessary via a temporary customs union. However, the degree of future regulatory cooperation is unclear and would have to be clarified during negotiations in the transition phase. For businesses where these regulations matter most, such as food, pharmaceuticals or indeed financial services, uncertainty post-Brexit deal would therefore persist and could heighten again towards the 31 December 2020 end of the transition period. We would therefore expect businesses to exercise caution in their hiring and investment plans (see Chapter 2).

3.4 Economic forecasts: a no-deal Brexit

If the UK leaves the EU on 31 October without a follow-on agreement, new customs and regulatory borders would be raised overnight and the EU and the UK would no longer automatically recognise licences to do cross-border business. This would likely happen in a context of heightened tensions between the EU27 and the UK over the implications for Northern Ireland as well as the UK’s financial obligations to the EU.

The imposition of new borders would likely create significant disruption and a big hit to economic growth. Even once the immediate disruption has been resolved, we expect lasting damage as significant parts of the economy (such as highly regulated tradable services or important parts of the manufacturing sector) would face a major challenge to their established business model. We would expect to shave 2–3% off our GDP forecast for the UK over two to three years in such a scenario. This means that, as Table 3.3 shows, growth over this period would be somewhere between very slow and non-existent, with our forecast for GDP to rise by only 0–0.5% per year, cumulatively speaking (the lowest three-year growth rate since 2012–13). In this section, we highlight the assumptions underlying our modelling and break down the impact by sector and expenditure category.

Table 3.3 Growth forecasts in a no-deal Brexit scenario, 2019 to 2022

| 2019 | 2020 | 2021 | 2022 | Cumulative, 2019–22 |

GDP | 0.9 | –0.4 | 0.3 | 1.1 | 1.0 |

Private consumption | 1.7 | 0.8 | 0.2 | 0.9 | 1.9 |

Public consumption | 2.5 | 3.2 | 2.2 | 0.9 | 6.3 |

Business investment | –1.2 | –3.7 | –3.2 | 1.3 | –5.6 |

Residential investment | 0.6 | –0.1 | –0.2 | 2.8 | 2.5 |

Exports | –0.4 | –3.9 | 0.6 | 2.7 | –0.7 |

Imports | 2.6 | –3.0 | 0.6 | 2.5 | 0.0 |

Note: Real GDP growth rates.

Source: ONS and Citi Research.

No-deal Brexit modelling assumptions

According to the government’s own contingency planning around a no-deal Brexit (code-named ‘Operation Yellowhammer’),4 a no-deal Brexit could cause significant short-term disruption, associated with delays at the borders and some immediate business, financial market and political uncertainty. This immediate shock presents major risks, but we assume that the worst impact would be overcome eventually as companies and consumers adjust.

We therefore focus here on the medium-term impact over two to three years. On this horizon, the impact of a no-deal Brexit depends on the choices the UK, the EU and other affected parties make. For our forecasts, we make a number of key – and debatable – assumptions:

- A stable government remains in place until 2022 aiming at low tariffs, low taxes and low regulation. No part of the UK leaves the union. This scenario likely requires a relatively stable Conservative government to be in place. We expect this to define other areas of the policy agenda.

- Following the tariff schedule it set out in March 2019, the UK imposes low tariffs on most imports, including those from outside the EU. Under this schedule, the government estimated in March that 87% of imported goods would have no tariff.5 Still, importers from the EU will have to fill in UK customs paperwork, which the Treasury estimated to add two or three times the cost of tariffs to traded goods.6 We assume they add about 3% to the cost of imports. There will be no new trade deals concluded with the EU or any other major trading partner over the next few years.

- The EU imposes its external tariffs on the UK: these average 2.8% on industrial goods and 8.7% on agricultural goods (WTO estimates). We assume that EU customs procedures would double the impact of the headline tariffs.

- UK financial and professional services providers would initially maintain access to the EU market via equivalence, but would lose most access after a year or two as EU authorities do not prolong transition rules. Crucially, the equivalence arrangements already in place minimise the immediate risk to financial stability.

- The Bank of England cuts the Bank Rate to near zero by the end of 2019 and leaves it there until 2022. It restarts asset purchases to the tune of £50 billion.

- The UK government cuts taxes and raises spending by around 2% of GDP in the first year. This would see spending well above levels announced in the 2019 Spending Round, and a fiscal loosening in excess of the additional plans Mr Johnson announced in the 2019 Conservative leadership race, but has yet to implement.

- The sterling exchange rate falls by 5–10% in trade-weighted terms.

- Net immigration to the UK falls to zero in the short term. We would expect that in such a scenario with an extra 5–10% decline in sterling, net emigration from the UK to the EU would grow sufficiently to offset the ongoing net immigration to the UK from non-EU countries of roughly 200,000 per year. This implies net immigration from the EU falling from a current 60,000 annual net inflow to a 150,000 net outflow as EU citizens leave, in addition to the ongoing net emigration of 50,000 UK citizens per year.

- We assume a 5% immediate drop in UK share prices and a 5% fall in house prices over two years. Note that the UK’s FTSE-100 index of large internationally exposed shares actually rose by 10% after the EU referendum in 2016 due to sterling’s 20% fall. But we would not expect such a large decline in sterling this time around, and the near-20% fall in the more domestically oriented FTSE-250 index in the immediate aftermath of the 2016 referendum arguably matters more for the financing conditions of the UK economy.

- Alongside the drop in sterling, we assume real goods shortages associated with near-term disruption are contained – preventing a widespread acceleration in inflation.

