Downloads

3-Outlook-for-the-public-finances.pdf

PDF | 650.92 KB

Since the March Budget, encouraging early indicators on the recovery in consumer spending, the labour market and government revenues have led to an upwards revision in most economic forecasts. In the short term, our analysis suggests that borrowing this financial year could be over £50 billion lower than official forecasts suggested at the time of the March Budget – a large improvement in such a small space of time. Large changes will of course be more common in the current climate: as highlighted by the fact that the latest estimate of borrowing in 2020–21 currently stands at £30 billion below what was forecast in Budget produced just weeks before the end of that financial year.

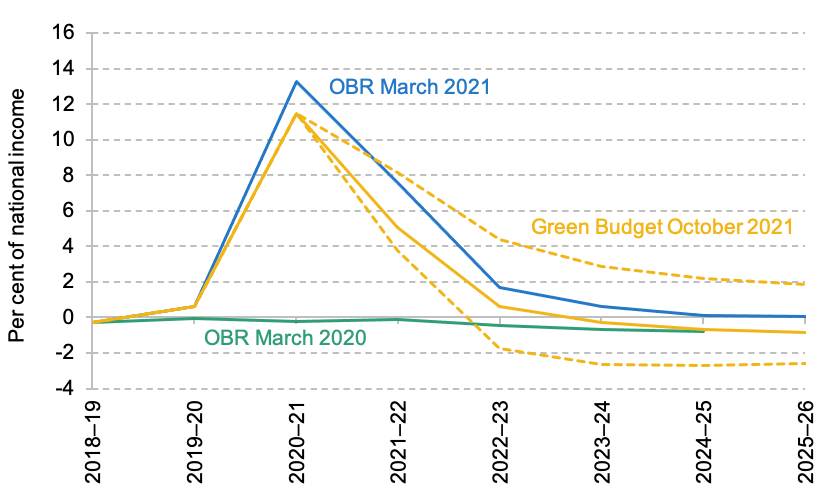

Some of this £50 billion ‘windfall’ looks likely to prove temporary: in the latter part of the forecast, the improvement in economic performance vis-à-vis the March forecast fades. Our forecast (which assumes that the government goes ahead with large planned tax rises and does not top up spending plans) is that borrowing in 2024–25 will be £21 billion below the March 2021 Budget – and £5 billion lower than forecast pre-pandemic as the tax rises announced in that Budget more than offset the enduring economic impact of the pandemic on revenues. This would – as shown in the Figure below – be enough to deliver a modest, but growing current budget surplus from 2023–24, that is to say the government may be on course to return to a sitatuation where revenues are sufficient to cover day-to-day (i.e. non-investment) spending. But uncertainty around this central forecast remains even more substantial than is typically the case, as illustrated by the enormous range of borrowing forecasts under Citi’s optimistic and pessimistic scenarios.

Figure 1. Forecasts for the current budget deficit (% of national income)

Note: Dashed lines indicate forecasts under Citi’s optimistic and pessimistic scenarios.

Source: OBR’s Economic and Fiscal Outlook, March 2020 and March 2021; Citi forecasts; authors’ calculations.

Key findings

- The economic and fiscal outlook for this year has improved hugely since the March Budget: our central projection is for borrowing in 2021–22 to be £180 billion, over £50 billion below the March Budget forecast. This striking reduction is driven by a boost to revenues from higher growth, alongside our assumption that departments will underspend by even more than the Office for Budget Responsibility (OBR) expects. Nevertheless, at 7.7% of national income, borrowing would remain extraordinarily high: since the Second World War, that level has only been reached during the financial crisis – and last year.

- Stronger economic performance is expected to be only partly persistent: by the middle of the decade, Citi’s forecast is for the economy to have returned closer to the path forecast in the March Budget, with the boost to real-terms growth fading out entirely. But assuming that large tax rises announced in March and September go ahead and current spending plans are not topped up, they appear sufficient for borrowing to continue to run at least £20 billion a year below the March 2021 Budget forecast, and for the current budget to be in surplus from 2023–24. Under our central scenario, borrowing in 2024–25 is £5 billion lower than forecast pre-pandemic as the tax rises announced in the March 2021 Budget more than offset the enduring economic impact of the pandemic on revenues.

- Uncertainty around this central scenario continues to be extraordinarily high: in Citi’s optimistic scenario, where there is no long-term economic damage, we would expect the overall budget deficit to be eliminated for the first time since the turn of the millennium. This would be driven by the Chancellor’s relatively tight set of spending plans, combined with large tax rises and higher inflation. Even a more moderately optimistic scenario based on the Bank of England’s growth forecast could lead to borrowing in 2023–24 being as low as 1.7% of national income (or £44 billion), some 0.8% of national income (£19 billion) lower than our central scenario. Under these more optimistic scenarios, some of the planned tax rises would be less likely to go ahead, and spending plans would be more likely to be topped up.

- In a pessimistic scenario where a vaccine-resistant COVID variant forces further lockdowns, borrowing is forecast to still be 5.1% of national income by 2024–25, more than twice the level forecast pre-pandemic. It would only take growth from now until 2025–26 to average around 3.2% a year, rather than the 3.7% a year in our central forecast, for there to be a £10 billion deficit on the current budget at the end of that period. Further tax rises and/or continued squeeze on some public spending would be likely to follow at some point if scenarios such as these came to pass.

- Under Citi’s central scenario, the tax rises set out by the Chancellor would, if implemented in full, be enough to prevent debt from rising further beyond 2023–24 – but it would only start to fall very slowly and, at 89% of national income, would be 17% of national income higher in 2025–26 than it was pre-pandemic. This additional debt has been effectively financed by increased deposits from commercial banks held by the Bank of England. This depresses debt interest spending, but also increases the exposure of debt interest spending to rises in interest rates.

- Interest rates on government bonds have risen this year, with yields on 30-year bonds averaging 1.13% in September 2021 having averaged just 0.86% in January 2021. Alongside this, RPI inflation – which feeds directly into interest payments on index-linked debt – has risen from just 1.4% in the year to January 2021 to 4.8% in the year to August 2021. This has pushed up debt interest spending such that we expect it will be around £15 billion a year higher than forecast in March.

- Long-term challenges that were known prior to the pandemic are putting additional pressure on the public finances and will continue to grow over the longer term. Were increasing costs for healthcare, adult social care and state pensions accommodated through higher borrowing, debt would be on an increasing, and indeed accelerating, path. The estimated direct fiscal impact of transitioning to a net-zero economy by 2050 makes this increase even steeper in the late 2020s, 2030s and 2040s, but that impact is expected to decrease over time. It seems unlikely that those pressures will be met by another dose of austerity for other public services. Given this, and the risks from much elevated debt, there will therefore be a strong case for further sizeable – and permanent – tax rises to be implemented in the second half of this decade.

- These long-term pressures, rather than the immediate consequences of the pandemic, are the drivers behind the tax rises announced by the Prime Minister last month. If the new health and social care levy is to rise to meet future health and social care pressures then we estimate that its rate will need to more than double from 1.25% to 3.15% by the end of this decade.

Authors

Carl Emmerson

Carl, a Deputy Director, is an editor of the IFS Green Budget, is expert on the UK pension system and sits on the Social Security Advisory Committee.

Isabel Stockton

Isabel works in the Healthcare sector, and on the public finances. Their research focuses on retaining and developing the NHS workforce.

More from IFS

Understand this issue

Policy analysis

Academic research