No-deal economic impacts: by UK economy sector

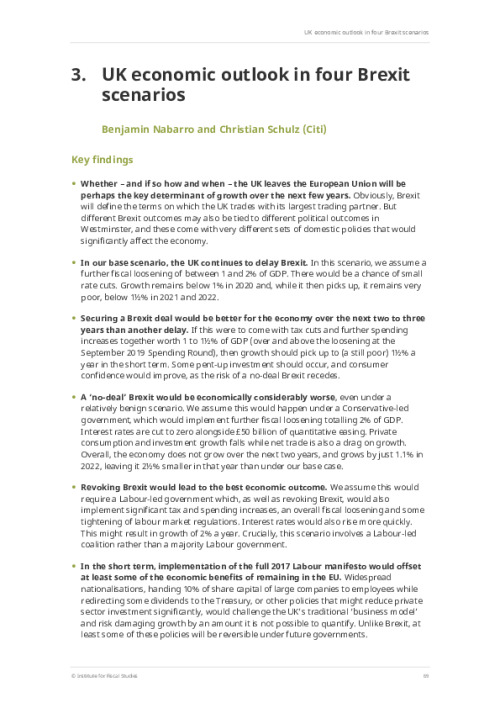

Based on the modelling assumptions outlined in the previous subsection, we estimate that a no-deal Brexit would reduce UK economic growth by 1.2 percentage points in 2020, 1.0ppt in 2021 and 0.3ppt in 2022. This hit to GDP compares with forecast average annual growth of 1.2% over the same period under our baseline scenario, which assumes ongoing uncertainty and further delays. As such, like the OECD, we suspect a no-deal exit would imply a near-term recession. A no-deal Brexit would leave the UK economy 2.6% or £57.7 billion (in 2019 prices) smaller in 2022 than it would have been under our baseline scenario.

Table 3.4 Breakdown of the impact of no-deal Brexit on the UK economy, by sector

Source: ONS and Citi Research.

In this and the next subsection, we highlight the elements underlying these forecasts, first looking at the different sectors of the UK economy and then turning to the different expenditure components of UK GDP.

Table 3.4 summarises how we would expect no-deal Brexit to affect the different sectors of the UK economy. For each sector, we summarise its weight in the economy (share of GDP / gross value added, GVA); our forecast for its growth in 2020, 2021 and 2022 if there is a no-deal Brexit at the end of October, as well as the cumulative growth rate over these three years; the contribution this cumulative impact makes to our overall forecast of the impact of no-deal on GDP; and, for reference, the average growth rate of the sector in the most recent three years.

Each sector of the economy will be affected differently by a no-deal Brexit, depending on both its exposure via trade (what and how much it trades with the EU) and its exposure to EU migration.

In 2016, UK trade with the EU (the sum of exports and imports) was roughly 30% of UK GDP, but this was highly concentrated in a few sectors of the economy. The EU trade intensity7 rises to more than 200% of GVA in the manufacturing sector and 85% in tourism-related industries. In many cases, exposure to both imports and exports matters in the sense that many UK sectors not only export to the EU, but also depend on EU imports either to produce for the domestic economy or to export elsewhere.

In addition, UK firms that employ large numbers of EU migrants are also disproportionately exposed. This is especially true in sectors where skills demand is quite specific, and may be difficult to replace via increased levels of immigration from elsewhere. Here manufacturing also stands out, as Figure 3.1 shows.

Figure 3.1. Share of EU workers in UK employment, by sector (2016)

Note: The EU14 refers to countries that were EU members prior to 2004, including, amongst others, Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Spain and Sweden. The EU8 refers to eight of the ten countries that joined the EU in its 2004 enlargement: the Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Slovakia and Slovenia. The EU2 comprises Bulgaria and Romania, which joined in 2007.

Source: ONS and Citi Research.

The five most trade-exposed sectors, which also include agriculture, mining and financial services in addition to manufacturing and tourism, only account for around 20% of UK output and employment. In the following, we highlight differentiated effects divided over four broad sector groups, in order of declining impact. A more detailed breakdown of the sector-by-sector impacts is displayed in Table 3.5.

Table 3.5. Exposure of different sectors of the UK economy to EU trade and immigration

Note: Thresholds are as follows: tariff/customs effect = high if goods trade intensity with the EU >30% of sector GVA, low if <6% (GVA = gross value added); regulation effect = high if subject to significant EU regulation at the moment, low if subject to minimal EU regulation / regulated by other international standards; immigration effect = high if share of EU workers ≥8% of workforce, low if <5%. We show figures from 2016 to strip out Brexit-induced changes that have already occurred. See also UK Economics & Strategy View - Brexit: Economic and Financial Implications of ‘No Deal’.

Source: ONS and Citi Research.

Highly regulated services

EU regulators have already adopted some transition provisions for a no-deal scenario.8 But the financial services sector and highly regulated parts of professional services, which together accounted for 14% of 2016 UK GVA, would still likely face high export hurdles while these arrangements are in place. Equally, once the transition provisions expire, which would be entirely at the EU’s discretion, service providers could be forced to move people and capital to the EU or to reorient their business model away from the EU. The companies would continue to function, but the services would no longer be provided from and accounted for in London.

Financial and regulated professional services are also exposed to significant risk from post-Brexit migration patterns. As Chapter 2 highlighted, both sectors employ significant numbers of EU workers, and thus their fortunes depend heavily on the new UK immigration system. Here, heightened sterling volatility and weaker perceived growth prospects may also have a direct near-term impact, dissuading would-be immigrants from coming to the UK.9

UK financial services may also be hit via the import side: if the UK unilaterally allows foreign-regulated financial services providers to operate in its markets, it would expose UK-based firms to additional competition. The CBI has noted the degree of asymmetry in the UK’s external relations following a deal, with the UK largely allowing imports even as the access of UK firms to the EU (and indeed other markets) remains impeded.10

The financial sector’s trade surplus with the EU in 2016 was nearly £25 billion, or 1.4% of GDP. If we add the entire professional services trade surplus with the EU, this becomes £46 billion or 2.6% of GDP. If that surplus were eliminated or even reversed (a possibility if, for example, banks move their European hubs to the continent and then reimport services to the UK), it would have a very large one-off impact on the UK’s economic growth. Most of this impact is likely to be independent of the UK’s choices on tariffs, regulations and immigration law. Indeed, deregulation in the form of deviation from international rules may even aggravate the loss of access to international (not just EU) markets. We would expect the sector’s GVA to be 4% smaller over two to three years than without a no-deal Brexit, with much of the impact in the later stages when transitory EU equivalence measures expire.

Manufacturing and other goods trading

Manufacturing, mining and agriculture, which together account for 12% of the UK economy, are highly EU-trade intensive. Under WTO rules, all three would face the EU’s external tariff framework (as well as new tariffs from the roughly 60 countries the EU has trade agreements with). EU tariffs average 2.8% for industrial goods, but rise to 10% for cars. For agricultural goods, the average tariff is 8.7% for countries trading on WTO rules. Customs bureaucracy might add another 2–3% of the value to the costs, not least because of the requirement to settle VAT at the point of customs. The new tariffs barriers could be mitigated by further exchange rate depreciation, but for highly time-critical production processes (for example, in the car industry), delays due to customs procedures would probably be more important than the actual level of tariffs.

On the import side, the impact of a ‘no-deal’ scenario would depend on the UK’s new import tariffs. In March, the government published a temporary customs scheme for a no-deal scenario where about 90% of imported goods would be tariff-free, compared with around 70% under the current EU external tariff. If the UK were unilaterally to keep zero tariffs on all imports from the EU, the rest of the world would also benefit under the most-favoured nation principle (which requires the UK to offer its ‘best’ tariff terms outside agreed trade deals to all other WTO members). This would expose UK producers to global rather than just European competition. This might also make it more difficult for the UK to strike favourable trade deals with other countries (since many of their incentives to negotiate better access to the UK market would be eroded), meaning UK firms are disadvantaged not just in the short term, but in the medium to long term too.

Outside import and export tariffs, regulation and thus Single Market rules matter greatly across most of the goods sector. Even though manufacturing products are often governed by global standards, EU regulations play a significant enough role in the sector that leaving the customs union could lead to new non-tariff barriers to trade both on exports and on imports. In addition, exports to the EU by some highly regulated sectors such as chemicals and pharmaceuticals (together 14% of manufacturing or 1.4% of the UK economy) are likely to be at risk.

A final risk factor for this sector is immigration. Manufacturing has the highest share of EU workers, suggesting it may be particularly hard-hit by tougher immigration laws. This is especially challenging for the sector given the skills composition of these workers, which may make them more difficult to replace at least over the next few years.

Taken together, we would expect manufacturing GVA to be 3% smaller after two to three years under a no-deal scenario than otherwise. That includes an assumed 2% rebound of production levels in year 3 due to factors such as deregulation, low tariffs, stimulus and sterling devaluation.

Low-regulation tradable services

Low-regulation tradable services such as tourism, parts of transportation, large parts of information and telecommunication, and real estate services should not be directly affected by external customs tariffs or diverging regulation and could largely continue trading with few obstacles. There are exceptions, but these tend to be small ones: within transport, for example, air transport might be affected by a no-deal Brexit, but it accounts for 10% of overall transport services and thus only 0.4% of the economy.

However, some of these sectors, in particular tourism and transport services, do depend on large numbers of workers from EU member states, and so might face labour shortages and higher personnel costs in the case of tight new immigration laws. All of these sectors also use EU-produced goods and services as an input into their services and could thus face further increases in costs (depending on the UK’s new import customs scheme and exchange rate moves).

If we assume that half of the business services sector falls into a similar category of low-regulation tradable services, this part of the economy currently accounts for 34% of UK GVA. We would expect this sector to suffer somewhat from the general demand weakness at the beginning, but then start benefiting from some of the fiscal and monetary policy counter-measures in 2022–23, so that three years out it ends up 1% smaller than under our base case of continued Brexit delay.

Non-tradables

The remaining two-fifths of the economy is sectors that do not trade their output directly with the EU. However, some of these do use EU inputs, especially goods and labour. Construction and retail & wholesale trade in particular, which together account for 17% of the economy, have low direct trade intensities but high shares of EU workers and also depend on EU goods input. Even utilities and public services such as education and health have significant shares of EU workers (and together account for 20% of output).

The effect of a ‘no-deal’ scenario on value added in these sectors may not be as sharp as in the tradable sectors, but it could be significant nonetheless. We expect a 2% hit over two to three years and little positive impact from some of the pro-growth measures the government may take.

No-deal economic impacts: by component of GDP

We can also analyse the impact of a no-deal Brexit based on the GDP ‘expenditure’ components. Table 3.6 summarises the effect on each of these components of spending. We would expect the initially most dramatic impact of no-deal Brexit to come through a further plunge in business investment and exports, but private consumption – which has a heavy weight in the UK economy (see Chapter 2) – would also be vulnerable. The reduction in the household saving rate to all-time lows since the referendum suggests this could be vulnerable in the event of a further shock. These downward impacts could be offset partly by a decline in imports as well as a fiscal expansion, which would drive up public consumption and investment.

Table 3.6 Breakdown of the impact of no-deal Brexit on the UK economy, by GDP expenditure component

Note: Real GDP growth rates.

Source: ONS and Citi Research.

Investment

We expect business and private sector dwellings investment to plummet initially after a no-deal Brexit; in 2020, we expect business investment to come in 4ppt lower than it otherwise would have, while residential investment would be 3ppt lower. The export of goods and services to the UK’s largest trading partners would become more difficult, and in some cases impossible, and the import of labour and capital inputs more costly due to new immigration rules and falling sterling.

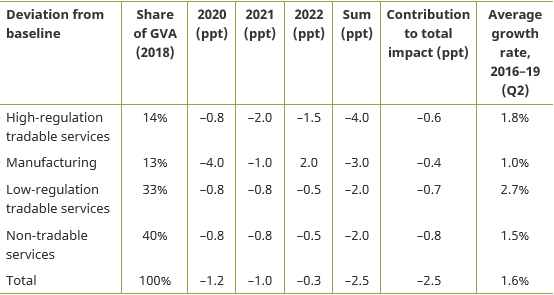

Investment disproportionately relies on sectors that are highly exposed to Brexit (see Figure 3.2). Manufacturing and other production industries accounted for 29% of investment alone in 2018. Investment in the real estate sector, which accounts for 18% of business investment, and in private sector dwellings would also likely fall given a likely decline in demand for commercial property and poorer prospects for national property valuations, respectively.

In principle, import substitution may require some offsetting investment to build up production capacity in the UK. However, much of the substitution is likely to occur between imports from the EU and the rest of the world (rather than boosting demand for domestic production), since we assume that the UK will lower tariffs for all importers in accordance with WTO rules. This means that much of the investment into new supply chains will occur outside the UK and the EU.

In addition, in those cases where alternative international suppliers cannot be found elsewhere, we suspect that onshoring, and subsequent boosts to domestic investment, will be appropriate in only relatively few cases. UK manufacturing, in particular, has often been based on a high degree of specialisation within equally specialised value chains. The loss of access to such transnational networks is then unlikely to generate any large-scale transitional investment in the UK; instead, firms will likely increase the scale of write-offs as existing UK production becomes unviable without easy access to EU supply chains.

On our current baseline (where no-deal is avoided but uncertainty continues due to further delays), we expect business investment to shrink by 1.2% this year and grow only modestly by 0.3%, 0.8% and 1.3% from 2020 to 2022 (2.4% cumulative). In a no-deal scenario, we would expect an additional cumulative fall of 8ppt by 2022. For investment in private sector dwellings in our baseline, we expect 0.6% growth this year and close to 3% thereafter. In a no-deal scenario, we would expect stagnation or a slight decline for another two years. Overall, we would expect a drag of 0.7ppt on annual GDP growth over the three forecast years 2020 to 2022 from the slowdown in private sector investment, or one-third of the overall negative impact of no-deal Brexit.

Figure 3.2. Share of different sectors in total investment, 2018

Source: ONS and Citi Research.

Private consumption

Private consumption would face a range of headwinds in the event of a no-deal Brexit. Prices would rise: a 10% depreciation of trade-weighted sterling would boost headline inflation by 1ppt in the following two years and thus diminish real wage growth. Import substitution would only partly mitigate this, as domestic production capacities are limited and probably expensive due to underinvestment. Instead, imports may be sourced from non-EU countries.

New competition from non-EU countries due to lower tariffs and import substitution would probably trigger a significant fall in employment. We would expect a 1–2ppt increase in the unemployment rate even if labour supply growth slows or stops due to reduced migration.

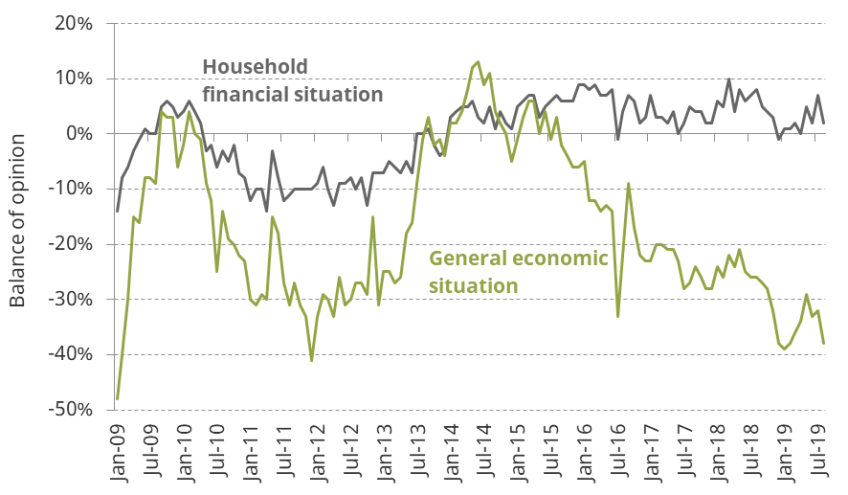

Over the last five years, rising employment has played an essential role in propping up private consumption growth. In particular, as Figure 3.3 shows, low unemployment has driven a wedge between household-level financial expectations (which remain, on balance, slightly optimistic) and perceptions of macroeconomic performance (where considerable doubt has settled in). As households do not see the macroeconomic uncertainty affecting their personal capacity to spend, household consumption has been resilient, even in the face of growing Brexit uncertainty. In this context, a sudden increase in unemployment could have a more extensive impact on consumption, further curtailing economic growth.

Figure 3.3. Consumer perceptions of household financial situation and general economic situation

Note: Surveyed ‘balance of opinion’ is obtained by taking the sum of the number of responses multiplied by the appropriate weight (–1 being very weak, –0.5 being weak, 0.5 and 1 being strong and very strong respectively). This is then divided by a weighted base of 2,000.

Source: GfK and Citi Research.

The negative wealth effect from another fall in house prices would also weigh on spending. Unlike in 2016, households will be less able to smooth through a period of adverse conditions as the saving rate is already extremely low in historical and international comparison.

However, there are some supportive factors for consumption. A rate cut by the Bank of England would reduce debt service for households with variable-rate mortgages (although the average time for interest rate changes to affect mortgage rates is much greater than it used to be).11 Government tax cuts would boost incomes, and new public spending could boost employment and wages in some sectors.

On balance, we would expect real private consumption to end up 2% smaller than without a no-deal Brexit, which implies household spending volumes flatlining for two years. This would reflect an increase in unemployment, pressure on real incomes and an increase in the household saving rate.

Public spending and investment

In a no-deal scenario, we suspect fiscal easing efforts would be stepped up, boosting public consumption and investment. In his 2019 Spending Round speech, Chancellor Sajid Javid commented that he had tasked the Treasury with developing a ‘comprehensive economic response to support the economy if needed’.12 These comments were made with close reference to a potential no-deal exit. Hence we would expect a further stimulus upgrade in a no-deal scenario. Just as in 2008–09, we expect public investment could prove the focus. That could leave public consumption 2% higher and public investment 6% higher than without no-deal. A more limited fiscal giveaway is already baked into our forecasts, given that almost any UK government seems likely to spend more in any Brexit scenario. But a no-deal case would likely see even more support forthcoming.

Exports and imports

Exports are likely to take a significant hit from the rise of new and significant tariff and non-tariff trade barriers between the UK and the EU. The EU accounted for 44% of total UK exports of goods and services in 2017.

While the hit to goods exports is likely to be immediate and, in the very short term, aggravated by transport disruptions and the running down of stockpiles of UK goods on the continent, services may initially benefit from transition periods. For example, the EU has announced that it will recognise equivalence for central counterparties (CCPs) until March 2020 and for central securities depositories (CSDs) until 30 March 2021. It will also facilitate the cross-border clearing of over-the-counter derivatives for 12 months after Brexit. However, in a no-deal scenario, UK-based firms might ramp up their EU-based operations swiftly as these temporary exemptions could end soon afterwards. Hence, in addition to the immediate and persistent drop in goods exports, we would expect a second wave of export declines due to some service provision relocating from the UK to the EU in 2020 and 2021. If the UK’s equivalence recognition ends up being more generous than the EU’s (which is realistic under the assumption of a low-regulation UK government), some services may even be moved abroad and reimported. This would cause a double hit to the UK’s national accounts, adding growth in imports to the fall in exports.

The drop in exports, in combination with lower domestic investment and private consumption and another sharp drop in the sterling exchange rate, should also trigger a decline in import volumes. However, we would expect that decline to be somewhat smaller than the export decline as the UK cuts tariffs and quotas on non-EU imports (meaning the trade environment becomes relatively more favourable for imports, compared with exports). On balance, we expect exports to grow 7ppt less over two to three years and imports 4ppt less, which together creates a drag of 0.7ppt on GDP.

Alternative paths under no-deal

We cannot rule out that the short-term consequences of a no-deal scenario are more disruptive than we factor in. In particular, if sterling depreciates much more than expected, a balance-of-payments crisis, where capital outflows reach such critical levels that the Bank of England has to raise interest rates at the expense of deepening the domestic financial crisis, is not impossible. The chances of this are increased by the UK’s balance-of-payments deficit.

In such crises, the UK would be particularly vulnerable to debt denominated in foreign currencies. The UK’s gross external debt is very large at 307% of GDP in 2018, more than double Germany’s external debt as a share of GDP in the same year (145% of GDP) and five times Argentina’s level (50% of GDP). However, these figures probably exaggerate the UK’s exposure to exchange rate volatility: at least on aggregate, the UK’s foreign liabilities largely fund foreign assets. The UK’s net negative international investment position, meaning more foreign capital is invested in the UK than vice versa, is only about 9% of GDP, suggesting a smaller risk.

For devaluation to drive the Bank of England to tighten rates, real goods shortages and accelerating inflation would likely be necessary. In the short run, we think any food and medicine shortages suggested in the Operation Yellowhammer documents13 may not have a major macroeconomic impact (although fuel shortages probably would). However, these could influence politics. This may not just lead to a change in government, but could also risk the cohesion of the UK, given a strong independence movement in Scotland and the special situation in Northern Ireland.

However, there is still a risk that a large depreciation could still make it more difficult attracting foreign capital – particularly in the midst of ongoing uncertainty. Since the referendum, the UK’s financial account has shifted decisively to being funded via portfolio flows (that is, financial assets), rather than via foreign direct investment (FDI) in UK companies or capital. While this means businesses may be less immediately affected by a reduction in attractiveness, there is evidence that a reduction in portfolio inflows can drive less accommodative bank lending.14 This can also occur relatively suddenly.

The fact that the 20% depreciation around the referendum did not trigger a crisis is reassuring. In addition, the Bank of England has established swap lines with the US Federal Reserve, the European Central Bank, the Bank of Japan, the Bank of Canada and the Swiss National Bank, which should ensure access to foreign currency even in the case of major volatility and forestall any major crisis. However, a further reduction in the perceived attractiveness of the UK could drive an increase in commercial rates at the margin, tightening financial conditions.

In the medium and long term, the UK’s economic trajectory post-Brexit would significantly depend on the structural choices future governments make with regards to tariffs, regulation and immigration. Over time, a low-tax, low-regulation and low-tariff approach could allow a steeper growth recovery (albeit still only a partial one), which we do not capture in our modelling due to the relatively short time horizon. One plausible scenario would be that, while the EU enters a trade war with the US, the UK could strike a free trade deal with Washington. In that case, European firms might invest in the UK in order to enter the US tariff zone.

By contrast, as discussed in last year’s Green Budget,15 an alternative, more protectionist approach to mitigate the impact of leaving the EU would soften the immediate impact but potentially make it worse over time. The result would be a shallower but longer no-deal Brexit impact.

3.5 Economic forecasts: revoking Brexit

A big shift in the distribution of likely outcomes of the Brexit process since the formation of Mr Johnson’s government in July is that the path towards revoking Brexit has become much clearer. Some of the moves of the current UK government to make no-deal Brexit a more plausible outcome, such as attempting to sideline parliament with a (since ruled illegal) five-week prorogation, have sparked new cooperation between several opposition parties and pro-EU former Conservative MPs. Parliament passed legislation to prevent no-deal Brexit and looks prepared to go further if necessary. In addition, the opposition has become more pro-EU. The Labour Party has adopted holding a second EU referendum between a ‘Labour Brexit’ and remaining in the EU as its policy. The Liberal Democrats even want to revoke Article 50 without a second referendum should they win a majority in a general election.

Polls advise some scepticism on the chances of Remain-leaning parties winning an election, jointly or alone. The Labour party is struggling at around 25% in the polls, but based on the first-past-the-post voting system remains likely to win the most seats of the current opposition parties. However, cooperation between pro-EU parties such as the Liberal Democrats, the Greens and the pro-EU regional parties has led to successful ‘Remain alliances’ in recent by-elections. Polls are still close enough for the Conservatives (and their potential allies DUP and Brexit Party) to lose, and thus for an alternative majority of Labour together with openly Remain-supporting parties. Importantly, since the start of the year, the growing support for the Liberal Democrats and the SNP means that, if a Remain-supporting group of parties are able to secure a parliamentary majority, this is likely to involve de facto parliamentary vetoes for both of these parties. For our ‘revoking Brexit’ scenario, our starting point is that, if such a majority materialised, it would commit to an eventual second referendum rather than revoking Article 50 outright.

Below, we consider three elements of such a pro-Remain coalition:

- Brexit policy: We would expect an attempt to negotiate a softer version of Brexit over a few months followed by a second referendum as early as mid 2020, with a choice between that negotiated Brexit deal and remaining in the EU. While it is not certain Remain would win, narrowing the options on the leave side to one particular compromise deal should make that outcome more likely. In any case, a Conservative defeat in a snap election would immediately – and greatly – diminish the likelihood of a no-deal Brexit. This could have a positive effect on investment in the short term,16 with greater subsequent benefits if Remain did indeed prevail.

- Economic policies: The economic benefit of having a clear path to reversing the 2016 EU referendum would arguably be offset in part by some elements of the broader economic agenda pursued by such a Labour-led government. Labour’s agenda poses risks to long-term growth by reducing the flexibility of the economy and increasing the role of the state. In the near term, some of Labour’s policies could make the UK less attractive for foreign direct investment (or even trigger domestic funds moving abroad). That is particularly sensitive for an economy with a large current account deficit. However, to the extent that Labour is constrained by its dependence on other parties, we assume that the radicalism of its domestic agenda – and so the economic risks some elements of it might pose – would be reduced.

- Fiscal policies: A fiscal expansion is likely, but would not obviously exceed levels implied by Conservative spending plans (discussed in Section 3.2). However, this would still provide some near-term support to growth.

Our judgement is that, over a medium-term period of two to three years, the positive effects of staying in the EU (especially for investment) would offset the negative effects of domestic economic policies, and the economy would outperform compared with the deal, no-deal and base-case scenarios.

As in the no-deal scenario, changes to the assumptions can have substantial implications for the economic trajectory. For example, an outright Labour majority might make Brexit reversal less likely (given Labour leader Jeremy Corbyn is historically a Eurosceptic himself) and high-tax, high-regulation policies that are detrimental to growth more likely. Conversely, a Remain alliance’s dependence on the SNP could lead to a second Scottish independence referendum bringing its own uncertainties – and thus lower investment – with it. We assume in our forecasts that Scotland remains a part of the UK.

Brexit stance of a Labour-led coalition

All parties that could conceivably be part of a Labour-led coalition would likely be willing to support a second EU referendum. At least for Labour and the SNP, this is official policy; for the Liberal Democrats, this was official policy until very recently,17 and would likely command their support.

While the SNP and the Liberal Democrats would probably not try to negotiate a Brexit deal, the Labour party is officially committed to holding negotiations with the EU before a second referendum. Labour’s plan foresees negotiating a permanent customs union with the EU and deep regulatory alignment, along with cooperation on issues such as climate change, refugee crises and counter-terrorism. Such a model should be largely in line with the current Withdrawal Agreement, but would require significant adaptation of the political declaration on future trade relations. Such a deal would then be put to a referendum, with Remain as the second option.

It is dubious whether the relationship Labour plans to negotiate with the EU is economically and politically viable. Like Turkey, the UK would lose any say about most of its external trade policy. It would be obliged to open its markets to goods from economies the EU strikes free trade deals with, but these economies would not be obliged to return that favour (the UK would be able to negotiate trade deals covering services independently, but would not be able to offer up access to the UK goods market in return). The UK would continue to make financial contributions to the EU, though likely at a lower level than under full membership. In addition, the customs union would not, in itself, solve the issue at the Irish border; the UK would still be forced to match EU regulations on industrial and agri-food goods, which may include competition and state-aid rules, to prevent a hard border. The only significant policy advantages of a customs union would be the ability to control immigration by ending free movement; the ability to negotiate independent trade deals covering services and intellectual property; leaving the jurisdiction of the European Court of Justice (on most matters); and exit from the common agricultural and fisheries policies. These would come at the cost of losing voting rights as well as membership of the EU’s single market – for example, for financial services.

There are other issues with such a plan too. Beginning negotiations with the subsequent intention of calling a second referendum could undermine discussions in the first place: if EU negotiators wanted UK voters to vote to stay, they could offer the worst-possible deal in order to make EU membership the obvious better alternative. However, that risk seems limited given that Labour would not ask for much more than the EU already offered to Theresa May and would presumably enter negotiations in a much more amicable manner. Still, it remains difficult to envisage a deal coming out of these negotiations which the majority of Labour MPs would campaign for.

Were this plan to become government policy (backed by a robust majority in parliament), it would have several immediate effects. The new policy would rule out a highly disruptive no-deal exit in the short term. A victory for the Brexit deal in the referendum would lead to an exit, but on the basis of a softer ultimate deal than either of the options (no-deal or the current Withdrawal Agreement) now on the table. If Remain won, the UK’s position in the EU would be restored.

As such, in the first year of such a government, Brexit-related uncertainty would not completely disappear. However, we expect ruling out a damaging no-deal exit would likely provide some near-term support to investment as businesses took advantage of the new ‘no no-deal’ policy to execute some projects that had been held back.18 During the referendum campaign, uncertainty would probably remain elevated, given that a Remain outcome could not be guaranteed. The prospect of near-term resolution would mean investment remained somewhat depressed until the actual result. In the event of a Remain result, we would expect pent-up projects and plans for an even closer relationship would provide a further boost to investment.

We acknowledge that a second EU referendum would not permanently settle the issue of the UK’s EU membership. Anti-EU campaigners might blame even a landslide victory for Remain on the framing of the question and the failure to negotiate an attractive deal. The announcement of the result of the second referendum could easily be the start of the campaign for the third referendum. The genie which escaped the bottle in 2016 cannot be put back in quite so easily, so neither economic circumstances nor risk asset prices would revert to the path that was expected prior to 2015. The UK’s position in the EU, while restored in the short term, would not be guaranteed.

However, for our scenario with a three-year horizon, we would expect a boost to business investment in the short term, with a further increase if Remain were to win in the subsequent referendum. Further improvement beyond this would depend on the nature of the political fallout. We expect some residual uncertainty would likely persist.

Economic and fiscal agenda of a Labour-led coalition

Labour’s economic policies have caused concern among businesses and investors since Jeremy Corbyn became party leader in 2015. In the 2017 general election, Labour’s manifesto plans included roughly £50 billion in additional day-to-day spending, offset by plans for a similar, if disputed, increase in taxation. In addition, the plans foresaw £250 billion of debt-funded investment spending over 10 years (on average, 1% of GDP each year).

Overall, this would have increased spending by a total of around £75 billion a year (3.4% of 2019 GDP), with tax-raising measures put in place that were intended to raise roughly £50 billion a year. While these numbers are large, as set out in Chapter 6 the Conservative government has already increased its plans for spending in 2020–21 dramatically since 2017 (especially on the NHS) and the prime minister has also discussed substantial tax cuts (see Chapter 8).

Labour’s specific tax-raising measures were a set of income tax increases focused on those with an income over £80,000 a year (which is a risky revenue-raiser, as these taxpayers already account for a large share of tax revenues and those on the highest incomes can be quite responsive to increased tax rates) and measures intended to increase taxes on companies, not least an increase in the corporation tax rate from 19% back to the 2011 rate of 26% (which would raise substantial sums, but over the longer term would also be likely to depress investment in the UK). Overall, the Labour party costed these measures as raising £48.6 billion in cash terms (£52.5 billion less a £3.9 billion allowance for additional behaviour change, further reducing the yield).

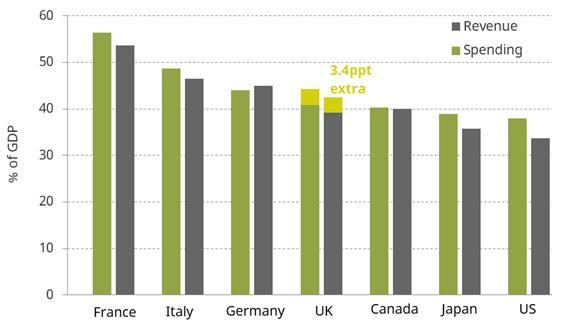

Figure 3.4. Government spending and revenue as a share of GDP among G7 economies

Source: OECD and Citi Research.

It is likely that many of the revenue assumptions were too optimistic – analysis by IFS researchers at the time argued that even a £41 billion estimate would, more likely than not, prove too optimistic.19 Failing to meet this revenue target would have meant a Labour government faced a choice between higher borrowing, more tax-raising measures or reneging on some of its spending commitment. Of course, if a government with this agenda also ended up stimulating growth by reversing the 2016 referendum result, it is also conceivable that fiscal space would be larger than Labour assumed in 2017.

While these are substantial tax and spending plans, and come with some risk, even if fully implemented the size of government in the UK would still be at the lower end of the range, at least in Europe. As Figure 3.4 shows, tax revenue in the UK was 39.1% of GDP in 2017. With Labour’s 3.4ppt increase, that would become 42.5%, still below Germany at 45.0%, Italy at 46.5% and France at 53.6%.

Instead, it is other aspects of Labour’s 2017 manifesto and additional announcements which would create structural changes to the economy and so might have the bigger economic impact. These include:

- reforms to the labour market, such as rolling out sectoral collective bargaining; introducing a minimum wage of £10 per hour (already matched by a Conservative pledge to raise the minimum wage to £10.50);20 banning zero-hours contracts; and introducing four new bank holidays;

- forcing large firms (employing more than 250 UK workers) to put 10% of all company equity into a fund owned by a firm’s workers, which would distribute dividends up to £500 per employee each year to workers and send the rest to the Treasury;

- nationalising water and energy utilities, postal services and train services, with compensation potentially below market prices;

- introducing right-to-buy for tenants in privately rented properties.

Some of these reforms would constitute a significant change to the UK’s ‘business model’ over the past four decades when it came to attracting foreign capital, which featured low tax rates, flexible labour laws and untouchable property rights. Given the UK depends on foreign capital inflows to fund its current account deficit (3.9% of GDP in 2018), challenges to the business model could make the UK less attractive for foreign investors, or trigger outflows of domestic capital. That would probably dampen sterling’s appreciation due to receding Brexit fears and may even lead to a knee-jerk depreciation of sterling upon an election result making a Labour government possible. Fully implemented, the impact of these changes would likely do significant damage to the outlook for UK growth.

Labour’s likely dependence on the Liberal Democrats and the SNP would probably limit the government’s ability to implement some or all of these plans. The Liberal Democrats’ 2017 plans were fiscally more conservative. For example, they wanted to eliminate the day-to-day budget deficit two years earlier than Labour and sought a 1 percentage point increase in income tax across the board rather than seeking to raise revenue from those on high incomes only. The Liberal Democrats wanted the corporate tax rate at 20% (not 26% like Labour), to review business rates and not to nationalise infrastructure. The Liberal Democrats could thus be a check on Labour’s plans for new spending and structural reform, especially if they contribute a large number of seats to the new majority.

How might economic growth change under a Labour-led coalition?

In order to spell out the growth implications of our Brexit revocation scenario, we make the following assumptions:

- Parliament calls a second referendum on the new deal versus staying in the EU in mid 2020. We assume Remain wins such a referendum.

- The rises in day-to-day spending by 2.4% of GDP (1.8ppt over the level announced at the September 2019 Spending Round) are offset by revenue increases, so that they are largely neutral for the economy.

- There would still be net fiscal easing from the £25 billion (1.1% of GDP) per year increase in public investment plus 0.6% of GDP for unfunded measures announced since 2017 to ‘end austerity’, so a total 1.7% of GDP.

- Labour market flexibility is reduced by limiting zero-hour contracts, reducing working hours (including the abolition of the voluntary opt-out of the working time directive) and raising the minimum wage.

- The government launches consultations into nationalising parts of the utilities sector, post and railways as well as a scheme to strengthen employee participation in larger companies, including handing over 10% of the shares of large companies to employees. But these measures are not implemented in the near term.

Starting with the profile of Brexit uncertainty, a Remain alliance victory would rule out a no-deal Brexit in the short term. We expect this would trigger a relief boost to business confidence in the UK and in the EU immediately, partly offset by uncertainty about the new government’s economic policies. Brexit uncertainty would further recede after a Remain victory in a mid-2020 second EU referendum. However, some uncertainty about the UK’s membership of the EU would remain, albeit at a longer time horizon.

During this period, households, businesses and investors would have to digest Labour’s economic policies. We would expect higher corporate and high-income taxes and tighter labour laws to cap the rebound in (private) investment. The increase in corporation tax, in particular, is notable here. The large increase in public investment may help offset some of the negative aggregate effects associated with higher corporation tax, complementing the improvement associated with the reduction in Brexit-related uncertainty. However, this will depend on exactly how this is directed. After a vote to remain in the EU in the mid-2020 referendum, there should be further upside for business investment in particular.

At the same time, a 1.8% of GDP fiscal loosening (including significant redistribution from wealthier households to consumption-intensive poorer households via the tax and welfare system), minimum wage hikes and the relief to have avoided no-deal Brexit could boost consumption. Since private consumption accounts for two-thirds of GDP, we would expect a significant acceleration of GDP growth to 2% or more annualised until the middle of next year (Table 3.7). While the potential downside to residential property prices associated with policies such as the right for private tenants to buy their rental property may weigh on this, such policies may also boost disposable incomes for non-homeowners. We make no assumption about the effects of such changes.

On balance, we expect that the positive impact of this scenario on growth and financial markets would be smaller than the negative reaction in a no-deal scenario. We would expect UK GDP to grow 1.5–2% more over the next two to three years than in the baseline scenario of unresolved Brexit tensions. In contrast to the no-deal scenario, the initial positive impact in 2020 would be quite small (+0.3ppt to 1.1% GDP growth), because it would take time until the new referendum is held. In 2021, the relief would be greatest after a pro-EU referendum result, with growth rising above 2% for the first time since the 2016 EU referendum. In 2022, growth would fade again towards the (higher) potential rate of 1.5–2% per year.

Table 3.7. Growth forecasts in a ‘never Brexit’ scenario, 2019 to 2022

No Brexit | 2019 | 2020 | 2021 | 2022 | Cumulative, 2019–22 |

GDP | 0.9 | 1.1 | 2.2 | 1.9 | 5.3 |

Private consumption | 1.7 | 1.5 | 1.9 | 1.7 | 5.2 |

Public consumption | 2.5 | 3.2 | 2.2 | 0.9 | 6.3 |

Business investment | –1.2 | 1.3 | 5.8 | 6.3 | 13.9 |

Residential investment | 0.6 | 3.9 | 5.8 | 5.8 | 16.3 |

Exports | –0.4 | 2.1 | 3.6 | 3.7 | 9.7 |

Imports | 2.6 | 1.0 | 4.6 | 4.5 | 10.3 |

Note: Real GDP growth rates.

Source: ONS and Citi Research.

With the economy at full employment already, and receiving the extra boost of less uncertainty and fiscal easing, underlying inflationary pressures should build rapidly and push the Bank of England to hike Bank Rate. Depending on external developments (sterling as well as foreign monetary policy), the MPC may wait until May 2020, but then we would expect two rate hikes per year, which would dampen growth and any rebound in the housing market, for example.

3.6 Conclusion

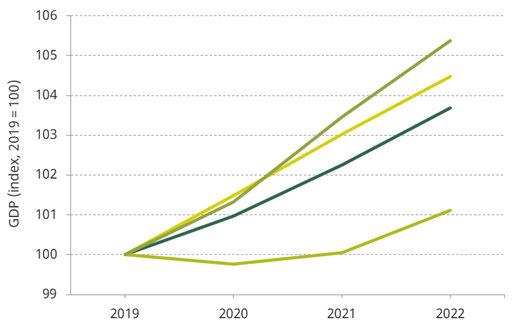

We have described here four potential paths for the UK economy. While there are many others, in particular when combining potential election outcomes with Brexit paths, these four scenarios provide a useful indicative picture of where the UK economy may go from here. From a growth perspective, we would expect the Brexit reversal (‘never Brexit’) to be the best outcome in the medium term, with the economy 5.3% larger in 2022 than in 2019 (see Figure 3.5 on the next page). Clearly, however, as we noted above, if this were associated with full implementation of Labour’s 2017 manifesto plans – perhaps under a Labour majority (rather than the assumed watered-down Labour minority) – the headwinds to growth would be substantial and the overall impact on growth remains unclear. A deal would still be better than our baseline, with GDP rising by 0.8% more than the 3.6% in total we expect in our baseline. Even in a no-deal scenario, we expect the economy to grow, but by more than 4% less than in the best scenario of ‘never Brexit’: in this scenario, the economy would only be 1.0% larger in 2022 than it is in 2019.

Figure 3.5. Real GDP growth in the UK under different Brexit scenarios (2019 = 100)

Source: ONS and Citi Research.

Endnotes

Authors

More from IFS

Understand this issue

Policy analysis

Academic research